North America Building Automation Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

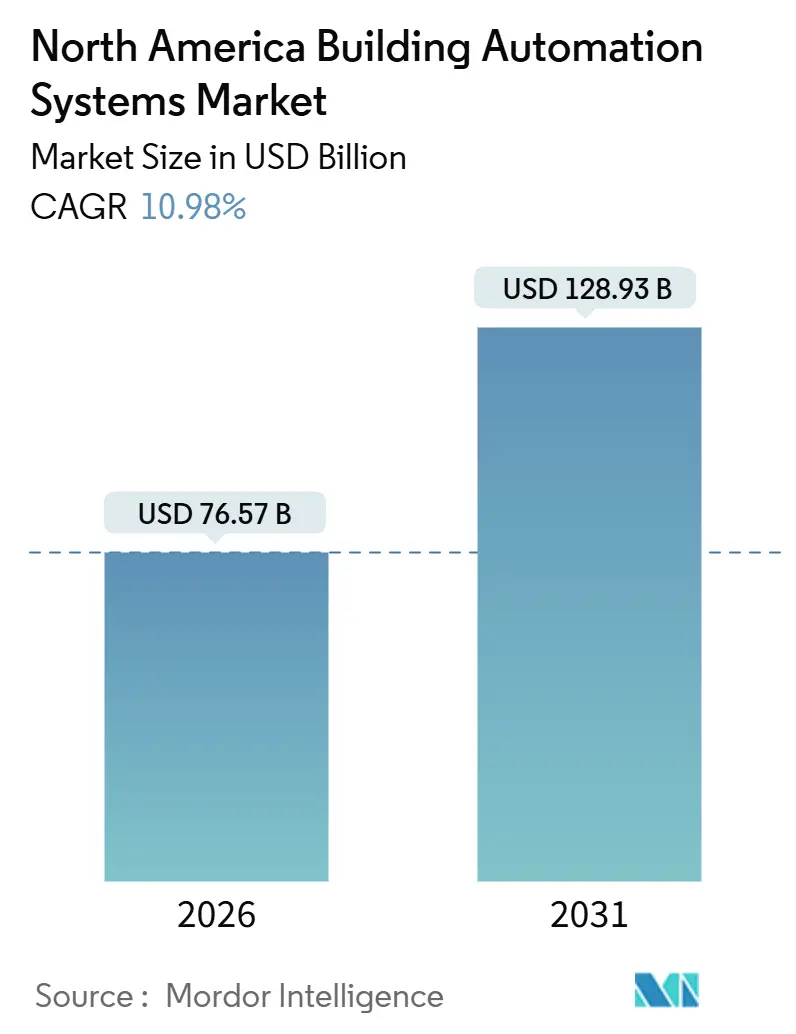

| Market Size (2026) | USD 76.57 Billion |

| Market Size (2031) | USD 128.93 Billion |

| Growth Rate (2026 - 2031) | 10.98% CAGR |

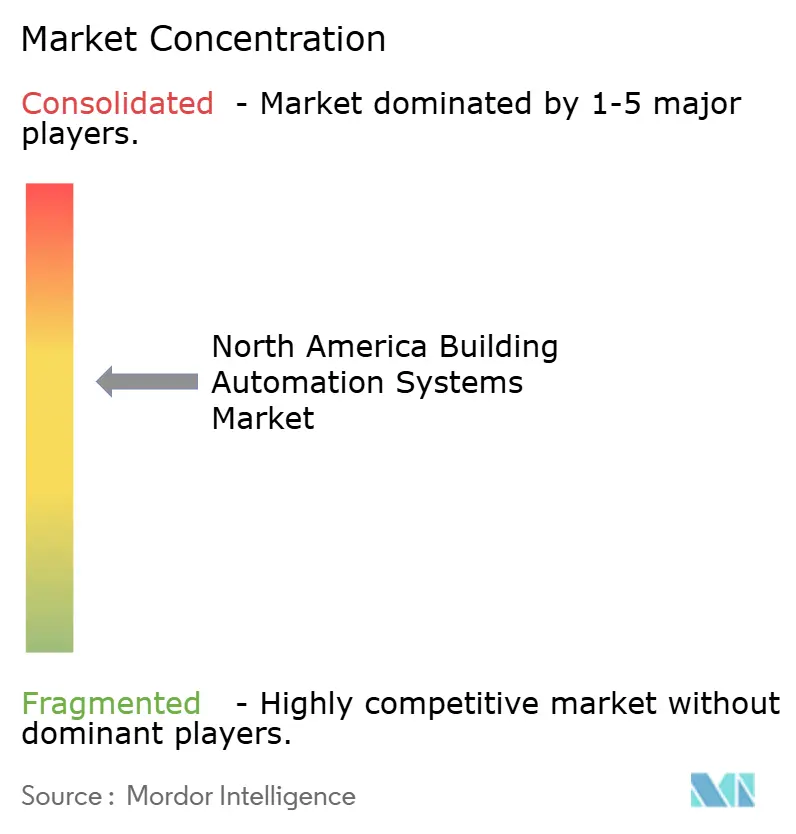

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Building Automation Systems Market Analysis by Mordor Intelligence

The North America building automation systems market size reached USD 76.57 billion in 2026 and is forecast to climb to USD 128.93 billion by 2031, reflecting a 10.98% CAGR. Strong federal decarbonization incentives, rapid tenant demand for verifiable carbon cuts, and the pivot to cloud-native analytics are reshaping procurement criteria and compressing project timelines. Hardware still contributes the largest single revenue block, yet software and wireless networking are capturing incremental growth as owners favor scalable, subscription-based models. Regulatory pressure in the United States and carbon-pricing schemes in Canada continue to convert voluntary upgrades into compliance obligations, while nearshoring in Mexico unlocks a surge of greenfield industrial projects. At the same time, cybersecurity directives and semiconductor volatility are lengthening lead times and lifting component costs, reinforcing the strategic value of integrated platforms that can de-risk deployment.

Key Report Takeaways

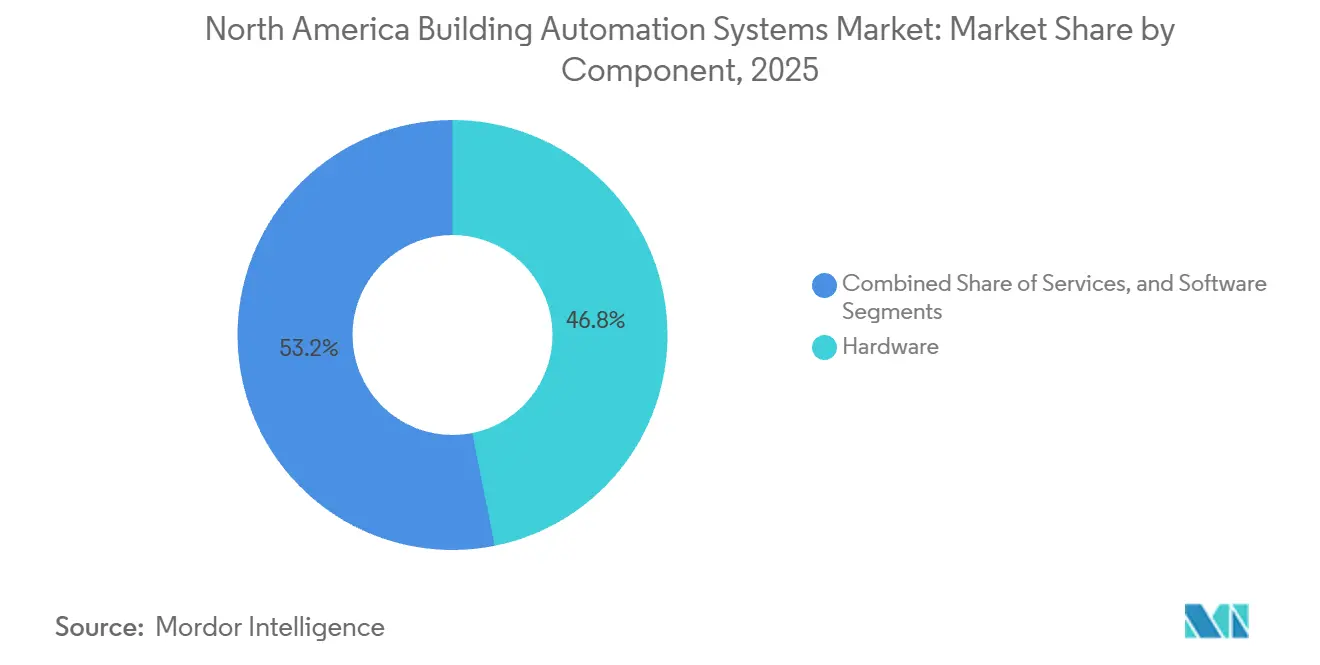

- By component, hardware led with 46.84% revenue share in 2025, while software is expanding at an 11.55% CAGR through 2031.

- By system type, heating, ventilation, and air conditioning control held 39.42% of the North America building automation systems market share in 2025, whereas energy management and analytics platforms are advancing at an 11.74% CAGR to 2031.

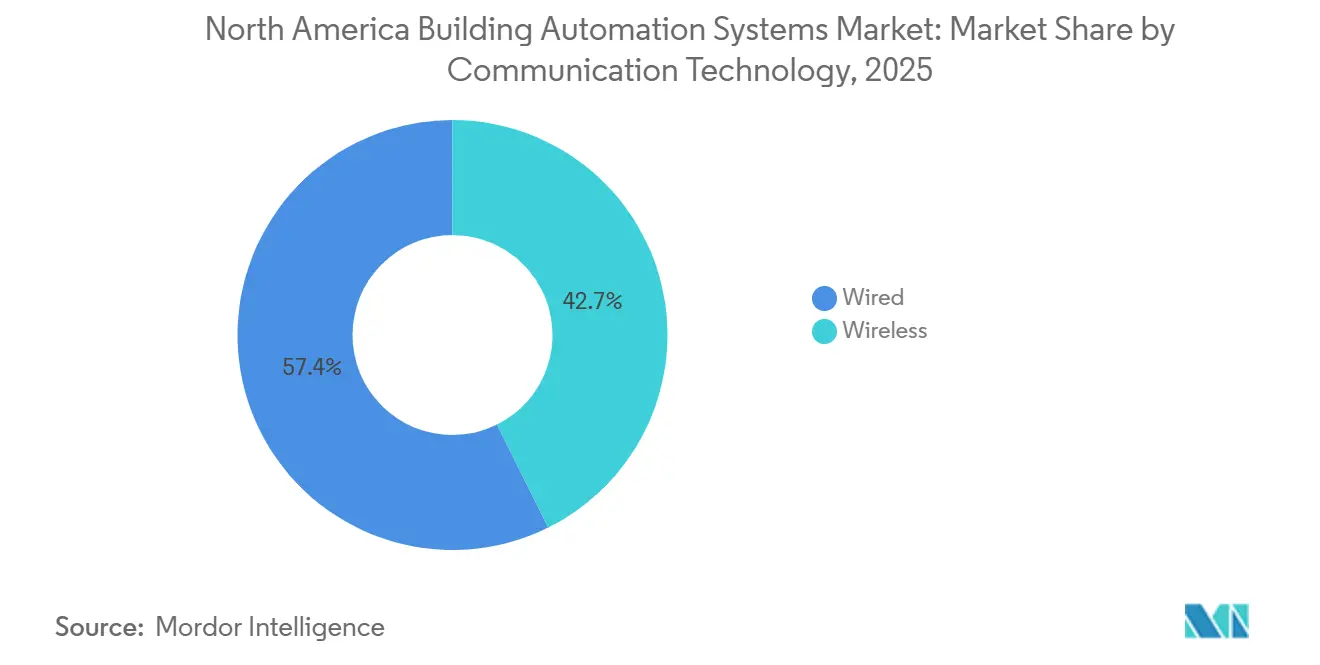

- By communication technology, wired infrastructure commanded 57.35% of the North America building automation systems market size in 2025, yet wireless protocols are projected to grow at an 11.46% CAGR.

- By end-user, commercial buildings accounted for 48.93% of spending in 2025, but industrial facilities are adopting automation at a 12.12% CAGR through 2031.

- By country, the United States captured 78.23% revenue share in 2025, while Mexico records the fastest growth at a 12.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Building Automation Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of AI Enabled Predictive Maintenance and Analytics | +2.1% | United States and Canada, early adoption in Mexico industrial corridors | Medium term (2-4 years) |

| Federal and State Incentives Accelerating Building Decarbonization | +1.9% | United States (California, New York, Washington), Canada federal programs | Short term (≤ 2 years) |

| Rapid Growth of Connected HVAC Retrofit Projects | +1.6% | North America, concentrated in commercial real estate hubs | Medium term (2-4 years) |

| Corporate ESG Commitments Driving Smart Building Investments | +1.4% | United States and Canada corporate portfolios, spillover to Mexico subsidiaries | Long term (≥ 4 years) |

| Move Toward Open Interoperable BACnet/IP and MQTT Protocols | +0.9% | North America, global standards adoption | Medium term (2-4 years) |

| Emerging Demand for Indoor Air Quality Monitoring Post-Pandemic | +0.8% | United States and Canada commercial and institutional sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adoption Of AI Enabled Predictive Maintenance And Analytics

Machine-learning models convert raw sensor feeds into early-warning diagnostics that predict equipment degradation three days ahead with 85% accuracy, cutting emergency repairs by 40% and lengthening asset life by 15%.[1]Honeywell, “Honeywell Forge for Buildings,” HONEYWELL.COM Subscription-based analytics platforms allow vendors to guarantee uptime, shifting revenue from one-time parts sales to performance contracts. A 2025 deployment across 1,200 buildings demonstrated that aggregated cloud data helps operators benchmark anomalies portfolio-wide, a task single-site analysis cannot match. Edge controllers embedding inference engines now execute algorithms locally, trimming latency to 50 milliseconds and reducing cloud bandwidth needs.

Federal And State Incentives Accelerating Building Decarbonization

The Inflation Reduction Act increased the Section 179D deduction to USD 5.00 per square foot for projects hitting 50% energy savings, halving simple payback from eight to four years.[2]Internal Revenue Service, “Energy Efficient Commercial Buildings Deduction,” IRS.GOV New York City’s Local Law 97 fines USD 268 per tonne of CO₂-equivalent emissions above caps, converting automation into a compliance tool rather than a discretionary upgrade. California’s 2025 Title 24 update mandates fault detection on large HVAC systems, effectively making automation standard in 90% of new commercial installs. Combined carrots and sticks have compressed procurement cycles from 18 months to nine as owners race to secure incentives before the 2032 phase-down.[3]U.S. Department of Energy, “Building Technologies Office,” ENERGY.GOV

Rapid Growth Of Connected HVAC Retrofit Projects

HVAC consumes 40% of commercial building electricity. Variable-frequency drives and smart thermostats synchronize output with occupancy and weather, eliminating 20%-30% waste. A 2025 portfolio retrofit cut peak demand charges by 22%, saving USD 180,000 annually across 500,000 square feet. Wireless overlay kits shorten installation from six weeks to ten days and slash labor costs by 35%. Utilities now pay USD 50 per kilowatt-year for demand response, transforming connected HVAC into a revenue generator.

Corporate ESG Commitments Driving Smart Building Investments

Institutional investors stewarding USD 130 trillion require portfolio companies to disclose Scope 1 and Scope 2 emissions. Buildings often represent half that footprint, making automation core to cost-of-capital discussions. Microsoft trimmed energy intensity 28% across 17 million square feet in 2025 after adding sub-metering and analytics. Green leases now oblige landlords to provide real-time dashboards, shifting ESG compliance risk to property managers. Class A adoption reached 75% in 2025, while Class B trailed at 40%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Retrofit Costs for Legacy Buildings | -1.2% | United States and Canada, concentrated in secondary markets with older building stock | Medium term (2-4 years) |

| Skilled Labor Shortage for BAS Integration and Cybersecurity | -0.9% | North America, acute in rural and secondary markets | Long term (≥ 4 years) |

| Rising Cyber-Security Compliance Costs | -0.7% | United States and Canada, regulatory pressure from CISA and NERC | Short term (≤ 2 years) |

| Semiconductor Supply Chain Volatility Impacting Controller Availability | -0.6% | North America, global supply dependencies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Retrofit Costs For Legacy Buildings

Comprehensive retrofits cost USD 2.50-USD 6.00 per square foot, pushing a 100,000 square-foot project to USD 250,000-USD 600,000. Smaller landlords face 7-10 year paybacks without rebates, exceeding the five-year hurdle typical of discretionary spending. Wireless kits trim labor by up to 40% but hardware still strains cash flow. On-bill, zero-interest utility financing reached 92% participation in a Seattle pilot, yet scaling needs regulatory approval that can take two years.

Skilled Labor Shortage For BAS Integration And Cybersecurity

Forty percent of automation technicians can retire by 2030, while training programs supply only two-thirds of replacements. Integration now demands IP networking and zero-trust security skills that traditional HVAC trades lack. Project schedules stretched 25% in 2025 and pushed revenue recognition into later quarters. Certified cybersecurity professionals bill USD 150-USD 250 per hour, raising commissioning costs. Vendors answer with remote diagnostics and augmented-reality tools that lift junior-tech productivity by 30%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component - Software Ascends As Analytics Monetize Data

Software grew 11.55% annually through 2031, outpacing hardware’s 46.84% of North America building automation systems market share in 2025 as cloud platforms convert device data into recurring fees. The building automation systems market size for software reached USD 1.2 billion at Johnson Controls alone in 2025, up 34% year over year. Owners favor opex contracts that avoid capital depreciation while scaling across portfolios. Hardware margins are tightening as commoditization pushes controller prices down by 8%-12% annually, prompting manufacturers to bundle devices with analytics subscriptions.

Edge computing blurs category lines. New controllers perform machine-learning inference locally, cutting latency from 500 milliseconds to 50 milliseconds and reducing outbound traffic. Service revenue pivots from break-fix calls to performance guarantees, commanding a 25% premium when vendors share savings. These shifts indicate that competitive advantage is migrating away from proprietary devices toward data ecosystems that improve algorithm accuracy with every additional building.

By System Type - Energy Management Platforms Outpace Legacy Controls

Energy management and analytics platforms are expanding at 11.74% a year, the fastest pace among system types. They forecast load a day ahead with 92% accuracy, enabling pre-cooling that avoids peak tariffs and trims utility bills by up to 25%. HVAC control retained 39.42% of the 2025 revenue share in the North America building automation systems market, yet its growth moderates as saturation rises in Class A offices. Lighting systems benefit from wireless commissioning tools that reduce installation time by 40% and lift retrofit viability.

Unified dashboards now link access control with HVAC zoning, eliminating energy waste from unoccupied areas. Fire and life-safety upgrades follow code mandates; the 2025 edition of NFPA 72 broadened networked detector requirements, growing the addressable retrofit pool by 18%. As utilities reward flexibility, PJM paid USD 85 per kilowatt-hour for demand response in 2025. Energy platforms unlock a new revenue stream, boosting returns by 300 basis points.

By Communication Technology - Wireless Gains As Retrofit Economics Improve

Wireless networks are rising at an 11.46% CAGR, narrowing the gap with wired systems that held 57.35% of revenue in 2025. Labor savings are decisive; avoiding conduit and cable pulls cuts total retrofit costs by up to 40%. Reliability fears recede as Zigbee and Bluetooth mesh deliver 99.9% uptime. Wired solutions still dominate new builds where deterministic latency below 10 milliseconds remains critical.

Hybrid architectures bridge both worlds. BACnet/IP over Wi-Fi 6 lets wireless sensors integrate with legacy trunks, enabling phased upgrades that protect sunk investments. Enhanced AES-256 encryption and certificate-based authentication meet federal cybersecurity guidance. Battery life is extending toward 10 years via energy harvesting, easing maintenance burdens.

By End-User - Industrial Facilities Accelerate Automation To Curb Energy Costs

Industrial users are the fastest adopters, growing 12.12% annually as plants consume three to five times more energy than offices. Predictive maintenance that detects motor bearing failure 48 hours in advance prevents downtime that can cost up to USD 250,000 an hour. Commercial properties still account for 48.93% of the North America building automation systems market share in 2025, supported by tenant experience features that boost lease renewal rates.

Residential penetration remains below 15% due to per-unit costs and privacy concerns, though smart thermostats saved households USD 180 in 2025. Institutional buildings must cut federal energy 30% by 2030, driving upgrades across 450 million square feet. K-12 districts redirect USD 120 per student in annual savings into instruction after automating HVAC.

Geography Analysis

The United States dominates the building automation systems market with 78.23% of regional revenue in 2025, powered by a blend of federal tax credits and state mandates that reduce payback periods from eight to four years. Title 24 in California and Local Law 97 in New York City both require real-time diagnostics, turning automation into table stakes for compliance. Coastal markets account for 45% of national spending despite only 28% of floor area, underscoring how regulations direct capital.

Canada maintains mid-single-digit growth as a rising carbon price, set to reach CAD 170 per tonne (USD 125) by 2030, pushes owners to retrofit ahead of future tax liabilities. Provinces such as Ontario and British Columbia require 15% energy-intensity cuts for buildings above 50,000 square feet, effectively mandating automation for 70% of commercial stock in Toronto and Vancouver. Workforce shortages, especially in Alberta, extend project timelines by up to 30%.

Mexico accelerates fastest at a 12.24% CAGR, buoyed by nearshoring that drew USD 1.3 billion in new automotive investment in 2025. Incentives that refund 30% of automation capital costs and the chance to design smart factories from the ground up lower total installed cost by 40% versus retrofits. Grid reliability remains a hurdle outside top metros, adding 10%-15% to project budgets for backup power, yet greenfield economics keep demand robust.

Competitive Landscape

The top five suppliers control roughly 45% of revenue, while installation and service remain fragmented among local integrators. Platform leaders such as Johnson Controls, Honeywell, and Siemens are buying software specialists to fold predictive analytics into legacy hardware, lifting subscription revenue. Schneider Electric leverages its electrical distribution footprint to win industrial projects that prefer single-vendor accountability. Open-protocol proponents like Distech Controls and Delta Controls chipped away at incumbent share in 2025 by offering BACnet/IP products priced 25% below proprietary systems.

Cybersecurity has emerged as a differentiator. Vendors capable of segmenting operational technology from IT networks under zero-trust rules win specifications in finance and healthcare. Carrier Global embeds AI in rooftop units to cut install costs by 30% and target 12 million aging units due for replacement by 2030.

Patent filings in edge computing and wireless mesh rose 40% in 2024, signaling industry focus on retrofit-friendly innovation. Ultimately, firms that build data network effects, where each additional building improves algorithmic accuracy, will capture outsized margins and resist commoditization.

North America Building Automation Systems Industry Leaders

Honeywell International Inc.

Johnson Control International PLC

Siemens AG

Schneider Electric SE

Greenwave Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Johnson Controls extended its OpenBlue platform with generative AI that automates fault resolution and cuts mean time to repair by 35% across 1,500 properties.

- December 2025: Honeywell launched Forge Energy Optimization, enrolling 400 facilities in demand-response and generating USD 12 million in annual utility payments.

- November 2025: Siemens acquired Brightly Software for USD 1.5 billion, adding computerized maintenance management to its Desigo CC suite.

- October 2025: Schneider Electric integrated Azure Digital Twins with EcoStruxure Building, achieving 18% HVAC energy savings in pilot sites.

North America Building Automation Systems Market Report Scope

Building automation systems exhibit functions such as control of the building's environment, operating systems depending on energy demand, and monitoring system performance, based on which the systems produce sound alerts as required. Moreover, it centrally controls the building's heating, ventilation, and air conditioning (HVAC), electrical, lighting, shading, access control, security systems, and other interrelated systems.

The North America Building Automation Systems Market Report is Segmented by Component (Hardware, Software, and Services), System Type (HVAC Control Systems, Lighting Control Systems, Security and Access Control Systems, Energy Management and Analytics Platforms, and Fire and Life Safety Systems), Communication Technology (Wired, and Wireless), End-User (Residential, Commercial, Industrial, and Institutional/Government), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| HVAC Control Systems |

| Lighting Control Systems |

| Security and Access Control Systems |

| Energy Management and Analytics Platforms |

| Fire and Life Safety Systems |

| Wired |

| Wireless |

| Residential |

| Commercial |

| Industrial |

| Institutional / Government |

| United States |

| Canada |

| Mexico |

| By Component | Hardware |

| Software | |

| Services | |

| By System Type | HVAC Control Systems |

| Lighting Control Systems | |

| Security and Access Control Systems | |

| Energy Management and Analytics Platforms | |

| Fire and Life Safety Systems | |

| By Communication Technology | Wired |

| Wireless | |

| By End-User | Residential |

| Commercial | |

| Industrial | |

| Institutional / Government | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large will North America’s building automation systems market be by 2031?

It is projected to reach USD 128.93 billion by 2031, up from USD 76.57 billion in 2026.

Which segment is growing fastest within the market?

Energy management and analytics platforms are advancing at an 11.74% CAGR through 2031.

Why are industrial facilities accelerating adoption?

Plants consume three to five times more energy than offices, so predictive maintenance and load optimization deliver rapid cost savings.

What role do federal incentives play?

The Section 179D tax deduction of up to USD 5.00 per square foot and state carbon penalties cut paybacks in half, making automation a compliance priority.

How is wireless technology affecting retrofit economics?

Eliminating conduit and cabling reduces installation labor up to 60%, lowering total retrofit costs by as much as 40%.

What is the main hurdle for smaller landlords?

Upfront retrofit costs of USD 2.50-USD 6.00 per square foot extend paybacks beyond the five-year threshold many owners require.

Page last updated on: