Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

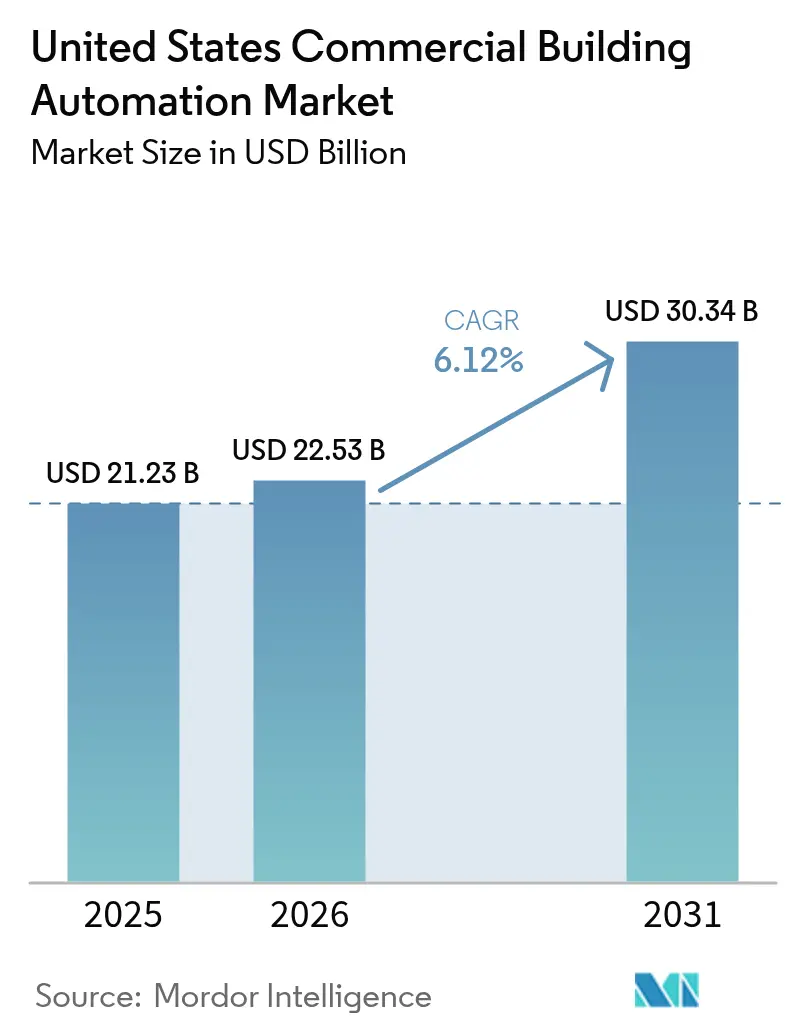

| Base Year Market Size (2025) | USD 21.23 Billion |

| Market Size (2026) | USD 22.53 Billion |

| Market Size (2031) | USD 30.34 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

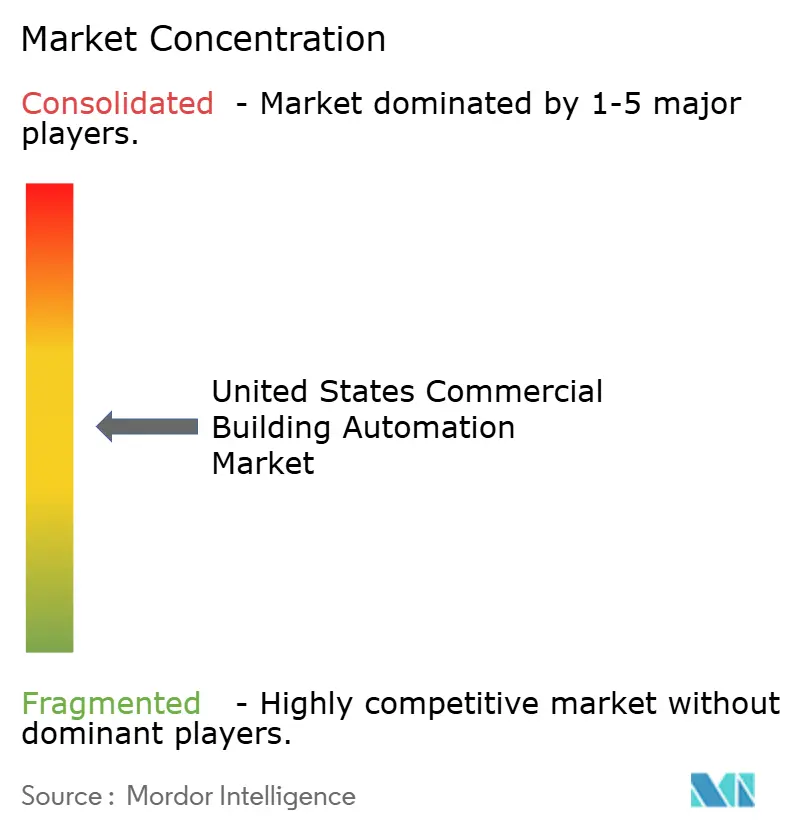

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Commercial Building Automation Market Analysis by Mordor Intelligence

The United States commercial building automation market size is expected to grow from USD 21.23 billion in 2025 to USD 22.53 billion in 2026 and is forecast to reach USD 30.34 billion by 2031 at 6.12% CAGR over 2026-2031. Federal net-zero regulations, the Inflation Reduction Act's tax deductions, and corporate ESG mandates are driving demand for connected HVAC, lighting, and power-monitoring platforms that can surface real-time data and automate energy savings. The rapid convergence of open-source IoT sensors with cloud-native analytics is lowering system costs, while utility programs now pay up to USD 200 per kilowatt for automated load shedding in regions facing grid stress. Vendors are responding by embedding AI in controllers, expanding wireless protocol support, and packaging turnkey incentive-capture services that shrink payback windows for mid-market properties. Heightened cybersecurity scrutiny, together with skilled-labor shortages, temper adoption but have also pushed software providers into managed-service models that ease owner resource constraints.

Key Report Takeaways

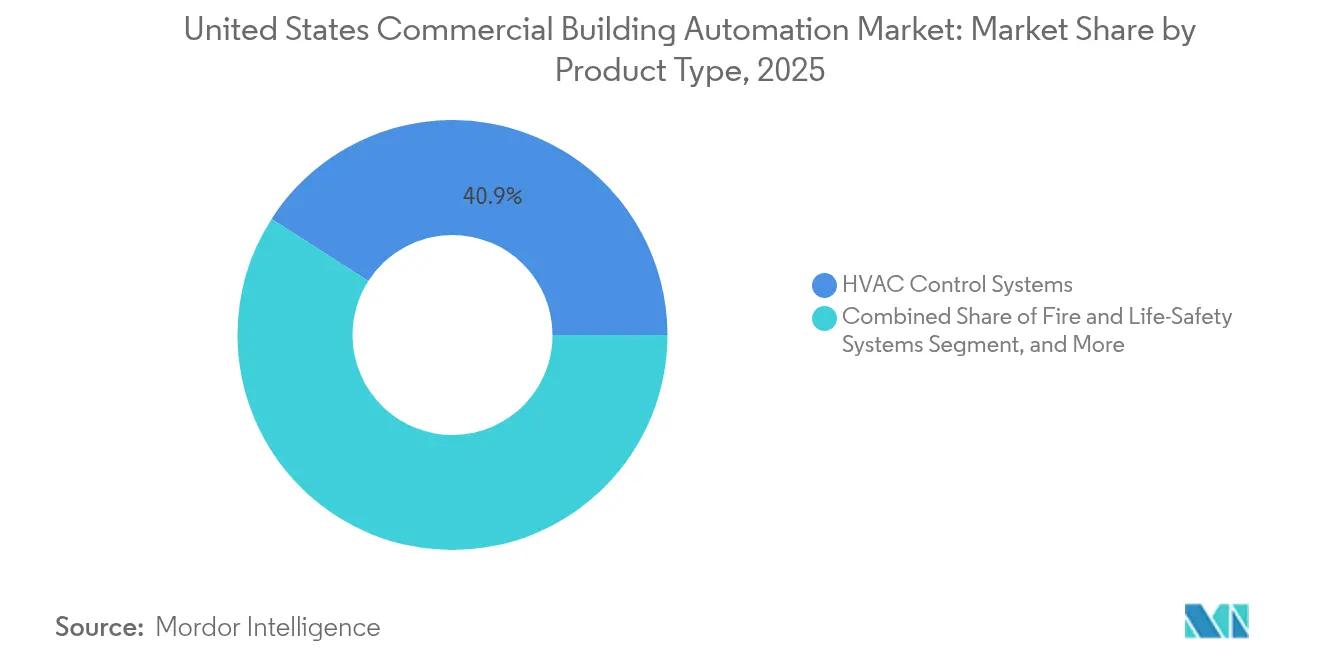

- By product category, HVAC control systems held 40.92% of the United States' commercial building automation market share in 2025, while integrated building-management platforms are projected to grow at 7.22% CAGR through 2031.

- By building type, office facilities led with 35.01% revenue in 2025 in the United States commercial building automation market; mixed-use developments are projected to expand at 7.01% CAGR to 2031.

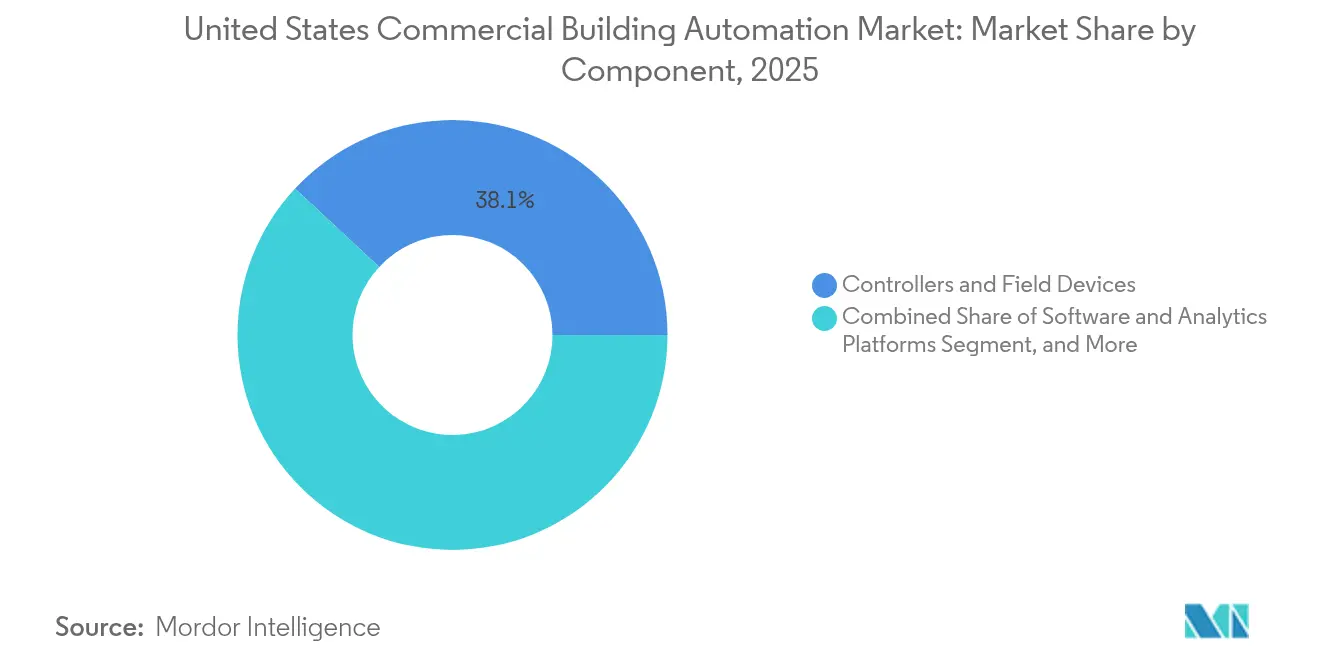

- By component, controllers and field devices accounted for a 38.08% share of the United States commercial building automation market size in 2025; however, software and analytics platforms are advancing at a 7.08% CAGR through 2031.

- By communication protocol, BACnet retained a 36.14% share in 2025 in the United States commercial building automation market, with Zigbee and other wireless options recording the fastest 7.06% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Commercial Building Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal and state net-zero / electrification mandates | +1.2% | National, with early gains in California, New York, Washington | Medium term (2-4 years) |

| Corporate ESG-driven demand for real-time energy data | +0.9% | National, concentrated in major metropolitan areas | Short term (≤ 2 years) |

| Inflation Reduction Act tax incentives for high-efficiency HVAC and controls | +0.8% | National, higher uptake in commercial-dense regions | Short term (≤ 2 years) |

| Hybrid-work shift requiring flexible space-utilization analytics | +0.7% | National, emphasis on office-heavy markets | Medium term (2-4 years) |

| Falling cost and interoperability of open-source IoT sensors / edge controllers | +0.6% | Global, accelerated adoption in retrofit markets | Long term (≥ 4 years) |

| Utility-sponsored demand-response monetisation for automated load-shedding | +0.5% | Regional, concentrated in California, Texas, Northeast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal and State Net-Zero Electrification Mandates

Federal performance standards compel buildings larger than 25,000 square feet to cut energy use 30% by 2030, pushing owners toward full-featured automation for compliance.[1]Office of Energy Efficiency & Renewable Energy, “Federal Building Performance Standard,” energy.gov California Title 24 and New York Local Law 97 add stricter carbon caps with penalties already in force, prompting rapid upgrades across government, education, and healthcare portfolios. Manual scheduling cannot reach 20–40% reduction thresholds, so connected HVAC, lighting, and plug-load controls have become default specifications in new leases. Vendors now bundle compliance dashboards that translate sensor data into audit-ready reports, shifting procurement decisions from cost-centric to mandate-driven. The ripple effect has expanded bid pipelines beyond early adopters to mainstream owners aiming to avoid fines and attract federal tenants.

Corporate ESG-Driven Demand for Real-Time Energy Data

New SEC climate disclosure rules require Fortune 500 firms to publish 15-minute Scope 2 emissions data, spurring a surge in sub-metering and cloud analytics.[2]U.S. Securities and Exchange Commission, “SEC Adopts Climate Disclosure Rules,” sec.gov Multi-tenant towers are wiring tenant-level meters so landlords can allocate costs accurately and supply ESG dashboards as a premium amenity. SaaS platforms that auto-populate disclosure templates command higher subscription fees while reducing manual reporting labor. Real-time transparency is also reshaping lease negotiations; tenants now insist on buildings capable of validating sustainability targets. In response, automation suppliers have partnered with ESG software vendors to integrate data pipelines that streamline compliance and unlock new recurring-revenue streams.

Inflation Reduction Act Tax Incentives for High-Efficiency HVAC and Controls

Section 179D now pays up to USD 5.00 per square foot for buildings achieving 50% energy savings versus ASHRAE 90.1 baselines, directly crediting automation investments.[3]Internal Revenue Service, “Inflation Reduction Act of 2022 Energy Incentives,” irs.gov Owners previously deterred by eight-year paybacks report net costs of USD 2–3 per square foot after incentives, cutting payback to three years. Because the credit rewards whole-building performance, integrated platforms coordinating HVAC, lighting, and plug loads enjoy a funding advantage over piecemeal retrofits. Vendors now market turnkey tax-capture services that pair design, commissioning, and documentation, accelerating board approvals and backlog conversion.

Hybrid-Work Shift Requiring Flexible Space-Utilization Analytics

Office utilization stabilizes at 60–70% of pre-2020 levels, prompting installation of occupancy sensors, mobile booking apps, and access-control integrations that adjust HVAC and lighting only where employees are present.[4]Johnson Controls, “Successful Building Outcomes Start with a Lifecycle Approach,” johnsoncontrols.com Predictive zoning cuts energy use by 15–25% while preserving comfort. Wireless protocols enable rapid reconfiguration as departments resize, lowering tenant churn risks. Corporations now cite automation-enabled flexibility among top three lease criteria, boosting adoption in Class A towers. The same analytic insights support space-right-sizing strategies, aligning real-estate costs with workforce patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security liabilities and insurance exclusions for connected BAS | -0.8% | National, concentrated in high-risk sectors | Short term (≤ 2 years) |

| Fragmented legacy infrastructure → high integration cost | -1.1% | National, emphasis on older building stock | Medium term (2-4 years) |

| Skilled‐labour shortages in BAS commissioning and analytics | -0.6% | National, acute in coastal metropolitan areas | Medium term (2-4 years) |

| Unclear ROI for small-/mid-size commercial properties | -0.9% | National, pronounced in secondary markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Liabilities and Insurance Exclusions for Connected BAS

40% of commercial property policies now exclude IoT-related losses, exposing owners to more than USD 1 million in potential breach costs, according to NAIC. Health-care and financial campuses, already subject to stringent data regulations, hesitate to expose operational technology to the public internet. Specialty cyber cover costs USD 0.50–1.00 per square foot annually, extending paybacks and delaying projects. Standards such as BACnet Secure Connect and NIST profiles remain in draft, leaving uncertainty over future compliance spending. Vendors answer with zero-trust architectures and managed security services, yet buyer caution persists.

Fragmented Legacy Infrastructure and High Integration Costs

Typical commercial properties house three to five discrete control systems installed over decades, and integration can consume 20–80% of a retrofit budget. Pneumatic or proprietary serial networks often require wholesale replacement, while skilled commissioning labor draws USD 80–120 per hour amid a 25% technician shortfall. Occupied-building work must be phased to avoid tenant disruption, adding 25–40% to costs. Proprietary protocols lock owners into single-vendor service contracts, inflating life-cycle expenses. The obstacle is most acute for buildings under 50,000 square feet, where limited economies of scale push payback beyond four years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: HVAC Dominance Faces Platform Integration

HVAC control systems accounted for 40.92% of 2025 revenue, driven by state performance standards that mandate the use of automated ventilation and temperature control. Yet, integrated building-management platforms are accelerating at a 7.22% CAGR, as owners pursue 30–50% whole-facility efficiency gains that are unattainable through siloed subsystems. This evolution positions platforms to capture a larger slice of the United States commercial building automation market over the forecast horizon.

Platform adoption also reflects a preference for unified ESG reporting that spans HVAC, lighting, security, and power. Vendors now offer cloud dashboards that aggregate data streams into single-pane-of-glass views, simplifying compliance and maintenance workflows. Interoperability with BACnet and wireless protocols ensures future-proofing, making integrated platforms attractive to investors valuing resilient asset performance.

By Building Type: Office Leadership Challenged by Mixed-Use Growth

Office properties retained 35.01% share of the United States commercial building automation market size in 2025, benefiting from corporate ESG disclosure obligations and hybrid-work analytics needs. Mixed-use complexes, however, are forecast to rise at 7.01% CAGR as urban planners combine retail, residential, and workspace functions that demand sophisticated zonal control.

Diverse occupancy patterns in mixed-use assets necessitate flexible automation that can adjust HVAC schedules by the hour. Landlords view such adaptability as a hedge against evolving tenant mixes, while municipalities encourage integrated developments through zoning incentives. Office owners continue to deploy advanced BAS to retain Class A designation, but competition from experience-driven mixed-use projects intensifies the technology race.

By Component: Hardware Foundation Supports Software Analytics Surge

Controllers and field devices generated 38.08% of 2025 component revenue, underscoring the essential hardware backbone of the United States commercial building automation market. Software and analytics platforms, growing 7.08% CAGR, are expected to outpace hardware as AI-enabled optimization becomes the primary value driver.

Edge-to-cloud platforms transform terabytes of sensor data into actionable insights, reducing energy consumption by 15–25% and enabling the prediction of maintenance needs weeks in advance. Service revenues from integration, commissioning, and monitoring augment vendor margins, with labor shortages allowing premium pricing. The combination of low-cost sensors and high-value analytics is shifting procurement budgets from capital expenditure toward recurring software subscriptions.

By Communication Protocol: BACnet Standard Faces Wireless Protocol Challenge

BACnet held 36.14% of the United States commercial building automation market share in 2025, thanks to two decades of open-standard support across major OEMs. Wireless protocols, led by Zigbee and EnOcean, are growing at a 7.06% CAGR as energy-harvesting devices remove wiring constraints, thereby slashing installation labor.

Owners prefer open protocols to avoid vendor lock-in and enable competitive bidding. BACnet Secure Connect adds encrypted IP transport, improving cyber resilience. Gateways now translate Zigbee, EnOcean, and LoRaWAN traffic into BACnet objects, allowing mixed-vendor deployments that balance cost, range, and power needs. Wireless adoption is strongest in retrofits where running conduit is impractical or disruptive.

Geography Analysis

The Southern states command the largest share of the United States' commercial building automation market, driven by robust construction in Texas, Florida, and Georgia, as well as lucrative utility demand-response programs that monetize automated load shedding. Western and Northeastern markets closely trail, driven by stringent energy codes such as Title 24 and Local Law 97, which penalize inefficiency. The Midwest exhibits slower uptake due to milder regulatory pressure and lower electricity prices; however, it gains momentum from manufacturing facilities that require precise environmental control.

California’s solar-heavy grid incentivizes automation that can absorb renewable volatility, while New York’s carbon caps elevate compliance urgency. The Northeast endures the nation’s highest energy costs, which magnify the savings from peak-demand controls. Federal standards unify baseline requirements, but state rebates and penalties dictate the variability of payback.

Labor market imbalances influence regional implementation timelines. Coastal hubs face premium technician rates and longer scheduling queues, whereas interior states leverage lower labor costs but contend with fewer certified professionals. Data-center expansion in Virginia, North Carolina, and Texas drives demand for advanced cooling and power automation, ensuring uptime and ESG alignment.

Competitive Landscape

The commercial building automation market is moderately concentrated. Johnson Controls, Honeywell, and Schneider Electric leverage their installed bases, end-to-end portfolios, and partner ecosystems to maintain market share against software-centric entrants. These incumbents now embed AI engines, roll out subscription models, and pursue vertical acquisitions such as Johnson Controls’ 2025 purchase of Webeasy, which expands SME reach.

New entrants bypass hardware dominance by offering cloud analytics compatible with existing BACnet infrastructures. Start-ups emphasize rapid ROI through incentive capture and autonomous optimization, challenging incumbents on agility rather than breadth. Partnerships between hardware giants and niche software firms are proliferating as both sides seek to leverage complementary strengths.

Competition also revolves around cybersecurity credentials; vendors now market compliance with BACnet Secure Connect and ISO 27001 to satisfy insurance underwriters. Smaller buildings remain underserved due to integration costs, representing a whitespace where plug-and-play wireless solutions could unlock scale.

United States Commercial Building Automation Industry Leaders

ABB Ltd.

Siemens AG

Schneider Electric SE

Emerson Electric Co.

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Johnson Controls acquired Webeasy, enhancing smart-building reach into European SME segment.

- January 2025: URC and Network Thermostat integrated Total Control with NetX thermostats for BACnet/IP and Modbus TCP/IP compatibility.

- January 2025: Siemens Smart Infrastructure launched Desigo PXC4 and PXC5 controllers with BACnet Secure Connect and cloud links targeting SME buildings.

- January 2025: BrainBox AI reported 15.8% HVAC energy savings and USD 42,951 annual cost reduction at Cammeby’s International after autonomous AI deployment.

United States Commercial Building Automation Market Report Scope

Building automation systems (BASs) or building automation control systems exhibit functions such as controlling the building's environment, operating systems according to energy demand, and monitoring system performance. The systems produce sound alerts as required. A BAS (Building Automation System) has related hardware and software to control and monitor electrical systems, heating, ventilation, air conditioning (HVAC), lighting control, security, and surveillance, among others, in buildings (commercial, residential, and mixed-use).

The United States Commercial Building Automation Market Report is Segmented by Product Type (HVAC Control Systems, Security and Access Control Systems, Energy Management and Power-Monitoring Systems, Lighting and Shading Control Systems, Fire and Life-Safety Systems, and Integrated Building-Management Platforms), Building Type (Office, Institutional, Retail, Hospitality, Industrial and Warehouse, and Mixed-Use and Other Commercial), Component (Controllers and Field Devices, Sensors, Software and Analytics Platforms, and Services), Communication Protocol (BACnet, Modbus, KNX, LonWorks, Zigbee and Other Wireless Protocols, EnOcean and Energy-Harvesting Protocols, and Proprietary Protocols). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| HVAC Control Systems |

| Security and Access Control Systems |

| Energy Management and Power-Monitoring Systems |

| Lighting and Shading Control Systems |

| Fire and Life-Safety Systems |

| Integrated Building-Management Platforms |

By Building Type

| Office |

| Institutional (Education and Healthcare) |

| Retail |

| Hospitality |

| Industrial and Warehouse |

| Mixed-Use and Other Commercial |

By Component

| Controllers and Field Devices |

| Sensors |

| Software and Analytics Platforms |

| Services (Consulting, Integration and Maintenance) |

By Communication Protocol / Network

| BACnet |

| Modbus |

| KNX |

| LonWorks |

| Zigbee and Other Wireless Protocols |

| EnOcean and Energy-Harvesting Protocols |

| Proprietary Protocols |

| By Product Type | HVAC Control Systems |

| Security and Access Control Systems | |

| Energy Management and Power-Monitoring Systems | |

| Lighting and Shading Control Systems | |

| Fire and Life-Safety Systems | |

| Integrated Building-Management Platforms | |

| By Building Type | Office |

| Institutional (Education and Healthcare) | |

| Retail | |

| Hospitality | |

| Industrial and Warehouse | |

| Mixed-Use and Other Commercial | |

| By Component | Controllers and Field Devices |

| Sensors | |

| Software and Analytics Platforms | |

| Services (Consulting, Integration and Maintenance) | |

| By Communication Protocol / Network | BACnet |

| Modbus | |

| KNX | |

| LonWorks | |

| Zigbee and Other Wireless Protocols | |

| EnOcean and Energy-Harvesting Protocols | |

| Proprietary Protocols |

Key Questions Answered in the Report

How large is the U.S. commercial building automation systems market in 2026?

It totals USD 22.53 billion with a 6.12% CAGR outlook to 2031.

Which product currently dominates adoption?

HVAC control systems hold 40.92% revenue due to mandatory energy-performance standards.

Which building category is growing fastest?

Mixed-use developments are projected to expand 7.01% CAGR as cities favor multi-function construction.

What role do tax incentives play in project ROI?

Section 179D deductions can cut installed costs to USD 2–3 per square foot, trimming payback to about three years.

Why are wireless protocols gaining share?

Energy-harvesting Zigbee and EnOcean devices remove wiring labor, lowering retrofit costs by up to 60%.

Page last updated on: