Postal Automation System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

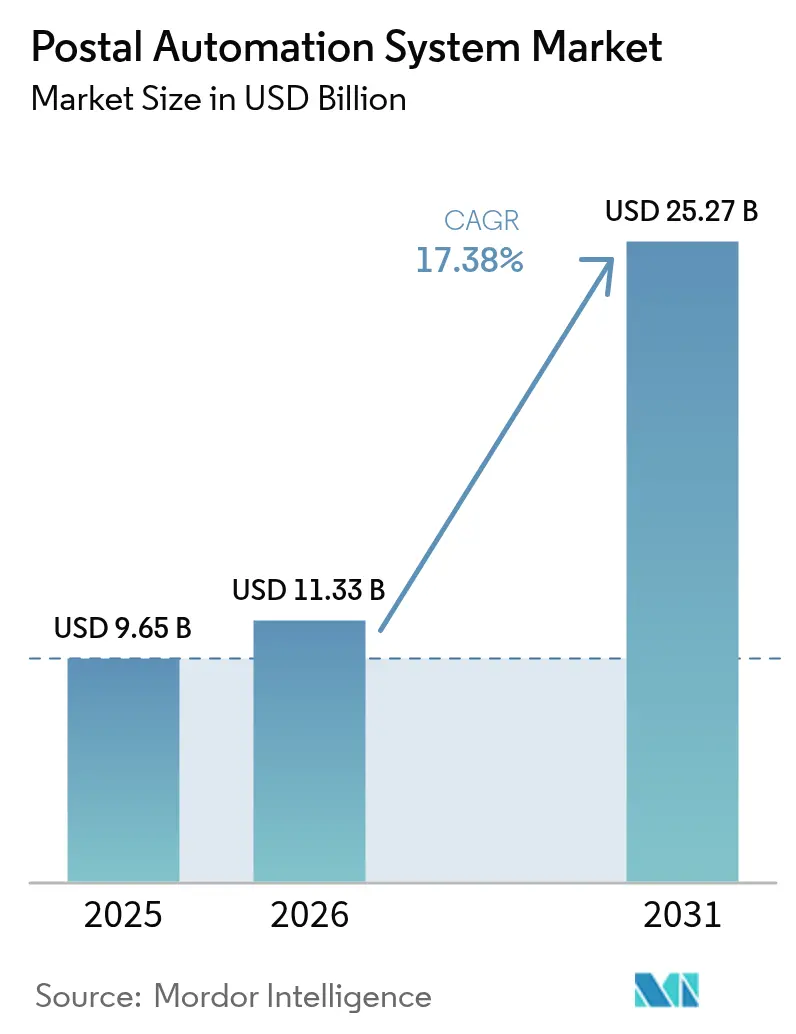

| Market Size (2026) | USD 11.33 Billion |

| Market Size (2031) | USD 25.27 Billion |

| Growth Rate (2026 - 2031) | 17.38% CAGR |

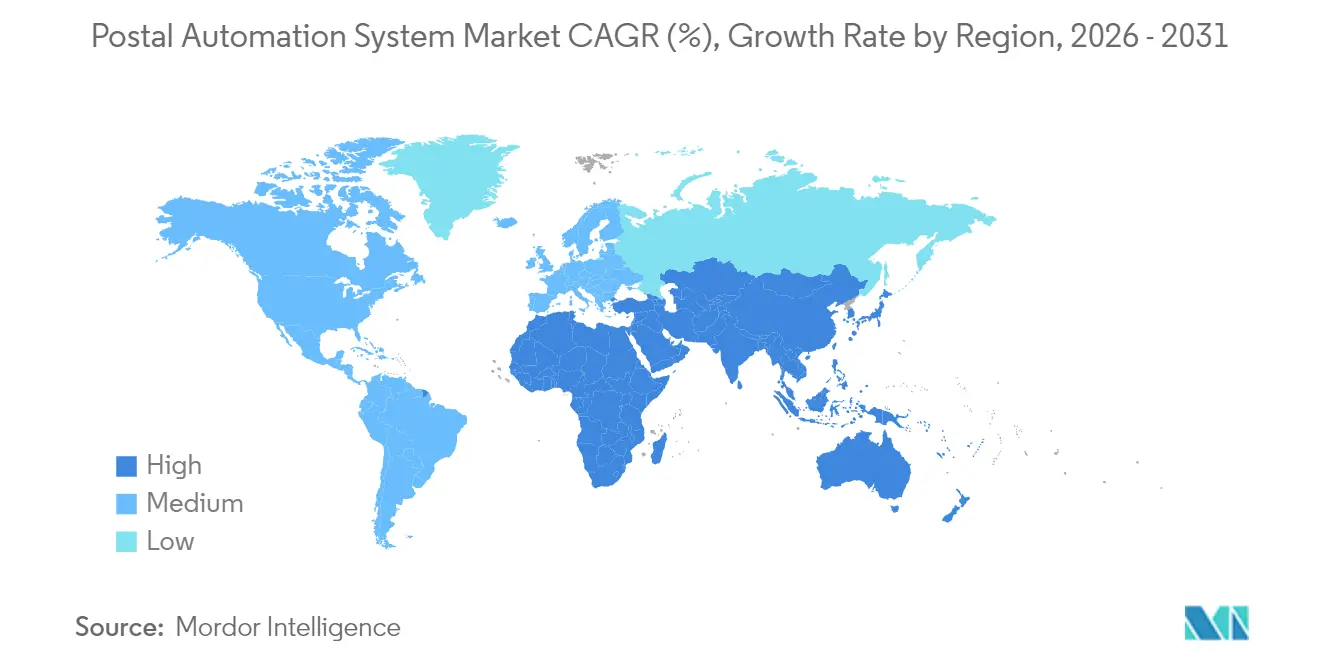

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

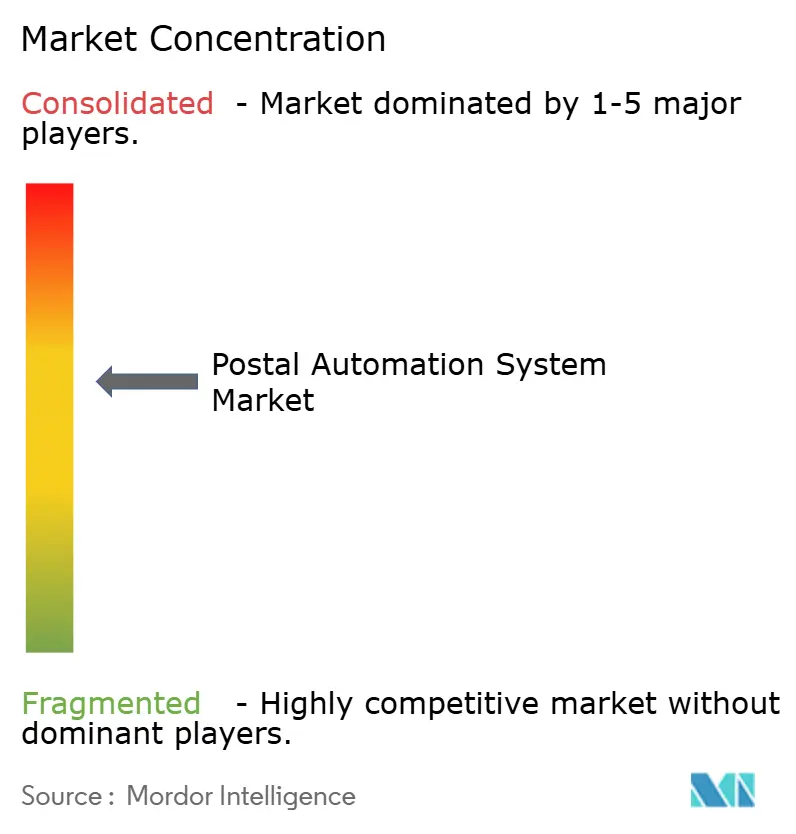

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Postal Automation System Market Analysis by Mordor Intelligence

Postal automation system systems market size in 2026 is estimated at USD 11.33 billion, growing from 2025 value of USD 9.65 billion with 2031 projections showing USD 25.27 billion, growing at 17.38% CAGR over 2026-2031. Growth reflects rising cross-border e-commerce demand, postal modernization programs and sustained labor cost pressures that make automation economically attractive. North America and Europe account for the largest installed base because of sizeable public-sector investments and energy-efficiency regulations that favor next-generation equipment. Asia-Pacific is the fastest-growing region as China Post, Cainiao and Japan Post accelerate rural and urban automation projects, shortening delivery times and lowering manual labor costs. Hardware continues to dominate purchases, yet demand is shifting toward service contracts and robotics-as-a-service models that transfer performance risk to suppliers. Competitive intensity is moderate, with Vanderlande’s purchase of Siemens Logistics and BlueCrest’s acquisition of Fluence Automation redefining scale advantages in integrated hardware-software offerings.

Key Report Takeaways

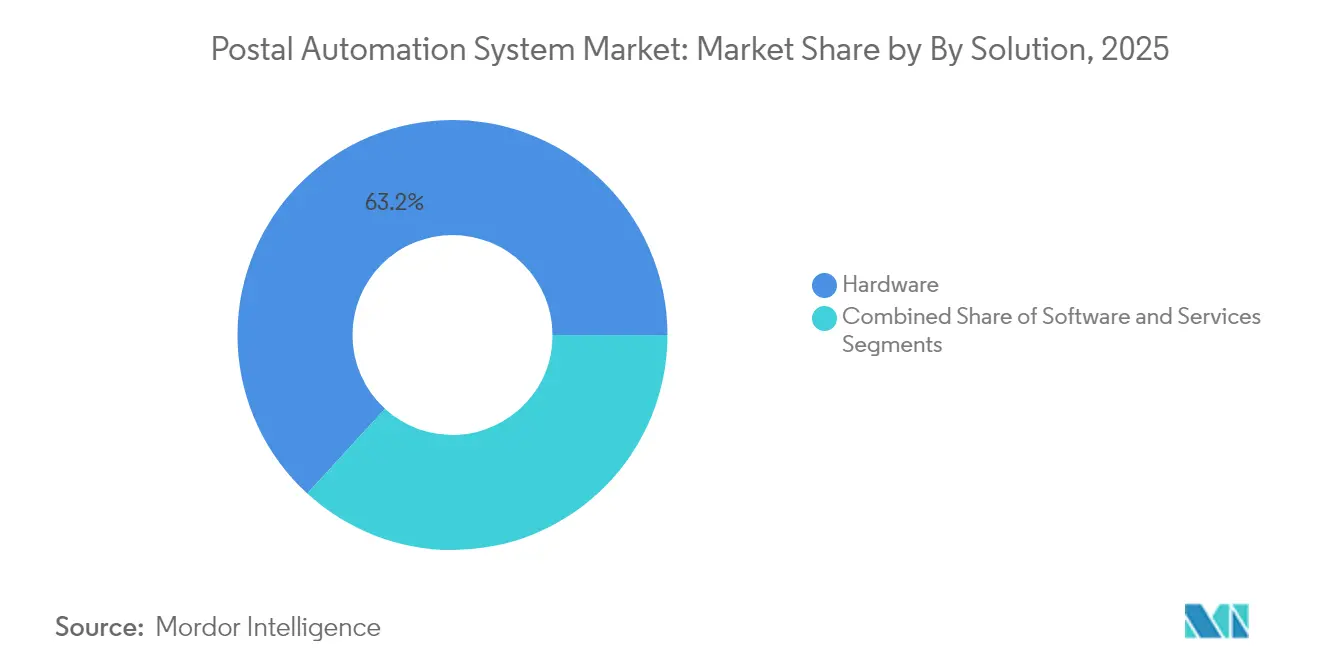

- By solution, hardware held 63.20% of the mail sorting systems market share in 2025, while the services segment is projected to expand at a 20.25% CAGR through 2031.

- By technology, parcel sorters led with 41.30% revenue share in 2025; automated guided vehicles and robotics record the highest projected CAGR at 23.2% through 2031.

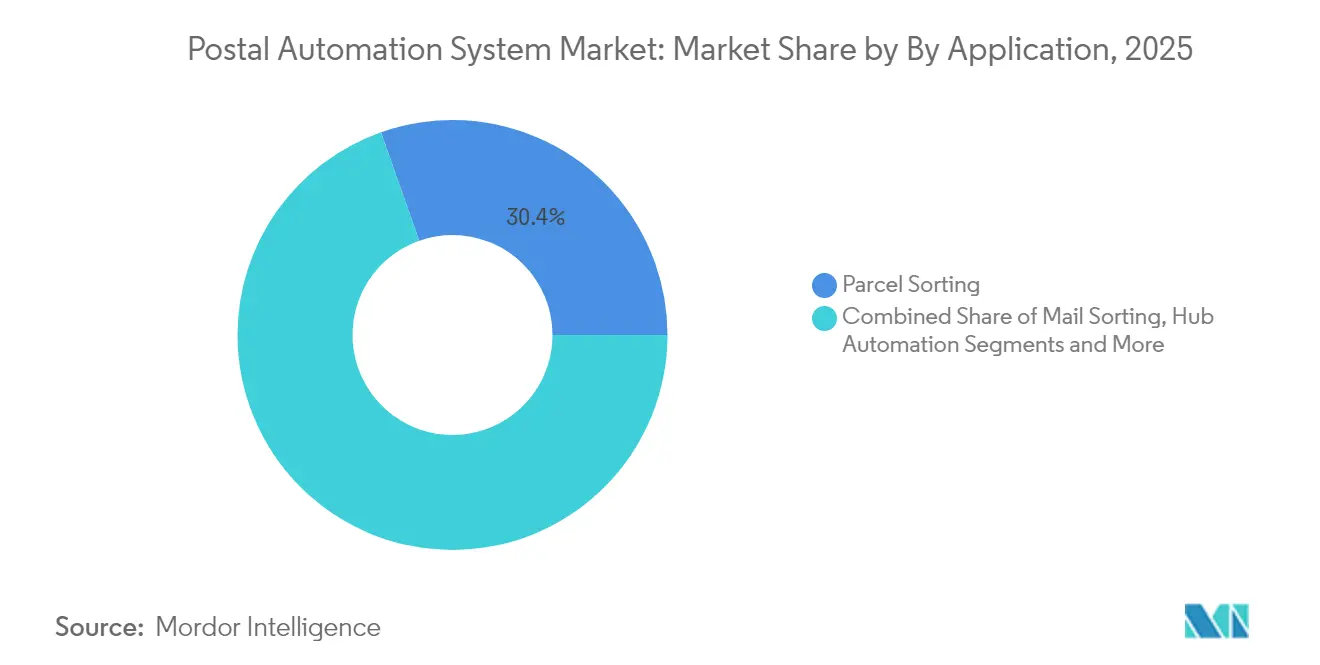

- By application, parcel sorting accounted for 30.40% of the mail sorting systems market size in 2025, while last-mile hub automation is advancing at a 25.45% CAGR to 2031.

- By end user, national postal operators captured 41.10% of the mail sorting systems market share in 2025; e-commerce fulfillment centers are expanding at a 22.6% CAGR through 2031.

- By geography, North America is the largest regional market, while Asia-Pacific posts the fastest CAGR on the back of large-scale projects in China and Japan.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Postal Automation System Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in cross-border e-commerce parcel volumes in Asia driving high-throughput parcel sorters | +3.2% | APAC core, spill-over to North America & EU | Medium term (2-4 years) |

| USPS "Delivering for America" modernization spurring automation upgrades in North America | +2.8% | North America, with technology transfer to global markets | Short term (≤ 2 years) |

| EU Green Deal demand for energy-efficient systems boosting replacement sales | +2.1% | Europe, with regulatory influence on global standards | Medium term (2-4 years) |

| Labor shortages & wage inflation accelerating robotic singulation adoption in CEP hubs | +4.3% | Global, with acute impact in developed markets | Short term (≤ 2 years) |

| Real-time track-and-trace mandates triggering RFID-enabled sorting adoption in Japan & South Korea | +1.7% | APAC core, with expansion to developed markets | Medium term (2-4 years) |

| Urban micro-fulfillment expansion increasing demand for compact modular sorters in Middle East | +1.4% | Middle East & North Africa, urban centers globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Cross-Border E-Commerce Parcel Volumes Driving High-Throughput Sorters

E-commerce parcels crossing borders continue to climb, with US parcel volumes reaching 21.7 billion in 2023 even as revenue per piece declined, underscoring the need for efficient high-throughput automation. Amazon Logistics overtook UPS on volume, proving that speed-optimized sorting networks confer a market edge. China Post and Cainiao lowered rural labor costs by deploying vision-guided systems that read waybills automatically, narrowing the urban-rural service gap. Operators now focus on processing density rather than cost per piece, since automation enables higher volumes without proportional staffing increases.[1] Pitney Bowes, “Parcel Shipping Index,” pitneybowes.com

USPS “Delivering for America” Modernization Spurring Automation Upgrades

USPS committed USD 40 billion to revamp its network, expanding daily package capacity to 60 million items and aligning mail and parcel flows for improved reliability. Zebra Technologies printers, a new remote forwarding system, and the USPS Ship migration reinforce the digital layer underpinning physical automation. Suppliers leverage USPS specifications to scale similar solutions globally, creating a technology spill-over that accelerates adoption in other regions.[2]Zebra Technologies, “USPS selects Zebra for printer refresh,” zebra.com

Labor Shortages Accelerating Robotic Singulation Adoption

Worker scarcity drove USD 55 billion in automation investment since 2021, with logistics leading the uptake. UPS will shutter 200 sort centers yet invest USD 9 billion in automation to save USD 3 billion annually by 2028. VTPost’s 160 LiBiao robots now handle 6,000 parcels hourly with negligible error, redeploying staff to higher-value tasks and reducing operating costs.

EU Green Deal Demand for Energy-Efficient Systems

Regulation 2024/1781 sets ecodesign rules for industrial products, making durability and recyclability mandatory. The Net Zero Industry Act aims for 40% manufacturing capacity in net-zero tech by 2030, encouraging public buyers to select systems with lower power use. DHL targets cutting logistics-related greenhouse gases below 29 million tons by 2030, reinforcing market demand for high-efficiency drives and low-noise solutions.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Legacy IT integration complexity within postal infrastructures in Africa & LatAm | -2.1% | Africa & Latin America, with spillover to emerging markets | Long term (≥ 4 years) |

| Capital-intensive investments with >7-year ROI deterring small CEP operators | -1.8% | Global, with acute impact on emerging market operators | Medium term (2-4 years) |

| Import tariffs on automation equipment in Brazil & India elevating TCO | -1.3% | Brazil & India, with regional trade bloc implications | Short term (≤ 2 years) |

| Declining letter-mail volumes limiting spending on letter-sorting technology in Europe | -1.5% | Europe, with secondary impact on developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy IT Integration Complexity Limiting Emerging Market Adoption

Developing posts often run on ageing platforms that cannot easily connect to modern sorters, extending project timelines and raising costs. The IMF highlights similar challenges in payment rails that mirror logistics bottlenecks, stressing a need for basic digital infrastructure before advanced automation can scale.

Capital-Intensive Investments Deterring Small CEP Operators

KION projects the mobile automation market at EUR 20 billion by 2027, a figure that underscores the hefty capital outlay required for competitiveness. Kardex posted a 24.3% revenue rise to EUR 702.9 million in 2023, yet order delays reveal customer hesitancy when payback exceeds seven years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Services Accelerate Despite Hardware Dominance

The mail sorting systems market size attributed to hardware reached USD 6.1 billion in 2025, reflecting capital-intensive conveyor, sensor and OCR investments. Services produced a smaller revenue base but are projected to grow at a 20.25% CAGR to 2031 as operators favor managed outcomes over outright equipment ownership. Software licenses bridge the two, enabling live performance dashboards, route optimization and predictive maintenance that extend asset life.

Adoption of outcome-based contracts shifts risk to vendors, with Quadient and BlueCrest guaranteeing throughput levels and uptime. These arrangements allow even mid-tier operators to access sophisticated capabilities without upfront capital, broadening the addressable base for the mail sorting systems market. Hardware spending will remain sizeable, yet revenue mix analysis shows services closing the gap by 2031 as subscription and pay-per-sort models scale.

By Technology: AGV and Robotics Disrupt Traditional Sorting

Parcel sorters commanded 41.30% of the mail sorting systems market share in 2025 on the strength of long-established cross-belt and tilt-tray designs. Growth momentum, however, lies with automated guided vehicles and collaborative robots that post a 23.2% CAGR through 2031. Robotics removes fixed-track constraints, letting operators re-configure hubs quickly to manage seasonal peaks.

La Poste’s data show mail contributing only 15.8% of revenue in 2024, down from 52% in 2010, signaling a structural shift away from letter-centric machinery toward parcel-centric robotics. Culler-facer-canceller units retain a niche in high-volume philatelic segments, but hybrid sites integrating AGVs, vision systems and coding modules deliver superior flexibility. Vendors now bundle fleet-management software with mobile robots, improving ROI for operators constrained by real estate limits in urban hubs.

By Application: Last-Mile Automation Drives Growth

Parcel sorting still generated 30.40% of revenue in 2025, yet last-mile hub automation will contribute the largest absolute growth as it scales at 25.45% CAGR. Fulfillment centers located closer to consumers opt for compact modular sorters that handle polybags, flats and small parcels in one stream, reducing the need for multiple downstream processes.

Japan Post’s digital address initiative enhances field-level accuracy, cutting mis-sorts and enabling smoother handoffs between automated central facilities and last-mile depots. Traditional mail sorting persists in government and financial services where physical delivery remains mandatory, yet operators integrate OCR and label-printing modules into single-pass processes to maximize floor space. Address printing systems now link directly with customer data to create audit trails, aligning with stricter compliance demands.

By End User: E-Commerce Fulfillment Centers Accelerate

National postal operators captured 41.10% of revenue in 2025, benefitting from universal service mandates and expansive networks that make large-scale automation cost-effective. However, e-commerce fulfillment centers are projected to expand revenue at a 22.6% CAGR through 2031 as platforms such as Amazon and Alibaba vertically integrate logistics to control customer experience.

Singapore Post provides a case study in transformation: logistics now accounts for 70% of revenue, up from 38% five years earlier, driven by 4PL platform expansion. Courier and parcel specialists occupy a middle space, pressured by postal incumbents’ scale and e-commerce players’ integrated models. Government agencies and financial institutions continue to demand bespoke solutions with advanced security features, supporting a premium niche for suppliers.

Geography Analysis

North America leads global revenue owing to the USPS “Delivering for America” program that injects USD 40 billion into facility upgrades and boosts daily capacity to 60 million packages. Canada follows a similar trajectory, adopting robotics to mitigate labor shortages in large urban hubs such as Toronto and Vancouver. Stable regulatory regimes and predictable parcel flows shorten payback periods, reinforcing vendor preference for early product rollouts in the region.

Europe contributes robust growth underpinned by the Net Zero Industry Act, which prioritizes energy-efficient equipment and accelerates replacement cycles. Germany’s updated postal law gives Deutsche Post flexibility to optimize routes, while DHL holds 63% mail and 40% parcel market shares, creating economies of scale for nationwide automation. The United Kingdom’s approval of the DHL eCommerce–Evri merger forms a combined network processing more than 1 billion parcels annually, anchoring further automation investments.

Asia-Pacific records the fastest CAGR, propelled by China Post and Cainiao’s automation deployments and Japan’s proposed 500-kilometer automated conveyor network to counter driver shortages. South Korea leverages advanced telecom infrastructure to roll out RFID-enabled sortation, while India wrestles with equipment tariffs that raise project costs. Australia’s dispersed population boosts interest in robotics that can flexibly scale capacity across long distances.

Latin America delivers uneven performance. Mexico benefits from USMCA proximity, attracting cross-border parcel flows that justify automation in northern hubs. Brazil’s compliance program supports e-commerce growth, yet tariffs on imported automation remain a drag on total cost of ownership. Argentina’s economic volatility prolongs investment decision cycles, limiting market penetration for high-end solutions.

The Middle East and Africa remain nascent but promising. Gulf states invest in urban micro-fulfillment facilities that demand compact modular systems, while Africa faces legacy IT hurdles that slow deployments. International aid programs targeting postal infrastructure modernization could unlock future demand, especially as smartphone-led commerce expands across major urban corridors.

Competitive Landscape

Competition in the mail sorting systems market remains moderate. Vanderlande’s USD 325 million acquisition of Siemens Logistics strengthens its postal and baggage-handling portfolio, creating synergies in conveyor technology and control software. Traditional OEMs such as Toshiba Infrastructure Systems, NEC and Pitney Bowes still command significant installed bases but face pressure from robotics specialists and software-first entrants.

Strategic shifts favor vertical integration and service-led revenue. BlueCrest’s 2025 purchase of Fluence Automation expands its ability to provide turnkey solutions from hardware through lifecycle optimization. Dematic and Beumer Group launch energy-efficient drive systems and cloud analytics platforms to comply with EU ecodesign rules and to differentiate on sustainability.

Emerging disruptors focus on robotics. LiBiao’s autonomous mobile sorters replace fixed cross-belt lines, offering scalability for operators facing real estate constraints. KION opened an Antwerp center of excellence to co-develop customer-specific robotic modules that integrate seamlessly with SAP and other WMS platforms. Software innovation—AI-enabled vision, predictive maintenance and digital twins—has become as critical as mechanical throughput, narrowing differentiation windows for legacy hardware players.

Postal Automation System Industry Leaders

Siemens Logistics GmbH

Toshiba Infrastructure Systems & Solutions Corp.

NEC Corporation

Vanderlande Industries B.V.

Pitney Bowes Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DHL eCommerce UK announced merger with Evri to create the UK's premier parcel delivery business, combining operations to deliver over 1 billion parcels annually through 15,000 access points and establishing entry into the UK business letter market.

- May 2025: Japan Post launched its digital address system to improve mail sorting and delivery efficiency through enhanced addressing accuracy and digital technology integration.

- April 2025: DHL Group reported Q1 2025 revenue of EUR 20.8 billion (2.8% increase) and EBIT of EUR 1.37 billion (4.5% increase), while launching EUR 2 billion investment in DHL Health Logistics brand to enhance life sciences capabilities

Global Postal Automation System Market Report Scope

With the advent of technological advancements across various end-user industries, the postal and parcel industry is also evolving rapidly. Globalization has boosted the world economy by the massive international flow of data, and new innovations in technology and data are reinventing the mail and parcel industry. For instance, when mail or parcels are scanned upon entering a facility, internet-based technology provides customers with real-time tracking information. Hence, automation in the postal and parcel industry is evolving rapidly owing to the various growth drivers.

| Hardware |

| Software |

| Services |

| Culler-Facer-Canceller (CFC) Systems |

| Letter Sorters |

| Flat Mail Sorters |

| Parcel Sorters |

| Mixed-Mail Sorters |

| Coding and Printing/OCR Systems |

| Automated Guided Vehicles and Robotics |

| Others |

| Parcel Sorting |

| Mail Sorting |

| Address Printing and Labelling |

| Data Capture and OCR |

| Last-Mile Delivery |

| Hub Automation |

| National Postal Operators |

| Courier, Express and Parcel (CEP) Companies |

| E-commerce Fulfilment Centers |

| Government Agencies and Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution | Hardware | |

| Software | ||

| Services | ||

| By Technology | Culler-Facer-Canceller (CFC) Systems | |

| Letter Sorters | ||

| Flat Mail Sorters | ||

| Parcel Sorters | ||

| Mixed-Mail Sorters | ||

| Coding and Printing/OCR Systems | ||

| Automated Guided Vehicles and Robotics | ||

| Others | ||

| By Application | Parcel Sorting | |

| Mail Sorting | ||

| Address Printing and Labelling | ||

| Data Capture and OCR | ||

| Last-Mile Delivery | ||

| Hub Automation | ||

| By End User | National Postal Operators | |

| Courier, Express and Parcel (CEP) Companies | ||

| E-commerce Fulfilment Centers | ||

| Government Agencies and Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the mail sorting systems market?

The market generated USD 11.33 billion in revenue in 2026 and is on track to reach USD 25.27 billion by 2031.

Which region is expanding fastest in mail sorting automation?

Asia-Pacific posts the highest CAGR as China, Japan and South Korea scale large-format projects to handle rising e-commerce volumes.

Why are services growing faster than hardware?

Operators prefer managed automation contracts that shift performance risk to vendors, accelerating service revenue at a 20.25% CAGR even as hardware remains essential.

How do labor shortages influence technology choices?

Worker scarcity increases demand for robotic singulation and AGV systems that sustain throughput without adding headcount, boosting robotics growth at 23.2% CAGR.

What role do sustainability regulations play in equipment selection?

EU ecodesign rules and the Net Zero Industry Act encourage buyers to replace older sorters with energy-efficient models, creating a strong replacement market in Europe.

Who are the leading vendors in the mail sorting systems market?

Key players include Vanderlande, Pitney Bowes, Toshiba Infrastructure Systems, NEC, BlueCrest, Dematic and LiBiao, each focusing on integrated hardware-software solutions and outcome-based services.

Page last updated on: