Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

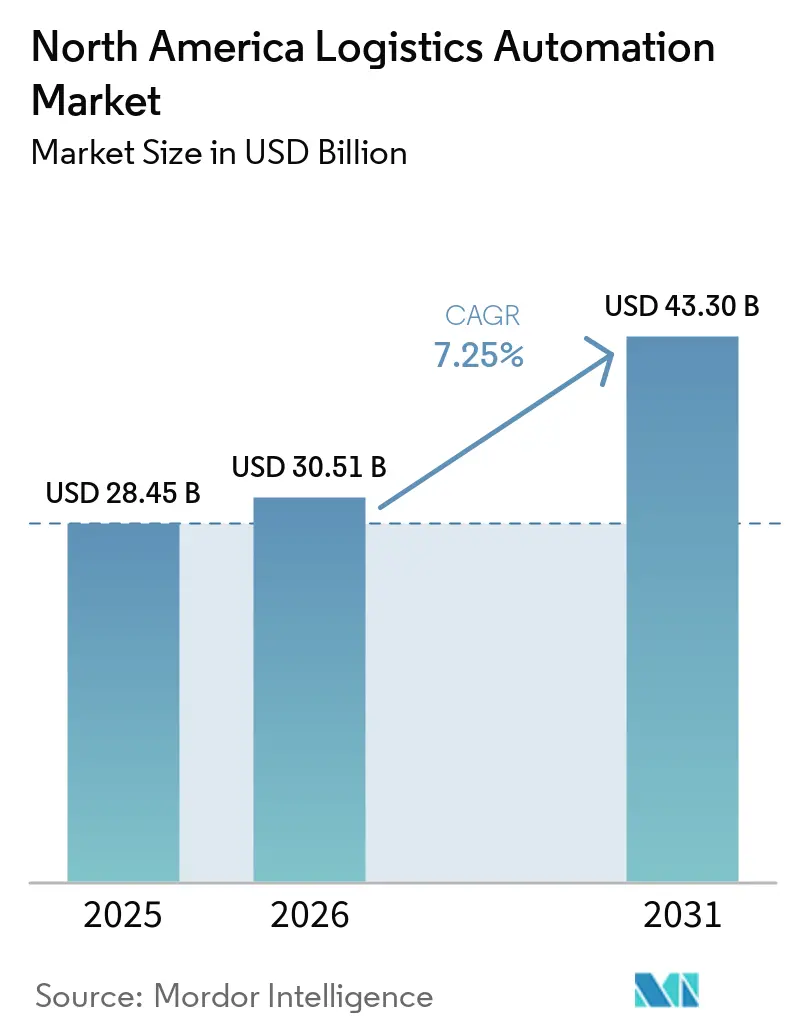

| Base Year Market Size (2025) | USD 28.45 Billion |

| Market Size (2026) | USD 30.51 Billion |

| Market Size (2031) | USD 43.30 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Logistics Automation Market Analysis by Mordor Intelligence

The North America logistics automation market size is expected to grow from USD 28.45 billion in 2025 to USD 30.51 billion in 2026 and is forecast to reach USD 43.30 billion by 2031 at 7.25% CAGR over 2026-2031. The North America logistics automation market is being reshaped by a long-term shift away from manual warehouse layouts and toward capital-heavy automated infrastructure built for faster delivery, tighter labor conditions, and redesigned regional supply chains. Demand is strongest where operators need more throughput from existing facilities, especially as delivery windows keep narrowing and labor availability remains uneven across major logistics corridors. The market also reflects a clear split between large operators that can fund multiyear automation programs and smaller providers that often phase projects more cautiously because integration and payback risks remain high. Competitive strategy in the North America logistics automation market is increasingly centered on software coordination, flexible robotics, and modular deployment models rather than only on the scale of fixed equipment. This leaves room for continued expansion across warehouses, transportation networks, and greenfield sites linked to nearshoring in the United States and Mexico.

Key Report Takeaways

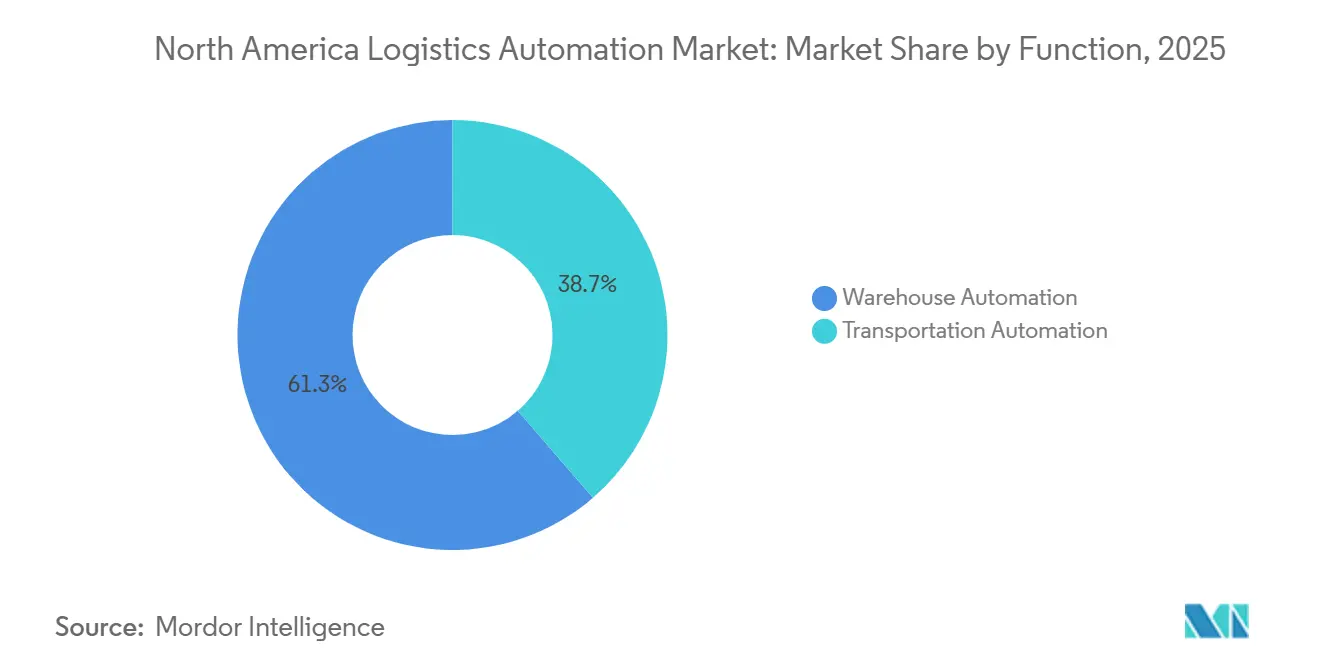

- By function, warehouse automation held 61.34% of the North America logistics automation market in 2025, while transportation automation is projected to grow at an 7.94% CAGR from 2026 to 2031.

- By automation level, semi-automated systems accounted for 55.90% of the North America logistics automation market in 2025, while fully-automated systems are forecast to expand at a 8.13% CAGR through 2031.

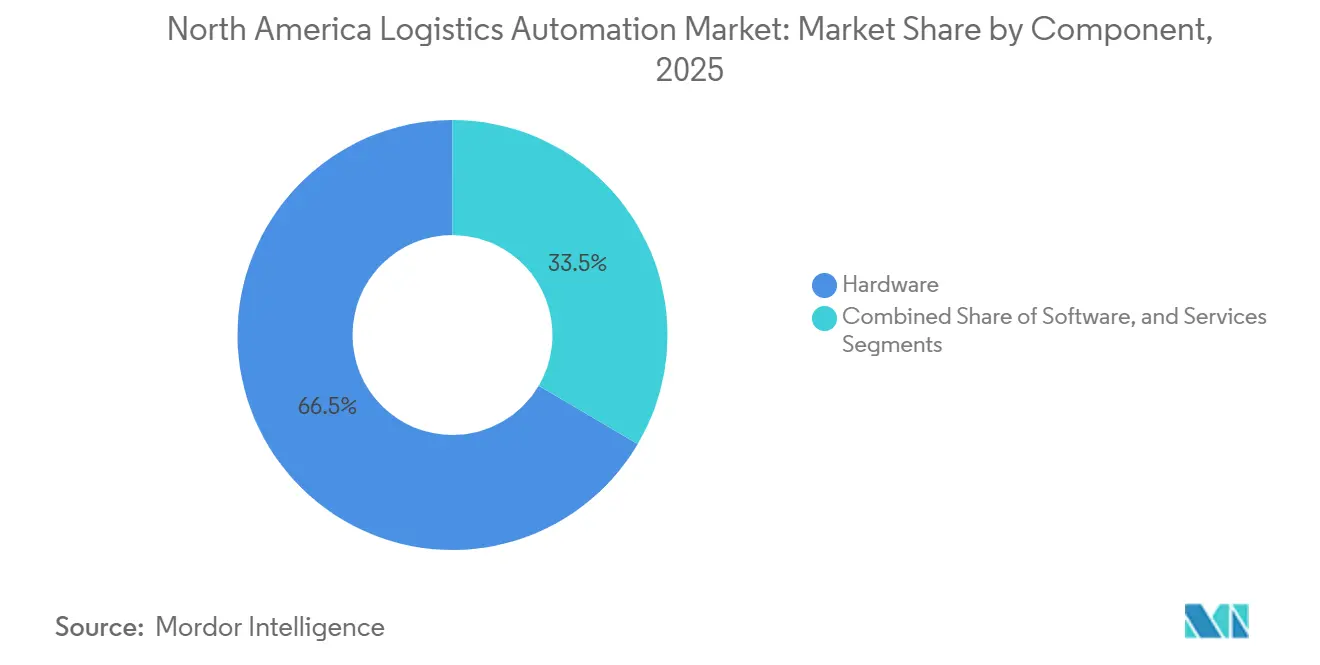

- By component, hardware accounted for 66.54% of the North America logistics automation market in 2025, while software is forecast to expand at a 8.21% CAGR through 2031.

- By end-user industry, e-commerce and parcel captured 42.67% of the North America logistics automation market in 2025, while grocery retail is set to grow at a 7.89% CAGR from 2026 to 2031.

- By country, the United States represented 77.89% of the North America logistics automation market in 2025, while Mexico is projected to record the fastest growth at an 8.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Logistics Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Fulfillment Density and Same-Day Service Levels | +2.1% | US core markets, spill-over to Canada and Mexico border hubs | Short term (≤ 2 years) |

| Warehouse Labor Scarcity and Wage Inflation | +1.8% | Global, most acute in US Sun Belt, Canada Prairie and Pacific regions | Short term (≤ 2 years) |

| AMR and AI Orchestration Adoption Across Fulfillment Centers | +1.3% | US-led, accelerating in Canada and Mexico automotive corridors | Medium term (2-4 years) |

| Nearshoring-Led Network Redesign in Mexico and the United States | +0.9% | Mexico Bajio and northern border states, US Sun Belt inland ports | Medium term (2-4 years) |

| Ergonomic-Risk Mitigation in High-Throughput Fulfillment Sites | +0.5% | US national, compliance influence from OSHA NEP CPL 03-00-026 | Short term (≤ 2 years) |

| Tax Incentives for Domestic and Cross-Border Automation Investments | +0.4% | US nationwide, USMCA-preferential zones in Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce Fulfillment Density and Same-Day Service Levels

Same-day delivery has moved from a premium service into a core operating requirement across the North America logistics automation market. Amazon exceeded 1 billion same-day or overnight deliveries in the year-to-date period through mid-2026 and added 18 same-day facilities in mid-sized US metro areas in April 2026, which pushed automation demand deeper into suburban and exurban nodes. That shift forces operators to process more units per square meter, which strengthens the case for high-speed sortation, compact ASRS, and goods-to-person workflows. It also redirects investment away from only very large fulfillment centers and toward smaller micro-hubs that still need dense automation to stay competitive. In the North America logistics automation market, service-level pressure is now shaping facility design as much as labor cost or storage density. The result is a faster move toward modular systems that can be deployed close to demand without waiting for full-scale greenfield construction.

Warehouse Labor Scarcity and Wage Inflation

Labor scarcity remains one of the strongest economic drivers in the North America logistics automation market because operators are responding to a structural problem rather than a short-term cycle. Average hourly earnings in US warehousing and storage reached USD 26.58 in January 2026 and USD 26.68 in February 2026, up from USD 25.02 in January 2025, which kept wage pressure elevated across warehouse networks.[1]U.S. Bureau of Labor Statistics, “Average Hourly Earnings of All Employees, Warehousing and Storage,” Bureau of Labor Statistics, bls.gov Compensation costs for private industry workers rose 3.4% in the 12 months to March 2026, which shows that payroll pressure remained firm even as real gains stayed limited. A 2025 ILR Review study found that warehouse robotics was associated with a 40% reduction in severe injuries and a 77% rise in non-severe injuries, which reinforced the need for better ergonomic design at human-robot workstations. This has shifted procurement priorities toward goods-to-person stations and better workflow design rather than only toward higher robot counts. In the North America logistics automation market, software that coordinates people and machines is increasingly viewed as the clearest path to labor-productivity gains.

AMR and AI Orchestration Adoption Across Fulfillment Centers

The North America logistics automation market is moving into a stage where software orchestration matters as much as the machines on the floor. MIT and Symbotic showed in March 2026 that an AI-based robot routing system improved warehouse throughput by 25% over baseline methods by rerouting robots before congestion formed. That result supports the growing view that competitive advantage now sits in the control layer that coordinates AMRs, ASRS, and human labor in real time. Dematic reinforced that direction in April 2026 when it partnered with GreyOrange to bring GreyMatter AI orchestration into its software ecosystem. AutoStore also expanded this shift in March 2026 through CubeVerse and AutoStore Intelligence, using more than 20 proprietary AI models to improve throughput without requiring additional hardware. In the North America logistics automation market, operators that adopt multi-vendor orchestration earlier are better placed to unlock capacity from mixed fleets and reduce congestion inside dense fulfillment networks. This is also why software is growing faster than hardware, even as robot deployments continue to rise.

Nearshoring-Led Network Redesign in Mexico and The United States

Nearshoring is adding a new layer of demand to the North America logistics automation market because manufacturing growth now requires matching distribution and cross-border logistics capacity. C.H. Robinson reported that Flex committed USD 1 billion to manufacturing operations across 3 Mexican states in 2025, and Mexico held a 37% share of US computing equipment imports as demand for data center and AI hardware rose. Those shifts matter because higher manufacturing output drives the need for faster sortation, denser storage, and better outbound visibility across cross-border flows. Logistic Properties of the Americas entered a master forward purchase agreement in March 2026 for Class A industrial real estate in the Mexico City metropolitan area, citing nearshoring demand and e-commerce growth as the key drivers. The North America logistics automation market is therefore gaining from greenfield construction in Mexico and from inland logistics investment tied to US Sun Belt freight corridors. This trend is especially supportive of automation vendors that can combine warehouse control, AIDC, and cross-border system connectivity in one deployment path.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Outlays for Fixed Automation | -1.5% | US national, especially acute for mid-market 3PLs and regional distributors | Short term (≤ 2 years) |

| Legacy-System Integration and Brownfield Retrofit Complexity | -1.0% | US Midwest and Northeast aging distribution infrastructure, Canadian brownfield sites | Medium term (2-4 years) |

| Steel Tariff Volatility and Longer Automation Payback | -0.6% | US national, highest impact in conveyor-heavy and ASRS-heavy installations | Short term (≤ 2 years) |

| Robot-Cell Safety and Cybersecurity Compliance Burden | -0.4% | US national, concentrated in food, pharmaceutical, and high-security distribution verticals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Outlays for Fixed Automation

Fixed automation remains a real constraint on the North America logistics automation market because large conveyor networks, integrated sortation, and end-to-end ASRS systems still require multiyear capital commitments. This pressure is strongest among mid-market 3PLs and regional distributors that do not have the same balance sheet flexibility as large retailers or large distributors. Steel-related equipment inflation has also made investment decisions harder by extending payback periods and increasing caution around turnkey projects. Operators do have some relief through tax policy, as the Section 179 deduction ceiling for qualifying equipment placed in service in 2026 reached USD 2,560,000 under IRS guidance.[2]U.S. Internal Revenue Service, “Publication 946, How To Depreciate Property,” Internal Revenue Service, irs.gov The same tax framework also supports 100% bonus depreciation for qualifying property, which lowers the effective first-year cost of eligible automation assets. Even with that support, many buyers in the North America logistics automation market still prefer phased deployments or flexible commercial models when project risk remains high.

Legacy-System Integration and Brownfield Retrofit Complexity

Brownfield retrofits slow the North America logistics automation market because much of the region's active warehouse capacity was built before modern robotics, WES, and digital orchestration became standard. Older facilities often combine legacy ERP and WMS logic, equipment from several vendors, narrow aisle layouts, and uneven floors that complicate navigation and commissioning. These issues make full automation harder to sequence, especially when operators must keep sites live during installation and cutover. A March 2026 case from Veltins Brewery shows how long these transitions can run, with a complete WMS replacement launched in 2026 and full commissioning expected only in 2029. This timeline illustrates why phased migration tools, API-first connectivity, and digital simulation are becoming more important in retrofit projects. In the North America logistics automation market, vendors with proven migration frameworks hold a practical advantage over suppliers whose systems are best suited only for greenfield environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Warehouse Automation Leads While Transportation Gains Speed

Warehouse automation held 61.34% of revenue in 2025, which placed it at the center of the North America logistics automation market as operators focused on picking, storage, sortation, and conveyor-intensive flows inside the facility. Warehouse automation accounted for 61.34% of the North America logistics automation market share in 2025 because the return on investment has historically been easiest to capture inside controlled indoor environments. Goods-to-person ASRS, AMR fleets, and warehouse execution software continue to define this segment because they directly improve throughput, labor productivity, and order accuracy. Medline expanded that pattern in May 2026 when it deployed its 24th AutoStore installation at its Aurora, Colorado distribution center, adding 96 robots and 38,000 bins to support regional demand. The North America logistics automation market continues to treat indoor handling as the first place where high-volume operators standardize automation across a national footprint.

Transportation automation started from a smaller base, but it is the fastest-growing function at a 7.94% CAGR through 2031, and that growth reflects the early commercialization of SAE Level 4 freight lanes. Gatik became the first US company to complete fully driverless commercial deliveries at scale in January 2026, recording 60,000 driverless orders for Fortune 50 retailers in Texas, Arkansas, and Arizona without incident. Aurora Innovation and McLane also announced in May 2026 that they would begin driverless hauls in Texas between Dallas and Houston, with plans to expand across the US Sun Belt.

By Automation Level: Semi-Automated Systems Still Dominate While Fully Automated Systems Advance

Semi-automated systems held 55.90% of revenue in 2025, which reflected the practical structure of most active warehouses in the North America logistics automation market. Semi-automated systems carried 55.90% of revenue because most brownfield sites still combine WMS-directed human labor with targeted robotics for repetitive tasks such as goods-to-person picking, pallet movement, or palletizing. This model helps operators improve throughput without taking on the cost and operational risk of a full cutover. Staples Canada showed the appeal of this approach in 2025 when it deployed 50 Locus Robotics AMRs in a Vancouver fulfillment center and reached full operational integration within 4 days. In the North America logistics automation industry, this hybrid structure remains the default for facilities with variable volumes, seasonal spikes, and existing layouts that are not easy to redesign.

Fully-automated systems are growing faster, with an 8.13% CAGR through 2031, because greenfield projects and major network refreshes are now being designed for unattended or near-unattended workflows. Falling sensor costs, better perception software, and stronger confidence in continuous robotic operation are supporting that move. Locus Robotics launched Locus Array at MODEX 2026 as a fully autonomous fulfillment system that combines mobile robotics, an integrated picking arm, and AI-powered perception, with early deployments already underway at DHL Supply Chain in North America. Locus then acquired Nexera Robotics in May 2026 to add NeuraGrasp technology and widen the system's SKU-handling range. The North America logistics automation market is therefore narrowing the gap between partial automation and full autonomy as mobile robotics and robotic manipulation increasingly run on a shared orchestration layer.

By Component: Hardware Anchors Revenue While Software Becomes the Control Layer

Hardware accounted for 66.54% of revenue in 2025, which kept it as the largest component segment in the North America logistics automation market. Hardware captured 66.54% of the North America logistics automation market size in 2025 because ASRS structures, conveyor systems, sortation equipment, mobile robots, and AIDC technologies still represent the largest upfront spending pool. This part of the market remains essential because physical throughput still depends on the installed base of machines that move, store, sort, and identify goods. Geekplus highlighted ongoing hardware innovation in March 2026 when it introduced RoboShuttle V5, a next-generation autonomous case-handling system built to integrate storage, pick-and-place, and put-away workflows.[3]Geekplus Technology Co., Ltd., “Geekplus Launches Next-Gen RoboShuttle V5, Setting a New Industry Standard for Autonomous Picking and Fulfillment,” Geekplus Newsroom, geekplus.com In practical terms, the North America logistics automation market still rests on hardware, but buyer preference is shifting toward modular equipment that can be expanded in phases rather than only through one large installation event.

Software at 8.21% CAGR through 2031 marks the fastest component expansion in the North America logistics automation market size profile because value is moving toward orchestration, visibility, and performance optimization. WES platforms, AI routing tools, cloud analytics, and real-time exception handling have become the most important tools for extracting more throughput from installed assets. Kardex strengthened that direction in April 2026 when it launched the Kardex ONE software ecosystem for WMS connectivity, monitoring, and AI-driven performance insights in AutoStore-based operations. Services continue to contribute through integration, maintenance, and subscription-led deployment models, but the decisive competitive layer in the North America logistics automation market is increasingly the software stack that sits above the equipment.

By End-User Industry: E-Commerce and Parcel Sets the Scale While Grocery Retail Grows the Fastest

E-commerce and parcel held 42.67% of revenue in 2025, which made it the largest end-user segment in the North America logistics automation market. E-commerce and parcel led because operators in this segment spent several years building fulfillment density to support same-day and next-day commitments, and that pressure has not eased. The largest retailers have raised the standard for speed and accuracy, which leaves 3PLs and direct-to-consumer brands under pressure to automate or accept weaker fulfillment economics. Exotec illustrated this in 2025 through its deployment at Komar Distribution Services' 760,000-square-foot Savannah facility, where the Skypod system is being used to support direct-to-consumer fulfillment across apparel, home goods, and consumer products brands.[4]Exotec, “Exotec and Komar Distribution Services Launch Next-Generation Automated Fulfillment Center in Savannah,” Exotec Newsroom, exotec.com In the North America logistics automation market, this segment remains the most visible buyer of high-density picking, storage, and sortation systems because order variety and delivery expectations are both high.

Grocery retail is the fastest-growing end-user vertical at a 7.89% CAGR through 2031 because online grocery, cold-chain handling, and labor intensity combine into a strong automation case. Associated Wholesale Grocers and Symbotic announced in March 2026 that they would deploy a high-density automated system across 114,000 square feet at AWG's Gulf Coast Division Support Center in Pearl River, Louisiana, with the capacity to handle nearly 19 million cases annually. OPEX and Peltier also introduced a multi-temperature zone and multi-deep cold storage automated fulfillment solution in January 2026, integrating active cooling directly into ASRS totes and removing the need for dedicated freezer chambers. These deployments show why temperature-controlled operations are becoming one of the most active adoption areas in the North America logistics automation market. Manufacturing, food and beverage, apparel, and other end-user groups still account for the balance, but grocery is expanding faster because cold-chain errors are costly and manual handling is difficult to scale.

Geography Analysis

The United States held 77.89% of regional revenue in 2025, which kept it as the center of the North America logistics automation market by installed base, operator scale, and vendor depth. The United States held 77.89% of the North America logistics automation market share in 2025 because it combines high e-commerce order density with the region's deepest fulfillment and distribution footprint. Amazon's addition of 18 same-day facilities in mid-sized US metro areas in April 2026 showed how quickly fulfillment infrastructure is moving closer to demand clusters. Tax policy also supports automation investment, as IRS guidance for 2026 preserved a Section 179 deduction ceiling of USD 2,560,000 and supported 100% bonus depreciation for qualifying property.

That environment favors large-scale and repeat automation programs, especially across the US Sun Belt, where new logistics construction remains active. The North America logistics automation market is also seeing more demand in older Midwest and Northeast facilities, but those projects lean more heavily toward modular systems because retrofit complexity is higher. This difference matters because brownfield demand in the United States is likely to reward suppliers that can layer automation onto existing WMS and equipment without long shutdowns. It also explains why flexible robotics and software-led control are gaining ground even as fixed automation remains important. Across the North America logistics automation market, the United States will likely remain the largest buyer base because both service-level pressure and capital access are stronger there than elsewhere in the region.

Mexico is the fastest-growing country market, with an 8.25% CAGR through 2031, and this growth is tied closely to nearshoring-led industrial buildout. Flex's USD 1 billion commitment across 3 Mexican states in 2025 and Mexico's 37% share of US computing equipment imports show how cross-border manufacturing density is strengthening. Logistic Properties of the Americas added to that pattern in March 2026 through a forward purchase agreement for Class A industrial real estate in the Mexico City metropolitan area, citing nearshoring demand and e-commerce growth. Canada held the remaining share of the North America logistics automation market and is developing through a different path that is driven more by labor shortages and facility productivity than by large-scale nearshoring. Staples Canada's AMR rollout across Vancouver and Ontario fulfillment centers reached full production in 4 days at each site, showing why AMR-first deployment models fit Canadian operations that need speed and flexibility. Canada also continues to benefit from cargo and logistics modernization around major transport nodes, while warehouse employers face persistent staffing gaps that support further automation adoption.

Competitive Landscape

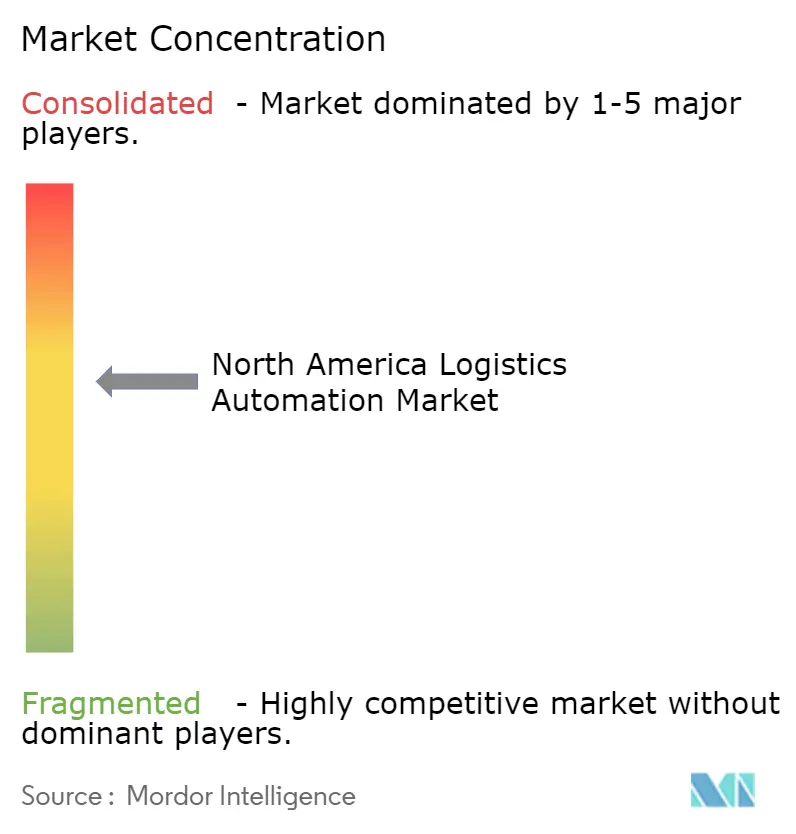

The North America logistics automation market is moderately concentrated in its upper tier, where Daifuku, Dematic, Toyota Automated Logistics, KNAPP, SSI SCHAEFER, and Swisslog compete for complex fixed-automation programs across large fulfillment and distribution sites. Below that level, the North America logistics automation market becomes more fragmented, with AMR-focused players such as AutoStore, Locus Robotics, Geekplus, and Hai Robotics contesting flexible deployments that offer faster implementation and lower entry capital requirements. This structure creates two competitive arenas, one centered on large integrated systems and another centered on modular robotics and software-led flexibility. It also explains why buyers often compare vendors on deployment speed, control software, and integration capability rather than only on equipment specifications.

One of the clearest strategic shifts in 2026 has been the collapse of the old separation between hardware suppliers and software providers. Dematic's April 2026 partnership with GreyOrange brought GreyMatter AI orchestration into Dematic's ecosystem, which signaled that even large fixed-automation players now view orchestration software as essential. AutoStore moved in the same direction as CubeVerse and AutoStore Intelligence, which were designed to improve throughput inside existing systems without adding hardware. Locus Robotics expanded its position through Locus Array in April 2026 and then strengthened robotic manipulation through the Nexera acquisition in May 2026. These moves show that the North America logistics automation market is rewarding vendors that can turn one-time hardware deployments into recurring software, service, and upgrade relationships.

Another major change came from Toyota Industries Corporation's April 2026 launch of Toyota Automated Logistics, which combined Vanderlande's warehousing business, Bastian Solutions, and viastore into one global brand. That reorganization created a stronger integration platform with broad reach across North America and reduced the relevance of Viastore as a standalone name in this market. At the same time, Geekplus reported that new signed orders in the Americas grew by more than 50% year on year in 2025, which showed that price-competitive and flexible robotics suppliers continue to make inroads. The North America logistics automation market still offers room in mid-market 3PL automation, cold-chain fulfillment, and cross-border transportation orchestration, but the vendors most likely to gain share are those that combine integration depth with vendor-agnostic software and faster deployment cycles.

North America Logistics Automation Industry Leaders

Daifuku Co., Ltd.

SSI SCHAEFER AG

KNAPP AG

Vanderlande Industries B.V.

BEUMER Group GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Medline unveiled its 24th AutoStore installation at its Aurora, Colorado distribution center, featuring 96 robots and 38,000 bins, expanding the company's global robot fleet to more than 2,100 units. The Aurora site is part of Medline's systematic effort to scale throughput and order capacity across its US distribution network to meet growing healthcare customer demand.

- April 2026: Dematic and GreyOrange announced a strategic partnering relationship at MODEX 2026, Atlanta, April 13-16, enabling Dematic to offer GreyOrange's GreyMatter AI-powered platform that coordinates robots and workflows for improved speed and accuracy, creating unified orchestration of fixed automation, AMRs, and human workflows within a single system.

- April 2026: Locus Robotics launched Locus Array, a fully autonomous fulfillment system combining mobile robotics, an integrated robotic picking arm, and AI-powered perception. Early deployments began with customers including DHL Supply Chain in North America, with global expansion to Europe and APAC underway.

- March 2026: AutoStore launched the CubeVerse platform, a new cloud-based software ecosystem that unifies data, applications, and AI capabilities across the fulfillment lifecycle, introducing AI-powered analytics, self-optimizing fulfillment, and 24/7 operation support within existing AutoStore grid installations without additional hardware.

North America Logistics Automation Market Report Scope

The North America Logistics Automation Market is Segmented by Function (Warehouse Automation and Transportation Automation), Automation Level (Fully-Automated and Semi-Automated), Component (Hardware, Software, and Services), End-User Industry (E-commerce and Parcel, Food and Beverage, Grocery Retail, Apparel and Fashion, Manufacturing, and Other End-User Industries), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Function

| Warehouse Automation | Component | Hardware | Mobile Robots |

| Automated Storage and Retrieval Systems | |||

| Automated Sorting Systems | |||

| Conveyor Systems | |||

| Automatic Identification and Data Collection (AIDC) | |||

| Order Picking | |||

| Software | |||

| Services | |||

| Transportation Automation | Component | Hardware | |

| Software | |||

| Services |

By Automation Level

| Fully-Automated Systems |

| Semi-Automated Systems |

By Component

| Hardware |

| Software |

| Services |

By End-User Industry

| E-commerce and Parcel |

| Food and Beverage |

| Grocery Retail |

| Apparel and Fashion |

| Manufacturing |

| Other End-User Industries |

By Country

| United States |

| Canada |

| Mexico |

| By Function | Warehouse Automation | Component | Hardware | Mobile Robots |

| Automated Storage and Retrieval Systems | ||||

| Automated Sorting Systems | ||||

| Conveyor Systems | ||||

| Automatic Identification and Data Collection (AIDC) | ||||

| Order Picking | ||||

| Software | ||||

| Services | ||||

| Transportation Automation | Component | Hardware | ||

| Software | ||||

| Services | ||||

| By Automation Level | Fully-Automated Systems | |||

| Semi-Automated Systems | ||||

| By Component | Hardware | |||

| Software | ||||

| Services | ||||

| By End-User Industry | E-commerce and Parcel | |||

| Food and Beverage | ||||

| Grocery Retail | ||||

| Apparel and Fashion | ||||

| Manufacturing | ||||

| Other End-User Industries | ||||

| By Country | United States | |||

| Canada | ||||

| Mexico | ||||

Key Questions Answered in the Report

What is the size outlook for North America logistics automation through 2031?

The North America logistics automation market stood at USD 30.51 billion in 2026 and is forecast to reach USD 43.30 billion by 2031 at a 7.25% CAGR.

Which function leads demand across this space?

Warehouse automation remained the largest function with 61.34% of revenue in 2025 because storage, picking, and sortation still offer the clearest return on automation spending.

Which area is growing fastest in logistics automation across North America?

Transportation automation is the fastest-growing function at a 7.94% CAGR through 2031, supported by early commercial deployments of SAE Level 4 autonomous freight operations.

Why is software gaining importance in fulfillment automation?

Software is the fastest-growing component at an 8.21% CAGR because operators increasingly need orchestration tools that coordinate robots, ASRS, and labor in real time across mixed environments.

Which end-user segment is shaping current investment patterns the most?

E-commerce and parcel led with 42.67% of revenue in 2025, while grocery retail is growing fastest at 7.89% CAGR as cold-chain and online grocery requirements push new automation spending.

Which country offers the fastest growth opportunity in the region?

Mexico is the fastest-growing country market at an 8.25% CAGR through 2031, supported by nearshoring-linked industrial expansion and rising demand for automated cross-border logistics infrastructure.

Page last updated on: