Main Automation Contractor (MAC) in the Oil and Gas Industry Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

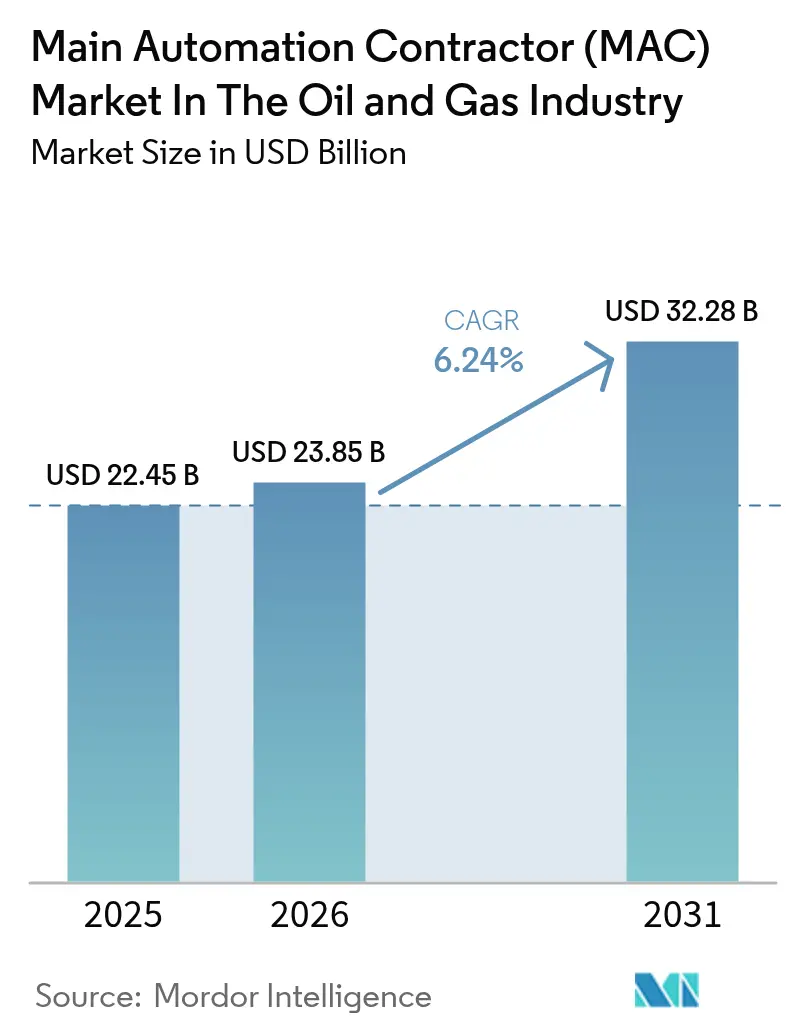

| Market Size (2026) | USD 23.85 Billion |

| Market Size (2031) | USD 32.28 Billion |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Middle East |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Main Automation Contractor (MAC) in the Oil and Gas Industry Analysis by Mordor Intelligence

The main automation contractor (MAC) market size in the oil and gas industry market size in 2026 is estimated at USD 23.85 billion, growing from 2025 value of USD 22.45 billion with 2031 projections showing USD 32.28 billion, growing at 6.24% CAGR over 2026-2031. Expanding digital-first production philosophies, stricter safety rules, and operator preference for lifecycle service contracts continue to redraw the competitive field. Brownfield retrofits of 20-year-old control assets are soaking up capital even as LNG megaproject sanctions revive greenfield activity. Meanwhile, national content mandates in the Middle East and Africa spur modular project scopes, encouraging local integrators and eroding Tier-1 pricing power. Subsea electrification, all-electric trees, and digital twins also widen the technology gap between full-scope Main Automation Contractor market leaders and regional challengers. Finally, IEC 62443 cybersecurity compliance has moved from best practice to bid-gate requirement, tilting revenue toward software, managed detection, and incident-response services.

Key Report Takeaways

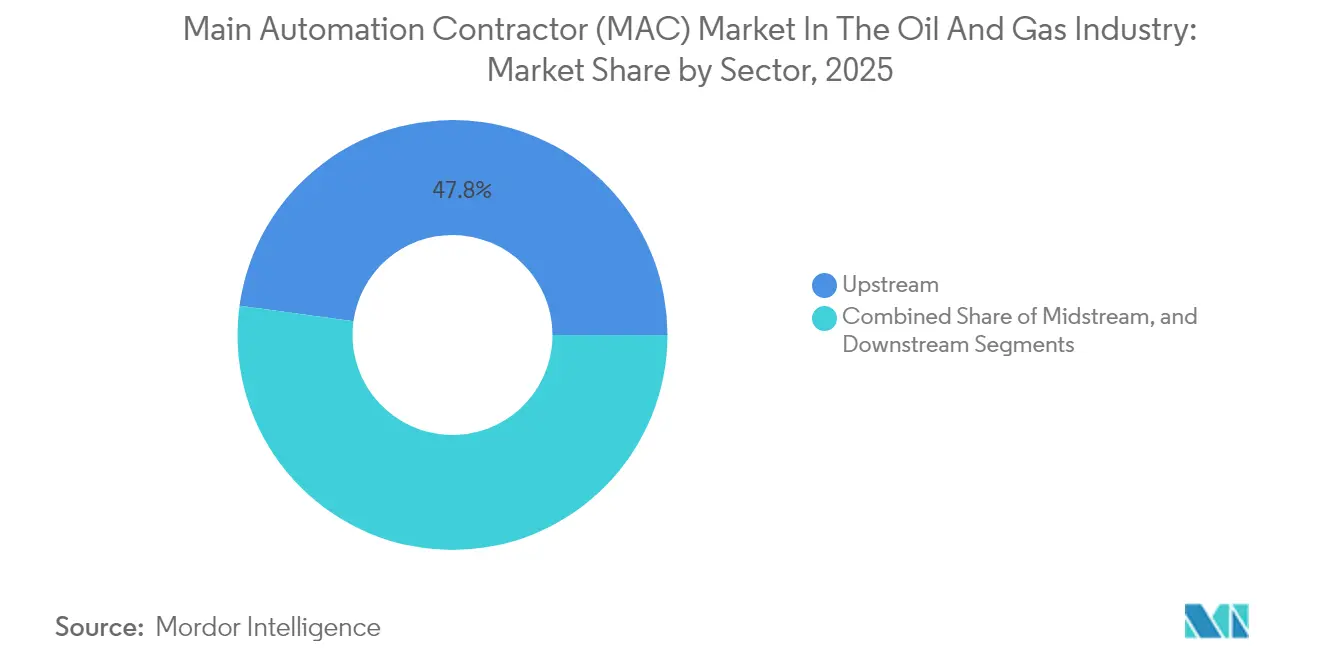

- By sector, upstream operations led with 47.82% of the Main Automation Contractor (MAC) in the Oil and Gas Industry share in 2025, while midstream is forecast to expand at a 7.12% CAGR through 2031.

- By project phase, brownfield retrofits held a 56.16% share of the Main Automation Contractor (MAC) in the Oil and Gas Industry in 2025; greenfield work is advancing at 7.98% CAGR to 2031.

- By service type, installation and commissioning commanded 34.71% of 2025 revenue, whereas maintenance and support is the fastest-growing segment at 7.53% CAGR.

- By automation system, Distributed Control Systems accounted for 42.21% share in 2025, while Supervisory Control and Data Acquisition platforms are growing at 9.31% CAGR.

- By project size, large awards above USD 31 million captured 59.08% of Main Automation Contractor (MAC) in the Oil and Gas Industry share in 2025; small and medium scopes between USD 5 million and USD 30 million are forecast to grow at 7.92% CAGR.

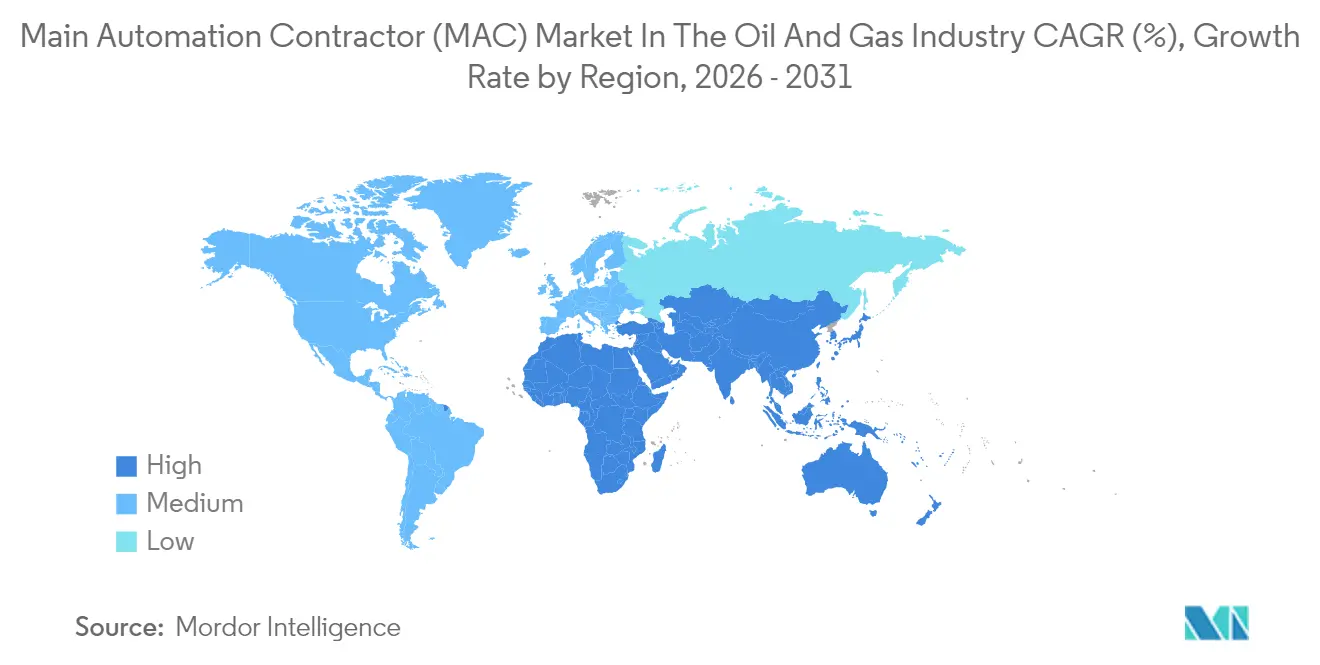

- By geography, the Middle East contributed 28.29% of 2025 spending, whereas Africa is expected to post the highest regional growth at 9.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Main Automation Contractor (MAC) in the Oil and Gas Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Integrated Automation Platforms to Reduce CAPEX and OPEX | +1.2% | Global, with early adoption in North America and Middle East | Medium term (2–4 years) |

| Accelerated Deployment of Deepwater and Subsea Projects Requiring Complex Automation | +0.9% | Global offshore basins, concentrated in Gulf of Mexico, Brazil, West Africa, and North Sea | Long term (≥ 4 years) |

| Digital Twin and Advanced Analytics Integration Enhancing MAC Value Proposition | +0.8% | Global, led by North America and Europe, expanding to Middle East and Asia-Pacific | Medium term (2–4 years) |

| Strict Safety and Environmental Regulations Driving Automation Upgrades | +0.7% | Global, with stringent enforcement in North America, Europe, and Middle East | Short term (≤ 2 years) |

| Growing Brownfield Modernization in Maturing Fields | +1.0% | Global, concentrated in Middle East, North America, and North Sea legacy assets | Short term (≤ 2 years) |

| Supply Chain Localization Incentives in Middle East Mega-Projects | +0.6% | Middle East (Saudi Arabia, UAE, Qatar) with spillover to North Africa | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Integrated Automation Platforms Cut Costs

Operators are pulling disparate point solutions into unified ecosystems that span distributed control, safety instrumentation, and asset performance modules. Emerson’s February 2024 overhaul of LyondellBasell’s Wesseling cracker compressed a two-month engineering window into a two-week turnaround by using AI-powered code conversion, demonstrating how integrated suites shrink schedule risk and maintenance burdens.[1]Emerson, “LyondellBasell Selects Emerson to Modernize Automation Technology,” emerson.com S-OIL’s three-year S-imoms program linked 30 legacy applications into one backbone and is forecast to recoup its KRW 25.5 billion investment in under 15 months. ADNOC’s August 2024 rollout of Neuron 5 AI illustrates the upside: a 50% cut in unplanned shutdowns and a 20% extension of service intervals.[2]ADNOC, “ADNOC Deploys Pioneering AI-Enabled Process Optimization Technology,” adnoc.ae These outcomes validate a pay-as-you-save argument that accelerates integrated-platform adoption worldwide.

Deepwater and Subsea Projects Require High-Reliability Control

Ultra-deepwater assets such as Chevron’s Anchor field in the Gulf of Mexico employ 20,000 psi subsea trees, all-electric actuation, and long-offset tiebacks that demand real-time, deterministic automation. Subsea investment is predicted to grow roughly 10% annually through 2027, reaching USD 32 billion by end-2024, thereby enlarging the addressable Main Automation Contractor market. SLB OneSubsea’s 2024 FEED award for Equinor’s Fram Sør 12-well all-electric system underscores the pivot from hydraulic to fully electric control that simplifies installation, reduces carbon intensity, and integrates natively with digital twins

Digital Twins Amplify Lifecycle Value

BP’s cloud-hosted production-system twin links live historian tags with first-principle models to create virtual sensors, raising throughput without new hardware. Mitsubishi Heavy Industries has applied vessel-scale finite-element twins to floating production, storage and offloading hulls, letting operators forecast corrosion-driven fatigue life in real time. A 2025 peer-reviewed survey lists ISO 23247, ISO 15926, and IEC 62443 as baseline standards Main Automation Contractor suppliers must meet for a twin to pass class-society verification. Proven gains in uptime, safety, and carbon reduction are moving twins from pilot to procurement spec.

Safety and Environmental Regulation Spurs Retrofits

IEC 62443-2-1:2024 introduced a maturity model that governments now reference when licensing critical infrastructure, pushing operators to swap unencrypted protocols for secure OPC UA or MQTT. In parallel, TSA pipeline directives in the United States, the EU’s NIS2 Directive, and API Standard 1164 demand auditable cybersecurity programs. A 2024 Global Flow Measurement Workshop paper shows that custody-transfer meters must now deploy encrypted Modbus-TLS and role-based access controls, a specification achievable only on modern controller platforms. Such mandates accelerate controller upgrades and fuel service backlogs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Crude Prices Limiting Capital Expenditure | -0.9% | Global, with acute sensitivity in North America shale and marginal offshore projects | Short term (≤ 2 years) |

| Talent Shortage in Integrated Control System Engineering | -0.6% | Global, most severe in North America and Europe; emerging in Middle East and Asia-Pacific | Medium term (2–4 years) |

| Cybersecurity Concerns Over Multivendor Integration | -0.4% | Global, with heightened risk in regions with legacy OT infrastructure and limited security maturity | Short term (≤ 2 years) |

| Lengthy Approval Cycles for National Oil Company Projects | -0.5% | Concentrated in Middle East, Africa, and Latin America NOC-dominated markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude Prices Pressure Budgets

When Brent hovers below USD 85 per barrel, discretionary automation scopes slide to future years. Petrobras, for example, targets USD 100 million in annual rig-fleet savings through automation but is staging spend over multiple phases to hedge price uncertainty. Deepwater tiebacks among the first deferred when forward curves flatten illustrate how cyclicality chips 0.9 percentage points off the forecast CAGR.

Talent Shortage Stalls Project Velocity

Modern programs blend process, IT, and cybersecurity disciplines that universities rarely teach in one track. A 2024 industry study notes companies earmark up to 20% of digital budgets for training yet still struggle to source IEC 62443-literate control engineers.[3]International Journal of Research in Computer Applications and Information Technology, “Digital Skills Gap in Oil and Gas,” ijrcit.org ExxonMobil’s 10-year journey to commercial Open Process Automation required a multi-specialist team that remains scarce outside Tier-1 vendors. This bottleneck stretches commissioning schedules and raises labor rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Dominance, Midstream Momentum

Upstream assets generated nearly half of 2025 spending, yet midstream’s higher 7.12% CAGR signals structural catch-up as pipeline operators electrify compressor stations and add edge SCADA for leak detection. ADNOC’s USD 920 million program to digitize its onshore fields typifies the upstream installed-base advantage. However, new hydrogen-ready pipelines and CO₂ trunk lines will give midstream a larger slice of future Main Automation Contractor (MAC) in the Oil and Gas Industry revenue. Integrated control suites that merge pipeline simulation, SCADA, and predictive maintenance are rapidly becoming bid-spec norms. Meanwhile, downstream margins remain tight, limiting capital allocation to incremental advanced process control rollouts rather than whole-of-plant DCS swaps.

The Main Automation Contractor (MAC) in the Oil and Gas Industry share tied to upstream control packages is expected to trail the broader market as greenfield LNG and carbon-capture projects realign spending toward transmission and export hubs. Operators also channel funds into autonomous drilling and electric fracturing platforms that reduce rig crew counts and improve rate of penetration, thereby demonstrating tangible payback to investment committees.

By Project Size: Modular Scopes Gain Ground

Projects exceeding USD 31 million still dominate revenue, but small and medium contracts are expanding faster at an 7.92% CAGR as NOCs break mega-EPCs into digestible modules. Saudi Vision 2030 and the UAE’s In-Country Value drive this fragmentation, giving local integrators an opening to compete for decoupled instrumentation, cyber-hardening, and brownfield DCS migration work. Emerson’s AI-assisted code-conversion tool shortens shutdown windows, making sub-USD 10 million revamp packages economically practical for aging plants.

Large LNG trains, gas-processing expansions, and deepwater host platforms will continue to underpin Main Automation Contractor (MAC) in the Oil and Gas Industry size growth, but award timing creates revenue volatility. Mega-projects offer scale economies yet expose suppliers to sharper commodity-linked repricing when crude drops. Consequently, many players balance portfolios with a higher volume of quick-turn, medium-sized jobs that carry lower execution risk and faster cash conversion.

By Automation System: SCADA and Edge Computing Surge

Distributed Control Systems account for the largest installed base, but SCADA’s 9.31% CAGR rides the push toward remote, unmanned operations. ADNOC’s Satah Al Razboot field manages wells 20 kilometers offshore from an island-based control center, showcasing the economic allure of fewer offshore personnel. Edge gateways running containerized analytics now sit beside remote terminal units, pushing data reduction and AI inference to the field.

Programmable Logic Controllers remain indispensable for discrete sequences and safety interlocks, yet face replacement by virtualized controllers that O-PAS champions argue will shrink lifecycle cost. Safety Instrumented Systems enjoy premium margins owing to certification hurdles under IEC 61511. A Los Alamos report spotlighting unencrypted legacy PLC protocols has accelerated encrypted Modbus-TLS adoption, a shift that disadvantages vendors with slow firmware roadmaps.

By Service Type: Shift to Lifecycle Partnerships

Installation and commissioning still account for over one-third of 2025 revenue, but maintenance and support contracts are expanding quicker as operators favor predictable OpEx over lump-sum CapEx. Gecko Robotics’ wall-climbing inspection drones, under a multi-year ADNOC Gas deal, demonstrate how robotics-as-a-service embeds suppliers for the asset life. Predictive analytics subscriptions, patch-as-a-service, and remote SOC monitoring are displacing one-off call-outs.

Front-end engineering design stays critical for technology selection but represents a slim revenue slice. Procurement has largely been folded into EPC or installation scopes, trimming standalone purchase-order management business. Training, once limited to console skills, now covers data science, cyber incident response, and model validation, expanding addressable wallet share per asset.

By Project Phase: Brownfield Anchors Revenue, Greenfield Leads Growth

Brownfield upgrades supply 56.16% of 2025 dollars as operators extract more from maturing assets. Fast-swap I/O cards, hot-cutover tools, and AI-guided configuration utilities minimize downtime, strengthening the brownfield case. The Main Automation Contractor (MAC) in the Oil and Gas Industry size tied to greenfield projects is nonetheless growing faster at 7.98% CAGR, carried by sanctioned LNG trains and all-electric deepwater hubs that bake digital-twin readiness into FEED.

Emerson’s global framework with Shell spans both phases, ensuring a seat at early concept tables and retrofit turnarounds alike. ExxonMobil’s Baton Rouge plant proves that greenfield O-PAS control can slash lifecycle cost by around 20%, yet the installed base of legacy systems guarantees a steady retrofit pipeline well beyond 2030.

Geography Analysis

The Middle East contributed 28.29% of 2025 spending, underpinned by Saudi Aramco’s USD 7.7 billion Fadhili expansion and ADNOC’s multi-asset AI rollouts. Supply-chain localization schemes force Tier-1s to form joint ventures, invest in local assembly, and cede workshare to regional integrators. Africa is projected to deliver the highest regional CAGR at 9.55% on the back of deepwater sanctioning in Nigeria, Angola, and Senegal plus gas-export facilities in Mozambique and Tanzania. Frame agreements for subsea inspection and maintenance indicate follow-on service revenue that will outlast construction spend.

North America benefits from mature shale automation and prototype Open Process Automation deployments yet wrestles with cost-of-capital inflation and labor scarcity. Europe concentrates on electrifying offshore platforms, integrating carbon capture, and migrating to electric subsea architectures that dovetail with continental decarbonization targets. Asia-Pacific presents a fragmented picture: China and India bankroll refinery-petrochemical complexes, Australia pursues deepwater gas, and Southeast Asia advances floating storage and regasification units, each with distinct approval timelines and local-content hurdles. Collectively, these dynamics sustain diversification opportunities for suppliers capable of balancing project risk across basins. Regional policy shifts, such as methane-fee rules in the United States or net-zero mandates in Europe, will further shape spending patterns and technology choice.

Competitive Landscape

Eight Tier-1 vendors Emerson, Honeywell, Schneider Electric, ABB, Siemens, Yokogawa, Mitsubishi Electric, and Rockwell Automation control roughly 60 to 65% of global Main Automation Contractor (MAC) in the Oil and Gas Industry revenue through long-term framework deals and an installed DCS base that cements switching costs. Consolidation of vendor lists at super-majors places downward pressure on hardware margins, so incumbents pivot to software, AI analytics, and cybersecurity services to defend wallet share. Emerson’s five-year global pact with Shell secures pipeline visibility but commits the supplier to aggressive pricing and on-call resource delivery across all business units.

White-space growth lies in autonomous operations, subsea robotics, and edge-analytics-enabled twins. Oceaneering’s 250-unit ROV fleet, Gecko Robotics’ AI inspection drones, and AVEVA’s hybrid-cloud digital-twin suite illustrate specialist inroads. Open Process Automation threatens to unbundle control hardware and software, enabling competition from IT-native entrants if certification bodies rapidly endorse multi-vendor stacks. IEC 62443 certification has become a non-negotiable contract clause, raising the compliance bar for emergent challengers.

Main Automation Contractor (MAC) in the Oil and Gas Market Leaders

Rockwell Automation Inc.

Schneider Electric SE

Yokogawa Electric Corporation

Honeywell International Inc.

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ExxonMobil completed commercial-scale Open Process Automation at its Baton Rouge resin finishing unit, deploying about 100 controllers and 1,000 I/O points and reporting at least 20% lower lifecycle cost.

- January 2025: Emerson signed a five-year global framework with Shell covering DCS, SIS, maintenance, and future capital projects across upstream, downstream, and renewables.

- December 2024: BP extended its global agreement with ABB for integrated automation across all upstream and downstream assets.

- November 2024: ADNOC awarded Jereh Oil and Gas Engineering up to USD 920 million to install remote sensing and well-operating equipment across onshore fields.

Global Main Automation Contractor (MAC) in the Oil and Gas Industry Report Scope

The main automation contractor (MAC) is a contractor responsible for the instrumentation, control, information, and safety aspects of the project, working as a partner with the organization and managing the overall automation solution. The MAC primarily identifies all the automation activities with the development of an execution plan, obtaining the best resources, selecting the best technologies, implementing design and engineering, supplying the programs and hardware, and installing assemblies to achieve the complete automation solution efficiently and effectively.

The Main Automation Contractor (MAC) in the Oil and Gas Industry Report is Segmented by Sector (Upstream, Midstream, Downstream), Project Size (Small and Medium, Large), Automation System Type (DCS, PLC, SCADA, SIS, Other), Service Type (FEED, Procurement, Installation and Commissioning, Training, Maintenance and Support), Project Phase (Greenfield, Brownfield), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Upstream (Offshore and Onshore) |

| Midstream |

| Downstream |

| Small and Medium (USD 5 million to USD 30 million) |

| Large (USD 31 million and Above) |

| Distributed Control System (DCS) |

| Programmable Logic Controller (PLC) |

| Supervisory Control and Data Acquisition (SCADA) |

| Safety Instrumented System (SIS) |

| Other Automation System Types |

| Front-End Engineering Design (FEED) |

| Procurement |

| Installation and Commissioning |

| Training |

| Maintenance and Support |

| Greenfield |

| Brownfield |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

| By Sector | Upstream (Offshore and Onshore) | ||

| Midstream | |||

| Downstream | |||

| By Project Size | Small and Medium (USD 5 million to USD 30 million) | ||

| Large (USD 31 million and Above) | |||

| By Automation System Type | Distributed Control System (DCS) | ||

| Programmable Logic Controller (PLC) | |||

| Supervisory Control and Data Acquisition (SCADA) | |||

| Safety Instrumented System (SIS) | |||

| Other Automation System Types | |||

| By Service Type | Front-End Engineering Design (FEED) | ||

| Procurement | |||

| Installation and Commissioning | |||

| Training | |||

| Maintenance and Support | |||

| By Project Phase | Greenfield | ||

| Brownfield | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected revenue for main automation contractors in oil and gas by 2031?

The Main Automation Contractor market is forecast to reach USD 32.28 billion by 2031, expanding at a 6.24% CAGR.

Which region is expected to post the fastest growth in automation spending?

Africa is projected to grow the fastest at a 9.55% CAGR, driven by deepwater projects in Nigeria, Angola, and Senegal.

Why are midstream automation investments accelerating?

Pipeline electrification, remote SCADA for integrity management, and hydrogen-blending readiness are lifting midstream spend at a 7.12% CAGR.

How does Open Process Automation impact vendor selection?

O-PAS standards allow plug-and-play hardware, reducing vendor lock-in and potentially trimming lifecycle costs by about 20%.

What service segment shows the highest growth potential?

Maintenance and support services, including predictive analytics and remote SOC operations, are expanding at 7.53% CAGR as operators shift to lifecycle contracts.

How are cybersecurity regulations influencing control-system upgrades?

Adoption of IEC 62443 frameworks and national mandates now makes encrypted protocols, network segmentation, and certified development lifecycles mandatory for new control installations.

Page last updated on: