Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

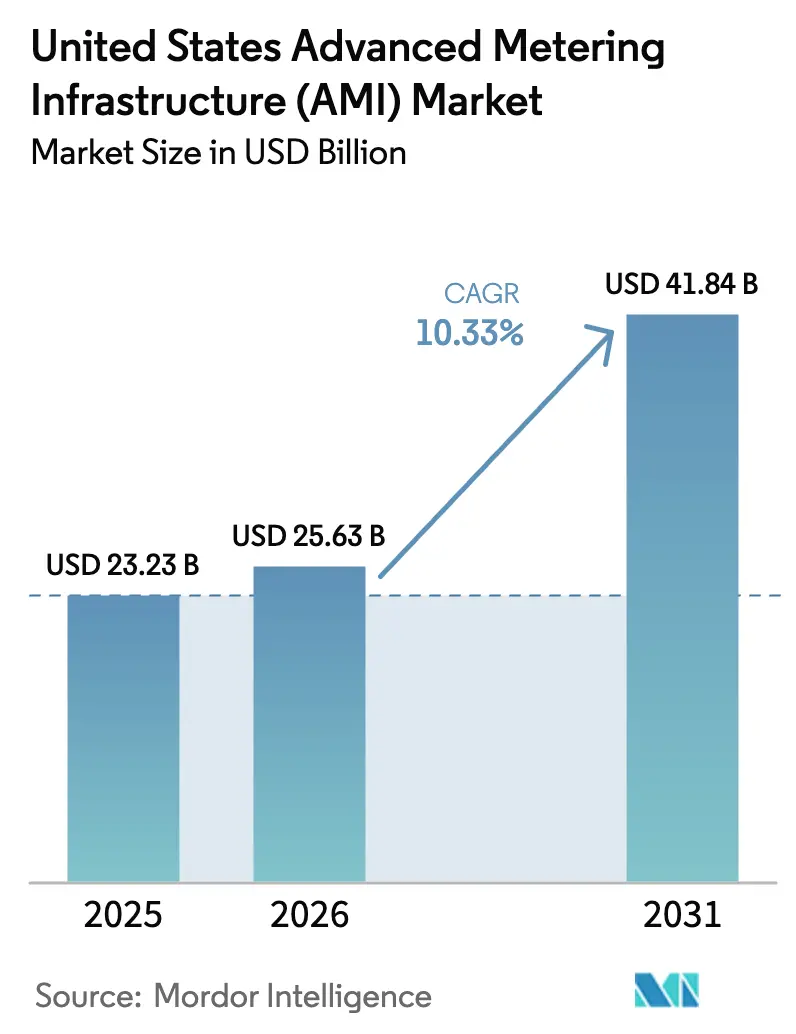

| Base Year Market Size (2025) | USD 23.23 Billion |

| Market Size (2026) | USD 25.63 Billion |

| Market Size (2031) | USD 41.84 Billion |

| Growth Rate (2026 - 2031) | 10.33% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Advanced Metering Infrastructure (AMI) Market Analysis by Mordor Intelligence

The US AMI market size is expected to grow from USD 23.23 billion in 2025 to USD 25.63 billion in 2026 and is forecast to reach USD 41.84 billion by 2031 at 10.33% CAGR over 2026-2031. Federal infrastructure incentives are shortening payback cycles and pushing utilities of every ownership model to procure advanced metering systems.[1]U.S. Department of Energy, “2024 Wrap-Up: Advancing a More Powerful Grid,” energy.gov Vendors now compete on analytics depth rather than meter counts, because utilities want grid optimization tools that create new revenue and customer value. Cybersecurity directives require embedded network monitoring, steering adoption toward secure, standards-compliant platforms.[2]Federal Energy Regulatory Commission, “FERC Strengthens Reliability Standards for Monitoring Electric Grid Cyber Systems,” ferc.gov A tightening labour pool is nudging utilities toward vendor-managed services and AI-enabled automation that streamlines grid operations.[3]Itron, “Utilities Face a Workforce Readiness Gap Amid AI/ML Adoption Challenges,” itron.com These forces are reshaping competitive strategies throughout the US AMI market by putting data-centric value creation ahead of hardware volume.

Key Report Takeaways

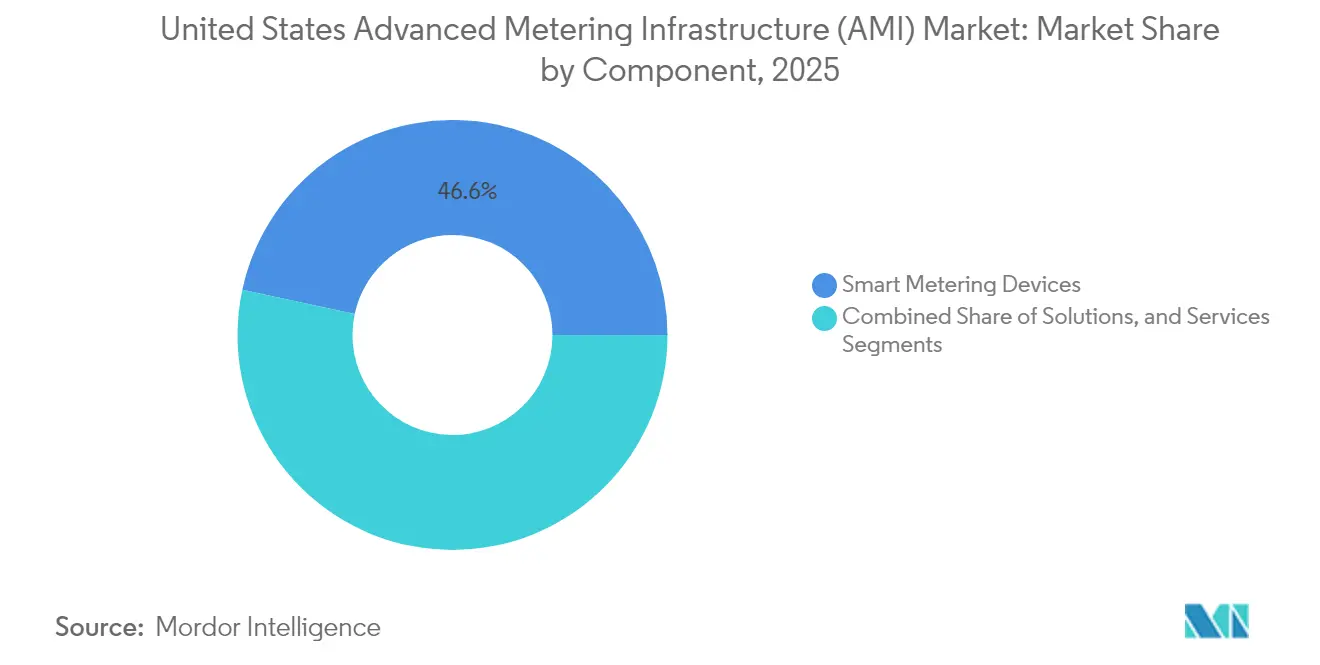

- By component, Smart Metering Devices captured 46.62% of the US AMI market share in 2025, while Software led by Meter Data Analytics is expanding at a 13.62% CAGR through 2031.

- By end-user, residential customers accounted for 88.35% of the US AMI market in 2025, whereas the industrial segment is growing at a 12.92% CAGR to 2031.

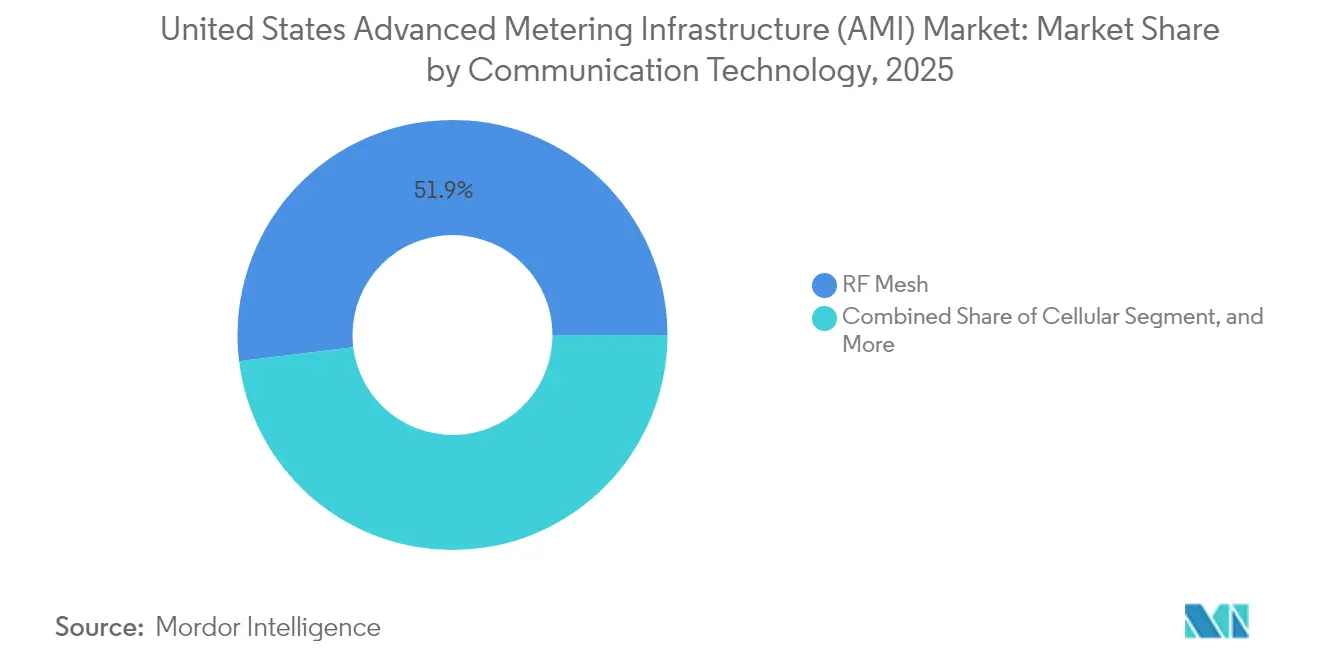

- By communication technology, RF Mesh commanded 51.94% share in 2025, yet Cellular connectivity is rising fastest with a 13.78% CAGR through 2031.

- By utility ownership type, Investor-Owned Utilities held 64.12% share in 2025, but Electric Cooperatives are advancing at the highest rate of 14.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Advanced Metering Infrastructure (AMI) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal Roll-out Mandates and Funding Surge | +2.80% | National, concentrated in rural and disadvantaged communities | Medium term (2-4 years) |

| Rising Grid Modernization and DER Integration Needs | +2.10% | National, with higher intensity in California, Texas, and Northeast | Long term (≥ 4 years) |

| Increasing Cybersecurity Standards for Critical Infrastructure | +1.60% | National, with stricter enforcement for investor-owned utilities | Short term (≤ 2 years) |

| Customer Demand for Near Real-Time Billing Insights | +1.20% | National, with higher adoption in urban and suburban markets | Medium term (2-4 years) |

| Shift Toward Cellular-Based AMI Backhaul | +1.40% | National, with faster adoption in areas with strong 5G coverage | Short term (≤ 2 years) |

| AI-Driven Meter Data Analytics Monetization | +1.80% | National, led by large investor-owned utilities and technology-forward cooperatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal Roll-Out Mandates and Funding Surge

Historic federal spending is changing the economics of the US AMI market by providing direct capital that lowers upfront cost risk for utilities. The Grid Resilience and Innovation Partnerships program has directed USD 5.7 billion across two rounds, with smart grid grants covering AMI, monitoring tools, and automation hardware. State and tribal formula grants have added USD 1.3 billion for resilience projects, many tagged specifically as “monitoring and control technologies.” Direct-pay tax credits under the Inflation Reduction Act allow municipal utilities and cooperatives to claim up to 30% of qualifying AMI investments, which improves project cash flow. These mechanisms shorten regulatory approval cycles and let smaller utilities bundle AMI upgrades with broader grid projects. Procurement momentum that once peaked near rate-case windows now continues year-round, giving vendors steadier order books across the US AMI market.

Rising Grid Modernization and DER Integration Needs

Distributed energy resource growth is forcing utilities to replace legacy meters that lack time-synchronized data. The Department of Energy’s Connected Communities 2.0 program awarded USD 32 million to pilot projects that rely on interval data for EV charging management and renewable coordination.[4]T&D World, “DOE Announces USD 32 Million for Grid-Edge Pilot Projects,” tdworld.com AMI datasets now feed queue-management software that accelerates clean-energy interconnections, as seen in the i2X Innovative Queue Management Solutions program. Utilities need deterministic visibility at the feeder level to run hosting-capacity studies in hours rather than months. This operational requirement turns AMI from a billing upgrade into a core grid-sensing layer for the US AMI market. States with high renewable targets are issuing guidance that any distribution upgrade plan must include metering visibility enhancements, feeding a virtuous cycle of demand.

Increasing Cybersecurity Standards for Critical Infrastructure

FERC’s 2025 order that requires NERC to craft Internal Network Security Monitoring rules pushes AMI procurement toward platforms with built-in encryption and continuous traffic analysis. Upcoming CIP-015-1 language stresses the detection of anomalous traffic inside segmented utility networks. Vendors now highlight packet-level inspection tools embedded in head-end software and endpoint clients. Utilities consider security posture a gating requirement equal to meter accuracy. Engineering firms warn that meters without secure boot or signed firmware create entry points for load oscillation attacks, which can trigger protective relays and jeopardize stability. Compliance deadlines accelerate refresh cycles, raising the baseline security bar across the US AMI market.

AI-Driven Meter Data Analytics Monetization

Analytics platforms that disaggregate appliance loads and forecast feeder headroom are generating new revenue paths for utilities. Honeywell’s integration of Innowatts analytics into its Forge platform illustrates how vendors stitch AI models into device fleets for real-time insight. Investor-owned utilities in high-growth states use AI tools to identify flexible loads and design dynamic pricing tiers. Cooperatives leverage cloud analytics to rank transformer overload risks and plan capital deferrals. These use cases translate raw meter reads into actionable intelligence, raising the ROI narrative that fuels adoption in the US AMI market. The trend also underpins an emerging service model where vendors license predictive modules alongside hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy IT/OT Interoperability Gaps | -1.80% | National, with higher impact at smaller utilities with limited IT resources | Medium term (2-4 years) |

| Persistent Consumer-Privacy Pushback | -1.20% | National, with concentrated opposition in privacy-conscious states | Long term (≥ 4 years) |

| Utility Workforce Skill Shortages for Digital Integration Applications | -1.40% | National, with acute shortages in rural and smaller utility territories | Long term (≥ 4 years) |

| Semiconductor Supply Constraints for Meter Integrated Circuits | -0.90% | Global supply chain impacts affecting all US deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy IT/OT Interoperability Gaps

Many first-generation rollouts underinvested in enterprise architecture, producing siloed systems that complicate data exchange. Utilities now face costly middleware deployments to link AMI head-ends with outage, distribution, and customer platforms. Integration of labour shortages inflates project budgets, especially for small public power entities that lack in-house talent. Cloud-native head-ends and open APIs promise relief, yet migration from on-premises environments remains a multiyear process. These technical complexities can delay procurement and slow revenue realization for vendors in the US AMI market.

Persistent Consumer Privacy Pushback

Several states are debating or enacting opt-in clauses for smart meters, reflecting public concerns about granular usage visibility. Colorado’s HB25-1175 mandates consent and obliges utilities to provide non-communicating meters on request. Privacy advocates argue that 15-minute data can disclose occupancy patterns, generating heightened scrutiny over data retention and third-party sharing. Compliance requirements raise deployment costs because utilities must maintain parallel inventory and scheduling processes. Uncertainty around forthcoming privacy statutes complicates long-term AMI value-case modelling across the US AMI market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Intelligence Surpasses Hardware Scope

Smart Metering Devices represented 46.62% of the US AMI market in 2025, underlining ongoing meter replacement programs, yet Software is set to outpace with a 13.62% CAGR to 2031. This growth pivots on analytics modules that transform interval data into revenue-generating grid services and customer-focused insights. The US AMI market size for software is forecast to narrow the revenue gap with devices before the forecast horizon ends. Utilities pair communication gateways and head-end systems with cloud dashboards that benchmark transformer loading and automate voltage set-points. As data value overtakes meter counts, vendors bundle subscription layers into contracts, creating an annuity stream that boosts margins.

Services are evolving from basic installation to outcome-based agreements, such as guaranteed read-success thresholds and analytics-driven energy savings. Managed services appeal to utilities that cannot staff new data science teams. In the US AMI market, suppliers now propose turnkey models where they own backend infrastructure and deliver meter data through secure APIs. This reduces customer capex and speeds adoption while enlarging vendors’ total contract value.

By End-User: Residential Dominance, Industrial Acceleration

Residential connections made up 88.35% of 2025 revenue, reflecting household volume and federal equity priorities. Large utilities tie AMI rollouts to rate structures that reward conservation, reinforcing residential penetration. Industrial accounts, however, are posting the highest 12.92% CAGR through 2031 as factories electrify processes and integrate renewables. The US AMI market share for industrial users is still modest, yet high growth stems from granular metering needed for demand charges, power-quality monitoring, and wholesale participation.

Many industrial sites operate as prosumers with behind-the-meter solar, storage, or microgrids. They rely on time-synchronized data for settlement and reliability assurances. Some plants require redundant communications paths and cybersecurity certifications because outages translate directly to production losses. Vendors with hardened meters and real-time analytics capture this opportunity, raising the visibility of the industrial segment inside the US AMI market.

By Communication Technology: Cellular Growth Challenges Mesh Supremacy

RF Mesh held 51.94% of 2025 revenue thanks to proven resilience and utility control. Yet Cellular connectivity, propelled by nationwide 5G coverage, is registering the fastest 13.78% CAGR. Utilities like SECO Energy have chosen 5G-ready meters that accept over-the-air firmware updates without truck rolls. The US AMI market size for cellular is expanding as utilities favour carrier-managed backhaul, which lowers network operating complexity.

Private LTE pilots offer dedicated spectrum while leveraging telecom security controls. Mesh technology remains viable for dense urban circuits where hop-by-hop redundancy offsets bandwidth limits. Hybrid architectures combining mesh for local aggregation and cellular for backhaul are common in rural cooperatives. Choices now center on lifecycle cost, latency tolerance, and cybersecurity features rather than signal reach alone, broadening competitive channels across the US AMI market.

By Utility Ownership Type: Cooperatives Lead Pace of Change

Investor-Owned Utilities held 64.12% of 2025 revenue, reflecting expansive customer bases and stable capital flows. Yet, Electric Cooperatives are expanding at a 14.31% CAGR as federal programs earmark grants for rural infrastructure. The US AMI market size allocated to cooperatives grows faster because joint-action groups negotiate bulk hardware pricing and shared analytics hosting. Cooperative case studies, such as Southwestern Electric Cooperative’s Revelo deployment, illustrate how small utilities leapfrog to advanced grid sensing without shouldering full integration risk.

Municipal utilities leverage direct-pay tax incentives to close funding gaps. They often adopt subscription models that spread costs over service life, reducing rate shock. Public power entities benefit from community alignment, which lowers consumer pushback. Diversity in ownership models stimulates varied procurement strategies, widening addressable channels for vendors across the US AMI market.

Geography Analysis

California, Texas, and New York remained the largest state contributors in 2024, reflecting sizable customer bases and aggressive renewable mandates that require granular metering data for hosting-capacity studies. The US AMI market benefits from state programs that channel grants toward disadvantaged neighbourhoods in Los Angeles, Houston, and Buffalo, accelerating meter swap-outs. Western states secured significant allocations under federal resilience grants, sending funds to tribal utilities in Alaska and Arizona for voltage monitoring upgrades.

The Northeast shows accelerating uptake as aging infrastructure meets rising electrification. Utilities in Massachusetts and Maine bundle AMI with load-management pilots to support winter heat-pump adoption. Midwest cooperatives leverage Grain Belt Express interconnection planning to justify AMI analytics that inform power-flow modelling. Southern states, historically slower adopters, now pursue AMI to comply with FERC cybersecurity deadlines and to prepare distribution systems for EV corridor charging.

Privacy legislation creates regional complexity. Colorado’s opt-in rule forces utilities to manage dual meter inventories, while Texas operates under a competitive retail market that demands interval data for supplier billing. These contrasts shape vendor sales cycles and product features. Workforce constraints vary: coastal regions lure data scientists, whereas rural Plains utilities rely on managed-service contracts. Despite these differences, all regions converge on the need for secure, analytics-ready platforms, sustaining unified momentum inside the US AMI market.

Competitive Landscape

The US AMI market features moderate concentration, with a handful of vendors offering integrated suites. Itron, Landis+Gyr, and Honeywell stand out for full-stack solutions that blend devices, communications, and analytics. Each is layering AI modules into edge devices to detect voltage anomalies in real time, positioning analytics as a differentiator. Honeywell’s 5G alliance with Verizon showcases how meter suppliers tap telecom expertise for connectivity scale.

Acquisitions broaden portfolios. Badger Meter bought SmartCover Systems for USD 185 million to add sewer-line monitoring, signalling a push into adjacent infrastructure. ConnectM’s purchase of MHz Invensys deepened RF mesh capabilities for large-scale deployments. Partnerships are equally strategic; Itron’s collaboration with Schneider Electric and Microsoft bundles distributed intelligence with digital-grid software and cloud AI, aiming to raise grid capacity without new conductors.

Regulatory compliance is now a sales qualifier. Vendors advertise NERC-aligned encryption, role-based access, and signed firmware. Utilities prioritize suppliers able to deploy workforce training and managed SOC services that offset internal staffing gaps. Open-standard commitments, such as support for IEEE 2030.5, influence RFP scores. Competitive emphasis on cybersecurity, analytics depth, and service flexibility drives ongoing differentiation inside the US AMI market.

United States Advanced Metering Infrastructure (AMI) Industry Leaders

Itron Inc.

IBM Corporation

Cisco Systems Inc.

Mueller Systems LLC

Oncor Electric Delivery Company LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Honeywell partnered with Verizon to embed 5G connectivity in smart meters, enabling remote firmware updates and fleet management through ThingSpace.

- March 2025: Itron expanded Grid Edge Intelligence collaboration with Schneider Electric and Microsoft to deliver AI-driven capacity increases up to 20%.

- March 2025: Ameresco signed a USD 9 million AMI contract with the City of Hurst, Texas, covering water meters and customer portals.

- February 2025: SECO Energy became the first cooperative to deploy Honeywell Forge Performance+ with SparkMeter analytics.

United States Advanced Metering Infrastructure (AMI) Market Report Scope

Advanced Metering Infrastructure (AMI) facilitates two-way communication and gives system operators an IT-enabled interface with consumers in both the residential and commercial sectors. Another key driver for adopting AMI and smart grid technology is reducing energy theft. The residential, commercial, and industrial sectors use AMI's various products and services, including smart meters, meter communication infrastructure, and data management.

The scope of the report covers various segments that are segmented by type (smart metering devices, solutions, services), and end-user (residential, commercial, industrial). The study also indicates the impact of COVID-19 on the United States' AMI market.

By Component

| Smart Metering Devices (Electricity - Water - Gas) | ||

| Solutions | Meter Communication Infrastructure | |

| Software | Meter Data Management | |

| Meter Data Analytics | ||

| Services | ||

By End-User

| Residential |

| Commercial |

| Industrial |

By Communication Technology

| RF Mesh |

| Power Line Carrier (PLC) |

| Cellular |

| Wi-Fi and Other Communication Technologies |

By Utility Ownership Type

| Investor-Owned Utilities |

| Public Power Utilities |

| Electric Cooperatives |

| By Component | Smart Metering Devices (Electricity - Water - Gas) | ||

| Solutions | Meter Communication Infrastructure | ||

| Software | Meter Data Management | ||

| Meter Data Analytics | |||

| Services | |||

| By End-User | Residential | ||

| Commercial | |||

| Industrial | |||

| By Communication Technology | RF Mesh | ||

| Power Line Carrier (PLC) | |||

| Cellular | |||

| Wi-Fi and Other Communication Technologies | |||

| By Utility Ownership Type | Investor-Owned Utilities | ||

| Public Power Utilities | |||

| Electric Cooperatives | |||

Key Questions Answered in the Report

What is the projected value of the US AMI market in 2031?

The market is expected to reach USD 41.84 billion by 2031.

Which component is growing fastest within the US AMI market?

Software, led by meter data analytics, is expanding at a 13.62% CAGR through 2031.

Which communication technology is gaining share most rapidly?

Cellular connectivity is growing at a 13.78% CAGR thanks to nationwide 5G coverage.

How fast are electric cooperatives increasing AMI spending?

Cooperative investment is advancing at a 14.31% CAGR, the highest among ownership types.

Why are utilities prioritizing cybersecurity in AMI procurements?

FERC mandates for internal network security monitoring require secure, standards-compliant platforms.

What federal program provides direct capital for utility AMI projects?

The Grid Resilience and Innovation Partnerships program allocates billions for smart grid upgrades.

Page last updated on: