Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

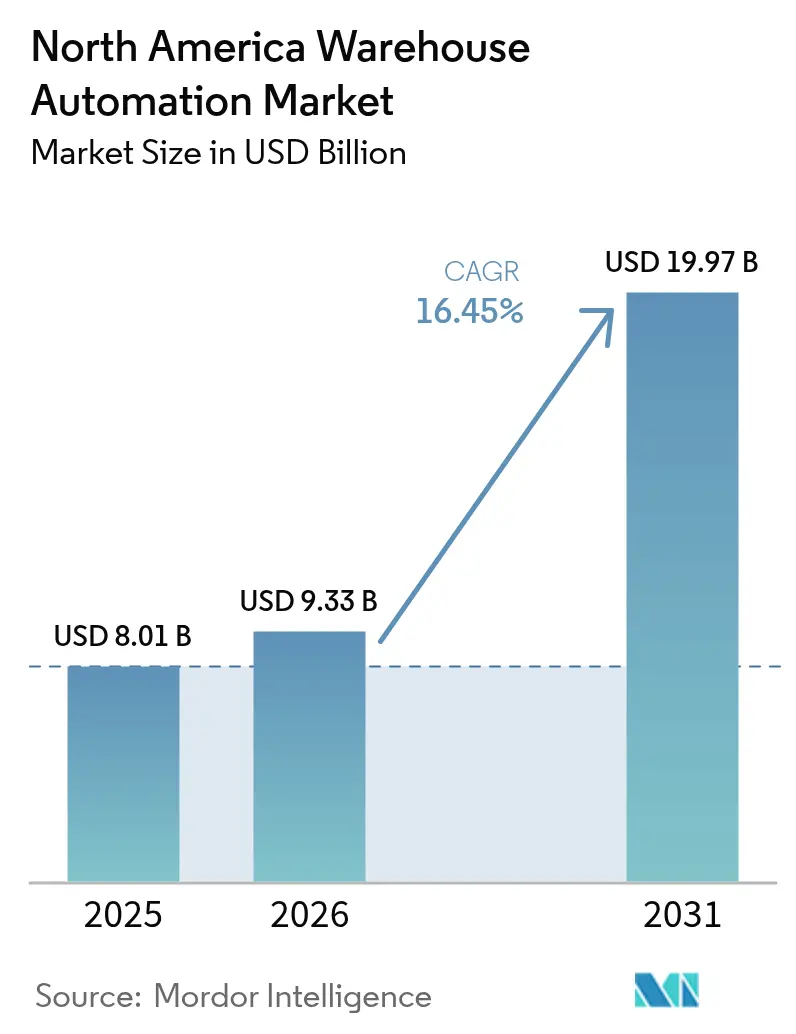

| Base Year Market Size (2025) | USD 8.01 Billion |

| Market Size (2026) | USD 9.33 Billion |

| Market Size (2031) | USD 19.97 Billion |

| Growth Rate (2026 - 2031) | 16.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Warehouse Automation Market Analysis by Mordor Intelligence

The North America warehouse automation market size is expected to grow from USD 8.01 billion in 2025 to USD 9.33 billion in 2026 and is forecast to reach USD 19.97 billion by 2031 at 16.45% CAGR over 2026-2031. Ongoing tariff pressures, persistent labor shortages, and rapid growth in e-commerce orders continue to accelerate capital spending on robotics, automated storage, and AI-driven orchestration platforms across the region. Hardware still dominates budgets, yet the highest incremental value now flows from cloud-native execution software that reallocates robots, conveyors, and human labor in real time. U.S. policy incentives, notably Section 45X production credits, are shortening domestic lead times for automation hardware and tilting sourcing toward North American suppliers. Retailers and 3PLs are embracing autonomous mobile robots (AMRs) because modular fleets can be deployed in weeks rather than months, a critical advantage in facilities where SKU counts and order profiles change daily. The interplay of nearshoring, wage inflation exceeding 4% in warehousing roles, and stricter traceability mandates in the food and pharmaceutical industries makes integrated automation an operational necessity rather than a discretionary upgrade.

Key Report Takeaways

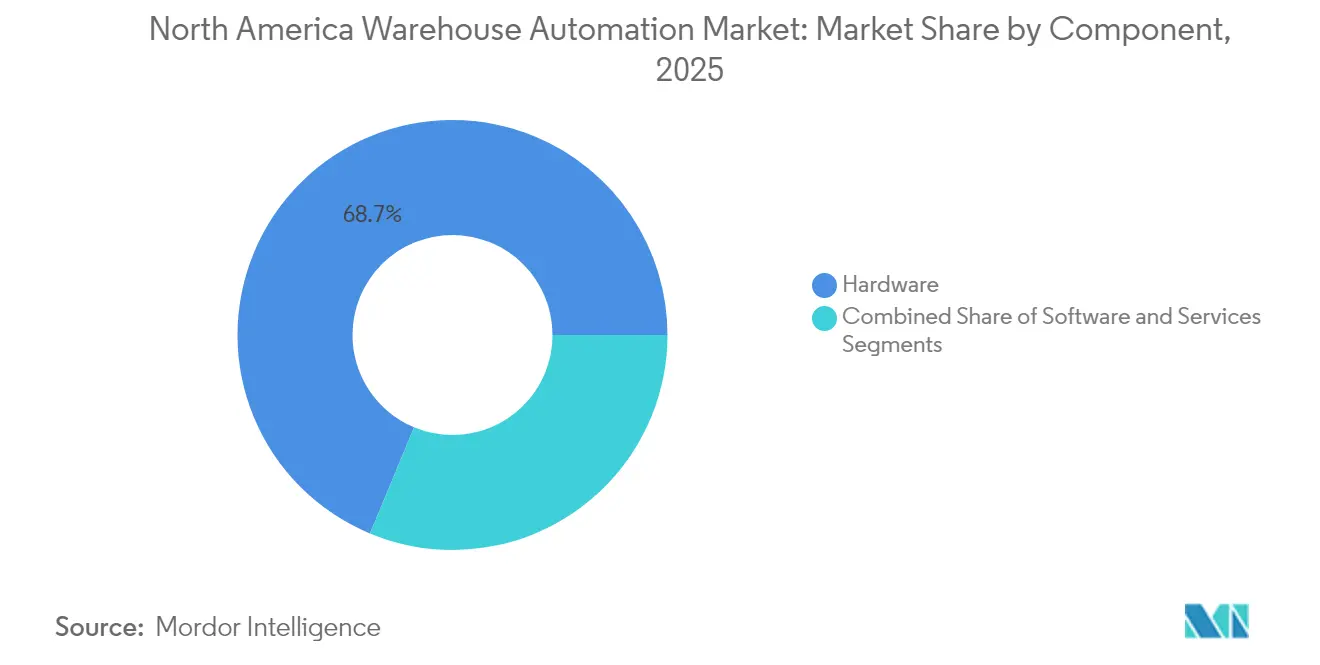

- By component, hardware led with a 68.73% share of the North America warehouse automation market in 2025, while software is advancing at a 16.85% CAGR through 2031.

- By technology, autonomous mobile robots and AGVs are expanding at a 17.35% CAGR to 2031, whereas automated storage and retrieval systems held a 33.15% share of the North America warehouse automation market size in 2025.

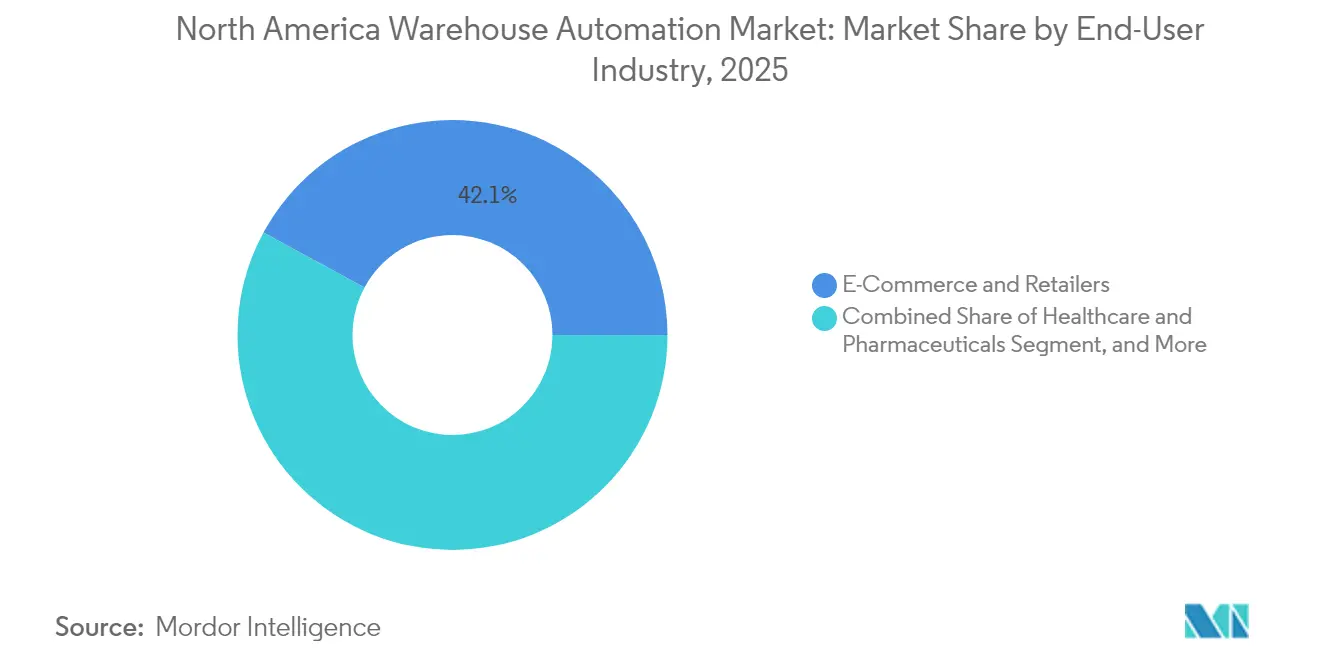

- By end-user, e-commerce and retailers accounted for 42.10% share of the North America warehouse automation market in 2025, but healthcare and pharmaceuticals are forecast to rise at a 17.40% CAGR.

- By function, storage commanded a 38.95% share of the North America warehouse automation market size in 2025, and order-picking automation is projected to track a 17.25% CAGR to 2031.

- By geography, the United States captured 75.10% share of the North America warehouse automation market in 2025, whereas Mexico is poised for the fastest 16.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Warehouse Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in E-Commerce Fulfillment Automation | +3.2% | United States and Canada, spillover to Mexico | Short term (≤ 2 years) |

| Rising Labor Shortages and Wage Inflation | +2.8% | United States and Canada | Medium term (2-4 years) |

| US Inflation Reduction Act Domestic Credits | +1.9% | United States | Medium term (2-4 years) |

| Integration of AI-Driven Orchestration | +2.4% | United States and Canada | Long term (≥ 4 years) |

| Demand for Cold-Chain Compliance Automation | +1.6% | United States and Canada | Medium term (2-4 years) |

| 2025 Tariff-Led Nearshoring of Supply Chains | +2.1% | United States and Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in E-Commerce Fulfillment Automation

Retailers are compressing order-to-ship cycles to hours, pushing capital toward high-speed sortation, goods-to-person picking, and robotic palletizing. Walmart allocated USD 200 million to autonomous forklifts in 2024, evidencing confidence that robotics offset margin pressure from online orders that carry 400-600 basis-point lower gross margins than stores.[1]Walmart, “Walmart to Add Autonomous Forklifts to Distribution Centers,” walmart.com Amazon’s Shreveport and Detroit fulfillment centers each deployed more than 1,000 AMRs to triple peak throughput during holiday surges. Third-party logistics operators serving multiple storefronts on Shopify are embracing modular automation so they can amortize costs across clients and redeploy robots as contract volumes shift. Real-estate premiums in urban cores are steering inventory toward larger regional hubs where dense, software-defined automation scales without expanding footprints. As same-day delivery becomes table stakes, the North America warehouse automation market embeds fulfillment speed as an existential competitive variable.

Rising Labor Shortages and Wage Inflation in Warehousing

Warehouse pay grew 4.1% year-over-year in Q3 2024, while vacancy rates in rural hubs remain acute, forcing operators to pay shift differentials for overnight coverage.[2]Bureau of Labor Statistics, “Employment Cost Index News Release,” bls.gov Shortfalls in certified robotics technicians further elevate compensation costs or push operators into vendor-locked service contracts. Vendors now embed predictive maintenance into control software to cut unplanned downtime and remote diagnostics that let a single engineer cover multiple sites. When wage growth exceeds 3% annually, autonomous mobile robots show sub-24-month paybacks in high-volume facilities, strengthening the structural ties between labor economics and automation capital plans. Consequently, AMR vendors that package hardware with fleet-optimization software are well positioned inside the North America warehouse automation market.

US Inflation Reduction Act Incentives for Domestic Automation Hardware

Section 45X production tax credits reward U.S. manufacturing of battery modules, inverters, and motion-control components integral to AMRs and high-density shuttle systems.[3]Internal Revenue Service, “Advanced Manufacturing Production Credit,” irs.gov Vendors localizing production cut freight costs and eliminate tariff risk, shrinking lead times that stretched to 18 months during the 2021-2023 semiconductor crunch. The credit also applies to stationary energy-storage systems that power microgrids in mega-warehouses, creating an additional savings layer for operators that can now arbitrage utility demand charges. Coupled with nearshoring trends, these subsidies underpin a virtuous cycle: domestic factories supply automation hardware, installers trim project timelines, and buyers lock in resilient, on-shore supply chains to hedge geopolitical shocks.

Integration of AI-Driven Warehouse Orchestration Platforms

Execution systems are shifting from static task queues to cloud-native engines that ingest orders, labor rosters, robot availability, and carrier cut-off times in real time, then issue optimized work instructions every few seconds. Open APIs break the vendor lock-in that long-hampered legacy warehouse control software, permitting AMRs from one supplier to cooperate with picking arms from another. Operators piloting AI orchestration platforms report 15-25% labor-productivity lifts and 10-15% lower inventory buffers as algorithms re-order tasks to minimize dwell time. Security frameworks, notably NIST Cybersecurity Framework 2.0, now guide software procurement, embedding zero-trust principles that reduce ransomware risk inside connected distribution centers. As predictive insights accumulate, orchestration data doubles as a digital twin that stress-tests future layouts before managers commit fresh capital.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure for SMEs | -1.8% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Integration Complexity with Legacy Systems | -1.4% | United States and Canada | Medium term (2-4 years) |

| Shortage of Skilled Robotics Technicians | -1.1% | United States and Canada | Medium term (2-4 years) |

| Cybersecurity Risks to Connected Controls | -0.9% | United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure for SMEs

Automated storage and retrieval systems can demand USD 5-20 million per site, a misalignment for third-party logistics contracts that often renew every three years. Robotics-as-a-service models convert equipment purchases into operating costs by charging per pick or pallet move, but they also shift utilization risk to the vendor. Lacking standardized performance benchmarks, smaller operators struggle to compare proposals, elongating sales cycles. This disparity concentrates automation adoption among big-box retailers and multi-site 3PLs that can amortize engineering and integration across distributed networks. Consequently, the North America warehouse automation market still shows under-penetration among mid-market operators despite falling hardware prices.

Integration Complexity with Legacy WMS and ERP Systems

Software deployed before 2015 rarely offers APIs or data schemas required for AMRs or vision-guided picking. Middleware projects add 20-30% to project costs and can stretch timelines by up to a year, deterring brown-field automation. Proprietary protocols hamper cross-vendor communication, forcing integrators to build custom translators that complicate maintenance. ISA/IEC 62443 standards outline secure platform integration, yet adoption lags among operators without dedicated cyber staff. For many small facilities, incremental upgrades beat wholesale rip-and-replace strategies, delaying full automation rollouts in the North America warehouse automation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Secures Growing Strategic Weight

Hardware retained 68.73% share in 2025, underscoring the capital intensity of conveyors and ASRS that anchor automated facilities across the North America warehouse automation market. Software is tracking a 16.85% CAGR because orchestration, labor planning, and inventory optimization are now the fastest levers to raise throughput without heavy construction. As subscription models replace perpetual licenses, operators can roll out feature enhancements over-the-air, decoupling capability from physical refresh cycles.

Expanding fleets of AMRs embed their own fleet-management layers that dynamically reassign robots to zones with rising order depth, cutting idle time and squeezing higher asset utilization. Digital-twin models simulate rack redeployments or aisle-width tweaks before crews step on the floor, slashing project risk. Service revenues installation, maintenance, managed operations are pivoting toward outcome-based contracts where integrators guarantee lines per hour rather than equipment uptime, aligning vendor incentives with the operator’s service-level goals.

By Technology: Mobile Robotics Outrun Fixed Infrastructure

Automated storage and retrieval systems delivered 33.15% revenue in 2025, prized for vertical density in parts and beverage distribution. Meanwhile, AMRs and AGVs are advancing at 17.35% annually as operators prioritize flexibility that lets fleets scale in increments of tens rather than hundreds. Conveyor and sortation assets remain indispensable for parcel hubs handling predictable volumes, but retrofits frequently embed diverters that interact with AMRs for last-meter routing.

AutoStore’s cube-based storage underscores a hybrid trend: dense static grids coupled with mobile robots on top to liberate bin content quickly. Locus Robotics surpassed 10,000 collaborative units across North America in 2024, validating the pay-per-pick model in high-mix e-commerce. Operators increasingly deploy hybrid estates where ASRS stores A-class inventory and AMRs ferry B- and C-class SKUs to ergonomic workstations, ensuring resilience when demand profiles shift.

By End-User Industry: Compliance Sets Healthcare’s Pace

E-commerce and retailers owned 42.10% of demand in 2025 thanks to perpetual peak seasons and free-shipping expectations. Healthcare and pharmaceuticals will swell at a 17.40% CAGR as FDA FSMA Section 204 and Drug Supply Chain Security Act deadlines force serialized, temperature-controlled handling for every pallet and case. Third-party logistics specialists absorb capital costs for multiple biotech clients, turning compliance expertise into a service moat.

Food and beverage operators automate blast freezers and refrigerated pick modules to maintain temperature integrity that regulators test with growing rigor. Automotive distributors favor shuttle systems for just-in-sequence part feeds, whereas electronics players invest in anti-static handling and camera-based verification to keep counterfeit risk near zero. Each vertical maps core constraints temperature, serialization, velocity to its automation stack, reinforcing the segmentation complexity of the North America warehouse automation market.

By Function: Order-Picking Automation Accelerates

Storage solutions held 38.95% in 2025, yet order picking is expanding 17.25% per year as SKU proliferation pushes labor variance upward. Goods-to-person systems double pick rates by eliminating travel, while vision-guided arms now handle deformable packaging once thought automation-proof. Collaborative robots trail human pickers, carrying totes and reducing ergonomic strain, a benefit that lowers injury costs and attrition.

High-speed cross-belt and tilt-tray sorters remain staple investments for parcel hubs shipping tens of thousands of units per hour, although their fixed footprints limit relevance for smaller buildings. Cartonization software nests inside packing stations, minimizing dim-weight penalties and cutting corrugate waste. Palletizing robots equipped with AI vision depalletize mixed inbound loads without expensive mechanical tooling, rounding out a balanced automation roadmap.

Geography Analysis

The United States captured 75.10% of 2025 revenue, propelled by dense e-commerce grids in California, New Jersey, and Illinois. Section 45X credits tilt capital toward domestically manufactured shuttles, lifts, and battery modules, compressing lead times by weeks and mitigating tariff exposure. Hourly warehouse wages in Los Angeles and New York passed USD 20 in 2024, locking in sub-two-year paybacks for AMR deployments. Cold-chain mandates for biologics and fresh produce require redundant chillers and automated temperature monitoring that integrate directly with warehouse execution software, driving premium system configurations. NIST Cybersecurity Framework 2.0 adoption is extending project timelines but bolstering insurance underwriting and board-level confidence.

Mexico is on a 16.80% CAGR trajectory to 2031 as multinationals cluster assembly and distribution near U.S. consumption to defuse 2025 tariff volatility. Automotive and electronics supply chains form an automation beachhead in Monterrey and Juárez, where AMRs navigate high-mix kitting zones. Rising wages in border plants narrow the cost gap while heightened U.S. delivery-time expectations raise service-level requirements. Vendors counter Mexico’s limited technician pool by delivering remote diagnostics and dispatching roving service teams from Texas hubs, bridging skill shortages without stalling adoption.

Canada’s automation demand clusters around Toronto and Vancouver cold-chain corridors to meet Health Canada Good Distribution Practice and Canadian Food Inspection Agency rules. Lower average labor costs temper urgency, yet a scarcity of overnight workers in refrigerated dock doors accelerates AMR pilots. Cross-border 3PLs handling U.S.-destined e-commerce invest in sortation and label automation to tame customs complexity. Concentrated population centers enable operators to scale automation in fewer mega-facilities, achieving favourable economies of scale despite a smaller national footprint within the North America warehouse automation market.

Competitive Landscape

The North America warehouse automation market shows moderate concentration: legacy integrators Dematic, Daifuku, and Honeywell Intelligrated hold sizable installed bases, yet face insurgent pressure from software-centric AMR providers. Established vendors now acquire or partner with robotics specialists KION Group’s Dematic aligns with AMR producers to deliver end-to-end portfolios that blend fixed infrastructure and mobile flexibility. Contract models shift toward performance guarantees, converting equipment sales into multi-year throughput commitments that re-shape revenue recognition.

Mid-market 3PLs, historically underserved, emerge as a strategic battleground. Robotics-as-a-service offerings from Locus Robotics, Geekplus, and Bastian Solutions reduce capital hurdles, expanding addressable demand. Intellectual-property battles intensify: Zebra Technologies’ Fetch Robotics purchase underscores the premium on autonomous navigation patents. Cloud-native orchestration platforms create defensible ecosystems by unifying disparate robot fleets, sparking coopetition between integrators vying to become the de-facto control layer.

Digital twins differentiate proposals by proving ROI before bolt-tightening begins. Vendors host customer experience centers where operators trial layouts in real time, shrinking sales cycles. Cybersecurity and data-sovereignty compliance add pre-sales workload but reward suppliers that bake zero-trust into firmware. As fleets scale, aftermarket parts, predictive-maintenance analytics, and remote support mature into high-margin annuities, reinforcing stickiness even when hardware commoditizes.

North America Warehouse Automation Industry Leaders

Daifuku Co., Ltd.

SSI Schaefer AG

Dematic Corp.

Swisslog Holding AG

AutoStore Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Geekplus and DHL roll out a robotics-as-a-service program across five Mexican border warehouses, deploying 1,500 AMRs to streamline cross-border e-commerce fulfillment under the USMCA framework.

- August 2025: AutoStore breaks ground on a USD 120 million cube-storage manufacturing plant in Tennessee, targeting 10-week delivery cycles for U.S. customers and creating 300 advanced-manufacturing jobs.

- April 2025: Locus Robotics debuts its LX4 collaborative mobile robot with a 25% payload boost and fast-swap lithium-iron-phosphate batteries, securing first deployments at two Target distribution centers in Illinois.

- February 2025: Honeywell Intelligrated opens a robotics research lab in Pittsburgh, adding 200 engineers to accelerate AI-driven warehouse execution software and next-generation AMR fleets across North America.

North America Warehouse Automation Market Report Scope

The North America Warehouse Automation Market Report is Segmented by Component (Hardware, Software, Services), Technology (Automated Storage and Retrieval Systems, Autonomous Mobile Robots and AGVs, Conveyor and Sortation Systems, Picking and Packing Automation, Warehouse Management and Execution Software), End-User Industry (E-Commerce and Retailers, Third-Party Logistics, Food and Beverage, Automotive, Healthcare and Pharmaceuticals, Electronics and Electrical), Function (Storage, Order Picking, Packing and Dispatch, Palletizing and Depalletizing, Sortation), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Component

| Hardware |

| Software |

| Services |

By Technology

| Automated Storage and Retrieval Systems |

| Autonomous Mobile Robots and AGVs |

| Conveyor and Sortation Systems |

| Picking and Packing Automation |

| Warehouse Management and Execution Software |

By End-User Industry

| E-Commerce and Retailers |

| Third-Party Logistics |

| Food and Beverage |

| Automotive |

| Healthcare and Pharmaceuticals |

| Electronics and Electrical |

By Function

| Storage |

| Order Picking |

| Packing and Dispatch |

| Palletizing and Depalletizing |

| Sortation |

By Country

| United States |

| Canada |

| Mexico |

| By Component | Hardware |

| Software | |

| Services | |

| By Technology | Automated Storage and Retrieval Systems |

| Autonomous Mobile Robots and AGVs | |

| Conveyor and Sortation Systems | |

| Picking and Packing Automation | |

| Warehouse Management and Execution Software | |

| By End-User Industry | E-Commerce and Retailers |

| Third-Party Logistics | |

| Food and Beverage | |

| Automotive | |

| Healthcare and Pharmaceuticals | |

| Electronics and Electrical | |

| By Function | Storage |

| Order Picking | |

| Packing and Dispatch | |

| Palletizing and Depalletizing | |

| Sortation | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected value of the North America warehouse automation market in 2031?

The North America warehouse automation market is forecast to reach USD 19.97 billion by 2031.

Which component is growing fastest within regional automation spending?

Software is expanding at a 16.85% CAGR as AI orchestration and cloud-native execution platforms become critical productivity levers.

Why are autonomous mobile robots gaining traction over fixed systems?

AMRs scale in small increments, deploy in weeks, and adapt to shifting SKU and order profiles, delivering sub-24-month paybacks in high-velocity facilities.

How do U.S. policy incentives influence warehouse automation sourcing?

Section 45X production credits encourage domestic manufacturing of batteries and motion components, reducing lead times and tariff exposure for U.S. operators.

Which end-user vertical will grow fastest through 2031?

Healthcare and pharmaceuticals, driven by stringent FDA traceability and serialization mandates, are projected to rise at a 17.40% CAGR.

What key risk slows automation adoption among small 3PLs?

High upfront capital costs, often USD 5-20 million per facility, deter smaller operators that operate on short contract cycles.

Page last updated on: