Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

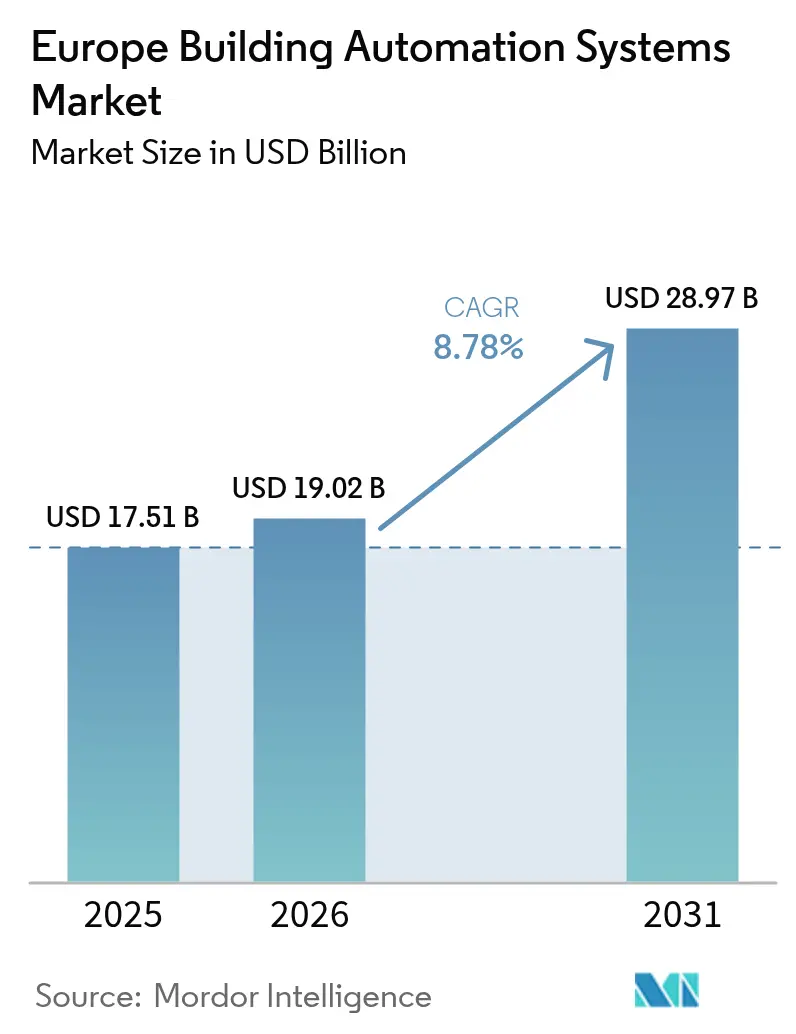

| Base Year Market Size (2025) | USD 17.51 Billion |

| Market Size (2026) | USD 19.02 Billion |

| Market Size (2031) | USD 28.97 Billion |

| Growth Rate (2026 - 2031) | 8.78% CAGR |

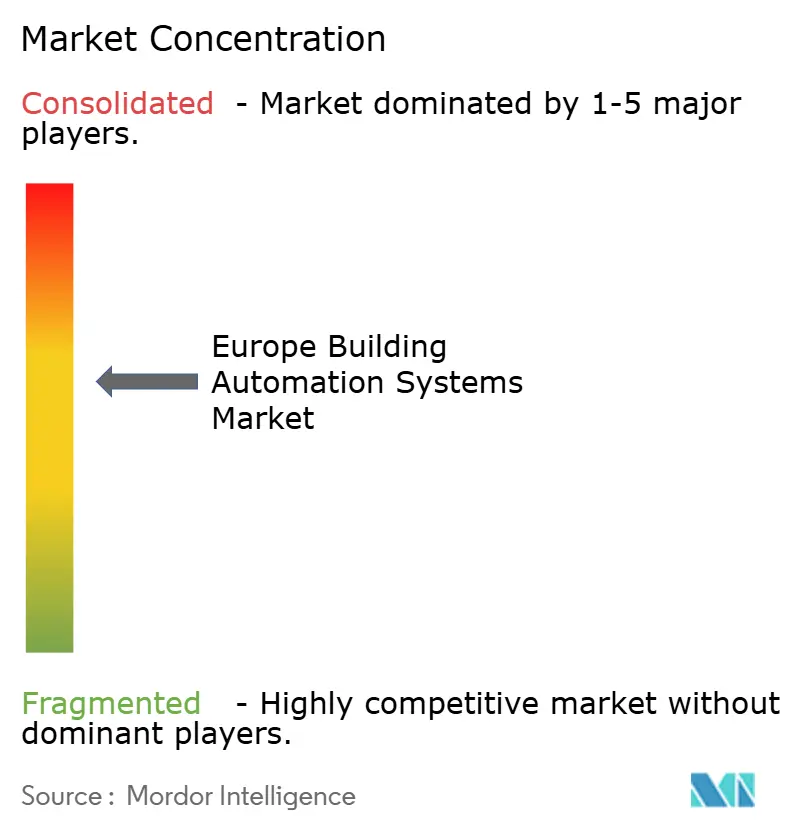

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Building Automation Systems Market Analysis by Mordor Intelligence

The Europe building automation system market size is projected to be USD 17.51 billion in 2025, USD 19.02 billion in 2026, and reach USD 28.97 billion by 2031, growing at a CAGR of 8.78% from 2026 to 2031. Surging retrofit activity, which already captures more than half of all European installations, is intensifying as mandatory Smart Readiness Indicator labels take effect in 2026, obliging owners to digitize legacy HVAC and lighting assets. Financial incentives amplify the pull; green-finance-linked loans now tie interest margins to verified real-time energy performance, turning automation from a discretionary upgrade into a compliance prerequisite for landlords pursuing favorable debt. Vendor strategies are also shifting, with manufacturers packaging recurring analytics subscriptions alongside controllers to smooth revenue volatility as hardware margins tighten. Secondary markets in Central and Eastern Europe, led by Poland, are expanding faster than Western incumbents because EU cohesion funds lower retrofit capital costs, creating a geographic rebalancing that incumbents can only offset by accelerating open-protocol-based offerings.

Key Report Takeaways

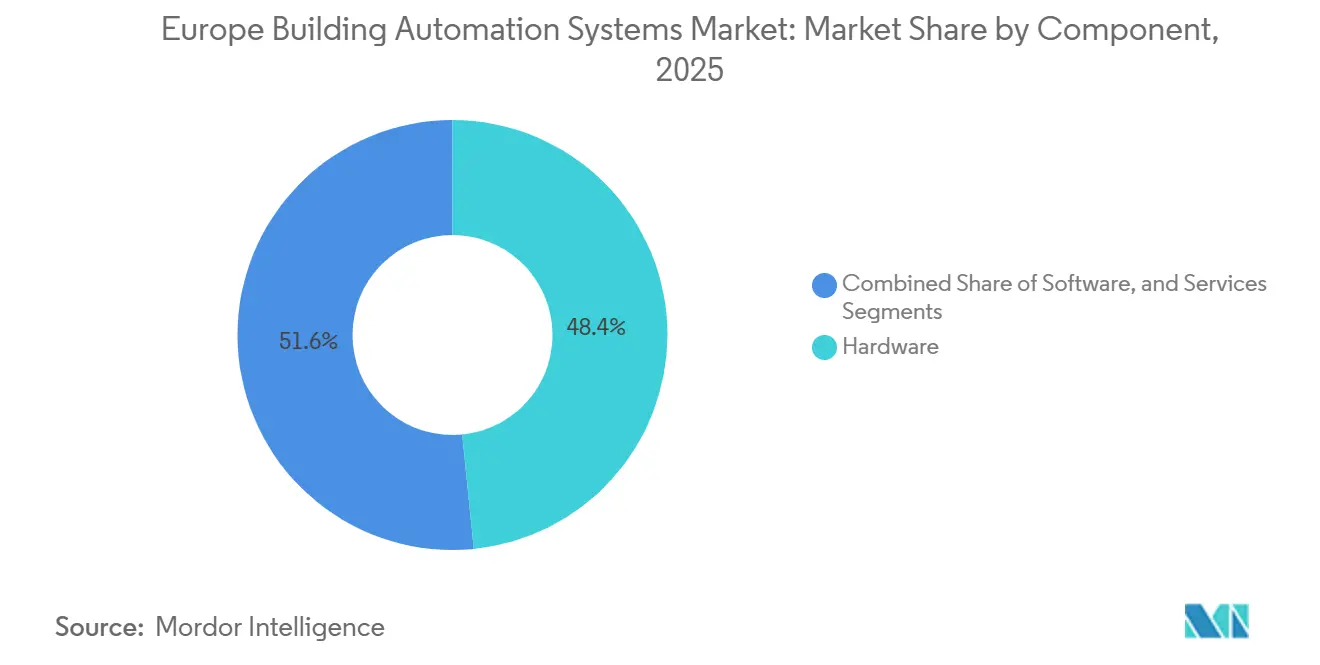

- By component, hardware led with 48.43% of Europe building automation system market share in 2025, while the services segment is projected to expand at a 9.37% CAGR to 2031.

- By system type, HVAC controls accounted for 40.51% of the Europe building automation system market size in 2025, whereas security and access control systems are advancing at a 9.53% CAGR through 2031.

- By communication technology, wired solutions accounted for 64.67% of revenue in 2025, but wireless platforms are forecast to grow at a 9.61% CAGR through 2031.

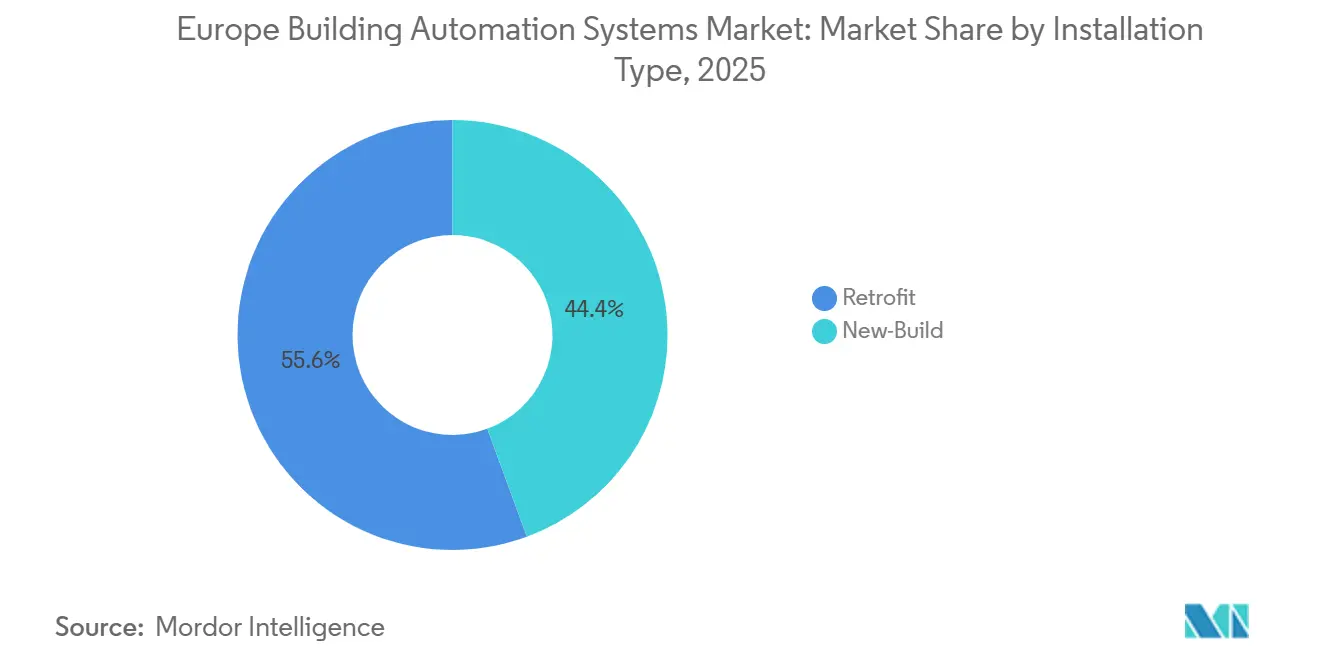

- By installation type, retrofits accounted for 55.63% of revenue in 2025 and are projected to grow at a 9.11% CAGR through 2031.

- By end user, commercial buildings accounted for 46.83% of revenue in 2025, while institutional and government facilities are on track for the fastest growth at a 9.46% CAGR to 2031.

- By country, Germany retained 37.33% of revenue in 2025, whereas Poland is set to grow at a market-leading 9.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Building Automation Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU Energy-Efficiency Directives and NZEB Mandates | +1.8% | EU-wide, earliest in Germany, France, Netherlands | Medium term (2-4 years) |

| Rising Demand for Smart Energy Management in Commercial Buildings | +1.5% | Germany, United Kingdom, France, Benelux; spillover to Poland, Spain | Short term (≤ 2 years) |

| Increasing Adoption of IoT and AI-Enabled BAS Platforms | +1.4% | Germany, Nordics, United Kingdom; expanding to Central Europe | Medium term (2-4 years) |

| Rapid Retrofits of Aging Building Stock | +1.6% | Western Europe; accelerating in Poland | Short term (≤ 2 years) |

| Mandatory Smart Readiness Indicator Labeling From 2026 | +1.3% | EU-wide, priority in commercial and institutional assets | Short term (≤ 2 years) |

| Surge in Green-Finance-Linked Loans Requiring Real-Time Reporting | +1.2% | Germany, France, United Kingdom, Netherlands, Belgium | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EU Energy-Efficiency Directives and NZEB Mandates

The 2024 recast of the Energy Performance of Buildings Directive compels all new structures to reach nearly zero-energy status by 2030 and requires building automation for HVAC systems above 290 kW. Member-state translations that reference EN 15232 move developers away from standalone thermostats toward networked supervisory software, embedding open APIs for 15-minute data logging that aligns with ISO 52120-1. Germany’s Gebäudeenergiegesetz and France’s RE2020 already integrate these benchmarks, making compliance‐driven BAS rollouts an unavoidable cost of construction.[1]European Commission, “Energy Performance of Buildings Directive,” energy.ec.europa.eu

Rising Demand for Smart Energy Management in Commercial Buildings

Hybrid work has left office utilization unpredictable, so landlords deploy AI-based HVAC scheduling that maps calendar bookings to occupancy sensors, cutting energy waste in case studies by up to 30%. The EU Taxonomy restricts green-bond eligibility to assets in the top 15% efficiency tier, encouraging sub-metering and model predictive control to maintain certification and protect access to cheaper capital.[2]European Commission, “EU Taxonomy for Sustainable Activities,” ec.europa.eu

Increasing Adoption of IoT and AI-Enabled BAS Platforms

Edge gateways now perform local machine-learning inference for leak detection or motor-wear monitoring, which trims emergency repair costs and reassures operators wary of exporting sensitive data off-site under GDPR. Platforms such as Johnson Controls OpenBlue or Siemens Desigo CC package pre-trained algorithms, sparing facility teams from custom data science projects and accelerating value realization.

Rapid Retrofits of Aging Building Stock

Roughly three-quarters of European buildings pre-date 1990, so energy penalties from constant-volume HVAC remain high. Wireless sensor meshes cut labor up to 50% versus cabled alternatives, which is pivotal for Poland, where cohesion funds reimburse upgrades only when EN 15232 Class B performance is achieved. Italy’s reduced-rate Superbonus extension similarly front-loaded demand before tapering incentives moderate growth after 2026.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Installation and Integration Costs | -1.1% | EU-wide, acute in Spain, Italy, Poland, Romania | Short term (≤ 2 years) |

| Cybersecurity and Data-Privacy Concerns | -0.9% | Germany, France, Netherlands, Belgium | Medium term (2-4 years) |

| Semiconductor Lead-Time and Tariff-Driven Cost Volatility | -0.7% | Germany, France, Italy manufacturing hubs | Short term (≤ 2 years) |

| Shortage of Skilled BAS Technicians in Secondary Cities | -0.6% | Central and Eastern Europe, Southern Europe secondary cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Installation and Integration Costs

Typical mid-rise commercial retrofits require USD 15-25 per m² for equipment and commissioning, which competes with tenant-improvement budgets and creates split-incentive hurdles under gross leases. Legacy pneumatic or proprietary DDC networks demand additional gateways and custom code, inflating engineering fees despite European Investment Bank support programs that mostly reach well-staffed municipalities.[3]

Cybersecurity and Data-Privacy Concerns

NIS2 reclassifies BAS as essential services, mandating incident reporting, network segmentation, and encrypted firmware updates. Facilities built before IEC 62443 standards often lack hardware headroom for cryptography, pushing owners toward partial or full controller replacement while GDPR limits the cloud-analytics route for vendors without stringent consent workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Rise on Recurring Revenue Momentum

Services revenue is projected to climb at 9.37% annually to 2031, surpassing hardware’s 48.43% share in 2025 as vendors convert one-time controller deliveries into multi-year support and analytics subscriptions. Schneider Electric, Honeywell, and others now package predictive-maintenance algorithms within software-as-a-service tiers, increasing stickiness and offsetting margin pressure from Asian component imports. Open-protocol adoption, notably BACnet/IP, lowers integration barriers for third-party value-add apps, letting the Europe building automation system market expand via specialist monitoring modules rather than large capital renewals.

Within hardware, sensors and field devices enjoy brisk turnover because 10-year-battery wireless models reduce maintenance, while energy and smart meters meet sub-metering rules that underpin green leasing. Actuators specified with feedback and fail-safe modes also lift average selling prices although manufacturers must harmonize with EN 12101 smoke-control standards to qualify for high-rise deployments.

By System Type: Security Integration Accelerates in Hybrid Work Era

Security and access control solutions are forecast to grow at 9.53% through 2031, outpacing the broader Europe building automation system market as occupancy-aware access points feed live data into HVAC scheduling tools. HVAC controls remain the largest slice at 40.51% share in 2025, but the installed base lengthens replacement intervals to about 15 years, moderating growth. Lighting upgrades ride LED retrofits that embed mesh radios, turning luminaires into digital sensors for desk-usage mapping. In parallel, energy-management layers are being implemented in industrial facilities striving for ISO 50001 certification, requiring analytics to document specific energy performance indicators.

Video surveillance and access analytics are now converging with environmental controls, enabling a single occupancy data stream to throttle ventilation, adjust lighting, and alert security teams in real time, minimizing server overhead while maximizing actionable insights. Suppliers that expose open REST or GraphQL APIs on their security panels are capturing incremental software revenue because facility managers can license third-party workplace analytics dashboards instead of installing separate people-counting cameras. This multipurpose architecture shortens payback periods for Europe building automation system market deployments in mid-size offices because one sensor network services both safety and energy objectives. Modules that bundle visitor-management kiosks with biometric verification further improve tenant experience, a differentiator for landlords competing against remote-work flexibility.

By Communication Technology: Wireless Narrows a Historically Wide Gap

Wireless platforms will grow at 9.61% annually through 2031, chipping away at wired systems’ 64.67% revenue lead in 2025 as Matter, Thread, and private 5G address vendor lock-in concerns. Building owners appreciate installation speed that avoids ceiling disturbances in occupied spaces, while BACnet/IP over IPv6 and TLS satisfy NIS2 cybersecurity rules. Wired Ethernet remains essential for life-safety loops that require hard supervision, but affordable battery-powered sensors are proving adequate for temperature and occupancy tasks that dominate routine energy optimization.

Mature projects still default to wired Ethernet for life-safety loops, yet wireless backbones increasingly act as redundancy layers that sustain basic HVAC control during network outages, satisfying business-continuity clauses in many green-lease agreements. Vendors have started shipping dual-radio controllers that auto-select between Wi-Fi 6 and Thread, letting installers mix node types as building materials or radio interference dictate. Private 5G pilots in German automotive plants illustrate how ultra-reliable, low-latency links can synchronize HVAC set points with robotic welding cells, trimming energy peaks in trimming processes without jeopardizing production targets. Facilities that overlay BACnet/IP traffic on the same spectrum secure compliance with NIS2 encryption mandates at no extra licensing cost, cutting total cost of ownership for large campuses.

By Installation Type: Retrofits Command the Growth Spotlight

Retrofits held 55.63% of 2025 revenue and will advance at 9.11% CAGR, reflecting Europe’s aging commercial inventory and slow greenfield construction pipeline. Wireless, self-commissioning devices lower labor costs and reduce project downtime, dovetailing with KfW Bank’s low-interest retrofit loans that prioritize holistic automation upgrades over piecemeal HVAC swaps. New-build projects, though technically advanced, account for fewer square meters because high interest rates and lengthy permitting temper speculative starts, limiting their proportionate influence on the Europe building automation system market.

Green-finance covenants increasingly include project-completion milestones, so retrofits that rely on battery-powered sensors appeal to lenders because material lead-time risk is lower than for custom-fabricated control panels. Municipalities exploiting KfW or cohesion-fund loans often stipulate that contractors finish commissioning during school summer breaks, a window achievable only with pre-programmed wireless kits that snap onto existing actuators. Self-commissioning devices also mitigate the technician shortage in provincial towns, where certified BAS specialists are scarce and travel premiums can exceed 15% of project budgets. The net effect is a growing preference for solution bundles that ship with cloud dashboards pre-mapped to EN 15232 performance classes, avoiding time-consuming on-site point mapping.

By End User: Public Mandates Propel Institutional Facilities

Institutional and government buildings are set for the fastest expansion at 9.46% CAGR, driven by EPBD milestones that push municipalities to install energy dashboards ahead of 2030 decarbonization goals. Commercial premises, which claimed 46.83% of 2025 revenue, still anchor demand because landlords chase LEED or BREEAM certificates to justify premium rents. Industrial adopters link BAS with process HVAC to curb energy by 15%-20%, meeting recurring audit requirements under the Energy Efficiency Directive and ISO 50001.

Public hospitals and universities now stipulate open-protocol controllers to future-proof against vendor lock-in, pushing suppliers to guarantee long-term firmware support that aligns with NIS2 patch cycles. Commercial landlords, meanwhile, leverage granular sub-metering to pass utility costs through to tenants under green leases, cutting common-area energy intensity by double digits and supporting lease-renewal negotiations with verified savings data. Industrial buyers integrate BAS alarms with manufacturing execution systems so that production slowdowns automatically trigger HVAC setbacks, conserving energy during unplanned downtime. Multifamily property managers increasingly bundle apartment-level smart-thermostat data into community dashboards that demonstrate compliance with local building-emissions caps, a feature that eases access to municipal retrofit rebates.

Geography Analysis

Germany’s 37.33% share in 2025 underscores its leadership in industrial automation and its stringent GEG code, which obliges smart gateways in new structures. Yet retrofits here face technician shortages outside Munich or Frankfurt, elongating commissioning queues and nudging owners toward wireless kits that technicians can configure remotely. Roof-mounted photovoltaics feed BAS data into energy-trading algorithms that earn frequency-regulation fees, reinforcing the Europe building automation system market’s value proposition.

Poland records the top national growth, with a 9.38% forecast CAGR, thanks to EUR 2.5 billion (USD 2.8 billion) of cohesion-fund grants reserved for public-building thermal modernization. Developers in Warsaw and Kraków increasingly specify open-protocol wireless controllers from day one, avoiding the retrofit overhead that Western peers confront.

France leverages the Tertiary Decree to compel buildings above 1,000 m² to shave energy use by 40% by 2030, a mandate that automatically pulls BAS into retrofit scopes because manual logs cannot satisfy OPERAT platform disclosure requirements. The United Kingdom mirrors EU ambition via its Future Homes Standard, ensuring continuity for cross-border suppliers. Nordic countries, led by Sweden and Finland, pioneer district-heating integration, using forecast algorithms to trim municipal peak loads by double digits proof of concept for colder Central European cities planning similar interventions.

Competitive Landscape

Market leaders are supplementing hardware lines with software marketplaces that host third-party analytics apps, replicating smartphone-style ecosystems that deepen customer lock-in without breaching antitrust thresholds. Siemens, for example, curates an app store on its Desigo X platform where certified partners publish fault-detection modules; revenues are split on a subscription basis that converts one-time controller deals into recurring income streams. Schneider Electric pursues a similar approach by exposing EcoStruxure APIs so real-estate technology firms can build bespoke ESG-reporting widgets, expanding platform stickiness when corporate landlords seek automated Scope 2 disclosures.

A second competitive front involves cybersecurity credentials. ABB and Honeywell have achieved IEC 62443-4-2 certification for their edge controllers, giving them an edge in bids for data-center and healthcare projects classified as essential services under NIS2. Smaller integrators respond by offering overlay software that segments legacy networks into virtual zones, allowing owners to postpone costly controller swaps while still passing mandatory penetration tests. This services niche is enabling regional specialists to win retrofit contracts even when hardware specifications appear to favor incumbents.

Finally, vendor alliances are forming around wireless standards to accelerate Matter adoption. Johnson Controls and Legrand co-sponsor interoperability labs that pre-certify multisupplier device bundles so that facility managers can issue a single purchase order rather than coordinate multi-vendor commissioning. Concurrently, open-source projects such as the Eclipse IoT stack reduce entry barriers for analytics startups that sell Kubernetes-based building-OS containers, further diluting hardware-centric dominance. Collectively, these dynamics reinforce a Europe building automation system market in which scale still matters, but agility and ecosystem depth increasingly dictate share gains.

Europe Building Automation Systems Industry Leaders

Siemens AG

Schneider Electric SE

Johnson Controls International plc

Honeywell International Inc.

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Johnson Controls earmarked EUR 85 million (USD 95 million) for a Warsaw R and D hub focused on wireless sensors and AI energy optimization.

- March 2026: Honeywell clinched a EUR 62 million (USD 70 million) retrofit contract for 120 Dutch public schools that couples HVAC controls with indoor air-quality monitoring.

- February 2026: Siemens released Desigo CC V5.2 featuring native NIS2 compliance, automated network segmentation, and encrypted controller traffic.

- January 2026: ABB bought a Swedish software firm for EUR 45 million (USD 50 million) to bolster district heating optimization in Nordic markets.

Europe Building Automation Systems Market Report Scope

The Europe Building Automation System Market is witnessing significant growth due to the increasing adoption of energy-efficient solutions, advancements in IoT technology, and the rising demand for smart buildings. These systems are becoming integral in optimizing energy consumption, enhancing security, and improving overall operational efficiency across various sectors.

The Europe Building Automation System Market Report is Segmented by Component (Hardware, Software, Services), System Type (HVAC Control, Lighting Control, Security and Access Control, Energy Management, Fire and Life-Safety), Communication Technology (Wired, Wireless), Installation Type (New-Build, Retrofit), End User (Residential, Commercial, Industrial, Institutional/Government), and Geography (Germany, UK, France, Spain, Italy, Netherlands, Belgium, Sweden, Finland, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

By Component

| Hardware | Controllers | |

| Sensors and Field Devices | Temperature Sensors | |

| Humidity Sensors | ||

| Occupancy Sensors | ||

| Smart Meters | ||

| Energy Meters | ||

| Current Transformers | ||

| Environmental Sensors | ||

| Actuators | ||

| Others | ||

| Software | Supervisory / Management Software | |

| Analytics / Energy Management Software | ||

| Services | Installation | |

| Maintenance and Support | ||

By System Type

| HVAC Control Systems | ||

| Lighting Control Systems | ||

| Security and Access Control Systems | Video Surveillance System | |

| Access Control Systems | Card / RFID Access | |

| Biometric Access | ||

| Energy Management Systems | ||

| Fire and Life-Safety Systems | ||

By Communication Technology

| Wired |

| Wireless |

By Installation Type

| New-Build |

| Retrofit |

By End User

| Residential |

| Commercial |

| Industrial |

| Institutional / Government |

By Country

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Netherlands |

| Belgium |

| Sweden |

| Finland |

| Rest of Europe |

| By Component | Hardware | Controllers | |

| Sensors and Field Devices | Temperature Sensors | ||

| Humidity Sensors | |||

| Occupancy Sensors | |||

| Smart Meters | |||

| Energy Meters | |||

| Current Transformers | |||

| Environmental Sensors | |||

| Actuators | |||

| Others | |||

| Software | Supervisory / Management Software | ||

| Analytics / Energy Management Software | |||

| Services | Installation | ||

| Maintenance and Support | |||

| By System Type | HVAC Control Systems | ||

| Lighting Control Systems | |||

| Security and Access Control Systems | Video Surveillance System | ||

| Access Control Systems | Card / RFID Access | ||

| Biometric Access | |||

| Energy Management Systems | |||

| Fire and Life-Safety Systems | |||

| By Communication Technology | Wired | ||

| Wireless | |||

| By Installation Type | New-Build | ||

| Retrofit | |||

| By End User | Residential | ||

| Commercial | |||

| Industrial | |||

| Institutional / Government | |||

| By Country | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Netherlands | |||

| Belgium | |||

| Sweden | |||

| Finland | |||

| Rest of Europe | |||

Key Questions Answered in the Report

How large will the Europe building automation system market be by 2031?

It is forecast to reach USD 28.97 billion, up from USD 19.02 billion in 2026 under an 8.78% CAGR.

Which component grows fastest across European projects?

Services, encompassing maintenance and cloud analytics, are projected to rise at 9.37% annually through 2031.

Why is Poland expanding more quickly than Western peers?

EU cohesion funding offsets retrofit costs, lifting Poland to a 9.38% forecast CAGR - the highest among European countries.

How are new energy rules influencing demand?

The 2026 Smart Readiness Indicator label and EPBD recast force automation adoption to document real-time performance required for green finance and regulatory compliance.

What role does wireless technology play in retrofits?

Wireless sensors and controllers cut installation labor by up to 50% and are expected to grow at 9.61% CAGR, steadily narrowing the gap with wired systems.

Which vendors lead the competitive field today?

Siemens, Schneider Electric, Johnson Controls, Honeywell, and ABB together capture nearly half of regional revenue, although open-protocol challengers continue to erode share.

Page last updated on: