Size and Share of North America Animal Feed Organic Trace Minerals

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

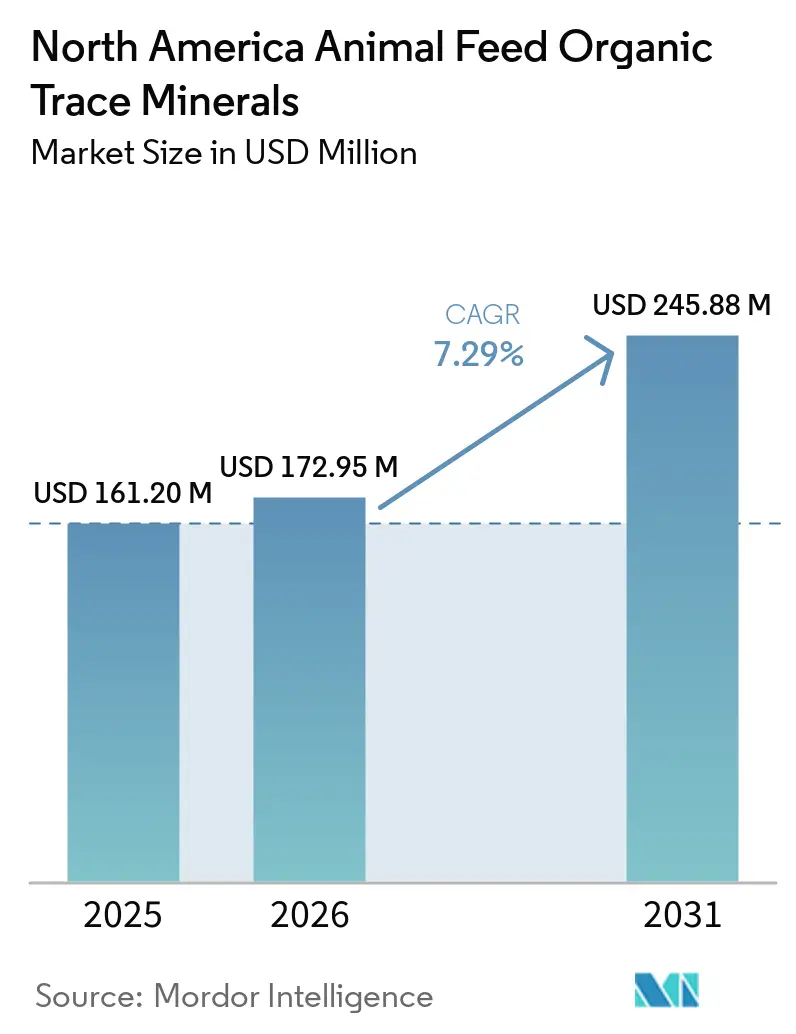

| Base Year Market Size (2025) | USD 161.20 Million |

| Market Size (2026) | USD 172.95 Million |

| Market Size (2031) | USD 245.88 Million |

| Growth Rate (2026 - 2031) | 7.29% CAGR |

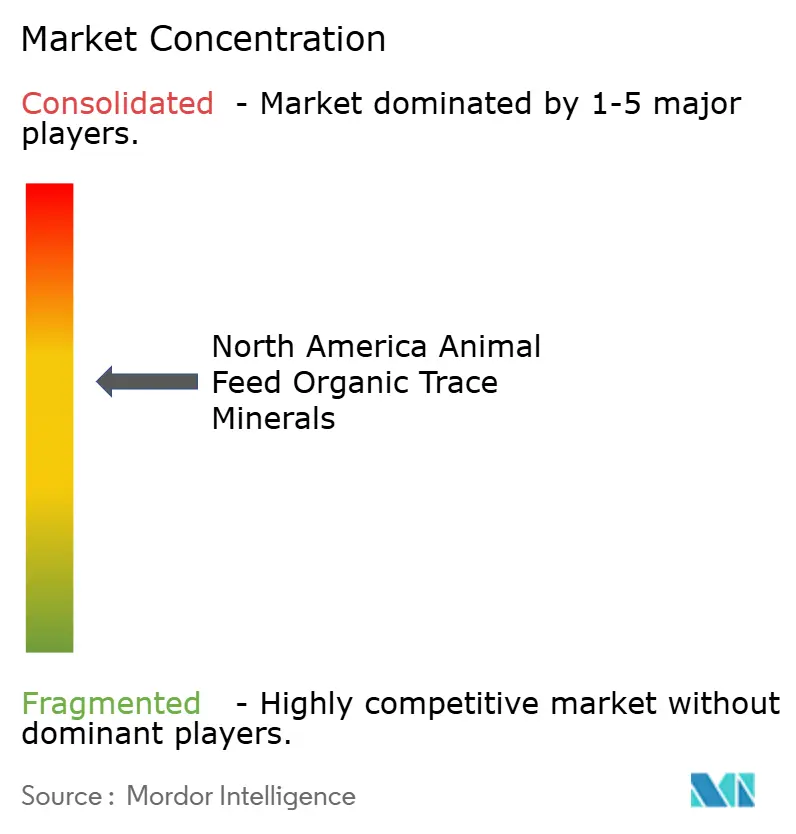

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of North America Animal Feed Organic Trace Minerals by Mordor Intelligence

The North America animal feed organic trace minerals market size is projected to expand from USD 161.20 million in 2025 and USD 172.95 million in 2026 to USD 245.88 million by 2031, registering a compound annual growth rate (CAGR) of 7.29% between 2026 and 2031. The North America animal feed organic trace minerals market is advancing as livestock producers replace inorganic sulfate and oxide sources with chelated, proteinated, and amino acid-complexed forms that deliver better bioavailability at lower inclusion levels. That change supports feed efficiency goals and aligns with the tighter regulatory framework for organic livestock feed in the United States and Canada. Demand remains anchored in the United States because certified organic livestock operations must follow defined feed rules under the United States Department of Agriculture National Organic Program, which keeps compliant mineral premixes in regular demand. Competition in the North America animal feed organic trace minerals market is shaped more by proprietary mineral chemistry, manufacturing control, and proof of animal response than by scale alone. Even so, the North America animal feed organic trace minerals market still faces pressure from premium pricing, certification costs, and volatility in amino acid-based chelation inputs, which can slow adoption when livestock margins weaken.

Key Report Takeaways

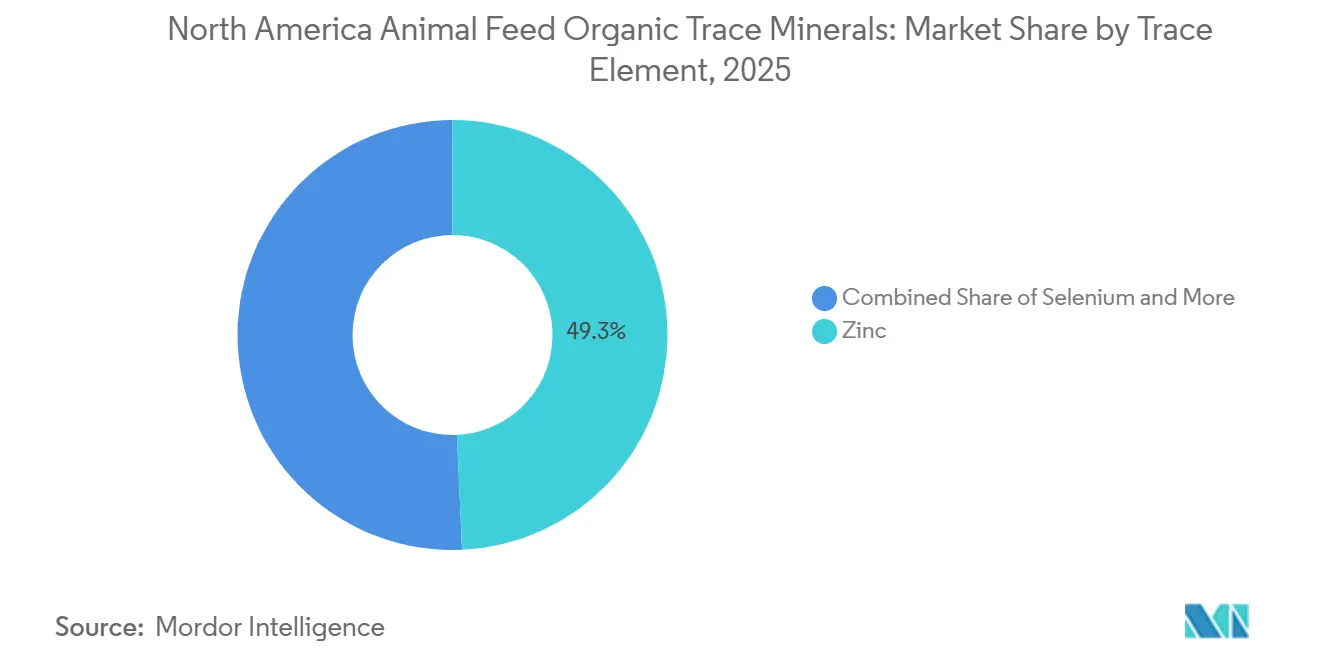

- By trace element, zinc was the largest segment and accounted for 49.3% of the North America animal feed organic trace minerals market share in 2025, while selenium was the fastest-growing segment and is forecast to expand at a 7.7% CAGR through 2031.

- By animal type, ruminants were the largest segment with 31.6% of the North America animal feed organic trace minerals market size in 2025, while aquaculture was the fastest-growing segment and is forecast to grow at an 8.9% CAGR through 2031.

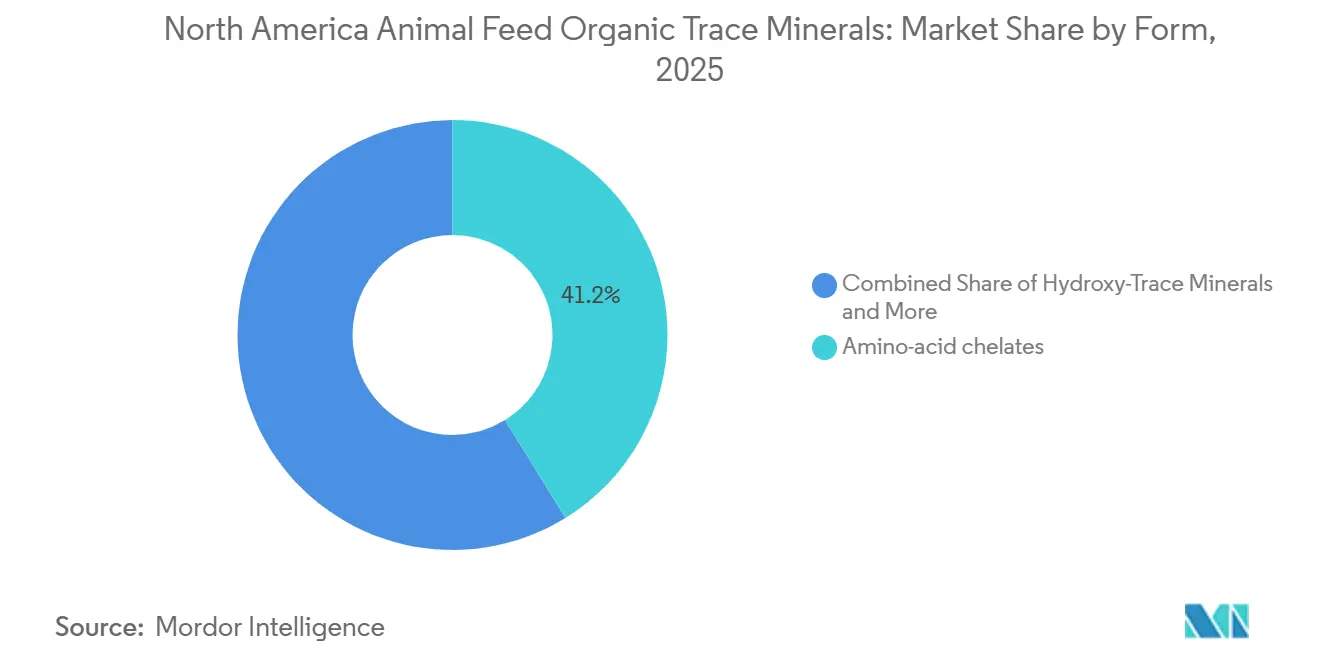

- By chelation type, amino-acid chelates accounted for 41.2% of revenue in 2025, whereas hydroxy-trace minerals are advancing at an 8.2% CAGR through 2031.

- By geography, the United States was the largest segment, which accounted for 73.7% of revenue share in 2025, and the fastest-growing, with a 7.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of North America Animal Feed Organic Trace Minerals

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher demand for premium animal protein and feed efficiency | +2.1% | United States and Canada, primary, Mexico, emerging | Long term (≥ 4 years) |

| Shift from inorganic salts to higher-bioavailability organic minerals | +1.5% | United States, primary, Canada, secondary | Medium term (2-4 years) |

| Tighter feed-safety and mineral-excretion compliance pressure | +1.0% | United States, Canada, and Mexico | Medium term (2-4 years) |

| Precision nutrition adoption in large integrated livestock systems | +0.8% | United States and Canada | Long term (≥ 4 years) |

| DDGS sulfur antagonism raising need for more stable mineral forms | +0.6% | United States Corn Belt and Western Canada feedlots | Short term (≤ 2 years) |

| Heat-stress mitigation demand for chromium, zinc, and selenium programs | +0.5% | Southern United States and Gulf Coast | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Demand for Premium Animal Protein and Feed Efficiency

The North America animal feed organic trace minerals market is benefiting from stronger consumer preference for food produced under organic and clean-label systems. That demand supports more certified organic livestock production, which, in turn, keeps mineral supplementation essential across feed programs. Under 7 Code of Federal Regulations 205.236 and 205.237, livestock sold as organic must remain under continuous organic management and must receive feed that meets organic handling rules, which supports steady replacement demand for approved mineral inputs[1]Source: Agricultural Marketing Service, Department of Agriculture, “7 CFR § 205.237, Livestock Feed,” Electronic Code of Federal Regulations, ecfr.gov. The buying case is also supported by measured animal responses, as Kansas State University Beef Cattle Institute reported in April 2024 that stressed beef heifers fed organic zinc, copper, manganese, and cobalt complexes showed lower morbidity and higher daily gain than those fed inorganic sulfates. As more producers see organic minerals as both a compliance tool and a performance input, the North America animal feed organic trace minerals market gains support beyond niche premium farming channels.

Shift From Inorganic Salts to Higher-Bioavailability Organic Minerals

The North America animal feed organic trace minerals market is also advancing, as many conventional producers are not waiting for full certification before changing parts of their mineral programs. Partial replacement strategies are becoming more common, as nutrition teams seek better feed conversion and lower trace mineral losses without changing the full ration system. This approach matters because it expands demand into the much larger conventional livestock base across the region, especially in poultry and dairy systems, where response to mineral form can be tracked more closely. The shift is strongest where producers already manage feed under clear quality and labeling standards, including organic feed programs overseen at the state level in the United States. Over time, this staged adoption pattern gives the North America animal feed organic trace minerals market a wider base than certified organic livestock alone.

Tighter Feed-safety and Mineral-Excretion Compliance Pressure

The North America animal feed organic trace minerals market is being supported by a stricter regulatory setting that rewards suppliers with stronger documentation and tested formulations. Canada’s Livestock Feed Regulations, 2024 introduced updated requirements around labeling, nutrient guarantees, and preventive control plans, which is pushing feed manufacturers to review the technical basis for mineral ingredients already in use[2]Source: Gouvernement du Canada, “Règlement de 2024 sur les Aliments du Bétail (DORS/2024-132),” Site Web de la législation, laws-lois.justice.gc.ca. The Canadian Food Inspection Agency also confirmed phased implementation steps in 2025 and 2026, which has added urgency for mid-sized blenders that still rely on less documented inputs. In this setting, suppliers that already hold organic mineral certifications and analytical dossiers gain an operational advantage by responding more quickly to audit requests and customer reformulation needs. The result is a regulatory environment that supports higher-quality suppliers and reinforces the growth path of the North America animal feed organic trace minerals market.

Precision Nutrition Adoption in Large Integrated Livestock Systems

The North America animal feed organic trace minerals market is also gaining from a broader move toward precision feeding and closer animal-level monitoring. Large dairy and beef operations increasingly use herd data, milk output measures, and nutrition models to adjust mineral supplementation by production stage and stress event rather than relying on uniform formulas. That favors organic trace minerals because their higher bioavailability can support more targeted dosing where outcomes such as reproductive performance, hoof health, and milk solids matter most. Suppliers are responding by linking products with advisory tools and service platforms, which makes customer relationships harder to displace even when competing products look similar on paper. As livestock systems become more data driven, the North America animal feed organic trace minerals market is likely to see stronger demand for branded mineral programs that can show measurable biological response.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing versus inorganic alternatives | -1.5% | United States commodity livestock segments and Canada beef feedlots | Short term (≤ 2 years) |

| Organic certification and labeling complexity | -1.2% | United States small and mid-scale feed manufacturers and Mexico | Medium term (2-4 years) |

| Restricted protein sources and organic-carrier rules for compliant premixes | -0.8% | North America wide, with dependence on Asian amino acid supply chains | Medium term (2-4 years) |

| Performance variability across loosely defined organic mineral chemistries | -0.5% | Rural United States and traditional beef operations in Canada and Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Versus Inorganic Alternatives

Premium pricing remains one of the clearest limits on how fast the North America animal feed organic trace minerals market can penetrate conventional livestock systems. Organic chelated and proteinated minerals carry a much higher cost than inorganic sulfates and oxides, and that gap becomes harder to absorb when feed grains are expensive, or animal selling prices soften. The pressure is strongest in swine and broiler operations, where per-head margins are thin, and ration costs are closely reviewed at every reformulation cycle. Large integrated producers can spread the premium across scale efficiencies and response gains, but smaller cattle and mixed-animal operators face greater direct exposure to the added cost. This keeps demand structurally positive while still making the North America animal feed organic trace minerals market vulnerable to cyclical pauses.

Organic Certification and Labeling Complexity

Organic certification barriers still slow broader participation in the North America animal feed organic trace minerals market, particularly for smaller regional feed manufacturers. Under the National Organic Program, synthetic ingredients used in livestock feed must be on the National List, and feed inputs sold into organic systems must meet documentation and handling requirements beyond ordinary commercial feed practices. The burden is not limited to the active mineral itself, as ingredient carriers and sourcing changes can trigger additional review and recordkeeping. That adds costs, extends lead times, and reduces flexibility for smaller blenders without dedicated compliance teams. As a result, the North America animal feed organic trace minerals market tends to concentrate on compliant premix manufacturing among larger suppliers with stronger regulatory systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Trace Element: Zinc Holds the Largest Position While Selenium Advances Fastest

Zinc held 49.3% of the North America animal feed organic trace minerals market share in 2025, which made it the largest trace element segment. Its leadership stems from its widespread use across dairy, beef, poultry, and swine, where hoof integrity, feather quality, immune function, and reproductive performance all depend on reliable zinc status. Producers also understand zinc better than many other trace elements, so repeat purchase behavior is stronger in both premix and direct supplementation formats. In addition, pressure to reduce trace mineral excretion keeps organic zinc relevant, as higher bioavailability can support lower inclusion rates without weakening performance.

The North America animal feed organic trace minerals market for selenium-linked demand is forecast to expand at a 7.7% CAGR through 2031, making selenium the fastest-growing trace element segment. Growth is closely tied to aquaculture and other intensive systems, where antioxidant defense and stress resilience matter more under high-density production conditions. Research published in Frontiers in Marine Science in February 2025 showed that organic selenium with vitamins C and E improved growth, antioxidant enzyme activity, and blood parameters in juvenile silver carp under intensive aquaculture conditions. Copper, iron, and manganese continue to serve narrower species and stage specific needs, while chromium remains a smaller specialty category. Across the North America organic feed minerals industry, that leaves zinc as the broadest volume anchor and selenium as the clearest expansion pocket.

By Animal Type: Ruminants Form the Largest Base While Aquaculture Expands Fastest

Ruminants accounted for 31.6% market share in 2025, making them the largest animal type segment in the North America animal feed organic trace minerals market. Dairy economics support that position because mineral status affects milk solids, udder health, fertility, and cow longevity, which keeps supplementation decisions highly visible at the farm level. Beef systems also contribute because stress management, hoof condition, and immune support remain important during backgrounding and feedlot transitions. Organic dairy rules in the United States and Canada further strengthen baseline demand because compliant trace mineral premixes remain central to certified feeding programs.

The North America animal feed organic trace minerals market for aquaculture applications is forecast to grow at an 8.9% CAGR through 2031, making aquaculture the fastest-growing animal type. Expansion in recirculating aquaculture systems (RAS) and marine shrimp production is increasing demand for minerals that can support oxidative balance, feed conversion, and survival under dense rearing conditions. Poultry already uses some chelated minerals and therefore grows from a more developed base, while swine, equine, and pet niches remain smaller but are improving. Within the North America animal feed organic trace minerals industry, aquaculture is moving from a specialty outlet into a more meaningful growth channel.

By Chelation Type: Amino-Acid Chelates Anchor Formulation While Hydroxy Minerals Advance Fastest

Amino-acid chelates held 41.2% of the market share in 2025, making them the largest chelation type in the North America animal feed organic trace minerals market share mix. Their lead comes from broad acceptance in livestock feed programs and from a structure that keeps the mineral more stable through digestion. The single mineral-single amino acid bond helps reduce interference from phytates, sulfur compounds, and other cations, which often weaken absorption from inorganic sources. That stability supports use across ruminants, swine, poultry, and aquaculture. Proteinates ranked behind amino-acid chelates because they offer a more balanced cost-to-efficacy profile in complete-feed programs, while polysaccharide complexes and propionates remained more limited in use.

The North America animal feed organic trace minerals market for hydroxy-trace minerals is projected to grow at an 8.2% CAGR from 2026 to 2031, making hydroxy minerals the fastest-growing chelation type segment. Their growth is tied to stronger feed-matrix stability during pelleting and steam conditioning, where less stable chelate forms can lose effectiveness. This makes hydroxy minerals more attractive in high-throughput feed manufacturing and in livestock systems exposed to heat stress or immune pressure. BASF’s November 2025 agreement with Biochem Zootechnik GmbH also highlighted how more stable mineral forms can reduce negative interactions with vitamins and enzymes in feed formulations. Yeast-based complexes are also gaining traction in certified organic and antibiotic-free systems because they fit clean-label positioning and support organically compatible supplementation pathways under United States Department of Agriculture National Organic Program feed rules.

Geography Analysis

The United States accounted for 73.7% of the North America animal feed organic trace minerals market share in 2025, which made it the largest country segment in the region. Its lead reflects the depth of certified organic livestock production, a broad commercial dairy and poultry base, and a mature distribution network that connects chelation plants with animal-dense production regions. The United States also records the fastest stated country CAGR at 7.6% through 2031, supported by aquaculture expansion and continued organic dairy herd development. The National Organic Program keeps demand firm because certified operations must use feed that meets organic livestock requirements. Cross-border field evidence also supports the buying case, as Asociación Angus Mexicana reported in January 2026 that organic micromineral supplementation improved daily gain and feed conversion in weaned Angus calves, which matters for Northern Mexico systems linked to United States feedlots.

Canada remained the second-largest national market in the region, with demand centered on dairy production in Ontario and Quebec and feedlot activity in Alberta. The Canadian Food Inspection Agency confirmed in June 2025 that phased support would continue and that preventive control plan inspections would begin in 2026, thereby raising the urgency of reformulation and compliance planning. DSM-Firmenich’s Ontario premix footprint supports supply, though the February 2026 agreement to divest its Animal Nutrition and Health business for EUR 3.85 billion (USD 4.20 billion) introduces a transition period for customer accounts.

Mexico growth is tied to poultry, aquaculture, and export-oriented beef systems that need better animal performance and stronger alignment with buyer quality expectations. Adoption still trails the United States and Canada because pricing pressure and weaker distributor coverage remain real barriers in non-metropolitan agricultural zones. Even so, evidence from Mexican fieldwork is strengthening the commercial case, as Asociación Angus Mexicana reported better daily gain and stronger feed conversion with organic micromineral supplementation in weaned calves. The wider Rest of North America adds smaller incremental demand and is served mainly through supply chains led from the United States.

Competitive Landscape

The North America animal feed organic trace minerals market is moderately concentrated, with Zinpro Corporation, Balchem Corporation, Alltech, Inc., Novus International, Inc., and Kemin Industries, Inc. as the most visible suppliers. These companies compete less on simple volume and more on mineral chemistry, species-specific support, technical service, and the ability to document biological response under commercial conditions. A second layer of suppliers, including Nutreco N.V., Kemin Industries, Adisseo USA, and Phibro Animal Health Corporation, adds depth across broader animal nutrition portfolios. This structure keeps the North America animal feed organic trace minerals market competitive, but it still favors companies that combine formulation expertise with strong manufacturing and customer support systems.

Strategic moves since late 2025 show that distribution reach and portfolio control are becoming more important. Biochem Zootechnik GmbH’s agreement to acquire BASF’s global glycinate business in November 2025 strengthens Biochem’s position in organic trace minerals and expands access to BASF’s distributor network. DSM-Firmenich’s February 2026 divestiture agreement also matters because it can reshape channel relationships and product positioning across North America once the business stands alone. Balchem Corporation’s 2026 price action and 2025 investment direction point to continued emphasis on specialized mineral formats and value-added processing rather than commodity competition. The North America animal feed organic trace minerals market is therefore becoming more structured around supply security and differentiated product platforms.

Technology and sustainability credentials are also becoming more important competitive filters in the North America animal feed organic trace minerals market. Suppliers increasingly need to support customers with better traceability, clearer environmental documentation, and advice that connects mineral use with animal performance outcomes. Smaller specialists such as BioZyme, Inc. and EW Nutrition still have room to win in niche species and stressed animal applications, but the broader market continues to favor suppliers with technical proof, service depth, and dependable manufacturing systems.

Leaders of North America Animal Feed Organic Trace Minerals

Novus International, Inc.

Alltech, Inc.

Kemin Industries, Inc.

Zinpro Corporation

Balchem Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DSM-Firmenich AG has signed a definitive agreement to divest its Animal Nutrition and Health business at an enterprise value of EUR 2.2 billion (USD 2.6 billion). This business, which includes organic-certified vitamins, premixes, and performance mineral solutions, will be restructured into two distinct, standalone companies based in Kaiseraugst, Switzerland. The divestment is subject to regulatory approvals, which are projected to be finalized by late 2026. This development is anticipated to reshape the distribution dynamics for organic mineral premixes within DSM-Firmenich AG's North American network.

- November 2025: Biochem Zootechnik GmbH and BASF signed a binding agreement for Biochem's acquisition of BASF's global glycinate business, which focuses on high-performance organic trace minerals with demonstrated advantages in reducing zinc and copper excretion. The deal transfers BASF's glycinate product lines and distributor network to Biochem, which has pioneered glycinate-based organic trace minerals through its EcoTrace and B.I.O.Key platforms.

- July 2025: Zinpro Corporation launched Zinpro ProFusion Paste, a new paste-format delivery system for organic performance trace minerals targeting beef cattle during high-stress periods such as weaning, transport, and commingling. The product is scientifically validated to elevate trace mineral status within 48 hours and provides sustained nutrient delivery over multiple days, addressing a formulation gap in acute stress-event mineral management.

Scope of Report on North America Animal Feed Organic Trace Minerals

Organic trace minerals in animal feed are essential micronutrients that are chemically bound (chelated) to organic molecules such as amino acids or peptides. This natural structure mimics how minerals exist in plants, protecting them from breaking down in the animal's digestive tract and significantly boosting absorption compared to cheap, inorganic alternatives.

The North America animal feed organic trace minerals report is segmented by trace element (zinc, iron, copper, manganese, selenium, chromium, and others), by animal type (poultry, dairy cattle, beef cattle, swine, aquaculture, equine, pets, and others), by chelation type (amino-acid chelates, proteinates, polysaccharide complexes, hydroxy-trace minerals, propionates, yeast-based complexes, others), and by geography (United States, Canada, Mexico, and Rest of North America). The market forecasts are provided in terms of value (USD).

| Zinc |

| Iron |

| Copper |

| Manganese |

| Selenium |

| Chromium |

| Others |

| Poultry |

| Dairy Cattle |

| Beef Cattle |

| Swine |

| Aquaculture |

| Equine |

| Pets |

| Others |

| Amino-Acid Chelates |

| Proteinates |

| Polysaccharide Complexes |

| Hydroxy-Trace Minerals |

| Propionates |

| Yeast-Based Complexes |

| Others |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Trace Element Type | Zinc |

| Iron | |

| Copper | |

| Manganese | |

| Selenium | |

| Chromium | |

| Others | |

| By Animal Type | Poultry |

| Dairy Cattle | |

| Beef Cattle | |

| Swine | |

| Aquaculture | |

| Equine | |

| Pets | |

| Others | |

| By Chelation Type | Amino-Acid Chelates |

| Proteinates | |

| Polysaccharide Complexes | |

| Hydroxy-Trace Minerals | |

| Propionates | |

| Yeast-Based Complexes | |

| Others | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is driving growth in North America animal feed organic trace minerals demand?

Growth is being supported by the move from inorganic minerals to chelated and proteinated forms, tighter organic feed rules, stronger demand for certified livestock products, and wider use of precision feeding systems.

How large could this space become by 2031?

The North America animal feed organic trace minerals market is forecast to reach USD 245.88 million by 2031.

Which trace element leads revenue today?

Zinc is the largest trace element segment, holding 49.3% revenue share in 2025 because it serves broad needs across dairy, beef, poultry, and swine systems.

Which animal type category is growing fastest?

Aquaculture is the fastest animal type segment, with a forecast CAGR of 8.9% through 2031, supported by intensive production systems and rising demand for stress management minerals.

Why does the United States lead regional demand?

The United States held 73.7% of regional revenue in 2025 because it has the largest certified organic livestock base, mature premix distribution, and clear organic feed rules under the National Organic Program.

What is the main commercial challenge for suppliers and buyers?

Premium pricing is still the main barrier, since organic mineral forms cost more than inorganic sources and can face slower uptake when livestock margins are under pressure.

Page last updated on: