Nordics Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

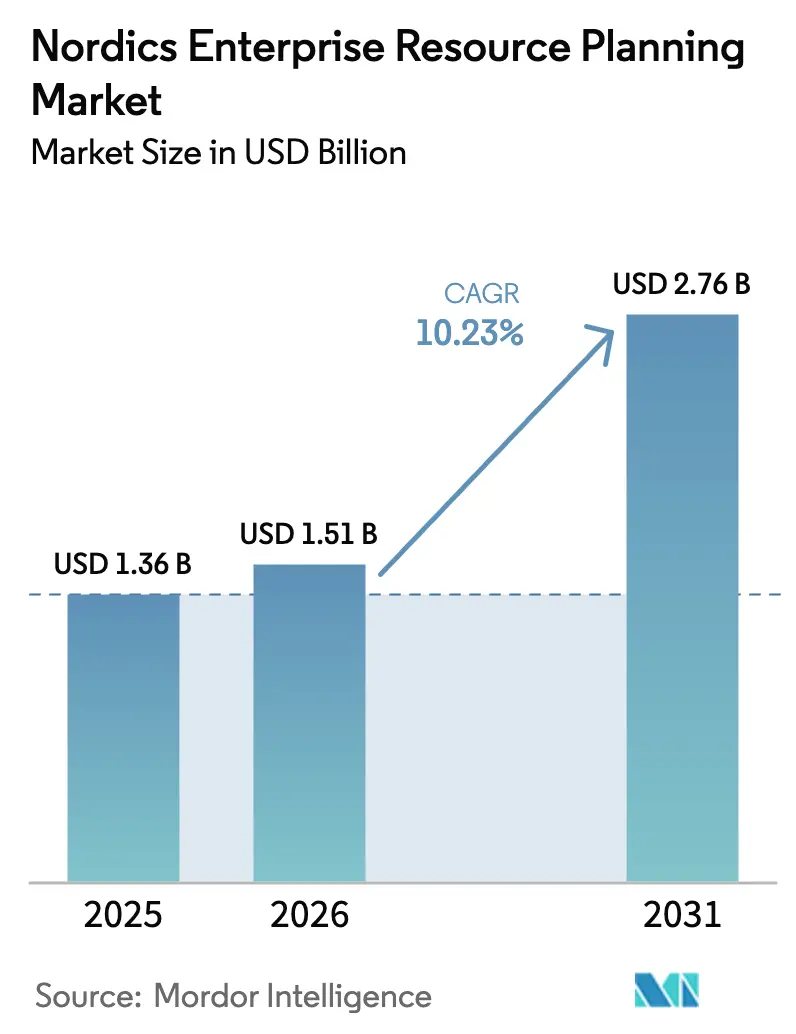

| Base Year Market Size (2025) | USD 1.36 Billion |

| Market Size (2026) | USD 1.51 Billion |

| Market Size (2031) | USD 2.76 Billion |

| Growth Rate (2026 - 2031) | 10.23% CAGR |

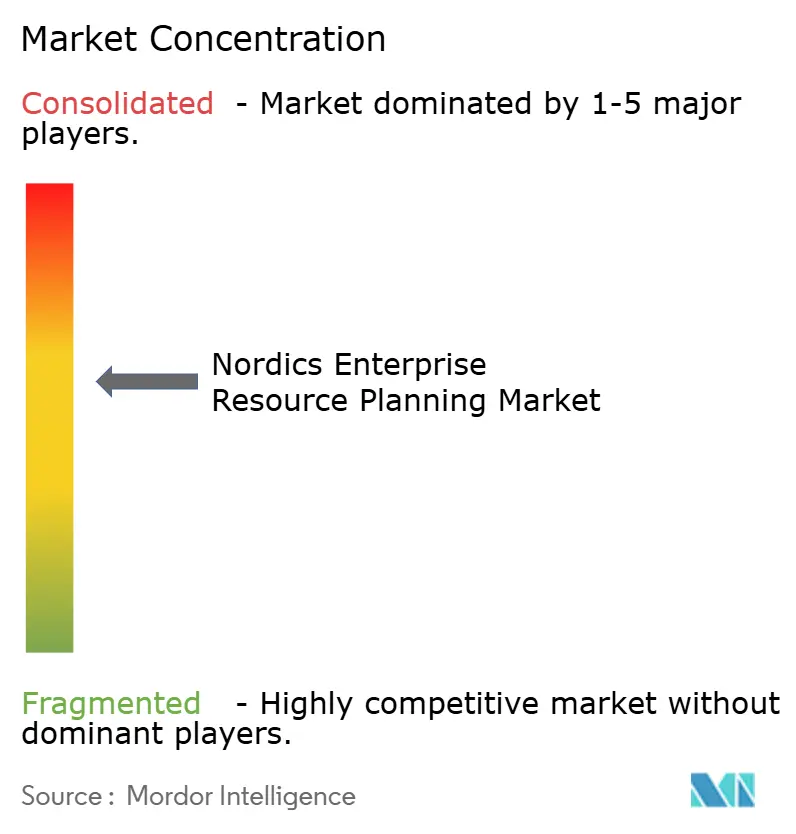

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nordics Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Nordic enterprise resource planning market size is projected to expand from USD 1.36 billion in 2025 and USD 1.51 billion in 2026 to USD 2.76 billion by 2031, registering a CAGR of 10.23% between 2026 to 2031. Strong preference for cloud-native platforms, mandatory near-real-time value-added tax reporting, and sovereign-cloud rollouts are steering investment decisions. Vendors that deliver pre-certified tax engines, embedded sustainability analytics, and Nordic-specific payroll integrations are winning new logos even as older on-premise systems linger in public-sector and heavy-industry accounts. The Nordic enterprise resource planning market is also shaped by a deepening technology-talent shortage that pushes finance and operations leaders toward extensive process automation, while divergent interpretations of data residency under the Schrems II ruling keep procurement teams cautious about hyperscalers that cannot provide in-country key custody. Despite inflation-linked budget freezes across municipal buyers, private manufacturers and service firms continue to modernize to ensure uninterrupted regulatory compliance and the sharing of real-time data with suppliers, auditors, and lenders.

Key Report Takeaways

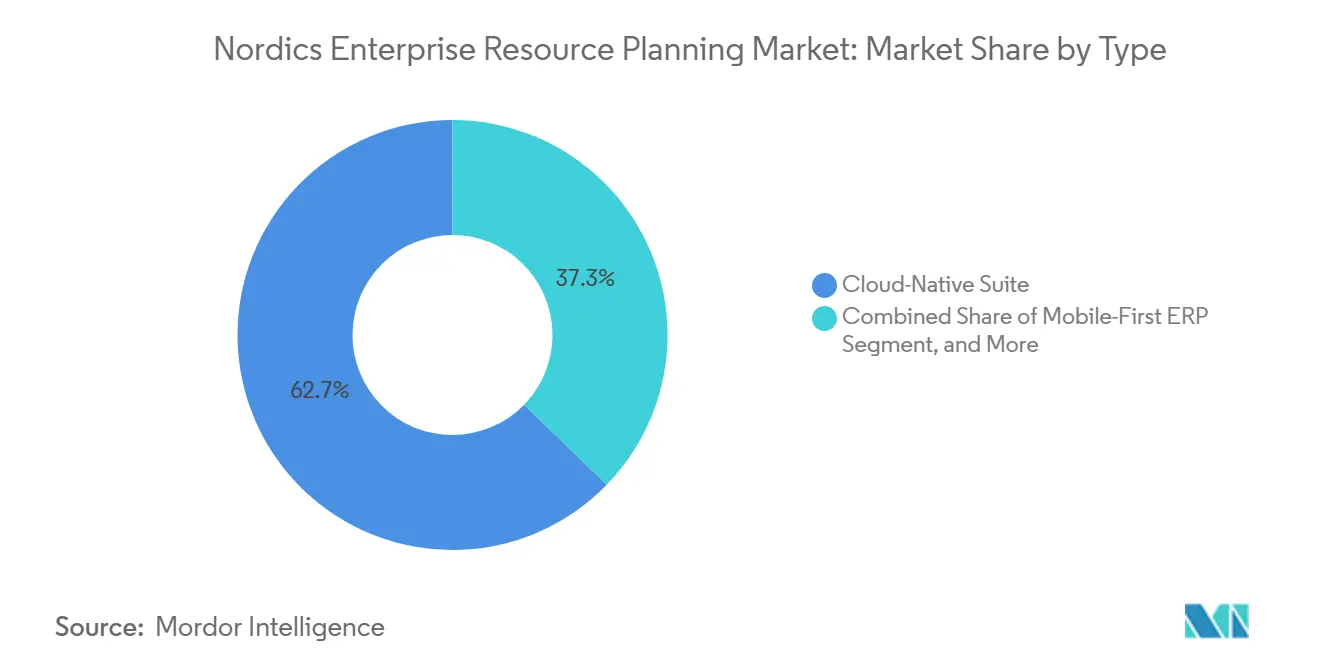

- By type, cloud-native suites led with a 62.73% revenue share in 2025, and the two-tier/edge ERP segment is forecast to grow at a 11.03% CAGR through 2031.

- By business function, finance and accounting captured 53.47% of the Nordic enterprise resource planning market share in 2025, and the manufacturing segment is projected to expand at an 11.23% CAGR to 2031.

- By deployment model, pure cloud instances accounted for 34.60% of the Nordic enterprise resource planning market in 2025, while on-premises remained larger but slower-growing at a 10.63% CAGR through 2031.

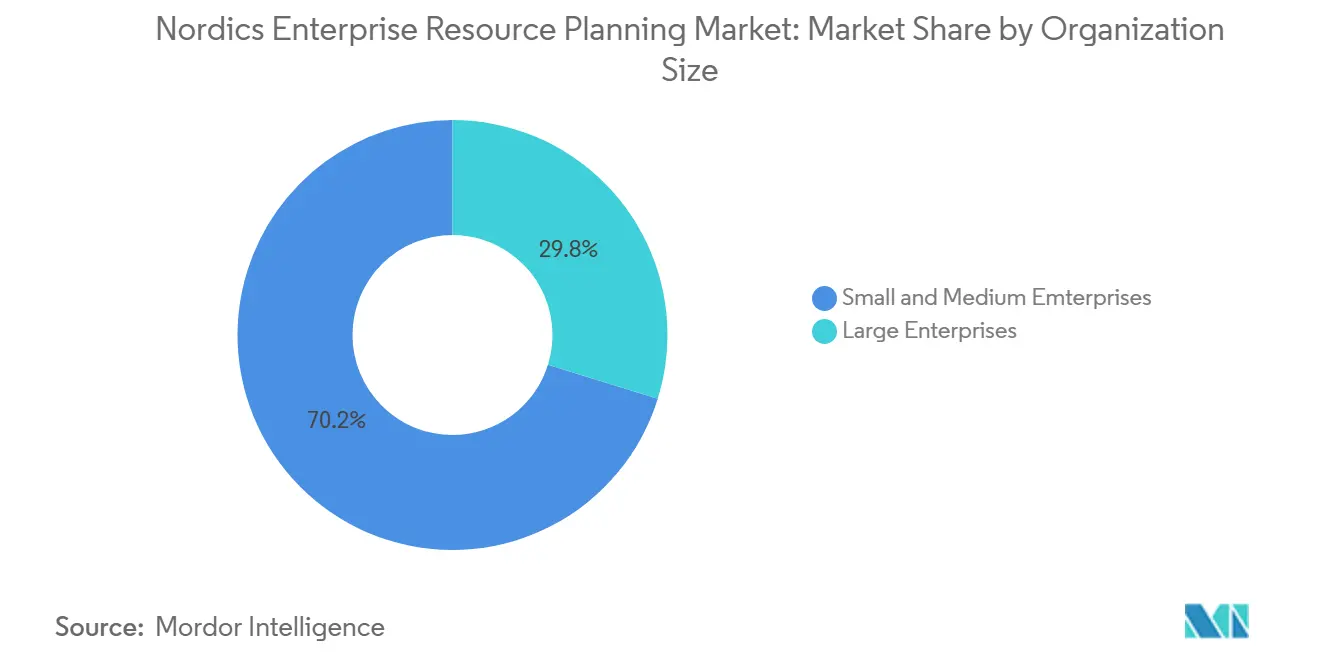

- By organization size, small and medium enterprises accounted for 70.20% of the market share in 2025 and is advancing at a 10.94% CAGR, outpacing large-enterprise projects that still account for the bulk of absolute spending.

- By industry, discrete manufacturing accounted for 37.50% of revenue in 2025 and is the retail and e-commerce segment is advancing at an 11.63% CAGR through 2031, the swiftest among all verticals.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nordics Enterprise Resource Planning Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Cloud Migration Across Nordic SMEs | +2.5% | Sweden, Denmark, Norway, Finland | Short term (≤ 2 years) |

| Government-Led Digital Transformation Initiatives | +2.2% | Finland, Denmark, Norway, Sweden | Medium term (2-4 years) |

| Rising Demand for ESG-Linked Reporting Modules | +1.8% | Sweden, Norway, Denmark | Medium term (2-4 years) |

| Near-Real-Time VAT Reporting Mandates | +1.5% | Sweden, Norway, Denmark (under review) | Short term (≤ 2 years) |

| Growing Shortage of Skilled Finance Talent | +1.3% | Region-wide | Long term (≥ 4 years) |

| Tight Integration with Nordic Open-Banking APIs | +0.8% | Sweden, Finland, Denmark, Norway | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Cloud Migration Across Nordic SMEs

Small and medium enterprises redirected capital budgets during 2024-2025 toward subscription models that eliminate server maintenance and free up scarce IT personnel. Local champions such as Fortnox added real-time corporate-card feeds that write directly to ledgers, and Visma migrated 17 acquired payroll platforms onto a single multitenant stack.[1]Source: Fortnox, “Corporate-Card Ledger Synchronization,” fortnox.se AI-first entrants like Done.ai embedded bookkeeping into banking apps, scaling to tens of thousands of users without standalone software rollouts. A March 2025 survey showed 91% of Nordic tax and finance leaders deem managed services vital for overcoming talent shortages, signaling sustained momentum for cloud conversions. Two-tier ERP pilots in Arctic supply chains further validate lightweight architectures that synchronize summary data to central systems during scheduled windows.

Government-Led Digital Transformation Initiatives

National digital-agency programs are underwriting multi-million-dollar replacements of fragmented municipal systems with interoperable suites. Examples include a nine-municipality contract in Kongsberg, Norway, and Stockholm City’s adoption of cloud budgeting tools that integrate into an existing SAP ledger. Finland’s Espoo expanded its integrator partnership to handle triple the ICT workload across its education and social service departments. Denmark’s central procurement body elevated IT security above sustainability in bid evaluations, demonstrating heightened scrutiny of vendor lock-in and cross-border data flows. These public projects create reference architectures that private buyers emulate, compressing vendor shortlists and spurring the Nordic enterprise resource planning market toward common data models.

Rising Demand for ESG-Linked Reporting Modules

The Corporate Sustainability Reporting Directive forces companies to capture granular environmental metrics at the transaction level. SAP, Workday, Microsoft, and Oracle each pushed sustainability contemporaneous updates in 2025, embedding carbon, water, and diversity analytics into core finance workflows. SAP introduced its Sustainability Control Tower in March 2025, embedding carbon-accounting logic into S/4HANA so procurement teams see scope-3 emissions alongside unit costs when approving purchase orders.[2]Source: SAP, “Sustainability Control Tower Launch,” sap.comMid-market manufacturers such as Bjelin consolidated environmental data across seven production sites after moving to IFS Cloud, replacing spreadsheet-based estimates. Because 81% of Nordic executives froze or reduced finance headcount in 2025, solutions that automate evidence gathering offer fast payback and a higher budget priority. Vendors that can pre-configure industry-specific key performance indicators unlock competitive differentiation as the Nordic enterprise resource planning market pivots from aggregated annual disclosures to real-time assurance.

Near-Real-Time VAT Reporting Mandates

Policy momentum is accelerating toward invoice-level data submission within hours of issuance. Sweden opened a public inquiry in February 2026, while Norway’s finance ministry set a 2028 clearance deadline affecting 400,000 firms. European-level proposals harmonize cross-border digital reporting by 2030, creating a clear compliance horizon. Empirical studies show that real-time controls can cut audit cycles by up to 40% and reduce posting errors when validation logic is embedded before ledger write-back. Nordic vendors that secure early certification with revenue agencies become preferred partners, as finance directors face personal liability for late or inaccurate filings, further energizing demand in the Nordic enterprise resource planning market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Custom-Built Systems with High Switching Costs | -1.2% | Sweden, Norway, Denmark | Medium term (2-4 years) |

| Data-Residency Concerns Under Schrems II | -0.9% | Denmark, Sweden, Finland, Norway | Short term (≤ 2 years) |

| Limited 5G Coverage in Remote Nordic Regions | -0.5% | Northern Sweden, Norway, Finland | Long term (≥ 4 years) |

| Inflation-Driven IT Budget Freezes in Public Sector | -0.7% | Denmark, Finland, Norway, Sweden | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy Custom-Built Systems with High Switching Costs

Many municipalities, universities, and conglomerates still rely on 1990s-era COBOL solutions welded to payroll and pension databases. Modernization entails multi-year parallel runs, costly data cleansing, and process re-engineering that can exceed annual maintenance fees by three times. Migrating these environments to commercial cloud platforms requires data cleansing, business-process reengineering, and parallel runs that can span 18 to 36 months and consume budgets three to five times the annual cost of maintaining the legacy system.[3]SKI Denmark, “IT Security as Top Procurement Priority,” ski.dk Recent public-sector migrations illustrate 14-month timelines even for limited-scope deployments, encouraging organizations to extend support contracts rather than replace core ledgers. This inertia slows cloud growth among larger entities and segments the Nordic enterprise resource planning market between agile SME adopters and risk-averse incumbents.

Data-Residency Concerns Under Schrems II

Since the invalidation of the Privacy Shield, procurement teams have scrutinized any vendor with operations exposed to United States surveillance law. Oracle introduced an EU sovereign cloud in 2025, and Microsoft hosts data in Norway and Sweden, yet buyers in Denmark and Finland sometimes insist that encryption keys never cross national borders. Divergent legal interpretations complicate disaster-recovery planning and prolong tender cycles. Local providers that guarantee in-country support teams and key custody gain a marketing edge, but uncertainty still delays decisions and suppresses short-term conversions in parts of the Nordic enterprise resource planning market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cloud-Native Suites Dominate as Two-Tier Models Expand

Cloud-native suites already account for 62.73% of the Nordic enterprise resource planning market in 2025, remain the cornerstone of modernization programs. Subscription pricing removes capital barriers for SMEs, while sovereign cloud regions address public-sector data-sovereignty concerns. Mobile-first offerings, which held a significant share, attract construction and logistics crews that work offline and sync later. Two-tier and edge deployments stand out in terms of growth, with an 11.03% CAGR, driven by rapid expansion as multinational manufacturers establish lightweight instances for Arctic subsidiaries.

Quarterly product releases illustrate rapid innovation. IFS Cloud 25R2 embedded generative planning, Oracle NetSuite Next unveiled conversational agents, and SIX ERP entered the scene with an AI-first platform promising EU-resident data by default. Pilot studies at Luleå University verify that edge nodes can operate over intermittent satellite links, lending credence to distributed architectures. Overall, deployment flexibility coupled with modular AI tools is reshaping vendor shortlists across the Nordic enterprise resource planning market.

By Business Function: Finance Remains the Anchor While Shop-Floor Modules Accelerate

Finance and accounting modules accounted for 53.47% of the Nordic enterprise resource planning market share in 2025, driven by statutory changes requiring invoice-level tax data and granular ESG cost allocation. Supply-chain suites follow as manufacturers connect warehousing, planning, and logistics to a single data fabric, with growth of 11.23% through 2031 underscoring an enduring priority. Meanwhile, manufacturing execution systems, although accounting for a smaller share of future revenues, are expected to grow at the fastest rate as Swedish and Norwegian factories integrate real-time shop-floor feeds to comply with CSRD traceability clauses.

AI-native add-ons such as MAKIRA’s invoice-automation engine and Semine’s payables bot deliver targeted productivity gains, slashing approval cycles and freeing accountants for advisory tasks. Healthcare providers, exemplified by Terveystalo, bridge electronic health records with payroll and procurement systems to comply with reimbursement rules. This convergence of clinical, operational, and financial data broadens the addressable scope for the Nordic enterprise resource planning industry while deepening integration complexity that favors vendors with robust platform ecosystems.

By Deployment Model: Cloud Closes the Gap but On-Premise Persists

Although on-premises installations still account for 65.40% of deployed value, cloud deployments are driving the growth narrative with a 10.63% CAGR. Newly opened Azure regions in Norway and Sweden, plus Oracle’s EU sovereign cloud, help regulated buyers comply with Schrems II-driven key location mandates. Construction firm Veidekke and distributor BAMA Gruppen demonstrate the business case by migrating to national cloud regions that provide mobile access for field managers and real-time logistics visibility.

Nonetheless, high-risk healthcare facilities, defense contractors, and some university hospitals keep core ledgers on site pending clearer rulings on cross-border backups. Cost comparisons show that multiyear operating expenses for cloud reach parity with legacy maintenance only when workloads scale or real-time analytics features are activated. Hence, the Nordic enterprise resource planning market will exhibit hybrid patterns well into the next decade, with vendors upselling integration middleware and API gateways.

By Organization Size: SME Volume Meets Enterprise Scale

SMEs generate the bulk of license volume, translating into a dominant 70.20% share in 2025 and the fastest 10.94% CAGR. Low-priced, pre-localized suites from Visma, Fortnox, and Odoo shorten implementation from months to weeks, making it an attractive value proposition for firms with fewer than 250 employees. Conversely, large enterprises still anchor absolute revenue, combining best-of-breed ERP cores from SAP or Oracle with specialized human-capital and project modules. The Nordic enterprise resource planning (ERP) market is experiencing a clear bifurcation. Small and medium-sized enterprises (SMEs) are increasingly seeking turnkey services that bundle essential features such as banking APIs and payroll compliance rules. These solutions cater to their need for simplicity, cost-effectiveness, and ease of implementation.

On the other hand, large conglomerates are gravitating toward composable architectures that allow seamless integration with global finance hubs, enabling them to customize ERP systems to meet their complex operational requirements. This duality in demand is creating significant pressure on ERP vendors. They are now required to maintain both hyper-configurable product lines for large enterprises and highly opinionated, pre-configured solutions for SMEs. This dual approach not only raises development and operational costs but also necessitates strategic alliances with vertical specialists to address the unique needs of different customer segments effectively. As a result, the Nordic ERP market is witnessing increased competition and innovation, with vendors striving to balance scalability, customization, and cost-efficiency to cater to this diverse customer base.

By Industry Vertical: Manufacturing Leads, Healthcare Surges

Manufacturing sustained a 37.50% share in 2025, underpinned by machinery, automotive, and timber operations adopting IoT-enabled execution modules. Retail and e-commerce players are closely following with an 11.63% CAGR. Banks and insurers adopt cloud ERP for non-core functions, but remain measured due to capital adequacy data-flow restrictions. Healthcare, although smaller as hospital districts integrate electronic health records with finance to align procurement with reimbursement caps.

Sustainability disclosure drives both manufacturers and healthcare operators to track material and waste flows in real time. This trend is fueled by increasing regulatory requirements and the growing emphasis on environmental, social, and governance (ESG) factors. Case studies at Bjelin Group and the Ostrobothnia region illustrate measurable gains in audit readiness, operational transparency, and overall efficiency. These organizations have successfully leveraged enterprise resource planning (ERP) systems to streamline compliance processes and enhance decision-making capabilities. As the Corporate Sustainability Reporting Directive (CSRD) scope broadens, vertical specificity will weigh more than functional breadth when selecting platforms. This shift is expected to significantly influence sales cycles and vendor strategies across the Nordic enterprise resource planning market, as businesses prioritize tailored solutions that address industry-specific challenges and regulatory demands.

Geography Analysis

Sweden, representing 41.3% of 2025 spend, benefits from dense manufacturing corridors in Gothenburg, Västerås, and Linköping, where asset-heavy ERP features such as field service, maintenance planning, and carbon accounting are indispensable. Regulatory leadership on VAT digitalization and 90% population-level 5G coverage further accelerates cloud adoption. Denmark follows, supported by pharmaceutical, shipping, and food-processing clusters that favor enterprise-grade platforms designed for complex multi-entity consolidation. Procurement teams, however, are notably focused on security, prioritizing encryption key sovereignty over sustainability in recent tenders.

Norway's share of the Nordic enterprise resource planning market is steadily increasing as oil-and-gas supply chains modernize logistics and aquaculture firms adopt project accounting to manage floating assets. Microsoft's national cloud regions meet residency requirements, enabling Dynamics 365 to gain traction. Finland, while smaller in comparison, is experiencing rapid adoption in public-sector and healthcare segments, as demonstrated by the Lifecare rollouts serving a significant population. Iceland, though currently a smaller player, is recording the fastest growth as fishing cooperatives and tourism operators transition from legacy spreadsheets to off-the-shelf SaaS solutions.

Digital-infrastructure disparity influences deployment tactics. Urban Sweden and Norway leverage 5G standalone for shop-floor analytics, whereas Lapland, Finnmark, and the Icelandic highlands rely on edge nodes that sync intermittently.[4]Telia, “5G Standalone Network Rollout,” telia.se Continuous-transaction-control pilots in Sweden and Norway set the pace for compliance-driven demand, creating spillover opportunities for ERP vendors that can replicate successful tax-engine certifications across all five Nordic countries.

Competitive Landscape

The Nordic enterprise resource planning market remains moderately concentrated, with the top five vendors, SAP, Microsoft, Oracle, Visma, and IFS, holding 68.7% combined share in 2025. SAP has a moderate share through entrenched manufacturing installs and targeted sustainability modules. Microsoft holds a significant share, leveraging in-country Azure zones and frequently updated Dynamics 365 offerings that include Nordic payroll templates. Oracle remains a key player, preferred by tier-1 finance departments requiring multi-currency consolidation and benefiting from its EU sovereign cloud for data-residency compliance.

Visma’s market presence highlights the effectiveness of hyper-localized functionality at competitive price points, while IFS caters to asset-intensive industries with strong demand for field-service and maintenance solutions. Emerging challengers such as Done.ai, Semine, and MAKIRA illustrate a shift toward AI-native microservices that bolt onto established ledgers, often achieving straight-through processing rates of 75% or higher for accounts payable. Strategic acquisitions by Visma and Oracle expand vertical coverage, whereas SAP and Microsoft double down on co-innovation with hyperscalers to infuse generative AI into core workflows.

Data residency, ESG analytics, and depth of automation now top the evaluation criteria for enterprise resource planning (ERP) solutions in the Nordic market. With increasing regulatory scrutiny, vendors unable to guarantee EU-only key management or pre-configure Corporate Sustainability Reporting Directive (CSRD) metrics face significant risks of exclusion from procurement shortlists. This shift in priorities has prompted ERP providers to enhance their offerings to ensure compliance with stringent data protection and sustainability requirements. Additionally, the growing emphasis on sustainability reporting has led to the integration of advanced ESG analytics into ERP platforms, enabling businesses to track and report on their environmental, social, and governance performance more effectively.

Nordics Enterprise Resource Planning Industry Leaders

SAP SE

Microsoft Corporation

Oracle Corporation

Visma AS

IFS AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SAP reported Nordic customers are consolidating to fewer systems and prioritizing data sovereignty, spotlighting vendors that operate EU-domiciled data centers.

- February 2026: Royal Greenland chose SAP to modernize procurement, production, and finance across its seafood network, improving traceability for Marine Stewardship Council audits.

- February 2026: Done.ai announced SEK 441.3 million (USD 41.2 million) fiscal-2025 revenue after divesting its legacy ERP line to focus on AI-driven finance automation.

- February 2026: LiveFlow launched Flow, an AI-native ERP for multi-entity consolidation, targeting Nordic subsidiaries of global firms.

Nordics Enterprise Resource Planning Market Report Scope

The market is an integrated software system used by organizations to manage, automate, and coordinate core business processes across different departments within a single unified platform. It enables seamless information flow across functions such as finance, supply chain management, human resources, customer relationship management (CRM), procurement, manufacturing, and inventory management, helping organizations improve efficiency, decision-making, and overall operational control.

The Nordics Enterprise Resource Planning Market Report is Segmented by Type (Cloud-Native Suite, Mobile-First ERP, Social/Collaborative ERP, and Two-Tier/Edge ERP), Business Function (Finance and Accounting, Supply-Chain and Operations, Human Capital Management, Customer Relationship and Commerce, and Manufacturing Execution and Quality), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, Retail and E-commerce, BFSI, Government and Public Sector, IT and Telecom, Healthcare and Life Sciences, and Other Industry Verticals), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Native Suite |

| Mobile-First ERP |

| Social / Collaborative ERP |

| Two-Tier / Edge ERP |

| Finance and Accounting |

| Supply-Chain and Operations |

| Human Capital Management |

| Customer Relationship and Commerce |

| Manufacturing Execution and Quality |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Retail and E-commerce |

| BFSI |

| Government and Public Sector |

| IT and Telecom |

| Healthcare and Life Sciences |

| Other Industry Verticals |

| By Type | Cloud-Native Suite |

| Mobile-First ERP | |

| Social / Collaborative ERP | |

| Two-Tier / Edge ERP | |

| By Business Function | Finance and Accounting |

| Supply-Chain and Operations | |

| Human Capital Management | |

| Customer Relationship and Commerce | |

| Manufacturing Execution and Quality | |

| By Deployment Model | On-Premise |

| Cloud | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Industry Vertical | Manufacturing |

| Retail and E-commerce | |

| BFSI | |

| Government and Public Sector | |

| IT and Telecom | |

| Healthcare and Life Sciences | |

| Other Industry Verticals |

Key Questions Answered in the Report

How large will Nordic ERP spending become by 2031?

The Nordic enterprise resource planning market size is forecast to reach USD 2.76 billion by 2031, reflecting a 10.23% CAGR from 2026.

Which deployment model is gaining ground fastest?

Pure cloud instances are advancing at 10.63% CAGR as sovereign-cloud regions and subscription pricing overcome data-sovereignty and capital-expense barriers.

What segment currently leads by function?

Finance and accounting modules command 53.47% share and remain the primary purchase driver as VAT and ESG rules necessitate real-time compliance automation.

Which country shows the highest growth rate?

Iceland posts the fastest 10.3% CAGR as fishing, tourism, and renewable-energy firms replace spreadsheets with SaaS suites.

Who are the dominant vendors in the region?

SAP, Microsoft, Oracle, Visma, and IFS collectively hold 68.7% share, with SAP leading at 23.4% through entrenched manufacturing installs.

Page last updated on: