Molded Pulp Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

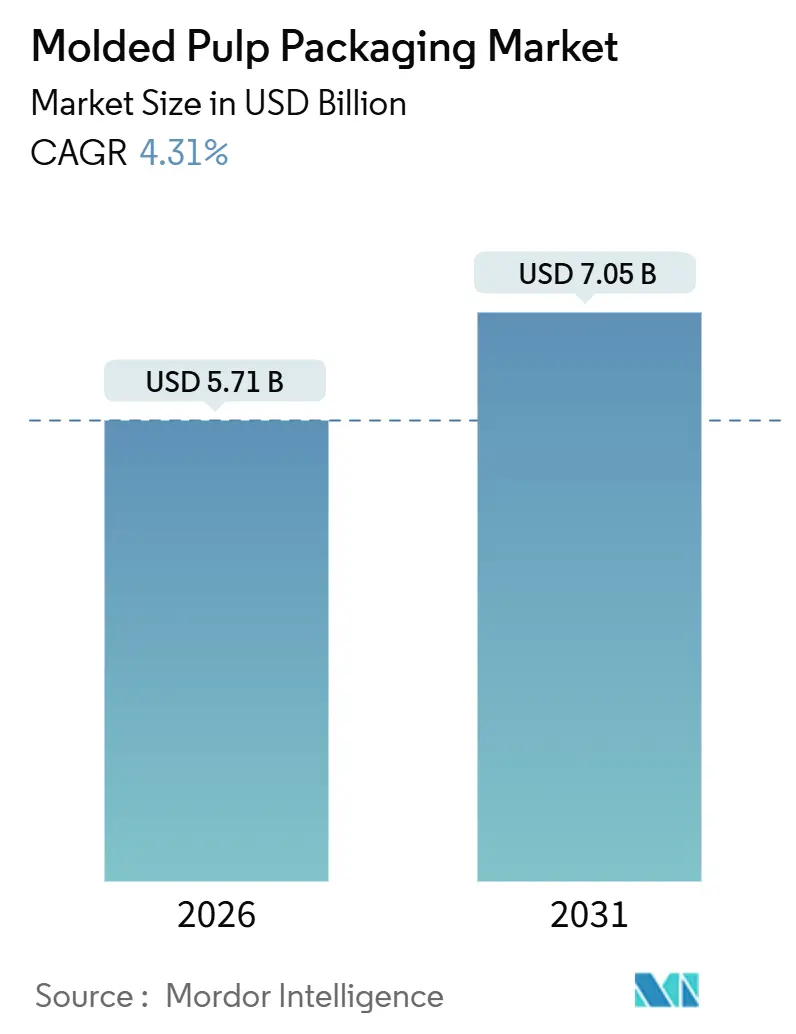

| Market Size (2026) | USD 5.71 Billion |

| Market Size (2031) | USD 7.05 Billion |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Molded Pulp Packaging Market Analysis by Mordor Intelligence

The molded pulp packaging market size stands at USD 5.71 billion in 2026 and is projected to reach USD 7.05 billion by 2031, advancing at a 4.31% CAGR. The growth trajectory is propelled by regulatory bans on single-use plastics in more than 100 countries, retailer scorecards that now rank recyclability ahead of unit cost, and rapid e-commerce expansion that favors curbside-recyclable protective fillers. Multinational brands are aligning with the European Union’s 2030 recyclability mandate and California’s SB 54 timeline, prompting suppliers to phase out polystyrene in favor of fiber-based alternatives[1]Source: European Commission, “Packaging and Packaging Waste,” ec.europa.eu. Technology leaps, including dry-molded-fiber processes that cut cycle time from minutes to seconds, are compressing the historical cost gap with injection-molded plastics. While recycled fiber anchors price competitiveness, blended formulations that pair recycled economics with virgin-fiber performance are accelerating, and geographic hot spots such as the Middle East are drawing fresh capital as local circular-economy targets gain momentum.

Key Report Takeaways

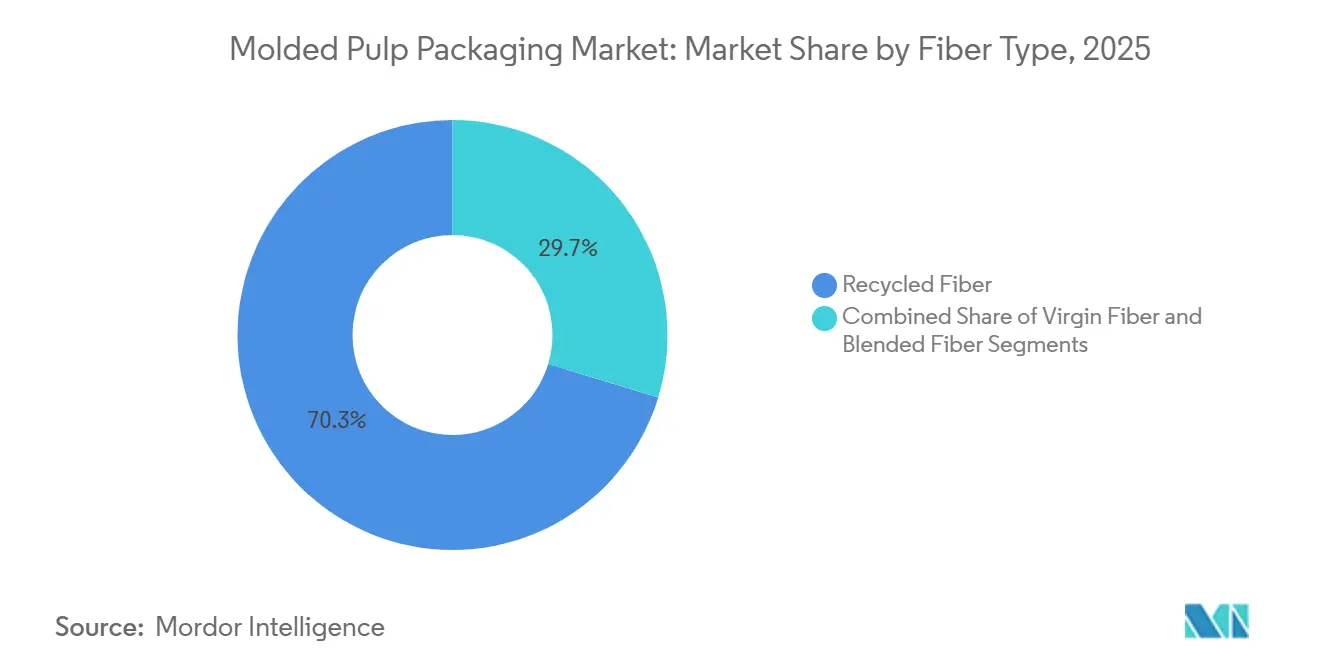

- Recycled fiber led with 70.3% molded pulp packaging market share in 2025, while blended fiber is forecast to expand at an 8.5% CAGR through 2031.

- Trays commanded 41.2% of 2025 revenue, whereas bowls and cups are projected to grow at 9.1% CAGR to 2031.

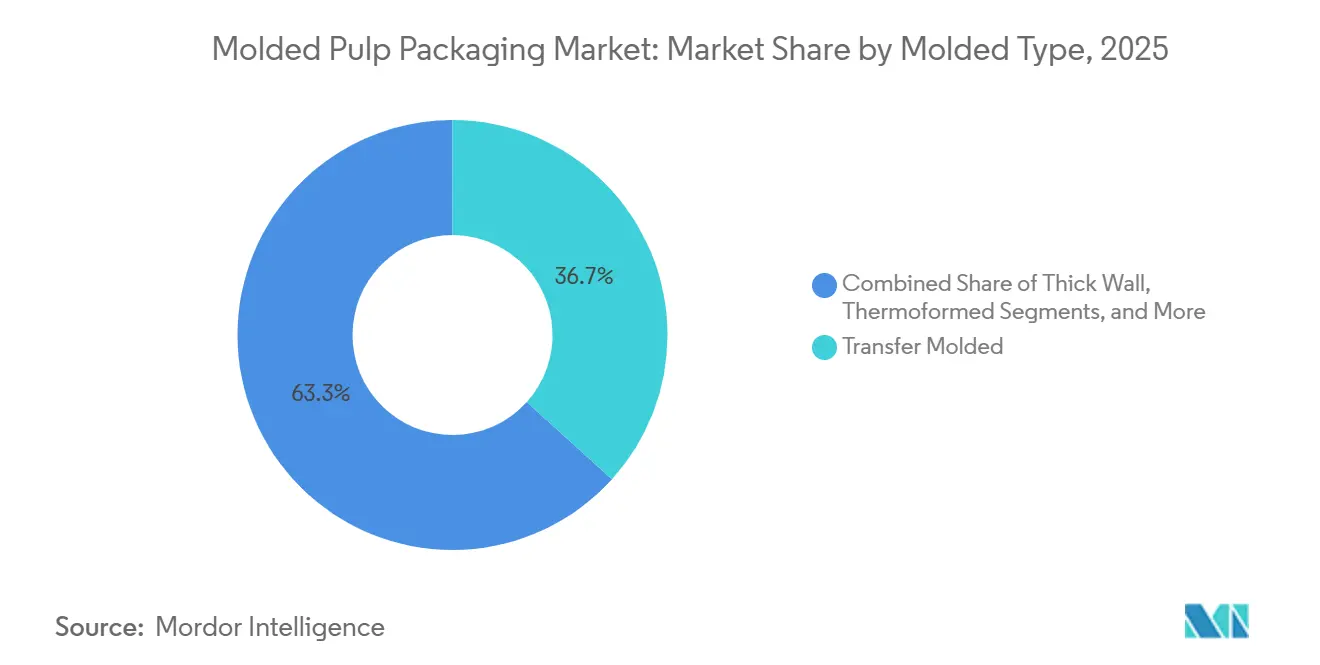

- Transfer molded technology captured 36.7% of 2025 volume, yet thermoformed molded pulp is on track for 7.24% CAGR through 2031.

- Food packaging accounted for 52.4% of demand in 2025, and healthcare and medical devices are poised to register an 8.6% CAGR.

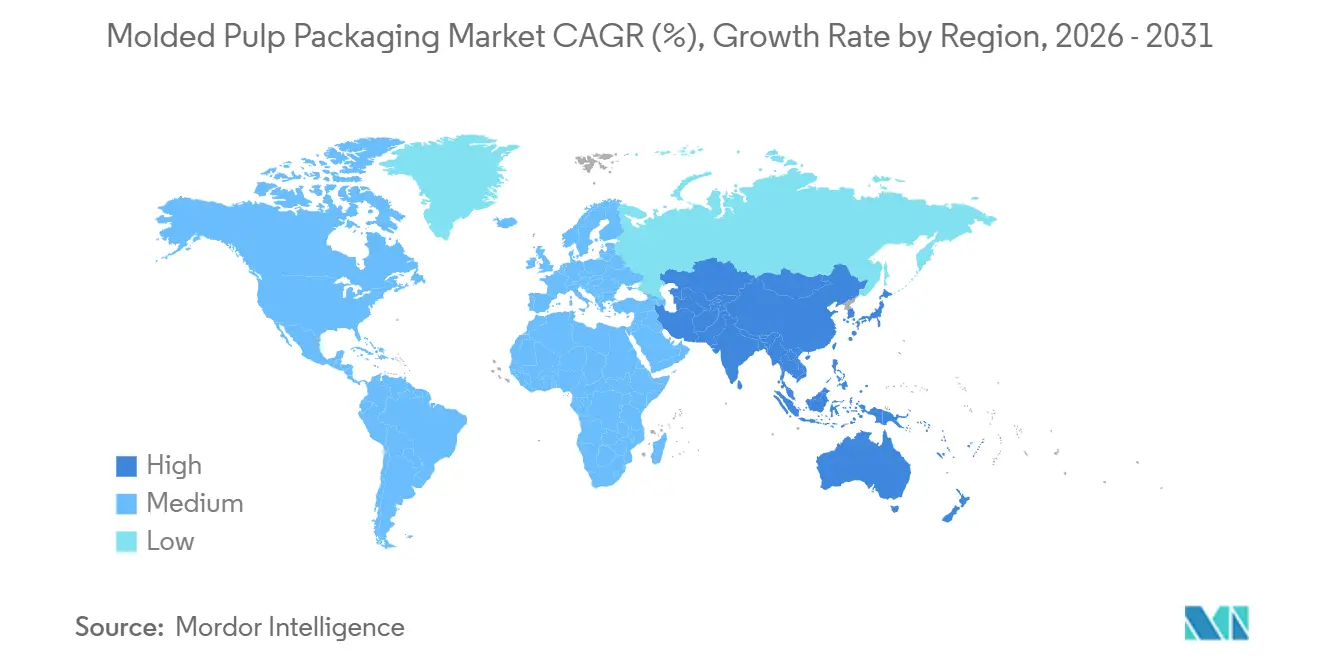

- North America contributed 46.56% of global sales in 2025, but the Middle East is expected to record an 8.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Molded Pulp Packaging Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on single-use plastics | +1.8% | Global, strongest in EU, North America, select Asia-Pacific | Medium term (2-4 years) |

| Corporate net-zero and plastic-neutral goals | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Cost advantage versus EPS and thermoformed | +0.7% | Global, especially South America and Asia-Pacific | Short term (≤ 2 years) |

| E-commerce demand for curbside-recyclable fillers | +0.9% | North America, Europe, Asia-Pacific e-commerce hubs | Short term (≤ 2 years) |

| Line-speed gains from dry-formed technology | +0.6% | North America and Europe first, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| PFAS-free legislation in foodservice | +1.0% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans On Single-Use Plastics

Legislation is redefining procurement priorities across the molded pulp packaging market. The European Union’s 2030 recyclability rule and California’s SB 54 both outlaw expanded polystyrene, instantly elevating molded pulp from cost-driven option to compliance necessity. India’s ban on 19 plastic items deepens demand in foodservice, while varying enforcement standards make multi-jurisdiction compliance complex. Integrated producers that command their own tooling and certification resources are best positioned to navigate divergent exemptions and accelerated timelines, reinforcing the market’s shift toward scale and vertical control.

Corporate Net-Zero And Plastic-Neutral Pledges

Retailer and brand commitments translate sustainability rhetoric into hard supplier mandates that favor the molded pulp packaging market. Unilever targets a 50% cut in virgin plastic, Walmart’s Project Gigaton embeds recyclable packaging in supplier scorecards, and Amazon’s frustration-free program removed millions of metric tons of plastic fillers. These cascading requirements compel contract packers to adopt molded pulp tooling even at a pricing premium because shelf access now hinges on ESG metrics, not just cents per unit.

Cost Advantage Versus EPS And Thermoformed Plastic

High virgin-plastic prices and landfill surcharges have widened the cost delta in favor of molded pulp, especially in price-sensitive South America and parts of Asia-Pacific. When feedstock is sourced locally, recycled-fiber trays can undercut expanded polystyrene by 10%, strengthening the molded pulp packaging market’s appeal to mass-market egg, produce, and consumer-electronics accounts. This cost edge supports penetration while technology upgrades continue to trim per-unit conversion expense.

E-Commerce Demand For Curbside-Recyclable Fillers

Record parcel volumes expose the shortcomings of peanuts and bubble wrap. Major carriers report that more than 90% of outgoing packaging is now curbside recyclable, a benchmark that molded pulp corner blocks and edge protectors comfortably meet. Although molded pulp can add 10-15% to unit cost, online retailers have shown willingness to absorb the premium to avoid penalties and preserve brand equity, reinforcing another structural tailwind for the molded pulp packaging market.

Restraints Impact Analysis of Molded Pulp Packaging Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of OCC and virgin fiber | -0.9% | Global, acute where recovered paper is imported | Short term (≤ 2 years) |

| Perceived poor barrier and print performance | -0.6% | Global, most visible in cosmetics and pharmaceuticals | Medium term (2-4 years) |

| Limited color-pulp recycling streams | -0.3% | North America and Europe where MRFs lack color separation | Long term (≥ 4 years) |

| High energy load during hot-press finishing | -0.4% | Regions with elevated electricity costs, notably Europe and parts of Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility Of OCC And Virgin Fiber

Fluctuating old-corrugated-container and softwood-pulp prices compress converter margins and complicate fixed-price contracts. Without hedging tools, many smaller players in the molded pulp packaging market absorb cost spikes that can push material expense up threefold within months. Vertical integration into paper trading, as executed by leading suppliers, is emerging as a key defense, yet regional producers remain exposed and occasionally shutter capacity, tightening supply just as demand surges.

Perceived Poor Barrier And Print Performance Versus Coated Plastic

Moisture-vapor transmission rates and print fidelity remain weaker than in coated plastics, limiting molded pulp usage in premium cosmetics, chilled ready meals, and pharmaceutical blister packs. Regulatory bans on PFAS have removed a low-cost barrier option, forcing converters to explore bio-polymer and water-based coatings that add expense and can complicate recycling streams. Until next-generation coatings mature, the molded pulp packaging market faces an innovation gap in the very segments that carry the highest margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Molded Pulp Packaging Market Segment Analysis

By Fiber Type:

Blended Formats Narrow The Performance GapBlended fiber formulations are projected to record an 8.5% CAGR through 2031, the fastest among fiber types, as converters balance recycled-fiber economics with virgin-fiber strength. Recycled grades controlled 70.3% of 2025 demand, reflecting mature supply chains and a 30-40% cost discount to virgin pulp. Yet brand owners seeking barrier performance for refrigerated or medical applications increasingly specify 60-40 blends, absorbing the surcharge to meet durability metrics. India’s pulp mills, already operating at 75% recycled content, showcase the scalability of recycled streams even in fast-growing economies. Conversely, virgin fiber retains a foothold in Class II medical packaging, where contamination risk is unacceptable, ensuring that all three fiber types coexist within the molded pulp packaging market.

Regional preferences differ. North American converters gravitate toward blended recipes to satisfy retailer sustainability audits without sacrificing carton strength, whereas Asian producers still favor recycled-only mixes to serve price-led foodservice demand. Vertical acquisitions that secure pre-sorted recycled feedstock enable higher recycled ratios without strength loss, giving integrated players a cost edge. As drying-energy cuts from emerging technology shrink processing overhead, the molded pulp packaging market size for blended products is expected to expand steadily, even as recycled grades remain the volume anchor.

By Product Type:

Bowls And Cups Ride Foodservice RecoveryTrays generated 41.2% of 2025 revenue, led by egg and produce applications, but bowls and cups are forecast to grow at 9.1% CAGR, outpacing every other product family. Quick-service restaurants in states with extended producer responsibility laws are shifting from polystyrene clamshells to molded pulp bowls and coffee lids, redirecting capital toward dedicated tooling lines. Clamshell volumes face pressure from nascent reusable-container pilots in Europe, whereas containers and lids gain from coffee-shop adoption of fiber-based covers that comply with polystyrene bans.

Foodservice survey data crowns molded pulp the “clear winner” among sustainable disposables, a sentiment that filters through purchasing portals of global chains. Compliance fees attached to single-use plastics have turned curbside recyclability into a bottom-line lever, accelerating conversion even when molded pulp commands a higher unit price. Awards for PFAS-free coatings validate new product lines and spur copy-cat launches, ensuring that bowls and cups remain the fastest-advancing slice of the molded pulp packaging market.

By Molded Type:

Thermoformed Technology Gains Precision AdvantageTransfer molded formats held 36.7% of 2025 volume on the strength of egg cartons and produce trays, yet thermoformed molded pulp is tracking a 7.24% CAGR to 2031, winning accounts in consumer electronics and cosmetics that demand tight tolerances. Thick-wall variants continue to serve industrial components where crush strength matters more than aesthetics, and processed slim-wall formats occupy high-value niches such as pharmaceutical blister inserts.

Major electronics brands report double-digit plastic reductions after switching to thermoformed fiber inserts that match the sleek form factors of high-end devices. Surface finish improvements coupled with denser footprints enable luxurious unboxing experiences that recycled corrugated could not achieve. As cycle times fall and defect rates shrink, the molded pulp packaging market sees a convergence of aesthetics, precision, and sustainability that erodes the final bastion of polystyrene in upscale packaging.

By End-User Industry:

Healthcare Segment Accelerates On Sterile-Barrier DemandFood packaging still comprised 52.4% of demand in 2025, but healthcare and medical devices are projected to log an 8.6% CAGR, the fastest among end users. Stringent ISO sterilization standards push converters toward virgin or blended fiber with ultra-low contaminant thresholds. PFAS bans further tilt hospitals away from coated plastics, opening a lane for thermoformed trays that can withstand autoclave cycles once thought exclusive to polymer formats.

Consumer electronics remain a second hot zone as sustainability targets cascade from headline brands to contract manufacturers, while personal-care adoption hinges on barrier-coating advancements. Industrial goods grow in line with manufacturing output but supply relatively stable volume that dampens cyclical swings. The resulting demand mosaic diversifies the molded pulp packaging market, buffering it against single-sector shocks and widening its strategic relevance across verticals.

Geography Analysis

North America Molded Pulp Packaging Market

North America captured 46.56% of global sales in 2025 thanks to early retailer mandates and state-level extended producer responsibility laws. Growth is moderating as egg and produce applications near saturation, yet policy tailwinds such as California’s 25% plastic-reduction rule keep the adoption curve positive. Canada’s ban on polystyrene foodservice ware and Mexico City’s compostability requirement echo U.S. shifts, sustaining regional momentum even as urban recycling programs mature.

Middle East Molded Pulp Packaging Market

The Middle East is set to post an 8.4% CAGR through 2031, the fastest worldwide. Saudi Arabia’s Vision 2030 targets and the UAE’s Circular Economy Policy have catalyzed large-scale local investments, including a USD 266 million plant aimed at displacing Asian imports. Upstream moves by regional containerboard producers secure feedstock, anchoring domestic supply chains that buffer against global pulp price spikes.

Europe, APAC, South America and Africa Molded Pulp Packaging Market

Europe benefits from the bloc-wide 2030 recyclability mandate, with Germany, France, and the United Kingdom at the forefront of molded pulp adoption in foodservice and retail. Asia-Pacific remains a mixed picture: India’s packaging boom, rising e-commerce penetration, and strict plastic-waste rules make it a demand engine, whereas several Southeast Asian nations still rely on cheap plastic amid under-developed recycling infrastructure[2]Source: India Brand Equity Foundation, “IBEF Homepage,” ibef.org. South America and Africa show patchier progress but register rising interest in molded pulp for quick-service restaurants and industrial exports as compliance costs for plastics escalate.

Regulatory Landscape

Regulation is tightening around packaging waste prevention, recyclability labeling, and restrictions on problematic materials, which is reinforcing substitution from expanded polystyrene and other single-use plastics toward fiber-based formats. In the European Union, Regulation (EU) 2025/40 on packaging and packaging waste (PPWR) entered into force on 11 February 2025 and applies from 12 August 2026, creating an enforcement timeline packaging producers and brand owners need to align across member states.

Food-contact compliance and chemical restrictions continue to shape molded pulp specifications, particularly for foodservice and healthcare trays where barrier solutions and additives are scrutinized. In the United States, molded pulp used for food contact must comply with the FD&C Act framework and applicable FDA clearances for paper and paperboard components (for example, 21 CFR 176.170 for aqueous and fatty foods), and the FDA Food Contact Substance Notification (FCN) system provides a route for specific cellulose-based additives and coatings used in fiber packaging structures.

Value Chain Analysis

The value chain starts with fiber sourcing (old corrugated containers and mixed recovered paper, plus virgin pulp where hygiene or performance requires it), then stock preparation, forming (thick-wall, transfer molded, thermoformed, or processed/slim-wall), and energy-intensive drying and hot-press finishing. Converters then add functional layers such as water-based or biopolymer coatings, quality testing (including food-contact and healthcare requirements), and packaging design and tooling before products move through distributors, contract packers, and brand-owner procurement into food packaging, foodservice, consumer electronics, and medical channels.

Recent activity points to tighter collaboration across material science, forming technology, and brand commercialization. Amcor and Metsa Group partnered (May 2025) to develop 3D molded fiber food packaging with high-barrier film liners, while SIG and PulPac (July 2025) launched a program to scale Dry Molded Fiber paper-based closures for aseptic cartons. Stora Enso and Matrix Pack formed a strategic partnership (June 2025) including a minority stake to scale formed-fiber technologies, and PulPac collaborated with Future Materials Sweden (November 2025) to advance fiber-based packaging solutions, reflecting how technology licensing and joint development are being used to shorten scale-up cycles and improve functional performance.

Competitive Landscape

The molded pulp packaging market retains moderate fragmentation; the top five suppliers hold roughly 35-40% of capacity, leaving space for regional specialists and technology entrants. Vertical integration dominates strategic agendas, evidenced by paper-trading acquisitions that shelter converters from recycled-fiber price swings. Capital outlays in North America and Europe are automating high-speed lines and consolidating regional egg-carton capacity, while cross-border deals in Asia-Pacific expand manufacturing footprints.

Technology licensing accelerates time-to-market for disruptive processes. Dry-molded-fiber lines installed in the United States, Sweden, and Malaysia slash cycle times, achieving near parity with thermoforming and opening premium categories such as cosmetics caps and coffee lids. Healthcare-grade trays remain a white-space opportunity; converters that pair virgin fiber with PFAS-free coatings and ISO-certified sterile-barrier performance can command premium margins.

Consolidation in broader packaging signals that scale is becoming a prerequisite. Multibillion-dollar mergers in containerboard and plastic packaging tighten feedstock control and broaden product portfolios, positioning conglomerates to bundle molded pulp with folding cartons or flexible films in integrated bids. Niche innovators continue to address color separation, energy-efficient hot-pressing, and digital printing, ensuring that the competitive landscape evolves on both volume and technology fronts.

Molded Pulp Packaging Industry Leaders

Brødrene Hartmann A/S

Huhtamaki Oyj

UFP Technologies, Inc.

Sabert Corporation

Sonoco Products Company

- *Disclaimer: Major Players sorted in no particular order

Molded Pulp Packaging Market Companies Covered in this Report

- Brodrene Hartmann A/S

- Huhtamaki Oyj

- UFP Technologies, Inc.

- Sabert Corporation

- Henry Molded Products, Inc.

- Keiding, Inc.

- Pacific Pulp Molding, Inc.

- Protopak Engineering Corporation

- EnviroPAK Corporation

- Maspack Ltd.

- CKF Inc.

- Moulded Fibre Products Ltd.

- Cellulopack Packaging S.L.

- FiberCel Packaging, LLC

- Greenpack (Yulin) Environmental Technology Co., Ltd.

- Dongguan Flyway Packaging Co., Ltd.

- Shenzhen Maider Packaging Co., Ltd.

- Qingdao Xinya Molded Pulp Packaging Co., Ltd.

- Taiwan Pulp Molding Co., Ltd.

- Nippon Molded Pulp Co., Ltd.

- Vegware Ltd.

- Earthpac Ltd.

- Papelyco S.A.

- PulpaPack SAS

- Western Pulp Products Co.

Market Opportunities and Future Outlook

White space is opening in high-speed, high-volume molded fiber formats where conversion has been constrained by cycle time, tooling lead times, and barrier performance. Industrial demonstrations and commercialization programs around dry-forming and Dry Molded Fiber provide concrete entry points: Fiberdom and Kiefel reported an industrial-speed demonstration on the Natureformer KFD 75 with output potential exceeding 80 million units annually per line (July 2026), and HZ Green Pulp partnered with Hotpack Global to commercialize Dry Molded Fiber coffee lids (June 2026). These initiatives track end uses that are already shifting away from polystyrene and other restricted single-use plastics, especially lids, trays, and protective inserts that need tighter tolerances.

Another opportunity comes from reducing customization friction for e-commerce and protective packaging. Specialized Packaging Group introduced EcoFlex (May 2026), a custom molded pulp concept built from modular square components laminated onto corrugated structures, positioned to eliminate traditional tooling and cut production timelines by 75-80%. Moorim P&P referenced a Korea facility operating at 10 million units per month for pulp molds using internally sourced raw pulp (April 2026), which supports scale economics when capacity additions align with pulp supply. IMFA-referenced survey results also indicate 74% of surveyed manufacturers planned capacity expansions within two years (2026), signaling an active build-out cycle that can expand application scope, assuming the resulting products also meet food-contact and PFAS-related compliance requirements in key geographies.

Recent Industry Developments in Molded Pulp Packaging Market

- May 2026: Huhtamaki collaborated with Hesburger to supply customized plant-based fiber lids produced at its Foodservice site in Alf, Germany, for hot and cold beverages. The rollout is framed around measurable plastic reduction (41,000 kg annually cited by Hesburger), supporting brand procurement shifts toward fiber lids where regulatory and retailer scorecards prioritize recyclability.

- April 2025: Huhtamaki acquired Zellwin Farms, an egg carton and egg flat molded fiber manufacturer in Zellwood, Florida, for an enterprise value of USD 18 million. The deal strengthened Huhtamaki's molded fiber footprint in North America and added capacity aligned to high-volume egg packaging demand.

- October 2024: Huhtamaki commenced smooth molded fiber production at its Lurgan, Northern Ireland site following its fiber-lid capacity expansion. Adding SMF capability supports higher-precision fiber formats for foodservice lids and helps shorten lead times for customers seeking alternatives to plastic closures.

Molded Pulp Packaging Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers molded pulp packaging products made from fiber pulp that are formed into rigid or semi-rigid protective and food contact shapes, and sold as finished packaging items across major end uses.

Scope exclusions: Excluded from this sizing are loose fill cellulose, plain bagasse dinnerware, and un-molded fiber pads that are not formed into molded packaging.

Segments Covered in This Report

- By Fiber Type

- Recycled Fiber

- Virgin Fiber

- Blended Fiber

- By Product Type

- Trays

- Bowls and Cups

- Clamshells

- Plates

- Containers and Lids

- Other Product Types

- By Molded Type

- Thick Wall

- Transfer Molded

- Thermoformed

- Processed / Slim Wall

- By End-User Industry

- Food Packaging

- Foodservice

- Consumer Electronics

- Healthcare and Medical Devices

- Industrial Goods

- Personal Care and Cosmetics

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the demand pool for molded pulp packaging and then checking how it connects to paper and packaging production, trade, and end market activity. Public sources are used to anchor the model, including US EPA materials and recycling facts, FAOSTAT pulp and paper supply indicators, UN Comtrade trade codes for pulp and paper articles, and International Energy Agency energy and industry series that help explain mill output swings.

We also rely on annual reports, investor decks, and earnings call notes to understand capacity adds, pricing language, and mix shifts, followed by packaging association publications and well-regarded press coverage to confirm adoption themes. When needed, paid subscriptions for company financials and intelligence, an import-export shipment-level database, and patent databases are used to cross-check where production is happening and which forming technologies are being commercialized. These examples are not exhaustive, and we referred to additional sources during data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary discussions were used to translate broad fiber packaging signals into molded-pulp specific assumptions, especially average selling prices, resin to fiber substitution points, and the adoption pace of thermoformed and processed slim wall formats. We spoke with packaging producers, converters, distributors, and large buyers, then checked the logic with contacts close to foodservice, electronics protective packaging, and healthcare packaging demand across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 41% |

| Mid tier: 53% | Functional/Unit leaders: 40% | EMEA: 34% |

| Smaller Players: 20% | Managers: 45% | Americas: 25% |

Market-Sizing & Forecasting

The sizing starts with a top-down build where paper pulp availability, packaging output indicators, and end use demand signals are used to reconstruct how much packaging spend can realistically sit in molded pulp formats. After that, we corroborate totals using selective bottom-up checks, including rolling up sampled producer revenues where available, and validating volume by product categories using approximate units times typical price bands.

Key inputs that shape the model include fiber input mix (recycled, virgin, and blended), product mix across trays, clamshells, bowls and cups, and containers and lids, and the split by molded type (thick wall, transfer molded, thermoformed, and processed or slim wall). We also track demand markers like food packaging and foodservice activity, electronics shipment trends that drive protective packaging, and policy or retailer scorecard pressure that accelerates substitution away from plastic. Where company disclosures are incomplete, gaps are handled using capacity ranges, utilization assumptions from interviews, and conservative conversion factors that are then tested against trade and production signals.

For forecasting, scenario analysis is used because pricing and mix can shift quickly with pulp costs, energy costs, and capacity expansions. The base case is tuned using expert views on ASP progression, adoption speed of faster-cycle technologies, and the timing of major end user conversion programs, then checked for reasonableness against historical trendlines.

Data Validation & Update Cycle

Validation is done in several passes so the final number is not driven by one data stream. We compare the modeled totals with independent signals like packaging production direction, trade movement, and end market activity, then investigate any large variances before sign-off.

If a key assumption shifts, such as pulp pricing, capacity additions, or regulatory enforcement timing, we re-contact relevant experts and re-run the affected parts of the model. Reports are refreshed annually, with interim updates when material events can change near-term demand or pricing. Before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Molded Pulp Packaging Market Estimate Compared With Other Published Estimates

Published market sizes can differ even when studies are focused on molded pulp packaging, because refresh timing, currency conversion windows, and pricing logic are not always aligned. Some studies also lean on a single demand proxy, which can miss mix shifts between thick wall and thermoformed formats.

In our work, the model is kept current through regular checks on pulp cost direction, technology adoption signals, and end user conversion programs. The sizing is rebalanced when ASP assumptions or currency timing move materially, which is why the 2026 figure from Mordor Intelligence can land away from estimates that keep older price bands fixed.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.71 B (2026) | |

| Global Research Publisher A | USD 6.21 B (2025) | Uses a different base year and a broader segmentation frame by pulp source and applications, and the earlier year can reflect a different pricing environment and currency window than a 2026 anchored model. |

| Industry Research Publisher B | USD 5.54 B (2025) | Reports a 2025 base and a longer forecast horizon, and the estimate appears more sensitive to fixed price progression assumptions that may not fully adjust for short-term pulp and energy cost swings. |

The spread is mainly explained by timing and pricing choices rather than a disagreement on the core adoption direction. By linking the value build to observable end use activity, molded type mix, and refreshed ASP bands, the approach stays traceable to clear inputs and can be repeated when new public signals emerge.

Key Questions Answered in the Report

How large is the molded pulp packaging market in 2026?

The molded pulp packaging market size is USD 5.71 billion and is forecast to reach USD 7.05 billion by 2031.

Which end-user sector is growing fastest for molded pulp?

Healthcare and medical devices lead with an anticipated 8.6% CAGR thanks to sterile-barrier requirements and PFAS bans.

What technology is disrupting molded-pulp production cycles?

Dry-molded-fiber lines cut forming times from minutes to seconds, narrowing the cost gap with injection-molded plastics.

Which geography is projected to expand most rapidly?

The Middle East is forecast to register an 8.4% CAGR to 2031, propelled by Saudi Arabia’s Vision 2030 and UAE circular-economy policies.

Page last updated on: