Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

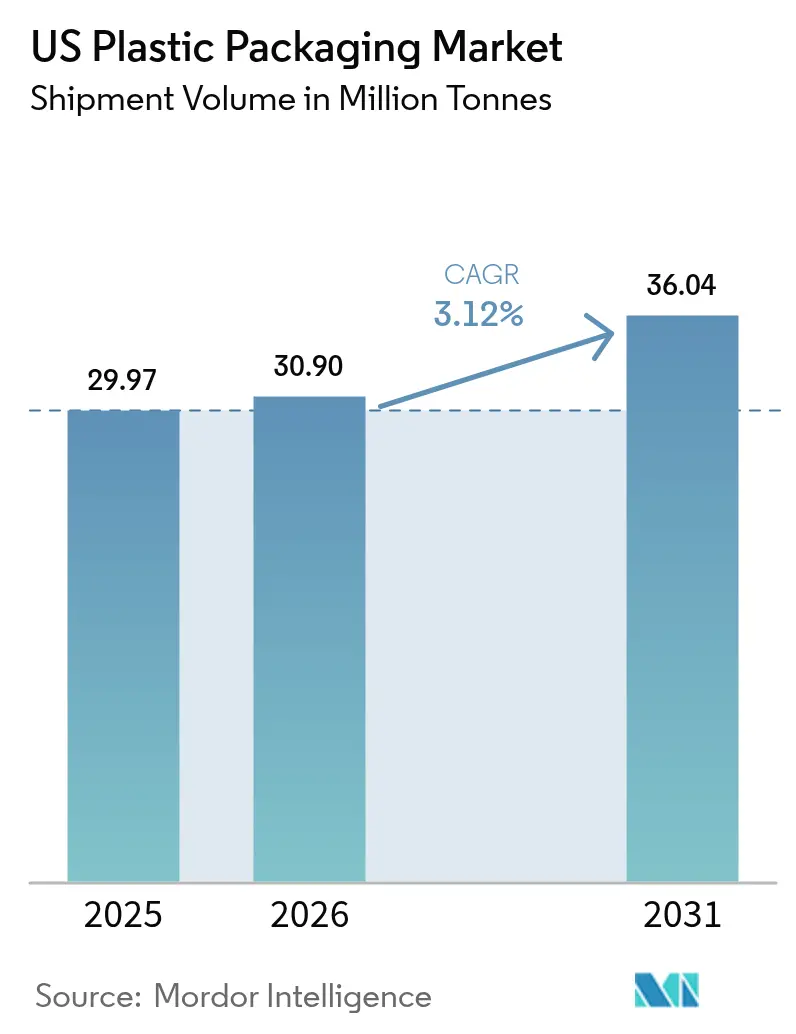

| Base Year Market Size (2025) | 29.97 Million tonnes |

| Market Volume (2026) | 30.9 Million tonnes |

| Market Volume (2031) | 36.04 Million tonnes |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Plastic Packaging Market Analysis by Mordor Intelligence

The United States plastic packaging market size in 2026 is estimated at 30.9 million tonnes, growing from 2025 value of 29.97 million tonnes with 2031 projections showing 36.04 million tonnes, growing at 3.12% CAGR over 2026-2031. Demand resilience comes from e-commerce parcel expansion, food and beverage convenience formats, and brand owner commitments to integrate 25% post-consumer recycled (PCR) resin into core stock-keeping units. Regulatory frameworks such as California SB 54 and Washington State’s recycled-content law are accelerating design shifts toward lighter gauges, mono-material laminates, and tethered closures. Adoption of FDA-cleared rPET, rHDPE, and rLLDPE has begun closing the feed-stock gap, while robotics installations—1,646 new units added by plastics molders in 2023—are streamlining throughput and raising quality yields within the United States plastic packaging market.

Key Report Takeaways

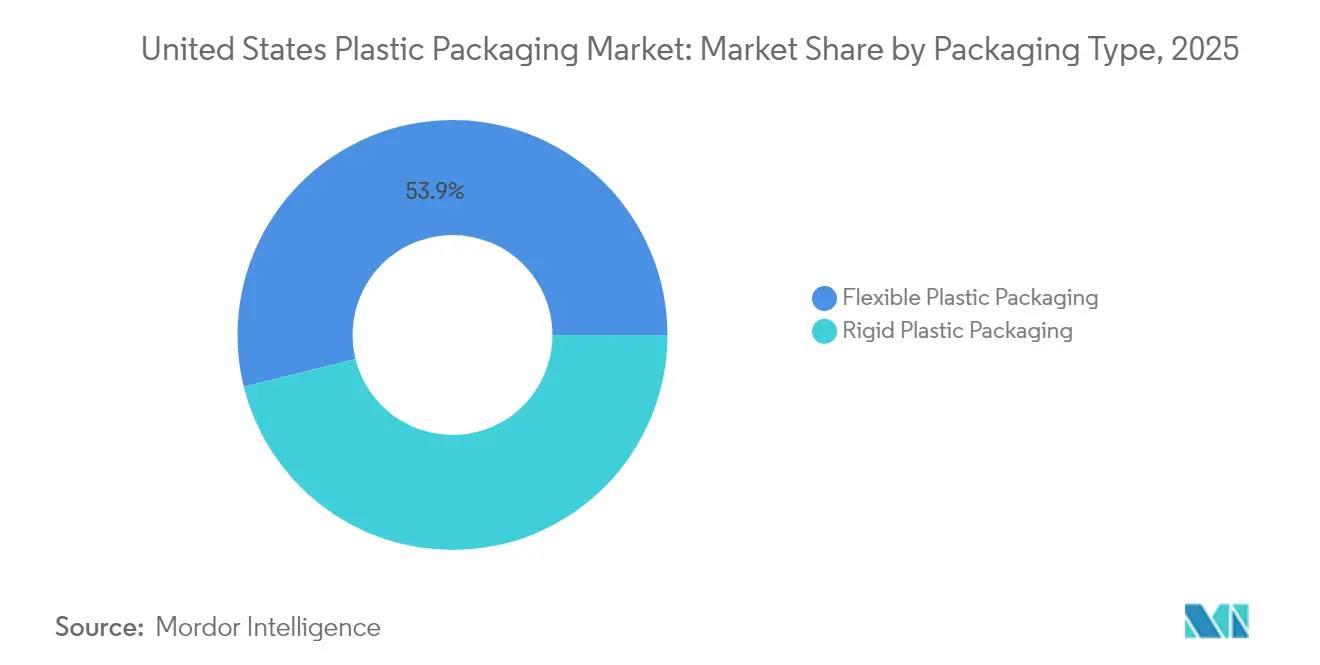

- By packaging type, flexible formats held 53.86% of the United States plastic packaging market share in 2025, and this segment is advancing at a 4.82% CAGR to 2031.

- By material type (flexible), polyethylene contributed 45.12% in 2025, whereas the “other materials” cluster records the fastest 6.09% CAGR through 2031.

- By material type (rigid), polyethylene captured 33.95% share in 2025, while specialty resins and bio-polymers rise at 5.71% CAGR.

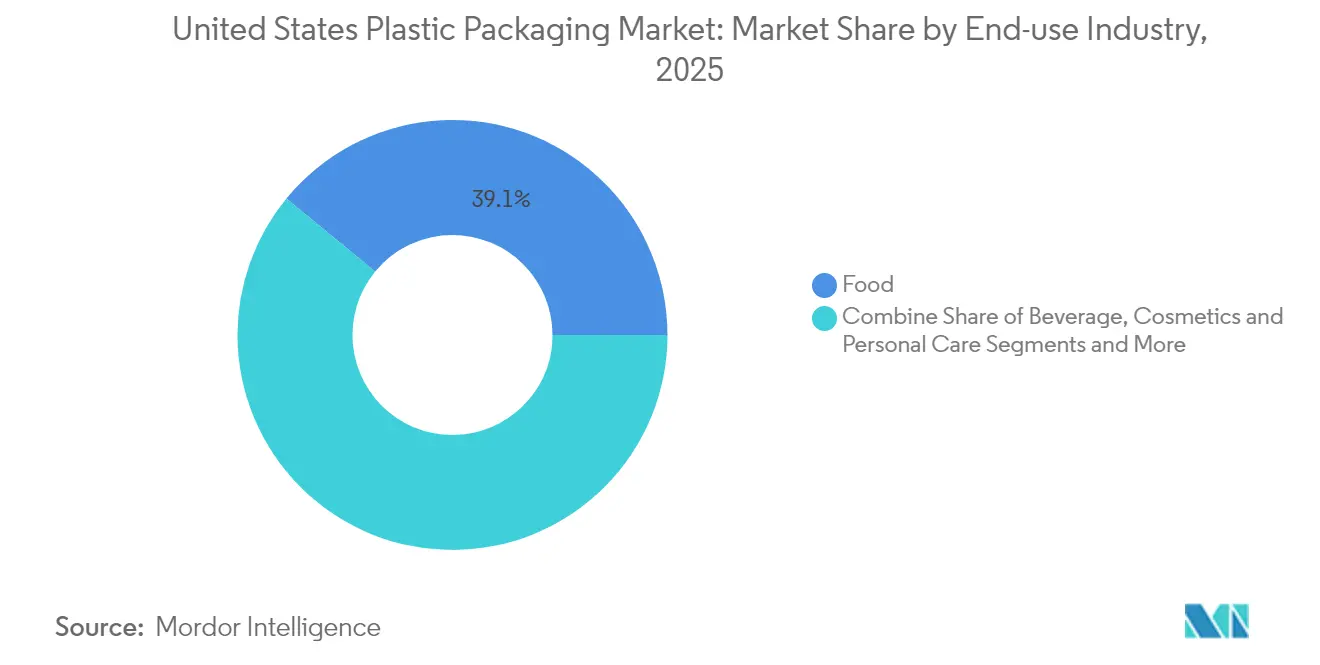

- By end-use industry, food commanded 39.05% of the United States plastic packaging market size in 2025; cosmetics and personal care is expanding fastest at 6.74% CAGR to 2031.

- By packaging technology, extrusion produced 38.42% of 2025 revenues, while thermoforming is set to accelerate at 6.69% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging e-commerce demand for lightweight protective mailers | +0.7% | National, urban logistics hubs | Short term (≤ 2 years) |

| Rapid adoption of recyclable mono-material pouches | +0.9% | National, coastal states first | Medium term (2-4 years) |

| Growth of ready-to-eat and on-the-go foods | +0.6% | National, metro areas | Medium term (2-4 years) |

| Pharmaceutical cold-chain expansion | +0.4% | Pharma corridors | Long term (≥ 4 years) |

| Corporate mandates for 25% PCR content | +0.5% | States with recycled-content laws | Medium term (2-4 years) |

| Investments in advanced digital printing | +0.3% | Innovation-focused regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Recyclable Mono-Material Pouches by US CPG Brands

Mono-material polyethylene and polypropylene laminates are replacing mixed-substrate films that once obstructed recycling streams. Converters now deliver heat-resistant, high-barrier pouches that comply with the U.S. Plastics Pact 2025 design targets, giving brand owners a straightforward route to “recycle-ready” claims. DNP Indonesia’s commercial roll-out of mono-material snack and pet-food packs demonstrates how barrier performance can be maintained while simplifying end-of-life processing. Retailers request specification parity with legacy foil structures, and test data confirm comparable oxygen-transmission rates, enabling broad SKU conversion. Packaging teams within the United States plastic packaging market are synchronizing material down-gauging with roll-stock width optimization to shrink film consumption per unit.

Surging E-Commerce Demand for Lightweight Protective Mailers in the US Parcel Network

Parcel shippers continue to eliminate unnecessary void fill, driving interest in thin-gauge, curbside-recyclable mailers that cut dimensional-weight fees while preserving product integrity. Amazon has shifted one-third of its U.S. outbound parcels to paper-based alternatives, eliminating 15 billion plastic air pillows since program inception. The company’s pilot plants validate line speeds exceeding 250 parcels per minute, setting new benchmarks for automation. Competitors are matching performance with mono-material LDPE bubble mailers containing 30% PCR, as mandated by Washington’s recycled-content law. Converters positioned within the United States plastic packaging market are investing in high-output blown-film towers and automated wicketing to address the spike in daily parcel volumes.

Growth of Ready-to-Eat and On-the-Go Foods Requiring High-Barrier Flexible Films

Demand for convenient meal kits, chilled entrées, and shelf-stable snacks is lifting multilayer barrier film volumes. Pressure-assisted thermal sterilization (PATS) lines rely on EVOH-based or metal-oxide-coated structures with oxygen-transmission rates below 0.2 cc/m²-day, doubling shelf life for low-acid entrées compared with legacy retort pouches.[1]Food Research International, “High-Barrier Multilayer Polymer Films for Pressure-Assisted Thermal Sterilization,” sciencedirect.com Brand owners report food-waste reductions of 15-18% in test markets, strengthening the value proposition for advanced barriers. Fabricators inside the United States plastic packaging market are combining five-layer co-extrusion with in-line corona treatment to support direct-print surfaces, cutting lamination steps and enabling faster artwork changes. Retail buyers increasingly mandate “store drop-off” recyclability, which favors mono-family structures over foil laminations.

Corporate Commitments to 25% PCR Content Boosting Demand for rPET and rHDPE Bottles

Multinational beverage and home-care producers have pledged to integrate 25% PCR across U.S. portfolios by 2025, lifting demand for food-grade rPET and rHDPE beyond domestic reclaim capacity. FDA clearances for Borcycle M rHDPE and SYNDIGO rLLDPE prove 100% PCR is achievable in select dry-food and flexible applications.[2]Borealis, “FDA Clears Borealis Borcycle M Recycled Plastics for Use in Food-Grade Packaging,” borealisgroup.com Washington State’s statute phases PCR minimums to 50% by 2036, reinforcing procurement stability for infrastructure investors. Price premiums for rPET flake reached 25–30% above virgin in 2025, yet converters report high contract renewal rates because corporate scorecards link PCR progress to C-suite incentives. The United States plastic packaging market thus faces a feed-stock race that rewards vertically integrated reclaimers and brand-owned closed-loop systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State-level single-use plastics bans | −0.5% | Coastal states | Medium term (2-4 years) |

| Polyolefin resin price volatility | −0.3% | National | Short term (≤ 2 years) |

| Consumer shift to paper / aluminum | −0.4% | Eco-conscious metros | Medium term (2-4 years) |

| Capital intensity of chemical recycling | −0.2% | Limited to sites with large-scale projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating State-Level Single-Use Plastics Bans Reducing Certain Packaging Formats

California SB 54 mandates a 25% reduction in virgin plastic packaging sold within state borders by 2032, and producers must join a Producer Responsibility Organization by 2025. Similar mandates in New Jersey, Colorado, and Maine create a fragmented compliance map that raises complexity for nationwide brands. Converters are pre-emptively retiring PS clamshells and PVC blisters from their catalogs, turning to PET G and coated paperboard alternatives even when cost of goods rises. The regulatory uncertainty embeds risk premiums into long-term supply contracts, curbing discretionary capital spend within the United States plastic packaging market as firms await harmonized federal guidelines.

Consumer Shift Toward Paper and Aluminum Alternatives for Sustainability

Rising eco-consciousness among millennials and Gen Z buyers is prompting retailers to pilot fiber-based and aluminum refill formats. The State University of New York system’s pledge to phase out single-use plastics underscores a broader institutional pivot toward alternative substrates. [3]State University of New York, “Phase-Out of Single-Use Plastics,” suny.edu Source: Packaging News, “Packaging Innovations 2025: Big-Name Brands to Make Waves,” packagingnews.co.uk EP Group’s RePapaPac kraft carrier holds 20 kg yet remains kerbside recyclable, illustrating functional parity that pulls volume from LDPE t-shirt bags. Within the United States plastic packaging market, brand teams hedge risk by trialing hybrid packs—paper shells with thin PE liners—that satisfy barrier requirements while signalling sustainability credentials on shelf.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Flexible Dominance Accelerates Innovation

Flexible formats delivered 53.86% of United States plastic packaging market share in 2025 and are marching ahead at a 4.82% CAGR. Each new pouch replaces rigid counterparts with 60-70% less polymer, reducing freight emissions and warehouse footprints. E-commerce giants favor flat mailers because they collapse to one-tenth the inbound cube of corrugated boxes, slashing storage overhead. Brands now employ near-infrared (NIR) readable inks so flexibles sort efficiently at material-recovery facilities, improving real recycling rates. Meanwhile, “smart” pouches embed RFID or NFC tags, providing end-to-end visibility from filler to consumer scanning events.

Rigid plastics still account for essential roles in beverages, pharmaceuticals, and household chemicals, yet growth lags at 2.03% CAGR. Lightweight HDPE bottles use up to 12% less resin than 2023 designs, but performance thresholds on drop strength and taste neutrality limit further down-gauging. Washington State’s recycled-content law compels bottle makers to secure stable rHDPE streams, prompting co-investment in in-house wash lines. Competition within the United States plastic packaging market now revolves around tethered caps that comply with forthcoming closure-retention mandates, merging convenience and litter reduction.

By Material Type (Flexible Packaging): PE Leadership Amid Sustainability Innovation

Polyethylene retained a 45.12% share of flexible volumes in 2025, supported by its broad processing window and robust curbside collection infrastructure. FDA approval for 100% rLLDPE content in snack wrappers confirms food-safety compliance pathways, allowing national retailers to launch “circular” private labels. Development teams adopt metallocene catalysts that provide higher dart impact at reduced gauge, contributing to resin savings of 8-10%. The United States plastic packaging market size for PE-based flexibles will continue scaling as co-extrusion technology accommodates recycled pellet variability without compromising film clarity.

The “other materials” category advances 6.09% CAGR, propelled by compostable PLA blends, cellulose-based films, and silicium-oxide coated papers. Consumer brands experiment with bio-PE derived from sugarcane that offers equivalent mechanical properties and a lower carbon footprint. BOPP remains indispensable for glossy snack and confectionery overwraps, yet new varnish systems deliver metallization-free barrier performance aligned with mono-material recycling guidelines. Partnerships between resin suppliers and film converters accelerate qualification cycles, shortening time-to-market for emerging formulations.

By Material Type (Rigid Packaging): PE Dominance Despite Diversification Pressures

High-density PE bottles, jugs, and caps claimed 33.95% share in 2025, anchored by dairy, motor oil, and detergents. Borcycle M technology unlocks 100% PCR use in dry-food containers, letting supermarkets promote closed-loop cereal dispensers and bulk goods sections. Brands also standardize color master-batch selections, enabling clearer optical sorting of natural and white streams that fetch higher bale revenues. The United States plastic packaging market size for rigid PE is forecast to surpass 5.7 million tonnes by 2031.

Specialty resins led by clarified PP, cyclic olefin polymer (COP), and PET-G are accelerating at 5.71% CAGR on the back of pharma, nutraceutical, and prestige beauty applications. COP syringes tolerate −70 °C storage required for mRNA drug shipping, while clarified PP jars deliver glass-like clarity without shatter risk. CleanStream mechanical recycling now feeds yogurt and margarine tub production, removing odor-causing contaminants and broadening food-grade PP’s reach. Design engineers inside the United States plastic packaging market weigh resin selection on both performance and policy alignment, anticipating stricter extended producer-responsibility fees on low-recycling-rate polymers.

By End-use Industry: Food Leadership with Cosmetics Surge

Food applications held 39.05% of United States plastic packaging market share in 2025 as barrier pouches, thermoformed trays, and lidding films supported shelf-stable, frozen, and chilled ranges. Plant-based meat analogues require high-oxygen-barrier film to prevent product browning, prompting co-extruders to incorporate EVOH layers as thin as 3 µm without sacrificing recyclability. High-pressure processing (HPP) ready meals leverage flexible trays that withstand 87,000 psi pulses, extending chilled shelf life by 60 days and opening new direct-to-consumer distribution routes. Retailers report 15–18% shrink reduction post roll-out, validating the cost premium of advanced films.

Cosmetics and personal care expand at 6.74% CAGR to 2031, buoyed by premiumization and refill trends. Nanocellulose-reinforced PLA compacts weigh 25% less than legacy ABS housings yet convey luxury haptics, helping prestige brands meet carbon goals without aesthetic compromise. Digital print lines deliver 5-color metallic effects in batches of 1,000 units, allowing indie labels to refresh artwork monthly. Within the United States plastic packaging market, refill-ready HDPE deodorant sticks and mono-material droppers resonate with zero-waste advocacy groups, creating upsell opportunities in refill pods and pouches.

By Packaging Technology: Extrusion Leads Manufacturing Innovation

Extrusion accounted for 38.42% of 2025 revenues, reflecting its versatility in blown-film, cast-film, and profile outputs. Five-layer air-ring towers equipped with gravimetric dosing can run up to 30% PCR without gauge variation, cutting scrap below 2%. Co-extruded tie layers compatible with solvent-free adhesive systems eliminate secondary lamination, streamlining lead times. Real-time thickness mapping feeds machine-learning algorithms that automatically fine-tune heater zones, reducing energy use by 7% compared with 2023 baselines within the United States plastic packaging market.

Thermoforming posts a brisk 6.69% CAGR to 2031 as demand for lightweight protein trays, dual-ovenable pans, and salad bowls grows. Inline forming-and-sealing systems operate at 55 cycles per minute, lowering touchpoints and minimizing micro-perforations. Injection-compression technology gains favor in cap and closure production, achieving tight tolerances with lower clamping forces and energy consumption. Single-stage PET stretch-blow lines integrate tethered-closure molds, helping beverage brands comply with closure-retention laws without disrupting filling speeds.

Geography Analysis

Regional disparities shape investment priorities across the United States plastic packaging market. California, New York, and Washington collectively enforce the strictest recycled-content and EPR measures; converters active in these coastal states accelerate innovation cycles to comply with SB 54 reduction mandates and curbside-recyclability criteria EcoEnclose. Brands often standardize national SKUs to the most stringent state rule set, channeling incremental cost into pack design rather than regional variance.

The Gulf Coast and Midwestern corridors dominate virgin and recycled resin supply thanks to shale-gas feedstock, competitive power rates, and efficient rail networks. Texas hosts integrated cracker-to-film complexes that supply both domestic and export markets, stabilizing feed-stock flow during port disruptions. Tariffs on Canadian polyolefins implemented in 2024 redirected procurement to domestic facilities, raising utilization rates and encouraging investments in PCR blending silos at extrusion plants.

Urban agglomerations such as New York City, Los Angeles, and Chicago generate disproportionate parcel volumes, pushing local fulfillment centers to adopt automated bag-on-demand systems. These hubs favor lightweight LDPE mailers and padded envelopes that qualify for kerbside collection schemes, bolstering flexible demand. Rural regions with nascent material-recovery infrastructure continue to rely on rigid HDPE containers that integrate smoothly into drop-off recycling streams, underlining how collection realities steer design decisions within the United States plastic packaging market.

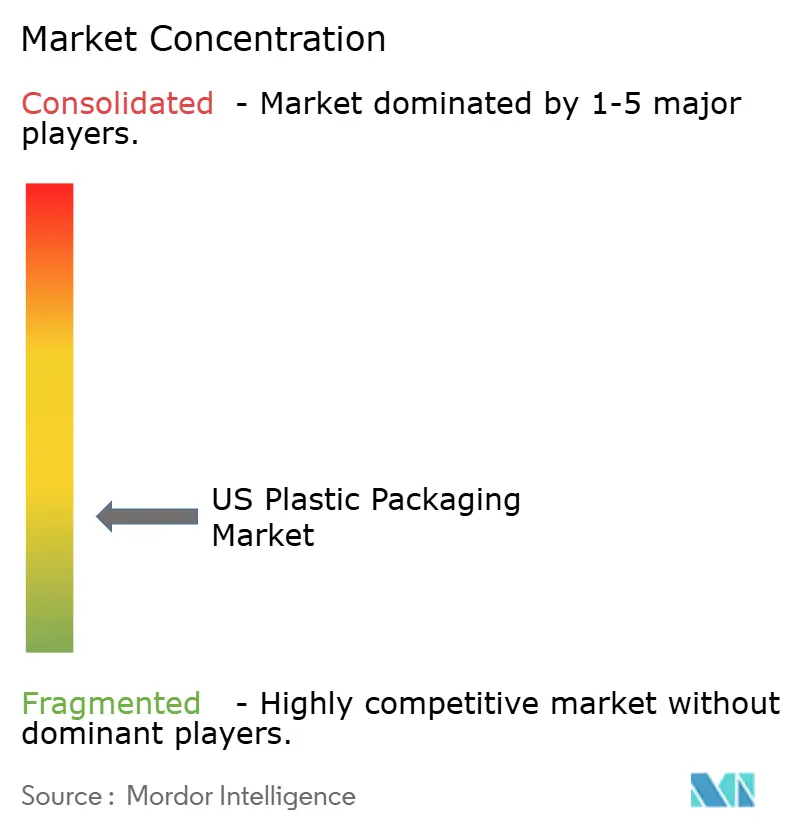

Competitive Landscape

Industry concentration is fragmented. The combined Amcor–Berry entity, Sealed Air, Sonoco, and others are the major players in the market. Amcor’s USD 8.4 billion acquisition of Berry Global, completed in May 2025, yields unmatched scale in resin sourcing and a global footprint spanning 250 plants Amcor plc. The merger promises EUR 650 million in synergies, including rationalized extrusion lines and shared digital-printing assets, with 12% EPS accretion projected for FY 2026.

Sealed Air leverages proprietary Cryovac vacuum systems to dominate fresh protein cases, while its automation division deploys AI-enabled vision cameras that cut seal failures by 70%. Sonoco targets recyclable paper-poly hybrids and recently introduced a polyethylene-free, microwave-safe bowl for shelf-stable soups. Niche converters focus on digital print agility and rapid prototyping, serving craft beverage, nutraceutical, and direct-to-consumer brands that demand low minimum order quantities.

Emerging disruptors include PureCycle, whose solvent-based depolymerization supplies odor-free, food-grade PP flake, and Addi-Flex, which commercializes compostable master batches compatible with standard blown-film lines. Robotics integrators report average payback under 28 months on in-mold labeling pick-and-place cells, driving adoption at mid-size injection molders that compete on unit cost within the United States plastic packaging market. Strategic alliances between resin giants and reclaimers aim to lock in PCR supply, creating a closed-loop moat that advantages integrated players over toll converters.

US Plastic Packaging Industry Leaders

Sigma Plastics Group Inc.

Amcor PLC

Sealed Air Corporation

Sonoco Products Company

Alpha Packaging Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Amcor completed its USD 8.4 billion acquisition of Berry Global, estimating EUR 650 million synergy capture and 12% EPS growth in FY 2026.

- January 2025: Berry Global unveiled new pharma-grade barrier containers at Pharmapack, optimized for nitrogen-flush filling and serialization compliance.

- November 2024: Arkema (Bostik) finalized purchase of Dow’s flexible-packaging adhesives business, bolstering U-S supply of solvent-free laminating grades for high-barrier snack films.

- June 2024: NOVA Chemicals secured FDA approval for its Connersville, Indiana mechanical-recycling process, enabling SYNDIGO rLLDPE films with up to 100% recycled content for food contact uses .

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the US plastic packaging market as all virgin and recycled rigid and flexible plastic formats, including bottles, jars, tubs, trays, closures, films, pouches, and mailers, sold to converters, fillers, and brand owners inside the United States for primary or secondary product protection, preservation, or transport.

Scope Exclusions: Industrial bulk containers above one ton capacity and purely fiber-based or metal laminate structures fall outside this coverage.

Segmentation Overview

- By Material Type

- Rigid Plastic

- Polyethylene (PE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS) and Expanded Polystyrene (EPS)

- Other Material Types

- Flexible Plastic

- Polyethylene (PE)

- Biaxially Oriented Polypropylene (BOPP)

- Cast Polypropylene (CPP)

- Other Material Types

- Rigid Plastic

- By Packaging Type

- Rigid Plastic Packaging

- Bottles and Jars

- Caps and Closures

- Trays and Clamshells

- Other Product Types

- Flexible Plastic Packaging

- Pouches

- Bags

- Films and Wraps

- Other Product Types

- Rigid Plastic Packaging

- By End-use Industry

- Food

- Beverage

- Pharmaceutical

- Cosmetics and Personal Care

- Home and Industrial Chemicals

- Pet Food and Animal Care

- Other End-use Industry

- By Packaging Technology

- Injection Molding

- Blow Molding

- Extrusion

- Thermoforming

Detailed Research Methodology and Data Validation

Primary Research

Our analysts spoke with resin producers, mid-size converters, e-commerce fulfillment managers, and state recycling officials across the Midwest, West Coast, and Sunbelt. Interviews confirmed PCR penetration targets, average gauge-reduction rates, and real-world converter utilization, which sharpened model sensitivities and trimmed desk-research bias.

Desk Research

We gathered baseline demand clues from reputable, open sources such as the US Census Annual Survey of Manufactures, the Bureau of Labor Statistics resin price index, the American Chemistry Council resin production data, and import-export volumes from the USITC DataWeb. Trade association briefs (Flexible Packaging Association, Plastics Industry Association) and peer-reviewed journals tracking post-consumer-recycled (PCR) adoption enriched our material split assumptions.

Company 10-Ks, converter investor decks, and news archived in Dow Jones Factiva filled revenue and capacity gaps, while D&B Hoovers enabled cross-checks of converter shipments by state. This list is illustrative; many other secondary sources helped validate numbers and clarify definitions.

Market-Sizing & Forecasting

A top-down build starts with domestic resin production plus net imports, which is then re-allocated by pack type, end user, and loss factors to yield the baseline volume. Supplier roll-ups and sampled average selling price multiplied by volume checks serve as selective bottom-up tests. Key variables, food retail volume, e-commerce parcel count, state PCR-mandate timelines, virgin-resin spot prices, and converter utilization, feed a multivariate regression forecast that projects tonnage out to the forecast period. Missing data points, such as unreported flexible film imports, are bridged using three-year moving averages anchored to customs records before final triangulation.

Data Validation & Update Cycle

Outputs pass anomaly scans, peer review, and senior analyst sign-off. We refresh models annually and issue interim tweaks after material events, for example, national EPR legislation, ensuring clients receive the newest view before every delivery.

Why Our United States Plastic Packaging Baseline Earns Trust

Published estimates often diverge because firms mix units, cover wider geographies, or freeze models for years.

Key gap drivers include differing treatment of flexible film imports, varied PCR content forecasts, and the cadence at which resin price shocks are folded back into average selling prices.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 29.97 million tons (2025) | Mordor Intelligence | - |

| USD 72.47 billion (2023) | Regional Consultancy A | Aggregates revenue across all pack types and prices; 2023 base year not yet refreshed |

| USD 53.7 billion (2023) | Industry Association B | Omits thin-gauge film imports and applies conservative ASP escalation |

| USD 92.93 billion (2025, North America) | Trade Journal C | Covers entire North America and relies on GDP scaling rather than resin flow analysis |

These comparisons show that Mordor's converter-level tonnage reconstruction, timely refresh cycle, and dual-path validation give decision makers a balanced, transparent baseline that is traceable to real, publicly verifiable variables.

Key Questions Answered in the Report

What is the current size of the United States plastic packaging market?

It stands at 30.9 million tonnes in 2026 and is projected to reach 36.04 million tonnes by 2031.

Which packaging type is growing the fastest?

Flexible plastic packaging is expanding at a 4.82% CAGR, outpacing rigid formats because it uses up to 70% less resin and meets e-commerce efficiency needs.

How are regulations affecting material choices?

State EPR laws and recycled-content mandates are pushing brands toward mono-material PE or PP laminates and boosting demand for food-grade rPET and rHDPE.

What end-use sector leads demand?

Food applications hold 39.05% share, driven by high-barrier pouches and trays that extend shelf life for ready-to-eat and chilled products.

Which technology commands the largest share of production?

Extrusion accounts for 38.42% of market revenue, thanks to its versatility in producing multi-layer films and profiles with rising PCR content.

Page last updated on: