Corrugated Fanfold Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.01 Billion |

| Market Size (2031) | USD 13.47 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

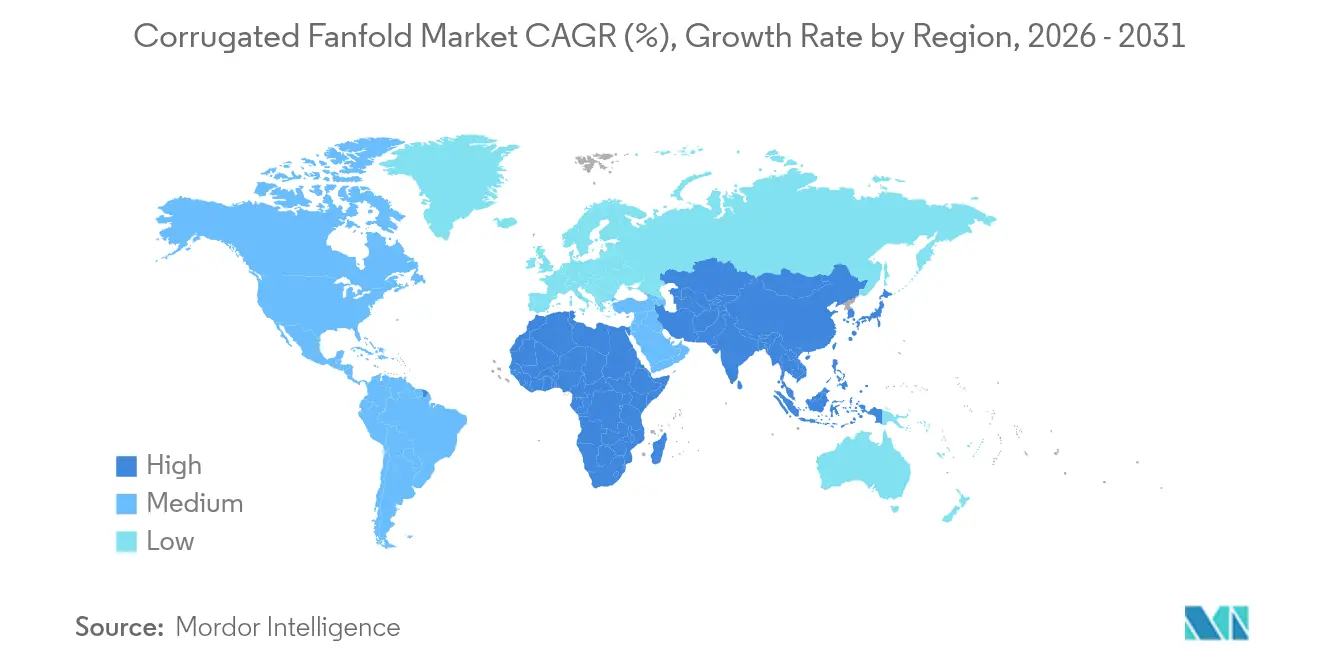

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

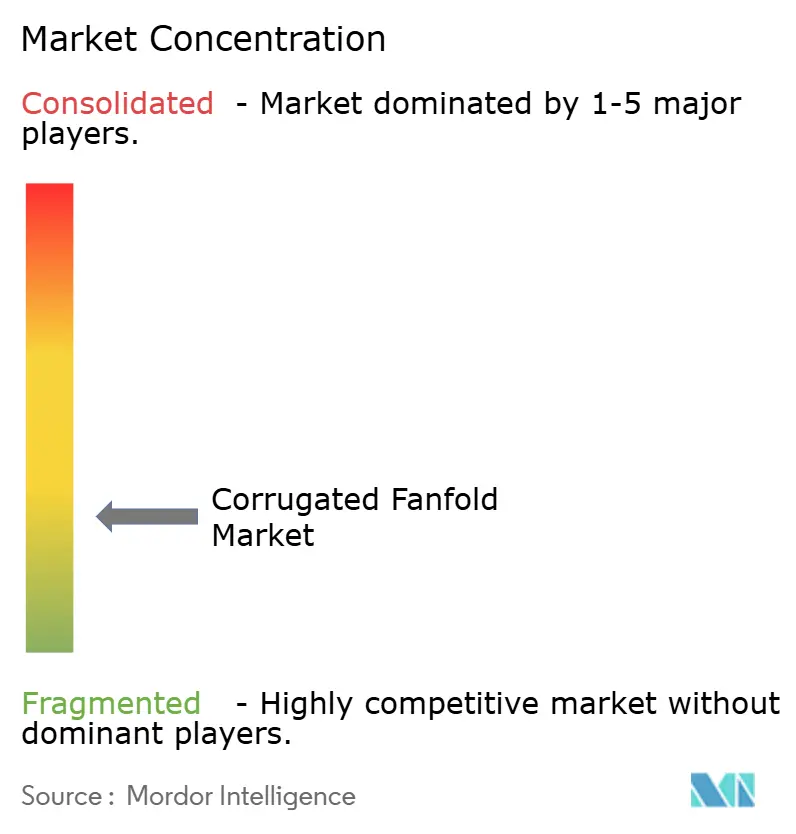

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corrugated Fanfold Market Analysis by Mordor Intelligence

The corrugated fanfold market size was valued at USD 10.57 billion in 2025 and estimated to grow from USD 11.01 billion in 2026 to reach USD 13.47 billion by 2031, at a CAGR of 4.11% during the forecast period (2026-2031). Adoption accelerates because fanfold reduces material waste by 26% and lifts truck utilisation by 33%, making every tonne of containerboard work harder for shippers. Digital workflows produce custom boxes in 3.5 seconds, mitigate labour shortages, and eliminate void fillers—benefits that resonate strongly with e-commerce operators facing elevated last-mile costs. Regionally, North America held the largest corrugated fanfold market share of 38.54% in 2024, while Asia-Pacific is on track for the quickest expansion at 7.88% CAGR, buoyed by new capacity from Nine Dragons Paper and surging Vietnamese demand. Product-wise, single-wall formats dominated with 55.63% share in 2024, yet triple-wall grades are expanding at 7.85% CAGR as automotive and pharmaceutical supply chains require extra compression strength.

Key Report Takeaways

- By wall type, single-wall held 55.32% of the corrugated fanfold market share in 2025, whereas triple-wall is forecast to compound at 7.78% CAGR to 2031.

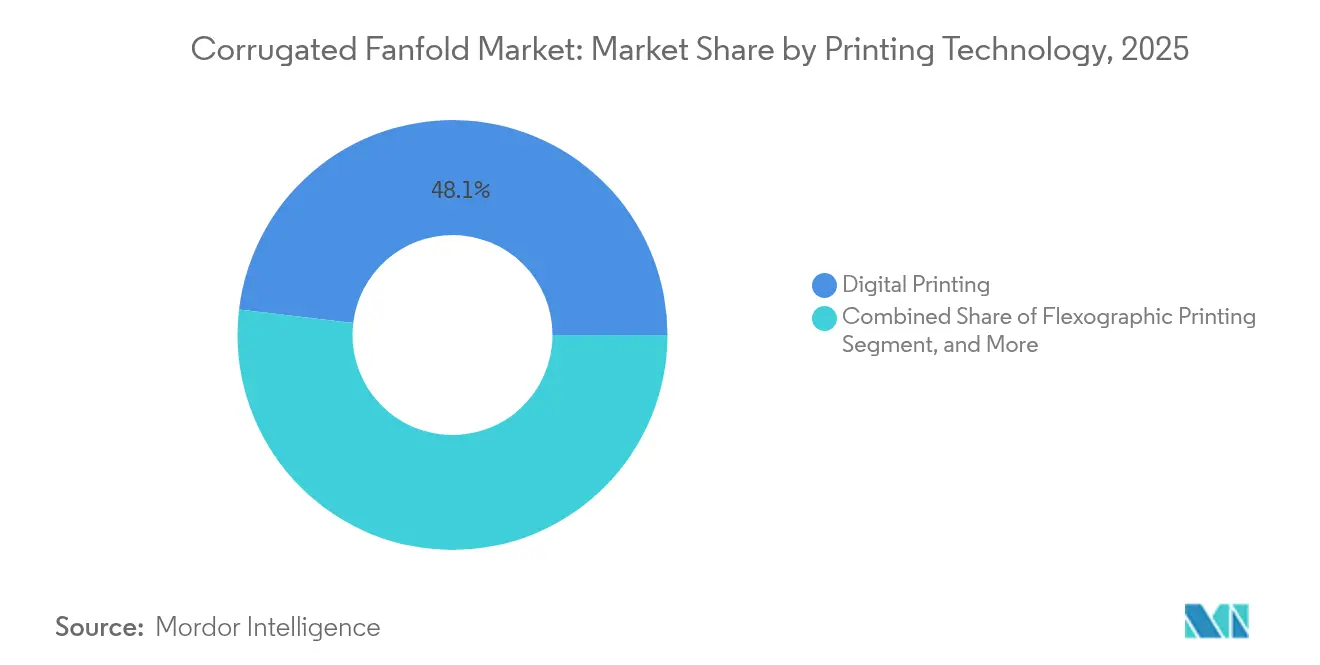

- By printing technology, digital printing led with 48.10% revenue in 2025; flexographic printing is poised for the fastest 7.59% CAGR through 2031 thanks to hybrid presses such as Uteco’s OnyxOMNIA.

- By end-use, shipping and logistics retained 42.10% of the corrugated fanfold market size in 2025, while e-commerce fulfillment is projected to climb at an 8.85% CAGR between 2026-2031.

- By geography, North America led with 38.20% revenue in 2025; Asia-Pacific is advancing at a 7.79% CAGR to 2031 on the back of regional capacity additions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Corrugated Fanfold Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in right-sized packaging demand from e-commerce fulfillment centres | +1.2% | Global, with early gains in North America, Europe | Short term (≤ 2 years) |

| Fit-to-product (FtP) automated systems accelerating fanfold uptake | +0.8% | North America & EU, spill-over to APAC core | Medium term (2-4 years) |

| Brand-owner pivot to mono-material, kerb-side-recyclable solutions | +0.7% | Global, with regulatory push in EU, California | Medium term (2-4 years) |

| Surge in corrugator-on-demand leasing models for SMEs | +0.4% | APAC core, emerging in Latin America | Long term (≥ 4 years) |

| Government bans on expanded polystyrene void-fill in key states | +0.3% | National, with early gains in California, New York | Short term (≤ 2 years) |

| IoT-enabled converting lines improving OEE and lowering change-over cost | +0.6% | Global, with manufacturing hubs leading adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Boom in Right-Sized Packaging Demand from E-Commerce Fulfillment Centres

E-commerce operators continue to prioritise right-sized automation because oversized parcels attract dimensional-weight penalties of up to 30% and frustrate consumers with excess void fill. Packsize’s X5 installation at Performance Health lifted productivity by 97% while halving pick-line labour, demonstrating why the corrugated fanfold market is integral to lean fulfillment. TNT Deals achieved 400 orders per hour after migrating to continuous-feed fanfold, lowering corrugated spend by more than 50%. Each machine dispenses a made-to-fit box every 3.5 seconds, outpacing manual assembly that can take 30 seconds or more. Right-sized outputs raise trailer density by a quarter and shrink material usage by 26%, directly enhancing carbon intensity scores for retailers targeting Scope 3 reductions.

Fit-to-Product Automated Systems Accelerating Fanfold Uptake

Fit-to-product (FtP) equipment converts fanfold from a generic linerboard substrate into a precision packaging medium that mirrors real-time product dimensions. WestRock’s BoxSizer dynamically resizes each case to slash void and cut carbon per shipment. ReadyWise shifted to Packsize’s X4, enabling output of 1 million pouches weekly while eliminating all dunnage, further stimulating corrugated fanfold market growth. BHS Corrugated’s “Corrugated 4.0” embeds IoT sensors to adjust quality in real-time, cutting defects 25% and lifting OEE to 85%.[1]BHS Corrugated, “Corrugated 4.0,” bhs-world.com Such productivity gains reinforce the corrugated fanfold market’s attractiveness for sites where footprint, labour and uptime are tightly scrutinised.

Brand-Owner Pivot to Mono-Material, Curb-Side-Recyclable Solutions

Corporate sustainability programmes increasingly demand mono-material formats recyclable through household curb-side schemes, making fanfold an intuitive substitute for EPS or multi-layer plastics. VELUX replaced plastic with corrugated packs, stripping 900 tonnes of polymer and trimming CO₂ by 13%. DS Smith’s TailorTemp keeps cold-chain goods within range for 36 hours, yet is made of fully recyclable fibre. European targets for 100% recyclable packaging by 2030 further accelerate the corrugated fanfold market as its fibres can be reprocessed 25 times, outclassing plastics’ limited cycles

IoT-Enabled Converting Lines Improving OEE and Cutting Change-Over Cost

Predictive analytics and machine-learning platforms extend uptime and reduce trim waste, underpinning a smarter corrugated fanfold industry. SUN Automation’s Helios IIoT suite lowers unplanned downtime by 35%, adding steady capacity without new capital. Voith’s autonomous mill vision shows how AI can fine-tune fanfold parameters to save 15% energy and uphold grade quality. Each initiative feeds directly into total delivered-cost metrics, reinforcing buyer preference for suppliers that master data-driven production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kraft liner and recycled containerboard price volatility | -0.9% | Global, with acute pressure in North America | Short term (≤ 2 years) |

| Capital-intensive digital printing presses limit SME adoption | -0.6% | Global, particularly affecting independent corrugators | Medium term (2-4 years) |

| Supply bottlenecks for starch-based, bio-adhesives | -0.4% | Global, with supply chain concentration in Asia | Short term (≤ 2 years) |

| Limited corrugated recycling infrastructure in emerging APAC | -0.5% | APAC emerging markets, rural distribution networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Kraft Liner and Recycled Containerboard Price Volatility

The corrugated fanfold market contends with cyclical pulp and OCC swings that pushed North American linerboard up USD 70 per ton in early 2025, pressuring converters’ margins and triggering short-term price pass-throughs for OEMs. Caps on Chinese wastepaper imports continue to destabilise global recovered fibre flows, causing tighter supply at precisely the moment e-commerce volumes climb. Although integrated players partially offset spikes through internal mills, SME sheet-plants face greater exposure, compelling many to hedge via longer-term fibre contracts or mixed-sheet recipes that temper cost but complicate quality management.

Capital-Intensive Digital Printing Presses Limit SME Adoption

Single-pass digital inkjet presses can exceed USD 3 million, a hurdle for independents comprising a large slice of the corrugated fanfold market. Hybrid FLEXO-inkjet systems attempt to reconcile cost efficiency with custom graphics, yet plate, ink, and service contracts still strain SME budgets. Equipment leasing eases upfront burdens but elongates payback periods, keeping some converters on legacy machinery that struggles with short-run SKUs driven by omnichannel retail. Such investment friction may curb penetration in underserved regions until financing schemes scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wall Type: Triple Wall Gains Momentum in Heavy-Duty Applications

Single-wall grades maintained 55.32% share of the corrugated fanfold market in 2025 as retailers favoured a cost-efficient structure for high-velocity SKUs. Triple-wall variants, however, are forecast to expand at 7.78% CAGR because EV battery modules, industrial machinery and temperature-sensitive pharmaceuticals demand higher edge-crush strength.

Smurfit Kappa’s programme for Scania illustrates the shift: triple-wall packs lowered material spending by 30% and secured parts in automated handling loops, validating premium adoption. As automated warehouses proliferate, buyers increasingly view heavy-duty fanfold as insurance against drop impacts that can halt production lines, positioning triple-wall as a growth lever within the corrugated fanfold market.

By Flute Type: E-Flute Emerges as Digital Printing Catalyst

C-flute retained 40.46% share in 2025, reflecting its strength-to-weight balance for parcel carriers. Yet E-flute’s 8.06% CAGR shows how thinner profiles align with dimensional-weight optimisation while supplying a smooth print surface for 1,200×1,200 DPI graphics.

Domino’s X630i achieves food-safe aqueous prints at up to 246 fpm on E-flute without primer, meeting brand requirements for shelf-ready display. Logistics stakeholders gain 20% more boxes per container when swapping C- for E-flute, freeing freight and warehouse capacity in the global corrugated fanfold market.

By Printing Technology: Flexographic Printing Accelerates Through Hybrid Innovation

Digital systems captured 48.10% of corrugated fanfold market share in 2025 as customisation demands grew. Nonetheless, flexographic presses are growing at 7.59% CAGR thanks to plates that change in minutes and hybrid architectures like Uteco’s OnyxOMNIA, which blends single-pass inkjet for variable graphics with 400 m/min flexo speed for bulk coverage .

Water-based inks now satisfy food-contact rules while curbing VOC emissions, narrowing sustainability gaps with digital. Runs above 10,000 linear metres swing cost advantage back to flexo, ensuring sizeable share retention through 2031 in the evolving corrugated fanfold market.

By End-Use: E-Commerce Fulfillment Drives Fastest Expansion

Shipping and logistics represented 42.10% of the corrugated fanfold market size in 2025 as 3PLs continued to migrate from sheets to continuous fanfold for high-throughput operations. E-commerce fulfillment is projected to post an 8.85% CAGR because automated fit-to-product systems crank out 1,020 boxes per hour, enabling same-day dispatch promises.

Food-and-beverage brands increasingly specify fanfold for leak-resistant, curb-side-recyclable crates that meet cold-chain regulations, as seen in Taartenwinkel Bakery’s sub-7°C dessert shipments . Healthcare and personal-care firms leverage the medium for premium unboxing experiences, embedding QR-code-driven traceability without adding labels, extending corrugated fanfold market penetration into lifestyle categories.

Geography Analysis

North America anchors the corrugated fanfold market, accounting for 38.20% revenue in 2025 as fulfilment centres nationwide race to automate amid record parcel volumes and rising minimum wages. State-level EPS bans, such as Los Angeles’ Ordinance 187717, compel shippers to adopt fibre-based alternatives, securing near-term demand. Fibre price volatility remains a headwind, but mill investments—USD 1 billion at Green Bay Packaging’s Arkansas site and Georgia-Pacific’s USD 80 million Alabama upgrade—signal confidence in regional consumption.

Asia-Pacific is forecast to clock the fastest 7.79% CAGR through 2031, fuelled by Nine Dragons Paper’s 600,000-900,000 tpa capacity build-out and Vietnam’s USD 3.5 billion packaging appetite, climbing 9.73% annually. China’s recovered-fibre-starved mills report 3.04% containerboard price upticks in 2024, while weak recycling in emerging ASEAN markets restrains raw-material security and raises imported OCC dependence. Governments are therefore accelerating collection schemes, which in turn reinforce supply for the region’s booming corrugated fanfold market.

Europe sustains mid-single-digit growth on the strength of regulatory certainty. The EU Packaging and Packaging Waste Regulation mandates full recyclability by 2030, making fanfold a compliance default for brand-owners. Converters are repositioning assets accordingly: Norske Skog’s EUR 320 million Golbey conversion brings 550,000 tpa recycled containerboard online, while Stora Enso’s acquisition of Junnikkala secures 700,000 m³ extra saw logs for fibreboard. With continental recycling rates around 90%, European producers enjoy a structural raw-material advantage that underpins steady corrugated fanfold market supply.

Competitive Landscape

The corrugated fanfold market is of moderate fragmentation, with integrated multinationals and over 1,100 independent U.S. corrugators coexisting. The USD 11.2 billion Smurfit-WestRock merger and International Paper’s USD 7.2 billion purchase of DS Smith create global entities generating around USD 34 billion in combined sales across more than 40 countries. Their vertical integration secures linerboard, converting and design services under one roof, enabling scale plays in North America, Europe and Latin America.

Mid-tier converters differentiate through technology. BHS Corrugated offers “Corrugated 4.0” lines with predictive maintenance baked in, while Packsize partners with Henkel to cut adhesive carbon footprints 32% across 340 million boxes per year. Voith’s autonomous mill concept promises 15% energy savings, furnishing cost leadership for adopters. Such process innovations cement loyalty among global brands seeking reliable, low-carbon packaging.

Independent sheet-plants leverage equipment-as-a-service contracts that replace USD 2-5 million capital outlays with sub-USD 50,000 monthly leases, easing entry into the corrugated fanfold industry. Access to IoT dashboards elevates OEE and shortens changeovers, enabling smaller firms to serve specialised SKUs the giants overlook. This two-tier landscape is expected to endure as niche agility offsets the purchasing muscle of conglomerates in the global corrugated fanfold market.

Corrugated Fanfold Industry Leaders

International Paper Company

Mondi Plc

Oji Holdings Corporation

Smurfit WestRock

Sonoco Products Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Stora Enso finalised the EUR 137 million (USD 155 million) acquisition of sawmill Junnikkala Oy, adding 700,000 m³ of annual capacity for future board grades.

- April 2025: UFP Industries inaugurated its third corrugated facility to satisfy rising multi-industry demand.

- April 2025: Packaging Corporation of America posted record Q1 revenue with 2.5% higher shipments year-on-year.

- January 2025: DS Smith unveiled TailorTemp, a recyclable cold-chain pack maintaining 36-hour temperature control.

Global Corrugated Fanfold Market Report Scope

Corrugated fan fold is a long sheet of cardboard that has been scored and folded at regular intervals to resemble a fan. When used with automated box-making machines, it allows large-scale businesses to produce bespoke packaging on demand. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrive at top-down and bottom-up approaches.

The corrugated fanfold market is segmented by wall type (Single Wall, Double Wall and Triple Wall), by flute type (C Flute, B Flute, E Flute and Others), by printing technology (Digital Printing, Flexographic Printing and Lithographic Printing) , by end-use (Shipping & Logistics, E-Commerce, Pharmaceutical, Personal Care & Cosmetics, Food & Beverage and Other End-uses) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa). The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Single Wall |

| Double Wall |

| Triple Wall |

| Quad Wall |

| C Flute |

| B Flute |

| E Flute |

| F Flute |

| Other Flute Type |

| Digital Printing |

| Flexographic Printing |

| Lithographic Printing |

| Offset Inkjet |

| Shipping and Logistics |

| E-Commerce, Fulfilment and 3PL |

| Food and Beverage |

| Pharmaceutical and Healthcare |

| Personal Care and Cosmetics |

| Industrial and Automotive Parts |

| Other End-Use |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Wall Type | Single Wall | ||

| Double Wall | |||

| Triple Wall | |||

| Quad Wall | |||

| By Flute Type | C Flute | ||

| B Flute | |||

| E Flute | |||

| F Flute | |||

| Other Flute Type | |||

| By Printing Technology | Digital Printing | ||

| Flexographic Printing | |||

| Lithographic Printing | |||

| Offset Inkjet | |||

| By End-Use | Shipping and Logistics | ||

| E-Commerce, Fulfilment and 3PL | |||

| Food and Beverage | |||

| Pharmaceutical and Healthcare | |||

| Personal Care and Cosmetics | |||

| Industrial and Automotive Parts | |||

| Other End-Use | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current corrugated fanfold market size?

The corrugated fanfold market size reached USD 11.01 billion in 2026 and is projected to reach USD 13.47 billion by 2031.

Which region leads the corrugated fanfold market?

North America led with 38.20% revenue in 2025 thanks to advanced automation and EPS restrictions.

Which segment is growing fastest within the corrugated fanfold market?

E-commerce fulfillment is expanding at an 8.85% CAGR as right-sized automation becomes mainstream.

Why is triple-wall fanfold gaining traction?

Industrial, automotive and pharmaceutical shippers need higher compression strength, driving triple-wall’s 7.78% CAGR.

How are regulations influencing adoption?

EU and U.S. bans on expanded polystyrene and mandates for recyclable packaging steer brands toward fibre-based fanfold solutions.

What technologies are reshaping production efficiency?

IoT-enabled converting lines and hybrid flexographic-digital presses are boosting OEE and lowering change-over costs for converters.

Page last updated on: