Non-Toxic Nail Polish Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

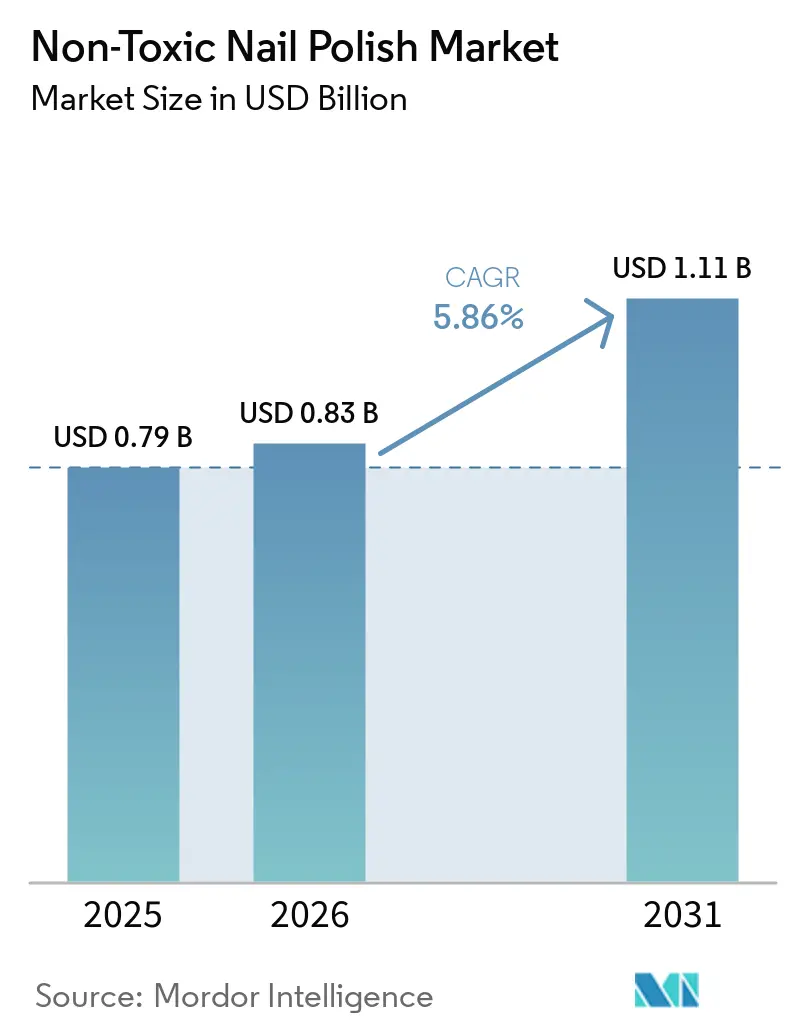

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.11 Billion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

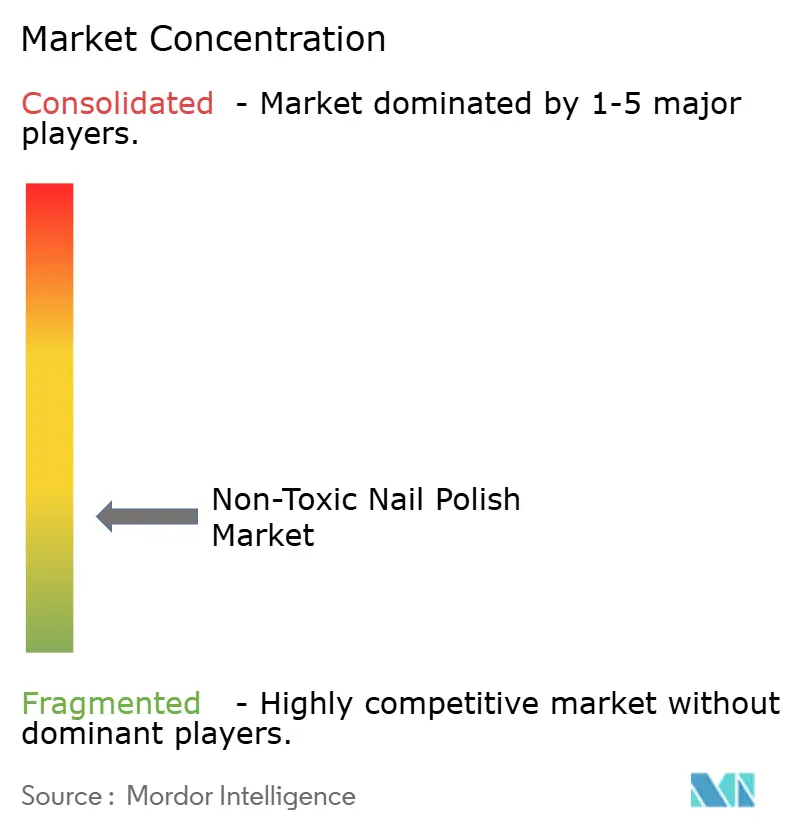

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-Toxic Nail Polish Market Analysis by Mordor Intelligence

The non-toxic nail polish market size stood at USD 0.79 billion in 2025, and is expected to reach USD 0.83 billion in 2026, and is forecasted to reach USD 1.11 billion by 2031 at a CAGR of 5.9% over 2026-2031. The non-toxic nail polish market has moved beyond a niche wellness position because buyers now expect safer ingredient profiles without giving up shade range, finish quality, or wear performance. European regulation has accelerated that shift after Regulation (EU) 2025/877 took effect on September 1, 2025, and banned TPO and DMTA with no transition period for existing stock, which forced immediate reformulation or withdrawal for affected products. In the United States, the MoCRA framework has increased the importance of product registration, safety support, and claim substantiation, which favors brands that have built their clean positioning on formal compliance rather than marketing language alone. Even with higher input costs, tighter scrutiny of green claims, and a fragmented supplier base, the non-toxic nail polish market remains supported by regulatory momentum, broader ingredient literacy, and product innovation that expands appeal across retail, salon, breathable, and halal-oriented demand pockets.

Key Report Takeaways

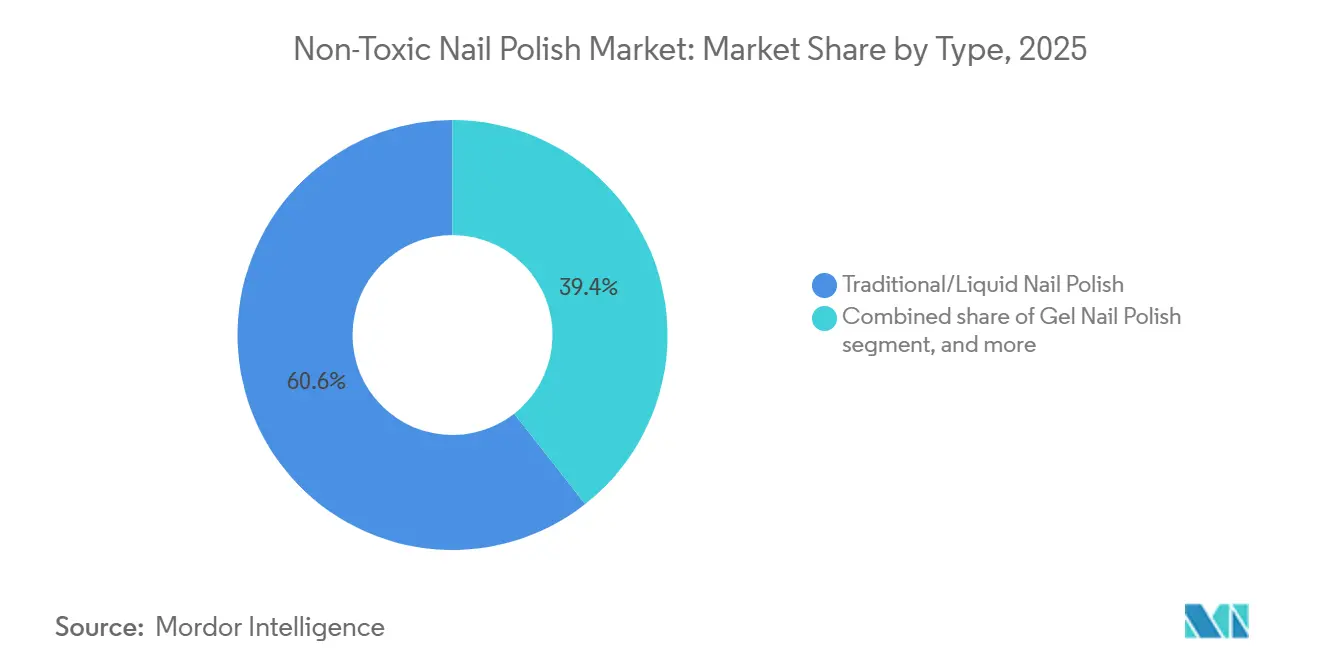

- By type, Traditional/Liquid Nail Polish held 60.5% of the non-toxic nail polish market share in 2025, while Gel Nail Polish is forecast to grow at a 7.87% CAGR through 2031.

- By coat type, Base Coat accounted for 80.3% of the segment in 2025, while Top Coat is projected to expand at a 6.59% CAGR through 2031.

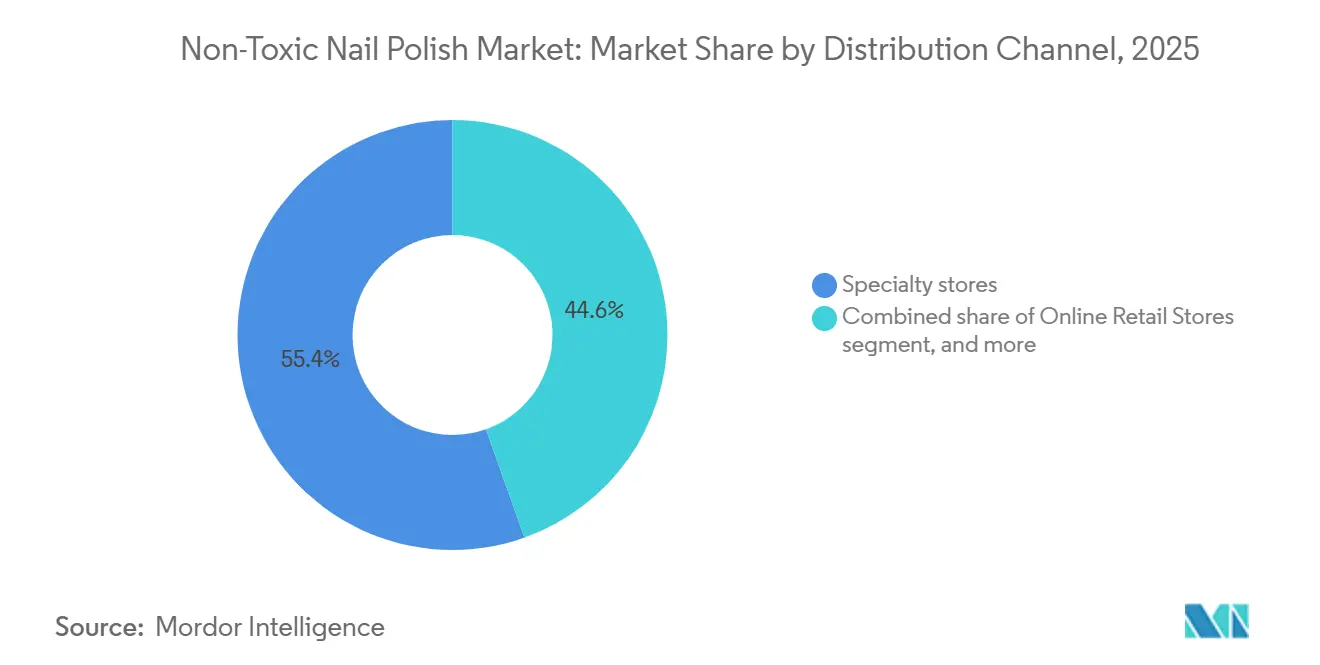

- By distribution channel, Specialty Stores held 55.43% of the segment in 2025, while Online Retail Stores are forecast to grow at a 7.32% CAGR through 2031.

- By geography, North America held 36.58% of the non-toxic nail polish market share in 2025, while Asia-Pacific is projected to advance at a 7.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Non-Toxic Nail Polish Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean beauty and ingredient transparency | +1.5% | Global, with North America and Europe as primary demand centers | Short term (≤ 2 years) |

| Regulatory pressure on toxic cosmetic ingredients | +1.2% | EU core, with spillover to the United Kingdom and Asia-Pacific | Short term (≤ 2 years) |

| E-commerce expansion for niche beauty brands | +0.9% | Global, with Asia-Pacific and North America leading by platform scale | Medium term (2-4 years) |

| Salon adoption of safer formulations | +0.7% | North America, Europe, South Korea, Japan | Medium term (2-4 years) |

| Breathable and halal-certified product innovation | +0.8% | Middle East and Africa, Southeast Asia, with spillover to North America and Europe | Long term (≥ 4 years) |

| Premiumization through hybrid treatment-color formulas | +0.6% | North America, Europe, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean beauty and ingredient transparency

Consumer awareness in beauty has shifted from passive interest to active screening, and that has created a stronger base for the non-toxic nail polish market. The draft shows that ingredient safety now influences purchase behavior more directly than simple demographic targeting, which means brands compete on trust as much as color or finish. New launch activity also supports this change, with more nail polish launches described as vegan, cruelty-free, or water-based, which indicates that clean positioning has become a standard commercial response rather than a fringe tactic. As this pattern expands, the non-toxic nail polish market gains a shelf access advantage because retailers increasingly expect clear disclosure and cleaner claims before granting premium placement. That pressure matters because once ingredient transparency becomes part of the retailer screening process, weaker formulations risk losing visibility even before end demand softens. The result is that the non-toxic nail polish market benefits not only from stronger consumer pull, but also from a stricter retail filter that steadily raises the minimum standard for participation.

Regulatory pressure on toxic cosmetic ingredients

Regulatory change has become one of the clearest demand and supply catalysts in the non-toxic nail polish market. Regulation (EU) 2025/877 classified Trimethylbenzoyl Diphenylphosphine Oxide (TPO) and Dimethyltolylamine (DMTA) as carcinogenic, Mutagenic, and Reprotoxic (CMR) category 1B substances and required immediate withdrawal of non-compliant products from September 1, 2025, which reset the compliance timetable for gel and semi-permanent products across the affected region[1]Source: European Commission, “Commission Regulation (EU) 2025/877,” EUR-Lex, eur-lex.europa.eu. Commentary cited in the draft also points to comparable scrutiny in the United Kingdom, which suggests that the regulatory perimeter around conventional gel chemistry is still tightening rather than stabilizing. This matters because the non-toxic nail polish market no longer depends only on a consumer preference story when regulation is forcing conventional players to reformulate on similar chemistry platforms. Brands that already built compliant or lower-toxicity systems enter this phase with less disruption, faster shelf continuity, and clearer proof points in discussions with salons and retail buyers.

E-commerce expansion for niche beauty brands

Digital commerce is changing the route to market for the non-toxic nail polish market by reducing the old dependence on physical shelf access. The Mordor Intelligence Analysis identifies Online Retail Stores as the fastest-growing channel at a 7.32% CAGR through 2031, which fits the economics of a category built around compact units, repeat shade purchases, and bundle-friendly shipping. In this setting, smaller clean brands can launch, test, and scale without first winning national retail distribution, which weakens one of the biggest defenses once held by mass conventional players. The non-toxic nail polish market also benefits from digital merchandising tools such as ingredient filters, clean badges, and creator-led demonstrations, because these tools help explain formulation differences in ways that a standard shelf card often cannot. Social commerce adds another layer because it shortens the time between product launch, consumer feedback, and reorder behavior, especially for indie brands with faster development cycles. As a result, the non-toxic nail polish market gains not only incremental channel growth, but also a more flexible commercialization model that favors focused brands with clear ingredient stories.

Breathable and halal-certified product innovation

Breathable and halal-certified formats give the non-toxic nail polish market a demand pool that conventional polish cannot fully serve. The draft connects this opportunity to religious practice because water permeability matters for wudu, which turns breathable performance from a marketing feature into a functional requirement in several Muslim-majority markets. That distinction matters because the non-toxic nail polish market can access premium demand where the product specification itself creates separation from standard formulations. The draft also notes that certification quality varies across bodies, which means trust will depend not only on ingredient screening but also on whether the brand can support water-permeability and halal claims with credible documentation. Over time, this could shift competition away from broad clean claims and toward more exact compliance language, especially in Southeast Asia and Gulf markets, where certification credibility shapes repeat purchase. The non-toxic nail polish market, therefore, has room to widen geographically through a niche that is still underpenetrated and less exposed to direct substitution from conventional long-wear products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher formulation and certification costs | -0.8% | Global, with the sharpest burden on independent brands in North America and Europe | Medium term (2-4 years) |

| Performance gap versus conventional long-wear polishes | -0.7% | North America and Europe, with rising relevance in Asia-Pacific as gel adoption increases | Medium term (2-4 years) |

| Consumer skepticism around greenwashing and efficacy claims | -0.5% | North America and Western Europe, with growing visibility in South Korea and Australia | Short term (≤ 2 years) |

| Narrow shade depth and finish constraints in some non-toxic systems | -0.3% | Global, with stronger relevance in premium North American and European demand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher formulation and certification costs

Cost remains a meaningful brake on the non-toxic nail polish market because cleaner chemistry often requires more expensive raw materials, more testing, and more documentation. The draft points to bio-sourced inputs such as plant cellulose, castor oil, and sugar beet ethanol, which lift formulation costs above petroleum-derived solvent systems. Compliance adds another layer because the Modernization of Cosmetics Regulation Act of 2022 (MoCRA) requires facility registration and product listing, and those obligations are easier for scaled brands to absorb than for smaller independent labels[2]Source: U.S. Food and Drug Administration, “Nail Care Products,” FDA, fda.gov. Third-party certifications can also accumulate quickly when a brand pursues vegan, cruelty-free, environmental, and halal credibility at the same time. This expense does not stop the non-toxic nail polish market from growing, but it does raise the volume threshold needed to protect margins and fund expansion. In a fragmented field, cost pressure supports consolidation, favors brands with deeper capital access, and makes operational scale more important than it was during the early clean beauty phase.

Performance gap versus conventional long-wear polishes

The non-toxic nail polish market still faces a practical challenge because durability remains one of the main reasons some consumers hesitate to switch from conventional products. The draft notes that conventional systems using standard resins and petrochemical plasticizers still deliver longer chip-resistant wear in many cases, especially in formats tied to long-wear expectations. A 2025 safety review cited in the draft also noted that toxin-free systems may lose some adhesion support when key resins are excluded, while performance claims are not necessarily backed by pre-market validation under current United States or EU rules[3]Source: PubMed Central, “The Safety of Nail Products, Health Threats in the Nail Industry,” NCBI, pmc.ncbi.nlm.nih.gov. That matters because one weak trial can shape category perception well beyond the individual brand that underperformed. The non-toxic nail polish market is responding through hybrid systems that combine treatment benefits with stronger visible results, including Butter London’s 2026 launch, built around a patented hexanal molecule and user-reported nail strengthening after two weeks. Even so, the non-toxic nail polish market will need continued product proof and repeat-use confidence to close the lingering gap between cleaner positioning and performance expectations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Traditional Polish Retains Scale While Gel Reformulation Supports the Fastest Growth

Traditional/Liquid Nail Polish accounted for 60.5% of the non-toxic nail polish market size in 2025, which reflects its broad retail penetration, easy use, and strong consumer familiarity. This format benefits from not requiring ultraviolet equipment, which keeps it accessible across home users, occasional buyers, and retail shoppers who value convenience. The non-toxic nail polish market has also seen the clean positioning of liquid polish mature steadily, with brands moving from earlier 3-free claims toward 17-free and 21-free positioning as product standards rose. That progression matters because it widened the appeal of liquid formats without forcing consumers to learn a new application routine.

Gel Nail Polish is forecast to grow at a 7.87% CAGR through 2031, and that makes it the fastest-expanding type in the non-toxic nail polish market. The growth path is shaped less by old salon habits alone and more by the current reformulation cycle, because brands that adapt quickly can capture premium shelf space left open by non-compliant products. The draft highlights this through The GelBottle Inc.’s TPO-free transition ahead of the United Kingdom timeline and CND’s June 2026 relaunch of SHELLAC with a Visible Light Lamp, both of which show that the growth story in gel now depends on compliant performance innovation rather than on legacy chemistry alone.

By Coat Type: Base Coat Holds the Functional Core While Top Coat Gains Through Treatment Upside

Base Coat held 80.3% of the segment in 2025, which shows how central preparation and adhesion remain within the non-toxic nail polish market. A compliant manicure still depends on a reliable first layer, especially when the color system is designed to avoid higher-risk ingredients that once supported adhesion or wear. This explains why base coat demand stays steady across both retail and professional settings, with salons treating the step as a requirement rather than an optional add-on. The draft also links this segment to tighter compliance needs under European cosmetic regulation because gel-compatible bases often sit closer to chemical scrutiny around acrylates and methacrylates.

Top Coat is projected to grow at a 6.59% CAGR through 2031, and that makes it the fastest-moving coat segment in the non-toxic nail polish market. The reason is not simple replacement demand, because the top coat is being repositioned as a treatment carrier that adds gloss, protection, and visible nail care in one layer. This supports premium pricing because consumers can justify the purchase as both appearance maintenance and nail health support. It also fits the broader move toward hybrid treatment-color formulas, where the non-toxic nail polish industry is trying to reduce the old distinction between cosmetic finish and care benefit.

By Distribution Channel: Specialty Retail Leads Today While Online Scales the Next Phase

Specialty Stores held 55.43% of the channel mix in 2025, which shows that curated discovery still matters in the non-toxic nail polish market. This channel does more than distribute inventory because it helps shoppers interpret ingredient language, compare clean claims, and connect premium prices to product rationale. The format is especially important for a category where purchase decisions are often shaped by trust, retailer curation, and staff guidance rather than by shade choice alone. Salon-linked specialty retail strengthens this position because professional validation reduces the perceived risk of trying a cleaner formula. The draft’s reference to branded salon environments, including Tenoverten, supports the idea that the non-toxic nail polish market still benefits from spaces where service and product education are closely tied.

Online Retail Stores are forecast to grow at a 7.3% CAGR through 2031, which makes them the fastest-growing route to market in the non-toxic nail polish market. The economics are favorable because bottles are light, reorderable, and well-suited to bundles, subscriptions, and creator-led discovery. Digital platforms also help indie brands reach buyers without building a full physical footprint, and that matters in a fragmented category where many strong labels remain underdistributed in traditional chains.

Geography Analysis

North America held 3658% of the non-toxic nail polish market share in 2025, which kept it in the leading regional position. The region benefits from strong ingredient literacy, established clean beauty merchandising, and a premium consumer base that is already familiar with safety-oriented product claims. These factors give the non-toxic nail polish market a supportive retail environment in the United States and Canada, where cleaner positioning can translate into repeat purchase rather than just trial demand. Europe remains critical even without the leading share because the non-toxic nail polish market is being reshaped there by regulation, with Germany, France, Italy, and the United Kingdom all tied closely to the reformulation cycle that followed the September 2025 Trimethylbenzoyl Diphenylphosphine Oxide (TPO) and Dimethyltolylamine (DMTA) ban.

Asia-Pacific is forecast to grow at a 7.81% CAGR through 2031, which makes it the fastest-expanding regional block in the non-toxic nail polish market. The region combines rising disposable income, a digitally connected beauty buyer, and strong openness to new formats, which gives cleaner products room to scale quickly once distribution is in place. South Korea adds an important quality layer because buyers there tend to combine ingredient scrutiny with a high willingness to try technology-led beauty solutions, including hybrid treatments and advanced finishing systems. Australia is still a smaller market in the non-toxic nail polish market, but local vegan and certified brands show that export-friendly clean positioning can build traction beyond domestic demand.

The Middle East and Africa present the most distinct structural case in the non-toxic nail polish market because breathable and halal-certified products address a clear use requirement rather than a broad preference alone. Saudi Arabia and the United Arab Emirates lead this pattern through high disposable incomes, premium beauty demand, and a large consumer base that values halal-aligned formulation standards. The draft also notes rising executive expectations for Middle East beauty growth, which supports the view that the non-toxic nail polish market could see outsized premium demand there as distribution improves. South Africa remains smaller, yet it offers early-stage upside as modern beauty retail expands and international clean brands build awareness. In South America, Brazil and Argentina remain the main demand centers, though the non-toxic nail polish market is still less mature there than in North America or Western Europe.

Competitive Landscape

The non-toxic nail polish market remains highly fragmented, and that keeps competition centered on brand identity, ingredient credibility, and product architecture rather than on dominant scale alone. The field includes indie clean brands with strong followings, established players with dedicated safer ranges, and adjacent lifestyle brands that now view cleaner nail care as a logical extension of wellness positioning. This mix means the non-toxic nail polish market rewards companies that can communicate a credible claim set while still meeting everyday expectations on shade, finish, and wear. It also means shelf access and digital discovery matter almost as much as formulation quality because many capable brands still operate with narrower distribution than mass conventional players.

A clear pattern across the non-toxic nail polish market is the escalation of free-from claims, with brands moving from lower-threshold exclusion lists toward 17-free, 21-free, and beyond. A second pattern is certification stacking, where vegan, cruelty-free, environmental, and halal credentials are combined to strengthen trust and widen audience reach. A third pattern is treatment-color convergence, where companies use nail care actives, strengthening agents, ultraviolet protection, or breathable systems to justify premium pricing and reduce the old safety-performance tradeoff. Kure Bazaar’s RTC range reflects this approach through serum-polish positioning and a formula story built around repair and visible care, while Butter London’s 2026 Nail Blush launch shows similar logic through a color-plus-treatment format supported by user testing. Birkenstock’s April 2026 entry into a 23-free, vegan, plant-based range is another sign that the non-toxic nail polish market now has enough commercial relevance to attract value-chain expansion from adjacent lifestyle brands.

Technology is altering the competitive balance in the non-toxic nail polish market from both the supply side and the demand side. On the supply side, contract manufacturers with strong Reserach and Development capabilities make it easier for smaller brands to access bio-based chemistry, which reduces the moat once created by formulation know-how alone. On the demand side, tools such as Aritificial Intelligence-led shade customization suggest that even historically offline advantages like broad assortment may become easier to replicate across digital touchpoints. The non-toxic nail polish market also still has open space in professional salon distribution for halal-breathable and durable compliant systems, especially in Gulf and Southeast Asian markets where many Western clean brands remain underrepresented. Compliance itself is becoming a competitive filter as International Standard's Organization (ISO) 22716-oriented manufacturing discipline and alignment with EU cosmetic rules matter more in buyer conversations than they did during the earlier phase of clean beauty growth

Non-Toxic Nail Polish Industry Leaders

Zoya

Ella + Mila

Butter London

Kure Bazaar SAS

Pacifica Beauty

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: CND relaunched the CND SHELLAC system with a next-generation Visible Light Lamp that avoids ultra-violent and LED curing, alongside nearly 140 new shades in a reformulated non-toxic architecture with patented GLIDE-OFF REMOVAL technology. The product directly addresses the professional salon segment's growing demand for toxin-reduced gel alternatives following the EU TPO ban.

- April 2026: Birkenstock launched a "23-free" vegan, plant-based nail polish collection in five shades as part of its CARE ESSENTIALS range, manufactured in Europe in 100% recyclable glass bottles using natural ingredients, including sugar beet and cane derivatives.

- March 2026: Fiabila unveiled SPF50+ Color Shield Nail Polish and a Nail'N'Hair Milky Serum (dual-function formula for nails and hair with ceramides, fatty acids, and argan oil) at Cosmoprof Bologna, the first colored nail polish incorporating SPF 50+ sun protection with ultraviolet A/ultraviolet B technology and antioxidant marine extracts, materially advancing the hybrid treatment-color architecture.

Global Non-Toxic Nail Polish Market Report Scope

Non-toxic nail polish avoids using certain chemicals, like formaldehyde, toluene, and DBP, that are often found in traditional formulas. The non-toxic nail polish market is segmented by type, coat type, distribution channel, and geography. By type, the market is segmented into traditional/liquid, gel, dip powder, and others. By coat type, the market is segmented into base coat and top coat. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online retail stores, salons, and others. By Geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, market sizing and forecasts were made based on the value (USD).

| Traditional/Liquid Nail Polish |

| Gel Nail Polish |

| Dip Powder Nail Polish |

| Others |

| Base Coat |

| Top Coat |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Salons |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Traditional/Liquid Nail Polish | |

| Gel Nail Polish | ||

| Dip Powder Nail Polish | ||

| Others | ||

| By Coat Type | Base Coat | |

| Top Coat | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Salons | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 size and 2031 outlook for non-toxic nail polish?

The non-toxic nail polish market stands at USD 0.83 billion in 2026 and is forecast to reach USD 1.11 billion by 2031 at a 5.86% CAGR.

Which product format is largest today?

Traditional/Liquid Nail Polish led with 60.5% share in 2025 because it combines broad availability, simple use, and established brand familiarity.

What are the main constraints on wider adoption?

Higher formulation and certification costs, plus the remaining durability gap versus conventional long-wear products, continue to limit broader switching in some buyer groups.

Which sales channel is gaining the most traction?

Online Retail Stores are projected to grow at 7.3% CAGR through 2031 as clean brands use digital discovery, direct selling, and social commerce to scale faster.

Page last updated on: