Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

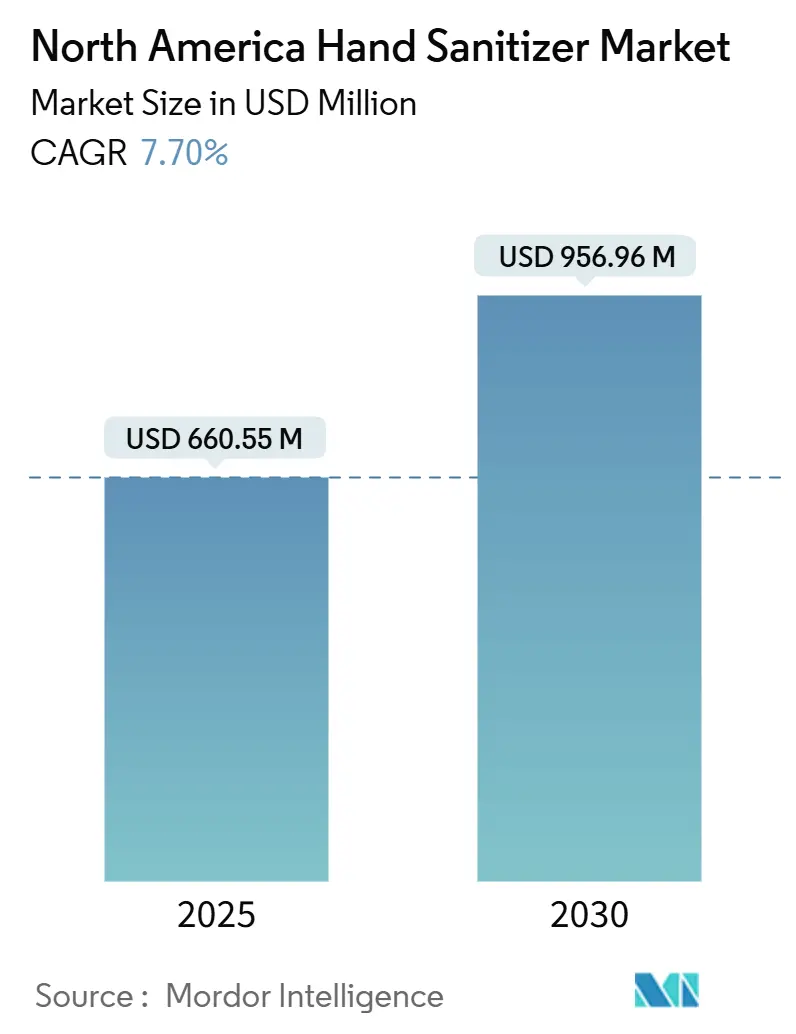

| Market Size (2025) | USD 660.55 Million |

| Market Size (2030) | USD 956.96 Million |

| Growth Rate (2025 - 2030) | 7.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Hand Sanitizer Market Analysis by Mordor Intelligence

The North America hand sanitizer market, valued at USD 660.55 million in 2025, is projected to reach USD 956.96 million by 2030, growing at a CAGR of 7.70%. The market's evolution from a pandemic-driven surge to sustained growth reflects fundamental behavioral shifts in hygiene consciousness, with hand sanitization becoming a core component of public health infrastructure across commercial and residential settings. While traditional market growth was limited by general consumer awareness of hand hygiene, the convenience of sanitizers compared to handwashes has attracted a substantial consumer base. This shift, combined with increased institutional adoption and regulatory compliance, has established a stable foundation for continued market expansion. Healthcare facilities, educational institutions, and corporate offices have integrated hand sanitizer dispensers into their standard operational protocols, further driving market demand. The integration of advanced formulations, including organic and natural ingredients, has expanded consumer choice and market penetration. Additionally, manufacturers' focus on sustainable packaging and eco-friendly solutions has resonated with environmentally conscious consumers, contributing to market growth.

Key Report Takeaways

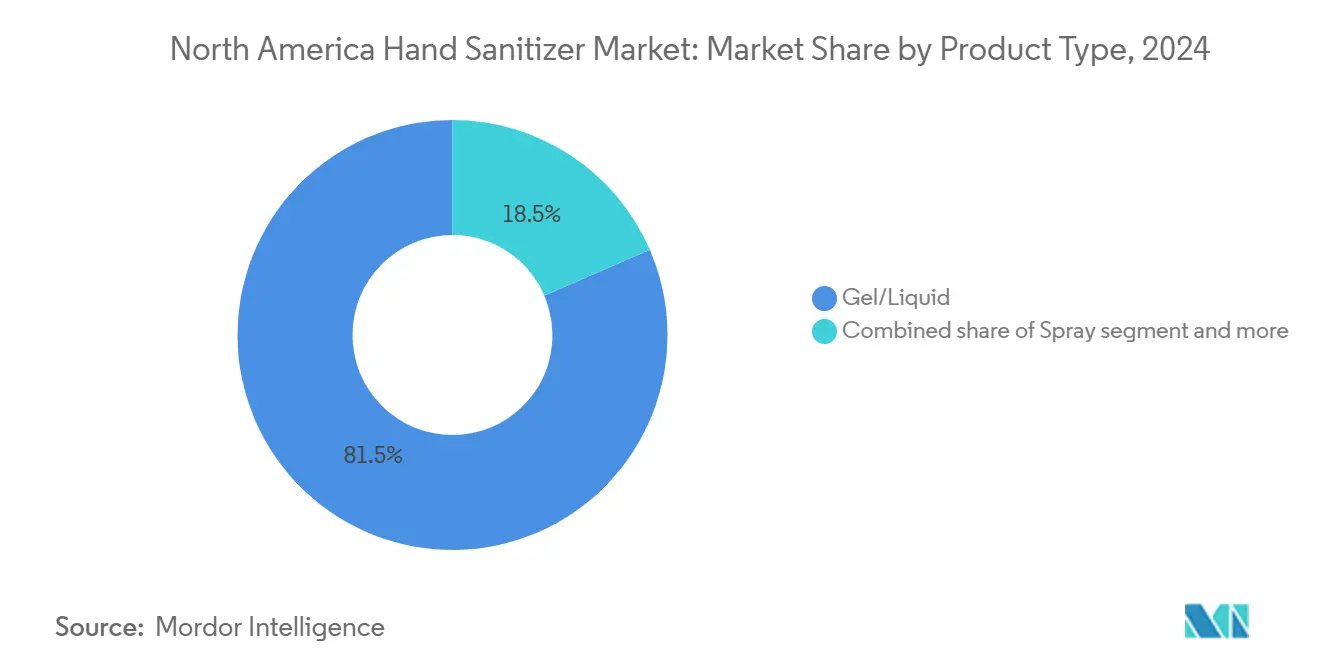

- By product type, gel/liquid formats led with 81.48% of hand sanitizer market share in 2024, while other product types are projected to grow at a 7.94% CAGR through 2030 across North America.

- By end user, adults accounted for 83.59% of the hand sanitizer market size in 2024; the kids/children’s segment is forecast to advance at an 8.44% CAGR to 2030, driven by pediatric-safe, alcohol-free lines.

- By ingredients, conventional formulations held 78.48% of hand sanitizer market share in 2024, whereas natural ingredients are expected to register an 8.74% CAGR over the outlook period.

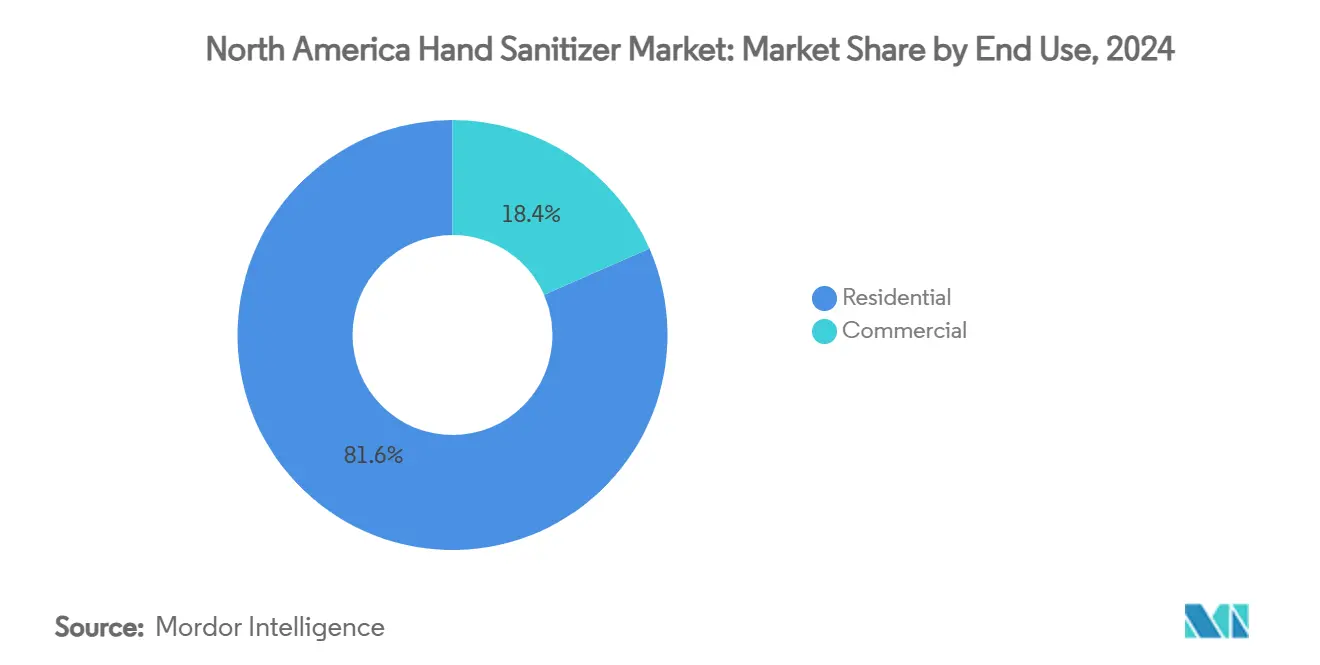

- By end use, residential applications captured 81.58% of the hand sanitizer market size in 2024; commercial settings are expanding at a 9.25% CAGR on the back of permanent dispenser installations.

- By geography, the United States dominated with an 88.65% share of the hand sanitizer market in 2024, and Mexico is set to post the fastest 9.63% CAGR through 2030 on rising commercial real estate and hygiene standards.

North America Hand Sanitizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing emphasis on hygiene and sanitation | +2.1% | North America, strongest in US healthcare | Long term (≥ 4 years) |

| Increased consumer awareness post-COVID | +1.8% | Global, highest in US and Canada | Medium term (2-4 years) |

| Technological advancement in ingredients | +1.3% | North America innovation centers | Long term (≥ 4 years) |

| Consumers’ shift to natural and organic | +1.0% | US and Canada premium tiers | Medium term (2-4 years) |

| Growth in real estate development | +0.8% | Mexico and US commercial projects | Short term (≤ 2 years) |

| Social media influence and endorsements | +0.4% | US and Canada consumer markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Emphasis on Hygiene and Sanitation

North American institutions have transitioned from reactive hygiene measures to proactive investments, driven by CDC recommendations for hand sanitizers with at least 60% alcohol as an alternative to soap and water [1]Source: Centers for Disease Control and Prevention, “Hand Sanitizer Use and Effectiveness,” cdc.gov. These evidence-based protocols have created sustained market demand, resilient to temporary health concerns, seasonal changes, and economic cycles, reflecting a long-term shift in hygiene practices. The inclusion of hand sanitizer dispensers in building codes further supports this change. Educational, healthcare, and corporate institutions now allocate budgets for sanitization infrastructure and maintain strategic reserves to ensure uninterrupted supply.

Increased Consumer Awareness About the Product

Through education campaigns and public health initiatives, consumers now possess a deeper understanding of hand sanitizers, focusing on ingredients, formulation effectiveness, and proper application rather than just alcohol content. This awareness aligns with U.S. healthcare spending trends, which rose by 7.5% in 2023 to USD 4.9 trillion (USD 14,570 per person), representing 17.6% of GDP [2]Source: Centers for Medicare & Medicaid Services, “National Health Expenditure Data: 1960–2023,” cms.gov. These trends highlight strong market growth potential as consumers prioritize hygiene and preventive healthcare. The demand for products with antimicrobial properties and skin-friendly formulations has grown, with hand sanitizers becoming a staple in daily routines beyond traditional healthcare settings.

Technological Advancement in Terms of Ingredients

Hand sanitizer formulations have advanced beyond alcohol bases to include sustained-release technologies and alternative active ingredients. Alcohol-free options, such as those with benzalkonium chloride and hypochlorous acid, are gaining traction for their effectiveness against norovirus and non-enveloped viruses. Companies like SC Johnson Professional and Ecolab are introducing non-alcohol-based sanitizers, enabling product differentiation, premium pricing, and expanded market reach in North America. These innovations address concerns about skin sensitivity and dryness from alcohol-based products. Longer-lasting formulations appeal to healthcare and food service sectors, while added moisturizing agents enhance user compliance and antimicrobial efficacy.

Consumers' Inclination Towards Natural and Organic Sanitizers

Consumer awareness of natural hand sanitizers is rising, with many willing to pay a premium for products that balance antimicrobial properties with skin health benefits. Innovations like Stepan's alcohol-free foaming hand sanitizer, which meets FDA standards and offers better skin compatibility, highlight this trend. Manufacturers are also adopting eco-friendly packaging, such as refillable systems and biodegradable materials, to reduce environmental impact. As manufacturing scales improve, natural hand sanitizers are shifting from niche products to mainstream options in North America. Retailers are allocating more shelf space to these products, while educational efforts by manufacturers and healthcare organizations are driving market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory oversight | -1.4% | US and Mexico border, online channels | Short term (≤ 2 years) |

| Price fluctuation in raw material | -1.1% | North America manufacturing hubs | Medium term (2-4 years) |

| Health concerns over chemical ingredients | -0.8% | US and Canada premium tiers | Long term (≥ 4 years) |

| Strong penetration of other hand-cleaning products | -0.6% | Commercial and healthcare settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Oversight Impacts Market Growth

In fiscal year 2023, FDA reports showed that 71.6% of alcohol-based hand sanitizers from newly registered domestic manufacturers in North America failed quality standards [3]Source: International Society for Pharmaceutical Engineering, “FDA FY 2023 Report on Hand Sanitizer Quality,” ispe.org . Violations related to formulation and contamination led to recalls, manufacturing suspensions, and increased compliance costs, particularly for smaller manufacturers. To meet FDA standards, many invested heavily in testing facilities and quality assurance. Heightened scrutiny also extended product approval timelines and raised entry barriers, consolidating market share among established manufacturers with strong quality control systems.

Price Fluctuation in Raw Material

Fluctuations in ethanol pricing, driven by agricultural commodity cycles and biofuel policies, are increasing formulation costs, particularly for institutional manufacturers. While the WHO supports local production for economic benefits, North American manufacturers face higher labor and regulatory costs than global competitors. Larger firms are adopting vertical integration to address cost pressures, creating barriers for new entrants. Rising raw material volatility and operational expenses have led manufacturers to optimize supply chains, invest in automation, and improve process efficiency to maintain quality. These dynamics have also accelerated industry consolidation, with major players acquiring smaller firms to achieve economies of scale and strengthen market positions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Alternative Formats Drive Innovation

In 2024, gels and liquids command a dominant 81.48% of the market, underscoring entrenched consumer preferences and institutional buying habits. Yet, the spray segment is on the rise, boasting a robust 7.94% CAGR through 2030, with dried powder formulations leading the charge. These cutting-edge formats deliver prolonged antimicrobial protection, owing to their sustained-release mechanisms, outpacing the effectiveness of traditional liquids. Such alternative formats are gaining traction, especially in healthcare and industrial sectors, where extended protection is paramount for upholding hygiene standards.

While gels and liquids continue to reign supreme, bolstered by well-established distribution channels and user familiarity, they grapple with mounting competition from these novel formats. The market is evolving, with a pronounced shift towards valuing functional performance over mere sanitization. Despite their higher unit costs, attributed to specialized packaging, spray formats strike a harmonious balance between user-friendly application and the familiar traits of liquids. This market evolution not only paves the way for premium positioning but also highlights specialized applications that promise fatter margins than traditional gels. The trend towards diversification is further underscored by a surge in research and development investments, focusing on innovative delivery systems and advanced formulation technologies.

By End User: Children's Safety Drives Specialized Formulations

In 2024, adults account for a dominant 83.59% share of the market, underscoring established usage patterns and institutional procurement cycles. Yet, the children's segment is on a rapid ascent, boasting an 8.44% CAGR through 2030. This surge is fueled by heightened safety awareness and the development of specialized products catering to pediatric needs. A notable trend is the rising preference for alcohol-free formulations, utilizing benzalkonium chloride and natural ingredients. These alternatives promise reduced toxicity and better skin compatibility over traditional alcohol-based products. Responding to this shift, manufacturers are increasingly rolling out child-centric product lines, emphasizing gentle formulations for sensitive skin.

The children's segment stands out in product development and market strategy. Pediatric formulations, due to their rigorous safety testing and specialized anti-ingestion packaging, command premium prices. As the segment evolves, children's products are not just seen as safety-first options but are emerging as platforms for innovation. This shift is steering broader market trends, especially towards natural ingredients and sustained-release technologies. Research shows parents are now more inclined to invest in children's products that prioritize safety and natural components, bolstering the segment's revenue growth.

By End Use: Commercial Sector Drives Infrastructure Investment

In 2024, residential applications dominate the hand sanitizer market with an 81.58% share, driven by widespread consumer adoption and regular replenishment cycles. The commercial segment is growing at a 9.25% CAGR through 2030, supported by enhanced workplace safety protocols and public facility standards exceeding pre-pandemic levels. The National Fire Protection Association's standardized requirements for alcohol-based hand sanitizer dispensers further boost the commercial market [4]Source: National Fire Protection Association, “NFPA 101 Public Input Report 2023,” nfpa.org . Increased health awareness and the integration of hand sanitizers into daily household routines, especially in high-traffic areas, reinforce the residential segment's dominance.

The commercial sector is expanding with permanent sanitization setups in offices and retail spaces, requiring specialized dispensing systems and bulk packaging. These factors create entry barriers and enable premium pricing for suppliers meeting institutional needs. This shift reflects a lasting change in hygiene practices, establishing predictable demand patterns that support long-term supply agreements and product innovation. Healthcare facilities, schools, and hospitality venues drive demand through comprehensive sanitization programs with regular monitoring and maintenance of dispensing systems.

By Ingredients: Natural Formulations Gain Commercial Viability

Conventional ingredients dominate the market with a 78.48% share in 2024, supported by proven efficacy profiles, established supply chains, and cost advantages. However, these formulations face growing concerns regarding skin irritation and environmental impact, creating opportunities for natural alternatives, which are projected to grow at an 8.74% CAGR through 2030. The widespread availability and standardized manufacturing processes of conventional ingredients continue to make them the preferred choice for many manufacturers, despite the emerging challenges.

Natural formulations are transitioning from niche premium products to mainstream alternatives by achieving cost parity without sacrificing performance. Regulatory changes, such as FDA guidelines recognizing plant-based antimicrobial agents, support this shift. As manufacturing scales commercially and consumers pay premiums for sustainability, natural and organic formulations gain market traction. Increased R&D in natural ingredient processing is improving production efficiency and product stability, driving this evolution.

Geography Analysis

The United States holds a commanding 88.65% market share in 2024, supported by its robust consumer goods infrastructure and established regulatory frameworks. In contrast, Mexico emerges as the region's fastest-growing market with a projected 9.63% CAGR through 2030, driven by expanding commercial real estate development and evolving hygiene standards. The U.S. market benefits from extensive distribution networks and sophisticated retail channels that ensure widespread product availability. Additionally, stringent quality control measures and consumer protection regulations maintain high product standards, fostering consumer trust and market stability.

Mexico's growth trajectory is underpinned by significant infrastructure development and increasing hygiene consciousness, creating sustained demand across residential and commercial sectors. The country's integration with North American supply chains provides access to advanced formulations, while its developing local manufacturing capabilities reduce costs and improve product availability. This combination of factors positions Mexico favorably for both domestic consumption and export opportunities. The government's initiatives to improve public health standards have accelerated market growth, particularly in urban areas. Furthermore, rising disposable incomes and urbanization contribute to increased consumer spending on hygiene products.

Canada's market maturity offers stability through established procurement cycles and regulatory compliance. Its proximity to US innovation centers enables quick adoption of new technologies and formulations, enhancing market competitiveness. The regional trade integration facilitates technology transfer and regulatory harmonization, particularly benefiting Mexico's adoption of sophisticated sanitization practices in commercial and institutional settings, extending beyond residential applications to workplace safety protocols and public facility requirements. Canadian consumers demonstrate high awareness of environmental sustainability, driving demand for eco-friendly products. The country's robust healthcare system also influences institutional buying patterns, maintaining consistent demand levels throughout economic cycles.

Competitive Landscape

The North America hand sanitizer market demonstrates moderate fragmentation, characterized by a mix of established consumer goods companies and specialized manufacturers. Major players like Reckitt Benckiser, Church & Dwight Co., Inc., and Henkel AG & Company hold significant market share, leveraging their brand equity and extensive distribution networks to maintain leadership positions. However, they face growing competition from specialized sanitization companies and natural product manufacturers who target specific consumer segments with differentiated formulations.

Strategic collaborations have emerged as a key competitive strategy in the market. For example, Touchland's partnership with Disney in May 2025 to launch a limited edition Mickey Mouse hand sanitizer case showcases how manufacturers are combining product innovation with brand partnerships to expand their consumer reach and enhance market presence. These collaborations often extend beyond product development to include joint marketing initiatives and shared distribution channels. Additionally, such partnerships enable companies to tap into new consumer segments and create unique value propositions in an increasingly competitive market environment.

The market continues to present growth opportunities in specialized applications, particularly where traditional formulations show limitations. This is evident in areas such as norovirus prevention, where alcohol-based sanitizers demonstrate reduced effectiveness compared to hypochlorous acid alternatives. These gaps in traditional product effectiveness create potential growth segments for innovative manufacturers who can develop targeted solutions. The demand for specialized formulations has led to increased research and development investments across the industry. Furthermore, regulatory support for novel sanitization technologies has encouraged manufacturers to explore advanced antimicrobial compounds and delivery systems.

North America Hand Sanitizer Industry Leaders

Reckitt Benckiser Group PLC

3M Company

Henkel AG & Company, KGaA

Unilever Plc

Church & Dwight Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Church & Dwight acquired Touchland, a hand sanitizer brand, for USD 880 million. The acquisition strengthens Church & Dwight’s position in the personal care and hygiene market.

- April 2025: Safetec of America launched a 2 oz. Instant Hand Sanitizer Spray. The product features a no-touch application system and contains aloe vera for moisturizing. The formula eliminates 99.9% of germs.

- March 2025: SC Johnson Professional introduced Alcare® Enhanced hand sanitizer with OPTIDOSE™ technology for industrial, institutional, and healthcare applications. This foaming sanitizer expands the company’s existing Alcare® Enhanced product line.

- January 2025: Touchland launched its products at Sephora Canada, introducing a hand sanitizer that eliminates germs while maintaining skin hydration.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North America hand-sanitizer market as all alcohol-based and alcohol-free gels, liquids, sprays, and foams expressly formulated for skin hygiene and distributed through retail shelves, online channels, and institutional refill systems across homes, workplaces, schools, healthcare, food service, travel hubs, and other public venues.

Scope exclusion: Products such as surgical scrubs, antibacterial hand soaps, surface wipes, and standalone dispenser hardware are not counted.

Segmentation Overview

- By Product Type

- Gel/Liquid

- Spray

- Other Product Types

- By End User

- Adult

- Kids/Children

- By Ingredients

- Conventional

- Natural and Organic

- By End Use

- Residential

- Commercial

- By Geography

- United States

- Canada

- Mexico

- Rest of North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed infection-control nurses, distributor buyers, contract-cleaning supervisors, and brand R&D chemists across the United States, Canada, and Mexico. These conversations clarified real-world usage rates, dispenser refill cycles, emerging natural-ingredient preferences, and typical contract pricing, allowing us to reconcile secondary figures and test model sensitivities.

Desk Research

We began with open-access authorities, including Centers for Disease Control and Prevention advisories, US FDA OTC drug monograph filings, Health Canada Natural Health Product registers, and OSHA hygiene mandates, before layering United States International Trade Commission HS-code import data and Bureau of Labor Statistics production indices to size domestic output trends. Trade-association bulletins from the American Cleaning Institute, Canadian Consumer Specialty Products Association, and the Mexican Chamber of the Chemical Industry enriched demand signals. Commercial disclosures pulled from D&B Hoovers and Dow Jones Factiva, alongside peer-reviewed journals on ethanol efficacy, anchored price and formulation benchmarks. This list is illustrative; many additional sources informed data checks and narrative context.

Market-Sizing & Forecasting

Top-down reconstruction starts with population and workforce cohorts mapped to sanitizer-adoption penetration and average annual consumption (ml per capita or per bed), which are then valued using weighted average selling prices captured from retail panel data and institutional procurement quotes. Supplier roll-ups of leading fill-line capacities and sampled e-commerce unit sales provide bottom-up reasonableness checks. Key variables like hospital bed density, food-service outlet growth, CDC campaign intensity index, ethyl-alcohol spot prices, and online search popularity feed an ARIMA-based forecast that is stress-tested through scenario analysis before final calibration.

Data Validation & Update Cycle

Outputs undergo variance screens against independent hygiene-product shipments and customs trends. Senior reviewers challenge anomalies, and findings are re-checked with a subset of earlier experts. Reports refresh every twelve months, with interim flashes if regulation, supply shocks, or public-health events materially shift the baseline.

Why Mordor's North America Hand Sanitizer Baseline Numbers Stand Firm

Published market values often diverge; definitions, channel mix, and update rhythms seldom align across firms.

Our disciplined scope and annual refresh keep the baseline tightly tied to in-market variables.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 660.55 Mn (2025) | Mordor Intelligence | - |

| USD 1.34 Bn (2024) | Global Consultancy A | Combines dispenser equipment and bulk surface sanitizers with personal-use formats |

| USD 1.65 Bn (2024) | Trade Journal B | Uses list prices and includes Latin-American spill-over sales reported by U.S. exporters |

| USD 1.54 Bn (2023) | Research Publisher C | Retains pandemic spike volumes, with no post-COVID demand taper adjustment |

In sum, by isolating true personal-hand-hygiene products, validating usage metrics with frontline stakeholders, and refreshing figures yearly, Mordor Intelligence delivers a balanced, transparent baseline stakeholders can rely on for confident decision-making.

Key Questions Answered in the Report

What is the current size of the North America hand sanitizer market?

The hand sanitizer market stands at USD 660.55 million in 2025 and is projected to reach USD 956.96 million by 2030.

Which product type leads market revenue in North America?

Gel/liquid formats command 81.48% of market revenue, supported by institutional bulk procurement.

Why is Mexico the fastest-growing country market?

Mexico benefits from rapid commercial real estate expansion, updated hygiene regulations, and cost-competitive local production, driving a 9.63% CAGR.

How are natural formulations influencing the market?

Natural and organic sanitizers are growing at an 8.74% CAGR as consumers seek gentler, eco-friendly options that now match conventional efficacy.

Which end-use segment is expanding the fastest?

Commercial settings, including offices and retail venues, are advancing at a 9.25% CAGR as permanent dispenser installations become part of building standards.

How is the children’s segment evolving?

Pediatric formulations, often alcohol-free and packaged for safety, are expanding at an 8.44% CAGR driven by heightened school hygiene protocols.

Page last updated on: