NFC Juice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 22.71 Billion |

| Market Size (2031) | USD 28.49 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

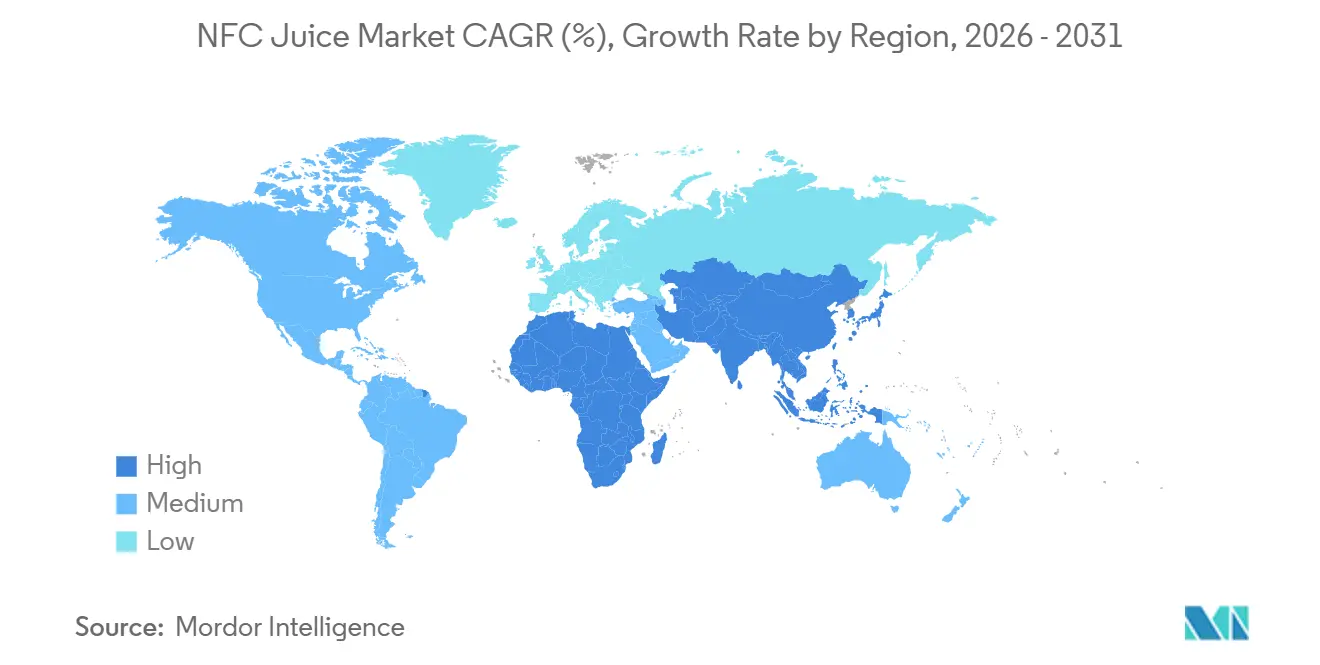

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

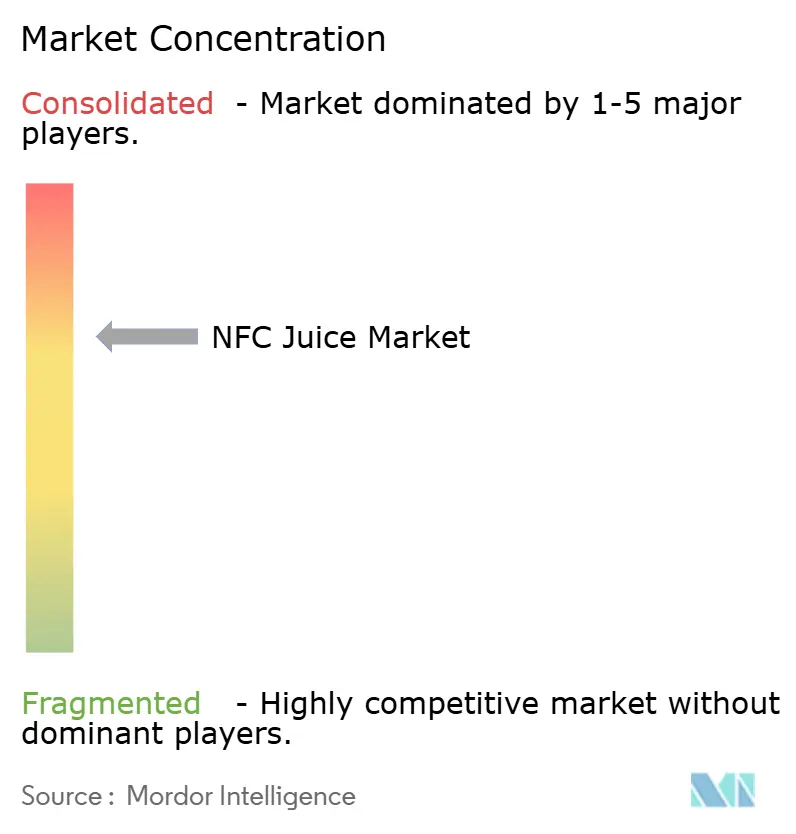

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

NFC Juice Market Analysis by Mordor Intelligence

The NFC juice market size was valued at USD 21.72 billion in 2025 and estimated to grow from USD 22.71 billion in 2026 to reach USD 28.49 billion by 2031, at a CAGR of 4.63% during the forecast period (2026-2031). Import dependence for citrus, widening adoption of high-pressure processing (HPP), and a shift toward functional, wellness-positioned juice formats continue to reshape supply chains. Vegetable-based NFC lines are gaining share as consumers search for lower-sugar, nutrient-dense options, while premium organic SKUs are accelerating behind USDA certification that guarantees a three-year pesticide-free land history. Processing innovation is lowering costs; 600-liter HPP systems, such as Quintus Technologies’ QIF 600L, deployed at WakeFresh in April 2026, now achieve throughputs of 4,150 kg per hour, underscoring a scale inflection that brings cold-pressed quality into mass-market territory. Key brand strategies emphasize portfolio pruning and retail realignment. Coca-Cola exited frozen concentrates in February 2026 after category sales fell 8% year-over-year, redeploying investment toward chilled Simply and functional shot lines. Online direct-to-consumer models help small brands bypass refrigerated shelf competition, supporting the NFC juice market’s evolution from commoditized breakfast beverage to premium, subscription-based wellness staple.

Key Report Takeaways

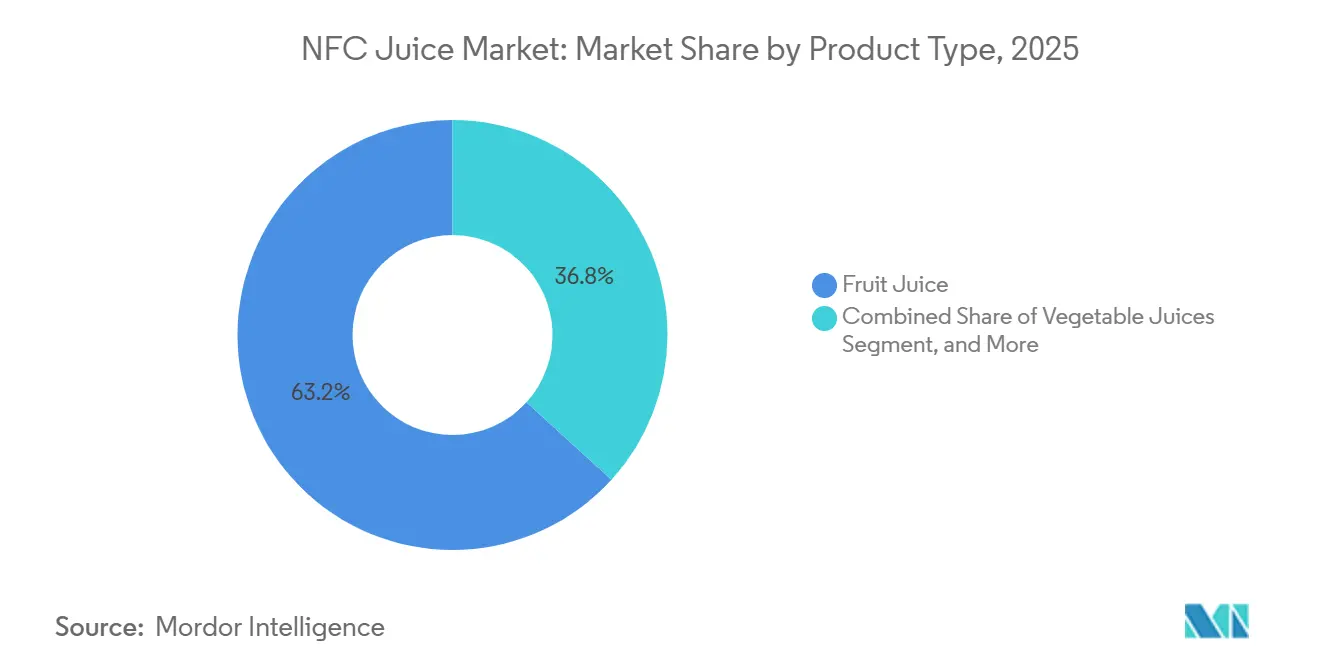

- By product type, fruit juice led with 63.25% of the NFC juice market share in 2025, whereas vegetable juices are advancing at a 5.57% CAGR through 2031.

- By category, conventional products accounted for 85.58% of the NFC juice market size in 2025, while organic variants recorded the highest projected CAGR at 6.63% through 2031.

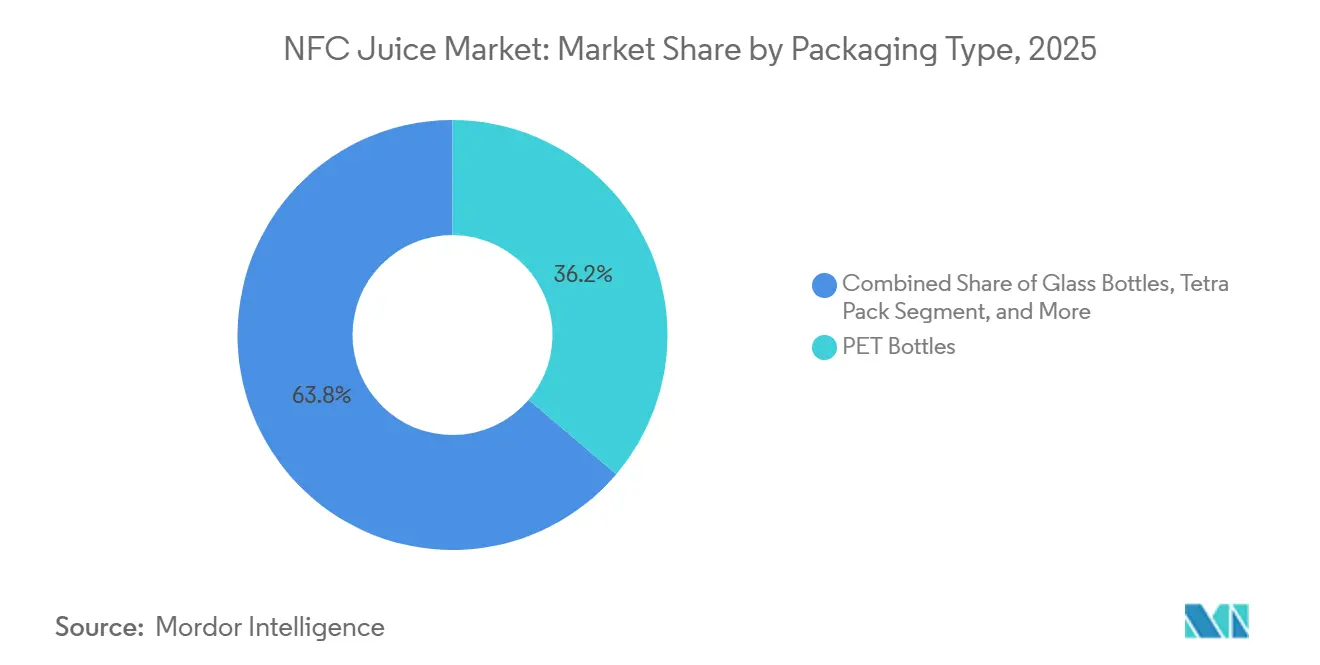

- By packaging, PET bottles captured 36.21% of the NFC juice market in 2025, and pouches are forecast to register a 5.76% CAGR through 2031.

- By distribution, hypermarkets and supermarkets held 41.86% share in 2025, whereas online retail is expanding at a 7.79% CAGR, the fastest channel until 2031.

- By geography, North America accounted for 31.44% of the value in 2025, yet Asia-Pacific is poised to grow at a 6.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global NFC Juice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-Pressed and HPP Differentiation | +1.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Functional NFC Shot Formats (Immunity, Gut, Energy) | +0.9% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Advancements in Cold-Press and Gentle Processing Technology | +0.7% | Global | Long term (≥ 4 years) |

| Expansion of Premium and Organic Product Lines | +0.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Foodservice and Café Fresh-Juice-Bar Positioning | +0.5% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Regulatory Push Toward Transparent Labeling | +0.4% | Global, emphasis on North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cold-pressed and high-pressure processing (HPP) differentiation

HPP enables NFC producers to extend refrigerated shelf life to 30-45 days without thermal degradation of heat-sensitive vitamins and polyphenols, creating a premium tier that commands 15-25% price premiums over pasteurized equivalents. Quintus Technologies' installation of a QIF 400L-5400 system at Portugal's Frubaça cooperative in July 2025 exemplifies European capacity expansion to meet clean-label demand for preservative-free juices, smoothies, and purées. Daily Dose Juice UK reported throughput increases exceeding 100%, from approximately 100,000 bottles per week to over 400,000, after installing Avure HPP equipment, enabling 24-hour continuous production and reducing reliance on third-party tollers. The technology's limitation lies in packaging constraints: HPP requires flexible, waterproof containers, typically PET, which raises sustainability concerns as plant-based PET and polylactic acid alternatives face cost and oxygen-barrier challenges critical for NFC shelf stability. Capital intensity remains a barrier for mid-tier brands; machines can cost more than USD 3 million, pushing smaller producers toward pay-per-use tolling arrangements that sacrifice margins for flexibility.

Functional NFC shot formats (Immunity, Gut, Energy)

Small-format wellness shots, typically 60 to 120 milliliters, are capturing share by delivering concentrated functional ingredients (probiotics, prebiotics, adaptogens, vitamins) in single-serve doses that align with "food as medicine" consumer behavior. Suja Organic's Digestion Goldenberry Wellness Shot, launched nationwide at Kroger, combines probiotics and prebiotic fiber with goldenberry, pear, and ginger, targeting gut-health claims that resonate with over 50% of consumers who view digestive wellness as important. Mockingbird's Raw Gut Shot, retailing at GBP 6.25 (approximately USD 7.90) for 420 milliliters in select Waitrose stores, incorporates chicory root fiber as a prebiotic alongside lemon, honey, and lemon balm. The segment benefits from "fibermaxxing" social trends and clinical evidence linking fiber intake to reduced cardiovascular disease and type 2 diabetes risk, yet faces the challenge that many mood-support and adaptogen ingredients require consistent daily use rather than delivering acute, perceptible effects that drive repeat purchase. Brands must balance functional efficacy with taste; consumers will not sacrifice flavor for wellness claims, making HPP-preserved fresh fruit profiles a competitive advantage over concentrate-based formulations.

Advancements in cold-press and gentle processing technology

Equipment innovation is lowering the technical and economic barriers to gentle processing, enabling regional cooperatives and startup brands to compete on quality without a multinational scale. Quintus Technologies' QIF 600L system, delivered to WakeFresh in China for April 2026 installation, features a 600-liter cycle capacity and 47-centimeter pressure vessel diameter, achieving 4,150 kilograms per hour throughput and positioning HPP as viable for high-volume production rather than niche artisanal batches[1]Source: Quintus Technologies, “World’s Largest High Pressure Processing System,” prweb.com. JBT Avure's modular AV-X series allows processors to start with smaller capacities (AV-40X) and expand via add-on accessories, reducing the upfront capital commitment. HPP's ability to inactivate vegetative pathogens (achieving 5-7 log reductions comparable to thermal pasteurization) while preserving low-molecular-weight flavor and nutrient compounds supports NFC's fresh-like positioning, yet incomplete enzyme inactivation, particularly polyphenol oxidase and pectin methylesterase, can cause browning and texture changes during storage, necessitating refrigeration and hurdle strategies such as mild heat or natural antimicrobials. The technology's unpredictable performance across fruit matrices (effective for high-water-content avocados, less suitable for air-pocket fruits like strawberries unless formulated appropriately) requires processors to optimize pressure, time, and cycling for each SKU, adding complexity to multi-product lines.

Expansion of premium and organic product lines

Organic NFC juice growth at 6.63% CAGR reflects consumer willingness to pay premiums for USDA-certified products that meet stringent land-management and input requirements. USDA National Organic Program standards mandate that land used for organic juice crops must have had no prohibited substances applied for at least 3 years prior to harvest, and products labeled "organic" must contain at least 95% certified organic content to display the USDA seal[2]Source: USDA Agricultural Marketing Service, “Organic Standards,” ams.usda.gov. Organic processing apples in Washington traded at USD 250 to USD 300 per ton in April 2026, versus USD 75 to USD 130 for conventional stock, illustrating the raw-material cost premium that organic NFC brands must either absorb or pass through, according to the USDA AMS Apple Processing Report. Certification complexity, particularly commingling prevention, documentation of non-agricultural inputs, and verification that all ingredients are organically produced unless listed under specific exemptions, creates operational friction for multi-line processors handling both conventional and organic SKUs. The segment's appeal extends beyond health-conscious consumers to include parents seeking pesticide-free options for children and environmentally motivated buyers, yet supply-chain transparency requirements and third-party audits add cost and administrative burden that favor larger, vertically integrated players or dedicated organic cooperatives

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Chilled Shelf-Space in Price-First Retailers | -0.6% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Fruit-Price Volatility Squeezing Margins | -0.8% | Global | Short term (≤ 2 years) |

| Regulatory and Certification Complexity for Organic NFC | -0.3% | North America, Europe | Medium term (2-4 years) |

| Substitution Risk from Whole Fruits and Smoothies | -0.5% | Global, led by developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited chilled shelf-space in price-first retailers

Refrigerated shelf allocation in mass-market grocery and discount chains prioritizes high-turnover dairy, ready meals, and protein products, leaving NFC juice brands to compete for limited linear footage against yogurt, plant-based milk, and grab-and-go meal kits. Retailers impose slotting fees, promotional calendars, and velocity thresholds that smaller NFC brands struggle to meet, effectively ceding prime eye-level positions to multinational beverage companies with category-captain relationships. The constraint is most acute in price-sensitive formats, where ambient juice boxes and shelf-stable concentrates occupy far more facings than chilled NFC products, and where consumers prioritize unit price over fresh-like attributes. Cold-chain logistics add complexity and cost: NFC requires unbroken refrigeration from processing through retail, increasing shrink from temperature excursions and limiting distribution to stores with adequate cooler capacity. This structural disadvantage explains why online retail is growing at 7.79% CAGR; direct-to-consumer models bypass retail shelf negotiations and enable subscription delivery that guarantees freshness, though at the cost of higher last-mile logistics expenses.

Fruit-price volatility squeezing margins

Citrus greening disease (Huanglongbing) and adverse weather events have decimated Florida orange production, which fell to 522,000 tons in 2024-25, down 35% from the prior season, pushing processing orange on-tree-equivalent prices to USD 11.48 per box, a 74% year-over-year increase, according to the USDA ERS Fruit and Tree Nuts Outlook. Apple juice concentrate spot prices ranged from USD 13.31 to USD 27.00 per gallon in April 2026, while import offers from China ranged from USD 10.45 to USD 12.05 per gallon, highlighting the price dispersion that complicates procurement planning, according to the USDA AMS Apple Processing Report. Brands with long-term supply contracts or vertical integration into orchards can partially hedge input-cost risk, but most NFC producers operate on spot or short-term agreements that expose them to seasonal and annual swings. The inability to pass through rapid price increases without losing price-sensitive consumers compresses gross margins, particularly for mid-tier brands lacking the scale to negotiate volume discounts or the premium positioning to justify retail prices above USD 5 per liter.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vegetable Juices Gain on Wellness Shift

Fruit juice held 63.25% market share in 2025, anchored by orange, apple, and citrus blends that dominate refrigerated and shelf-stable facings, yet vegetable juices are forecast to expand at 5.57% CAGR through 2031, outpacing the category average as consumers seek lower-sugar, nutrient-dense alternatives. Orange juice within the fruit segment faces structural headwinds from Florida production collapse; U.S. domestic orange juice production is forecast at approximately 100 million single-strength-equivalent gallons in 2024-25, down from over 1 billion gallons two decades ago, with import share reaching 87%, according to the USDA ERS Fruit and Tree Nuts Outlook. Apple juice benefits from more diversified sourcing (Washington, New York, Appalachian regions, plus imports from Turkey, Canada, and China) but faces consumer skepticism over sugar content despite NFC's fresh positioning. Citrus blends and tropical variants (mango, pineapple, passion fruit) capture premiumization opportunities by offering exotic flavor profiles and vitamin C fortification, yet remain niche relative to orange and apple. Fruit and vegetable blends occupy a middle ground, combining the familiarity of fruit sweetness with the health halo of vegetable inclusion (carrot, beet, spinach), and appeal to consumers seeking gradual transitions toward vegetable-forward diets.

Vegetable juices, pure carrot, beet, tomato, and green blends, are leveraging functional claims around nitrates for cardiovascular health, antioxidants, and lower glycemic impact. The segment's growth is concentrated in urban centers with health-conscious demographics willing to pay USD 4 to USD 8 per liter for cold-pressed, HPP-treated vegetable SKUs positioned as meal replacements or post-workout recovery drinks. Suja Organic's expansion into probiotic-fortified cold-pressed juices, including watermelon-based variants with 1 billion CFU probiotics per 12-ounce bottle, illustrates how brands are blurring product-type boundaries by adding functional ingredients that appeal across fruit and vegetable platforms. Regulatory influence from FDA labeling requirements ensures that vegetable juice blends disclose percentage composition, preventing misleading "vegetable juice" claims on predominantly fruit-based products.

By Category: Organic Accelerates Despite Certification Hurdles

Conventional NFC products commanded 85.58% market share in 2025, reflecting their price accessibility, widespread retail distribution, and consumer familiarity, yet organic variants are growing at 6.63% CAGR, the fastest among category segments, driven by parents seeking pesticide-free options, environmentally motivated buyers, and premium-positioned brands leveraging USDA certification as a quality signal. Organic NFC must meet USDA National Organic Program standards requiring at least 95% certified organic content and a 3-year pesticide-free land history, creating supply constraints that sustain price premiums of 30-50% over conventional equivalents, according to the USDA AMS Organic Standards. Washington organic processing apples traded at USD 250 to USD 300 per ton in April 2026 versus USD 75 to USD 130 for conventional stock, illustrating the raw-material cost differential that organic NFC brands must absorb or pass through, according to the USDA AMS Apple Processing Report.

The segment's expansion is concentrated in North America and Europe, where organic retail penetration is highest, and consumers are willing to pay for certified products. Certification complexity, particularly commingling prevention, documentation of non-agricultural inputs, and third-party audits, favors vertically integrated organic cooperatives and dedicated organic brands over conventional players attempting line extensions. Organic NFC benefits from the broader "clean label" trend, where consumers scrutinize ingredient lists and processing methods, yet faces the challenge that organic certification alone does not guarantee minimal processing or superior nutritional content compared to conventional NFC. Brands are layering additional claims (non-GMO, fair trade, carbon-neutral) to differentiate within the organic tier, creating sub-segments that command even higher premiums but risk fragmenting the market and confusing consumers.

By Packaging Type: Pouches Gain on Portion Control and Sustainability

PET bottles captured 36.21% of packaging share in 2025, benefiting from transparency that showcases product color and pulp, resealability for multi-serve formats, and compatibility with HPP processing, yet pouches are forecast to grow at 5.76% CAGR through 2031 as brands pursue portion control, on-the-go convenience, and sustainability narratives around lightweighting and material reduction. Glass bottles appeal to premium and organic segments seeking inert, recyclable packaging that avoids plastic migration concerns, but carry weight penalties that increase freight costs and breakage risk. Tetra Pak and other aseptic cartons dominate shelf-stable NFC (where permitted by processing method), offering extended ambient shelf life and efficient cube utilization, yet lack the fresh-like perception of refrigerated PET and glass. Cans are emerging in functional shot formats, leveraging aluminum's infinite recyclability and barrier properties, though consumer associations with carbonated soft drinks and beer can hinder acceptance of juice in cans.

Pouches, particularly stand-up formats with spouts or straws, are gaining traction in kids' segments (Capri Sun Hydrate's electrolyte-fortified juice pouch exemplifies this positioning) and single-serve adult wellness shots. The format's flexibility enables portion sizes from 60 milliliters (concentrated functional shots) to 250 milliliters (meal-replacement blends), and lightweighting reduces transportation emissions relative to glass or rigid PET. Sustainability claims, however, face scrutiny: many pouches use multi-layer laminates (plastic-aluminum-plastic) that complicate recycling, and plant-based alternatives (PLA, bio-PET) struggle with oxygen-barrier performance critical for NFC shelf stability. Brands must balance consumer demand for sustainable packaging with the technical requirements of HPP (flexible, waterproof containers) and refrigerated distribution (moisture resistance, seal integrity), creating trade-offs that favor incremental improvements (thinner PET, higher recycled content) over wholesale material shifts.

By Distribution Channel: Online Retail Surges on Subscription Models

Hypermarkets and supermarkets held 41.86% of the distribution share in 2025, anchored by their refrigerated shelf space, high foot traffic, and ability to offer promotional pricing, yet online retail is expanding at 7.79% CAGR, the fastest among all channels, as direct-to-consumer subscription models, cold-chain logistics improvements, and pandemic-accelerated e-commerce adoption reshape NFC purchasing behavior. Convenience and grocery stores serve immediate consumption occasions and top-up shopping, capturing share in single-serve formats (250-500 milliliters) priced at USD 3 to USD 5, but lack the breadth of assortment and promotional depth of larger formats. Other retail (specialty health stores, juice bars, gyms) commands premium pricing and targets wellness-focused consumers, yet represents a small share constrained by limited geographic reach.

Online retail's growth is driven by subscription services that deliver weekly or monthly NFC assortments directly to consumers, guaranteeing freshness (products often ship within 24-48 hours of pressing) and enabling brands to bypass retail shelf negotiations and slotting fees. The channel's economics favor high-margin, premium-positioned SKUs (organic, functional, cold-pressed) that justify last-mile delivery costs of USD 5 to USD 10 per order. Cold-chain logistics remain a constraint: NFC requires refrigerated transport and insulated packaging (gel packs, dry ice) that add cost and environmental footprint, and delivery failures (missed deliveries, temperature excursions) result in product loss and customer dissatisfaction. Brands are experimenting with regional micro-fulfillment centers and partnerships with grocery-delivery platforms (Instacart, Amazon Fresh) to reduce delivery windows and improve cold-chain reliability, yet the channel's profitability remains challenged by thin margins and high customer-acquisition costs.

Geography Analysis

North America commanded 31.44% of global NFC juice value in 2025, yet faces structural supply constraints that are reshaping sourcing strategies and import dependencies. U.S. orange juice production collapsed to approximately 100 million single-strength-equivalent gallons in 2024-25, down from over 1 billion gallons two decades ago, forcing import share to 87%, with Brazil and Mexico supplying roughly 95% of those imports, according to the USDA ERS Fruit and Tree Nuts Outlook[3]Source: Catharine Weber et al., “Fruit and Tree Nuts Outlook: March 2025,” Economic Research Service, ers.usda.gov . Florida's 2024-25 orange crop totaled 522,000 tons, down 35% from the prior season, as citrus greening disease and Hurricane Milton decimated bearing acreage, which fell to 188,400 acres, 61,400 acres below 2023-24, according to the USDA NASS Florida Citrus Summary. Processing orange on-tree-equivalent prices surged to USD 11.48 per box, a 74% year-over-year increase, compressing margins for NFC brands unable to pass through cost inflation, as per the USDA ERS Fruit and Tree Nuts Outlook. Coca-Cola's February 2026 decision to discontinue Minute Maid frozen concentrates in the U.S. and Canada, exiting the frozen-can category after nearly 80 years, signals a strategic shift toward chilled, ready-to-drink formats as frozen beverage sales declined nearly 8% in the 52 weeks ending January 24, 2026. Canada and Mexico within the region benefit from USMCA trade provisions that facilitate cross-border NFC flows, yet face similar retail shelf-space constraints and consumer shifts toward lower-sugar alternatives.

Asia-Pacific is forecast to expand at 6.37% CAGR through 2031, propelled by rising middle-class incomes in China, India, Indonesia, and Southeast Asia, where NFC is positioned as a premium, Westernized beverage category. China's WakeFresh, described as the country's largest HPP ready-to-drink product manufacturer, signed for Quintus Technologies' QIF 600L system (the world's largest HPP press) for April 2026 installation at its Anhui facility, underscoring domestic capacity expansion to serve urban demand for cold-pressed fruit and vegetable juices and cold-brew teas. India's organized retail penetration and cold-chain infrastructure improvements are enabling NFC distribution beyond metro cities, though price sensitivity and preference for fresh-squeezed juice from street vendors limit mass-market adoption. Japan, South Korea, and Singapore represent mature, high-value markets where functional NFC variants (collagen-infused, probiotic-fortified) command premium pricing, yet face competition from tea-based and fermented beverages. Australia's domestic citrus production and proximity to Southeast Asian export markets position it as a regional processing hub, though drought and labor shortages constrain supply.

Europe held a significant share in 2025, anchored by Germany, the United Kingdom, France, and the Netherlands, where organic and premium NFC penetration is highest and consumers demonstrate strong preference for local and regional sourcing. Frubaça's July 2025 installation of a Quintus QIF 400L-5400 HPP system at its COPA Fruit Centre in Portugal exemplifies European cooperative investment in gentle processing to meet clean-label demand for preservative-free juices and smoothies featuring IGP-certified apples. The European Union's organic certification framework and pesticide-residue regulations impose stricter standards than many other regions, creating both a barrier to entry for non-EU suppliers and a quality signal that European NFC brands leverage in export markets. Spain and Italy benefit from Mediterranean citrus production (oranges, lemons), though yields are lower than historical norms due to water scarcity and climate variability. Poland, Belgium, and Sweden represent emerging markets where NFC is gaining share as retail modernization and cold-chain expansion enable wider distribution. South America, led by Brazil, Argentina, and Colombia, serves dual roles as a major NFC exporter (Brazil supplies the majority of U.S. orange juice imports) and a growing domestic market where urbanization and rising incomes drive demand for packaged, refrigerated beverages. The Middle East and Africa remain smaller markets constrained by limited cold-chain infrastructure, price sensitivity, and preference for ambient juice boxes, yet urban centers (Dubai, Riyadh, Johannesburg, Lagos) are seeing premium NFC adoption among affluent consumers.

Competitive Landscape

The NFC juice market operates at moderate consolidation, with multinational beverage conglomerates (Coca-Cola, PepsiCo) controlling refrigerated shelf access and category-captain relationships, yet facing persistent competition from regional cooperatives (Florida's Natural, Eckes-Granini), private-label programs, and cold-press startups emphasizing local sourcing and functional claims. Strategic patterns center on portfolio rationalization, Coca-Cola's discontinuation of Minute Maid frozen concentrates, and a shift toward chilled ready-to-drink formats mirrors broader industry exits from lower-margin, declining SKUs to defend share in premium NFC and functional shots. Technology adoption is bifurcating the competitive landscape: large-scale processors install 600-liter HPP systems to achieve throughput exceeding 4,000 kilograms per hour and lower per-unit costs, while smaller brands rely on tolling centers to access HPP without capital outlays exceeding USD 3 million per machine.

White-space opportunities lie in functional NFC variants targeting specific wellness occasions (post-workout recovery, gut health, immunity support) and in direct-to-consumer subscription models that bypass retail shelf negotiations and capture higher margins. Emerging disruptors include vertically integrated organic cooperatives that control orchard-to-bottle supply chains, reducing exposure to commodity price volatility, and regional cold-press brands leveraging local sourcing narratives to command USD 6 to USD 12 per liter retail prices in urban markets. USDA National Organic Program certification and FSSC 22000 food-safety standards serve as competitive moats, requiring documentation, third-party audits, and operational discipline that favor established players or well-capitalized entrants according to the USDA AMS Organic Standards.

WakeFresh's collaboration with China Agricultural University and Shandong Agricultural University, alongside its 41 patents and involvement in national and industry standards, illustrates how technology-forward processors are building intellectual property and regulatory influence to shape market development. The competitive intensity is highest in North America and Europe, where shelf-space scarcity, promotional calendars, and slotting fees create barriers to entry, and lowest in Asia-Pacific and emerging markets where distribution fragmentation and underdeveloped cold chains offer greenfield opportunities for brands willing to invest in infrastructure and consumer education.

NFC Juice Industry Leaders

Eckes-Granini Group

Florida’s Natural Growers

Grupo Jumex

The Coca-Cola Company

PepsiCo Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Quintus Technologies completed installation of the QIF 600L HPP system at WakeFresh's Anhui facility in China, delivering 600-liter cycle capacity and 4,150 kilograms per hour throughput to support the country's largest HPP-ready-to-drink product manufacturer's expansion into premium fruit and vegetable juices and cold-brew teas.

- March 2026: Suja Organic launched Watermelon Love Cold-Pressed Juice (part of the "Loves" lineup) and Digestion Goldenberry Wellness Shot, both featuring probiotics and available nationwide at Kroger and Albertsons.

- July 2025: Frubaça, a Portuguese fruit and vegetable cooperative, installed a Quintus QIF 400L-5400 HPP system at its COPA Fruit Center in Acipreste (near Alcobaça, central Portugal) to expand production capacity for COPA-branded juices, smoothies, and purées made without preservatives.

- April 2025: Daily Dose Juice UK reported HPP production throughput increases exceeding 100% within the first year of installing Avure HPP equipment (AV-10/AV-20M-40M), enabling output to rise from approximately 100,000 bottles per week to over 400,000 bottles per week. The installation automated in-loading and out-loading, reduced labor costs, decreased cost per liter, and allowed shift expansion from 8-hour to 24-hour continuous production, reducing reliance on third-party processors and lowering carbon footprint through local processing.

Global NFC Juice Market Report Scope

NFC (Not From Concentrate) juice refers to juice that is extracted directly from fruits or vegetables and not concentrated or reconstituted, thereby retaining its natural taste and nutrients. The NFC juice market is segmented by product type, category, packaging type, distribution channel, and geography. By product type, the market includes fruit juice, vegetable juices, and fruit and vegetable blends. By category, the market is divided into conventional and organic products. Based on packaging type, the market is categorized into PET bottles, glass bottles, tetra pack, cans, pouches, and other packaging formats. By distribution channel, the market covers hypermarkets and supermarkets, convenience and grocery stores, online retail, and other retail channels. By geography, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market size and forecasts provided for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD million) and volume (Liters).

| Fruit Juice | Orange |

| Apple | |

| Citrus Blend | |

| Tropical | |

| Others | |

| Vegetable Juices | |

| Fruit and Vegetable Blends |

| Conventional |

| Organic |

| PET Bottles |

| Glass Bottles |

| Tetra Pack |

| Cans |

| Pouches |

| Others |

| Hypermarkets and Supermarkets |

| Convenience and Grocery Stores |

| Online Retail |

| Other Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Fruit Juice | Orange |

| Apple | ||

| Citrus Blend | ||

| Tropical | ||

| Others | ||

| Vegetable Juices | ||

| Fruit and Vegetable Blends | ||

| By Category | Conventional | |

| Organic | ||

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Tetra Pack | ||

| Cans | ||

| Pouches | ||

| Others | ||

| By Distribution Channel | Hypermarkets and Supermarkets | |

| Convenience and Grocery Stores | ||

| Online Retail | ||

| Other Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the NFC juice market and how fast is it growing?

The NFC juice market was valued at USD 22.71 billion in 2026 and is forecast to reach USD 28.49 billion by 2031, representing a 4.63% CAGR during 2026-2031.

Which product type is expanding the quickest within NFC juice?

Vegetable-based NFC juices are projected to grow at a 5.57% CAGR through 2031, outpacing fruit juices as consumers look for lower-sugar, nutrient-dense options.

How significant is organic NFC juice in overall sales?

Organic NFC accounted for 14.42% of 2025 sales and is the fastest-growing category, advancing at a 6.63% CAGR through 2031.

Which sales channel shows the highest growth outlook?

Online retail is the fastest-growing channel, expanding at a 7.79% CAGR thanks to subscription models that bypass limited refrigerated shelf space.

Why does North America remain supply-constrained for NFC orange juice?

Florida’s citrus greening crisis cut domestic output to historic lows, so nearly 90% of U.S. orange juice now comes from Brazil and Mexico, raising exposure to import price swings.

Page last updated on: