Nano-enabled Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

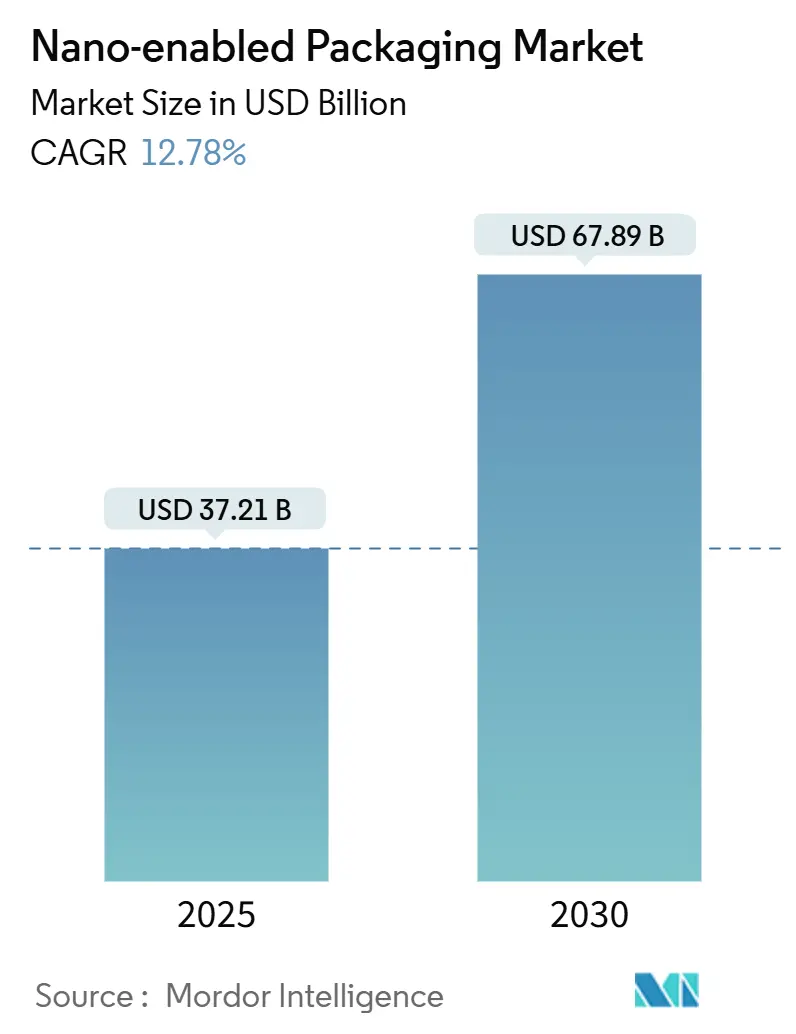

| Market Size (2025) | USD 37.21 Billion |

| Market Size (2030) | USD 67.89 Billion |

| Growth Rate (2025 - 2030) | 12.78% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nano-enabled Packaging Market Analysis by Mordor Intelligence

The nano-enabled packaging market size reached USD 37.21 billion in 2025 and is projected to advance to USD 67.89 billion by 2030, reflecting a compound annual growth rate (CAGR) of 12.78%. Momentum is sustained by rapid growth in fresh-food e-commerce, pharmaceutical cold-chain expansion, and escalating sustainability targets that redefine performance expectations. Widespread cost reductions in nano-clay barrier films have lowered manufacturing expenses by 15-20% since 2024, aligning price-performance metrics with conventional alternatives while delivering oxygen-transmission rates below 0.1 cc/m²/day.[1]U.S. Food and Drug Administration, “Food Contact Substances,” fda.gov Brand owners now view nano-enabled solutions as essential for extending shelf life, protecting temperature-sensitive biologics, and meeting circular-economy mandates. Capital-intensive investments in nano-coating lines, often exceeding USD 75 million, create high entry barriers that favor established players, even as innovation cycles accelerate. Geographically, the Asia-Pacific region maintains leadership in terms of manufacturing scale, while the Middle East posts the strongest growth rate, thanks to investments in food security and healthcare.

Key Report Takeaways

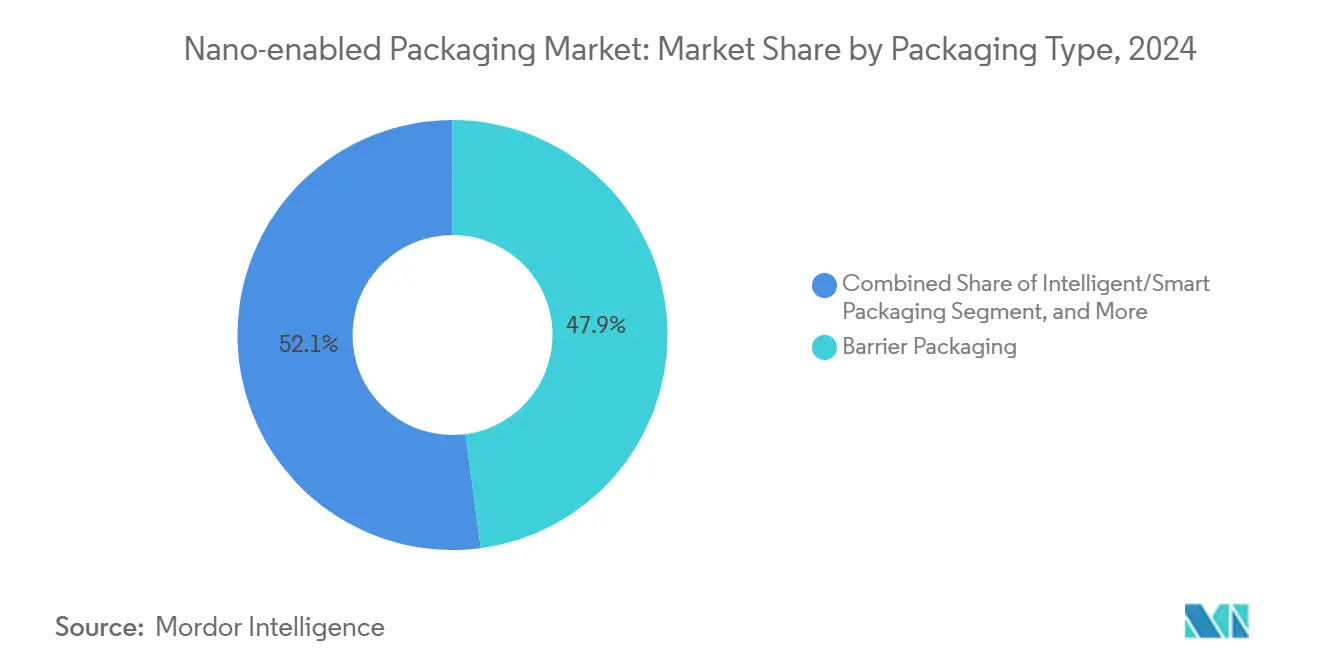

- By packaging type, barrier solutions captured 47.91% of the nano-enabled packaging market share in 2024.

- By material, the nano-enabled packaging market size for paper and board nano-coatings is projected to expand at a 15.89% CAGR between 2025-2030.

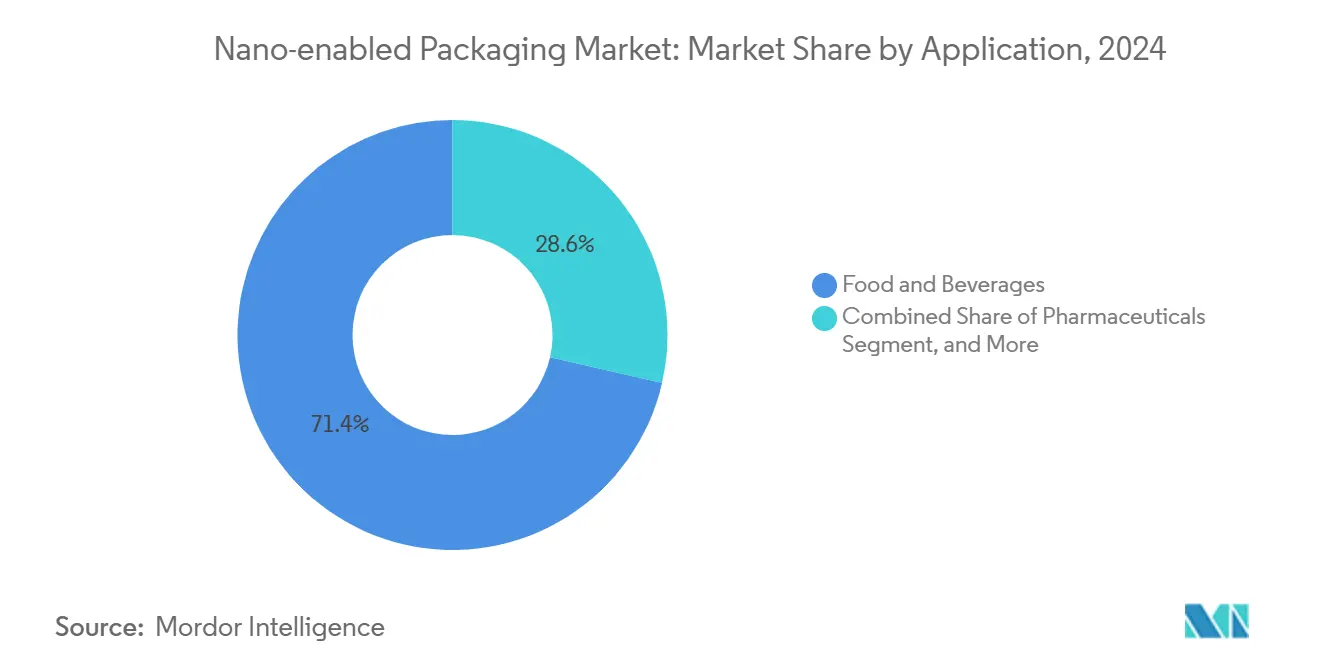

- By application, food and beverages held 71.41% of the nano-enabled packaging market share in 2024.

- By end-user industry, the nano-enabled packaging market size for healthcare logistics is projected to grow at a 13.61% CAGR through 2030.

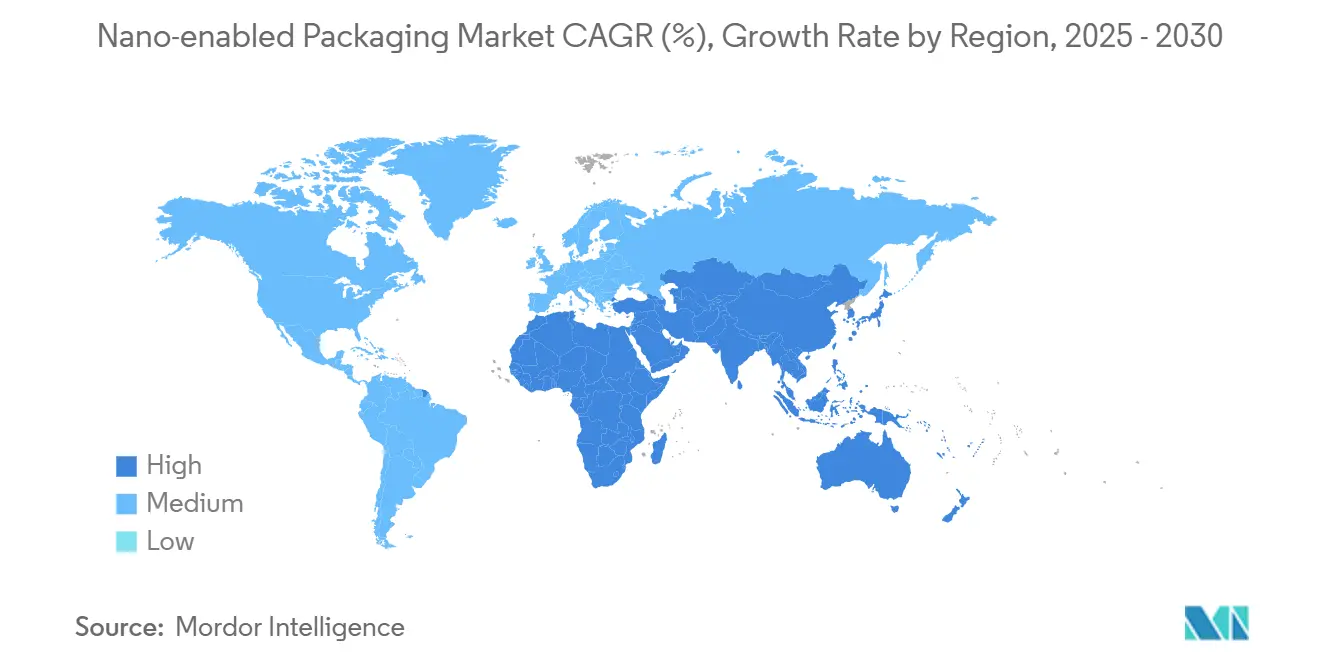

- By geography, Asia-Pacific accounted for 35.61% of the nano-enabled packaging market share in 2024.

Global Nano-enabled Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of fresh food e-commerce | +3.2% | Global urban corridors | Short term (≤ 2 years) |

| Increasing regulatory push for smart traceability | +2.8% | Europe and North America | Medium term (2-4 years) |

| Cost-down advances in nano-clay barrier films | +2.1% | Asia-Pacific and Europe | Short term (≤ 2 years) |

| Pharma cold-chain expansion in emerging markets | +1.9% | Asia-Pacific and Middle East | Medium term (2-4 years) |

| Active antimicrobial nano-silver adoption by meat processors | +1.4% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Brand-owner sustainability targets beyond recyclability | +1.3% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Fresh Food E-Commerce Transforms Packaging Requirements

Escalating online grocery volumes have intensified the need for packaging that can safeguard perishables across longer, multi-node distribution chains. Global e-commerce food sales scaled from USD 150 billion in 2020 to more than USD 400 billion in 2024, prompting retailers and third-party logistics providers to adopt nano-clay barrier films that extend shelf life by up to 50% compared with legacy structures.[2]Bloomberg News, “Fresh Food Delivery Market Growth Drives Packaging Innovations,” bloomberg.com Major platforms continue to invest in temperature-controlled infrastructure, exemplified by Amazon’s USD 1.2 billion allocation in 2024 to upgrade cold-chain nodes, which in turn accelerates demand for high-performance, flexible pouches and lidding materials. Clearer U.S. regulatory guidance on nano-materials in direct food contact, released in 2024, shortened commercialization cycles and reduced approval uncertainty. As urban fulfillment networks mature, brand owners are layering data-logging sensors onto barrier substrates, creating hybrid intelligent packaging that maintains freshness and delivers traceability insights.

Cost-Down Advances in Nano-Clay Barrier Films Enable Mass-Market Adoption

Process innovations, chiefly solvent-free coatings and continuous deposition methods, have reduced production costs for nano-clay films by roughly 18-22% since early 2024. Dow’s USD 200 million capacity expansion in Texas illustrates confidence in sustained volume growth, as improved dispersion allows for lower nanoparticle loadings without compromising performance. Harmonized European REACH requirements have prompted manufacturers to adopt standard formulations, thereby enhancing scale benefits and reducing per-unit costs. These efficiencies position the nano-enabled packaging market as a direct substitute for incumbent EVOH-based multilayers, opening up high-volume snack, produce, and dairy segments that were previously priced out of adoption.

Increasing Regulatory Push for Smart Traceability Fuels Intelligent Packaging Uptake

Serial-level monitoring mandates from European and U.S. agencies now oblige food suppliers to provide end-to-end visibility, spurring investment in NFC, QR, and RFID solutions printed directly on nano-enabled substrates. Walmart’s directive for blockchain-verified leafy-green shipments triggered parallel initiatives across major retailers, making smart labeling a baseline requirement. FDA guidance issued in September 2024 clarified performance criteria for electronic monitoring devices in pharmaceutical packs, further accelerating integration. Component miniaturization and falling sensor costs have brought intelligent formats within reach of mid-tier brands, driving a forecast 14.67% CAGR for the segment.

Pharma Cold-Chain Expansion in Emerging Markets Broadens Scope

Rising biologics pipelines and vaccine distribution programs require materials that maintain integrity at sub-zero temperatures across complex supply chains. Investment programs, such as Pfizer’s USD 2.1 billion outlay in Asia-Pacific and Latin America for 2024, highlight the industry's focus on robust shippers, pouches, and blister formats that combine barrier and temperature-monitoring functions. Emerging economies prioritize local fill-finish capacity, which heightens demand for advanced packs that conform to international good distribution practice standards while withstanding high ambient temperatures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food-contact toxicology concerns on nano-particles | -2.1% | Europe and North America | Medium term (2-4 years) |

| High capital intensity of nano-coating lines | -1.8% | Global manufacturing hubs | Long term (≥ 4 years) |

| Lack of recycling streams for multi-layer nano-films | -1.4% | Europe and North America | Long term (≥ 4 years) |

| Fragmented global regulatory standards | -1.2% | Cross-border trade lanes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Food-Contact Toxicology Concerns Create Regulatory Uncertainty

Stringent European Food Safety Authority protocols, including 90-day migration tests, lengthen approval cycles by up to 18 months, raising development costs and delaying launches.[3]EFSA Journal, “Scientific Opinion on Nanomaterials in Food Contact Materials,” efsa.onlinelibrary.wiley.com Academic studies citing nanoparticle accumulation in liver tissue have triggered precautionary restrictions, compelling firms to undertake multi-jurisdictional toxicological assessments. Divergent interpretations of ISO 10993 standards necessitate manufacturers to create region-specific dossiers, which complicates global rollouts and hinders the near-term acceleration of the nano-enabled packaging market in regulated food segments.

High Capital Intensity Limits Manufacturing Scale-Up

A state-of-the-art nano-coating line demands USD 75-120 million and specialist equipment procured from a concentrated supplier base. Depreciation periods extend beyond seven years, yet rapid technological advances risk early obsolescence, elevating financial exposure for mid-sized converters. Sealed Air’s USD 150 million German plant, scheduled for 2026 completion, underscores the capital commitment needed to reach competitive economies of scale. These barriers curb new-entrant activity and concentrate market power among incumbents with sizable balance sheets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Barrier Dominance Meets Intelligent Surge

Barrier formats accounted for 47.91% of 2024 revenue, underscoring their indispensable role in protecting moisture-sensitive foods and biologics. Within the nano-enabled packaging market size for packaging types, diminished oxygen ingress translates into documented 30-50% shelf-life gains, a metric that resonates with e-commerce grocers and pharmaceutical distributors alike. Continuous cost improvements have entrenched barrier films across mainstream snack and dairy lines, while also opening up lower-margin produce categories.

Intelligent packaging, forecasted to grow at a 14.67% CAGR, draws strength from regulatory traceability obligations and from retailers seeking data analytics on product condition. Sensor platforms printed on barrier layers furnish time-temperature histories that authenticate cold-chain compliance in a single tap, easing audit burdens. Early pilots demonstrate ROI through reduced spoilage claims and increased consumer trust, encouraging a broader rollout across premium and private-label ranges. Active antimicrobial variants, leveraging nano-silver or zinc oxide, continue to gain market share in protein processing plants that face stringent recall risks. Controlled-release concepts remain niche but command premium pricing in high-value pharma and gourmet food lines.

By Material: Paper Innovations Challenge Polymer Supremacy

Polymers accounted for 66.12% of 2024 sales, thanks to their entrenched extrusion assets and versatile property profiles, which are adaptable to nano-coatings. Within the nano-enabled packaging market, polyolefins serve as the workhorse for flexible laminates, while PET structures underpin rigid trays for meat and ready meals. Coating adhesion, thermal stability, and mechanical durability collectively sustain polymer dominance.

Paper and board, however, are racing ahead at a projected 15.89% CAGR as nano-cellulose and hybrid clay systems close the performance gap with plastics. Recent commercial launches have achieved oxygen transmission rates of under 1 cc/m²/day, unlocking categories such as dry mixes and confectionery that were traditionally reserved for metalized films. Cost parity remains a few years distant, but brand sustainability pledges ensure a receptive demand base. Metals and glass persist in specialist roles where an absolute barrier or chemical inertia is mandatory, notably parenteral drugs and aroma-sensitive luxury foods.

By Application: Pharmaceuticals Gain Momentum Beyond Food Pre-eminence

Food and beverages generated 71.41% of 2024 revenue, reflecting the sector’s volume scale and the proven ability of nano-films to mitigate spoilage across global supply chains. Online grocery platforms are increasingly demanding thinner, lighter packs that maintain integrity through multiple touchpoints, driving substitution from conventional multilayer structures to nano-enabled ones.

Pharmaceutical applications are expected to outpace all others at a 15.58% CAGR, driven by biologics and vaccine pipelines that require sub-zero stability and authenticated custody records. Smart blister foils and vial stoppers integrate humidity sensors and RFID chips, ensuring regimen adherence and thwarting counterfeits. Regulatory alignment around digital monitoring, as evidenced by FDA guidance, further cements adoption. Personal care products utilize nano-barriers to prevent fragrance loss and oxidation, whereas industrial components employ the technology to shield sensitive electronics against corrosion during long-distance transit.

By End-User Industry: Logistics Specialists Accelerate Uptake

Meat, poultry, and seafood processors dominated with a 28.38% share in 2024, deploying antimicrobial films that cut pathogen loads and extend sell-by dates. Adoption is motivated by strict retailer scorecards and the financial upside from reduced shrink.

Healthcare logistics providers are expected to experience the fastest growth at a 13.61% CAGR as personalized therapies and extended-range vaccine programs are rolled out. Advanced shippers with embedded temperature probes help third-party providers comply with Good Distribution Practice rules and avoid costly product loss. Dairy brands continue scaling nano-enhanced cartons to minimize light-induced nutrient degradation, while fresh-produce exporters leverage respiration-control sachets embedded with nano-zeolites to maintain firmness throughout transoceanic voyages.

Geography Analysis

Asia-Pacific commanded 35.61% of 2024 global sales, a position secured by China’s vast converter network, Japan’s R and D depth, and India’s packaged-food boom. Governments actively foster nanotechnology development, with China’s 14th Five-Year Plan dedicating USD 15 billion to nanoresearch and India’s Production Linked Incentive program channeling subsidies toward barrier film expansion. South Korea pilots intelligent tags for the pharmaceutical and electronics industries, while ASEAN’s 2024 harmonized food-contact standards create regulatory clarity that attracts foreign investment. The nano-enabled packaging market is expected to continue growing at a double-digit rate as regional e-commerce penetration increases and sustainability regulations become more stringent.

North America leverages robust technology ecosystems and transparent approval processes to contribute significantly to revenue. FDA fast-track pathways have shortened time-to-market for novel materials, giving domestic converters a first-mover edge. Canada’s USD 125 million clean-tech program fuels nano-cellulose research, which in turn informs cross-border packaging supply chains. Mexico benefits from USMCA incentives, with expanded automotive and consumer electronics exports wrapped in nano-barrier pouches that can withstand long-haul distribution and humidity swings.

Europe balances expansion with stringent safety and sustainability mandates. Germany’s chemical industry and France’s gourmet-food producers serve as major demand centers, while Italy’s luxury-goods packaging adopts nano-coatings for anti-counterfeit functionality. The European Union’s Packaging and Packaging Waste Regulation promotes recyclability and drives the development of paper-based nano-barrier innovations. The United Kingdom mirrors EU standards post-Brexit but retains flexibility to approve pilot trials faster, enticing startups. Nordic countries showcase fibre-based packs with compostable nano-layers that align with high consumer environmental expectations.

The Middle East posts a 15.71% forecast CAGR highest worldwide underpinned by government diversification agendas such as UAE’s National Food Security Strategy 2051 and Saudi Arabia’s Vision 2030. Climate-controlled farming and burgeoning pharma manufacturing demand barrier and intelligent packs that survive high ambient temperatures. Logistics hubs in Dubai and Jeddah funnel goods between continents, necessitating resilient, data-enabled packaging solutions across temperature bands.

South America enjoys steady uptake led by Brazil’s agribusiness exporters, which specify antimicrobial liners to meet importer safety protocols. Chilean salmon producers adopt nano-barrier pouches to extend chilled shelf life on transpacific routes. Africa remains nascent, constrained by limited cold-chain infrastructure and divergent regulatory frameworks; however, donor-funded vaccine programs are seeding demand for temperature-monitoring vials in select markets.

Competitive Landscape

Concentration is moderate, with the top five companies capturing roughly 38% of 2024 revenue, reflecting both scale economies and vigorous innovation in the mid-tier. Conglomerates such as Amcor, Sealed Air, and Berry Global pursue bolt-on acquisitions to enhance their nanocapabilities, as seen in Sealed Air’s USD 320 million takeover of NanoGuard Technologies in December 2024. Technology partnerships flourish, with Mondi collaborating with BASF on controlled-release pharmaceutical packs, set for pilot production in 2025. Vertical integration from nanoparticle synthesis to converting differentiates leading players by simplifying compliance and safeguarding intellectual property.

Patent intensity is rising: USPTO filings related to nano-packaging climbed 45% year-on-year in 2024. Many inventions target dual objectives of performance and recyclability, reflecting customer insistence on end-of-life solutions. Companies capable of navigating multi-regional regulatory regimes command pricing power, especially in food-contact and medical applications. High capital requirements and rigorous qualification tests dissuade new entrants, although venture-funded specialists occasionally break through via licensing deals with incumbents seeking fresh ideas.

Looking forward, competitive dynamics will hinge on achieving cost parity for fiber-based nano-barriers, integrating seamless track-and-trace electronics, and establishing scalable recycling streams for multi-layer formats. Firms that harmonize sustainability with profit objectives stand to consolidate market share as legislative timelines tighten and retailers impose stricter packaging scorecards.

Nano-enabled Packaging Industry Leaders

Amcor plc

Sealed Air Corporation

Tetra Pak International SA

Mondi plc

Smurfit Westrock plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Amcor plc committed USD 180 million to build a nano-coating facility in Vietnam targeting pharmaceutical cold-chain packs for Southeast Asia, with 2.5 billion-unit annual capacity expected by 2027.

- December 2024: Sealed Air Corporation acquired NanoGuard Technologies for USD 320 million, adding antimicrobial nano-silver expertise and 47 patents to its portfolio.

- November 2024: Tetra Pak International commercially introduced nano-cellulose barrier coatings in Europe, delivering oxygen transmission rates below 0.8 cc/m²/day while retaining full recyclability.

- October 2024: Mondi plc and BASF partnered on controlled-release pharmaceutical packaging employing nano-encapsulation, with pilot runs slated for Q2 2025.

Global Nano-enabled Packaging Market Report Scope

| Active Packaging |

| Intelligent / Smart Packaging |

| Barrier Packaging |

| Controlled Release Packaging |

| Polymers |

| Metals |

| Glass |

| Paper and Board |

| Food and Beverages |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial |

| Meat, Poultry and Seafood |

| Dairy Products |

| Fresh Produce |

| Confectionery and Snacks |

| Healthcare Logistics Providers |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Type | Active Packaging | ||

| Intelligent / Smart Packaging | |||

| Barrier Packaging | |||

| Controlled Release Packaging | |||

| By Material | Polymers | ||

| Metals | |||

| Glass | |||

| Paper and Board | |||

| By Application | Food and Beverages | ||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Industrial | |||

| By End-user Industry | Meat, Poultry and Seafood | ||

| Dairy Products | |||

| Fresh Produce | |||

| Confectionery and Snacks | |||

| Healthcare Logistics Providers | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the nano-enabled packaging market in 2025?

It reached USD 37.21 billion in 2025 and is expected to grow rapidly through 2030.

What is driving the fastest growth within nano-enabled packaging?

Intelligent formats that embed traceability sensors are projected to register a 14.67% CAGR between 2025 and 2030.

Which material is gaining ground on polymers?

Paper and board coated with nano-cellulose barriers are forecast to expand at a 15.89% CAGR, challenging polymer dominance.

Why is the Middle East an attractive region for suppliers?

Government food-security and healthcare investments support a forecast 15.71% CAGR, the highest regional rate through 2030.

What limits new entrants in nano-enabled packaging?

Capital requirements of USD 75-120 million for state-of-the-art nano-coating lines create high barriers to entry.

How concentrated is the competitive landscape?

The top five firms hold roughly 38% share, reflecting moderate concentration that still allows room for niche innovators.

Page last updated on: