Netherlands IT Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

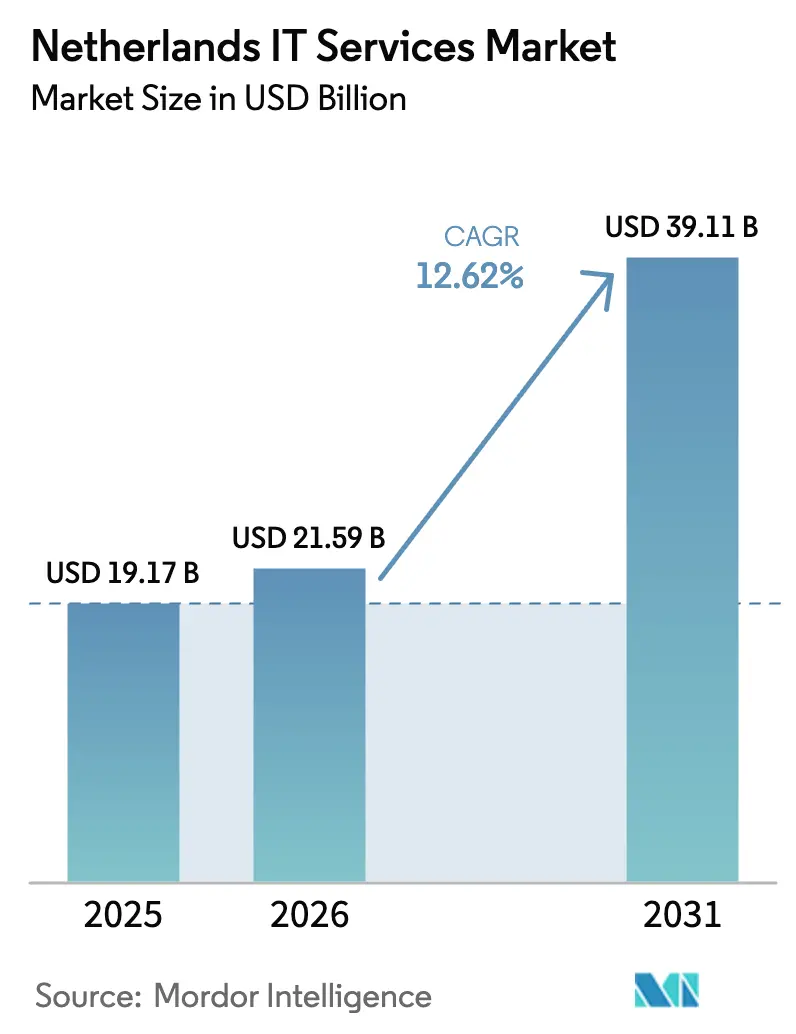

| Base Year Market Size (2025) | USD 19.17 Billion |

| Market Size (2026) | USD 21.59 Billion |

| Market Size (2031) | USD 39.11 Billion |

| Growth Rate (2026 - 2031) | 12.62% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands IT Services Market Analysis by Mordor Intelligence

The Netherlands IT Services market size is expected to grow from USD 19.17 billion in 2025 to USD 21.59 billion in 2026 and is forecast to reach USD 39.11 billion by 2031 at 12.62% CAGR over 2026-2031.[1]Nederlandse overheid, “Nederlandse Digitaliseringsstrategie 2025,” rijksoverheid.nl Sustained public-sector digitalization, expanding cloud adoption and persistent talent shortages together keep the Netherlands IT Services market on a steep growth path. Enterprises accelerating hybrid cloud programs, the broad rollout of NIS2 and DORA, and a maturing near-shoring ecosystem all reinforce demand. Competitive advantage increasingly stems from regulatory expertise and the ability to blend local governance with remote execution. At the same time, grid congestion in Noord-Holland and mounting onshore wage pressures are redefining location and pricing strategies across the Netherlands IT Services market.

Key Report Takeaways

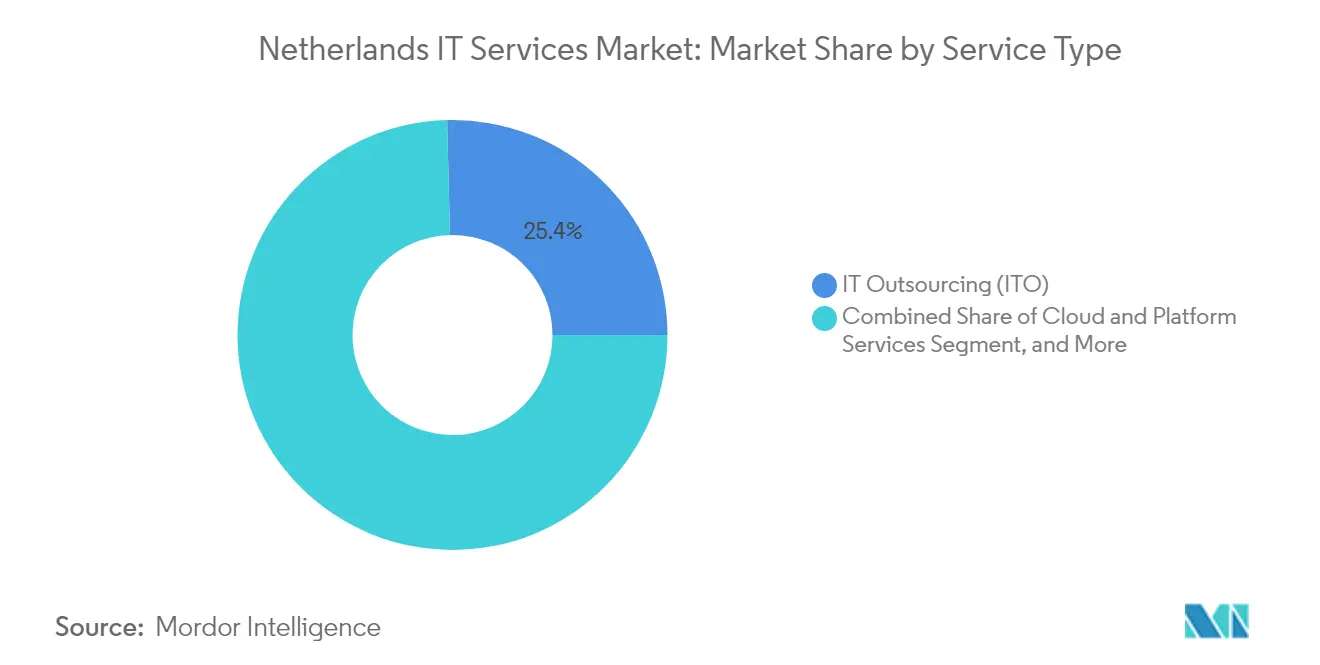

- By service type, IT outsourcing led with 25.40% of the Netherlands IT Services market share in 2025; managed security services are advancing at a 16.63% CAGR through 2031.

- By enterprise size, large enterprises held 68.08% of the Netherlands IT Services market share in 2025, while SMEs are growing fastest at 15.52% CAGR.

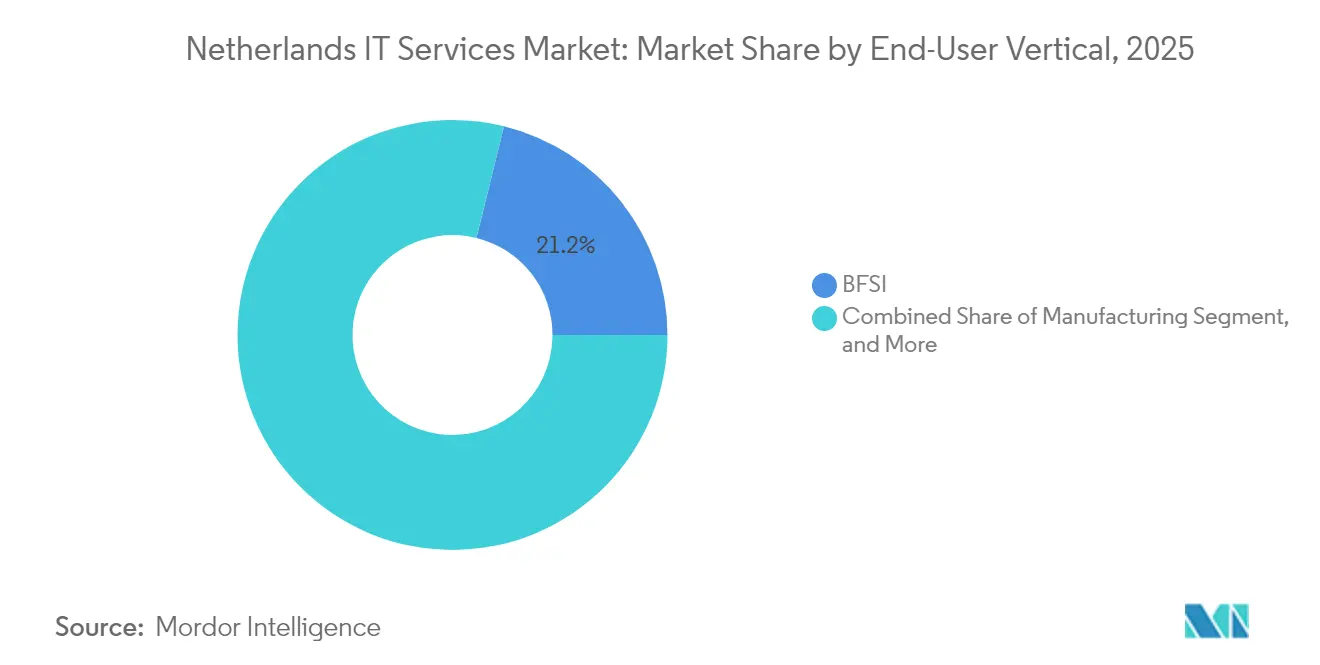

- By end-user vertical, BFSI captured 21.15% of the Netherlands IT Services market in 2025; healthcare and life-sciences are set to post a 14.8% CAGR to 2031.

- By service delivery model, on-site services accounted for 46.20% of the Netherlands IT Services market size in 2025 and remote/offshore services are climbing at a 16.05% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent government digital-first agenda and cloud-first mandates | +2.80% | National, with concentration in Randstad region | Medium term (2-4 years) |

| Acute domestic tech-talent shortage accelerating outsourcing | +3.10% | National, with highest impact in Amsterdam, Rotterdam, The Hague | Short term (≤ 2 years) |

| Rising cybersecurity and compliance obligations (NIS2, DORA) | +2.40% | EU-wide with Netherlands early adoption focus | Short term (≤ 2 years) |

| Dutch sovereign "Rijkscloud" initiative unlocking local spend | +1.90% | National government and critical infrastructure sectors | Long term (≥ 4 years) |

| AI-driven productivity projects in ports and logistics ecosystems | +1.60% | Concentrated in Rotterdam, Amsterdam ports | Medium term (2-4 years) |

| Manufacturing Industry 4.0 and smart factory automation initiatives | +1.40% | Industrial regions including Noord-Brabant, Gelderland, Limburg | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Government Digital-First Agenda and Cloud-First Mandates

NDS 2025 sets explicit cloud-first rules for non-sensitive workloads, commits EUR 8.7 million to modernize 58,000 government workplaces and earmarks multi-billion funding for a sovereign government cloud. Such top-down guidance generates steady consulting, migration and managed-service contracts across ministries and municipalities. Accelerated procurement cycles in 2025 already reflect the urgency to replace legacy platforms. Vendors that align with open-architecture principles and local data-sovereignty requirements win preferred-supplier status in the Netherlands IT Services market.

Acute Domestic Tech-Talent Shortage Accelerating Outsourcing

IT vacancies fell to 31,435 in 2024, yet 21% of Dutch firms still cannot fill key roles and software-developer salaries rose 11%.[2]Emerce B.V., “IT-arbeidsmarktmonitor 2024,” emerce.nl With cybersecurity roles showing a projected shortfall of 20,000 by 2025, Dutch buyers fast-track near-shore and offshore contracts. Competitive differentiation now centers on access to blended, multilingual delivery teams that comply with Dutch labour and privacy standards while containing cost. These dynamics underpin the double-digit expansion of the Netherlands IT Services market.

Rising Cybersecurity and Compliance Obligations (NIS2, DORA)

The January 2025 DORA enforcement date pushes every financial entity to prove operational resilience, while NIS2 extends critical-infrastructure security to healthcare, manufacturing and logistics. The Dutch National Cyber Security Centre logged a 55% year-on-year jump in attacks in 2024. Consequently, managed detection and response, continuous compliance monitoring and incident-response retain premium pricing and broaden the Netherlands IT Services market customer base beyond BFSI.

Dutch Sovereign “Rijkscloud” Initiative Unlocking Local Spend

The Rijkscloud program, announced April 2025, mandates that sensitive state workloads migrate to a Dutch-controlled cloud stack, backed by EUR 70 million in IPCEI-CIS contributions.[3]Security Delta, “Trend snippet: Technology and cybersecurity,” securitydelta.nl Agencies hurriedly assess existing SaaS deployments, opening incremental demand for migration roadmaps, multi-cloud brokerage and zero-trust re-architecture. Local integrators that certify on GAIA-X interoperability standards solidify a strategic foothold in the Netherlands IT Services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High local labour cost inflation for on-shore delivery | -1.80% | National, with highest impact in Randstad metropolitan area | Short term (≤ 2 years) |

| Vendor lock-in and high egress fees in public cloud contracts | -1.30% | Global cloud providers with Netherlands operations | Medium term (2-4 years) |

| Electricity-grid congestion delaying new data-centre builds | -0.90% | Noord-Holland, with spillover effects nationally | Long term (≥ 4 years) |

| Regulatory complexity and increasing compliance costs across multiple frameworks | -1.10% | EU-wide with concentrated impact on financial services and critical infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Local Labour Cost Inflation for On-Shore Delivery

Average Dutch wages climbed 5.2% in 2024, with IT roles seeing even steeper hikes. Consulting majors instituted partner-salary cuts and staff-reduction programs to protect margins. Mid-tier providers accelerate Suriname, Portugal and Eastern-Europe expansions to sustain blended delivery ratios that keep the Netherlands IT Services market competitive without eroding quality benchmarks.

Vendor Lock-In and High Egress Fees in Public-Cloud Contracts

Hyperscalers historically levied 10-15% of total cloud spend as egress fees. Even after partial waivers, Dutch CIOs weigh repatriation or hybrid alternatives that allow workload portability. Local providers such as GLBNXT pitch fee-free exit strategies and European-law aligned SLAs, redirecting spend toward private-cloud and colocation nodes inside the Netherlands IT Services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Security Services Drive Premium Growth

The Netherlands IT Services market size for managed security services is projected to rise from USD 3.05 billion in 2025 to USD 7.67 billion by 2031, translating into a 16.63% CAGR and reflecting the acute compliance agenda. IT outsourcing still anchors 25.40% of total 2025 revenue, yet its growth curve has flattened as routine infrastructure management commoditizes. Demand pivoted toward consulting on zero-trust frameworks, sovereign-cloud migrations and AI enablement, positioning advisory engagements as the entry point for longer-term managed contracts. Illustrative contracts include IBM’s April 2025 purchase of IntelliMagic that adds mainframe-performance tooling into its Dutch stack, illustrating how platform depth reinforces client stickiness inside the Netherlands IT Services market. Cloud and platform services benefit from Benelux-wide hyperscale investment plans even as power-grid limits force workload dispersal.

With security staffing gaps widening, buyers award multi-year managed-detection deals at above-inflation rates. The Netherlands IT Services market share of managed security services is therefore set to climb steadily, strengthening the pricing power of niche providers that combine SOC operations in Portugal with Dutch-based client management. Standardized playbooks and EU-accredited certification provide competitive insulation against commoditization trends affecting legacy ITO.

By Enterprise Size: SME Adoption Accelerates

Large enterprises account for USD 13.05 billion of the Netherlands IT Services market size in 2025, but the SME contribution is expanding fastest. SaaS subscriptions, pay-as-you-go cybersecurity and packaged cloud migrations reduce up-front capital requirements, enabling SMEs to leapfrog traditional data-center buildouts. Eye Security’s EUR 36 million funding directed at SME cyber-insurance showcases investor conviction in mid-market potential. The Netherlands IT Services market sees an influx of born-in-cloud MSPs that offer standardized bundles combining endpoint protection, compliance dashboards and helpdesk in Dutch language. As regulatory scope widens, SMEs opt for external audits and remediation roadmaps rather than hiring scarce talent, reinforcing double-digit growth momentum through 2031.

Simultaneously, large enterprises rationalize multi-provider estates, consolidating strategic suppliers able to guarantee EU-law alignment and carbon-reporting transparency. While consolidation can lower vendor count, contract values per supplier rise, ensuring sustained revenue expansion for incumbents that satisfy stringent ESG and data-sovereignty metrics within the Netherlands IT Services market.

By End-User Vertical: Healthcare Digitalization Leads Growth

The Netherlands IT Services market size for healthcare and life-sciences stood at USD 3.15 billion in 2025 and is projected to post a 14.8% CAGR. Electronic-health-record interoperability initiatives, the National Terminology Server rollout and tele-monitoring pilots all fuel sizeable systems-integration pipelines. Dedalus’ work on national terminology services underlines the depth of specialized mapping and testing assignments now entering execution phases. BFSI remains the single biggest spender, yet budget allocation increasingly skews toward resilience testing, fraud analytics and model-risk governance to satisfy DORA. Manufacturing continues steady digitization, focusing on predictive maintenance and digital-twin rollouts that knit OT and IT domains. Each vertical displays distinct compliance and integration challenges, but all converge on the need for secure, scalable cloud foundations, locking in sustained expansion across the Netherlands IT Services market.

By Service Delivery Model: Hybrid Models Gain Traction

On-site engagements still capture 46.20% of 2025 spend as ministries and heavily regulated industries favour local presence for risk workshops and stakeholder alignment. However, remote/offshore contracts are growing at 16.05% CAGR, pushed by wage inflation and severe staff scarcity. Dutch mid-sized providers pivot to Portugal, Poland and the Baltic states, leveraging near-time-zone alignment and EU data protection parity. Hybrid managed services, blending Dutch project managers with remote delivery squads, emerge as the reference architecture. This structure optimizes cost without breaching data-residency limits, advancing the Netherlands IT Services market toward a globally distributed yet locally governed delivery paradigm.

Geography Analysis

Amsterdam anchors regional demand as EMEA headquarters for digital-platform giants and houses AMS-IX, one of the world’s busiest internet exchanges. The Randstad concentrates finance, telecom and public administration workloads, making it the epicenter of contract signings and vendor account teams. Utrecht now posts the nation’s highest median IT salary at EUR 3,556 per month, a signal of tight labour supply. Rotterdam accelerates AI pilots in maritime logistics, from berth-planning algorithms to drone-based inspections, broadening use-case diversity within the Netherlands IT Services market.

Grid congestion in Noord-Holland pushes fresh data-center intake toward Zeeland and Groningen in the north-east, aided by planned hydrogen hubs that promise green-energy capacity. Rotterdam and The Hague position themselves as alternative colocation corridors, with operators marketing proximity to subsea-cable landings and government campuses. Rural provinces vie for edge deployments that support precision-agriculture platforms, thereby distributing infrastructure beyond the Randstad.

The Dutch regulatory environment continues to benchmark EU policy rollouts. Early NIS2 legislation prompts healthcare systems in Groningen and Friesland to harden OT networks, drawing specialist providers into secondary regions. Likewise, municipalities in Limburg adopt sovereign-cloud pilots aligned with the Rijkscloud blueprint, ensuring nationwide diffusion of workload modernization and sustaining a balanced regional contribution to the Netherlands IT Services market.

Competitive Landscape

Market fragmentation is moderate, with global consultancies, offshore-heritage integrators and specialist Dutch firms all wrestling for share. IBM’s purchase of IntelliMagic injects mainframe-performance IP, sharpening its differentiation. Imker Capital’s stake in Centric signals private-equity appetite for consolidation plays. Accenture leverages its global USD 52.1 billion turnover to bundle Gen-AI pilots with core-systems modernization yet must navigate talent scarcity and cost inflation similar to smaller rivals.

Technology leadership revolves around AI accelerators, low-code platforms and zero-trust frameworks. Deloitte formed a unified digital division and deepened alliances with hyperscalers to extend AI-as-a-service blueprints. Local niche players, such as Schuberg Philis, use ISO 27701 privacy certifications and Dutch-language 24 × 7 operations to lock in regulated-sector accounts. European-sovereignty propositions gain traction, with GLBNXT positioning a fully EU-controlled cloud stack to mitigate vendor-lock-in fears. The ability to blend sovereign-cloud advisory with cost-efficient remote delivery has become the discriminator that shapes win-rates inside the Netherlands IT Services market.

Given that the top five vendors together hold around 32% of total revenue, the competitive arena stays open for mid-tier specialists and emerging AI boutiques. Cross-border M&A is likely to continue, especially across cybersecurity and data-platform niches, as providers aim to deepen vertical expertise while broadening geographic reach.[4]Loyens & Loeff N.V., “Shareholders sell IntelliMagic B.V. to IBM,” loyensloeff.com

Netherlands IT Services Industry Leaders

Accenture plc

Capgemini SE

International Business Machines Corporation

Atos SE

CGI Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Kinly merged with Yorktel to expand unified-communications integration capabilities.

- July 2025: Government issued the Nederlandse Digitaliseringsstrategie outlining cloud-first architecture principles.

- April 2025: IBM closed its acquisition of IntelliMagic B.V. to enhance mainframe analytics.

- April 2025: IBM acquired Hakkoda Inc. to bolster data-and-AI consulting reach.

Netherlands IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| On-site Services |

| Remote / Offshore Services |

| Hybrid Managed Services |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals | |

| By Service Delivery Model | On-site Services |

| Remote / Offshore Services | |

| Hybrid Managed Services |

Key Questions Answered in the Report

What revenue does the Netherlands IT Services market generate in 2026?

The market reaches USD 21.59 billion in 2026 and is on track for USD 39.11 billion by 2031.

Which segment shows the fastest growth across Dutch IT services?

Managed security services expands at a 16.63% CAGR, driven by NIS2 and DORA compliance needs.

How are SMEs influencing Dutch IT services demand?

SMEs post a 15.52% CAGR as cloud subscriptions and packaged security services remove entry barriers.

What geographic factor most constrains Dutch data-center expansion?

Power-grid congestion in Noord-Holland restricts new connections until at least 2036.

Why is the healthcare sector important for service providers?

Healthcare and life-sciences grow at 14.8% CAGR thanks to interoperability mandates and e-health adoption.

How are wage pressures reshaping delivery models?

Rising local salaries accelerate hybrid and near-shore delivery, allowing providers to blend Dutch governance with cost-efficient remote execution.

Page last updated on: