Indonesia IT Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

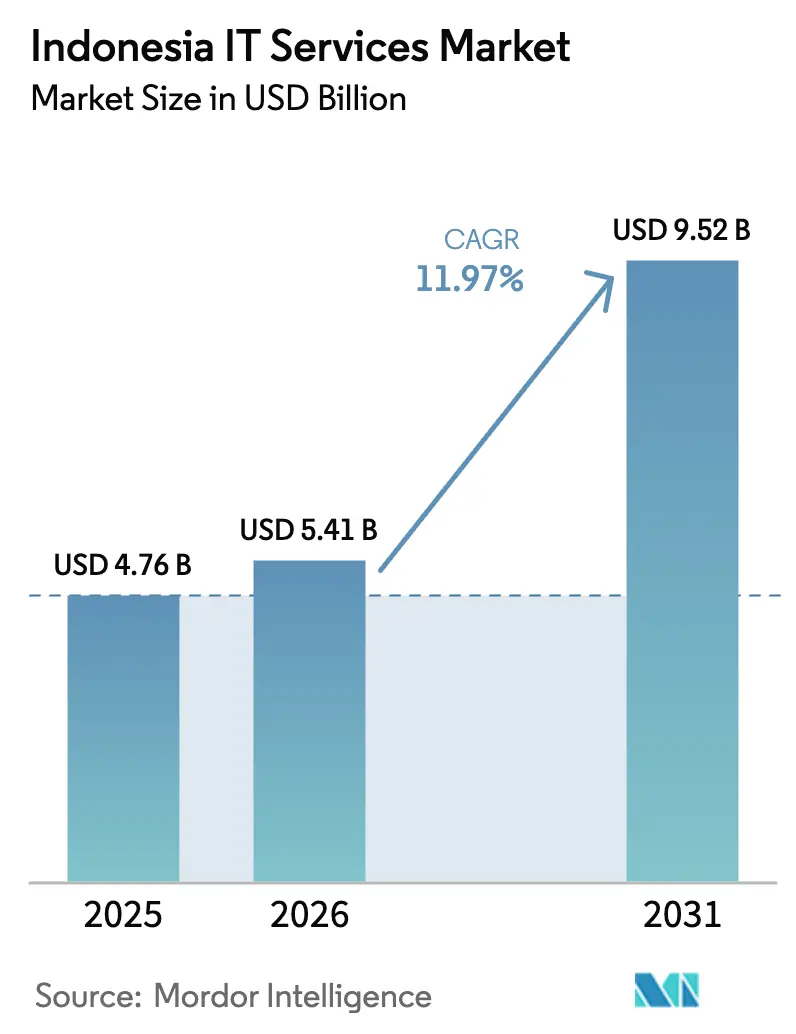

| Base Year Market Size (2025) | USD 4.76 Billion |

| Market Size (2026) | USD 5.41 Billion |

| Market Size (2031) | USD 9.52 Billion |

| Growth Rate (2026 - 2031) | 11.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia IT Services Market Analysis by Mordor Intelligence

The Indonesia IT services market size is expected to increase from USD 4.76 billion in 2025 to USD 5.41 billion in 2026 and reach USD 9.52 billion by 2031, growing at a CAGR of 11.97% over 2026-2031. Rapid cloud adoption, rising demand for production-grade artificial intelligence, and state-sponsored build-operate-transfer data-center agreements are reshaping revenue streams and compressing legacy maintenance spending. Financial-sector mandates on domestic data residency, combined with the Ministry of Communication and Informatics’ sovereign AI roadmap, push enterprises toward hybrid environments that blend local compliance with global scalability. Hyperscale investments by Microsoft, Google Cloud, and Telkom Group are improving regional latency, supporting nationwide e-commerce expansion and real-time digital payments. Meanwhile, persistent shortages in DevSecOps and cloud-security talent elevate consulting rates and encourage long-term managed-services contracts that stabilize integrator cash flows.

Key Report Takeaways

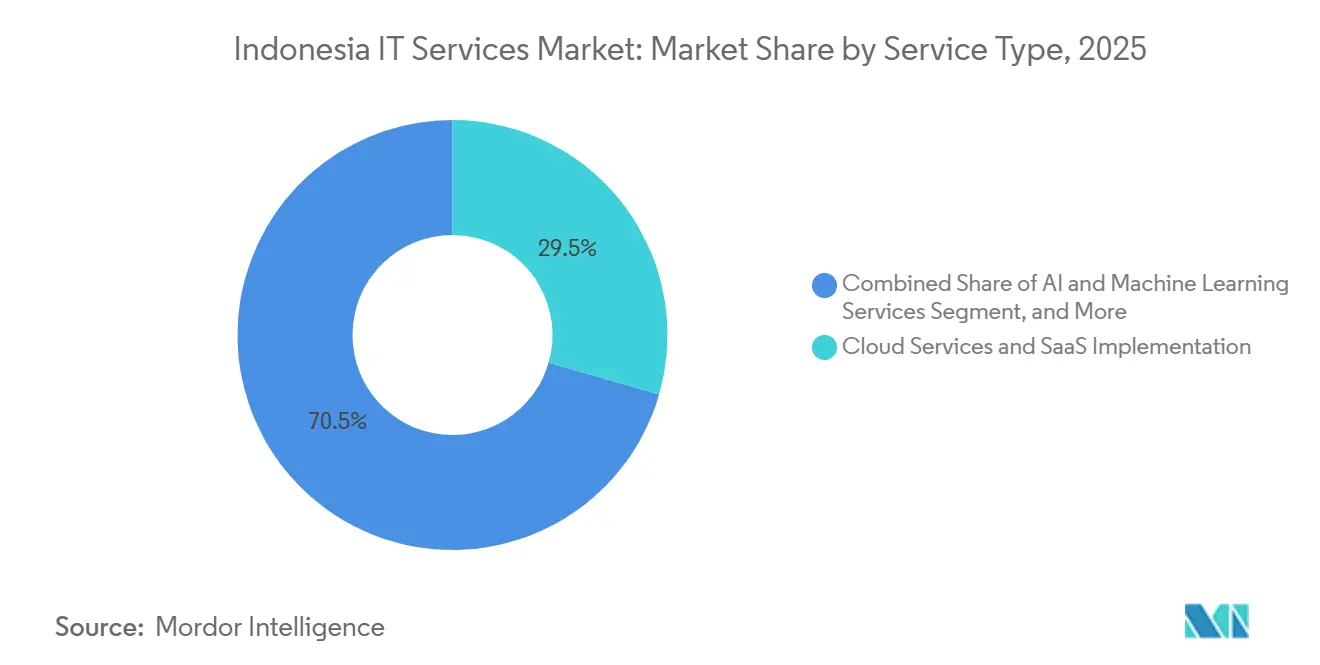

- By service type, Cloud Services and SaaS Implementation led with 29.47% revenue share in 2025, while Artificial Intelligence and Machine Learning services are projected to register the fastest expansion at a 12.55% CAGR through 2031.

- By enterprise size, large enterprises accounted for 61.29% of 2025 spending, whereas small and medium enterprises represent the fastest-growing customer group at a 12.97% CAGR to 2031.

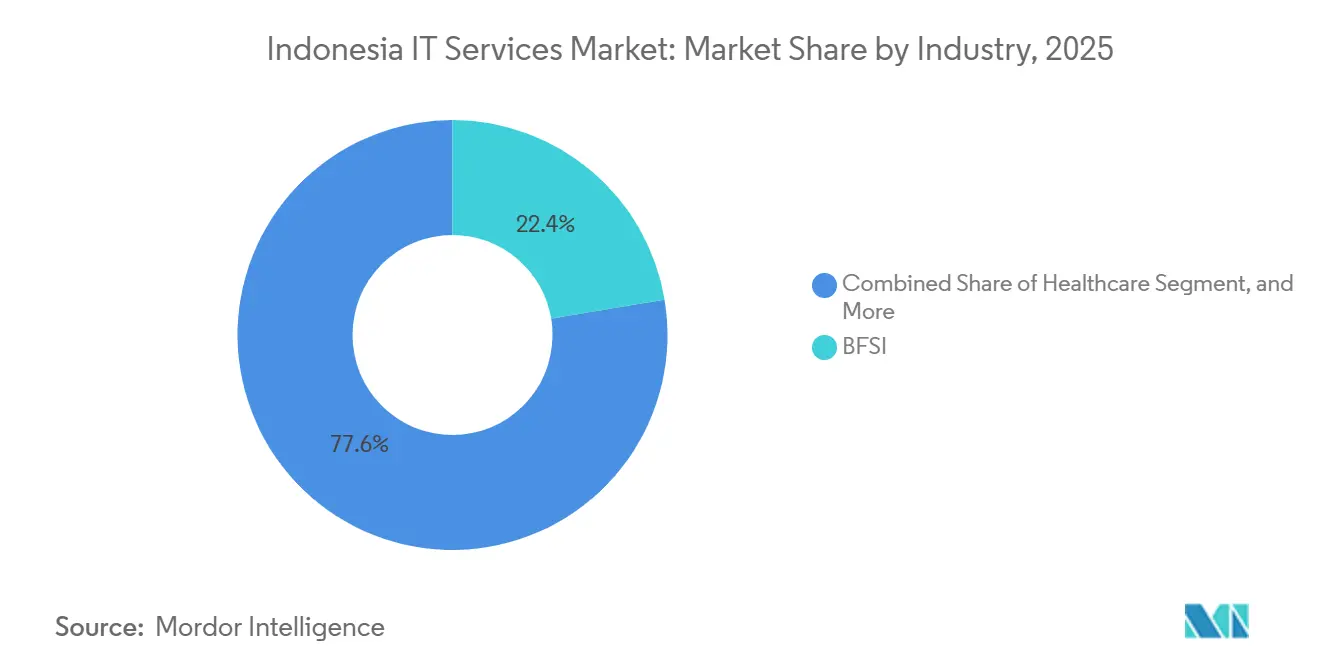

- By industry, Banking, Financial Services, and Insurance captured 22.37% of 2025 value, while healthcare shows the strongest forecast momentum with a 12.75% CAGR during 2026-2031.

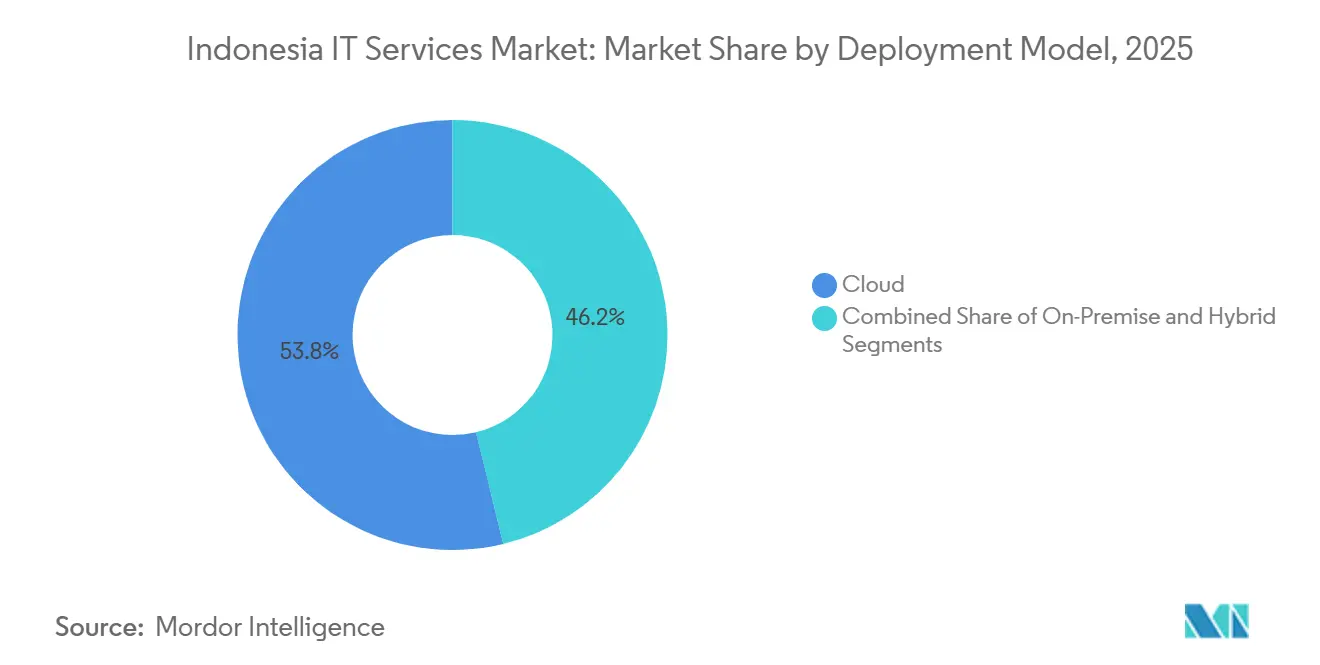

- By deployment model, cloud environments contributed 53.79% of 2025 revenue, yet hybrid architectures are expected to expand the quickest at a 12.83% CAGR through 2031.

- By technology, cloud computing generated 27.81% of 2025 revenue, but Artificial Intelligence and Machine Learning technologies are forecast to grow the fastest at a 13.04% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Enterprise Digital-First Strategies | +3.20% | National, concentrated in Jakarta, Surabaya, Bandung | Medium term (2-4 years) |

| Surge in Cloud-Native Application Migration | +2.80% | National, with Jakarta and Batam as primary cloud regions | Medium term (2-4 years) |

| Government "Making Indonesia 4.0" Incentives | +2.10% | National, with priority zones in Java and Batam | Long term (≥ 4 years) |

| Accelerated Fintech and E-Commerce Expansion | +1.90% | National, urban centers leading adoption | Short term (≤ 2 years) |

| Data-Center Build-Operate-Transfer Deals with SOEs | +1.40% | Jakarta, West Java, Batam | Medium term (2-4 years) |

| Mandated Domestic Disaster-Recovery Hosting for Critical Data | +0.90% | National, compliance-driven across all sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Enterprise Digital-First Strategies

Indonesian corporations now replace incremental upgrades with holistic overhauls that bundle cloud ERP, customer data platforms, and AI-driven analytics into unified architectures. A 2025 IBM survey found 62% of domestic firms piloting AI, well above regional peers.[1]IBM Corporation, “Indonesia AI Adoption Study 2025,” ibm.com Digital-native leaders such as GoTo Financial completed full cloud migrations in mid-2025, showing incumbents the performance gap that arises without end-to-end modernization. Multi-year managed-services contracts accompany these programs, securing predictable revenue and mitigating hardware refresh volatility. Certified integrators with ISO 27001 and SOC 2 documentation enjoy a bidding advantage because banks and telecom operators must pass strict regulatory audits.[2]Bank Indonesia, “Bank Indonesia Regulation No.2/2024,” bi.go.id Consequently, service providers emphasize consult-build-operate models that embed long-term account control.

Surge in Cloud-Native Application Migration

Google Cloud’s Jakarta region expansion in May 2025 catalysed a wave of microservices refactoring projects requiring Kubernetes and serverless skills.[3]Google Cloud, “Jakarta Region Expansion Announcement,” cloud.google.com Microsoft’s USD 1.7 billion commitment, including training for 840,000 Indonesians, signals confidence that platform-as-a-service demand will outpace lift-and-shift workloads.[4]Microsoft Corporation, “USD 1.7 Billion Indonesia Investment Announcement,” microsoft.com Enterprises adopting cloud-native patterns report 20% faster release cycles and 50% lower unplanned downtime, metrics that justify premium DevOps consulting fees. Bank Indonesia Regulation No.2/2024 compels banks to re-platform core systems on cloud infrastructure with domestic data residency, tripling average project value. Required certifications under ISO 27001 increase entry barriers, concentrating high-margin work among established integrators.

Government Making Indonesia 4.0 Incentives

Fiscal incentives tied to Manufacturing 4.0 compel factories in automotive, electronics, and textiles to digitalize production lines with IoT, AI, and digital twins. The National AI Roadmap targets 100,000 specialists annually by 2029, creating a domestic talent pipeline that lowers long-run delivery costs. Danantara, the sovereign wealth fund, earmarks capital for AI infrastructure, anchoring future hyperscale requirements. Streamlined licensing via the Online Single Submission system shortens market entry, although local procurement rules still vary by province. Presidential Regulation No.82/2022 further narrows supplier pools by requiring vital-information infrastructures to source only from providers meeting stringent resilience standards.

Accelerated Fintech and E-Commerce Expansion

Indonesia’s e-commerce gross merchandise value hit USD 71 billion in 2025 and is on track for USD 95 billion in 2026, overloading legacy IT and pushing retailers to cloud-based order management platforms. Digital payment volume climbed to USD 538 billion in 2025, creating heavy demand for fraud analytics and real-time settlement engines. Fintech lenders regulated under OJK rules deploy machine-learning credit models, opening advisory niches around model governance. Social-commerce convergence, exemplified by TikTok Shop integrations, drives omnichannel platform spending that synchronizes inventory across physical and digital storefronts in real time. Global integrators have responded by forming Jakarta-based fintech practices aimed at rapid MVP rollouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Domestic Skills Gap in Advanced Cloud and DevSecOps | -1.80% | National, acute in tier-2 and tier-3 cities | Medium term (2-4 years) |

| Ageing Legacy Infrastructure Outside Tier-1 Cities | -1.30% | Provincial regions, outer islands | Long term (≥ 4 years) |

| Fragmented Provincial Procurement Standards | -0.70% | Provincial and municipal levels | Medium term (2-4 years) |

| Rising Electricity Tariffs Impacting Hyperscale Economics | -0.50% | Jakarta, West Java, Batam | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Domestic Skills Gap in Advanced Cloud and DevSecOps

Nearly half of large enterprises report shortages in cloud-security expertise despite surging AI adoption. Universities produce fewer than 5,000 cybersecurity graduates a year, while the National Cyber and Crypto Agency tracked 403 million anomalous traffic events in 2023. Until the AI roadmap delivers sizable cohorts, integrators import expatriate talent at two to three times local salaries, squeezing margins. Skill scarcity lengthens project timelines, particularly for SME clients that cannot absorb premium rates. Providers hedge by opening remote security-operations centers in lower-cost Asian locations, a move that introduces latency and data-sovereignty concerns.

Ageing Legacy Infrastructure Outside Tier-1 Cities

Jakarta and West Java house about 80% of national data-center capacity, leaving outer islands dependent on pre-2020 gear lacking the density needed for AI model training. Satellite links produce latencies above 100 milliseconds, hampering ERP rollouts and telemedicine. Fragmented procurement across 34 provinces forces integrators to duplicate compliance paperwork and delays kick-offs by up to six months. Rising industrial power tariffs further erode hyperscale economics in provincial sites. Execution risks are evident in the National Data Center at Cikarang, which missed its June 2025 onboarding target for ministerial systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud and AI Elevate Revenue Mix

Cloud Services and SaaS Implementation held 29.47% of 2025 revenue in the Indonesia IT services market, showing enterprises’ strong preference for utility pricing over capex-heavy on-premises deployments. Artificial Intelligence and Machine Learning engagements grow at 12.55% annually, thanks to banks, retailers, and manufacturers moving pilot models into production. IT Consulting and Implementation remains foundational, guiding clients through microservices re-architecture and business-process redesign. Business Process Outsourcing is shifting toward AI-assisted credit underwriting and claims processing, lifting provider margins. IT Outsourcing and Managed Services anchor recurring income, although price competition from offshore vendors pressures local firms to differentiate via 24/7 Indonesian-language support and on-site response.

Other Service Types, dominated by legacy hardware break-fix, continue to contract yet still underpin mission-critical systems that cannot migrate in a single release. Telkomsigma’s pivot from classic integration to cloud-native consulting, and its AWS and Google Cloud partner badges, illustrates how incumbents can refresh portfolios while protecting embedded bases. Bank Indonesia’s residency mandate accelerates movement from perpetual licenses to SaaS, positioning integrators that manage hybrid entitlements for long-term relevance. As AI accelerates, cloud and data-platform expertise becomes the primary gatekeeper to high-value transformation deals.

By Enterprise Size: Mid-Market Volume, Large-Cap Value

Large enterprises contributed 61.29% of 2025 revenue in the Indonesia IT services market, reflecting regulatory burdens, larger IT estates, and capacity to fund multi-million-dollar projects. Banks, telecom operators, and diversified conglomerates sign multi-tower deals that bundle consulting, migration, and managed services for 3-to-7-year terms. They increasingly rationalize supplier rosters, awarding core transformation work to firms offering certified security frameworks and audited delivery processes.

SMEs expand at a 12.97% CAGR as government digital-voucher schemes offset advisory fees and cloud providers launch SME pricing tiers. Typical engagements focus on point solutions such as inventory SaaS or IoT-enabled machinery telemetry, favouring modular delivery and rapid payback. Microsoft’s nationwide skills academies nurture a future pool of cloud-ready SME owners, while hybrid models bridge connectivity gaps in provincial areas. The widening SME opportunity prompts local boutiques to package templated offerings with fixed-fee implementation, enhancing affordability without deep customization.

By Industry: BFSI Dominates, Healthcare Accelerates

Banking, Financial Services, and Insurance commanded 22.37% of 2025 spending in the Indonesia IT services market, fuelled by mandates for cloud adoption, real-time payments, and fraud analytics. Core-system re-platforming, regulatory audits, and continuous security testing produce steady demand for consulting and managed services. Digital-payment volume of USD 538 billion in 2025 sustains spend on settlement engines and anti-money-laundering analytics.

Healthcare grows at 12.75% CAGR as the Ministry of Health connects 10,000 facilities to the SATUSEHAT data exchange. Hospitals procure electronic records, telemedicine, and interoperability middleware, creating greenfield revenue for specialized integrators. Manufacturing pursues Industry 4.0 programs focusing on predictive maintenance and digital twins, though adoption concentrates in automotive and electronics clusters. Government spending proceeds under the SPBE digital-government framework, but provincial fragmentation tempers scale. Retail and e-commerce race to deploy omnichannel platforms that bind social-commerce, store, and warehouse systems.

By Deployment Model: Hybrid Bridges Compliance and Scale

Cloud deployments represented 53.79% of 2025 revenue, confirming the Indonesia IT services market’s shift toward consumption economics. Yet hybrid architectures grow at 12.83% CAGR because the Personal Data Protection Law allows sensitive workloads to remain on premises while analytics leverages public clouds. Banks keep core-banking hosts on private clusters while streaming customer insights into public-cloud AI engines.

Hybrid complexity rewards integrators versed in workload placement, encryption, and policy management across heterogeneous environments. Google Cloud’s extra Jakarta zones enable enterprises to architect regional disaster-recovery pairs without leaving national borders. On-premises estates persist in defense and critical infrastructure where air-gapped mandates apply, but many now add private-cloud orchestration to deliver self-service provisioning. Edge computing is emerging as a hybrid extension for factory and retail sites requiring sub-20-millisecond latency.

By Technology: AI-ML Outpaces All Other Toolsets

Cloud computing contributed 27.81% of 2025 revenue, encompassing IaaS, PaaS, and container orchestration. Artificial intelligence and machine learning grow 13.04% annually as enterprises shift from pilots to production, driving demand for data engineering, model validation, and continuous retraining. Cybersecurity services accelerate in parallel with rising incident counts and stricter audit regimes by the National Cyber and Crypto Agency.

Internet of Things deployments in manufacturing and logistics unlock predictive maintenance and asset tracking, although high upfront sensor costs restrict adoption to larger firms. Big-data platforms underpin AI, with organizations investing in data lakes and governance frameworks. Blockchain remains niche, limited to pilots in supply-chain traceability and digital identity, but a potential central-bank digital currency could expand its role. Robotic process automation and low-code tools democratize workflow creation, altering required skill profiles for future consultants.

Geography Analysis

Jakarta and West Java account for about 80% of the Indonesia IT services market size, driven by the concentration of banks, ministries, and multinational headquarters. Batam is an emerging secondary hub, leveraging submarine-cable proximity to Singapore for cross-border latency advantages. The Tier-4 National Data Center in Cikarang, slated to host 40 petabytes, remains pivotal to future public-sector consolidation despite onboarding delays.

Surabaya and Bandung form tertiary clusters supplying regional enterprises yet lag Jakarta by three to five years in power density and network redundancy. Outer islands such as Kalimantan and Sulawesi rely on satellite backhaul, which constrains telemedicine and real-time analytics, though the Palapa Ring fiber project aims to narrow the digital divide. Provincial procurement fragmentation stretches sales cycles, prompting providers to centralize compliance teams.

Edge-computing pilots in tier-2 cities process industrial IoT data locally, lowering backhaul cost and meeting latency targets. Hyperscale’s’ renewable-powered campuses in Batam and Bekasi help mitigate rising electricity tariffs, yet power availability remains a gating factor for capacity beyond Java. Microsoft’s skills investments across multiple provinces seek to ease talent disparities, though initial cohorts still cluster around Java-based universities. As infrastructure and skills diffuse, regional opportunities should mature beyond Jakarta’s orbit.

Competitive Landscape

The Indonesia IT services market features moderate concentration: Telkomsigma controls just over 11% of digital services through ministerial partnerships, while Accenture closed 62 transformation deals above USD 100 million in early 2025. Global firms such as IBM, Microsoft, and TCS differentiate through proprietary AI toolkits and industry accelerators that expedite modernization roadmaps. Local integrators Metrodata Electronics and Multipolar Technology leverage city-level service points in 130-plus locations to capture SME contracts unreachable by global peers.

Partnership ecosystems with AWS, Google Cloud, and Microsoft Azure represent the main competitive lever, commoditizing lift-and-shift migrations but placing premium on application modernization and managed security. Smaller challengers like Biznet Gio and Cloud4C attract mid-market customers with consumption-based pricing and turnkey SaaS blueprints. Regulatory emphasis on ISO 27001 and SOC 2 compliance filters out uncertified players, implicitly raising barriers to entry.

White-space prospects include edge nodes for factory IoT, sovereign AI infrastructure, and hybrid orchestration within regulated industries. Nvidia’s alliance with Indosat seeds the high-performance AI infrastructure layer, prompting services partners to build model-training offerings. Rising electricity tariffs pressure hyperscale ROI, motivating operators to explore liquid-cooling and renewable power purchase agreements that can become bundled consulting opportunities.

Indonesia IT Services Industry Leaders

PT Telekomunikasi Indonesia Tbk (Telkomsigma)

PT Multipolar Technology Tbk

PT Mitra Integrasi Informatika (MII)

PT Metrodata Electronics Tbk

PT Phintraco Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Amazon Kuiper committed USD 20 million to build six gateway stations for low-earth-orbit satellites, laying the groundwork for nationwide remote-area internet coverage.

- February 2025: TikTok finalised a 75%-stake merger with Tokopedia, pledging USD 1.5 billion to expand the combined e-commerce platform.

- January 2025: PT Pegadaian achieved 99.99% system availability through a Nutanix hybrid-cloud deployment that cut database provisioning to under 90 minutes.

- September 2024: Alibaba agreed to run GoTo workloads on Alibaba Cloud for at least five years, safeguarding future AI and analytics deployments.

Indonesia IT Services Market Report Scope

The Indonesia IT Services Market Report is Segmented by Service Type (IT Consulting and Implementation, Business Process Outsourcing Services, IT Outsourcing and Managed Services, Cloud Services and SaaS Implementation, Other Service Types), Enterprise Size (Small and Medium Enterprises, Large Enterprises), Industry (BFSI, IT and Telecom, Manufacturing, Healthcare, Government and Public Sector, Retail and E-Commerce, Energy and Utilities, Education, Other Industries), Deployment Model (On-Premise, Cloud, Hybrid), Technology (Cloud Computing, Artificial Intelligence and Machine Learning, Internet of Things, Cybersecurity Services, Big Data and Analytics, Blockchain and Emerging Tech, Other Technologies), and Geography (Indonesia). The Market Forecasts are Provided in Terms of Value (USD).

| IT Consulting and Implementation |

| Business Process Outsourcing Services |

| IT Outsourcing and Managed Services |

| Cloud Services and SaaS Implementation |

| Other Service Types |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| IT and Telecom |

| Manufacturing |

| Healthcare |

| Government and Public Sector |

| Retail and E-Commerce |

| Energy and Utilities |

| Education |

| Other Industries |

| On-Premise |

| Cloud |

| Hybrid |

| Cloud Computing |

| Artificial Intelligence and Machine Learning |

| Internet of Things |

| Cybersecurity Services |

| Big Data and Analytics |

| Blockchain and Emerging Tech |

| Other Technologies |

| By Service Type | IT Consulting and Implementation |

| Business Process Outsourcing Services | |

| IT Outsourcing and Managed Services | |

| Cloud Services and SaaS Implementation | |

| Other Service Types | |

| By Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By Industry | BFSI |

| IT and Telecom | |

| Manufacturing | |

| Healthcare | |

| Government and Public Sector | |

| Retail and E-Commerce | |

| Energy and Utilities | |

| Education | |

| Other Industries | |

| By Deployment Model | On-Premise |

| Cloud | |

| Hybrid | |

| By Technology | Cloud Computing |

| Artificial Intelligence and Machine Learning | |

| Internet of Things | |

| Cybersecurity Services | |

| Big Data and Analytics | |

| Blockchain and Emerging Tech | |

| Other Technologies |

Key Questions Answered in the Report

How large is the Indonesia IT services market in 2026?

The Indonesia IT services market size is projected at USD 5.41 billion in 2026, on its way to USD 9.52 billion by 2031.

Which customer group is expanding fastest?

Small and medium enterprises are forecast to grow at a 12.97% CAGR through 2031, outpacing large-enterprise expansion.

Why are hybrid deployments gaining popularity?

Hybrid architectures let organizations keep sensitive data on-premise to satisfy residency rules while moving analytics to cost-efficient public clouds.

What drives the surge in AI and ML services?

Banks, retailers, and manufacturers are moving generative-AI pilots into production, boosting demand for data engineering, model governance, and retraining services.

Who holds the largest share of Indonesias digital services?

Telkomsigma accounts for just over 11% of the digital segment, leveraging exclusive partnerships with state ministries and enterprises.

What is the main growth restraint outside Jakarta?

Ageing data-center infrastructure and limited connectivity in outer islands raise latency and restrict adoption of real-time applications.

Page last updated on: