Germany IT Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

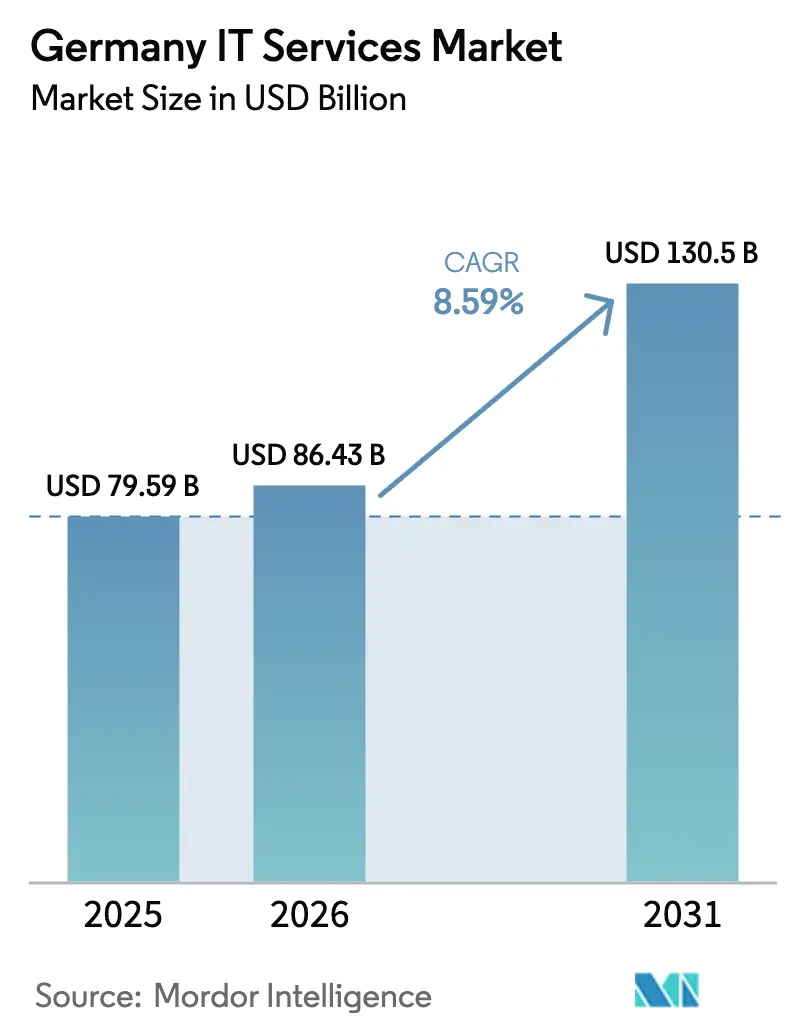

| Base Year Market Size (2025) | USD 79.59 Billion |

| Market Size (2026) | USD 86.43 Billion |

| Market Size (2031) | USD 130.5 Billion |

| Growth Rate (2026 - 2031) | 8.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany IT Services Market Analysis by Mordor Intelligence

The Germany IT Services market size was valued at USD 79.59 billion in 2025 and estimated to grow from USD 86.43 billion in 2026 to reach USD 130.5 billion by 2031, at a CAGR of 8.59% during the forecast period (2026-2031). This growth stems from Germany’s status as Europe’s largest economy, the federal push for digital sovereignty, and sustained enterprise demand for cloud-native platforms that comply with stringent data-protection laws. Robust industrial clusters, especially in Bavaria and Baden-Württemberg, continue to modernize production systems through Industrial IoT initiatives, while public-sector digitalization programs funded under the EU Digital Decade provide a long-term stimulus for advisory, integration, and managed services engagements.[1]Bundesministerium für Digitales und Verkehr, “Europa,” bmdv.bund.de Heightened cyber-threat complexity, paired with a shrinking domestic security workforce, is pivoting buyer priorities toward outsourced 24/7 monitoring and incident-response models anchored in German data centers. Cost inflation for highly skilled technologists and chronic talent shortages are, however, encouraging hybrid onshore–offshore delivery strategies, especially for standardized development and maintenance work.

Key Report Takeaways

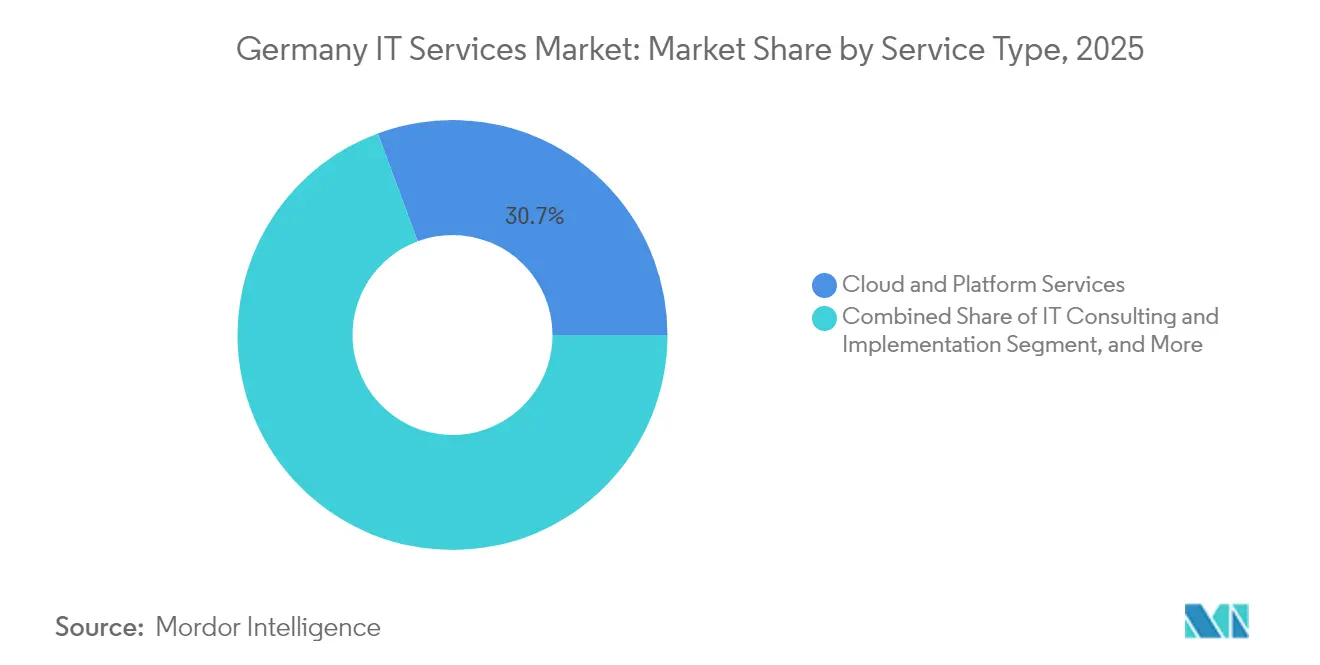

- By service type, Cloud and Platform Services led with 30.65% revenue share in 2025; Managed Security Services is forecast to expand at a 12.22% CAGR to 2031.

- By enterprise size, Large Enterprises held 64.10% of the Germany IT Services market share in 2025, while SMEs recorded the highest projected CAGR at 9.66% through 2031.

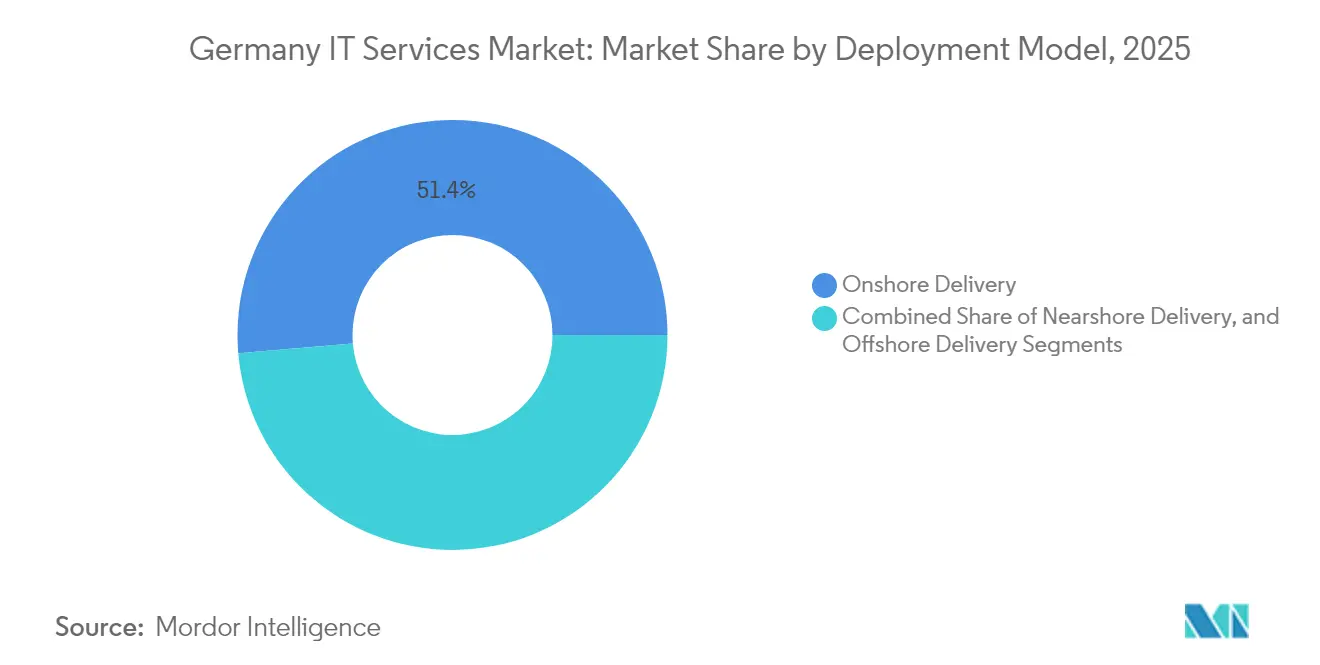

- By deployment model, Onshore Delivery represented 51.35% of the Germany IT Services market size in 2025, and Offshore Delivery is advancing at a 10.14% CAGR through 2031.

- By end-user vertical, Manufacturing captured 19.10% share of the Germany IT Services market size in 2025; Healthcare and Life-Sciences is growing at a 9.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Cloud-native Adoption in Mittelstand | +2.1% | National, concentrated in Bavaria, Baden-Württemberg, and North Rhine-Westphalia. | Medium term (2-4 years) |

| Rising Cyber-threat Complexity Driving MSS Demand | +1.8% | National, with priority focus on critical infrastructure sectors | Short term (≤ 2 years) |

| EU Digital Decade Funding Stimulus | +1.4% | National, with enhanced allocation to rural and underserved regions | Long term (≥ 4 years) |

| Industrial IoT-led Smart-Factory Upgrades | +1.2% | Regional, primarily in manufacturing clusters of Baden-Württemberg, Bavaria | Medium term (2-4 years) |

| Shortage of In-house IT Talent in SMEs | +0.9% | National, acute in metropolitan areas and tech hubs | Long term (≥ 4 years) |

| AI-assisted Software Modernisation Needs | +0.8% | National, early adoption in the financial services and automotive sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Cloud-native Adoption in the Mittelstand

Mittelstand firms are ramping up spending on scalable cloud platforms to replace aging on-premises systems, driven in part by a 50% federal co-funding scheme that subsidizes digital consulting fees up to EUR 1,100 (USD 1,243) per day. Specialized service providers have responded by building sovereign AWS-aligned practices staffed with several hundred engineers who focus exclusively on medium-sized manufacturing and professional-services clients. Despite historic caution over data-protection risks, three-quarters of German SMEs now view external cloud expertise as essential to competitiveness, setting the stage for multi-year migration and managed-services contracts that emphasize compliance, cost predictability, and rapid deployment.

Rising Cyber-threat Complexity Driving MSS Demand

The Germany IT Services market is experiencing double-digit growth in managed security services as executive boards elevate cyber resilience to a strategic priority. National regulations derived from the NIS 2 directive require critical-infrastructure operators to maintain continuous monitoring and incident-response capabilities by 2026, prompting a wave of SOC build-outs within German borders. Because the domestic cybersecurity workforce shrank from 455,951 to 439,243 professionals in 2024, enterprises increasingly outsource threat detection and response to providers that guarantee data residency and round-the-clock coverage. AI-enhanced analytics and quantum-resistant encryption are emerging differentiators that support premium pricing and contract extensions of five years or more.

EU Digital Decade Funding Stimulus

Germany will channel more than EUR 2 billion (USD 2.34 billion) into high-performance computing and EUR 1.4 billion (USD 1.64 billion) into cybersecurity infrastructure by 2027 under the EU Digital Decade program, with further investments earmarked for artificial intelligence and advanced connectivity. The program’s emphasis on digital sovereignty dovetails with national initiatives that restrict sensitive workloads to EU-based data centers, thereby expanding demand for consulting, integration, and managed services from domestic or European-owned providers. Seventeen European Digital Innovation Hubs across Germany give SMEs subsidized access to testing environments, digital-skills programs, and financing support, creating a pipeline of transformation projects that multiply revenue opportunities for local IT firms.

Industrial IoT-led Smart-Factory Upgrades

Manufacturing companies are implementing digital twins, edge analytics, and automated material flows to transform legacy plants into data-driven smart factories. Frameworks such as the BaSyx middleware platform from the Fraunhofer Institute require tailored integration, real-time data orchestration, and stringent safety protocols through the entire lifecycle.[2]Fraunhofer IESE, “Industrie 4.0,” iese.fraunhofer.de Providers that combine operational-technology expertise with cloud-native development skills can command premium rates for multi-year engagements covering feasibility assessment, architecture design, deployment, and continuous optimization. These programs boost plant-level productivity, reinforce Germany’s export competitiveness, and contribute meaningfully to the overall Germany IT Services market growth trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Federal Data-Residency Mandates | -1.3% | National, particularly affecting the healthcare and public sector | Short term (≤ 2 years) |

| Escalating Wage Inflation for Tech Specialists | -0.8% | National, concentrated in Berlin, Munich, and Hamburg tech corridors | Medium term (2-4 years) |

| Persistent Legacy Core-System Dependencies | -0.6% | National, prevalent in insurance, banking, and manufacturing sectors | Long term (≥ 4 years) |

| High Switching Costs for Mission-critical Apps | -0.4% | National, affecting large enterprises and public sector entities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Federal Data-Residency Mandates

Legislation effective July 2024 confines the processing of health and social data to Germany, EU member states, the EEA, Switzerland, or jurisdictions awarded GDPR adequacy status and obliges cloud providers to secure BSI C5 certification. Capital expenditure on additional domestic data-center capacity—forecast to triple to 3.3 GW by 2030—raises costs for both providers and clients, especially in price-sensitive SME segments. While the rules protect national interests and stimulate local infrastructure build-outs, they also limit the flexibility of global delivery models and slow the adoption of low-cost offshore resources.

Escalating Wage Inflation for Tech Specialists

Germany faces record IT-talent shortages, with 149,000 vacancies in 2023 and projections that unfilled roles could quadruple by 2040.[3]get in IT, “So sieht der IT-Arbeitsmarkt 2025 aus,” get-in-it.de Competition for AI engineers, cloud architects, and security analysts inflates salary budgets and compresses provider margins, prompting a reevaluation of sourcing strategies. Enterprises increasingly balance onshore regulatory demands with cost-effective nearshore or offshore centers of excellence, while automation and low-code platforms partially offset headcount pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud Platforms Drive Digital Sovereignty

The Cloud and Platform Services segment accounted for 30.65% of 2025 revenue, underscoring the strategic importance of scalable, compliant infrastructure as enterprises modernize core systems in line with GDPR and national sovereignty guidelines. Managed Security Services, although smaller today, shows the strongest momentum at 12.22% CAGR through 2031, fueled by NIS 2 regulatory deadlines and a diminishing domestic security workforce. Providers are bundling cloud migration, zero-trust architecture, and 24/7 SOC offerings into integrated contracts that extend five years or longer. The combination of sovereign hosting and AI-assisted automation differentiates market leaders and supports premium fee structures.

The Germany IT Services market size for managed security is expected to more than double during the forecast horizon as organizations replace fragmented in-house tools with platform-based services that validate data residency. Strategic tie-ups—such as sovereign-cloud partnerships between STACKIT and ServiceNow—demonstrate how vendors re-engineer product roadmaps to satisfy European compliance requirements while sustaining innovation velocity. Legacy outsourcing and business-process services remain relevant but face price pressure; value accrues to providers offering asset-light, platform-centric solutions.

By End-User Enterprise Size: SME Acceleration Reshapes Market Dynamics

Large Enterprises continue to anchor contract renewals and bespoke transformation programs, retaining 64.10% of 2025 revenue. However, SMEs are the fastest-growing cohort, posting a 9.66% CAGR through 2031 as federal and regional subsidy schemes lower adoption barriers. Programs such as Digitalbonus Thüringen cover half the cost of hardware, software, and external expertise up to EUR 15,000 (USD 16,950), encouraging even micro-enterprises to migrate workloads to the cloud.

The Germany IT Services market share differential will narrow over time as standardized SaaS and managed services packages become widely available on pay-as-you-go terms. Providers increasingly develop SME-centric service catalogs that offer fixed-price assessments, rapid deployment templates, and local language support. European Digital Innovation Hubs strengthen this trend by offering test labs, training, and match-making services that shrink the perceived risk and complexity of digital transformation for smaller firms.

By Deployment Model: Offshore Growth Challenges Onshore Preference

Onshore Delivery held 51.35% of 2025 spend, a reflection of Germany’s preference for face-to-face engagement, cultural affinity, and tight regulatory oversight. Even so, Offshore Delivery is forecast to expand at a 10.14% CAGR as clients pursue labor-arbitrage savings and 24-hour development cycles for non-regulated workloads. Providers mitigate sovereignty concerns by segmenting delivery: requirements analysis, architecture, and governance stay onshore, while coding and QA shift to certified centers in GDPR-adequate jurisdictions.

The Germany IT Services market size for nearshore operations is also rising as Central- and Eastern-European hubs capitalize on EU legal alignment and time-zone proximity. Hybrid models that blend local project management with offshore talent pools let enterprises manage cost, compliance, and agility factors in tandem. Heightened data-residency enforcement in health and public-sector workloads means that onshore capacity will remain indispensable even as offshore percentages climb.

By End-User Vertical: Healthcare Digitalization Accelerates Growth

Manufacturing preserved its lead with 19.10% of 2025 spend, driven by smart-factory rollouts that embed analytics, edge computing, and digital-twin functionality into production environments. The Germany IT Services market size attached to healthcare, however, is scaling quickly as the electronic patient record becomes compulsory and telemedicine services proliferate. With a forecast 9.95% CAGR, the vertical is on track to outpace all others by 2031, helped by EUR-scale federal grants for secure data networks and interoperability frameworks.

Financial services remain a sizable and regulation-intensive customer group, while the public sector is awarding multi-cloud brokerage and procurement-platform contracts that favor providers able to demonstrate data sovereignty and strong SLAs. Energy and utilities, telecom, and logistics clients pursue real-time monitoring and predictive-maintenance use cases that blend operational-technology integration with AI-driven analytics, expanding the addressable revenue pool for specialized vendors.

Geography Analysis

The Germany IT Services market is deeply domestic yet anchored in a broader European context that shapes regulatory frameworks and funding priorities. Berlin and Munich incubate a dense startup ecosystem and host R&D centers for global cloud and software companies, creating concentrated demand for specialized consulting and security services. Hamburg and the Rhine-Ruhr region supply logistics, e-commerce, and media clients that consume application-development and omnichannel-support offerings.

Baden-Württemberg and Bavaria, home to automotive and machinery leaders, generate high-value projects in predictive maintenance, robotics integration, and digital twin design. Federal digital-infrastructure programs earmark significant grants for rural fiber and 5G rollout, widening service opportunities beyond metropolitan areas. Cross-border expansion focuses on EU neighbors where shared data-protection rules simplify contractual obligations; German firms often act as prime contractors in multi-country tenders for secure cloud and public-sector modernization.

Infrastructure providers are adding capacity in Frankfurt, Berlin-Brandenburg, and Leipzig to meet in-country hosting requirements for critical data workloads. The Connecting Europe Facility Digital fund complements these domestic investments by subsidizing quantum-communications pilots and high-performance computing nodes that will anchor future digital-industrial projects. The geographic diversification of both demand and delivery resources reinforces Germany’s role as a linchpin for compliant, pan-European IT services.

Competitive Landscape

Competition is a hybrid mix of global consultancies, national champions, and sector-focused specialists. Accenture, Capgemini, and IBM leverage global scale and advanced delivery frameworks, yet must localize offerings to satisfy Germany’s data-sovereignty requirements. T-Systems leads the domestic tier, combining extensive network assets with cloud and security practices tailored to highly regulated verticals. Mid-size players such as Adesso—whose revenue surpassed EUR 1 billion (USD 1.14 billion) in 2024—differentiate through agility and deep industry know-how, especially in utilities and healthcare.

Providers sharpen their value propositions around compliance, sovereign hosting, and zero-trust security. Several, including Controlware and Datagroup, operate German-based SOCs that assure local log storage and incident handling. Private-equity activity is brisk: KKR purchased Datagroup for roughly USD 500 million, and H.I.G. Capital invested in TIMETOACT to accelerate portfolio expansion. Firms with mature hybrid-delivery models and vertical-specific accelerators are best positioned as clients seek partners that can navigate regulatory intricacies while delivering measurable ROI.

The competitive outlook will intensify as hyperscaler-aligned partners deepen specialization in analytics, AI, and cybersecurity. Nevertheless, German ownership structures and established public-sector credentials remain potent differentiators that protect domestic market share, especially in contracts governed by strict residency mandates.

Germany IT Services Industry Leaders

T-Systems International GmbH

IBM Deutschland GmbH

Accenture GmbH

Atos Information Technology GmbH

Capgemini Deutschland GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: H.I.G. Capital announced a strategic investment in TIMETOACT GROUP, expanding resources for cloud transformation and AI services.

- August 2025: Adesso SE reported 12% higher sales to EUR 709.5 million (USD 801.7 million) and a 34% EBITDA jump in H1 2025, citing robust healthcare and utilities demand.

- May 2025: Eviden secured a contract to digitize the federal “Kaufhaus des Bundes – Next Generation” procurement platform, covering 22,000 users across 480 agencies.

- April 2025: KKR finalized the USD 500 million acquisition of Datagroup, reinforcing consolidation among mid-tier German IT service providers.

Germany IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Onshore Delivery |

| Nearshore Delivery |

| Offshore Delivery |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-user Verticals |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By Deployment Model | Onshore Delivery |

| Nearshore Delivery | |

| Offshore Delivery | |

| By End-user Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-user Verticals |

Key Questions Answered in the Report

How large is the Germany IT Services market in 2026?

The market is valued at USD 86.43 billion in 2026 with an 8.59% CAGR projected to 2031.

Which service type is growing fastest?

Managed Security Services is forecast to grow at a 12.22% CAGR through 2031 as firms address rising cyber-risk exposure.

What drives SME demand for IT services?

Federal and regional subsidies covering up to 50% of digitalization costs, combined with easy-to-deploy cloud packages, accelerate SME adoption.

How do data-residency laws affect provider selection?

Laws that mandate processing sensitive data within EU jurisdictions favor domestic or European-owned vendors with certified German data centers.

Which German regions create the most IT services demand?

Berlin, Munich, Hamburg, and the Rhine-Ruhr cluster lead consulting and cloud uptake, while Baden-Württemberg and Bavaria dominate Industrial IoT projects.

What is the outlook for offshore delivery?

Offshore Delivery is projected to expand at a 10.14% CAGR as enterprises balance cost savings with compliance by adopting hybrid onshore–offshore models.

Page last updated on: