Netherlands Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

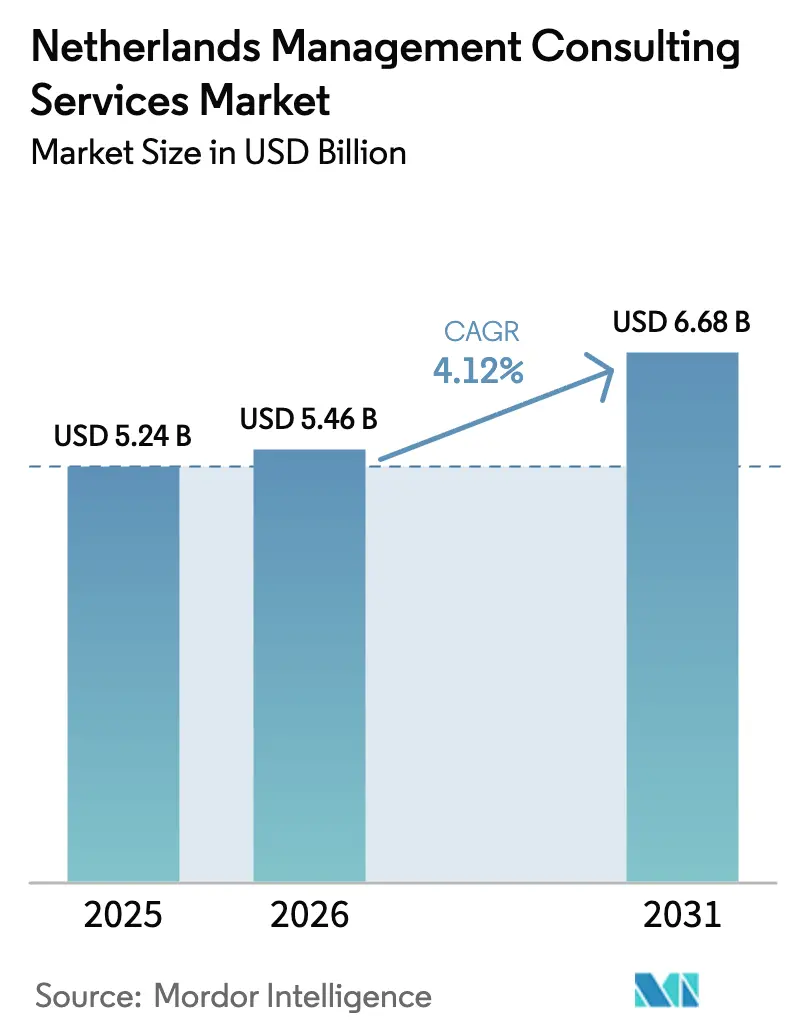

| Base Year Market Size (2025) | USD 5.24 Billion |

| Market Size (2026) | USD 5.46 Billion |

| Market Size (2031) | USD 6.68 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

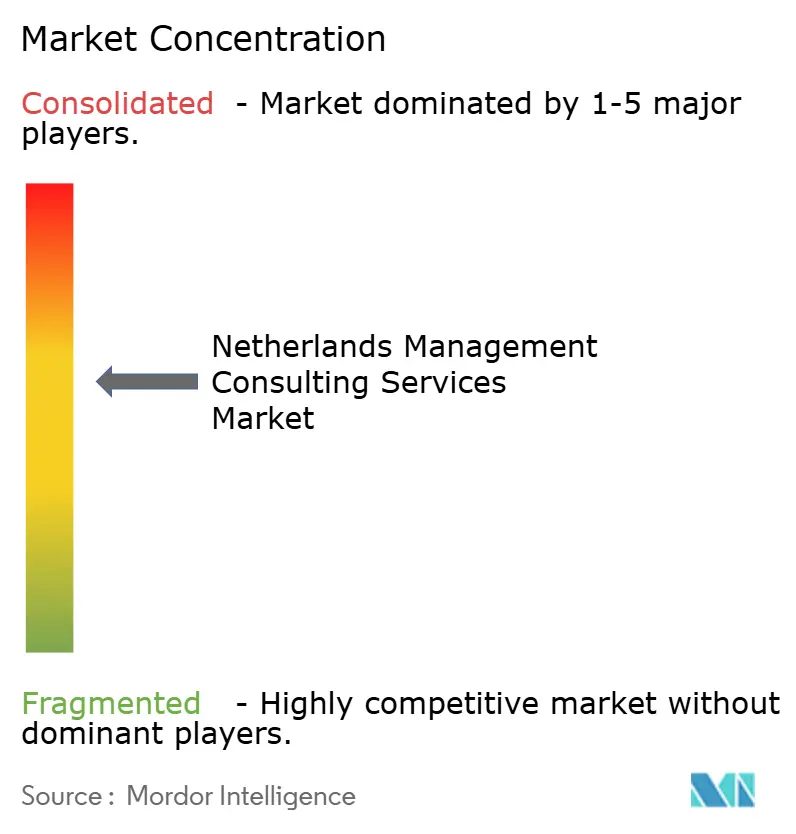

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Management Consulting Services Market Analysis by Mordor Intelligence

The Netherlands management consulting services market size is expected to grow from USD 5.24 billion in 2025 to USD 5.46 billion in 2026 and is forecast to reach USD 6.68 billion by 2031 at 4.12% CAGR over 2026-2031. The growth reflects continued demand for digital transformation, compliance with the Corporate Sustainability Reporting Directive (CSRD), and strategic advisory work linked to generative AI adoption. Large enterprises remain the primary revenue contributors, yet small and medium-sized enterprises (SMEs) are scaling consulting spend faster as cloud migration and automation become survival imperatives. Sustained government investment in sovereign cloud, tighter sustainability rules, and a vibrant start-up scene keep the Netherlands' management consulting services market on a measured but resilient expansion path. Competitive intensity is rising as global majors consolidate digital capabilities and local specialists leverage technology-enabled delivery to address a persistent senior-consultant talent gap.

Key Report Takeaways

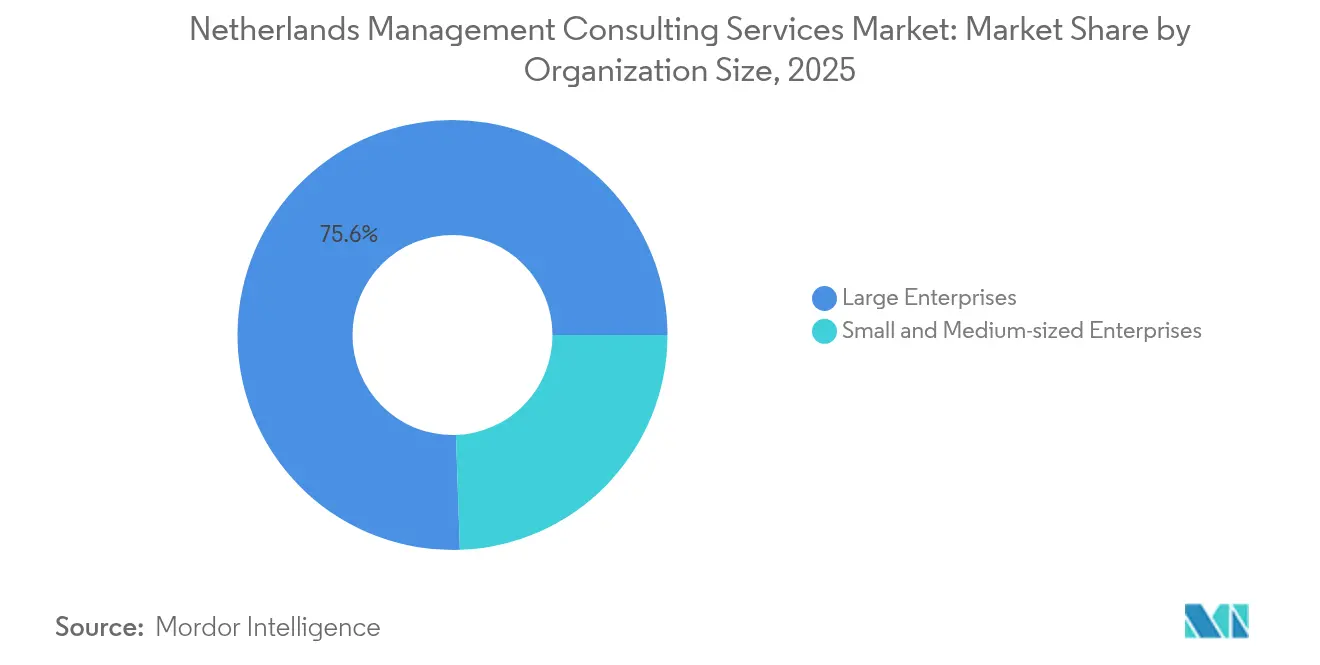

- By organization size, large enterprises held 75.55% of the Netherlands management consulting services market share in 2025, while SMEs are projected to expand at a 6.05% CAGR through 2031

- By service type, operations consulting led with 36.85% of the Netherlands management consulting services market size in 2025, whereas technology consulting is poised to grow at a 5.52% CAGR to 2031.

- By delivery model, on-site projects captured 62.45% of the Netherlands management consulting services market share in 2025; remote and virtual engagements are forecast to advance at a 5.78% CAGR over the same horizon.

- By end-user industry, financial services dominated with 26.35% of the Netherlands management consulting services market size in 2025, while healthcare and life sciences are expected to post the fastest 5.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong digital-first policy push by Dutch government | +0.8% | National – Amsterdam, The Hague, Rotterdam | Medium term (2-4 years) |

| Rapid cloud-migration wave among Dutch SMEs | +0.7% | National – Randstad early gains | Short term (≤ 2 years) |

| ESG regulations driving advisory demand (CSRD rollout) | +0.6% | National, EU-wide compliance | Medium term (2-4 years) |

| Post-pandemic hybrid-work operating-model redesign | +0.5% | National, urban business centers | Short term (≤ 2 years) |

| Defence and cyber-security spending uptick | +0.4% | National – NATO coordination | Long term (≥ 4 years) |

| Large corporates outsourcing Gen-AI road-mapping | +0.3% | National – multinational HQs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Digital-First Policy Push by Dutch Government

The January 2025 national digitalization strategy prioritizes sovereign cloud, data interoperability, and generative AI use across 355 municipalities, triggering multi-year advisory demand for cloud architecture, change management, and citizen-experience optimization. [1]Rijksoverheid, “Overheid verruimt standpunt inzet generatieve AI,” rijksoverheid.nl The EUR 590 million sovereign “Rijkscloud” motion alone opens a comparable consulting addressable market as ministries seek support in infrastructure design, migration, and risk governance. Preferential multi-year frameworks such as EY’s government-wide financial-advisory award illustrate the scale of public-sector outsourcing. Municipal pilots—Zuid-Holland’s PZH-assistant and Goes’ Chatbot Guus—signal an AI-first mindset that requires process re-engineering and ethics compliance expertise. As digital public-service benchmarks rise, private enterprises mirror best practices, reinforcing steady pipeline growth for the Netherlands management consulting services market.

Rapid Cloud-Migration Wave Among Dutch SMEs

Over two-thirds of government cloud services lacked the required risk assessments in 2025, underscoring parallel gaps across the SME landscape and creating a sizeable governance advisory niche. [2]Nederlandse Algemene Rekenkamer, “Dutch Central Government in the Cloud,” rekenkamer.nl Accelerated cloud adoption lets SMEs match large-company efficiency but exposes them to complex vendor-management, security, and data-sovereignty decisions. Xebia’s five-year AWS collaboration exemplifies partner-led ecosystems courting midsize clients through packaged migration and optimization offers. Clingendael Institute’s advocacy for European cloud options supports local-provider engagement, lifting domestic workload for security, compliance, and localisation specialists. The momentum feeds directly into a 6.0% CAGR for remote projects, a delivery mode well-suited to geographically dispersed SME customers and the evolving Netherlands management consulting services market.

ESG Regulations Driving Advisory Demand (CSRD Rollout)

The CSRD imposes 84 granular disclosures and 1,100 data points, propelling a EUR 1 billion advisory opportunity as firms integrate sustainability into financial reporting, supply-chain risk, and capital-allocation decisions. Dutch transposition law mirrors EU text, limiting legal interpretation risk yet demanding robust data infrastructure by FY 2026 filings. Half of Dutch corporates have drafted transition plans, above the global average, but execution complexity sustains external-consultant reliance. The forthcoming Corporate Sustainability Due Diligence Directive expands the scope to suppliers, while national WIVO rules introduce a six-step due diligence process enforced by the competition regulator. Transactions such as Alliander’s Kenter divestiture illustrate how ESG imperatives reshape portfolio strategy, a trend that channels higher-margin strategic and operational mandates into the Netherlands management consulting services market.

Post-Pandemic Hybrid-Work Operating-Model Redesign

Part-time work already involves 42% of Dutch employees, complicating hybrid scheduling and spurring demand for organisational-design consulting. Record labour-force participation at 68.7% compounds pressure to rethink workflows, benefits, and digital-workspace tools while maintaining productivity. Consulting firms are adopting diamond-shaped staffing models that emphasise mid-level expertise, mirroring the client side quest for agile structures. Integrated ERP rollouts such as Croonwolter&Dros’s SAP S/4HANA project show how technology underpins workforce flexibility. As hybrid norms stabilise, recurring advisory around culture, leadership, and performance measurement keeps the Netherlands management consulting services market resilient.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight senior-consultant labour pool in NL | -0.6% | National – Amsterdam, Rotterdam hubs | Long term (≥ 4 years) |

| Procurement-price pressure from large multinationals | -0.4% | National – Fortune 500 corporates | Medium term (2-4 years) |

| Slower FDI inflows into non-tech sectors | -0.3% | National, regional spill-over | Medium term (2-4 years) |

| Heightened client scrutiny on billable hours | -0.2% | National, cross-sector | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tight Senior-Consultant Labour Pool in NL

The Dutch labour market posts 1.5 million annual vacancies, and seasoned consultants rank among the scarcest profiles, especially in digital transformation and ESG. Demographic ageing means replacement demand outstrips new entrants, pushing firms to tap a 1.1 million-strong, highly educated freelancer base despite Wet DBA regulatory uncertainty. Housing shortages in Amsterdam and Rotterdam hamper relocation, while recent reductions in the 30% expat tax ruling curb international talent draw. The Highly Skilled Migrant Programme offers partial relief yet faces political debate, clouding long-term planning. Talent scarcity raises salary inflation and delivery-capacity constraints, tempering the otherwise upbeat Netherlands management consulting services market outlook.

Procurement-Price Pressure from Large Dutch Multinationals

Energy-intensive manufacturers cut gas usage by 25% in 2022, embedding frugality in support-service spending and cascading fee pressure on consultancies. Highly educated freelancer rates rose only 1.5% in 2025 against 3% inflation, signalling systemic pricing resistance. Global procurement teams benchmark Dutch fees with other EU hubs, pushing for outcome-based contracts and capped-rate cards. Firms respond by differentiating through proprietary accelerators and sector-specific technology alliances, yet margin squeeze remains acute, subtracting 0.4 percentage points from projected Netherlands management consulting services market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Large Enterprises Dominate Despite SME Acceleration

Large corporates accounted for 75.55% of the Netherlands management consulting services market share in 2025, reflecting their complex multi-jurisdictional compliance and multi-year digital-transformation mandates. Engagements often cover CSRD reporting frameworks encompassing 84 metrics and 1,100 data points. SMEs, however, represent the fastest-moving cohort with a 6.05% CAGR as cloud infrastructure and automation solutions become commoditised. Government digital-inclusion programmes and sovereign-cloud initiatives lower barriers, allowing smaller firms to access enterprise-grade advisory. Platforms such as Cinode bring large-firm project-management capability within SME reach, encouraging broader client penetration and underpinning long-term expansion of the Netherlands management consulting services market.

SME momentum also reflects the wider Dutch IT ecosystem: 25,000 technology enterprises generated EUR 34 billion turnover and employed 265,000 professionals in 2024. Consultants package cloud-migration blueprints, cybersecurity health checks, and generative-AI readiness assessments to serve these firms at scale. As a result, the Netherlands management consulting services market size for SMEs alone is projected to surpass USD 1.82 billion by 2031, adding diversification to a landscape historically weighted toward large-enterprise retainers.

By Service Type: Operations Consulting Leads While Technology Accelerates

Operations consulting retained 36.85% of the Netherlands management consulting services market size in 2025 on the back of process optimisation, supply-chain resilience, and cost-take-out programmes. The segment benefits from the Netherlands’ logistics centrality and energy-security challenges that place efficiency at a premium. Technology consulting’s 5.52% CAGR points to cloud migration, AI deployment, and cyber-resilience as core growth layers, with Capgemini investing EUR 3.3 billion to bolster its AI portfolio through the WNS acquisition. Strategy consulting overlaps these domains as ESG mandates reshape capital-allocation playbooks, while HR specialists redesign workforce architecture to mitigate the talent crunch.

Technology projects are increasingly embedded within broader operational transformation, blurring service-line borders. IG&H’s purchase of Sourceful ICT to expand low-code development underlines how local players extend digital depth to compete with global integrators. As automation permeates finance, government, and retail, technology consulting could approach one-third of the total Netherlands management consulting services market revenue by 2031, reducing operations lead but reinforcing advisory interdependence.

By Delivery Model: Remote Consulting Gains Traction

On-site engagements captured 62.45% of the Netherlands management consulting services market share in 2025, as C-suite workshops, stakeholder alignment, and culture-change sessions still favor physical presence. Yet remote and hybrid delivery is growing at a 5.78% CAGR, fuelled by videoconferencing normalisation and the need to tap global talent amid domestic shortages. Diamond-structure staffing models distribute execution to near-shore and offshore experts while client-facing leads remain local, optimising cost-to-serve.

This shift dovetails with the Netherlands’ high part-time employment rate, enabling consultants to balance travel with remote collaboration. Technology platforms such as Cinode streamline resource allocation across dispersed teams, reinforcing utilisation targets and timeline discipline. As clients increasingly accept outcome-based milestones over onsite hours, remote engagements could exceed 40% of overall Netherlands management consulting services market delivery by the end of the decade.

By End-User Industry: Financial Services Dominance Amid Healthcare Growth

Financial institutions generated 26.35% of the Netherlands management consulting services market size in 2025, anchored by regulatory change, fintech integration, and cyber-risk management. Amsterdam’s strong banking and insurance concentration guarantees a pipeline of strategy, risk, and digital-core transformation mandates. Healthcare and life sciences are forecast to lead growth at a 5.34% CAGR as EU pharmaceutical reforms introduce regulatory sandboxes and real-world evidence into approvals, demanding new data-governance and operating-model support. Digital health, hospital workflow optimisation, and med-tech innovation amplify consulting spend.

Meanwhile, manufacturing clients seek efficiency amid volatile energy prices, and energy-utility stakeholders fund large-scale decarbonisation planning. Retailers such as Albert Heijn evolve into tech-driven omnichannel operators, leaning on advisory input for data-platform design and customer-analytics road-maps. The diverse sector mix cushions cyclical swings and strengthens the structural case for the Netherlands' management consulting services market.

Geography Analysis

The Randstad—Amsterdam, Rotterdam, The Hague, and Utrecht—accounts for roughly 69.40% of the Netherlands' management consulting services market revenue. Amsterdam anchors multinational headquarters and fintech clusters requiring high-end strategy and regulatory expertise. Rotterdam, as Europe’s largest port, demands supply-chain optimisation and energy-transition consulting tied to its hydrogen hub ambitions. The Hague contributes sizeable public-sector spend, evidenced by a EUR 590 million multi-year framework for financial advisory across ministries.

Eindhoven’s Brainport region has become a technology-innovation magnet via ASML and allied suppliers, generating R&D-centric advisory demand and drawing global tech talent despite tight housing markets. Secondary cities such as Groningen and Maastricht emerge as cost-advantage locations for shared-service centres, sparking localised process-optimisation projects.

Digital-transformation mandates diffuse across all 355 municipalities under expanded AI guidelines, creating grassroots opportunities for smaller consultancies and niche specialists. Projects like Goes’ Chatbot Guus illustrate that advanced advisory is no longer confined to metropolitan hubs. Compact national geography and dense transport links allow firms to serve clients coast-to-coast from central bases, yet escalating urban housing costs push firms to embrace remote delivery to secure talent retention and cost competitiveness. Overall, geography remains a lens for sector specialisation more than access, reinforcing balanced capacity utilisation across the Netherlands management consulting services market.

Competitive Landscape

The market is moderately consolidated: Deloitte, KPMG, PwC, and EY collectively command a significant revenue share, leveraging global alliances, end-to-end service portfolios, and entrenched C-suite relationships. EY alone reported EUR 983 million in Dutch revenue in 2024, with consulting growing 30% to EUR 187 million. Strategy houses McKinsey, BCG, and Bain dominate premium problem-solving mandates, while technology integrators Accenture, Capgemini, IBM, and CGI exploit cloud engineering scale.

Consolidation is intensifying. Capgemini’s EUR 3.3 billion WNS purchase and its April 2025 takeover of Delta Capita’s Dutch unit expand AI and financial-crime capabilities, respectively. [4]Capgemini, “Capgemini acquires Delta Capita unit,” capgemini.com Local champions IG&H, Valcon, and BearingPoint retain share through sector-specific depth and agile delivery models, with IG&H reinforcing digital capability via Sourceful ICT. Emerging disruptors include platform-powered networks that orchestrate specialised freelancers, underpinning cost-flexible bids for midsize clients.

Pricing pressure from sophisticated procurement teams is steering the Netherlands management consulting services market toward outcome-based contracts, IP-based accelerators, and technology-enabled managed-service offerings. Firms that combine depth in sustainability, cyber-security, and data engineering with flexible engagement models are best positioned to protect margins and secure multi-year annuities in an otherwise competitive arena.

Netherlands Management Consulting Services Industry Leaders

Accenture Netherlands

Deloitte Consulting Netherlands

KPMG Advisory Netherlands

PwC Advisory Netherlands

EY Advisory Netherlands

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Capgemini acquired Delta Capita’s Dutch subsidiary, adding 200 specialists in financial crime compliance to strengthen Benelux regulatory advisory.

- February 2025: EY Netherlands secured a EUR 590 million preferred-supplier framework covering financial advisory across all Dutch ministries.

- January 2025: IG&H bought Polish software house Sourceful ICT, enhancing low-code delivery capability for digital-transformation clients.

- October 2024: Xebia signed a five-year strategic collaboration agreement with AWS to scale cloud-consulting services across Benelux manufacturing, finance, and retail.

Netherlands Management Consulting Services Market Report Scope

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types |

| On-site Consulting |

| Remote/Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment, and Sports |

| Hospitality and Travel |

| Other Industries |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types | |

| By Delivery Model | On-site Consulting |

| Remote/Virtual Consulting | |

| By End-user Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment, and Sports | |

| Hospitality and Travel | |

| Other Industries |

Key Questions Answered in the Report

What is the current size of the Netherlands management consulting services market?

The Netherlands management consulting services market size reached USD 5.46 billion in 2026 and is projected to climb to USD 6.68 billion by 2031.

Which segment is growing fastest in the Netherlands management consulting services market?

Technology consulting, driven by cloud migration and AI projects, is forecast to expand at a 5.52% CAGR through 2031.

How important are SMEs to future consulting growth in the Netherlands?

SMEs contribute the fastest growth momentum, increasing consulting spend at a 6.05% CAGR as they adopt cloud and automation solutions.

What role does CSRD play in consulting demand?

The CSRD mandates extensive sustainability disclosures, unlocking an estimated EUR 1 billion in advisory work for reporting, data-management, and supply-chain transformation.

How is talent scarcity affecting consulting firms in the Netherlands?

A persistent shortage of senior consultants inflates salaries and limits delivery capacity, subtracting an estimated 0.6 percentage points from the market’s forecast CAGR.

Are remote consulting models gaining traction?

Yes. Remote and hybrid engagements are expected to outpace on-site growth, posting a 5.78% CAGR as clients accept virtual delivery and firms tap global talent pools.

Page last updated on: