Belgium Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2024 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

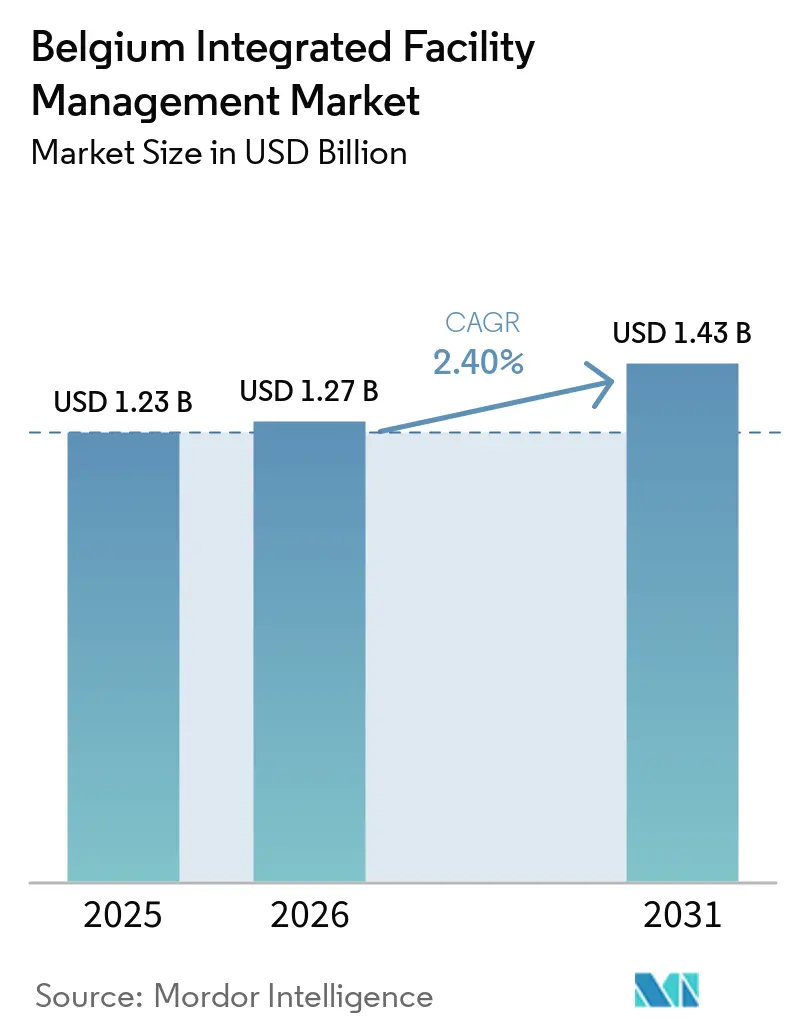

| Base Year Market Size (2025) | USD 1.23 Billion |

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 1.43 Billion |

| Growth Rate (2026 - 2031) | 2.40% CAGR |

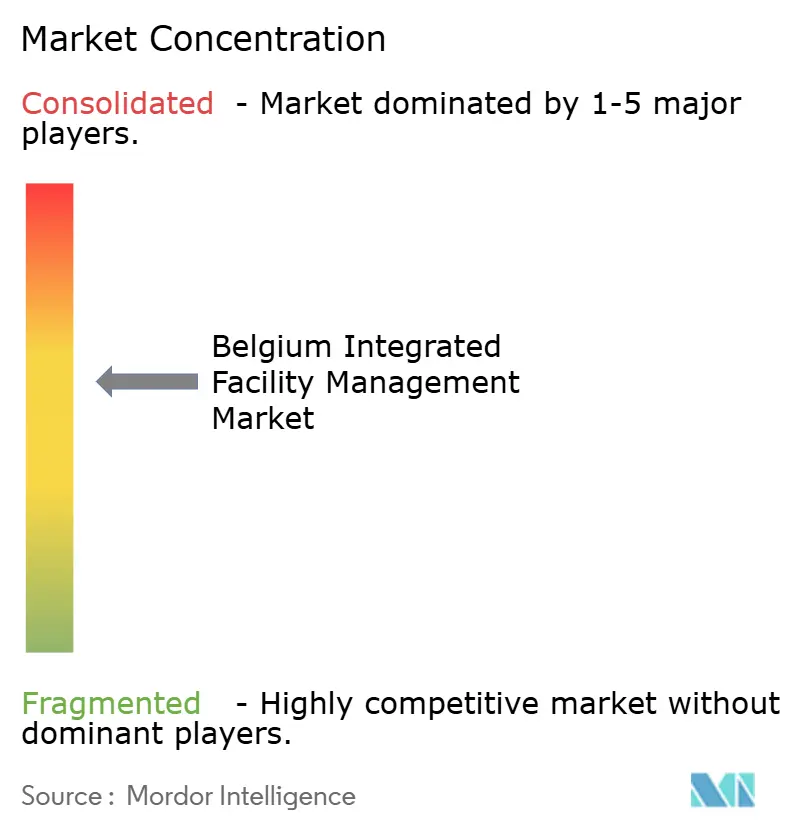

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Integrated Facility Management Market Analysis by Mordor Intelligence

The Belgium Integrated Facility Management Market size is expected to grow from USD 1.23 billion in 2025 to USD 1.27 billion in 2026 and is forecast to reach USD 1.43 billion by 2031 at 2.40% CAGR over 2026-2031.

The Belgium integrated facility management market is moving forward as enterprises shift from fragmented vendor structures toward single-provider operating models that offer better cost visibility and smoother service coordination across sites. Demand is also being shaped by mandatory building energy compliance, hybrid workplace redesign, and a broader move to position facility management as a governance and performance function rather than only a support line. The Belgium integrated facility management market still has room to deepen because Belgium’s outsourcing rate for facility services remained below the level seen in the Netherlands, which points to further conversion from bundled outsourcing to fuller integration over time. The Belgium integrated facility management market is also developing within a cautious procurement culture, where buyers often test bundled models first and then move toward broader integrated contracts once service reliability and KPI delivery are proven. Competition remains moderately concentrated, and larger operators are gaining an edge through acquisitions, local organizational investment, digital platforms, and stronger credentials in sustainability and cybersecurity compliance.

Key Report Takeaways

- By service type, soft facility management services led the Belgium integrated facility management market with a 64.61% share in 2025, while hard Facility Management services are projected to expand at a 3.36% CAGR through 2031.

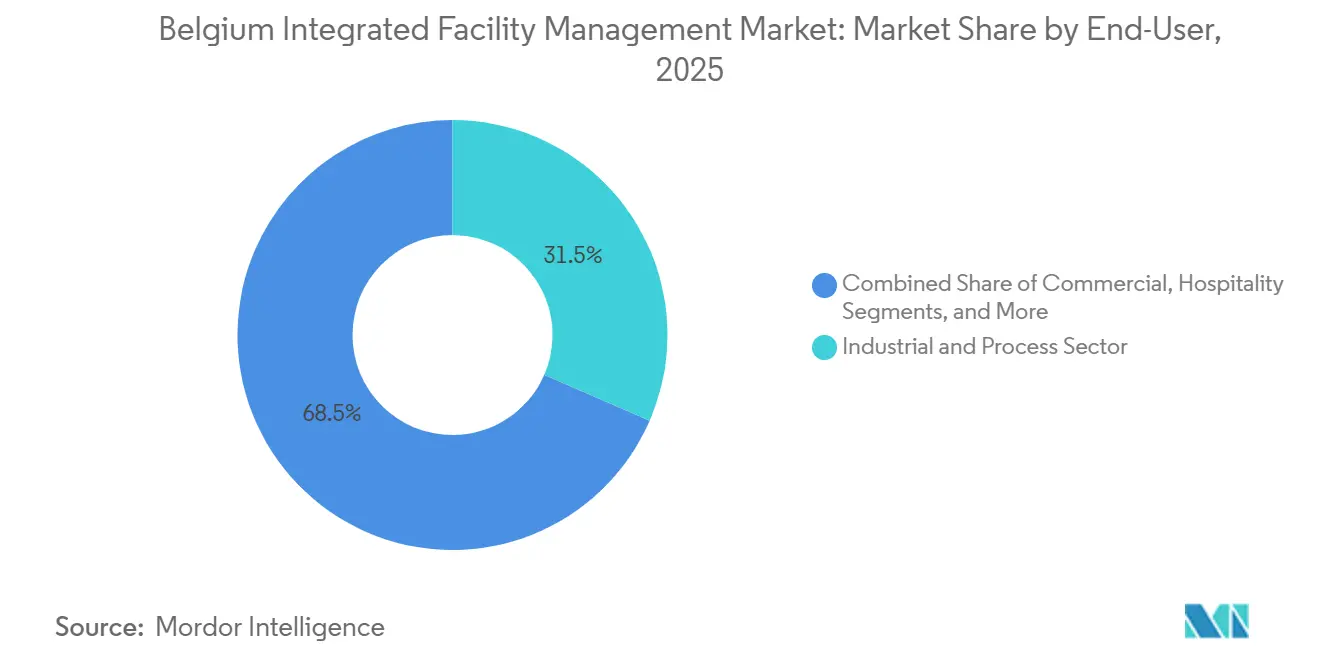

- By End-User, the industrial and process sector led the Belgium integrated facility management market with 31.52% share in 2025, while commercial end-users are forecast to grow at a 3.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Belgium Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Integrated Services for Cost Optimization | +0.7% | National, with concentration in Brussels, Antwerp, and Ghent metropolitan corridors | Short term (≤2 years) |

| Growing Demand for Energy-Efficient and Sustainable Building Solutions | +0.6% | National, highest intensity in Flanders under EPC NR and BACS mandates | Medium term (2-4 years) |

| Rising Outsourcing Trend Among Belgian Corporates | +0.5% | National, early uptake in Brussels financial and pharma clusters | Medium term (2-4 years) |

| Post-Pandemic IFM Recovery and Hybrid Work Model Adoption | +0.3% | National, with commercial real estate hubs as primary locus | Short term (≤2 years) |

| Expansion of Co-Investment and Joint Venture Activity in the FM Sector | +0.2% | National, with spill-over to Wallonia as cross-regional operators scale | Long term (≥4 years) |

| Significant Public Infrastructure Programs Driving Long-Term Facility Demand | +0.2% | National, early gains in Brussels federal facilities and Liège infrastructure projects | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Integrated Services for Cost Optimization

Belgian enterprises have steadily moved toward integrated service structures because managing one provider is simpler than coordinating many specialist vendors across the same estate. The PROCOS Group FM Trend Report 2025 identified cost predictability and supply-chain consolidation as the main reasons Belgian facility leaders were shifting toward integrated models.[1]PROCOS Group, “FM Trend Report 2025,” PROCOS Group, domain not provided in supplied draft. Multi-year IFM contracts also raise the practical cost of changing providers, which strengthens incumbent positions once a supplier proves stable KPI delivery over time. ISS Belgium’s 2025 acquisitions of Bluebridge Services and Vinca Services showed this logic clearly, because bringing specialist capability in-house reduced subcontractor dependence and improved control over delivery quality and margin visibility. That same model helps buyers standardize service levels across multi-site portfolios, which matters for multinational occupiers that manage Belgian sites within broader European real estate programs. The Belgium integrated facility management market is therefore advancing not only through new outsourcing wins, but also through deeper client relationships as buyers shift facility management into a more strategic operating role.

Growing Demand for Energy-Efficient and Sustainable Building Solutions

Energy and sustainability rules are turning technical facility management into a compliance-led service requirement for a wider set of Belgian building owners. From January 2026, large non-residential buildings in Flanders must maintain a valid EPC NR, while BACS compliance became mandatory from December 31, 2025, for buildings with heating or cooling systems above 290 kW.[2]Monard Law, “Flemish EPC NR and BACS Compliance Overview,” Monard Law, domain not provided in supplied draft. The planned reduction of the threshold to 70 kW by 2029 extends that obligation to mid-sized offices, schools, and healthcare facilities, which spreads the compliance workload through the full forecast period instead of concentrating it in one early wave.[3]EGEON Ingenieurs, “BACS Threshold and Compliance Update,” EGEON Ingenieurs, domain not provided in supplied draft. This change is allowing providers with energy monitoring, commissioning, retrofit coordination, and performance contracting capabilities to add new revenue streams beyond routine service delivery. Blue Pearl Energy’s acquisition of Energys showed that technical HVAC capability tied to energy efficiency is becoming more closely connected with the Belgian FM delivery stack.[4]IPE Real Assets, “Blue Pearl Energy Acquisition of Energys,” IPE Real Assets, domain not provided in supplied draft. Sustainability credentials are also becoming procurement filters, and Apleona’s SBTi-confirmed emissions target from February 2025 reinforced that enterprise buyers increasingly expect visible carbon-reduction commitments from facility partners.

Rising Outsourcing Trend Among Belgian Corporates

Belgium’s outsourcing penetration in facility services remained at 50% in 2025, which was below the Netherlands at 70% and left visible room for further adoption of integrated outsourcing models. That gap has reflected buyer caution, because many Belgian organizations have preferred to retain internal oversight until they are comfortable with the governance demands of full IFM delegation. At the same time, the role of the facility manager is becoming more cross-functional, with stronger links to HR, finance, IT, and real estate, which shifts internal teams toward policy and oversight rather than direct execution. The March 2026 belfa roundtable on single service versus IFM showed that the outsourcing model debate is moving from a specialist discussion to a broader market decision point. Providers are responding with phased onboarding structures that begin with bundled services and move toward fuller integration over 18 to 36 months, which reduces client concern over organizational disruption. The Belgium integrated facility management market is therefore widening its addressable base among mid-sized organizations that would have been reluctant to sign a full IFM contract under older delivery models.

Post-Pandemic IFM Recovery and Hybrid Work Model Adoption

Hybrid work has not reduced the importance of offices, but it has changed what clients expect those offices to deliver. ISS Belgium described this as a workplace performance gap, where facility spending can remain fixed even when occupancy patterns become uneven and less predictable. That shift is creating additional demand for occupancy analytics, flexible booking systems, adaptive cleaning, modular security coverage, and hospitality-led workplace services within the Belgium integrated facility management market. Providers are now framing the workplace as a tool for collaboration, culture, and talent retention rather than a fixed-capacity asset. Facilicom Belgium’s 2025 positioning of FM as added value rather than a cost line captured this change in buyer language and procurement framing. The supporting employee survey work cited by ISS across nearly 11,000 workers in 15 countries provided a broader evidence base for discussions that Belgian clients are already having around space quality, experience, and retention.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight Labor Force Driving Wage Inflation | -0.2% | National, most acute in Brussels with multilingual requirements and Antwerp industrial FM cluster | Short term (≤2 years) |

| Cost Uncertainty and Corporate CAPEX Constraints | -0.1% | National, intensified in sectors with high energy transition CAPEX exposure | Medium term (2-4 years) |

| Structural Price Competition and Margin Compression | -0.1% | National | Medium term (2-4 years) |

| Fragmented Multi-Procurement Models Restricting Service Innovation | -0.1% | National, higher prevalence in public sector | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Tight Labor Force Driving Wage Inflation

The Belgium integrated facility management market is facing a labour shortage that limits service scalability and pushes cost pressure directly into contract economics. The PROCOS Group FM Trend Report 2025 identified labour scarcity as a major issue and noted that current education pathways are not producing enough professionals with the digital, data, and sustainability skills required by modern IFM delivery. This shortfall is especially visible in technical roles such as BACS operators, energy performance engineers, and predictive maintenance specialists, where demand is rising at the same time as the compliance cycle is widening. Wage inflation is affecting both old and new contracts, because providers are carrying lower-priced multi-year agreements signed before current wage levels while also needing to submit higher bids on new tenders. ISS Belgium’s launch of the MyWork@ISS platform in January 2025 showed that providers are trying to use digital workforce management to improve visibility and productivity and reduce part of that pressure. Those efficiency gains have helped, but they have not fully absorbed sector-wide labour cost inflation, which keeps labour availability as the clearest near-term restraint on margin performance in the Belgium integrated facility management market.

Cost Uncertainty and Corporate CAPEX Constraints

Belgian building owners are facing overlapping compliance costs tied to EPC NR, BACS, and future renovation obligations, and that is tightening the budget space available for discretionary IFM upgrades. Many organizations must plan BACS installation, HVAC modernization, and EPC-driven improvements within compressed regulatory windows, which creates direct competition for capital across the same building portfolio. Profacility’s December 2025 review highlighted that older assets with basic technical systems face the highest upgrade burden because they need broader intervention to meet automated monitoring requirements. Uncertainty around energy prices and materials is also making long-term contract pricing harder to settle, especially when providers resist carrying escalation risk and buyers resist open price-adjustment clauses. This tension is strongest in hard FM arrangements that include performance guarantees, because both parties must define who absorbs cost changes over a multi-year period. The Belgium integrated facility management market therefore continues to face slower procurement cycles and more complex negotiations where capital planning and FM contract timing do not align cleanly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Facility Management Compliance Cycle Elevates Technical Services

Soft Facility Management (FM) services held 64.61% of the Belgium integrated facility management market (IFM) share in 2025, which reflected the steady and repeated demand for cleaning, catering, office support, and security across occupied buildings. That demand stayed resilient because occupier-facing services remain necessary even when office attendance varies by day or by site. Cleaning has also become more specialized within the Belgium IFM market, with ISS Belgium adopting Tersano ozone-water-based cleaning in April 2024 to remove chemical products from selected accounts and respond to both regulatory and health priorities. By June 2025, ISS had also deployed intelligent cleaning robots at Belgian sites, which showed that labour-saving automation is moving from pilot use into practical service delivery. Security and office support models are adjusting to hybrid occupancy as clients move away from fixed staffing patterns and toward service levels that track actual building use.

Catering is also changing, and ISS Belgium’s February 2025 partnership with Ecotarian introduced CO2 scoring for meal options in company restaurants, which aligned with the sustainability reporting needs of corporate clients. ISO 41001 is being referenced more frequently in Belgian enterprise RFPs, which is reinforcing a common baseline for service quality across soft and hard delivery requirements. Hard FM services are the fastest-growing service category, and the Belgium IFM market size for hard FM services is projected to expand at a 3.36% CAGR through 2031. The main reason is the widening compliance cycle around BACS, because large non-residential buildings had to operate those systems continuously by the end of 2025, and Brussels-based buildings were already subject to earlier compliance timing from January 1, 2025. Providers are responding by repositioning technical maintenance as a continuous performance service built around monitoring, fault detection, and predictive action, a direction also visible in VINCI Facilities Belgium, Coor Belgium, and Sweco Belgium’s MPC-led HVAC optimization work.

By End-User: Commercial Growth Driven by Compliance and Talent Competition

Industrial and manufacturing accounted for 31.52% of the Belgium IFM market share in 2025, supported by the intensity and continuity of service needs in production settings that require 24/7 asset oversight, safety control, and environmental monitoring. This part of the Belgium IFM market remains especially important in pharma, biotech, and heavy manufacturing clusters where uptime, controlled environments, and technical maintenance standards are critical. Belgium’s pharma and biotech activity, especially around Antwerp, creates strong demand for HVAC servicing, clean-room management, and specialized monitoring under GMP conditions. Coor Belgium’s positioning around industrial services and ISS’s dedicated focus on pharma and biotech show how deeply service models must be tailored for these clients. Healthcare is smaller in revenue terms, but it is developing into a steadier pipeline for integrated contracts as property ownership consolidates and specialized care assets expand.

Aedifica’s March 2026 move to secure 79.57% of Cofinimmo’s shares pointed to a larger healthcare property platform that can support recurring FM demand across a substantial care estate. Government and public infrastructure contracts add stability to the Belgium IFM market, although procurement cycles remain slow and often reduce flexibility once service requirements change. Commercial end-users are the fastest-growing category, and the Belgium IFM market size for commercial end-users is projected to rise at a 3.49% CAGR through 2031. Offices, retail assets, and mixed-use properties are carrying the strongest exposure to EPC NR, workplace redesign, and ESG requirements, which is pushing more owners toward professional outsourcing rather than in-house coordination. That same commercial shift is tied to talent competition, because employers are investing in workplace hospitality, air quality, ergonomic environments, and better catering to make the office more attractive, a priority that PROCOS identified directly in its 2025 trend work on employee well-being.

Geography Analysis

The Belgium integrated facility management market size was USD 1.23 billion in 2025, and that demand was distributed across Flanders, Wallonia, and the Brussels-Capital Region with clear differences in regulatory timing, asset mix, and procurement behaviour. Brussels remained the center of commercial and government demand because it hosts EU institutions, NATO headquarters, and a dense base of multinational corporate offices that require complex multi-site service delivery. This concentration supports steady soft FM demand and favours operators that can manage multilingual, high-compliance environments across multiple occupier profiles. Brussels also moved earlier on building automation, because large non-residential buildings in the region were required to operate BACS from January 1, 2025, which gave buyers and providers in the capital an earlier technical transition cycle than those in Flanders. The Belgium integrated facility management market therefore shows regional differences not only in demand scale, but also in the timing of hard FM service complexity.

Flanders carries the strongest industrial FM profile within the Belgium integrated facility management market, supported by chemicals, pharma, food processing, logistics, and manufacturing activity around Antwerp and Ghent. EPC NR coverage for all non-residential buildings from January 2026 and the future BACS threshold reduction to 70 kW by 2029 mean Flanders will continue to generate a broad stream of technical maintenance, monitoring, and retrofit coordination work. Wallonia presents a different demand pattern, with lower outsourcing penetration, a larger share of public-sector buildings, and an industrial base that is moving through structural transition. That mix delays part of the compliance response, but it can also extend the need for hard FM over a longer period because older building stock often requires deeper intervention once upgrades begin.

BELFA identified sustainability as the most influential factor for the Belgian FM sector at present and in the 2026 outlook, and that priority runs across all three regions even when the immediate trigger differs. The PROCOS Group FM Trend Report 2025 also noted that outsourcing penetration slipped slightly in 2024, which suggested some organizations were temporarily building internal capability before returning to the outsourcing market at a higher maturity level. That pattern appears more visible in Wallonia’s institutional and public segments than in Flanders’ corporate clusters. Cross-border workforce mobility and the concentration of multinational headquarters in Brussels and the Flemish Diamond also mean that many Belgian contracts are managed within broader European frameworks, as shown by the VELUX mobilization that reached Belgium from January 1, 2026, under a global agreement signed in July 2025. The newly founded Belgian Green Building Council is also starting to shape circularity and lifecycle assessment practices in the built environment, which is likely to bring more circular FM criteria into procurement specifications over time.

Competitive Landscape

The Belgium integrated facility management market is moderately concentrated, with international operators such as Sodexo, ISS, CBRE GWS, Apleona, and VINCI Facilities holding strong positions through integrated service scope, cross-border account management, and digital operating platforms. Domestic and regional specialists such as Facilicom Solutions, Coor Belgium, Multi Masters Group, and ATALIAN Global Services still compete effectively in service-specific mandates and regionally bounded contracts where local responsiveness matters. The leading players are strengthening their positions by internalizing specialist delivery rather than relying on fragmented subcontracting models. ISS Belgium’s March 2025 acquisitions of Bluebridge Services and Vinca Services illustrated this clearly, because the deals expanded in-house technical and landscaping capacity and improved control over integrated account delivery. Apleona’s move in March 2026 to create a fully independent Belgian organization also showed that larger European groups still see Belgium as a market that justifies dedicated leadership, local account structure, and direct go-to-market investment.

Technology is becoming the sharpest point of competition in the Belgium integrated facility management market because clients increasingly compare providers on analytics, reporting, monitoring, and outcome visibility rather than on labour deployment alone. CBRE Belgium’s CORE model, ISS workplace analytics capabilities, and Sweco Belgium’s use of digital twins and model predictive control all point to a market where technical and data-led differentiation is gaining weight in enterprise RFPs. There is also open space in the mid-market, where buyers face regulatory pressure from EPC NR, BACS, and NIS2 but often lack the scale needed for a classic full IFM contract at the start. Providers that can begin with compliance-heavy hard FM and then broaden into integrated delivery are likely to win this client group more effectively than operators that insist on full-scale onboarding from day 1.

A second competitive shift is coming from software-native platforms such as ALT-F1, Clicx, and fixform, which are separating FM information systems and asset intelligence from physical service delivery and putting pressure on incumbents to build or acquire stronger digital layers. Belgium’s early implementation of NIS2 has added another screening layer, because providers with CyberFundamentals or ISO 27001 credentials are better placed to pass supply-chain audits for the 2,410 Belgian organizations operating under those obligations. That is raising the vendor qualification threshold before contract award, especially in enterprise and public-sector settings where cybersecurity risk is now being evaluated alongside service capability. Smaller domestic firms can still compete in selected scopes, but those without visible digital and compliance credentials are likely to find fewer opportunities in the most demanding parts of the Belgium integrated facility management market.

Belgium Integrated Facility Management Industry Leaders

ISS Facility Services NV/SA

Sodexo S.A.

ATALIAN Global Services Belgium NV

VINCI Facilities Belgium

CBRE Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: BESIX Group reported solid financial results for 2025, including increased revenues, and published its 2025 Activity & ESG Report. BESIX's smart building and asset management division, which integrates IoT sensors, digital twins via its Neanex partnership, and a smart building collaboration with Proximus, positions the group as a growing technical FM capability across Belgium's industrial and infrastructure segments.

- March 2026: Apleona established a new leadership team for its Benelux operations, creating fully independent country organizations for Belgium, the Netherlands, and Luxembourg. The structural separation enables Apleona Belgium to compete for Belgian enterprise and public-sector IFM contracts with dedicated local account management, accelerating the company's growth ambition in the market.

- March 2026: Aedifica secured 79.57% of Cofinimmo's shares through an exchange offer approved by the Belgian Competition Authority and the Financial Services and Markets Authority, paving the way for a full merger to create a leading European healthcare real estate investment trust. The combined portfolio of 615+ care properties across Belgium and six other countries will generate a significant pipeline of integrated FM contracts in Belgium's healthcare end-user segment.

- March 2026: ISS Belgium announced a partnership with the Belgian Olympic and Interfederal Committee to provide professional cleaning services in support of Team Belgium. The contract reinforces ISS's institutional and event-based soft FM delivery positioning in Belgium.

Belgium Integrated Facility Management Market Report Scope

The Belgium Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the size of the Belgium integrated facility management market by 2031?

The Belgium integrated facility management market is forecast to reach USD 1.43 billion by 2031, up from USD 1.23 billion in 2025, with growth supported by outsourcing, compliance demand, and workplace reconfiguration.

What is driving growth in facility management demand in Belgium?

The main growth factors are integrated service adoption for cost control, energy compliance needs tied to EPC NR and BACS, higher outsourcing interest among corporates, and hybrid workplace redesign.

Which service category leads revenue in Belgium?

Soft FM services led revenue with a 64.61% share in 2025 because cleaning, catering, security, and office support remain recurring occupier-facing needs across building portfolios.

Which end-user group is expanding fastest in Belgium?

Commercial end-users are projected to grow the fastest at a 3.49% CAGR through 2031, driven by office redesign, ESG reporting pressure, and building energy compliance needs.

Why is hard FM becoming more important in Belgium?

Hard FM services are projected to grow at a 3.36% CAGR through 2031 because BACS, EPC NR, and ongoing technical maintenance are pushing buyers toward continuous monitoring and performance-led maintenance models.

How competitive is the Belgium integrated facility management market?

The market is moderately concentrated, with large international operators holding strong positions, while regional specialists still compete in selected scopes where local execution and flexibility remain important.

Page last updated on: