Neem-Based Fertilizer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.05 Billion |

| Market Size (2031) | USD 1.66 Billion |

| Growth Rate (2026 - 2031) | 11.10% CAGR |

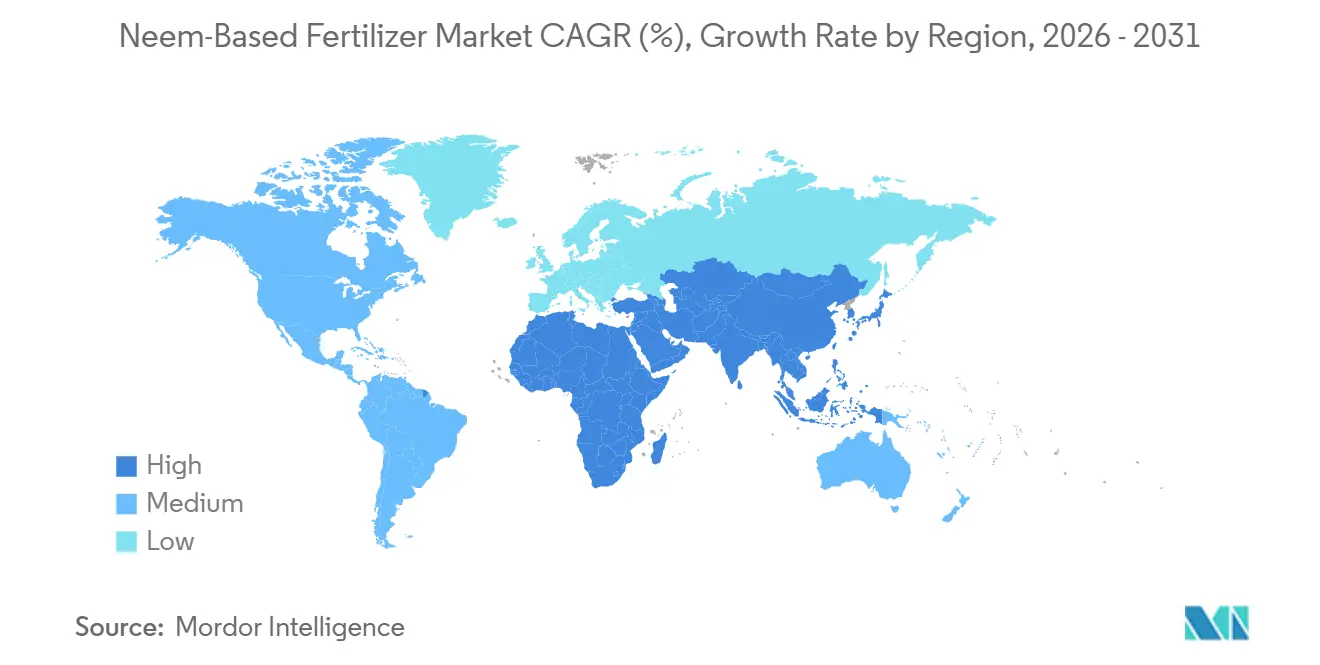

| Fastest Growing Market | Africa |

| Largest Market | Asia-Pacific |

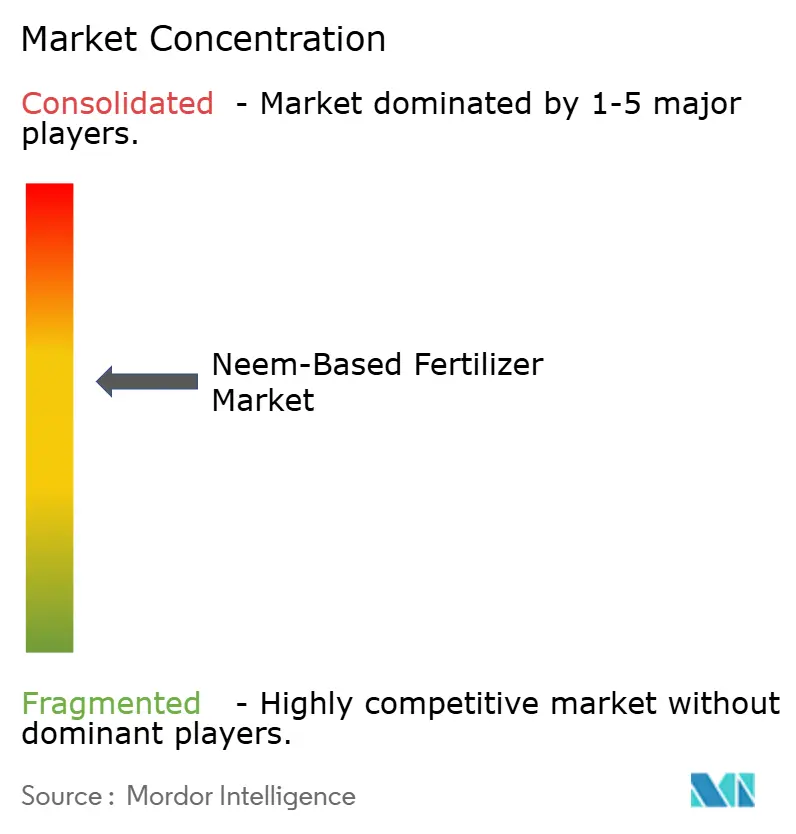

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neem-Based Fertilizer Market Analysis by Mordor Intelligence

The neem-based fertilizer market size was valued at USD 0.98 billion in 2025 and is projected to grow from USD 1.05 billion in 2026 to USD 1.66 billion by 2031, growing at a CAGR of 11.1% from 2026 to 2031. Mandatory neem-coating rules in India, rising restrictions on synthetic nitrification inhibitors in Europe, and surging demand for organic horticulture inputs worldwide are all accelerating growth. Asia-Pacific remains the largest regional consumer, while Africa records the fastest uptake as micro-dosing programs scale rural access. Liquid formulations gain momentum in precision fertigation, although granular products still dominate broad-acre cereal systems. Direct-to-farmer digital channels compress dealer margins and widen smallholder access to premium biological nutrient enhancers.

Key Report Takeaways

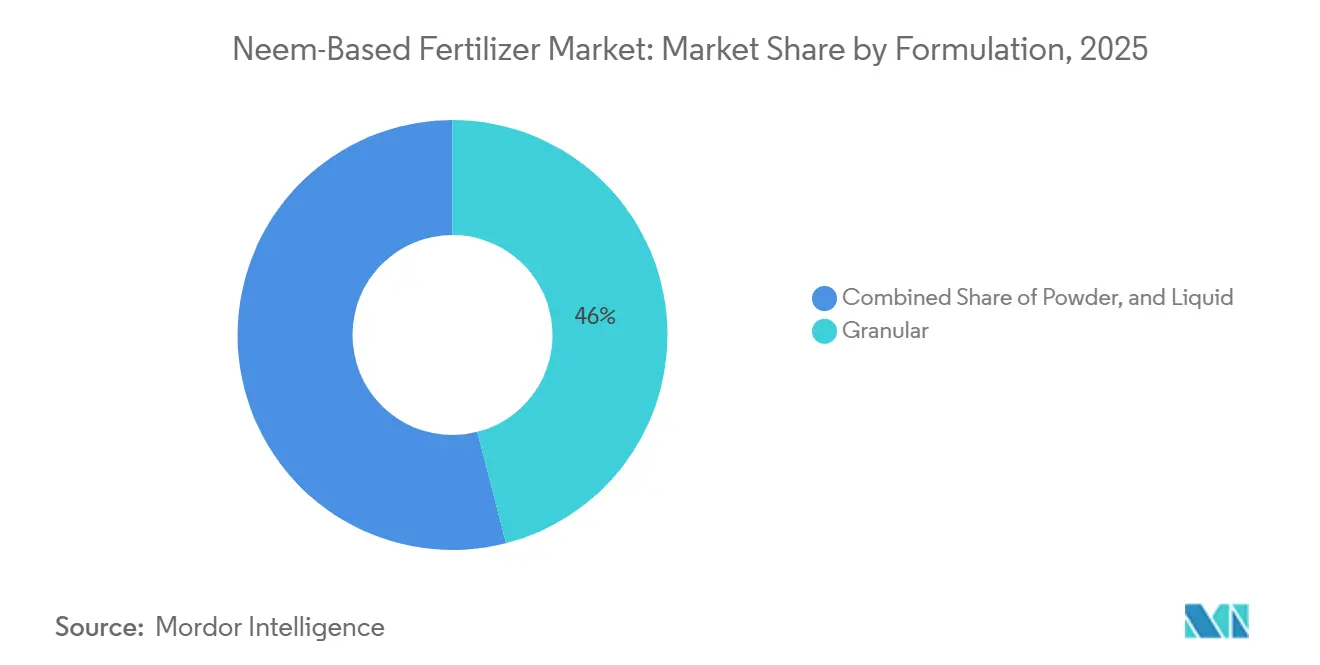

- By formulation, granular products held the largest 46% of the neem-based fertilizer market share in 2025, whereas liquid products are projected to advance at the fastest 13.0% CAGR through 2026-2031.

- By crop type, cereals and grains accounted for the 40% of the neem-based fertilizer market size in 2025, whereas fruits and vegetables are projected to advance at the fastest 11.5% CAGR during 2026-2031.

- By application method, soil application accounted for the largest 50% of the market share in 2025, yet fertigation is projected to advance at the fastest 13.0% CAGR to 2026-2031.

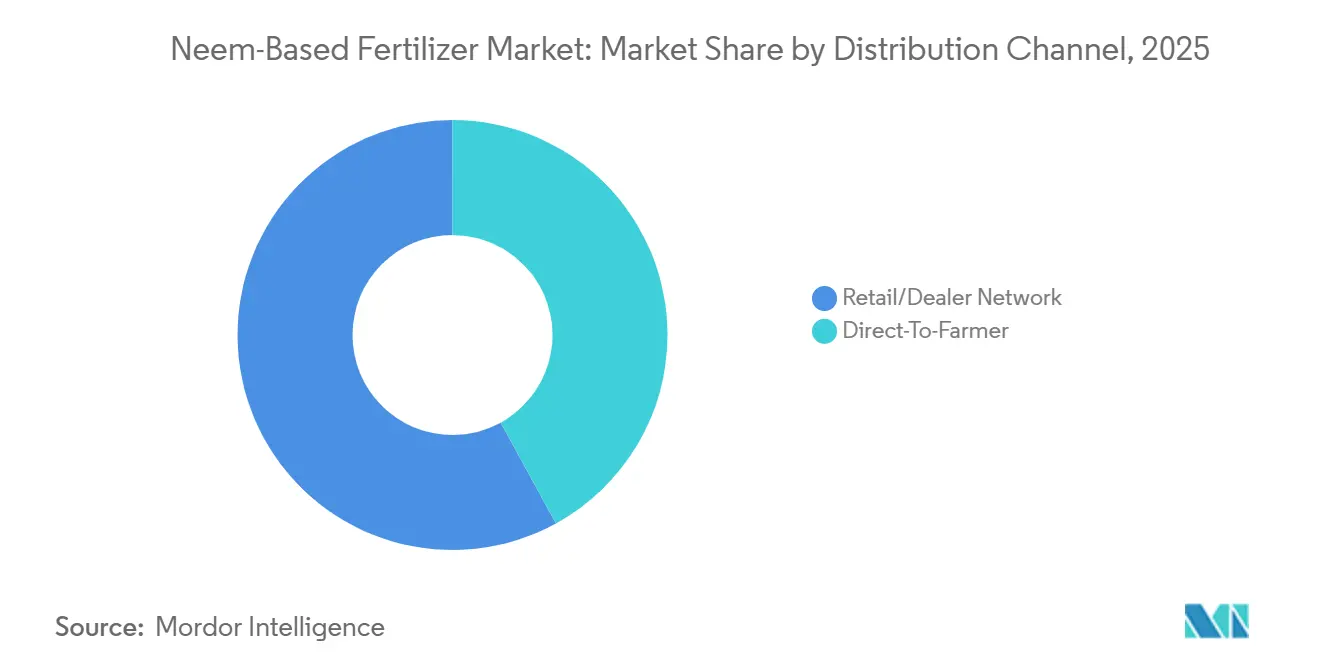

- By distribution channel, retail/dealer networks accounted for the largest 58% of the neem-based fertilizer market share in 2025, but direct-to-farmer models are projected to grow at the fastest 14.0% CAGR during 2026-2031.

- By geography, Asia-Pacific accounted for the largest 45.3% in 2025, and Africa is projected to grow at the fastest CAGR of 12.6% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Neem-Based Fertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government mandate on neem-coated urea for subsidized nitrogen fertilizers | +3.2% | India and the spillover to South Asia | Long term (≥ 4 years) |

| Growing demand for organic crop protection in high-value horticulture | +2.1% | Global export hubs | Medium term (2-4 years) |

| Rising restrictions on synthetic nitrification inhibitors in Europe | +1.8% | European Union | Medium term (2-4 years) |

| Increasing smallholder adoption via micro-dosing programs in Africa | +1.5% | Sub-Saharan Africa | Long term (≥ 4 years) |

| Commercial roll-out of controlled-release neem nanocarriers | +1.3% | Asia-Pacific and North America | Long term (≥ 4 years) |

| Blockchain-enabled provenance premiums for neem-fertilized produce | +0.9% | India, South America, and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Mandate on Neem-Coated Urea for Subsidized Nitrogen Fertilizers

India's emphasis on promoting neem-coated urea is driving demand for neem-derived agricultural inputs used in fertilizer production. According to the Press Information Bureau (PIB) of the Government of India, neem-coated urea enhances nitrogen-use efficiency by slowing the release of nitrogen in the soil. This allows farmers to achieve similar results while using approximately 10% less urea compared to conventional formulations[1]Source: Press Information Bureau (PIB), Government of India, “Empowering India's Farmers Through Strategic Fertilizer Policy,” pib.gov.in.. The policy mandating neem coating on subsidized urea remains active, sustaining significant consumption of neem-based coating materials within the fertilizer industry. As manufacturers continue producing neem-coated urea to meet agricultural needs, the demand for neem-derived inputs, including neem oil and azadirachtin, is expected to remain robust, supporting growth in the neem-based fertilizer market.

Growing Demand for Organic Crop Protection in High-Value Horticulture

Fruit and vegetable growers seeking premium export prices adopt neem inputs that comply with the United States Department of Agriculture National Organic Program and the European Union organic regulation. Biological fertilizers provide both nutrient delivery and secondary pest suppression, reducing the need for separate insecticide applications. UPL Limited launched the seaweed-based HYCOXA in 2025, signaling intensified competition within premium biological niches. Price premiums offset higher per-hectare input costs, especially for grapes, tomatoes, and peppers. Wider acceptance in protected agriculture strengthens year-round demand consistency.

Rising Restrictions on Synthetic Nitrification Inhibitors in Europe

The European Union Fertilizing Products Regulation 2019/1009 simplifies market entry for natural nitrification inhibitors such as neem[2]Source: European Parliament and Council, “Regulation (EU) 2019/1009 Laying Down Rules on the Making Available on the Market of EU Fertilizing Products,” Official Journal of the European Union, eur-lex.europa.eu. Denmark and the Netherlands issued agronomic guidance encouraging the use of natural substitutes to reduce nitrous oxide emissions and groundwater contamination. Alignment with the Farm to Fork nutrient-loss reduction target bolsters farmer adoption. Compliance with the Corporate Sustainability Reporting Directive pushes food companies to audit fertilizer footprints, catalyzing input substitution. Early adopters document yield stability, creating reference protocols for mainstream cereal growers.

Increasing Smallholder Adoption via Micro-Dosing Programs in Africa

Alliance for a Green Revolution in Africa projects distribute neem-coated urea sachets sized for single planting holes, cutting upfront cash outlays. Trials by the International Crops Research Institute for the Semi-Arid Tropics reported 20%-40% yield gains on maize and sorghum fields averaging one hectare[3]Source: Brahima Tabo et al., “Fertilizer Microdosing for the Prosperity of Smallholder Farmers in the Sahel,” International Crops Research Institute for the Semi-Arid Tropics, oar.icrisat.org. Lightweight packs remove transport constraints for rural agro-dealers lacking bulk storage. Mobile-money platforms streamline payments and data capture, enabling field-level performance tracking. As donor funding aligns with climate-smart agriculture goals, micro-dosing is scaling from pilot to national programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile supply of azadirachtin feedstock due to climate-sensitive neem yields | -1.4% | India and sub-Saharan Africa | Short term (≤ 2 years) |

| Limited agronomic extension support outside South Asia | -1.1% | Africa and South America | Medium term (2-4 years) |

| Competing cost-effective bio-fertilizer blends with seaweed extracts | -0.8% | Global premium segments | Medium term (2-4 years) |

| Slow registration timelines for biostimulants in South America | -0.6% | Brazil and Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Supply of Azadirachtin Feedstock Due to Climate-Sensitive Neem Yields

The growth of the neem-based fertilizer market is limited by the inconsistent availability of neem seeds, which are the primary source of azadirachtin used in neem-based agricultural products. The flowering and fruiting of neem trees are heavily influenced by seasonal rainfall and climatic conditions, making the feedstock supply susceptible to droughts, irregular monsoons, and extreme weather events. Variations in seed availability can disrupt raw material procurement, raise extraction and processing costs, and pose challenges in ensuring consistent product quality. These supply uncertainties hinder production scalability and profitability, restricting the overall expansion of the neem-based fertilizer market.

Limited Agronomic Extension Support Outside South Asia

Extension officers in Africa and South America receive limited training in biological slow-release solutions, leading smallholders to make risk-averse fertilizer choices. Published trial data often stay within research stations rather than reaching village demonstration plots. Private companies sponsor field schools, but coverage is uneven and concentrated in high-value zones. Without clear dosage and timing guidelines, farmers over- or under-apply neem products, eroding confidence in efficacy. Strengthening public-private knowledge partnerships will be essential for sustained adoption growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation: Liquid Fertigation Gains on Granular Incumbents

Granular products commanded the largest 46% share of the neem-based fertilizer market in 2025 because farmers can apply them with existing broadcast spreaders and seed drills. The format stores well in humid monsoon zones and faces minimal caking risk during warehouse storage. Granular sales remain strong in rice, wheat, and maize systems that dominate Asian and African acreage. Coating technology innovations improve granule integrity, limiting azadirachtin loss during handling. Established dealer networks keep granular shelves stocked in rural outlets, reinforcing farmer familiarity.

Liquid formulations are advancing at the fastest 13.0% CAGR through 2031 as drip irrigation widens across protected horticulture and water-scarce regions. Liquids integrate seamlessly with automated nutrient injection, allowing precise split applications that match crop nitrogen uptake curves. Growers of tomatoes, cucumbers, and bell peppers value the lower labor requirement compared with manual broadcasting. Manufacturers invest in emulsification techniques that stabilize azadirachtin in concentrate form, extending shelf life. Rising fertigation infrastructure investment in the Middle East and Southern Europe further expands the addressable base for liquid products.

By Crop Type: Fruits and Vegetables Outpace Cereals and Grains

Cereals and grains retained the largest 40% of the neem-based fertilizer market size in 2025, as India’s mandatory policy targets urea, a cereal input staple. Broadcast application during rice puddling and wheat top-dressing offers straightforward integration. Government procurement programs channel coated urea to public distribution outlets, ensuring consistent offtake. Yield response data collected over a decade reinforces farmer confidence, sustaining repeat purchase cycles. The segment will keep adding absolute volume even as its proportional share tilts downward.

Fruits and vegetables represent the fastest-expanding segment, with a 11.5% CAGR during 2026-2031, as organic-certified production grows for export consumers. Protected cultivation requires tight nutrient management, and neem inputs double as mild pest suppressants, reducing chemical residue risk. Price premiums on grapes, berries, and leafy greens justify higher per-hectare spending on biological fertilizers. Traceability programs that record neem usage help growers access blockchain-verified supply chains. Rising adoption in South American avocado and Asian mango orchards further accelerates demand.

By Application Method: Fertigation Scales Rapidly

Soil incorporation maintained the largest 50% share of the neem-based fertilizer market in 2025 because cereals dominate planted area in low-irrigation regions. Farmers blend neem cake or coated urea into seedbeds before sowing, leveraging existing manual or tractor-drawn implements. The method requires no new capital equipment and delivers a season-long nitrogen release profile. Government extension bulletins in India and Kenya provide dosage charts that support this traditional practice. Soil incorporation, therefore, continues to underpin baseline demand.

Fertigation is the fastest-growing method, with a 13.0% CAGR to 2031, as drip lines spread across horticulture, vineyard, and greenhouse operations. Pressurized lines deliver uniform nutrient solution, cutting leaching losses in sandy or saline soils. Setup costs decline as manufacturers localize emitter production and governments subsidize water-saving technologies. Neem liquids or soluble powder blends dissolve readily in stock tanks and remain stable in dilution. Growers measure leaf chlorophyll with mobile apps to fine-tune injection schedules, reinforcing uptake of fertigation-ready neem products.

By Distribution Channel: Digital Direct-to-Farmer Models Disrupt Retail

Conventional retail and dealer outlets held the largest 58% share of the neem-based fertilizer market in 2025 through established storefronts that offer seasonal credit. Dealers bundle fertilizers, seeds, and pesticides, creating one-stop shops. Many also run demonstration plots that build farmer trust in new formulations. However, inventory holding costs and margin stacking raise growers' final prices. As rural smartphones proliferate, farmers increasingly benchmark prices online, pressuring dealer mark-ups.

Direct-to-farmer channels are scaling at the fastest 14.0% CAGR during 2026-2031. Coromandel International and Indian Farmers Fertilizer Cooperative field mobile apps that provide weather alerts, dose calculators, and click-to-order capability. Digital logistics start-ups consolidate orders and deliver from regional warehouses, shortening lead times. Traceability requirements from produce buyers motivate direct procurement, enabling manufacturers to certify input quality. Cooperative bulk-purchase models lower per-unit costs for smallholders, encouraging wider adoption of premium neem formulations.

Geography Analysis

Asia-Pacific is the largest geography, accounting for 45.3% of the neem-based fertilizer market share in 2025, driven by India’s full urea-coating mandate, which locks in annual demand for 25 million metric tons of production. China’s push for organic certification in greenhouse vegetables and fruit orchards adds incremental offtake. Japan and South Korea, although smaller, command premium pricing on residue-conscious supermarket channels. ICL Group’s 2026 specialty fertilizer plant in Maharashtra underpins the regional supply of water-soluble neem blends. Ongoing subsidies for micro-irrigation in India stimulate the uptake of liquid formulations.

Africa posts the fastest 12.6% CAGR forecast for 2026-2031 as donor-sponsored micro-dosing programs scale from pilot to national coverage in Kenya, Tanzania, and Nigeria. Local neem seed collection initiatives expand raw-material supply and create rural employment. Commercial estates in South Africa adopt neem inputs in citrus and grape orchards to secure European import clearances. North African growers adopt controlled-release products to manage salinity stress under deficit irrigation. Mobile-money ecosystems ease last-mile payment frictions, unlocking demand in remote villages.

Europe and North America grow steadily on the back of organic produce premiums and regulatory limits on synthetic inhibitors. The European Union Fertilizing Products Regulation provides a harmonized route to market, lowering administrative hurdles for Indian and Israeli suppliers. Denmark, the Netherlands, and Germany showcase national nutrient-loss reduction targets that nudge adoption in conventional cereal farms. United States organic acreage in California and Florida absorbs liquid neem concentrates for high-value berries and leafy greens. Canada’s greenhouse vegetable cluster increasingly uses neem liquids in fertigation to meet supermarket residue specifications.

Competitive Landscape

The neem-based fertilizer market remains moderately concentrated, with the top five suppliers accounting for the majority share in 2025. Coromandel International Limited deepened its technical reach by acquiring a 53% stake in NACL Industries in 2025 for Rs 820 crore (USD 98 million). Indian Farmers Fertilizer Cooperative Limited and National Fertilizers Limited capitalize on captive urea plants that guarantee neem-coating volumes under the subsidy program. E.I.D. Parry (India) Limited leverages integrated sugar and bio-products lines to secure raw neem seed supply. Godrej Agrovet Limited invests in nanocarrier patents to compete in precision agriculture niches.

Multinational entrants widen biological portfolios through mergers. ICL Group Ltd. opened a 7-acre specialty plant in Maharashtra in 2026 and acquired microbiome specialist Lavie Bio in 2025 for an undisclosed amount to blend microbial strains with neem extracts. UPL Limited allocated EUR 990 million (USD 1.04 billion) to research spending in fiscal 2025 and launched HYCOXA to compete in the nitrogen-efficiency segment. BASF SE acquired AgBiTech in 2026 to bolster viral biocontrol assets that pair with neem nutrient programs in integrated solutions. HGS BioScience snapped up Pharmgrade in 2026 to add microbial capabilities and create a one-stop soil-health platform.

Regional specialists flourish in raw-material extraction and contract manufacturing. Fortune Biotech operates United States Environmental Protection Agency and European Union-approved azadirachtin lines that supply formulators worldwide. Ozone Biotech sells cold-pressed neem oil to niche organic fertilizer blenders. Kan Biosys expanded bio-nutrient powders in 2025, aimed at Indian vegetable smallholders lacking fertigation equipment. Agro-dealer loyalty and localized crop advisory services remain decisive for market share in fragmented rural catchments. Fast digitalization opens space for agile newcomers to bypass legacy distribution and capture value directly from growers.

Neem-Based Fertilizer Industry Leaders

Coromandel International Limited

Indian Farmers Fertiliser Cooperative Limited

National Fertilizers Limited

E.I.D. Parry (India) Limited

Godrej Agrovet Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: AgroPlantae Inc. completed the acquisition of Kemin Industries' crop technologies portfolio, including neem-adjacent botanical biopesticides. This move broadens AgroPlantae’s biological offerings, supporting integrated solutions that pair neem-based fertilizers with complementary pest-management actives, which is likely to accelerate product bundling opportunities and lift overall market demand.

- March 2026: ICL Group inaugurated a specialty fertilizer facility in Maharashtra, India, dedicated to water-soluble and neem-blend products. The plant boosts regional supply capacity and shortens lead times for precision fertigation solutions, helping drive adoption of liquid neem formulations and supporting market growth in Asia-Pacific’s high-value horticulture segments.

- May 2024: Coromandel International launched a neem-coated bio plant and soil health promoter designed to enhance soil fertility and support sustainable crop nutrition practices. This neem-based product aims to improve nutrient availability, encourage beneficial soil microbial activity, and support long-term soil health management.

Global Neem-Based Fertilizer Market Report Scope

Neem-based fertilizers are sustainable and organic soil conditioners that serve as nutrient sources. They are derived from products of the Azadirachta indica (neem) tree, primarily neem cake (de-oiled residue) and kernel powder.

The Neem Based Fertilizer Market Report is Segmented by Formulation (Powder, Granular, and Liquid), by Crop Type (Cereals and Grains, Oilseeds and Pulses, and More), by Application Method (Soil Application, Foliar Spray, and More), by Distribution Channel (Direct -To-Farmer and Retail/Dealer Network), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Powder |

| Granular |

| Liquid |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Other Crops |

| Soil Application |

| Foliar Spray |

| Fertigation |

| Seed Treatment |

| Direct-To-Farmer |

| Retail/Dealer Network |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Formulation | Powder | |

| Granular | ||

| Liquid | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Other Crops | ||

| By Application Method | Soil Application | |

| Foliar Spray | ||

| Fertigation | ||

| Seed Treatment | ||

| By Distribution Channel | Direct-To-Farmer | |

| Retail/Dealer Network | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the neem-based fertilizer market be by 2031?

The neem-based fertilizer market size is projected to reach USD 1.66 billion by 2031.

Which region is expanding the quickest in neem inputs?

Africa records the fastest 12.6% CAGR during 2026-2031, driven by donor-funded micro-dosing and soil-health initiatives.

What formulation type grows the fastest?

Liquid products advance at a 13.0% CAGR through 2031 as fertigation infrastructure spreads in horticulture.

What drives adoption in Europe?

Rising restrictions on synthetic nitrification inhibitors, along with the European Union Fertilizing Products Regulation, are encouraging the use of natural alternatives.

How do neem nanocarriers improve efficiency?

Controlled-release nanocarriers synchronize nutrient release with crop uptake, cutting total nitrogen use by up to 15% in field trials.

Page last updated on: