United States Biodegradable Controlled-Release Fertilizer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

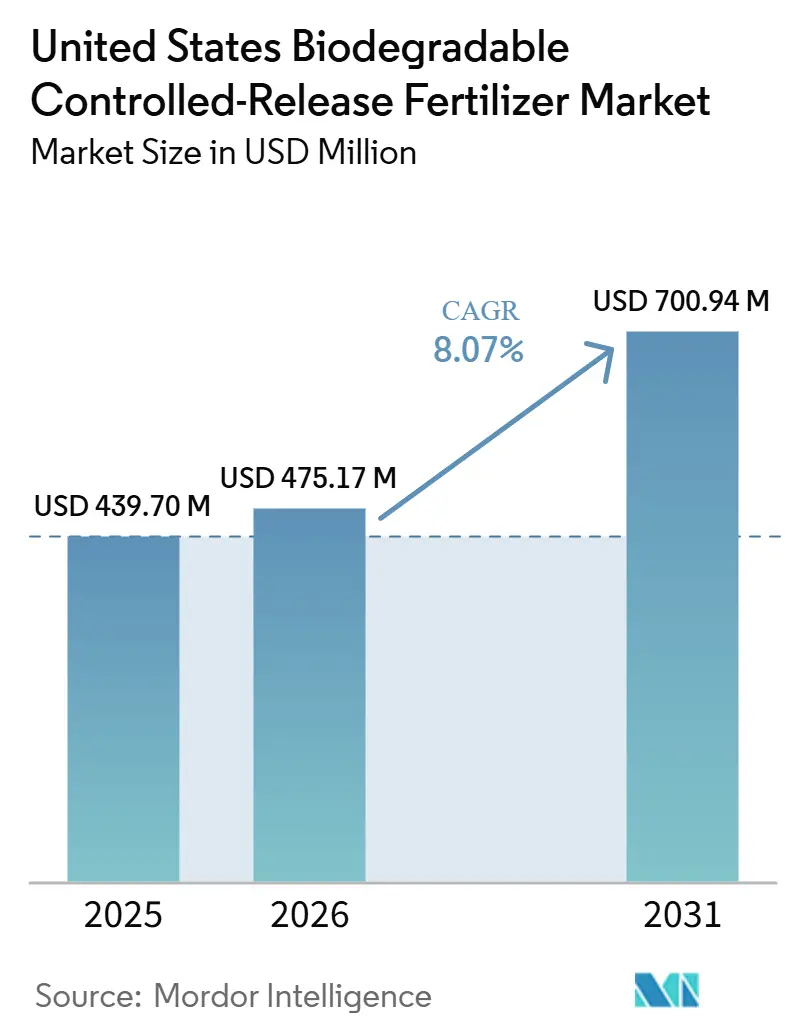

| Base Year Market Size (2025) | USD 439.70 Million |

| Market Size (2026) | USD 475.17 Million |

| Market Size (2031) | USD 700.94 Million |

| Growth Rate (2026 - 2031) | 8.07% CAGR |

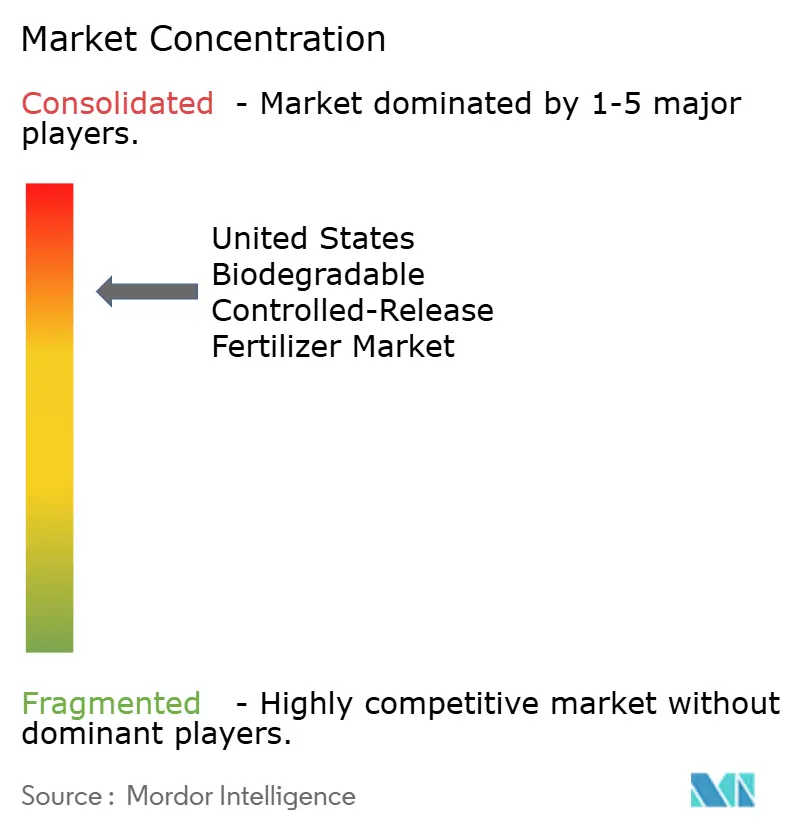

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Biodegradable Controlled-Release Fertilizer Market Analysis by Mordor Intelligence

The United States biodegradable controlled-release fertilizer market size was valued at USD 439.7 million in 2025 and is estimated to grow from USD 475.2 million in 2026 to reach USD 700.9 million by 2031, at a CAGR of 8.1% during the forecast period (2026-2031). The market is gaining support from tighter nutrient-loss controls, wider use of precision application systems, and a steady shift toward products that better match nutrient release with crop uptake. Federal conservation funding is also helping the category, as the United States Department of Agriculture (USDA) has dedicated funding in fiscal year 2026 through the Environmental Quality Incentives Program (EQIP) and the Conservation Stewardship Program (CSP) under its regenerative pilot program, which improves the economics for growers adopting nitrogen-efficient practices[1]Source: USDA, “USDA Launches New Regenerative Pilot Program to Lower Farmer Production Costs and Advance MAHA Agenda,” USDA, usda.gov. Supplier competition is increasingly shaped by coating technology, product certification, and the ability to position biodegradable offerings ahead of stricter environmental scrutiny around conventional polymer residues. Demand is also broadening from specialty horticulture into larger-acreage grain systems as growers seek fewer application passes, improved nutrient retention, and cleaner compliance outcomes under state and local runoff rules. The market still faces pricing pressure from volatile fertilizer inputs, yet ongoing patent activity, field validation, and policy support are steadily improving its commercial position.

Key Report Takeaways

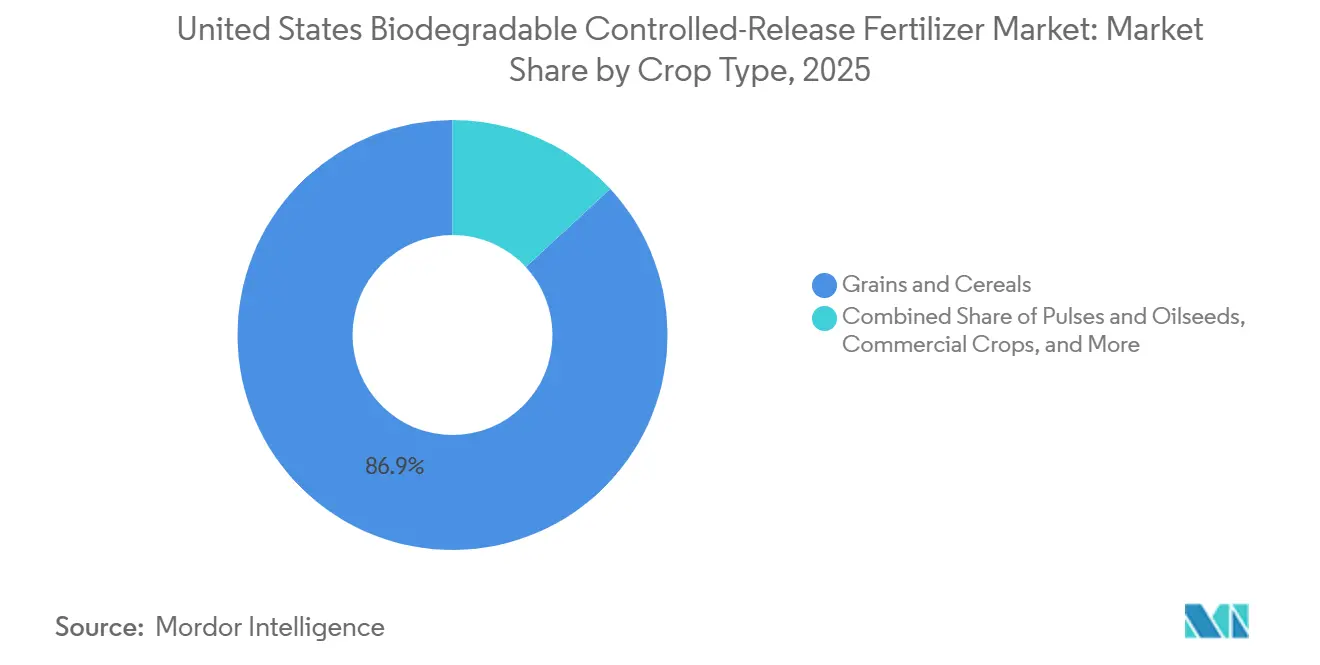

- By crop type, grains and cereals accounted for 86.9% of the United States biodegradable controlled-release fertilizer market size in 2025, while fruits and vegetables are advancing at a 12.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Biodegradable Controlled-Release Fertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising precision agriculture adoption in row crop farming | +1.8% | National, with strongest gains in Iowa, Illinois, Indiana, and Nebraska | Medium term (2-4 years) |

| State runoff compliance, tightening nutrient loss controls | +1.6% | Mid-Atlantic states, Florida, Iowa, Minnesota, and adjacent regions | Short term (≤ 2 years) |

| Biodegradable coating commercialization reduces price barriers | +1.3% | National, with early development activity in Alabama and New Jersey | Medium term (2-4 years) |

| Sun belt turf and ornamental demand is expanding premium fertilizer usage | +1.2% | Florida, Texas, Georgia, Arizona, and California | Short term (≤ 2 years) |

| USDA climate-smart incentives supporting nitrogen efficiency | +0.9% | National | Medium term (2-4 years) |

| Municipal and institutional sustainability procurement is in increasing demand | +0.7% | Florida, California, and Mid-Atlantic urban corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Precision Agriculture Adoption in Row Crop Farming

Variable-rate systems and sensor-guided nutrient placement are making the United States biodegradable controlled-release fertilizer market increasingly relevant to mainstream grain farming. Adoption of precision technologies has expanded significantly across major commodity crops, creating a strong installed base that supports data-driven nutrient management. Controlled-release fertilizers align well with single-pass application strategies, helping reduce overlap, minimize waste, and improve timing accuracy. This alignment is particularly beneficial in no-till and reduced-pass systems, where growers seek season-long nutrient performance without repeated field applications. Precision guidance also helps limit fertilizer loss at field edges, where inefficiencies are typically highest, making the value of controlled-release products easier to justify even in well-managed operations. As precision agriculture becomes more widely adopted in corn and soybean systems, retailers are increasingly integrating controlled-release fertilizers into standard fertility programs rather than positioning them as niche or specialty solutions.

State Runoff Compliance Tightening Nutrient Loss Controls

State nutrient-loss rules are turning the United States biodegradable controlled-release fertilizer market into a more compliance-linked category rather than a purely discretionary agronomic upgrade. Iowa updated its Nutrient Reduction Strategy in February 2025, providing growers with a more formal framework for optimizing nitrogen decisions based on local conditions. Policy updates and state programs are providing clearer frameworks for optimizing nitrogen use, while incentive-based initiatives are improving the economic case for adopting efficiency-enhancing products. These measures are encouraging growers to align nutrient application practices with environmental performance standards. At the same time, continued pressure on watershed regions to meet nutrient reduction targets is reinforcing the need for solutions that limit leaching and runoff. Local regulations are further strengthening this trend by setting minimum requirements for slow-release nitrogen content in fertilizers used across agricultural and non-agricultural applications. While these policies do not mandate specific product types, they consistently favor higher nutrient-use efficiency and reduce reliance on conventional applications. As a result, regulatory tightening remains a key near-term driver supporting adoption in the United States biodegradable controlled-release fertilizer market.

Biodegradable Coating Commercialization Reduces Price Barriers

Commercial progress in biodegradable coatings is reducing one of the key barriers in the United States biodegradable controlled-release fertilizer market, particularly the cost premium associated with coated formulations. Advances in patent development and field validation are improving the viability of biodegradable coating technologies, while early commercialization efforts are demonstrating that these solutions can meet performance standards within established regulatory frameworks. Ongoing research is also addressing historical challenges related to release control and durability, making newer coating systems more consistent and reliable across different applications. In parallel, the exploration of alternative raw materials, including agro-industrial residues, is expanding the potential supply base and may, over time, reduce reliance on higher-cost synthetic inputs. As more of these innovations move from trial phases into commercial use, the market is anticipated to scale more effectively across a broader range of agricultural acreage.

Sun Belt Turf and Ornamental Demand is Expanding Premium Fertilizer Usage

The Sun Belt remains an important demand pocket for the United States biodegradable controlled-release fertilizer market because turf, ornamentals, and landscape maintenance can absorb premium products more easily than commodity row crops. Florida, Texas, Georgia, Arizona, and California support long growing seasons and frequent maintenance cycles, which favor slow, controlled nutrient release over multiple quick applications. The 2026 Georgia Sod Producers Inventory Survey found that 68% of producers planned to add acreage in 2026, and golf courses accounted for 19% of the anticipated sales, pointing to continued support from professional turf channels[2]Source: Urban Ag Council, “2026 Annual Georgia Sod Producers Inventory Survey,” Urban Ag Council, urbanagcouncil.com. Municipal runoff restrictions add another layer because professional landscapers must meet local nitrogen rules while maintaining visual quality and predictable treatment schedules. That requirement shifts product choice toward controlled-release formats even when homeowners are not the primary buyer. The segment also benefits from a service model that uses fewer passes and longer feeding intervals, helping labor planning for commercial applicators. This makes the Sun Belt an early commercial base for premium-coated products, while the United States biodegradable controlled-release fertilizer industry expands further into broadacre agriculture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium price gap versus conventional urea | -2.1% | National, with the strongest effect in the Corn Belt | Short term (≤ 2 years) |

| Imported resin and feedstock dependence | -1.3% | National, especially the Gulf Coast and Midwest supply hubs | Medium term (2-4 years) |

| Limited independent grower awareness in the corn belt | -0.9% | Iowa, Illinois, Indiana, Nebraska, and Ohio | Medium term (2-4 years) |

| Return on investment sensitivity under commodity price volatility | -0.8% | National, with the strongest effect in corn and soybean regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Price Gap Versus Conventional Urea

The biggest barrier in the United States biodegradable controlled-release fertilizer market remains the price premium compared with conventional urea. Rising nitrogen fertilizer costs, driven by supply disruptions and broader geopolitical uncertainties, have increased pressure on grower budgets and heightened sensitivity to higher input costs. This challenge is particularly pronounced in large-scale farming regions, where producers closely evaluate per-acre returns and benchmark all inputs against lower-cost commodity fertilizers. Although controlled-release products offer benefits such as improved efficiency, reduced nutrient loss, and fewer application passes, these advantages are not always reflected in simple upfront price comparisons. While incentive programs at the state and federal levels can help offset some of the cost difference, they do not fully eliminate the initial purchase barrier. As long as conventional fertilizers remain the more straightforward, low-cost option, price resistance is likely to continue limiting broader adoption of biodegradable controlled-release fertilizers in the United States.

Imported Resin and Feedstock Dependence

Imported resin and feedstock exposure remains a structural risk for the United States biodegradable controlled-release fertilizer market, as coated products depend on stable raw material supply and predictable processing costs. Volatility across the fertilizer value chain has shown how quickly disruptions can affect production, with fluctuations in key inputs such as sulfur influencing output decisions and tightening supply conditions. Broader uncertainty around global trade policies and export dynamics continues to impact input planning across North America. This challenge is more pronounced for biodegradable products, as many next-generation coating technologies are still transitioning from limited commercial scale to wider manufacturing adoption. Supply instability can increase the delivered cost of finished fertilizers and affect product availability during critical application windows. As a result, larger suppliers with stronger sourcing networks and inventory management capabilities hold a competitive advantage, while smaller producers face tighter operating margins. Until coating inputs are sourced more widely and at greater scale, feedstock dependence will remain a key constraint on the United States biodegradable controlled-release fertilizer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Grain-Driven Scale, Horticulture Powers the Growth Rate

Grains and cereals accounted for 86.9% of the market in 2025, which gave this segment the largest United States biodegradable controlled-release fertilizer market share by crop type. The segment’s scale is tied to the sheer acreage base of corn and the central role of nitrogen management in row-crop profitability and compliance. Even modest increases in the adoption of coated fertilizer across large crop areas can translate into significant overall volume growth. Research also indicates that controlled-release nitrogen fertilizers improve nutrient-use efficiency and yield performance in cereal crops, supporting broader adoption across grain systems. Pulses and oilseeds benefit from reduced application passes during tight planting windows, while commercial crops and turf applications provide more consistent use cases where timing and labor efficiency are critical.

Fruits and vegetables are projected to grow at a 12.0% CAGR through 2031, which makes them the fastest-growing crop segment in the United States biodegradable controlled-release fertilizer market. That growth reflects stronger per-acre economics in berries, citrus, tree nuts, and fresh vegetables, where the value of better nutrient timing is easier to monetize. The ability to better manage nutrient timing directly translates into improved crop quality and higher returns, making premium fertilizer solutions more economically viable for specialty growers. This segment also aligns closely with sustainability goals and efficient water use, increasing its appeal in professional horticulture. While grains remain dominant in scale, the higher growth rate in fruits and vegetables provides suppliers with a profitable pathway to expand biodegradable fertilizer adoption before wider penetration in row crops.

Geography Analysis

The Corn Belt remained the largest demand base within the United States biodegradable controlled-release fertilizer market in 2025 because corn acreage and nitrogen intensity continue to set the tone for commercial fertilizer volumes. Iowa, Illinois, Indiana, Ohio, and Nebraska are central to this position because row-crop acres there offer the largest scale opportunity for efficiency products that can reduce nutrient loss without requiring major changes in farm structure. Iowa’s February 2025 Nutrient Reduction Strategy update made nutrient optimization a clearer policy objective by embedding the N-FACT tool into official guidance[3]Source: Iowa Capital Dispatch, “Iowa Updates Its Strategy to Reduce Nutrient Runoff,” Iowa Capital Dispatch, iowacapitaldispatch.com. Policy support is also reinforcing this trend through clearer nutrient optimization frameworks and incentive-based programs tied to nitrogen-use efficiency. Even small shifts toward controlled-release adoption across these large acreages can generate substantial volume gains at the national level.

The Southeast and Sun Belt corridor represents the most dynamic regional pocket in the United States biodegradable controlled-release fertilizer market, supported by a diverse mix of turf, ornamentals, nursery crops, and increasing runoff management requirements. Favorable growing conditions and high visual performance standards in applications such as golf courses, sports turf, and managed landscapes make premium controlled-release products easier to adopt compared to commodity farming systems. Local regulations are further shaping demand by encouraging higher proportions of slow-release nitrogen, while steady expansion in professional turf segments continues to support consistent product usage.

The Pacific Coast is emerging as a strong specialty-crop outlet, with growth driven by fruits and vegetables where nutrient timing and application efficiency directly influence crop value. California is central to this trend due to its high-value crop mix, labor considerations, and emphasis on water-use efficiency, all of which favor fewer-pass nutrient programs with improved release control. The region also places greater emphasis on sustainability and procurement standards, creating a favorable environment for biodegradable formulations. As a result, the Pacific Coast serves as a key proving ground where premium products can scale through value-based adoption rather than cost competition alone.

Competitive Landscape

The United States biodegradable controlled-release fertilizer market remained concentrated in 2025, with the top 5 producers, Nutrien Ltd., ICL Group Ltd., Haifa Group, Grupa Azoty S.A. (COMPO EXPERT), and Florikan ESA LLC (Profile Products LLC), collectively holding significant market share. Competition is centered on coating technology, distribution reach, and the speed of biodegradable product commercialization. Nutrien benefits from a broad retail footprint and strong nitrogen positioning, and its early work on biodegradable coating credibility. The Mosaic Company’s Q1 2026 results also showed that scale still matters in this space, as raw material shocks, sulfur costs, and production decisions can affect downstream availability and pricing across fertilizer categories. That scale advantage makes the United States biodegradable controlled-release fertilizer market harder for smaller entrants to penetrate quickly.

Several recent moves show how market leaders are protecting or improving their position. ICL Group Ltd. secured the first EU-recognized biodegradability certification for eqo.x, giving it a clear first-mover advantage as regulatory attention on coating residues rises[4]Source: ICL Growing Solutions, “eqo.x Receives Official Certification for Biodegradable Coating,” ICL Growing Solutions, icl-growingsolutions.com. Yara International’s 2026 capital markets strategy also emphasized premium products, nutrient-use efficiency, and digital precision-farming tools, which support a broader shift toward value-added fertilizer systems.

White space remains in row-crop biodegradable products that can compete more directly on price and in institutional procurement channels where sustainability requirements matter more than commodity benchmarks. Kingenta’s July 2025 launch of its first overseas slow-release fertilizer model factory in the Netherlands shows that international producers are also building export-ready coated fertilizer capacity with future relevance for North America. Florikan ESA LLC remains important in horticulture because performance consistency and shelf-life behavior matter strongly in greenhouse and nursery channels. Overall, the leaders in the United States biodegradable controlled-release fertilizer market are the firms that can combine proven release performance, secure supply, and a credible path toward biodegradable compliance.

United States Biodegradable Controlled-Release Fertilizer Industry Leaders

Nutrien Ltd.

ICL Group Ltd.

Haifa Group

Grupa Azoty S.A. (COMPO EXPERT)

Florikan ESA LLC (Profile Products LLC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Scotts Miracle-Gro Company introduced a pesticide-free, slow-release Turf Builder product designed for safer use around homes. This supports the United States biodegradable controlled-release fertilizer market by aligning with rising consumer preference for environmentally safe and residue-free nutrient solutions, especially in turf and residential applications.

- January 2026: Yara International outlined its long-term strategy focused on premium fertilizers, improved nutrient-use efficiency, and digital precision farming tools. This drives the United States biodegradable controlled-release fertilizer market by reinforcing the shift toward efficiency-led, value-added fertilizer systems where controlled-release solutions fit naturally.

- July 2025: Kingenta Ecological Engineering Group established an overseas slow-release fertilizer production facility in the Netherlands to expand global reach. This relates to the United States biodegradable controlled-release fertilizer market by increasing global supply capacity and competitive pressure, which can accelerate technology diffusion and improve product availability in North America.

United States Biodegradable Controlled-Release Fertilizer Market Report Scope

Biodegradable controlled-release fertilizer is a type of fertilizer that releases nutrients gradually over time through a coating or matrix made from biodegradable materials. These coatings regulate nutrient availability in sync with plant uptake, improving nutrient-use efficiency while reducing losses from leaching, volatilization, or runoff.

The United States Biodegradable Control Released Fertilizer Market Report is Segmented by Crop Type (Grains and Cereals, Pulses and Oilseeds, Commercial Crops, Fruits and Vegetables, and Turfs and Ornamentals). The Market Forecasts are Provided in Terms of Value (USD) and Volume in (Metric Tons).

| Grains and Cereals |

| Pulses and Oilseeds |

| Commercial Crops |

| Fruits and Vegetables |

| Turf and Ornamentals |

| By Crop Type | Grains and Cereals |

| Pulses and Oilseeds | |

| Commercial Crops | |

| Fruits and Vegetables | |

| Turf and Ornamentals |

Key Questions Answered in the Report

What is the 2026 size of the United States biodegradable controlled-release fertilizer space?

It is valued at USD 475.17 million in 2026 and is forecast to reach USD 700.94 million by 2031 at an 8.07% CAGR.

Which crop group is growing the fastest through 2031?

Fruits and vegetables are projected to grow at a 12.0% CAGR through 2031 because premium crop economics make it easier to absorb higher input costs.

Why are growers considering controlled-release fertilizers more seriously now?

Tighter nutrient-loss rules, precision agriculture adoption, and USDA conservation support are making nitrogen efficiency a more practical purchase decision in 2026.

What is the biggest hurdle for wider adoption in row crops?

The main hurdle is the price gap versus conventional urea, especially in the Corn Belt, where growers closely track per-acre return and remain sensitive to fertilizer cost spikes.

Page last updated on: