Feed Fertilizer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

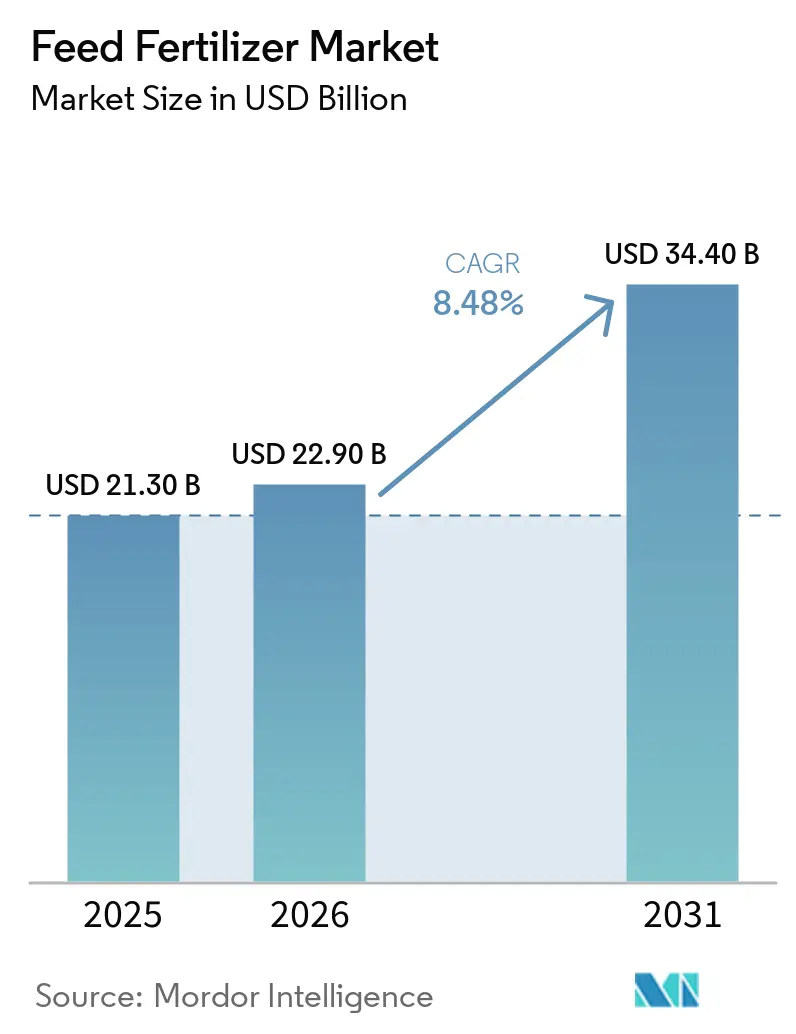

| Market Size (2026) | USD 22.90 Billion |

| Market Size (2031) | USD 34.40 Billion |

| Growth Rate (2026 - 2031) | 8.48% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Fertilizer Market Analysis by Mordor Intelligence

The feed fertilizer market size is projected to expand from USD 21.3 billion in 2025 and USD 22.9 billion in 2026 to USD 34.4 billion by 2031, registering a CAGR of 8.48% during 2026-2031. Nitrogen products remain the largest revenue contributor, but accelerating adoption of bio-based formulations and precision-dosing platforms is realigning competitive advantages. Strong government mandates on sustainable livestock productivity, the rapid scale-up of aquaculture, and emerging carbon-credit incentives underpin resilient medium-term demand. At the same time, heightened raw-material volatility and tightening residue limits urge producers to advance specialty nutrients rather than compete on undifferentiated volume. Supply-side shifts favor vertically integrated firms that control mining, manufacturing, and digital advisory services, insulating margins against commodity swings.

Key Report Takeaways

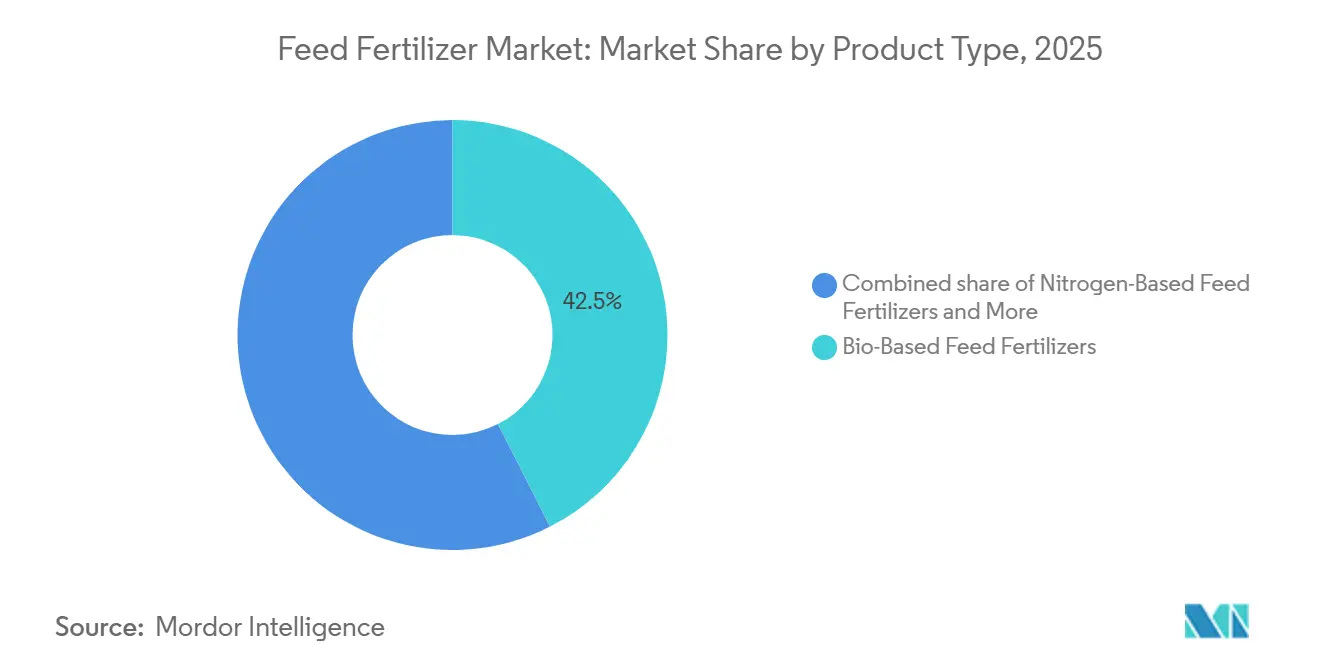

- By product type, nitrogen-based feed fertilizers captured the largest 42.5% share of the feed fertilizer market in 2025, while bio-based feed fertilizers are projected to post the fastest 12.7% CAGR during 2026-2031.

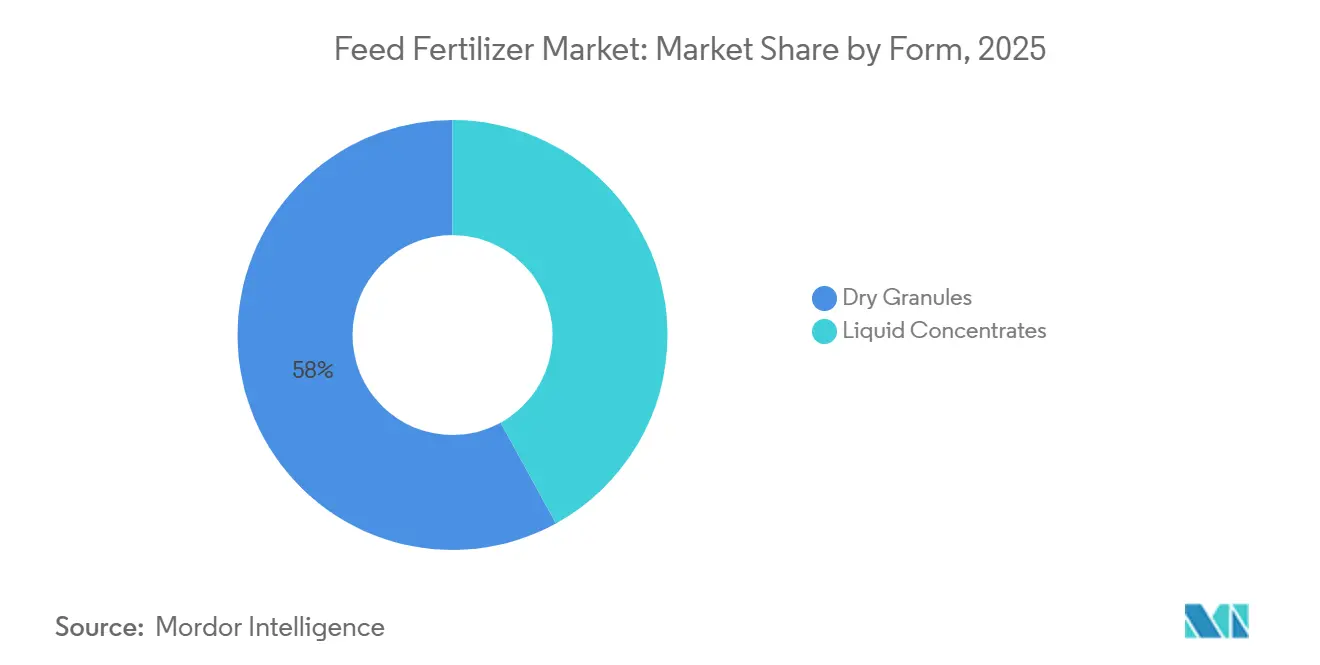

- By form, dry granules held the largest 58% share in 2025, whereas liquid concentrates are the fastest-growing segment, with a 11.9% projected CAGR during 2026-2031.

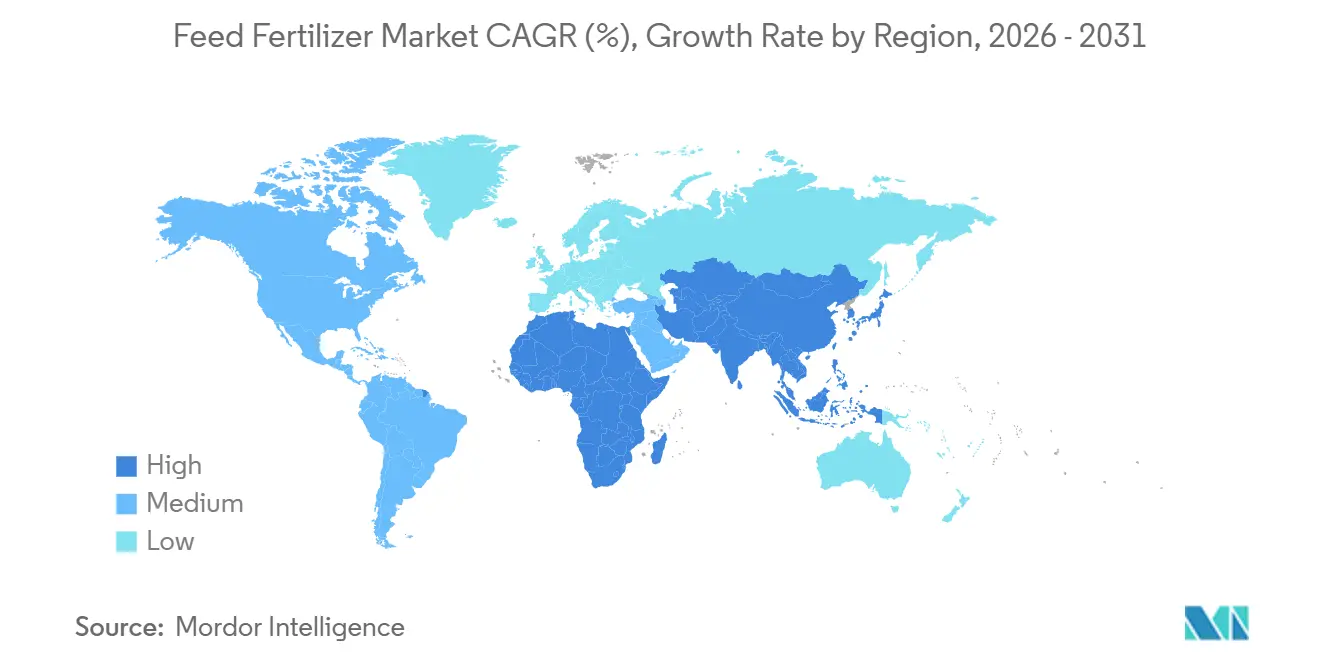

- By geography, Asia-Pacific accounted for the largest share of 38.2% in 2025, and Africa is forecast to register the fastest CAGR of 9.4% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Feed Fertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government mandates on sustainable livestock productivity | +1.8% | Global, the highest in Europe and North America | Medium term (2-4 years) |

| Growing demand for high-protein diets in emerging economies | +2.1% | Asia-Pacific core, spill-over to the Middle East and Africa | Long term (≥ 4 years) |

| Expansion of aquaculture requires water-soluble feed fertilizers | +1.5% | Asia-Pacific dominant, South America secondary | Medium term (2-4 years) |

| Rising adoption of precision farming in animal husbandry | +1.2% | North America and Europe are early adopters, and Asia-Pacific uptake | Long term (≥ 4 years) |

| Algae-based biofertilizers are improving feed conversion ratios | +0.7% | Global, especially in Europe, and the Asia-Pacific | Long term (≥ 4 years) |

| Carbon-credit monetization of manure-derived fertilizers | +0.9% | North America and Europe lead, and Japan and Australia are emerging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Mandates on Sustainable Livestock Productivity

In 2025, the European Union Common Agricultural Policy introduced mandatory nutrient budgeting rules, requiring farms to document fertilizer usage in accordance with soil threshold limits[1]Source: Agriculture and Rural Development Directorate, “Common Agricultural Policy Reform 2025,” European Commission, europa.eu . Similarly, in the United States and Canada, compliance measures tie subsidy eligibility to nutrient audits, encouraging the adoption of precision-dosed products with full traceability. These regulatory frameworks have driven innovation in the agricultural sector, as seen with Yara International's launch of the YaraPlus platform in 2025, which provides real-time recommendations aligned with regulatory requirements and creates new service-based revenue opportunities. Complementing these global efforts, India introduced a fermented organic manure program in the same year, subsidizing 50% of setup costs for smallholder dairy farmers. Together, these initiatives highlight a global shift towards sustainable livestock practices, fostering increased demand for precision agriculture and organic inputs while aligning with environmental and economic goals.

Growing Demand for High-Protein Diets in Emerging Economies

Dietary shifts in the Asia-Pacific region toward higher consumption of meat, fish, and eggs are driving growth in compound feed volumes, subsequently impacting the feed fertilizer market[2]Source: Fisheries and Aquaculture Department, “Global Aquaculture Production 2025,” Food and Agriculture Organization, fao.org. This trend is further supported by rising disposable incomes in countries such as Indonesia, Bangladesh, and Vietnam, which are fueling the expansion of intensive shrimp farming operations requiring precise nitrogen and phosphate applications. While poultry remains dominant, its growth is stabilizing in mature exporting countries like Thailand, prompting investors to redirect capital toward fish and shrimp value chains. Consequently, the increasing demand for protein is steering the market toward liquid concentrates optimized for closed-loop systems, marking a shift away from traditional broad-acre granules and aligning with the evolving needs of these emerging economies.

Expansion of Aquaculture Requiring Water-Soluble Feed Fertilizers

In 2025, the Aquaculture Stewardship Council updated its Feed Standard to version 1.2, emphasizing ingredient traceability and stricter nutrient runoff thresholds[3]Source: Aquaculture Stewardship Council, “Feed Standard Version 1.2,” Aquaculture Stewardship Council, asc-aqua.org. This shift led certified shrimp and salmon farms in Europe and North America to pay premiums for inputs that mitigate eutrophication risks, driving demand for water-soluble fertilizers. Liquid concentrates, favored for their compatibility with recirculating aquaculture systems, captured the majority of aquaculture feed sales. Simultaneously, the United States Food and Drug Administration's phosphate inclusion limits to prevent skeletal deformities in farmed fish pushed formulators toward enhanced-efficiency blends. These interconnected developments have elevated entry barriers for commodity suppliers while rewarding environmentally innovative solutions, consolidating the role of water-soluble fertilizers in sustainable aquaculture practices.

Rising Adoption of Precision Farming in Animal Husbandry

Sensor-equipped feeders and near-infrared analyzers are optimizing rations in real time, reducing waste and nitrogen losses. Early adopters in the United States and Canada report fertilizer cost reductions of 10-15%, even amid raw material price inflation. However, data-sharing concerns under the General Data Protection Regulation (GDPR) are slowing adoption in Europe, as independent farms fear exposing sensitive information. While technology vendors offer encrypted, farm-owned storage solutions, high onboarding costs deter smaller operators. Consequently, precision farming platforms are primarily concentrated among vertically integrated producers, who can efficiently distribute investments across large herds and nutrient management systems, driving more streamlined adoption in this segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of key raw materials | -1.1% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Stringent residue limits in animal-source foods | -0.6% | Europe and North America are primary, Asia-Pacific is gradual | Medium term (2-4 years) |

| Slow regulatory approvals for novel microbial fertilizers | -0.4% | Global, strictest in the European Union and North America | Long term (≥ 4 years) |

| Farm-level resistance to data-sharing for precision plans | -0.3% | North America and Europe are concentrated | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Key Raw Materials

Fluctuations in phosphate and nitrate prices disrupt procurement planning and reduce operating margins for feed fertilizer suppliers. Nutrien's 2025 closure of its Trinidad nitrogen facility, cutting 0.7 million metric tons of ammonia production, underscores how sustained cost inflation forces capacity reductions. Simultaneously, China's 2025 phosphate export quota tightened global supply, driving price surges in Africa and South America. Smaller producers, lacking vertical integration or long-term contracts, face the full impact of these shocks, leading to reduced innovation spending and higher costs for livestock farmers, ultimately constraining market growth.

Stringent Residue Limits in Animal-Source Foods

In 2026, the European Food Safety Authority enforced stricter residue thresholds, while the United States Food and Drug Administration introduced similar aquaculture feed limits in 2025, driving costly reformulations. These changes have increased analytical testing and documentation expenses by 15-20% compared to 2024, creating challenges for smaller entrants. Producers attempting to offload unsalable inventories in lenient regions face growing pressure from global retailers demanding compliance proof. As a result, heightened regulatory risks are curbing market expansion, particularly for conventional phosphate products, emphasizing the need for compliance to sustain growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bio-Based Momentum Next to Nitrogen Supremacy

Nitrogen-based feed fertilizers held the largest share, accounting for 42.5% of 2025 revenue in the feed fertilizer market, reflecting their critical role in protein synthesis and their linkage to global ammonia networks. Bio-based feed fertilizers held only a limited share yet posted the fastest 12.7% CAGR through 2026-2031, suggesting a rising appetite for carbon-friendly inputs. Phosphate-based feed fertilizers captured a prominent share of the market, driven by skeletal growth requirements in poultry and swine, while potash served ruminants. The segment narrative, therefore, revolves around nitrogen defending its dominant position while bio-based lines become premium niches.

Coromandel International recorded 18% specialty-nutrient growth in Q3 FY 2025 after the launch of Gromor Bio Organic, indicating tangible traction among Indian dairies. YaraBasa TURBO, launched in Brazil in 2025, integrates urease inhibitors that reduce ammonia loss by 30%, illustrating how incumbents defend their share via upgraded chemistries. China’s export quotas pressure phosphate availability, widening price differentials, and nudging buyers toward nitrogen-potash blends. Over 2026-2031, the feed fertilizer market for nitrogen remains sturdy, but portfolio growth will tilt toward bio-based innovations that bundle carbon credit revenue.

By Form: Liquid Concentrates Accelerate Under Aquaculture Demand

Dry granules remained the largest, accounting for 58% of 2025 sales, due to established spreader infrastructure on mixed farms. However, liquid concentrates logged an 11.9% CAGR through 2026-2031, the fastest among form factors, because aquaculture systems require homogenous dissolution to safeguard water quality. Swine operations transitioning to wet feeding also favor liquids that minimize dust and aid palatability. Transportation costs for water-rich liquids limit adoption in regions without dense farm clusters, yet rising clusterization in Southeast Asia offsets this drawback. Consequently, product strategists diversify into two parallel lines rugged granules for broad-acre ruminant zones and precise liquids for intensive fish and pig enterprises.

Equipment vendors now offer mobile on-farm blending units that mix liquid concentrates on demand, lowering freight charges. Certified farms under the Aquaculture Stewardship Council Feed Standard pay premiums for traceable liquid nutrients, further reinforcing the growth differential. Dry granule suppliers respond by micronizing particles to improve dissolution rates, narrowing performance gaps. Nonetheless, as aquaculture’s share of global protein climbs, liquids will capture an incremental share of the feed-fertilizer market's growth.

Geography Analysis

In 2025, Asia-Pacific led the market with a 38.2% share, driven by concentrated poultry clusters in China, expanding dairy operations in India, and robust shrimp farming in Vietnam and Indonesia. Tightened phosphate-export quotas in China prompted diversification into nitrogen and bio-based blends, enhancing per-unit value. Africa is projected to grow at a 9.4% CAGR during 2026-2031, is advancing through government initiatives promoting protein self-sufficiency and feed infrastructure upgrades, with mobile payments and cooperative hubs improving distribution despite logistical challenges.

North America’s steady growth is fueled by carbon-credit monetization supporting manure-derived fertilizers, while South America benefits from vertically integrated poultry and swine chains that optimize input costs. Europe’s growth remains constrained by strict nutrient budgets, though premium enhanced-efficiency products mitigate tonnage declines. The Middle East is expanding through investments in domestic nutrient complexes for food security, while Russia’s herd rebuilding efforts are tempered by limited access to precision-farming technologies due to sanctions.

Global demand is rising as sustainability mandates and protein consumption increase. Asia-Pacific’s scale sets pricing benchmarks, Africa’s rapid growth adds new volume opportunities, and innovation from North and South America spreads globally through partnerships. These interconnected regional dynamics, supported by synchronized policy incentives and digital platforms, are anticipated to narrow adoption gaps and drive the global feed fertilizer market forward.

Competitive Landscape

The feed fertilizers market is moderately consolidated, with the top five suppliers, Yara International ASA, Nutrien Ltd., The Mosaic Company, ICL Group, and EuroChem Group, dominating the market, collectively accounting for the majority of the 2025 revenue. Yara International ASA leads with its upstream mine ownership, large-scale ammonia synthesis, and the YaraPlus digital platform, which integrates compliance tools and agronomic advisory services. Nutrien Ltd. complements this leadership with a similar integrated model, reallocating capital from high-cost phosphate assets to higher-margin specialty nutrients and retail services. These two companies set pricing trends, define product standards, and secure enterprise-scale contracts, shaping the competitive dynamics.

The Mosaic Company has bolstered its potash market position with the Esterhazy K3 expansion completed in 2024, targeting ruminant and broad-acre agricultural segments. ICL Group leverages proprietary phosphorus technologies and specialty blends to capture value-added niches, while EuroChem Group benefits from strategically located nitrogen and phosphate assets near key grain-producing regions, offering freight advantages in Eastern Europe and Central Asia. Together, these companies enhance their competitive edge by combining upstream resource control with tailored formulations for livestock applications.

Growth strategies across these leaders converge on digital agronomy, carbon-credit monetization, and geographic diversification into high-growth aquaculture regions. Yara International ASA and Nutrien Ltd. are expanding subscription-based advisory services to secure recurring fertilizer sales, while The Mosaic Company and ICL Group are certifying manure-derived products through partnerships with registries like the Climate Action Reserve. As regulatory scrutiny intensifies and sustainability demands rise, companies integrating data analytics, vertical operations, and environmental credentials are poised to drive the feed fertilizer market forward, solidifying their leadership positions.

Feed Fertilizer Industry Leaders

Yara International ASA

Nutrien Ltd.

The Mosaic Company

ICL Group

EuroChem Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Climate Action Reserve issued over 2 million soil credits under its Soil Enrichment Protocol, covering fertilizer and soil-amendment practices derived from organic and manure-based sources. This milestone legitimizes carbon-credit revenue streams for manure-derived fertilizers and is anticipated to accelerate market growth by improving the return on investment for integrated livestock-fertilizer operations.

- January 2026: The European Food Safety Authority revised its feed-additive application procedures and residue-evaluation framework, heightening scientific assessment stringency for new nutrient products. Stricter standards will likely shift demand toward premium, enhanced-efficiency formulations, thereby raising the average selling price within the feed fertilizer market.

- December 2025: Nutrien Ltd. completed the sale of its 50% stake in Profertil S.A. to Adecoagro S.A. and Asociación de Cooperativas Argentinas for about USD 600 million as part of portfolio streamlinin. Divestment of this high-cost asset enables Nutrien Ltd. to redeploy capital into specialty nutrients and digital retail services, supporting product innovation that will lift overall market value.

Global Feed Fertilizer Market Report Scope

The feed fertilizer market covers nutrient products, both synthetic and bio-based, formulated to improve feed conversion and animal health across poultry, swine, ruminant, and aquaculture systems. It includes nitrogen, phosphate, potash, and specialty organic inputs supplied in dry granular or liquid forms through direct, cooperative, and retail channels. The Feed Fertilizer Market Report is Segmented by Product Type (Nitrogen-Based, Phosphate-Based, Potash-Based, and Bio-Based), by Form (Dry Granules and Liquid Concentrates), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Nitrogen-Based Feed Fertilizers |

| Phosphate-Based Feed Fertilizers |

| Potash-Based Feed Fertilizers |

| Bio-Based Feed Fertilizers |

| Dry Granules |

| Liquid Concentrates |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Nitrogen-Based Feed Fertilizers | |

| Phosphate-Based Feed Fertilizers | ||

| Potash-Based Feed Fertilizers | ||

| Bio-Based Feed Fertilizers | ||

| By Form | Dry Granules | |

| Liquid Concentrates | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the feed fertilizer market by 2031?

The feed fertilizer market size is projected to reach USD 34.4 billion by 2031.

Which product type is growing the fastest through 2026-2031?

Bio-based formulations are forecast to post the fastest 12.7% CAGR during 2026-2031.

How large is Asia-Pacific's share in the feed fertilizer market?

Asia-Pacific held the largest share of the feed fertilizer market, accounting for 38.2% in 2025.

Who are the leading companies in feed fertilizers?

Yara International, Nutrien, The Mosaic Company, ICL Group, and EuroChem Group accounted for moderate share of 2025 revenue, with Yara International leading.

Page last updated on: