UK Pet Treats Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

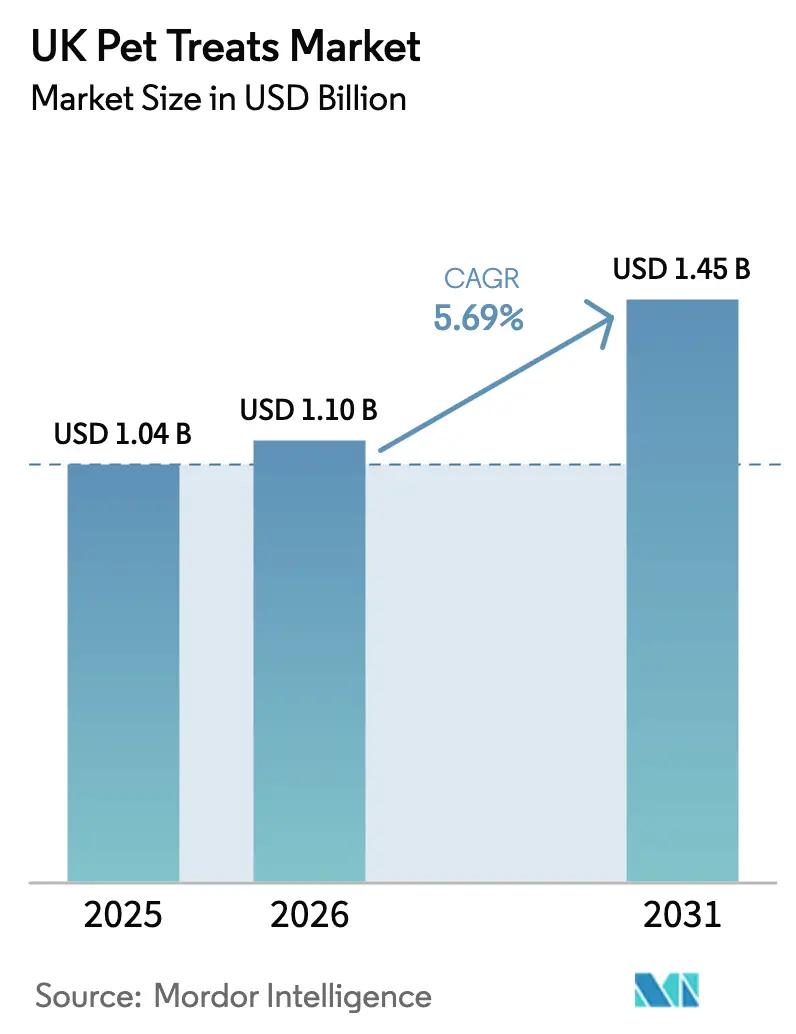

| Base Year Market Size (2025) | USD 1.04 Billion |

| Market Size (2026) | USD 1.1 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

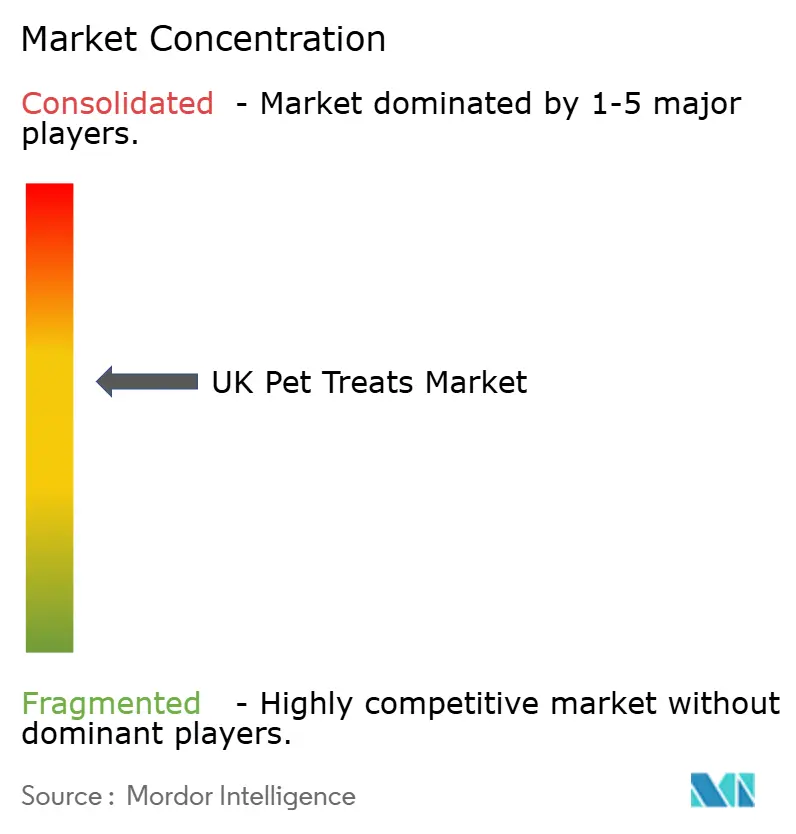

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Pet Treats Market Analysis by Mordor Intelligence

The UK pet treats market size was valued at USD 1.04 billion in 2025 and estimated to grow from USD 1.1 billion in 2026 to reach USD 1.45 billion by 2031, at a CAGR of 5.69% during the forecast period (2026-2031). Robust demand stems from millions of pet-owning households that continue to prioritize animal health despite the headwinds of rising living costs. Novel protein approvals, the rapid adoption of e-commerce subscriptions, and a steady influx of premium functional products sustain the growth momentum. Dogs remain the dominant consumer group, yet feline-specific innovation is adding incremental value. Consolidation among processors and retailers is intensifying competition, while inflationary protein costs are driving greater interest in insect and cultivated alternatives. As a result, the UK pet treats market shows a durable pathway for value expansion even in a cautious spending environment.

Key Report Takeaways

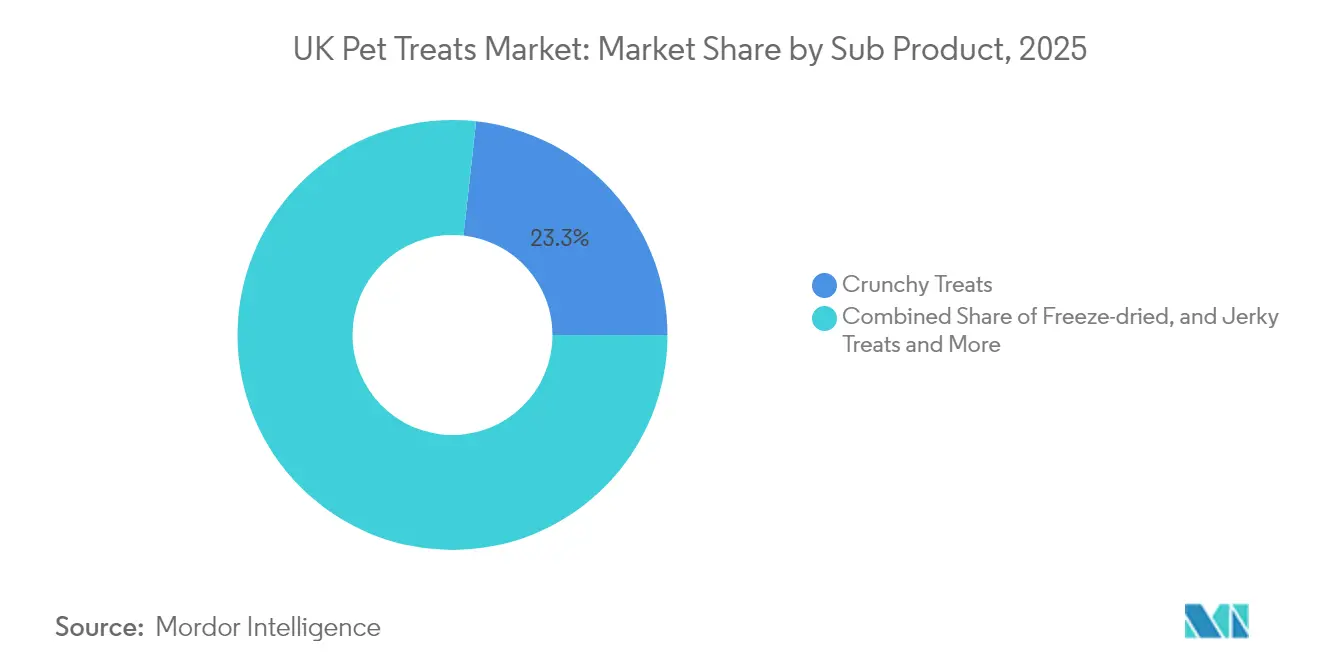

- By sub-product, crunchy treats led with a 23.25% revenue share in 2025, while freeze-dried and jerky treats are projected to grow at a 6.81% CAGR through 2031.

- By pet, dogs held 52.10% of the UK pet treats market share in 2025, and cats were projected to have the highest growth rate of 7.09% from 2025 to 2031.

- By distribution channel, supermarkets and hypermarkets accounted for a 32.85% share of the UK pet treats market size in 2025, whereas the online channel is projected to advance at a 6.71% CAGR through 2031.

- The UK pet treats market exhibits moderate fragmentation, with the top companies, including Mars, Incorporated, Nestle (Purina), Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.), Real Pet Food Co., and VAFO Group a.s., accounting for 42.90% of market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UK Pet Treats Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet humanization and premiumization surge | +1.8% | UK-wide, strongest in urban centers | Medium term (2-4 years) |

| Rapid expansion of e-commerce and D2C subscription models | +1.2% | National, with higher penetration in metropolitan areas | Short term (≤ 2 years) |

| Veterinary-endorsed functional treats gaining traction | +0.9% | UK-wide, concentrated around veterinary practices | Medium term (2-4 years) |

| Post-Brexit approvals for novel proteins | +0.7% | UK national regulatory advantage | Long term (≥ 4 years) |

| Data-driven personalization of treat formulations | +0.5% | Urban areas with higher digital adoption | Long term (≥ 4 years) |

| Flexible recyclable pouches reducing shelf-space constraints | +0.4% | National retail distribution | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pet Humanization and Premiumization Surge

Premium functional treats now command price premiums of 40-60% over conventional lines, aided by product launches such as DoggyRade’s superfood snacks, which blend pumpkin, cranberries, and prebiotics[1]Source: David Rees, “DoggyRade launches superfood snacks range,” Pet Business World, petbusinessworld.co.uk. Human-grade recipes, upscale packaging designs, and lifestyle branding encourage shoppers to treat their pets as family members, sustaining their willingness to pay. Veterinary endorsement strengthens differentiation, as Nutravet reports 2024, a high level of professional recommendations for functional chews priced between GBP 20-60 (USD 25-75). These dynamics elevate average selling prices, reinforcing revenue resilience for the UK pet treats market and allowing smaller innovators to capture niches through high-quality formulations that mirror human wellness trends.

Rapid Expansion of E-commerce and D2C Subscription Models

Digital transformation has revolutionized the distribution of UK pet treats, particularly in online pet supplies. Subscription pioneers such as Tails.com and Butternut Box fuel the trend through algorithms that curate monthly selections tailored to breed, age, and health conditions. Pets at Home reports that subscriptions already generate a good amount of consumer revenue, confirming mainstream adoption. Data harvested from these recurring orders informs product development, while predictable revenue helps brands navigate protein price volatility. As digital penetration deepens, the UK pet treats market benefits from lower customer acquisition costs and richer consumer insight that fuel agile innovation.

Veterinary-Endorsed Functional Treats Gaining Traction

Blurring the line between supplements and snacks, veterinary-endorsed chews target dental hygiene, joint mobility, and digestive comfort. Zesty Paws has logged more than 350,000 five-star reviews for its science-based range in 2024 alone. Exclusive VetSelect lines from Nutravet, sold only through clinics, achieve premium price points by leveraging professional trust. Regulatory bodies such as the Veterinary Oral Health Council validate dental formulas, while emerging probiotic and anxiety-relief SKUs borrow rigor from human nutraceutical science. This clinical framing reassures owners that functional treats complement, rather than compromise, medical care, sustaining high-margin growth inside the UK pet treats market.

Post-Brexit Approvals for Novel Proteins

The Food Standards Agency introduced fast-track rules that cleared Meatly’s cultivated chicken for commercial sale in 2024, making the United Kingdom an early adopter of cell-grown proteins. Insect and precision-fermented options share similar tailwinds, creating a sustainability narrative that appeals to environmentally conscious buyers. Manufacturers can now diversify ingredient sourcing, hedge against meat inflation, and market hypoallergenic formulas. Foreign developers view the United Kingdom as a strategic springboard into Europe, which in turn drives investment and job creation into local production facilities. Over the long term, this regulatory edge can anchor the UK pet treats market as a hub for next-generation protein innovation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Meat-protein price inflation squeezing margins | -1.1% | UK-wide, affecting all protein-based treats | Short term (≤ 2 years) |

| Stringent United Kingdom feed-safety and labeling compliance costs | -0.8% | National regulatory compliance burden | Medium term (2-4 years) |

| Discretionary nature of treats amid cost-of-living crisis | -0.9% | UK-wide, strongest impact on lower-income households | Short term (≤ 2 years) |

| Obesity awareness curbing treat frequency | -0.4% | Urban areas with higher veterinary awareness | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Meat-Protein Price Inflation Squeezing Margins

Elevated livestock costs have forced treat makers to weigh price hikes against demand elasticity. Premium brands that rely on high-quality cuts feel the squeeze most acutely, prompting reformulation with insect or plant-based proteins to stabilize input costs. Smaller producers lack volume buying leverage and therefore face heightened takeover risk, hastening consolidation. The headwind shaves near-term profitability but also steers the UK pet treats market toward more sustainable proteins that carry lower cost volatility over time.

Discretionary Nature of Treats Amid Cost-of-Living Crisis

The cost-of-living crisis has fundamentally altered consumer behavior in the UK pet treats market. Pet treats, being discretionary purchases, face particular vulnerability during economic downturns, with consumers likely to reduce frequency of purchase or trade down to lower-priced alternatives. The RSPCA (Royal Society for the Prevention of Cruelty to Animals) has responded by expanding pet food bank services and promoting homemade treat recipes, highlighting the severity of financial pressures on pet-owning households[2]Source: RSPCA, “Looking after your pets in the cost of living crisis,” RSPCA, rspca.org.uk. Even so, emotional bonds often elevate pet needs above personal luxuries, limiting volume decline. Brands that offer small-pack formats or multipack promotions retain engagement, cushioning downside risk for the UK pet treats market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Premium Positioning Drives Category Evolution

Crunchy treats accounted for 23.25% revenue share in 2025, owing to familiar textures and extended shelf life across mass outlets. Freeze-dried and jerky formats, supported by a 6.81% CAGR projection, ride premium perception and nutrient retention. The freeze-dry method removes water without additives, allowing for labeling that highlights a raw-like nutrition at higher price points. Soft and chewy snacks appeal to owners of senior animals who require easy-to-chew options, while dental sticks earn trust through Veterinary Oral Health Council seals. Emerging technologies, such as low-temperature air drying, help companies to introduce supercharged formulas blending meat with gut-support botanicals.

New entrants focus on single-protein and grain-free promises to capture allergy-aware buyers, elevating average unit value for the UK pet treats market. Other sub-product niches, ranging from DIY kits to seasonal gifting boxes, diversify the aisle and sustain shopper excitement. Collectively, premiumization inside each format keeps revenue growth outpacing volume growth, reinforcing how functional positioning now anchors brand equity.

By Pets: Feline Innovation Accelerates Growth

Dogs held 52.10% of the UK pet treats market share in 2025 because of entrenched training routines that rely on reward snacks. Large dental chews and multi-occasion packs maintain canine leadership. Cats, however, record the fastest 7.09% CAGR, driven by texture innovations and meat-first recipes that resolve historic pickiness. Brands such as KittyRade leverage freeze-dry powders that dissolve into broth-like treats, meeting feline hydration needs.

Growth also stems from weight-management chews that balance caloric density and functional ingredients. Smaller animal categories, including rabbits and guinea pigs, gain visibility in specialty chains that tailor assortments for alternative companions. Though a niche, this diversification introduces incremental value, revealing the inclusive scope of the UK pet treats market.

By Distribution Channel: Digital Transformation Reshapes Retail

Supermarkets and hypermarkets represented 32.85% of the UK pet treats market size in 2025. High weekly footfall encourages impulse buys, while private-label lines give retailers margin control. The online channel, projected at 6.71% CAGR, attracts digital natives with auto-ship discounts and personalized dashboards. Direct-to-consumer innovators bypass shelf-space constraints, instead bundling treats into meal plans for continuous cross-sell.

Specialty stores maintain relevance by pairing merchandise with grooming or vet consultations that enrich advice-led shopping. Convenience stores satisfy last-minute needs in transit corridors, and veterinary clinics add professional credibility to therapeutic chews. Winning players blend channels through click-and-collect or mobile apps, ensuring frictionless access for all shopper segments within the UK pet treats market.

Geography Analysis

England anchors value leadership for the UK pet treats market due to dense population and higher disposable incomes that fuel premium purchases. London and the South East showcase above-average uptake of functional and subscription models, evidencing how urban digital fluency stimulates category trade-up. Scotland and Wales contribute steady volume through supermarkets and farm stores, while Northern Ireland exhibits rising online penetration despite smaller absolute demand. Regional vet density correlates with functional treat sales, confirming professional influence on shopper behavior.

Brexit-enabled regulatory flexibility favors nationwide rollout of novel proteins ahead of European counterparts, an advantage most evident in manufacturing clusters across Yorkshire and the Midlands. These zones welcome inward investment for cultured-meat pilot plants, enriching local job markets. Meanwhile, northern regions with sharper cost-of-living pressure see higher adoption of value packs and private label, signaling price sensitivity variations. Weather patterns also sway ingredient sourcing, with coastal processors capitalizing on fish by-products for omega-rich chew lines, injecting regional supply differentiation into the UK pet treats market.

Rural communities rely on specialty farm stores where seasonal promotions tie treats to broader animal-husbandry events, demonstrating localized marketing. Across all geographies, pet humanization remains a unifying force that mitigates economic volatility, although assortment optimization by postal code remains key for retailers seeking to maximize share.

Competitive Landscape

The UK pet treats market exhibits moderate fragmentation, with the top companies, including Mars, Incorporated, Nestle (Purina), Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.), Real Pet Food Co., and VAFO Group a.s., accounting for 43.24% of market share in 2024. Inspired Pet Nutrition paid GBP 43 million (USD 54 million) for Butcher’s Pet Care in 2024, expanding its treats footprint and manufacturing capacity[3]Source: Niamh Leonard-Bedwell, “Natural dog treat brand NAW launches 10 lines into Sainsbury's,” The Grocer, thegrocer.co.uk. The Nutriment Company acquired Natural Instinct and other peers, signaling its interest in premium, raw-inspired chew lines. Multinationals Mars, Incorporated, and Nestlé Purina safeguard their scale advantages through nationwide shelf presence and marketing muscle, whereas nimble direct-to-consumer brands, such as Lily’s Kitchen, secure loyalty by spotlighting high percentages of fresh meat and recyclable pouches.

Technology is a strategic moat. Data analytics optimize flavor rotation in subscription boxes, reduce stockouts, and personalize promotions. Larger groups invest in cold-chain logistics to preserve nutrient integrity in high-meat SKUs, whereas many startups outsource to co-packers until volume justifies vertical integration. Channel dynamics influence power balance; supermarket category captains command end-cap visibility, while online startups rely on influencer marketing and user-generated reviews to substitute for physical shelf discovery.

Sustainability credentials are now baseline expectations, pushing companies to audit supply chains, publish carbon footprints, and prioritize up-cycled ingredients. Functional health claims require clinical evidence, so firms partner with universities or veterinary hospitals for small-scale efficacy studies. These collaborations build reputational capital and justify premium price points, solidifying customer trust throughout the UK pet treats market.

UK Pet Treats Industry Leaders

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

Nestle (Purina)

Real Pet Food Co.

VAFO Group a.s.

Mars, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: NAW (No Animal Wasted) launched 10-SKU natural dog treat range into 309 Sainsbury's stores nationwide, featuring Buffalo, beef, lamb, chicken, and fish products priced USD 5.35-10.70, emphasizing animal offcut repurposing and air-drying processing to minimize waste and retain nutrients

- May 2023: Nestle Purina launched new cat treats under the Friskies "Friskies Playfuls - treats" brand. These treats are round in shape and are available in chicken and liver and salmon, and shrimp flavors for adult cats.

- May 2023: Vafo Praha, s.r.o. launched its new range of Brit RAW Freeze-dried treats and toppers for dogs. These products are made up of high-quality proteins and minimally processed ingredients for potential health benefits.

UK Pet Treats Market Report Scope

Crunchy Treats, Dental Treats, Freeze-dried and Jerky Treats, Soft & Chewy Treats are covered as segments by Sub Product. Cats, Dogs are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel.

| Dental Treats |

| Crunchy Treats |

| Soft and Chewy Treats |

| Freeze-dried and Jerky Treats |

| Other Treats |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Dental Treats |

| Crunchy Treats | |

| Soft and Chewy Treats | |

| Freeze-dried and Jerky Treats | |

| Other Treats | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms