Pet Calming Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 3.10 Billion |

| Growth Rate (2026 - 2031) | 14.90% CAGR |

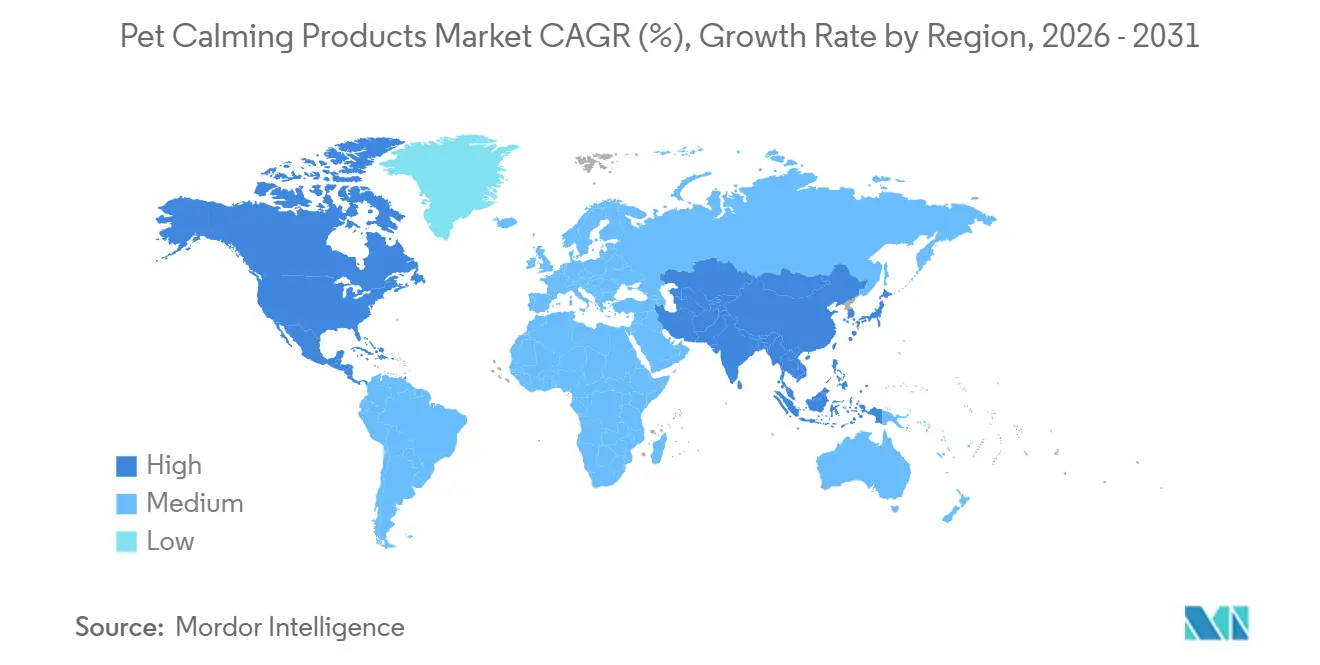

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

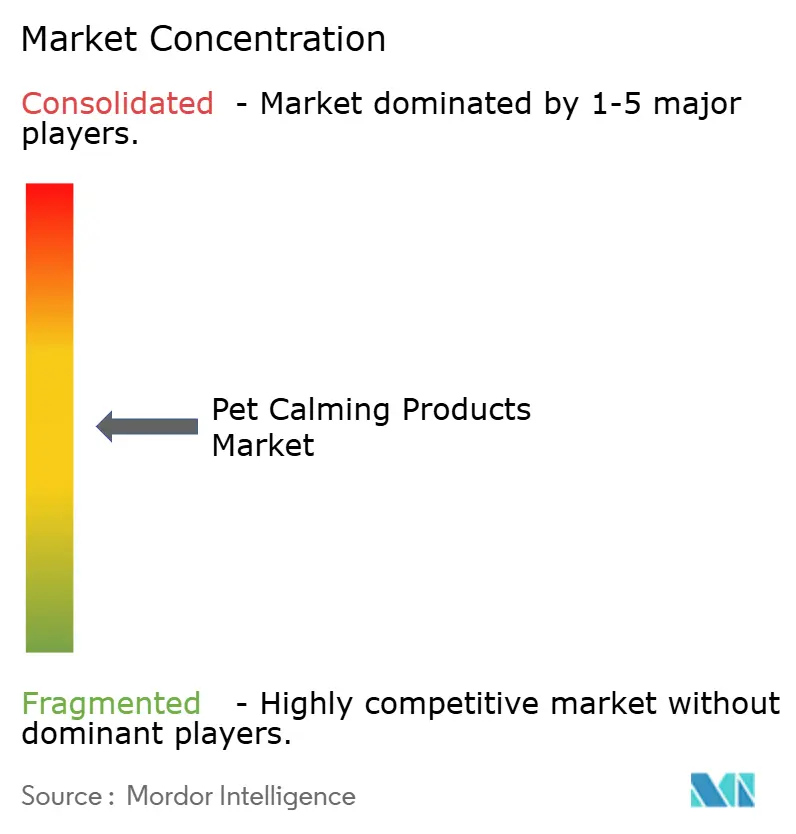

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Calming Products Market Analysis by Mordor Intelligence

The pet calming products market size is projected to expand from USD 1.55 billion in 2025 and USD 1.78 billion in 2026 to USD 3.10 billion by 2031, registering a CAGR of 14.9% between 2026 and 2031. Heightened urban noise, growth in multi-pet households, and wider veterinary endorsement are shifting anxiety relief from niche specialty to routine companion-animal care. Pheromone-based formats are gaining favor as randomized trials show stronger efficacy than edible treats, while natural botanicals retain a significant share as owners seek clean-label formulas. Online retail, led by subscription services that already generate significant revenue for Chewy, is scaling fastest and capturing repeat sales through autoship convenience. Regionally, Asia-Pacific is the growth frontrunner following Japan’s cannabinoid (CBD) rule change, which allows hemp-derived ingredients containing no more than 10 parts per million of THC (Tetrahydrocannabinol).

Key Report Takeaways

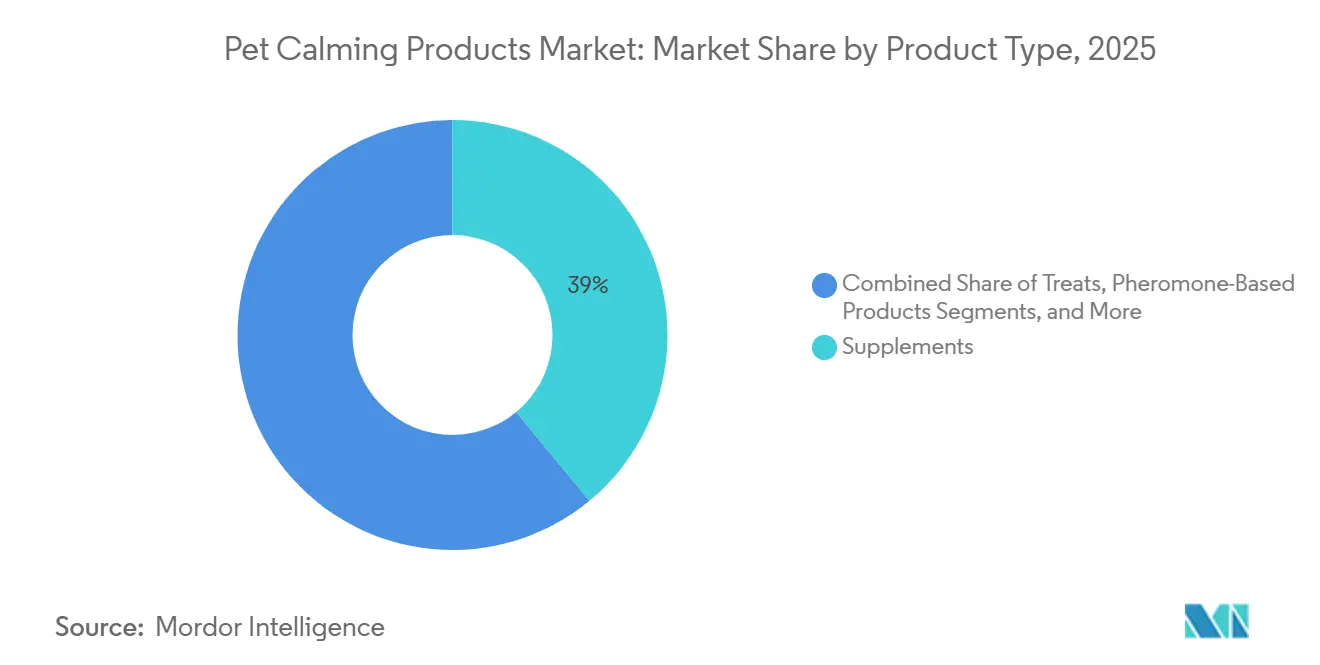

- By product type, supplements led the largest segment, with 39.0% of the pet calming products market share in 2025, while pheromone-based products are the fastest-growing segment, projected to advance at an 18.5% CAGR through 2026-2031.

- By pet type, dogs commanded the largest segment, 62.0% of the pet calming products market share in 2025, whereas the cat segment is the fastest-growing, projected to grow at 16.2% CAGR from 2026 to 2031.

- By distribution channel, online retail is the largest segment, capturing 46.0% of the pet calming products market size in 2025 and the fastest-growing segment, expanding at a 17.9% CAGR from 2026-2031.

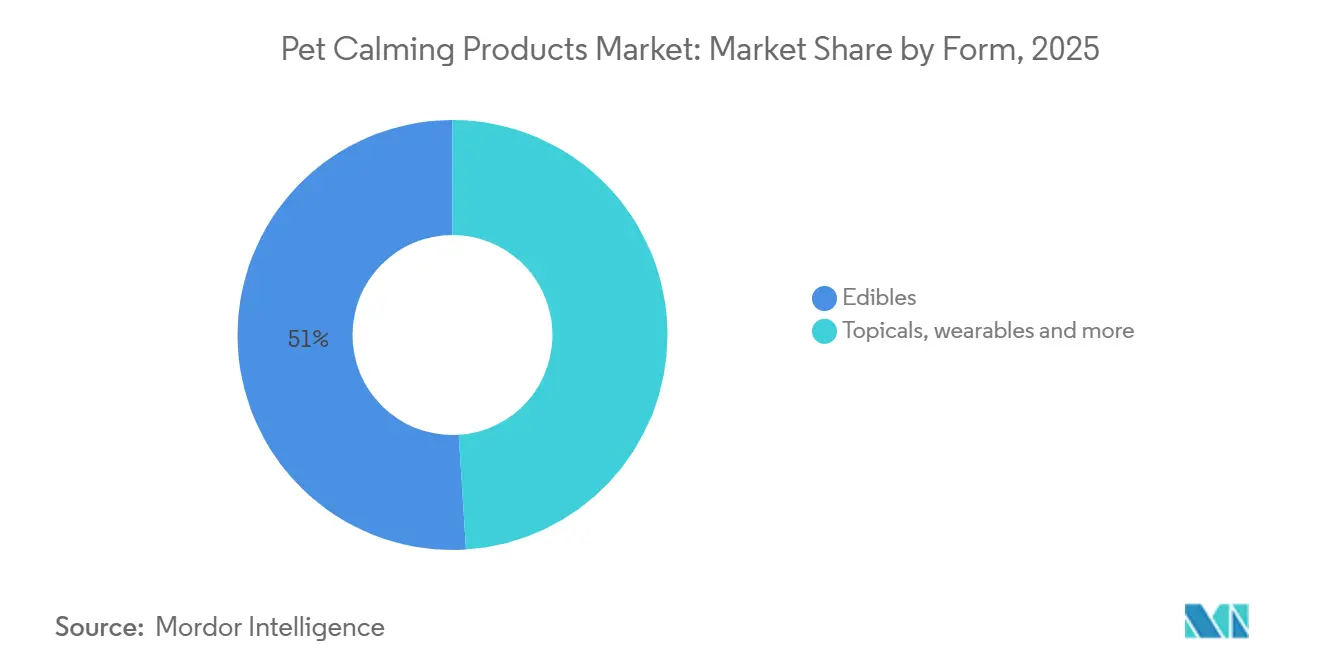

- By form, edibles are the largest segment, accounting for 51.0% of the pet calming products market size in 2025, while wearables are the fastest-growing segment, rising at a 19.3% CAGR through 2026-2031.

- By ingredient source, natural formulations is largest segment, dominated with 71.0% of the pet calming products market size in 2025, and are the fastest-growing segment, forecast to grow at a 17.0% CAGR from 2026-2031.

- By geography, North America led largest region, with 37% pet calming products market share in 2025, while Asia-Pacific exhibits the fastest trajectory at 14.9% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Calming Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet anxiety due to urban lifestyles | +3.2% | Global, with peak intensity in North America, Europe, and the Asia-Pacific urban centers | Medium term (2-4 years) |

| Increasing humanization of pets is driving premium spend | +3.8% | Global, strongest in North America and Europe, and accelerating in Asia-Pacific | Long term (≥ 4 years) |

| Surge in veterinarian-led behavioral wellness programs | +2.1% | North America and Europe, emerging in the Asia-Pacific | Medium term (2-4 years) |

| Expansion of e-commerce subscription models | +2.5% | Global, led by North America, is experiencing rapid adoption in the Asia-Pacific | Short term (≤ 2 years) |

| Adoption of wearable biomonitoring devices | +1.6% | North America and Europe, and early trials in the Asia-Pacific | Long term (≥ 4 years) |

| Relaxed hemp-derived Cannabidiol (CBD) regulations in key markets | +1.7% | North America, select Asia-Pacific markets (Japan), and limited Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Anxiety Due to Urban Lifestyles

Urban density exacerbates separation anxiety, noise hypersensitivity, and territorial stress in companion animals, driving consistent demand for calming solutions. The trend toward high-rise living in regions such as Singapore and Hong Kong has reduced outdoor access, confining pet activities to limited spaces and increasing chronic stress indicators. In 2025, research from the Texas A&M College of Veterinary Medicine and Biomedical Sciences (VMBS) revealed that over 99% of dogs in the United States exhibit potentially problematic behaviors, with the most common categories being aggression (55.6%), separation and attachment behaviors (85.9%), and fear and anxiety behaviors (49.9%)[1]Source: American Veterinary Medical Association, “2025 U.S. Pet Demographics Survey,” avma.org.

Increasing Humanization of Pets Driving Premium Spend

Pet owners are increasingly allocating discretionary income toward behavioral wellness for their pets, approaching it with the same priority as human healthcare. Anxiety management is now viewed as a preventive measure rather than a reactive one. In 2024, according to the American Pet Products Association (APPA), pet ownership in the United States is experiencing renewed growth, with 94 million households owning at least one pet. Gen Z is notably contributing to a significant rise in multi-pet ownership. Consumer spending patterns in this market parallel trends in the human supplements market, where higher unit costs are accepted for products featuring pharmaceutical-grade botanicals, clinical trial validation, and sustainability certifications.

Expansion of E-Commerce Subscription Models

Direct-to-consumer subscription platforms are fostering recurring revenue streams, lowering customer acquisition costs, and allowing brands to bypass traditional retail channels. Companies that combine calming supplements with personalized behavioral coaching or telemedicine consultations create switching costs, reducing vulnerability to price competition. The growth of e-commerce subscription models is further propelling market expansion. These platforms offer convenience by ensuring the regular delivery of pet calming products, eliminating the need for frequent purchases. This approach not only strengthens customer retention and brand loyalty but also improves access to premium and specialized calming solutions.

Adoption of Wearable Biomonitoring Devices

Wearable sensors that monitor heart rate variability, respiration, and activity patterns provide objective stress metrics, enabling the selection of calming products to shift from anecdotal trial-and-error to a data-driven approach. In March 2026, PetPace's collar tracks real-time physiological indicators and issues veterinarian-grade alerts when stress levels exceed baseline norms. This enables preemptive actions, such as administering calming supplements or activating pheromones. The adoption of wearable biomonitoring devices is significantly influencing the pet calming products market. These devices allow pet owners to track stress levels, activity patterns, and overall health in real time, facilitating early detection of anxiety or behavioral issues. This data-driven methodology enhances the effectiveness of targeted calming solutions, promoting wider adoption of such products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory gray zones around functional actives | -1.8% | Global, acute in Europe and select Asia-Pacific markets | Medium term (2-4 years) |

| Limited double-blind clinical efficacy studies | -1.2% | Global, constraining veterinary adoption and premium pricing | Long term (≥ 4 years) |

| Pharmaceutical-grade botanical supply constraints | -0.9% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Online counterfeits fuel consumer skepticism | -1.1% | Global, concentrated in e-commerce-heavy markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Gray Zones Around Functional Actives

Ambiguous regulatory frameworks for functional ingredients pose compliance risks, delay product launches, and complicate market access strategies. In 2024, the European Food Safety Authority's (EFSA) Panel on Additives and Products or Substances used in Animal Feed (FEEDAP) determined that the additive under assessment is safe for use in complete feed for dogs at a maximum level of 30 mg/kg[2]Source: European Food Safety Authority, “Scientific Opinion on CBD Safety in Food and Feed,” efsa.onlinelibrary.wiley.com. This lack of regulatory clarity often leads to conservative labeling practices, which obscure product benefits and reduce conversion rates among pet owners seeking targeted anxiety solutions. In the Asia-Pacific region, regulatory variability is even more pronounced. Companies that invest in regulatory intelligence and maintain adaptable supply chains are better positioned to navigate these complexities. Smaller market entrants often withdraw due to the high costs of compliance.

Limited Double-Blind Clinical Efficacy Studies

The lack of randomized controlled trials hinders veterinary endorsement, restricts the ability to command premium pricing, and exposes product differentiation to reliance on anecdotal marketing. The absence of standardized efficacy benchmarks enables low-quality competitors to make unverified claims, thereby reducing price premiums for clinically validated products. Veterinarians, reluctant to recommend supplements without peer-reviewed evidence, often resort to prescribing anxiolytics, which shifts market share toward pharmaceutical channels. Brands that invest in independent trials and publish findings in peer-reviewed journals can achieve differentiation, the high cost of such studies limits participation to companies with substantial financial resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pheromone Innovation Outpaces Supplement Incumbency

Supplements led the largest segment, with 39.0% of pet calming products market share in 2025, this dominance is attributed to consumer preference for easy-to-administer formats such as chews, tablets, and powders, which aid in stress and anxiety relief for pets. These products typically include natural ingredients such as herbs, amino acids, and vitamins, making them a preferred choice for pet owners seeking safe, non-invasive calming solutions. Furthermore, their widespread availability through veterinary channels and retail platforms enhances their market presence.

Pheromone-based products are the fastest-growing segment, projected to advance at an 18.5% CAGR through 2026-2031. These products function by mimicking natural calming signals, effectively reducing stress-related behaviors in pets, particularly dogs and cats. Their growing adoption is driven by increased awareness of behavior-based solutions and endorsements from veterinarians and pet behaviorists. As pet owners increasingly prioritize scientifically supported, non-pharmaceutical approaches, pheromone-based products are gaining significant market traction.

By Pet Type: Feline Segment Accelerates as Multi-Cat Households Proliferate

Dogs commanded the largest segment, 62.0% of the pet calming products market share in 2025. This dominance reflects the higher baseline prevalence of anxiety in dogs and the greater willingness of dog owners to invest in behavioral interventions. Factors such as higher global dog ownership rates and increased awareness among dog owners regarding anxiety-related behaviors, including separation anxiety, noise phobia, and travel stress, drive this trend. Additionally, the availability and marketing of a wide range of calming products, such as supplements, chews, collars, and anxiety wraps, further reinforce the leading position of the dog segment.

The cat segment is the fastest-growing, projected to grow at 16.2% CAGR to 2026-2031, attributed to rising cat adoption, particularly in urban areas where cats are often preferred because of their lower maintenance requirements. Increasing awareness of stress-related issues in cats, such as environmental changes and multi-pet households, is also boosting demand for specialized calming solutions. In Asia-Pacific markets, where cats outnumber dogs in urban apartments due to space constraints and landlord restrictions, this trend is particularly pronounced. According to the China Pet Industry Association, the total pet population in China reached 124.1 million in 2024, comprising 52.6 million dogs and 71.5 million cats, reflecting increase of 1.6% and 2.5%, respectively, from 2023[3]Source: Pet Hadoop, “China Pet Industry White Paper 2025,” pethadoop.com.

By Distribution Channel: Subscription E-Commerce Reshapes Retail Economics

Online retail is the largest segment, capturing 46.0% of the pet calming products market share in 2025 and the fastest-growing, expanding at a 17.9% CAGR to 2026-2031. This was driven by subscription models that transform episodic purchases into predictable cash flows. The dominance of online retail is attributed to the growing preference for convenient shopping, broader product availability, and easy access to customer reviews and product comparisons. E-commerce platforms also allow pet owners to explore a wide range of calming solutions, including niche and premium products that may not be easily found in physical stores. Targeted digital marketing, discounts, and doorstep delivery are enhancing consumer engagement and accelerating the shift toward online channels in the pet calming products market.

Veterinary clinics represent the highest-margin channel, as products sold through this channel often carry premiums due to the trust associated with professional recommendations. The growth of this channel is limited by veterinarians' reluctance to stock inventory and the administrative challenges of managing supplement sales alongside pharmaceutical dispensing. Brands that provide consignment arrangements or direct-ship programs help reduce friction for clinics but often sacrifice margins to intermediaries. Meanwhile, social commerce platforms such as TikTok and Instagram are emerging as discovery channels, with influencer endorsements encouraging trials among Generation Z pet owners.

By Form: Wearables Integrate Biometrics to Command Premium Pricing

Edibles are the largest segment, accounting for 51.0% of the pet calming products market size in 2025. Their popularity is attributed to ease of administration, high palatability, and strong acceptance among pets. Products like calming chews, treats, and supplements are particularly favored as they can be easily integrated into daily feeding routines while providing stress-relief benefits. Furthermore, the growing preference for natural, functional ingredients continues to drive the adoption of edible calming solutions.

Wearables are the fastest-growing segment, rising at a 19.3% CAGR through 2026-2031. This growth is driven by advancements in pet technology, including smart collars, vests, and biomonitoring devices that measure stress levels and behavioral patterns. Wearables offer real-time insights and enable proactive stress management through features such as calming signals or vibration-based interventions. As pet owners increasingly prioritize data-driven, non-invasive solutions, demand for wearable calming products is projected to grow substantially.

By Ingredient Source: Natural Formulations Dominate Amid Synthetic Skepticism

Natural formulations are the largest segment, accounting for 71.0% of the pet calming products market in 2025, and the fastest-growing segment, forecast to grow at a 17.0% CAGR from 2026-2031. This preference is driven by a growing consumer inclination toward clean-label, plant-based, and non-synthetic ingredients. Pet owners increasingly prioritize safety, transparency, and holistic wellness for their pets. Common natural calming ingredients include chamomile, valerian root, melatonin, and L-theanine, which are perceived as safer alternatives to pharmaceutical options. Their widespread availability and strong presence in both veterinary and retail channels further solidify their market leadership.

Synthetic ingredients, including pharmaceutical analogs of amino acids and neurotransmitter precursors, account for a significant share of the market but are often met with consumer skepticism. This skepticism is often intensified by social media narratives that associate synthetic ingredients with potentially harmful effects. Brands that conduct clinical trials to validate the safety and efficacy of synthetic ingredients can justify premium pricing, they face greater marketing challenges compared to natural alternatives. Probiotics, such as Purina's BL999 strain, further complicate the distinction between natural and synthetic by challenging consumer perceptions. Although these probiotics are naturally occurring, their laboratory cultivation introduces labeling challenges that may lead to consumer confusion, as consumers may struggle to categorize them as either natural or synthetic.

Geography Analysis

North America led largest region, with 37% pet calming products market share in 2025, this leadership is driven by high pet ownership rates, strong consumer spending on pet wellness, and widespread awareness of stress and anxiety issues in pets. According to the American Pet Products Association (APPA), total United States pet industry expenditures reached USD 152 billion in 2024, reflecting sustained growth and resilience. Well-established retail and e-commerce channels, coupled with a mature veterinary and pet care infrastructure, further support the adoption of a wide range of calming solutions across the region.

Asia-Pacific exhibits the fastest trajectory at 14.9% CAGR through 2026-2031, this rapid growth is fueled by rising pet adoption, increasing disposable incomes, and growing awareness of pet health and wellness. Emerging markets in countries such as China, India, and Southeast Asian nations are witnessing expanding e-commerce penetration and greater availability of innovative calming products, driving accelerated market adoption across the region.

In the European pet calming products market, Germany, France, and the United Kingdom lead regional demand. Specialty pet stores hold stronger market positions in North America than elsewhere, driven by a cultural preference for in-store consultations. Regulatory fragmentation across member states increases compliance costs, benefiting vertically integrated companies with legal teams adept at managing country-specific regulations. This fragmentation often leads to delays in product launches and additional expenses for smaller players, who may lack the resources to effectively address varying compliance requirements.

Competitive Landscape

The pet calming products market shows moderate concentration in 2025, with key players including Ceva Santé Animale S.A., Nestlé Purina PetCare Company, Central Garden & Pet Company, Vetoquinol S.A., and PetHonesty, LLC. Ceva Santé Animale S.A. maintains a leading position with its pheromone-based products, Adaptil and Feliway, supported by omnichannel distribution and strong relationships with veterinary professionals. Nestlé Purina PetCare capitalizes on its manufacturing scale and brand trust to drive sales of its probiotic-infused product, Calming Care.

Direct-to-consumer brands are increasingly utilizing influencer partnerships and content marketing to engage younger demographics. These companies often bundle supplements with wearable sensors, offering a technology-driven approach to pet calming solutions. Certification from the National Animal Supplement Council is becoming a critical requirement, particularly for Cannabidiol (CBD) products, as regulatory scrutiny intensifies.

Significant opportunities exist in developing feline-specific formulations, sourcing pharmaceutical-grade botanicals, and creating multi-sensory wearables that integrate compression, aromatherapy, and auditory elements. Emerging players are focusing on underserved segments, such as multi-cat households and exotic pets. Additionally, there is potential for growth in expanding product lines to address specific behavioral issues, such as separation anxiety and noise phobias, which are prevalent among pets. Meanwhile, established companies are defending their market share by investing in clinical trials and strengthening veterinary partnership programs, which help create barriers to switching for consumers.ing costs.

Pet Calming Products Industry Leaders

Ceva Santé Animale S.A.

Nestlé Purina PetCare Company

Central Garden & Pet Company.

Vetoquinol S.A.

PetHonesty, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Health Canada opened consultations on non-prescription CBD animal products. This initiative lays the groundwork for harmonized North American standards that could accelerate cross-border product launches.

- August 2024: Extract Labs earned NASC certification for its Fetch CBD line. The accreditation underscores a growing industry focus on third-party testing and batch-level transparency for cannabinoid pet products.

- April 2024: Zoetis launched Bonqat oral pregabalin, the first Food and Drug Administration (FDA)-approved feline anxiety therapy. The launch provides veterinarians with a prescription-strength option that validates clinical demand for cat-specific calming solutions.

Global Pet Calming Products Market Report Scope

Pet calming products are specifically designed to alleviate stress, anxiety, and behavioral issues in pets, including dogs, cats, and other companion animals. The pet calming products market report is segmented by product type (supplements, treats, pheromone-based products, pressure wraps/vests, and calming toys), by pet type (dogs, cats, and other pet types), by distribution channel (online retail, specialty pet stores, mass merchandisers/supermarkets, and veterinary clinics), by form (edibles, topicals, wearables, and devices), by ingredient source (natural and synthetic), and by geography (North America, Europe, Asia-Pacific, Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Supplements |

| Treats |

| Pheromone-Based Products |

| Pressure Wraps/Vests |

| Calming Toys |

| Dogs |

| Cats |

| Other Pet Types |

| Online Retail |

| Specialty Pet Stores |

| Mass Merchandisers/Supermarkets |

| Veterinary Clinics |

| Edibles |

| Topicals |

| Wearables |

| Devices |

| Natural |

| Synthetic |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Supplements | |

| Treats | ||

| Pheromone-Based Products | ||

| Pressure Wraps/Vests | ||

| Calming Toys | ||

| By Pet Type | Dogs | |

| Cats | ||

| Other Pet Types | ||

| By Distribution Channel | Online Retail | |

| Specialty Pet Stores | ||

| Mass Merchandisers/Supermarkets | ||

| Veterinary Clinics | ||

| By Form | Edibles | |

| Topicals | ||

| Wearables | ||

| Devices | ||

| By Ingredient Source | Natural | |

| Synthetic | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is global demand for pet calming solutions anticipated to become by 2031?

Pet calming solutions market is projected to reach USD 3.10 billion in 2031, up from USD 1.78 billion in 2026 as buyers seek reliable tools to manage companion-animal stress.

Which product category is growing fastest among calming options?

Pheromone-based formats are leading expansion with an anticipated 18.5% CAGR from 2026-2031, outpacing treats, supplements, and pressure wraps.

What makes subscription ecommerce critical for suppliers?

Autoship services already account for 80% of Chewy revenue, turning one-time purchases into recurring sales while lowering customer acquisition costs and improving loyalty.

Which geography shows the strongest growth outlook to 2031?

Asia-Pacific leads with an anticipated 14.9% CAGR through 2026-2031, fueled by China's expanding pet population and Japan's clear rules on hemp-derived CBD ingredients.

Page last updated on: