Surgical Snare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

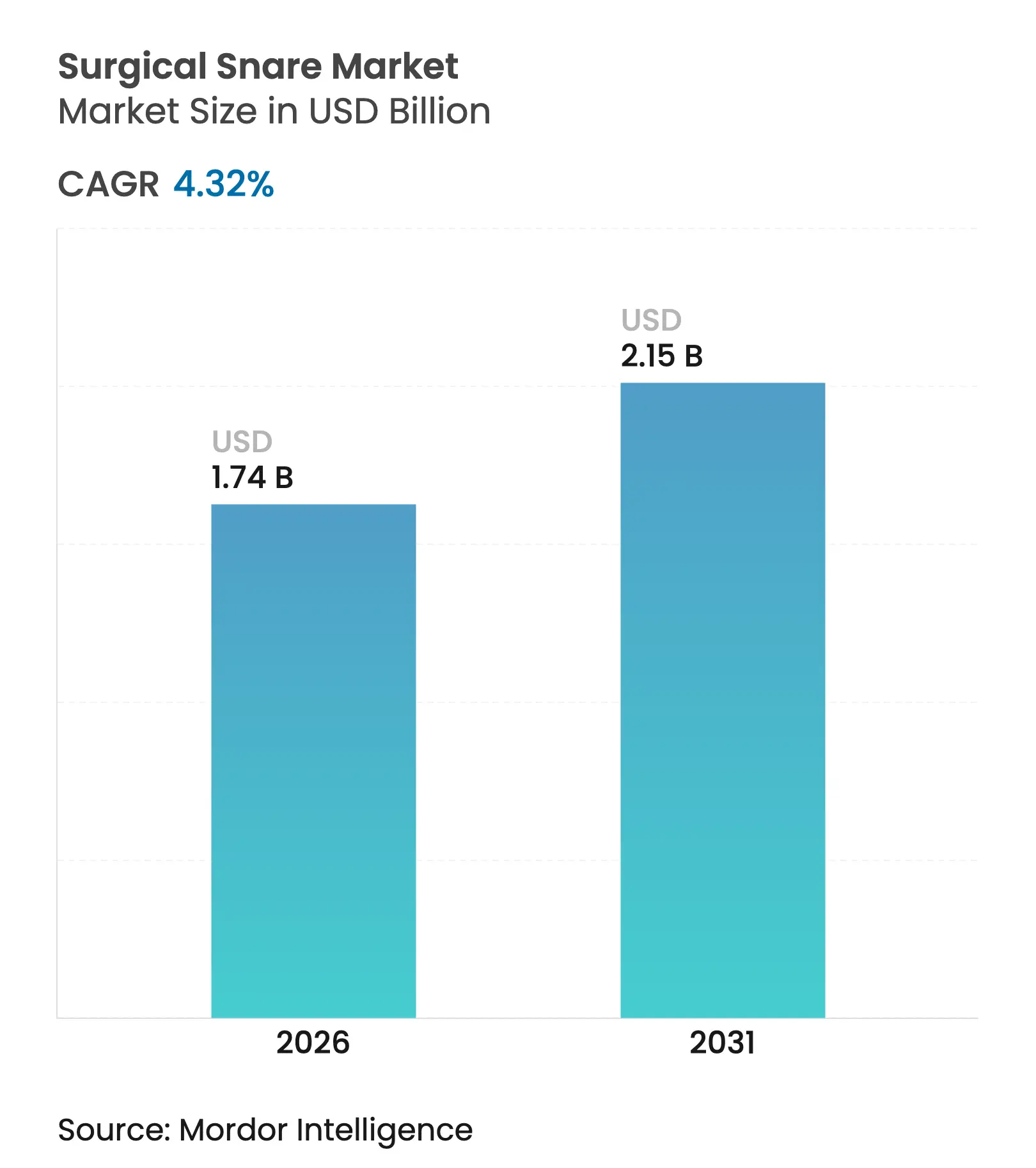

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 2.15 Billion |

| Growth Rate (2026 - 2031) | 4.32 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Surgical Snare Market Analysis by Mordor Intelligence

Surgical snare market size in 2026 is estimated at USD 1.74 billion, growing from 2025 value of USD 1.67 billion with 2031 projections showing USD 2.15 billion, growing at 4.32% CAGR over 2026-2031. Growth aligns with rising colorectal-cancer screening volumes, broader adoption of AI-assisted detection systems, and the transition toward cold-snare polypectomy that improves safety profiles. Ambulatory surgery centers (ASCs) now perform 72% of United States procedures at 45-60% lower costs than hospital settings, sharply increasing demand for single-use snares. Demographic tailwinds from aging populations further sustain procedure volumes, while technology leaders differentiate through shape optimization and artificial intelligence rather than price competition. Quality-assurance challenges, including recent recalls of single-use guide sheath kits, underscore the need for robust clinical evidence and post-market surveillance to protect adoption trajectories.

Key Report Takeaways

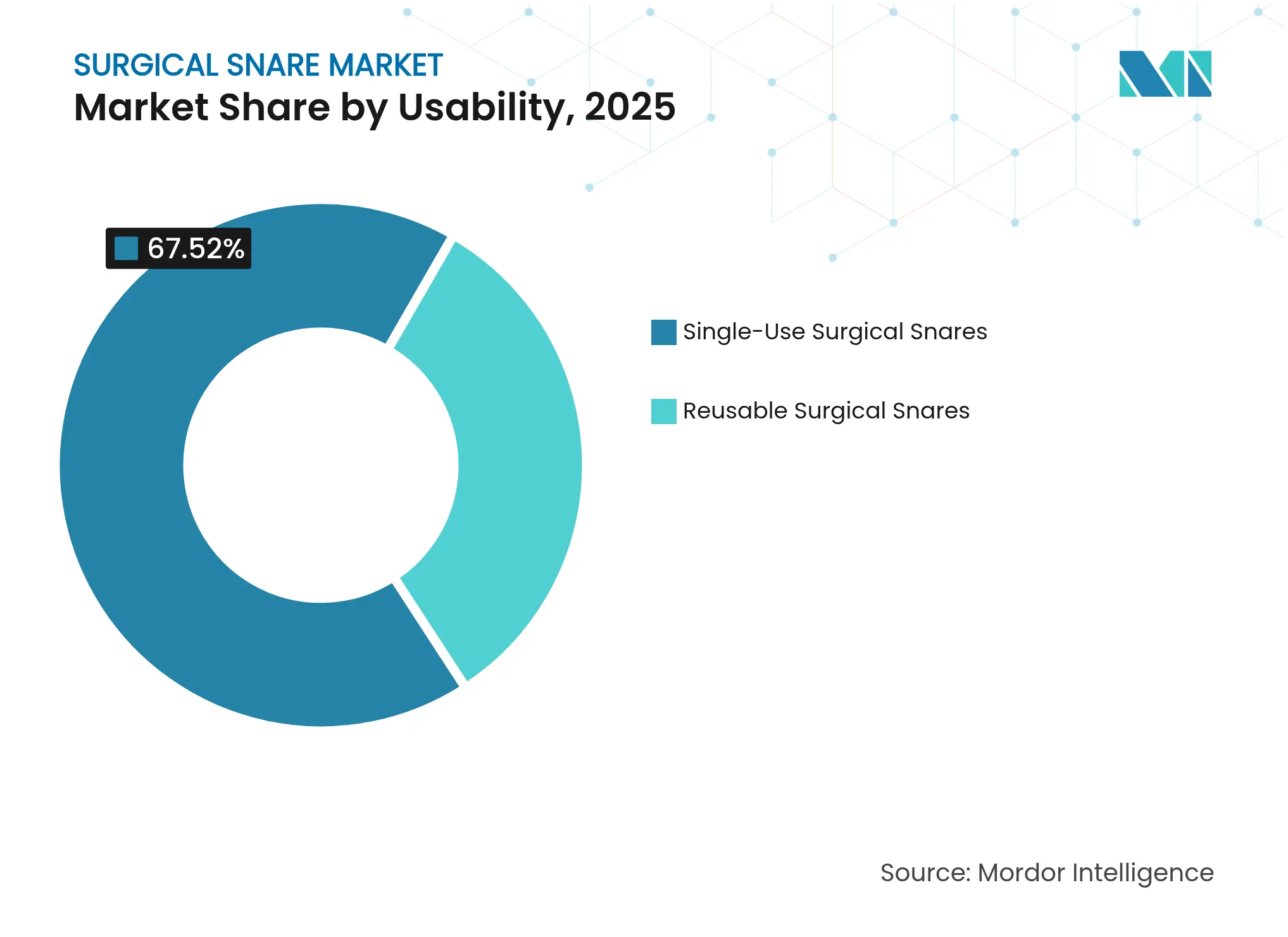

- By usability, single-use devices held 67.52% of the surgical snare market share in 2025; reusable devices lagged as infection-control priorities intensified.

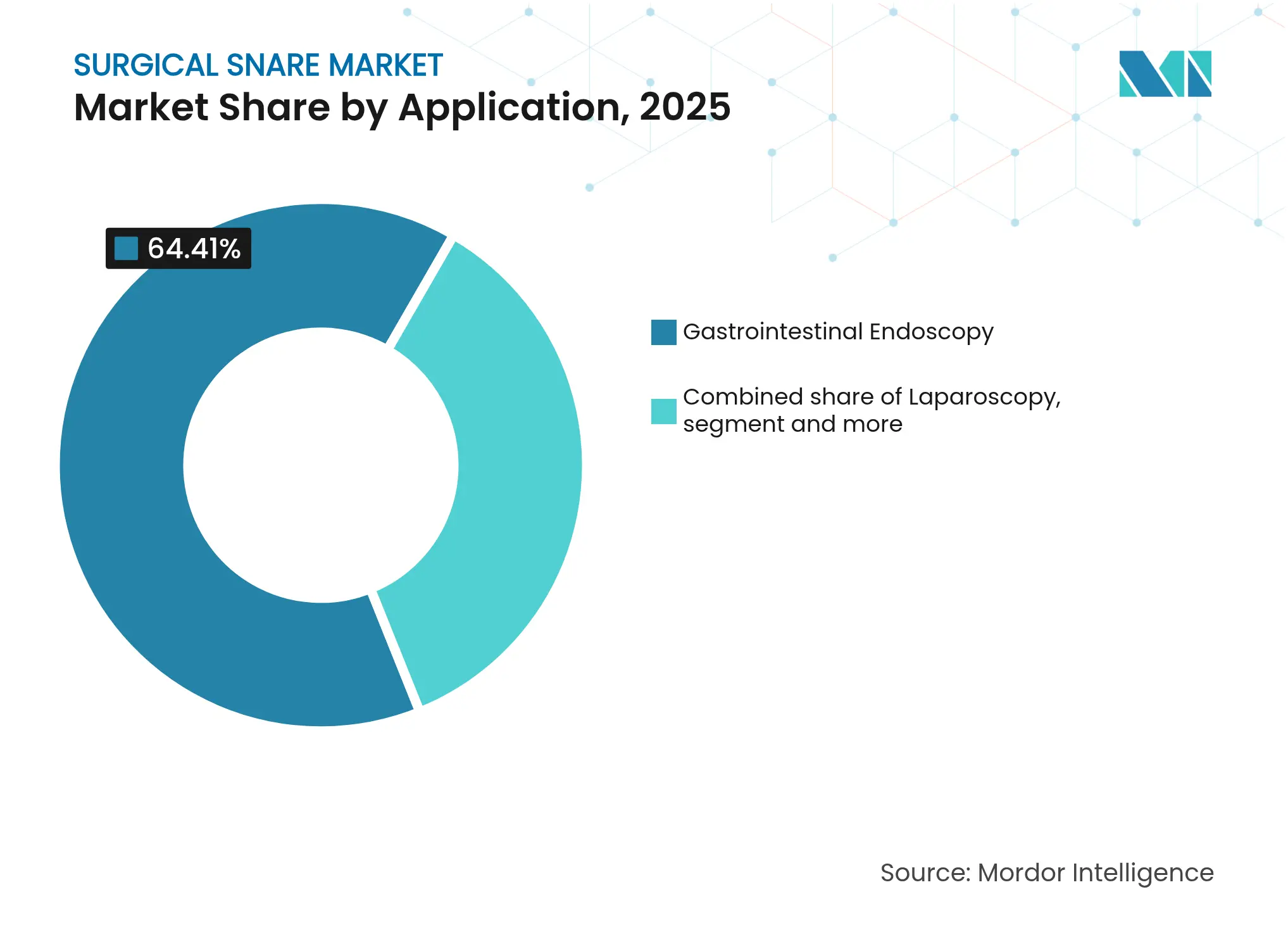

- By application, gastrointestinal endoscopy commanded 64.41% revenue share in 2025, while urology endoscopy is forecast to expand at a 5.03% CAGR through 2031.

- By shape, oval designs led with 40.76% share in 2025; crescent designs are projected to grow at 4.56% CAGR to 2031.

- By end-user, hospitals accounted for 55.98% of 2025 revenue, whereas ASCs are advancing at a 5.20% CAGR on the back of procedure migration.

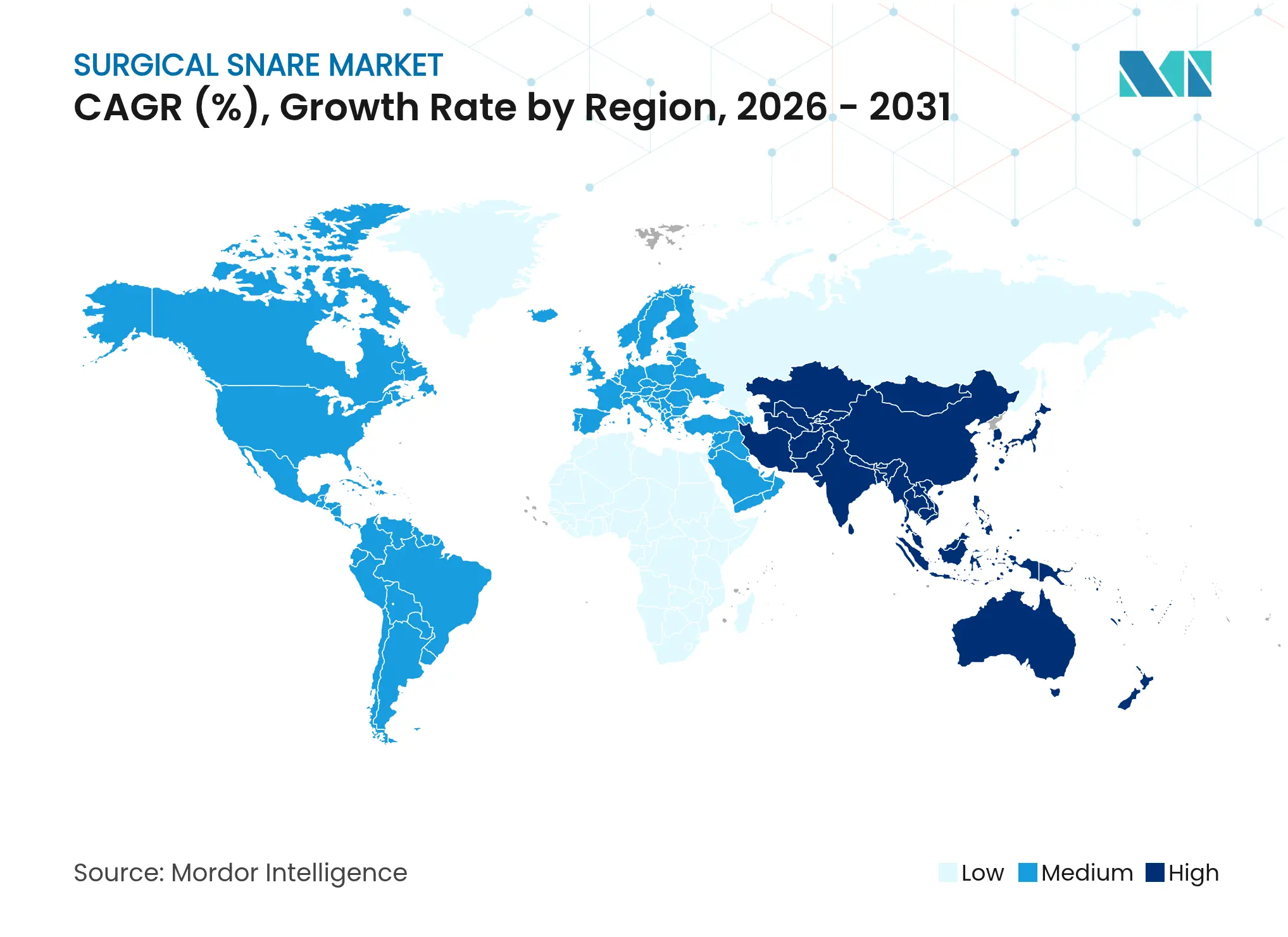

- By geography, North America contributed 42.83% of 2025 revenue; Asia-Pacific is the fastest-growing region at 5.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Snare Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising preference for minimally-invasive surgeries Rising preference for minimally-invasive surgeries | +1.2% | Global, with highest adoption in North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, with highest adoption in North America & Europe | Impact Timeline:Medium term (2-4 years) |

Expansion of endoscopic ambulatory surgery centers Expansion of endoscopic ambulatory surgery centers | +0.8% | North America core, expanding to APAC | Long term (≥ 4 years) | |||

Hospital investments in advanced endoscopy suites Hospital investments in advanced endoscopy suites | +0.6% | Global, concentrated in developed markets | Medium term (2-4 years) | |||

Intensifying colorectal-cancer screening programs Intensifying colorectal-cancer screening programs | +0.9% | Global, with accelerated adoption in APAC | Long term (≥ 4 years) | |||

Increasing adoption of cold-snare polypectomy techniques Increasing adoption of cold-snare polypectomy techniques | +0.4% | North America & Europe, spreading to APAC | Short term (≤ 2 years) | |||

AI-enabled snare devices enhancing detection & resection efficiency AI-enabled snare devices enhancing detection & resection efficiency | +0.5% | Developed markets initially, global expansion | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Preference for Minimally-Invasive Surgeries

Patient demand for faster recovery and lower complication rates is shifting procedural volumes toward endoscopic techniques. Device requirements now emphasize precise tissue capture through small lumens, favoring cold-snare designs compatible with robotic-assisted platforms. Seventeen robotic endoscopy systems remain under development, while nine hold regulatory approval. ASCs leverage this trend to attract cases, forecasting 25% volume growth over the next decade. The preference boosts the surgical snares market as clinicians standardize on single-use snares to secure sterility. Vendors that bundle AI-enabled visualization with snares gain additional traction in value-focused health systems.

Expansion of Endoscopic Ambulatory Surgery Centers

Thirty new gastrointestinal ASCs opened in 2023, illustrating a structural shift away from inpatient settings.[1]Journal of Clinical Medicine, “Global Growth of GI ASCs,” jofcm.org CMS supports site-neutral reimbursement and plans a 2.6% ASC rate update for 2025, raising total payments to USD 7.4 billion. Private-equity funding accelerates network build-out in metropolitan areas, increasing standardized purchasing of disposable snares. Since ASCs emphasize quick turnover and infection control, the single-use segment of the surgical snares market expands faster than the reusable segment. Manufacturers that design procedure-specific kits gain purchasing preference as administrators seek inventory simplification.

Hospital Investments in Advanced Endoscopy Suites

Hospitals upgrade endoscopy infrastructure to protect complex case volumes and meet value-based reimbursement criteria. Micro-Tech launched the EdgeHog Hot Snare in 2025 to improve endoscopic mucosal resection performance. STERIS validated its Exacto Cold Snare, achieving 91% complete resection versus 79% for legacy snares.[2]STERIS, “Exacto Cold Snare Clinical Data,” steris.com These data support premium pricing and strengthen vendor-provider relationships. Investment in 4K imaging and AI decision support further elevates snare performance expectations. Hospitals often lock into long-term supply contracts to secure technology upgrades, stabilizing revenue for leading manufacturers in the surgical snares market.

Intensifying Colorectal-Cancer Screening Programs

Guidelines lowering the screening age to 45 expand eligible populations. Denmark’s participation rate sits at 74.9%, while Bulgaria trails at 6.3%. China relies on community-based risk stratification, and Thailand cites cost as a barrier for 25% of citizens. Device makers that deliver value-engineered snares address emerging-market affordability challenges. FDA clearance of the ColoSense non-invasive test broadens the funnel of patients referred to endoscopy. Growing procedure volumes reinforce long-run demand across the surgical snares market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Post-polypectomy bleeding & perforation risks Post-polypectomy bleeding & perforation risks | -0.3% | Global, with higher impact in developing markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.3% | Geographic Relevance:Global, with higher impact in developing markets | Impact Timeline:Short term (≤ 2 years) |

Reimbursement cuts for GI endoscopy procedures Reimbursement cuts for GI endoscopy procedures | -0.7% | North America & Europe primarily | Medium term (2-4 years) | |||

Stringent approval pathway for single-use devices Stringent approval pathway for single-use devices | -0.4% | Global, with EU MDR creating highest barriers | Long term (≥ 4 years) | |||

Shift toward endoscopic submucosal dissection tools Shift toward endoscopic submucosal dissection tools | -0.2% | APAC leading, gradual adoption elsewhere | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Post-Polypectomy Bleeding and Perforation Risks

Cold snare techniques record 10.8% immediate bleeding compared with 3.2% for hot snare use, though delayed bleeding rates favor cold techniques. Liability exposure therefore influences device selection and training requirements. Regulators intensify clinical-evidence demands, particularly under the European Medical Device Regulation that mandates enhanced safety data. Manufacturers with established surveillance systems and rigorous post-market follow-up capitalize despite the hurdle. Emerging markets feel the risk more acutely due to limited emergency capacity, which moderates short-term uptake in high-volume centers.

Reimbursement Cuts for GI Endoscopy Procedures

Medicare finalized a 2.83% physician fee schedule reduction for 2025, compounding a 33% inflation-adjusted decline over 15 years. Commercial insurers often follow CMS trends, leading providers to constrain device budgets. Some hospitals weigh a return to reusable snares despite infection control benefits of disposables. Conversely, Japan granted reimbursement for AI computer-aided detection in colonoscopy during 2024, indicating that clear clinical benefit can still command premium pricing. Manufacturers that prove efficiency gains and reduce adverse events offset downward reimbursement pressure, sustaining share in the surgical snares market.

Segment Analysis

By Usability: Single-Use Dominance Reshapes Economics

Single-use devices captured 67.52% of the surgical snares market share in 2025. The segment should advance at 4.72% CAGR to 2031 as infection-control mandates override per-procedure cost concerns. Recent contamination incidents involving reusable endoscopes push purchasers toward disposable options. However, rising waste management costs and new European packaging rules effective August 2026 create sustainability pressures on single-use models. Cardinal Health collected 18.3 million single-use items for recycling in 2024, showcasing emerging circular-economy responses.

Reusable snares remain relevant in high-volume centers that operate validated sterilization workflows. These facilities highlight lower lifetime costs compared with the USD 797–USD 4,400 per procedure expense for single-use duodenoscopes. Yet EU Medical Device Regulation compliance raises ongoing testing costs for reusables, narrowing the savings gap. Given the current adoption curve, the surgical snares market size for single-use devices will surpass USD 1.48 billion by 2031, representing a majority of incremental revenue. Providers increasingly demand eco-friendly materials to mitigate landfill impact, prompting vendors to explore biodegradable polymers.

Note: Segment shares of all individual segments available upon report purchase

By Shape: Oval Leadership Faces Crescent Innovation

Oval designs held 40.76% market share in 2025, underscoring physician familiarity and broad lesion applicability. Crescent designs, however, post the fastest 4.56% CAGR to 2031 due to superior capture efficiency in flat lesions and favorable ergonomics in the right colon. Early clinical evidence shows crescent snares improving complete resection rates for lateral spreading tumors. Vendors respond by integrating micro-serrated wire edges to enhance tissue grip.

Specialized shield and hexagonal shapes address niche anatomical scenarios but account for a smaller slice of the surgical snares market. The Exacto Cold Snare’s shield shape yielded 91% complete resection versus 79% for traditional ovals, highlighting the performance boost that shape optimization can deliver. Demand for AI-guided navigation systems could accelerate adoption of shape-specific snares because algorithms prefer devices with predictable curvature profiles. As these innovations mature, the surgical snares market size for crescent designs could reach USD 623 million by 2031.

By Application: GI Endoscopy Dominance Amid Urology Surge

Gastrointestinal endoscopy maintained 64.41% share in 2025, benefiting from guideline-expansion and high global colorectal-cancer incidence. Urology procedures form the fastest-growing application at 5.03% CAGR through 2031, propelled by rising stone disease prevalence and improved 4K visualization such as the camera launched by Olympus in September 2024. Laparoscopy and gynecology contribute steady growth, driven by minimally-invasive adoption across broader surgical indications.

Emerging AI software that identifies bladder lesions or common bile duct stones in real time will further lift demand in non-GI specialties. The surgical snares market size for urology could climb above USD 235 million by 2031 from a low base, diversifying revenue streams for established endoscopy brands. Application-specific snares, such as those optimized for flexible ureteroscopes, amplify competitive differentiation beyond generic GI solutions.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Hospital Leadership Challenged by ASC Growth

Hospitals delivered 55.98% of 2025 revenue due to complex case handling and established procurement contracts. Yet ASCs are projected to grow at a 5.20% CAGR through 2031 as 21% procedure volume migration is expected, totaling 44 million ASC cases by 2034. Specialty clinics focus on selective procedures like inflammatory bowel disease surveillance, preferring single-use snares that simplify inventory.

ASC buyers value standardized kits that shorten turnover times, reinforcing single-use momentum. Vendors that can supply bulk-priced yet premium-featured snares will capture this high-growth channel. Reimbursement parity initiatives and expanding covered procedure codes reinforce the case shift, narrowing cost differentials with hospitals and funneling incremental demand into the surgical snares market.

Geography Analysis

North America led with 42.83% of 2025 revenue, underpinned by mature screening programs, robust ASC infrastructure, and early adoption of AI decision support. Growth through 2031 sits at 4.05% as value-based care rewards high resection completeness and low complication rates. FDA scrutiny following safety recalls prompts providers to favor manufacturers with transparent real-world evidence. The surgical snare market size in North America is expected to exceed USD 905 million by 2031, with single-use penetration topping 75.00%.

Europe presents a sophisticated regulatory environment anchored by the EU Medical Device Regulation. Higher approval costs create competitive moats for compliant suppliers, while environmental policy drives recyclable packaging mandates starting 2026. Germany, France, and the Nordic region continue to invest in AI CADe systems, positioning the surgical snare market for steady 3.96% CAGR despite reimbursement headwinds. Hospitals increasingly sign multiyear strategic agreements to secure evidence-backed snare designs and training services.

Asia-Pacific posts the fastest 5.54% CAGR through 2031 due to infrastructure expansion and screening guideline adoption. China continues to pilot community screening programs, and Japan’s decision to reimburse AI colonoscopy tools in 2024 boosts technology demand. Cost sensitivity persists in Thailand and Indonesia, steering buyers toward value-engineered devices. Local manufacturing partnerships reduce import duties and strengthen regional competitiveness. By 2031, Asia-Pacific could contribute 30.00% of global surgical snare market revenue, narrowing the gap with North America.

Competitive Landscape

Market Concentration

The surgical snare market displays moderate concentration. Olympus, Boston Scientific, and Cook Medical combine long tenures, comprehensive portfolios, and extensive clinical data to defend leadership. Olympus derived 63.8% of its FY 2025 sales, or ¥997.3 billion, from Endoscopic Solutions. Boston Scientific closed acquisitions worth USD 3.7 billion for Axonics and USD 1.26 billion for Silk Road Medical in 2024, signaling an appetite for consolidation that widens barriers to entry.

Emerging differentiation lies in AI-enabled detection, recyclable materials, and shape-specific performance. Mid-tier players such as CONMED and Merit Medical pursue niche indications and regional markets. CONMED posted USD 321.3 million revenue in Q1 2025 and raised full-year outlook on robust endoscopy growth. Karl Storz acquired Asensus Surgical in 2024 to secure robotic capability at USD 0.35 per share. Patent portfolios covering micro-serrated wire and low-friction coatings create tactical defenses against commoditization.

Pricing remains relatively stable as hospitals and ASCs prioritize proven safety over low cost. The 2025 recall of Olympus single-use guide sheath kits after 26 serious injuries underscores the importance of post-market vigilance. Firms that combine design innovation with clinical surveillance are best positioned to expand share. As AI integration and sustainability standards rise, competitive advantage will hinge on meeting both clinical and environmental benchmarks across the surgical snare market.

Surgical Snare Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Olympus acquired Sur Medical SpA, its longstanding Chilean distributor, to establish direct presence in the Chilean market.

- November 2024: American Journal of Gastroenterology published data showing 10.8% immediate bleeding with cold snare polypectomy versus 3.2% with hot snare techniques for pedunculated polyps ≤10 mm.

- May 2024: Videogie reported favorable outcomes for bipolar hot snare polypectomy on intermediate lesions.

- March 2024: STERIS study confirmed Exacto Cold Snare achieved 91% complete resection compared with 79% for conventional snares.

Table of Contents for Surgical Snare Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising preference for minimally-invasive surgeries

- 4.2.2Expansion of endoscopic ambulatory surgery centers

- 4.2.3Hospital investments in advanced endoscopy suites

- 4.2.4Intensifying colorectal-cancer screening programs

- 4.2.5Increasing adoption of cold-snare polypectomy techniques

- 4.2.6AI-enabled snare devices enhancing detection & resection efficiency

- 4.3Market Restraints

- 4.3.1Post-polypectomy bleeding & perforation risks

- 4.3.2Reimbursement cuts for GI endoscopy procedures

- 4.3.3Stringent approval pathway for single-use devices

- 4.3.4Shift toward endoscopic submucosal dissection tools

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Usability

- 5.1.1Reusable Surgical Snares

- 5.1.2Single-Use Surgical Snares

- 5.2By Shape

- 5.2.1Oval

- 5.2.2Crescent

- 5.2.3Hexagonal

- 5.2.4Others

- 5.3By Application

- 5.3.1Gastrointestinal Endoscopy

- 5.3.2Laparoscopy

- 5.3.3Urology Endoscopy

- 5.3.4Gynecology / Obstetrics Endoscopy

- 5.3.5Others

- 5.4By End-User

- 5.4.1Hospitals

- 5.4.2Ambulatory Surgical Centers

- 5.4.3Specialty Clinics

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1Olympus Corporation

- 6.3.2Boston Scientific Corporation

- 6.3.3Cook Medical (Cook Group)

- 6.3.4CONMED Corporation

- 6.3.5Medline Industries

- 6.3.6Medtronic plc

- 6.3.7STERIS plc

- 6.3.8Merit Medical Systems

- 6.3.9HOYA Group – Pentax Medical

- 6.3.10Karl Storz SE & Co. KG

- 6.3.11Micro-Tech Endoscopy

- 6.3.12Endo-Flex GmbH

- 6.3.13Taewoong Medical Co. Ltd

- 6.3.14Medico’s Hirata Inc.

- 6.3.15EMED Endoscopy

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the surgical snare market as all sterile, loop-shaped instruments, manual or electrocautery, that excise polyps, foreign bodies, or abnormal tissue during flexible or rigid endoscopic procedures. The market generated roughly USD 1.67 billion in 2025.

Scope exclusion: retrieval kits engineered exclusively for intravascular capture are outside this study.

Segmentation Overview

- By Usability

- Reusable Surgical Snares

- Single-Use Surgical Snares

- Reusable Surgical Snares

- By Shape

- Oval

- Crescent

- Hexagonal

- Others

- Oval

- By Application

- Gastrointestinal Endoscopy

- Laparoscopy

- Urology Endoscopy

- Gynecology / Obstetrics Endoscopy

- Others

- Gastrointestinal Endoscopy

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Hospitals

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Gastroenterologists, endoscopy nurses, device distributors, and sterile-processing managers across North America, Europe, and Asia shared insights on average selling prices, single-use uptake, and cold-snare protocols. Their feedback validated secondary findings and fine-tuned regional assumptions.

Desk Research

We began with open regulatory sources such as FDA 510(k) clearances, EUDAMED device listings, and Japan's PMDA approvals to map active product codes and launch cadence. Procedure counts from the American Society for Gastrointestinal Endoscopy, OECD Health Data, and the WHO Global Health Observatory anchored baseline utilization. Company 10-Ks, UN Comtrade trade sheets, peer-reviewed articles in PubMed, and procurement notices added volume, price, and channel nuance. Where revenue splits were needed, analysts referenced D&B Hoovers and Dow Jones Factiva. The sources cited here are illustrative rather than exhaustive.

Market-Sizing & Forecasting

A top-down model links annual GI endoscopy volumes, ASC counts, and polypectomy prevalence to a demand pool, which we value with blended ASPs gathered from interviews. Supplier roll-ups act as a bottom-up sense-check, and material gaps are reconciled before totals are frozen. Key variables include colonoscopy rate per 1,000 population, reusable-to-single-use conversion, cold-snare penetration, regional GI disease incidence, and currency trends. Multivariate regression with scenario analysis projects each driver to 2030, after which values are expressed in constant 2024 USD.

Data Validation & Update Cycle

Outputs pass automated variance scans, peer review, and final lead analyst sign-off. Reports refresh yearly, with interim updates for recalls, reimbursement shifts, or major regulatory events. When anomalies surface, the model reopens, assumptions are re-tested, and only then is the estimate released.

Why Mordor's Surgical Snare Baseline Commands Reliability

Benchmark comparison

Published estimates often differ because providers vary scope, pricing basis, and refresh cadence.

Knowing these levers explains the spread.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 1.67 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 1.80 B (2024) | Global Consultancy A | Includes vascular snares and uses retail ASPs | ||

USD 2.27 B (2024) | Industry Journal B | Applies aggressive CAGR to 2024 base without device attrition |