Nasal Spray Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

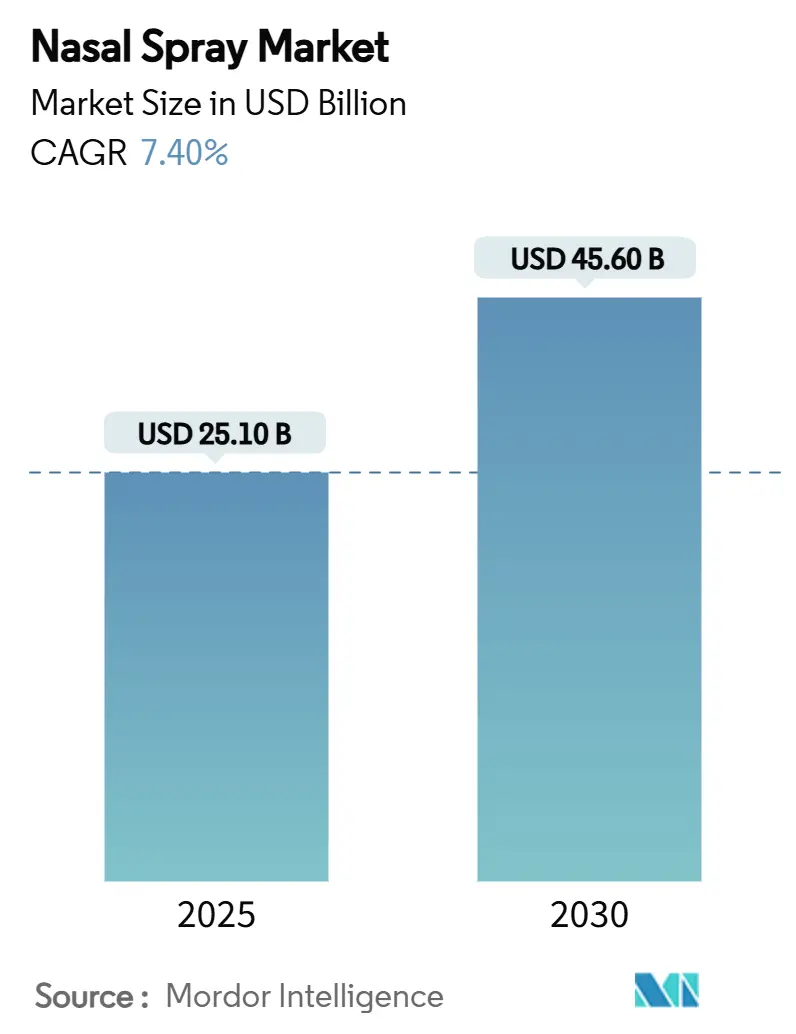

| Market Size (2025) | USD 25.10 Billion |

| Market Size (2030) | USD 45.60 Billion |

| Growth Rate (2025 - 2030) | 7.40% CAGR |

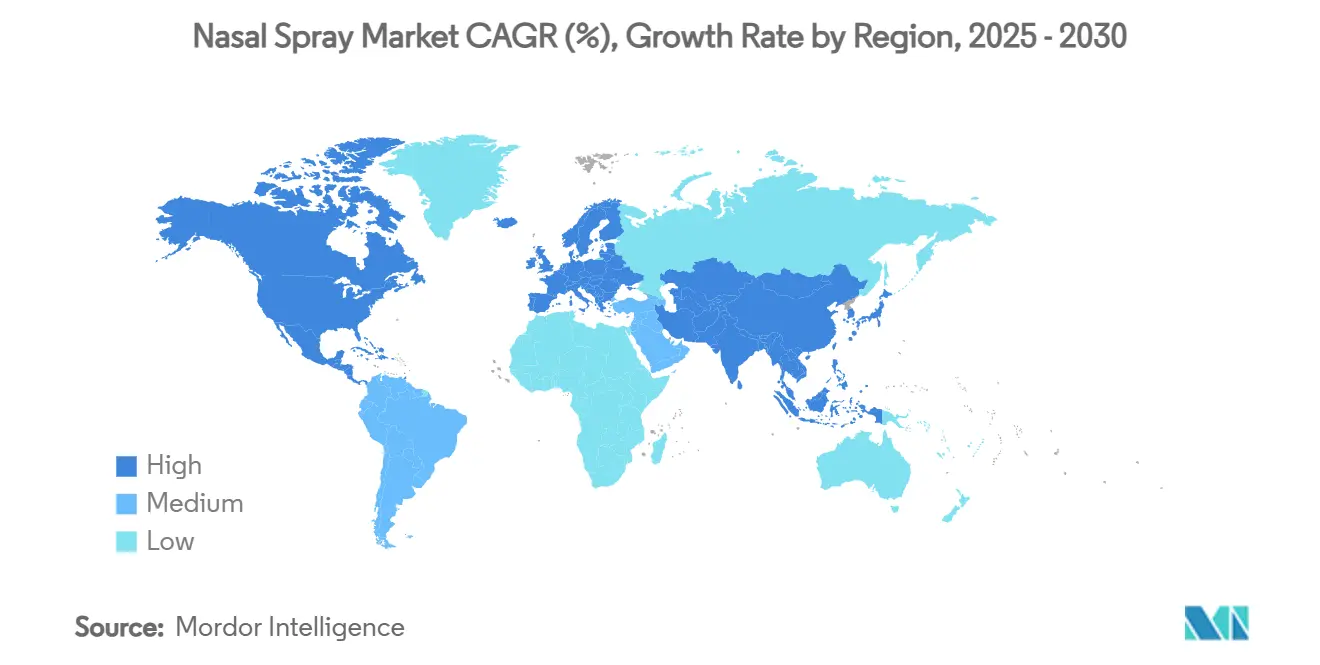

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nasal Spray Market Analysis by Mordor Intelligence

The nasal spray market size stands at USD 25.1 billion in 2025 and is forecast to reach USD 45.6 billion by 2030, translating to a 7.4% CAGR for the review period. Robust demand stems from sustained adoption of non-invasive therapies, steady prescription-to-OTC switches, and a widening pipeline of central-nervous-system (CNS) and emergency-care indications. Steroid sprays remain the revenue cornerstone, yet combination products are accelerating fastest as clinicians seek single-device regimens that improve adherence. Consumer appetite for self-care reinforces OTC dominance, while regulatory approvals for complex agents such as epinephrine and esketamine open higher-value prescription lanes. Distribution patterns mirror omnichannel retailing: brick-and-mortar pharmacies still lead, but rapid e-commerce growth is reshaping last-mile fulfillment and pricing dynamics. Competitive intensity is moderate, with leading brands defending share through line extensions, preservative-free formulations, and greener packaging, while start-ups exploit nose-to-brain delivery and needle-free vaccination niches.

Key Report Takeaways

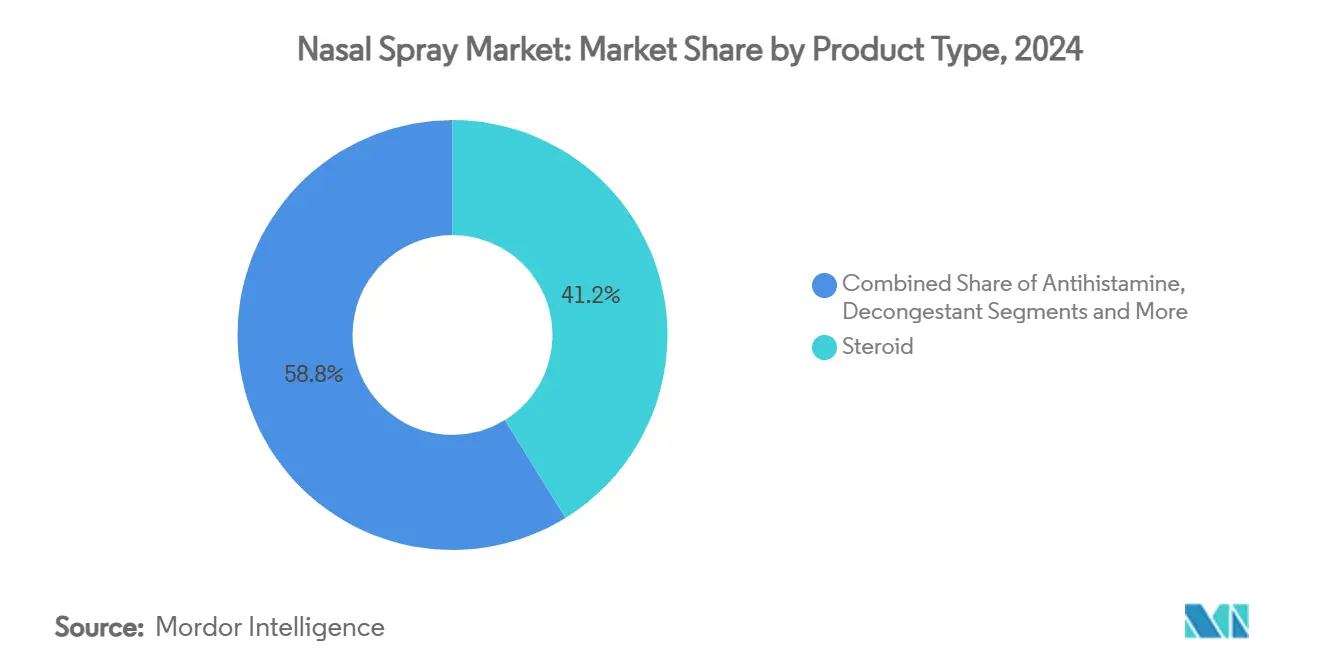

- By product type, steroid sprays captured 41.2% of nasal spray market share in 2024; combination formulations are projected to advance at a 12.0% CAGR through 2030.

- By prescription type, the OTC segment held 64.2% of the nasal spray market size in 2024, whereas prescription products are expanding at 9.3% CAGR to 2030.

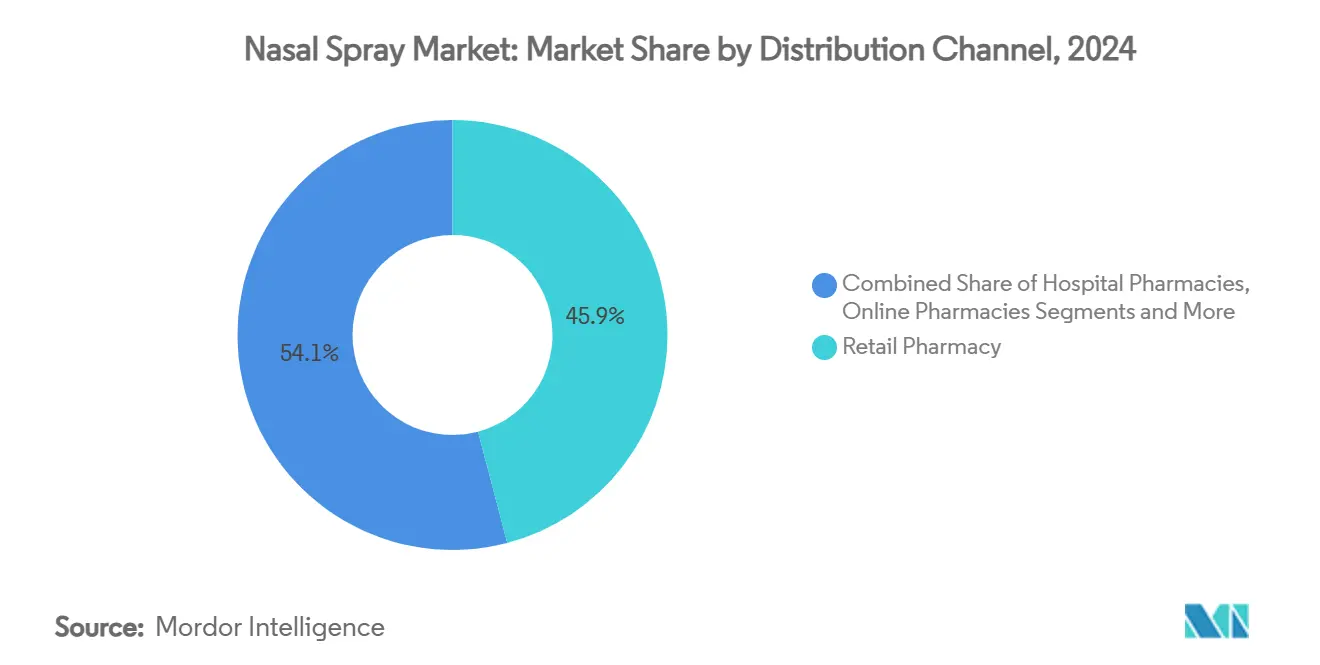

- By distribution channel, retail pharmacies accounted for 45.9% of 2024 revenues; online pharmacies are adding 14.2% CAGR through 2030.

- By geography, North America led with 34.7% revenue share in 2024; Asia–Pacific is growing fastest at 10.9% CAGR.

Global Nasal Spray Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising allergic rhinitis prevalence | +1.80% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Growing self-medication and OTC uptake | +1.50% | Global, faster in Asia–Pacific | Medium term (2–4 years) |

| Expansion of intranasal CNS therapies | +1.20% | North America & EU core | Long term (≥ 4 years) |

| Surge in demand for needle-free vaccination | +1.00% | Global | Medium term (2–4 years) |

| Rapid e-commerce penetration | +0.80% | Global, led by APAC & Latin America | Short term (≤ 2 years) |

| Uptake of preservative-free formulations | +0.60% | North America & EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Allergic Rhinitis

More than 400 million people live with allergic rhinitis, and urban air-quality deterioration amplifies symptom severity, especially where PM2.5 and NO₂ levels exceed WHO limits.[1]Frontiers in Allergy Editorial Team, “Air Pollution and Allergic Rhinitis,” frontiersin.org High unmet need underpins sustained demand for corticosteroid and antihistamine sprays, while combination formulas such as azelastine–fluticasone deliver superior symptom control and shorten rescue-medication use. Pediatric segments remain underserved; allergen-barrier agents are showing favorable efficacy without systemic side effects. Long-term direct medical costs already exceeded USD 11 billion by 2024, confirming the economic magnitude of this chronic indication.

Growing Self-Medication & OTC Uptake

Preference for self-care continues rising as consumers pursue convenience and cost containment. The broader OTC medicines category surpassed USD 40 billion in 2025 and is expanding at 3.5% annually, with Millennials reporting the highest purchase frequency for nasal decongestants and saline rinses. FDA precedent for prescription-to-OTC switches, notably Bayer’s Astepro antihistamine spray, has normalized direct consumer access.[2]U.S. Food and Drug Administration, “Bayer Astepro OTC Approval,” fda.gov Although 61% of shoppers still value in-store pharmacist guidance, one-third of OTC volume is expected online by 2028.

Expansion of Intranasal Drug Delivery for CNS Therapies

Nose-to-brain transport circumvents the blood–brain barrier, enabling rapid onset for neurological agents. FDA clearance of esketamine spray (Spravato) in treatment-resistant depression validated the route. Parkinson’s trials with levodopa sprays have demonstrated improved bioavailability versus oral dosing. Nanoparticle carriers, including borneol-modified lipids, enhance stability and targeting, accelerating pipelines for Alzheimer’s, autism, and anxiety therapies.[3]David P. Skoner, “Azelastine Hydrochloride/Fluticasone Propionate Combination Nasal Spray in Seasonal Allergic Rhinitis: Randomized Trial Results,” International Archives of Allergy and Immunology, pubmed.ncbi.nlm.nih.gov

Surge in Demand for Needle-Free Vaccination Platforms

Public health agencies regard mucosal immunity as essential for respiratory virus control. Nasal vaccines elicit secretory IgA at entry sites and avoid sharps-waste logistics. University research shows that intranasal boosters generate stronger airway immunity than intramuscular comparators. Candidates for influenza, RSV, and future coronaviruses are in late-stage trials, positioning sprays as a mainstay in pandemic preparedness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse Events From Chronic Decongestant Use | -0.90% | Global, with highest impact in developed markets | Short term (≤ 2 years) |

| Stringent Propellant & Plastic Sustainability Rules | -0.70% | EU & North America core, expanding globally | Medium term (2-4 years) |

| OTC Price Erosion From Generics & Store Brands | -0.50% | Global, with acute pressure in North America & Europe | Medium term (2-4 years) |

| Ingredient Scrutiny On Pseudoephedrine & Codeine | -0.40% | North America & EU regulatory focus, spill-over to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse Events from Chronic Decongestant Use

Long-term application of oxymetazoline or xylometazoline can trigger rhinitis medicamentosa, leading to rebound congestion and dependency that dampens repeat volumes. Documentation of severe use disorder cases is prompting tighter usage guidelines and encouraging a pivot toward steroid, antihistamine, and saline alternatives.

Stringent Propellant & Plastic Sustainability Rules

Environmental regulation is tightening around hydrofluorocarbon propellants and single-use plastics. The US Consumer Product Safety Commission proposed phasing out HFC-based aerosol dusters in 2024, while the EU is mandating progressive cuts in global-warming-potential propellant usage. Honeywell’s Solstice Air and Aptar’s metal-free pump designs demonstrate industry responses to cost-intensive compliance requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Steroids Hold the Lead as Combinations Accelerate

Steroid sprays retained 41.2% of 2024 revenue, anchored in robust efficacy for allergic rhinitis and chronic rhinosinusitis. The nasal spray market size for this class is further buoyed by March 2025 FDA clearance of fluticasone propionate (XHANCE) in non-polyp CRS—the first therapy granted for this prevalence-heavy condition. Despite maturity, incremental volume gains stem from preservative-free and low-volume droplet formats that cut leakage and throat-drip complaints.

Combination sprays are climbing fastest at 12.0% CAGR, leveraging dual-mechanism symptom control that shortens time-to-relief. Products pairing olopatadine with mometasone or azelastine with fluticasone illustrate clinically superior performance documented in randomized trials. As guideline bodies increasingly endorse combination first-line therapy for moderate-to-severe disease, the nasal spray market is expected to widen for this premium-priced category.

Antihistamine products benefit from prescription-to-OTC migration, though unit growth is tempered by seasonal spikes. Decongestant sprays face volume pressure tied to dependency concerns and labeling restrictions. Saline and natural-ingredient lines prosper in daily hygiene use cases and pediatric relief, helped by essential-oil-based preservatives that address parental safety expectations. Nano-enabled carriers, such as quercetin-cross-linked chitosan particles, improve mucosal residence time and signal next-wave innovation.

By Prescription Type: OTC Dominance Meets High-Value Prescription Innovation

OTC products controlled 64.2% of the nasal spray market share in 2024, a position safeguarded by mass-merchandiser reach and shopper familiarity. Conversion to OTC continues as sponsors present robust real-world safety dossiers, positioning self-care as the default for mild-to-moderate cases. Meanwhile, digital-first pharmacies expand basket sizes via algorithm-based cross-selling of complementary OTC allergy regimens.

Prescription lines are climbing at 9.3% CAGR, underpinned by approvals of high-acuity agents. The FDA’s August 2024 nod to neffy epinephrine spray, the first needle-free anaphylaxis rescue therapy, exemplifies how specialized formulations can command premium pricing and protected distribution. Payer policies influence uptake; insurers often require steroid trial failure before covering costly combos such as Dymista, prompting cross-border sourcing by U.S. patients at one-quarter domestic prices.

Prescription developers also spotlight preservative-free technology. Stanford University findings confirm acidified saline maintains sterility, guiding pipeline design toward gentler chronic-use profiles.

By Distribution Channel: Retail Strength With Digital Disruption

Retail pharmacies contributed 45.9% of 2024 revenue, leveraging immediate product access and pharmacist counseling on spray technique, a determinant of dose deposition and therapeutic outcome. Hospital pharmacies handle specialized acute indications, notably CNS agents administered under monitoring and emergency stock for anaphylaxis.

E-pharmacy, expanding at 14.2% CAGR, capitalizes on frictionless refills, dynamic pricing, and home delivery. Amazon Pharmacy scales same-day fulfillment in major U.S. metros, while CVS embeds tele-consults for prescription renewals. Quick-commerce operators pilot two-hour delivery for high-turn OTC lines. Regulatory relaxation around electronic prescriptions and secure cold-chain packaging further de-risks remote channels.

Geography Analysis

North America remained the most significant regional contributor with 34.7% revenue share in 2024. The United States anchors the region through frequent FDA approvals of breakthrough sprays such as neffy for anaphylaxis and Zavzpret for migraine, showcasing receptive regulatory pathways. High insurance penetration, clinician familiarity, and strong direct-to-consumer advertising fuel rapid uptake. Canada and Mexico add incremental volume via cross-border trade agreements and expanding universal-care formularies. Distribution sophistication is evident in ARS Pharmaceuticals’ co-promotion with ALK-Abelló, which targets roughly 20,000 U.S. healthcare professionals, illustrating refined go-to-market execution.

Asia–Pacific is the fastest-growing territory at 10.9% CAGR to 2030, propelled by rising disposable income, urbanization-linked allergy incidence, and growing acceptance of nasal vaccination. India’s launch of Bharat Biotech’s iNCOVACC and Glenmark’s FabiSpray underscores regulatory support for novel indications. China, Japan, and Australia represent large addressable bases; ARS Pharmaceuticals already filed for neffy approval across these jurisdictions under licensing alliances . Domestic manufacturers pair cost-advantaged production with region-specific flavors and device ergonomics, widening appeal among local consumers.

Europe posts steady mid-single-digit growth, underpinned by stringent therapeutic and environmental standards that spur early adoption of sustainable packaging. The European Medicines Agency granted EURneffy adrenaline spray eight years of data exclusivity and ten years of market protection in August 2024. Key markets—Germany, France, Italy, Spain, and the United Kingdom—feature mature pharmacy networks and high allergic-rhinitis prevalence. Eco-design mandates accelerate shift to recyclable pumps and low-GWP propellants. Post-Brexit dual-filing requirements have lengthened launch timelines but also created opportunities for specialized regulatory consultancies.

Competitive Landscape

The nasal spray industry exhibits moderate consolidation. The top five players generated close to 50% of global revenue in 2024. GlaxoSmithKline, Bayer, and Viatris leverage legacy brands, wide distributor contracts, and economies of scale to defend incumbency. Bayer’s Astepro OTC switch and Viatris’ generic portfolio diversification typify lifecycle-management tactics.

Emerging companies carve niches by pairing novel APIs with advanced delivery systems. ARS Pharmaceuticals leads needle-free anaphylaxis therapy, having gained both U.S. and EU approvals within one year. Its partnership with ALK-Abelló spreads detailing costs while doubling physician reach. Aptar Pharma, the dominant device supplier, extends its moat through inorganic moves: the USD 12.5 million acquisition of SipNose assets provides proprietary plume-engineering technology that improves nose-to-brain deposition. Furthermore, the January 2025 launch of the first metal-free, fully recyclable pump anticipates eco-regulation and differentiates CMO partnerships.

Patent landscapes feature device and formulation advances rather than novel chemical entities. Applications range from tightly controlled particle-size distributions for improved fluticasone bioavailability to vitamin B12 nutritional sprays targeting deficiency management. Start-ups embracing nanoparticle and liposome carriers aim to secure IP around CNS delivery, where systemic bypass offers clear clinical advantages.

Nasal Spray Industry Leaders

-

GlaxoSmithKline plc

-

Bayer AG

-

Viatris Inc.

-

Bausch Health Companies Inc.

-

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ARS Pharmaceuticals launched neffy (epinephrine nasal spray) 1 mg for pediatric patients 15 kg–<30 kg, broadening non-injection anaphylaxis coverage in the United States.

- March 2025: FDA approved fluticasone propionate (XHANCE) for chronic rhinosinusitis without nasal polyps, the first therapy cleared for this high-prevalence indication.

- January 2025: Aptar Pharma introduced the first metal-free, highly recyclable nasal pump, aligning device performance with evolving sustainability standards.

- December 2024: neffy obtained listing on Express Scripts Commercial National Formularies, improving U.S. reimbursement access.

Global Nasal Spray Market Report Scope

| Steroid Nasal Sprays |

| Antihistamine Nasal Sprays |

| Decongestant Nasal Sprays |

| Saline Nasal Sprays |

| Combination & Others |

| Over-the-Counter (OTC) |

| Prescription (Rx) |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Steroid Nasal Sprays | |

| Antihistamine Nasal Sprays | ||

| Decongestant Nasal Sprays | ||

| Saline Nasal Sprays | ||

| Combination & Others | ||

| By Prescription Type | Over-the-Counter (OTC) | |

| Prescription (Rx) | ||

| By Distribution Channel | Retail Pharmacies | |

| Hospital Pharmacies | ||

| Online Pharmacies | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the nasal spray market?

The nasal spray market size is USD 25 billion in 2025 and is projected to reach USD 45 billion by 2030.

Which product segment leads global sales?

Steroid sprays dominate, holding 41.2% of 2024 revenue.

How fast is the combination-formulation segment growing?

Combination sprays are advancing at a 12.0% CAGR through 2030.

Why is Asia–Pacific considered the fastest-growing region?

Asia–Pacific is expanding at 10.9% CAGR due to rising allergy incidence, broadened healthcare access, and supportive approval pathways.

Which recent regulatory milestone is most transformative?

FDA approval of neffy epinephrine nasal spray introduces the first needle-free emergency treatment for anaphylaxis, opening a new therapeutic category.

How are sustainability mandates influencing device design?

Manufacturers are replacing HFC propellants and adopting metal-free recyclable pumps to comply with stricter environmental regulations, as seen in Aptar Pharma’s 2025 launch.

Page last updated on: