Throat Lozenges Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

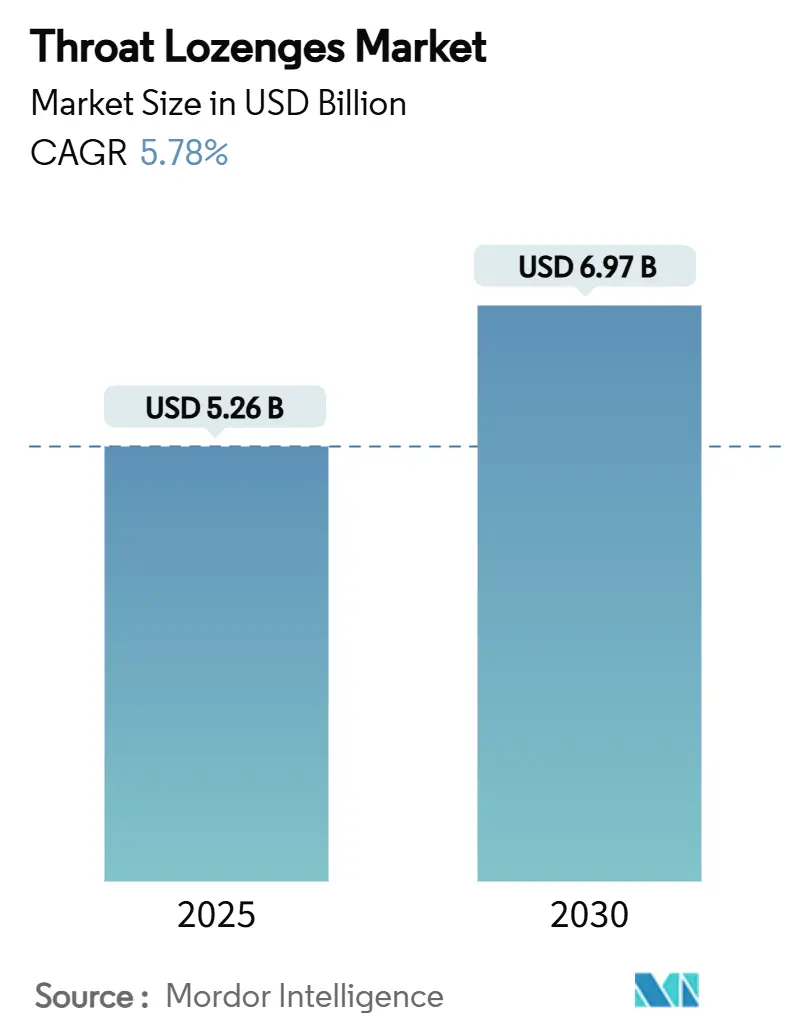

| Market Size (2025) | USD 5.26 Billion |

| Market Size (2030) | USD 6.97 Billion |

| Growth Rate (2025 - 2030) | 5.78% CAGR |

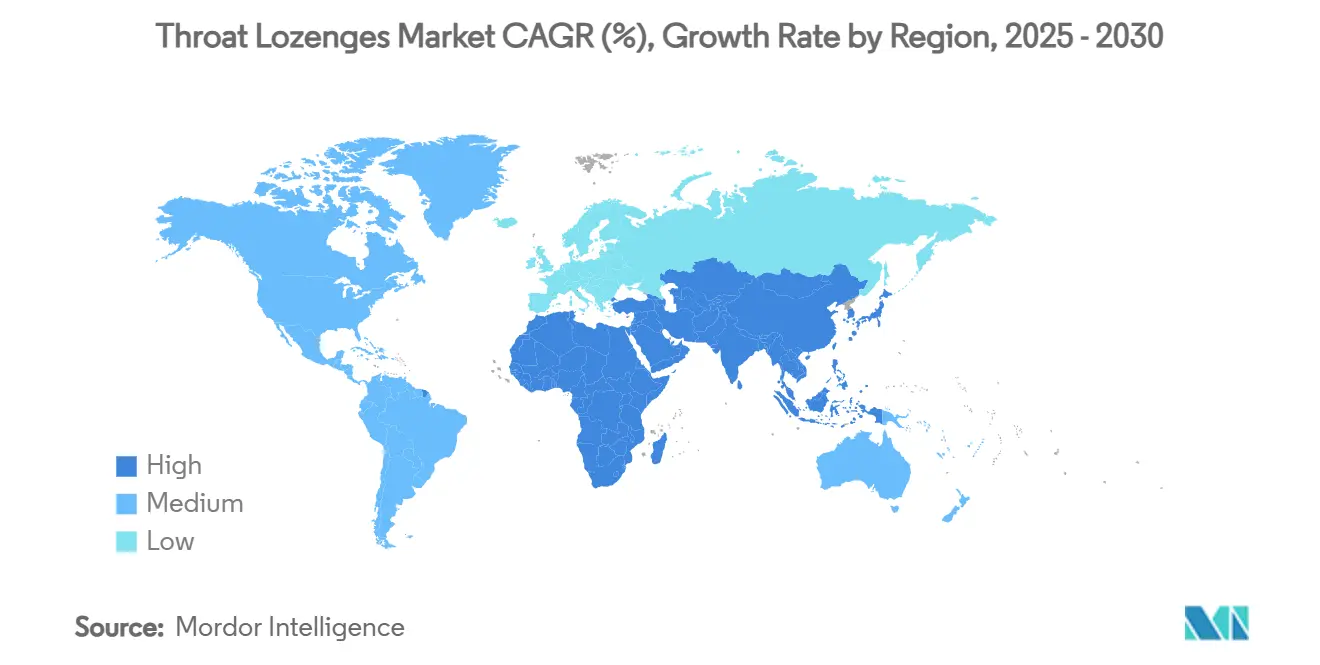

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Throat Lozenges Market Analysis by Mordor Intelligence

The throat lozenges market is valued at USD 5.26 billion in 2025 and is forecast to reach USD 6.97 billion by 2030, expanding at a 5.78% CAGR. The current throat lozenges market size reflects resilience within the wider OTC segment as an aging population, rapid e-commerce adoption, and advances in dissolvable drug-delivery technologies reinforce demand. North America leads with 33.44% share in 2024, yet Asia-Pacific delivers the fastest 7.98% CAGR thanks to rising middle-class healthcare spending. Menthol-eucalyptus and herbal actives compete for ingredient leadership, while sugar-free and diabetic-friendly formulations widen consumer reach. Digital fulfilment models transform impulse-purchase dynamics, and regulatory reform in the United States encourages next-generation OTC formats that bridge convenience with therapeutic precision.[1]U.S. Food and Drug Administration, “MUCINEX INSTASOOTHE SORE THROAT PLUS SOOTHING COMFORT,” fda.gov

Key Report Takeaways

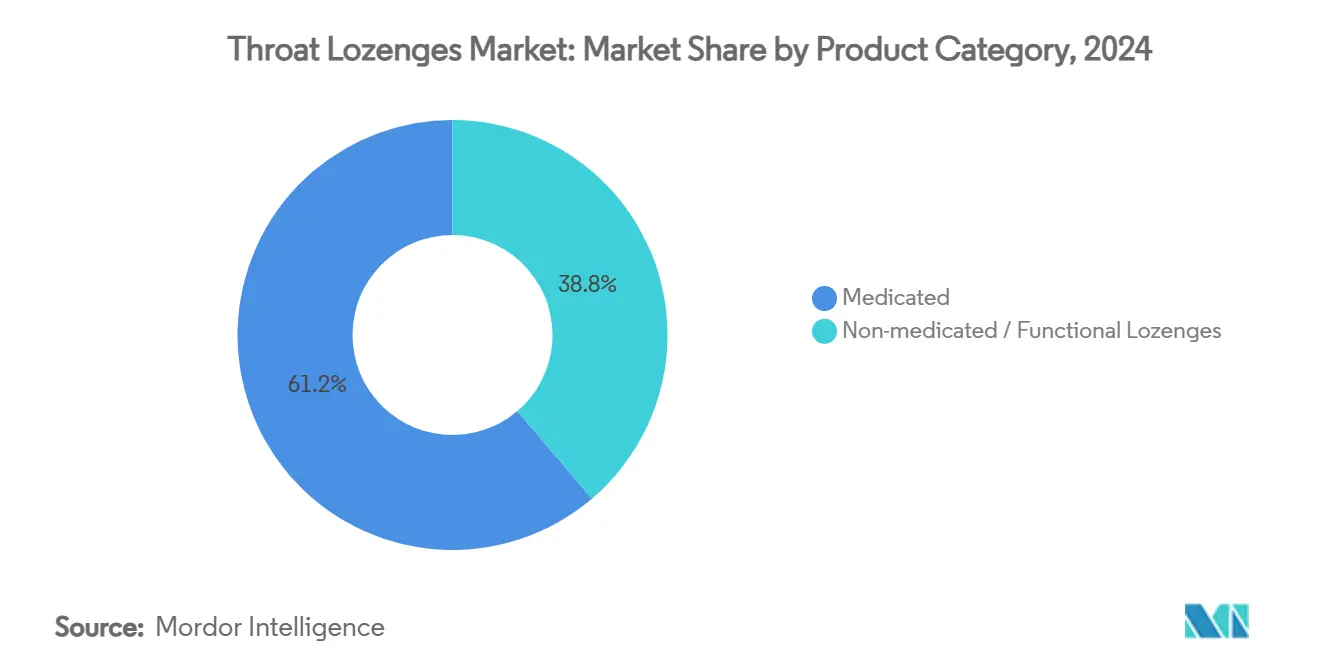

- By product category, medicated lozenges captured 61.23% of throat lozenges market share in 2024, while non-medicated/functional lozenges are poised for the quickest expansion at an 8.49% CAGR through 2030.

- By ingredient type, menthol & eucalyptus held 27.39% of the throat lozenges market size in 2024, whereas herbal actives are set to grow the fastest at 9.56% CAGR between 2025 and 2030.

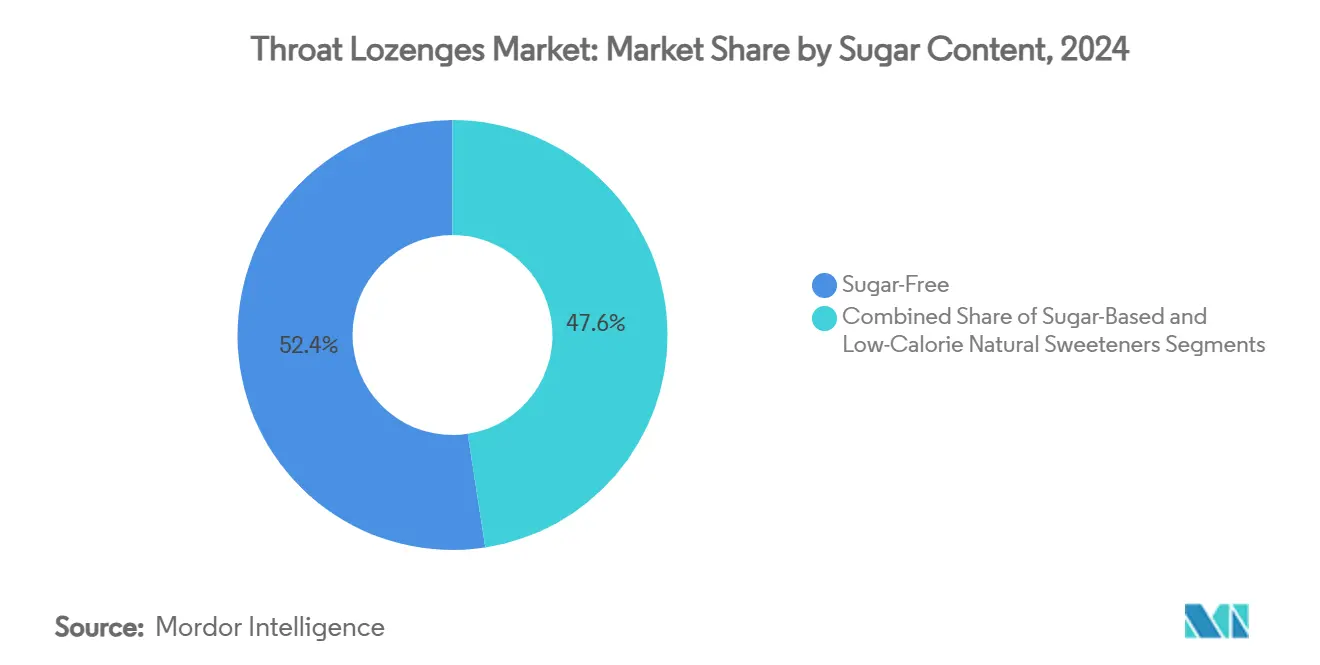

- By sugar content, sugar-free variants commanded 52.44% of throat lozenges market share in 2024 and are projected to rise at an 8.29% CAGR to 2030.

- By distribution channel, pharmacies & drug stores retained 34.72% of the throat lozenges market size in 2024, yet online retail is on track for the highest 9.82% CAGR through 2030.

- By geography, North America led with 33.44% market share in 2024, while Asia-Pacific is forecast to generate the fastest 7.98% CAGR over the same period.

Global Throat Lozenges Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing Global Population & Rising OTC Self-Medication Culture | +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Rapid E-Commerce Penetration For OTC Healthcare | +0.8% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Shift To Sugar-Free & Diabetic-Friendly Lozenges | +0.6% | Global, particularly developed markets | Medium term (2-4 years) |

| Growing Demand For Multifunctional Immune-Boost Lozenges | +0.9% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Nanoparticle-Enabled Fast-Dissolve Actives | +0.4% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Voice-Centric Professions Seeking Prophylactic Throat Care | +0.3% | Global, concentrated in urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Self-Medication Culture

Growth in the throat lozenges market accelerates as people aged over 60 increasingly prefer convenient OTC remedies for common throat discomfort. U.S. census projections indicate a 26% over-60 cohort by 2035, a demographic that historically registers higher self-medication rates. This shift aligns with hospital cost-containment policies that favor preventive care, making lozenges a low-cost intervention for mild pharyngitis episodes. High repeat-purchase intent among seniors further elevates volume demand. Pharmacy-backed guidance assures safety perceptions, reinforcing habit formation among older consumers.[2]Xiang-xing Quan et al., “Patterns of Self-Medication Among Older Adults During COVID-19 in Macao,” BMC Public Health, bmcpubmedcentral.com

Rapid E-Commerce Penetration

Digital pharmacies shorten path-to-purchase, positioning lozenges next to household essentials in the online basket. European regulators now permit verified e-pharmacies to distribute select OTC drugs across borders, expanding reach beyond brick-and-mortar. Same-day delivery services convert occasional buyers into routine purchasers by satisfying impulse needs during sore-throat onset. Brand owners leverage direct-to-consumer storefronts to cross-sell bundled immunity supplements, lifting average order values and strengthening loyalty programs supported by real-time consumer analytics.

Shift to Sugar-Free & Diabetic-Friendly Lozenges

Rising global diabetes prevalence fuels steady uptake of sugar-free variants, which already represent more than half of throat lozenges market sales. Climate-driven sugar price volatility gives manufacturers added cost incentives to reformulate with alternative sweeteners such as stevia or monk-fruit extracts. Pharmaceutical-grade polyols deliver comparable mouth-feel, easing consumer transition. Retailers promote sugar-free SKUs in wellness aisles, fostering premium positioning and enabling brands to command higher unit margins.

Demand for Multifunctional Immune-Boost Lozenges

Post-pandemic routines have normalised year-round immune support, creating interest in lozenges fortified with vitamin C, zinc, and echinacea. Clinical trials confirm botanical blends can reduce chronic pharyngitis symptoms while enhancing patient satisfaction, solidifying medicinal credibility. Brand portfolios now include season-agnostic SKUs marketed for continual throat and immune maintenance, boosting consumption frequency across demographic groups that range from school-age children to voice professionals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Taste & Mouth-Feel Requirements Limiting APIs | -0.7% | Global, particularly developed markets with sophisticated consumers | Medium term (2-4 years) |

| Margin Pressure From Sugar & Menthol Price Volatility | -0.5% | Global, with acute impact in cost-sensitive markets | Short term (≤ 2 years) |

| Rising Scepticism Over Efficacy Of OTC Lozenges | -0.4% | North America & Europe, driven by healthcare professional influence | Medium term (2-4 years) |

| Pushback From ENT Specialists Favouring Sprays / Gargles | -0.3% | Global, concentrated in developed healthcare systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Taste & Mouth-Feel Limitations on APIs

Active ingredients such as benzocaine require aggressive taste-masking to meet consumer palatability expectations. Complex masking techniques add formulation costs and may reduce API loading, moderating clinical efficacy. Regulators demand proof of acceptability in pediatric populations, and negative sensory feedback curbs repeat sales. Emerging platforms like orally disintegrating tablets promise solutions, yet high capital costs restrict adoption among smaller firms.[3]Lara K. Matthews et al., “Efficacy of a Benzocaine Lozenge for Sore Throat,” International Journal of Pharmaceutical Sciences, ijpsjournal.com

Raw-Material Cost Volatility

Global sugar futures and menthol feedstock prices fluctuate sharply in response to climate events and regional supply constraints. Sugar-based brands must decide between passing cost spikes to consumers or eroding margins. Menthol price swings, tied to India’s 70% production dominance, intensify exposure risk. Volatility discourages long-term supply contracts and hampers new-product budgeting, thus dampening near-term throat lozenges market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Medicated Leadership Sustains Therapeutic Trust

Medicated formats generated 61.23% of 2024 revenue, confirming persistent consumer trust in clinically proven formulations. The throat lozenges market size for medicated SKUs is forecast to expand steadily at 5.3% CAGR as multinational brands upgrade delivery systems to nanoparticle oromucosal matrices that heighten API bioavailability. Non-medicated/functional lozenges surge at 8.49% CAGR, capitalising on immunity positioning that broadens usage beyond acute episodes.

Increasing clinical validation of botanicals narrows credibility gaps between categories. Trials on Lactobacillus-based paraprobiotic lozenges show reduced antibiotic reliance in children, signalling convergence of wellness and medical benefits. Brands weave evidence-backed claims into on-pack communication without breaching OTC marketing limits, appealing to health-engaged shoppers seeking everyday preventive solutions.

By Ingredient Type: Herbal Actives Earn Rapid Adoption

The classic menthol-eucalyptus duo still leads with 27.39% share, underpinned by immediate cooling perception and expectorant familiarity. Nonetheless, herbal actives deliver the fastest 9.56% CAGR, anchored by consumer movement toward plant-derived therapeutics. Honey-lemon combinations and antiseptic AMC/DCBA blends compete for niche needs, while benzocaine and hexylresorcinol occupy specialist pain-relief corners.

Anti-inflammatory molecules such as flurbiprofen and benzydamine register high efficacy for post-procedure discomfort, finding favour in hospital settings. Researchers also spotlight octenidine dihydrochloride for superior biofilm disruption against oral pathogens, foreshadowing new entrants that expand the functional range of the throat lozenges market. Manufacturers prioritise transparent labelling of plant species and clinical references to build trust among ingredient-conscious buyers.

By Sugar Content: Health-Conscious Formulation Drives Premiumisation

Sugar-free SKUs already command 52.44% share and will keep outpacing overall category growth. Stevia, erythritol, and isomalt provide non-cariogenic sweetness while maintaining mouth-feel, enabling brands to secure shelf space in diabetic and weight-management aisles. The throat lozenges market share of sugar-free lines is set to widen as reformulation aligns health benefits with raw-material cost hedging. Low-calorie natural sweeteners attract shoppers wanting both botanical and metabolic reassurance, fostering tiered price architectures.

Sugar-based lozenges remain relevant in value niches and cultures favouring traditional taste cues, although manufacturers diversify packaging sizes to minimise sticker shock from sugar price peaks. Hybrid recipes—blending reduced cane sugar with polyols—balance flavour familiarity with caloric moderation, softening transition for legacy consumers.

By Distribution Channel: Digital Fulfilment Rewrites Impulse Dynamics

Pharmacies and drug stores retain authority through pharmacist endorsement, yet online retail emerges as the pivotal 9.82% CAGR growth node. Direct-to-consumer platforms capitalise on search-driven traffic at sore-throat onset, while quick-commerce partnerships deliver within minutes, redefining impulse thresholds. The throat lozenges market size attributable to e-commerce is set to double by 2030 as household-level auto-replenishment programs normalise.

Supermarkets and hypermarkets sustain relevance for bundled family care baskets, whereas convenience stores leverage commuter traffic for grab-and-go packs. Specialty travel retail channels capture premium heritage brands favoured by frequent flyers, cushioning revenue against seasonal cold fluctuations. The omnichannel environment compels manufacturers to synchronise pack graphics, pricing, and promotions across all touchpoints to ensure coherent brand perception.

Geography Analysis

North America’s 33.44% slice of 2024 revenue reflects entrenched self-care culture, widespread health-insurance deductibles that push minor ailment management to OTC, and abundant retail formats. The FDA’s 2025 ACNU ruling simplifies pathway approvals for combo formulas integrating digital adherence aids—opening scope for smart lozenges with dosage-tracking sensors. Reckitt’s USD 200 million expansion in North Carolina augments domestic production resilience, targeting faster replenishment during cold seasons.

Europe occupies the second-largest share, buoyed by consumer affinity for botanical remedies and harmonised herbal monographs that streamline market entry. Regulatory respect for long-standing plant combinations such as thyme-primula supports heritage brands while enabling newcomers to cite official positive opinions. E-pharmacy growth improves access in rural areas, and sugar-free reformulation dovetails with the continent’s stringent nutrition labelling norms.

Asia-Pacific supplies the strongest growth pulse at 7.98% CAGR. China’s oral-probiotics boom and India’s dominant menthol crop position the region as both demand and supply hub. Local manufacturers like Wellona Pharma leverage lower production costs to serve export and domestic markets, while Japanese incumbents nurture premium provenance stories that appeal to health-savvy urban consumers. Rising disposable income and smartphone penetration combine to accelerate digital ordering, compressing traditional distribution hierarchies across the throat lozenges market.

Competitive Landscape

Market structure is moderately fragmented. Global leaders rely on brand legacy, R&D pipelines, and omnichannel distribution to defend territory. Reckitt scales production through facility upgrades and exploits proprietary drug-delivery platforms to widen its medicated lines. Mondelez leverages confectionery heritage to innovate honey-based relief SKUs that straddle wellness and indulgence. Ricola’s 2024 acquisition of a Hero Group plant integrates upstream capacity, tightening control over Swiss herb sourcing and EU logistics.

Technological differentiation is intensifying. Nanoparticle encapsulation promises faster dissolution and targeted mucosal release, while orally disintegrating tablet (ODT) platforms enable multi-API layering. Collaboration between ingredient suppliers and dosage-form engineers shortens commercialisation cycles. Competitive tactics also extend to niche audience targeting: singers, teachers, and call-centre agents receive tailored prophylactic formats with lubricating glycerin bases and voice-friendly flavours.

Consolidation remains likely among mid-tier regional players facing margin pressure from volatile sugar and menthol inputs. Strategic alliances, private-label contracts with large retailers, and shared manufacturing agreements help dilute cost shocks. Intellectual property around novel botanicals or sensor-enabled lozenges offers newer entrants protective moats, signalling a shift from commodity positioning to functional, data-augmented solutions across the throat lozenges market.

Throat Lozenges Industry Leaders

GlaxoSmithKline plc

Reckitt Benckiser Group plc

Mondelez International Inc.

Ricola AG

Procter & Gamble Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Drugs Technical Advisory Board in India approved sales of several OTC medications, including cough lozenges, through neighborhood grocery stores.

- July 2024: Cooper Consumer Health completed the acquisition of Viatris Inc.’s OTC business, broadening its throat-lozenge portfolio and multi-country distribution network.

Global Throat Lozenges Market Report Scope

| Medicated Lozenges |

| Non-medicated / Functional Lozenges |

| Menthol & Eucalyptus |

| Honey & Lemon |

| Antiseptic (AMC & DCBA) |

| Local Anaesthetic (Benzocaine, Hexylresorcinol) |

| Anti-inflammatory (Flurbiprofen, Benzydamine) |

| Herbal Actives (Echinacea, Ginger, Liquorice) |

| Others |

| Sugar-Based |

| Sugar-Free |

| Low-Calorie Natural Sweeteners |

| Pharmacies & Drug Stores |

| Supermarkets & Hypermarkets |

| Convenience Stores |

| Online Retail |

| Other Channels (Duty-Free, Specialty) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Category | Medicated Lozenges | |

| Non-medicated / Functional Lozenges | ||

| By Ingredient Type | Menthol & Eucalyptus | |

| Honey & Lemon | ||

| Antiseptic (AMC & DCBA) | ||

| Local Anaesthetic (Benzocaine, Hexylresorcinol) | ||

| Anti-inflammatory (Flurbiprofen, Benzydamine) | ||

| Herbal Actives (Echinacea, Ginger, Liquorice) | ||

| Others | ||

| By Sugar Content | Sugar-Based | |

| Sugar-Free | ||

| Low-Calorie Natural Sweeteners | ||

| By Distribution Channel | Pharmacies & Drug Stores | |

| Supermarkets & Hypermarkets | ||

| Convenience Stores | ||

| Online Retail | ||

| Other Channels (Duty-Free, Specialty) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current market value of the throat lozenges market?

The throat lozenges market stands at USD 5.26 billion in 2025 and is forecast to hit USD 6.97 billion by 2030 at a 5.78% CAGR.

2. Which product category leads the throat lozenges market?

Medicated lozenges dominate with 61.23% share thanks to strong clinical validation and consumer trust.

3. Why are sugar-free throat lozenges gaining popularity?

Sugar-free lozenges already capture 52.44% share and grow at 8.29% CAGR due to rising diabetes prevalence and consumer demand for healthier sweetening systems.

4. Which region is growing the fastest in the throat lozenges market?

Asia-Pacific records the highest 7.98% CAGR, driven by expanding middle-class healthcare spending and increasing e-commerce access.

5. What are the major restraints impacting growth?

Taste-masking challenges for certain APIs and volatility in sugar and menthol prices can restrict product development and margin stability.

Page last updated on: