Spirometers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

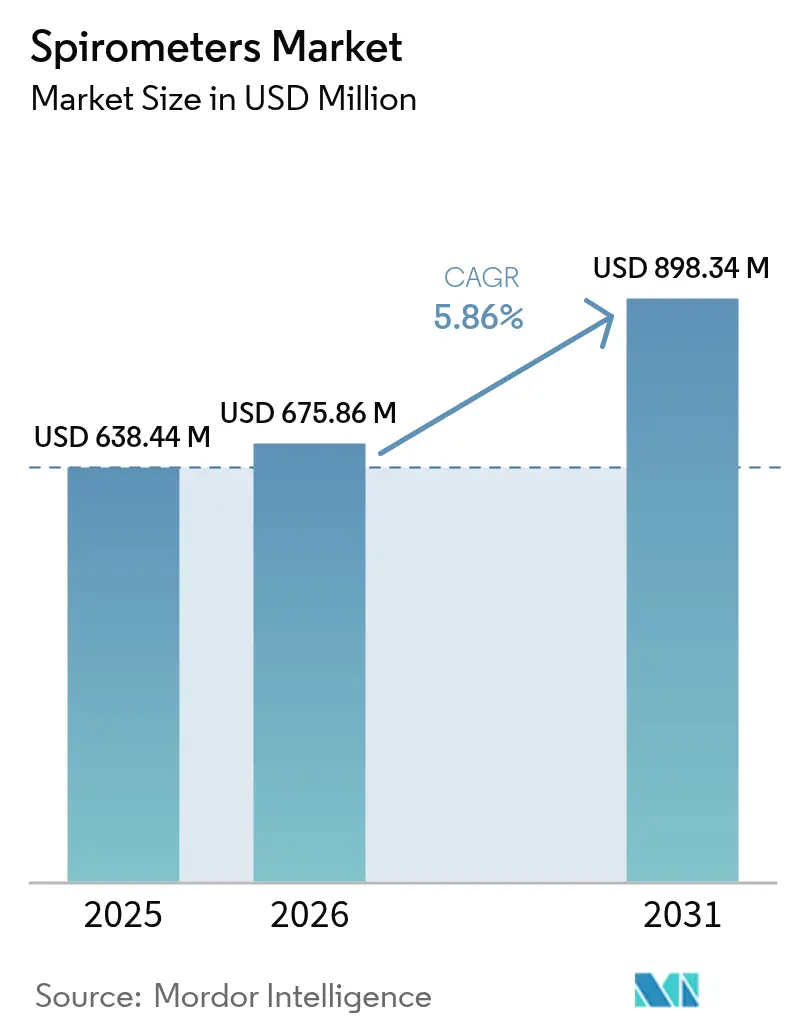

| Market Size (2026) | USD 675.86 Million |

| Market Size (2031) | USD 898.34 Million |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spirometers Market Analysis by Mordor Intelligence

Spirometers Market size in 2026 is estimated at USD 675.86 million, growing from 2025 value of USD 638.44 million with 2031 projections showing USD 898.34 million, growing at 5.86% CAGR over 2026-2031.

The expansion reflects growing respiratory disease prevalence, tighter environmental regulation, and rapid technology adoption in point-of-care and remote settings. COPD’s heavy global burden, tighter PM2.5 limits, and employers’ wellness programs continue to stimulate testing demand. Parallel advances in smartphone-linked micro-spirometers, AI-based analytics, and ultrasonic sensors strengthen clinical confidence while broadening use beyond tertiary hospitals. Strategic acquisitions among established vendors, coupled with new entrants focused on digital health, suggest sustained innovation and orderly competitive maturation.

Key Report Takeaways

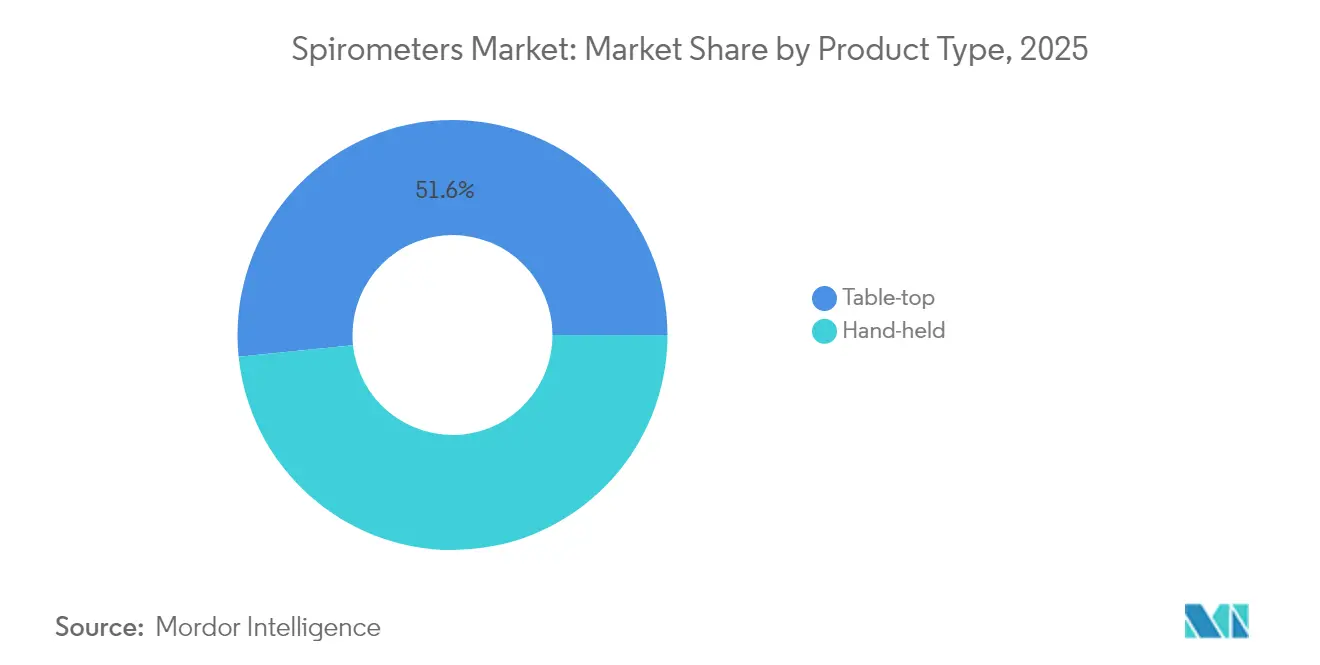

- By product type, table-top systems led with 51.62% revenue share in 2025; hand-held devices are projected to post the fastest 7.71% CAGR through 2031.

- By technology, flow measurement dominated with 53.12% of the spirometers market share in 2025, whereas volume measurement is on track for the highest 10.98% CAGR to 2031.

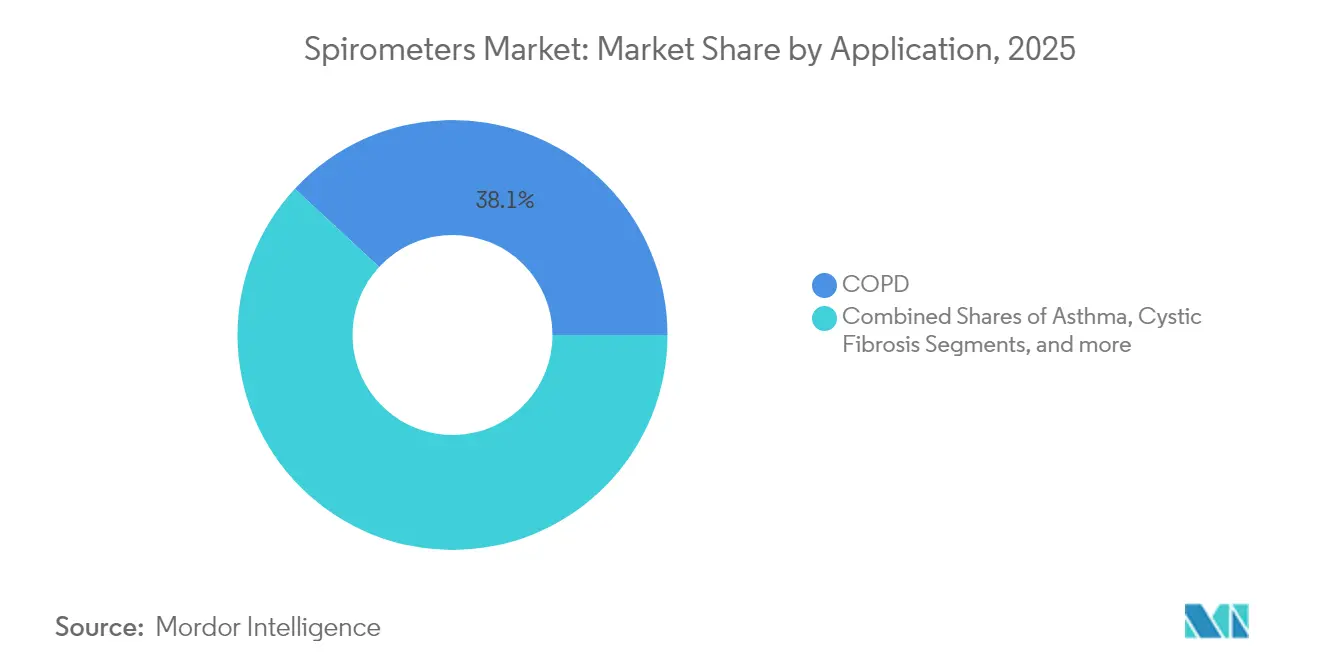

- By application, COPD retained 38.10% share of the spirometers market size in 2025, while asthma monitoring is poised for a 9.31% CAGR through 2031.

- By end-user, hospitals and clinics accounted for 50.62% share in 2025, yet home healthcare will expand at an 7.94% CAGR to 2031.

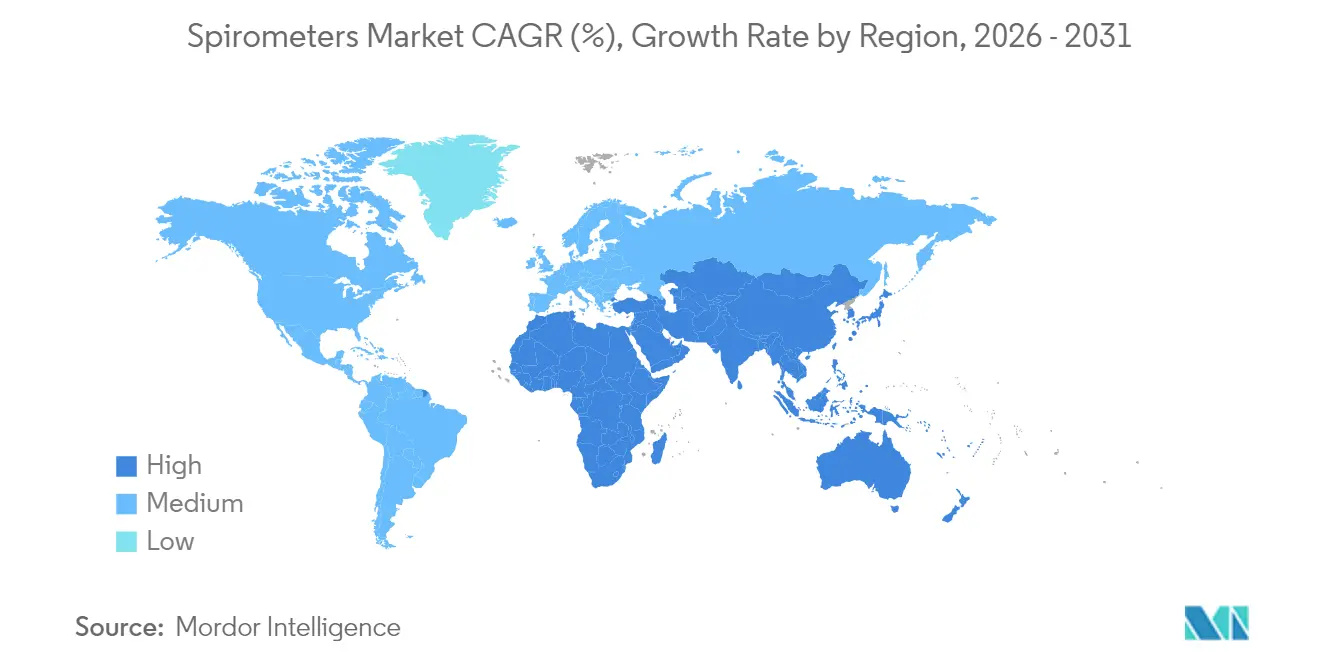

- By geography, North America commanded 37.05% revenue in 2025; Asia-Pacific is forecast to record the quickest 10.89% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spirometers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| COPD prevalence surge in low- & middle-income countries | +1.8% | Global, concentrated in APAC & LAMEA | Long term (≥ 4 years) |

| Ambient-air quality regulation tightening | +1.2% | North America & EU, expanding globally | Medium term (2-4 years) |

| Smartphone-linked micro-spirometers gain clinical acceptance | +1.5% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Employer-funded wellness screening programs | +0.8% | North America & developed APAC markets | Medium term (2-4 years) |

| AI algorithms for remote FEV₁ trending & adherence alerts | +1.3% | Global, technology-forward markets | Short term (≤ 2 years) |

| ESG-driven hospital decarbonisation budgets | +0.7% | Europe & North America, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

COPD prevalence surge drives diagnostic infrastructure expansion

The global COPD patient pool ranges between 213 million and 454 million, with prevalence peaking at 13.1% among adults over 40 in developing economies compared with 8.5% in developed markets. Intensifying exposure to biomass combustion and industrial pollutants magnifies disease incidence and encourages governments to deploy outreach screening. India’s SAVE program screened 15,602 residents and confirmed 1,154 chronic respiratory diagnoses using portable “PFT in a Box” devices, proving the feasibility of large-scale community testing and underscoring latent demand for cost-effective solutions.

Smartphone integration accelerates clinical adoption

FDA clearance of NuvoAir’s Bluetooth-enabled home spirometer in January 2024 validated remote testing workflows. Peer-reviewed trials reported correlation coefficients above 0.994 for FEV1 and 0.993 for FVC versus laboratory reference systems. Real-time data transfer into electronic records shortens decision cycles, and 95% of cystic-fibrosis centers now prescribe home spirometers, with 88% citing quality-of-care gains.

AI-powered analytics transform respiratory care

Machine-learning platforms such as COPDPredict offer automated exacerbation alerts with high sensitivity, supporting preventive intervention.[1]BMJ Publishing Group, “COPDPredict validation study,” bmj.com Respira Labs’ wearable Sylvee device secured Medicare reimbursement for continuous COPD monitoring, pairing acoustic resonance with cloud analytics. These advances re-cast spirometers from diagnostic tools into longitudinal health-management nodes, especially in telehealth ecosystems.

Ambient air quality regulations drive workplace screening

The US EPA trimmed the annual PM2.5 limit to 9.0 µg/m³ in 2024, compelling employers to intensify respiratory surveillance.[2]Federal Register, “National Ambient Air Quality Standards for Particulate Matter; Final Rule,” federalregister.gov OSHA mandates spirometry for workers exposed to 14 hazardous agents, anchoring recurring demand in construction, mining, and chemical industries. Academic evidence linking benzene exposure with impaired lung function strengthens the case for proactive occupational screening.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device inaccuracy due to poor calibration compliance | -1.1% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Reimbursement gaps outside OECD | -0.9% | LAMEA & developing APAC | Long term (≥ 4 years) |

| Shortage of trained respiratory technologists | -0.7% | Global, acute in rural areas | Medium term (2-4 years) |

| Data-privacy concerns around cloud PFT platforms | -0.5% | Europe & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Device calibration challenges undermine clinical confidence

Variability among low-cost turbines erodes diagnostic reliability; some portables drift outside acceptable limits within six months. Ultrasonic sensors remove moving parts and lessen maintenance, but higher price points and regulatory lag defer mass uptake.

Reimbursement disparities limit global market penetration

OECD nations reimburse spirometry under standardized CPT codes, whereas many emerging markets lack structured funding, forcing patients to pay out of pocket.[3]Center for Medicare & Medicaid Services, “Pulmonary Function Testing Codes,” cms.gov The gap dampens uptake where respiratory disease is most prevalent, spurring philanthropic pilots yet underscoring the need for systemic finance reform.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portability Re-shapes Care Delivery

Table-top equipment retained 51.62% revenue in 2025, supported by multi-parameter testing and integration with hospital information systems. Their deep protocol catalog—bronchial challenge, respiratory muscle strength, and diffusing capacity—keeps them essential for pulmonology labs. Nonetheless, hand-held models are set to grow at a 7.71% CAGR, propelled by employer screenings, emergency triage, and home monitoring programs. The performance gap is narrowing; devices like HooHoo posted intraclass correlation scores above 0.887 versus lab reference instruments, satisfying ATS/ERS thresholds. Desktop-PC-attached units serve midsized clinics, marrying analytic software with modest portability.

Demand tilts toward lightweight solutions as reimbursement frameworks embrace remote care, and as clinicians favor quicker throughput. Battery life exceeding 30 hours, Bluetooth 5.0, and disposable mouthpieces align with infection-control mandates. Manufacturers answer with hybrid designs featuring detachable turbine heads, cloud dashboards, and automated acceptability grading. The shift indicates continued migration toward mobility without sacrificing accuracy, steering the spirometers market toward decentralized models.

By Technology: Ultrasonic Volume Sensors Gain Traction

Flow-based systems captured 53.12% of 2025 revenue, favored for real-time loop plotting and affordability. Turbine and Fleisch pneumotach designs dominate primary-care deployments, generating immediate flow-volume curves that underpin guideline-driven interpretation. Yet volume-measurement platforms led by ultrasonic arrays are climbing at an 10.98% CAGR. Their contactless architecture sidesteps condensation and microbial buildup, consequently cutting recalibration needs and boosting longevity.

The spirometers market size for ultrasonic technology is projected to expand as hospitals standardize on low-maintenance capital assets amid staffing constraints. Hybrid devices now combine differential pressure for low-flow accuracy with ultrasonic transit-time at higher ranges, improving linearity. Peak-flow meters keep a niche for pediatric asthma action plans due to simplicity and rock-bottom price. Over the forecast window, sensor miniaturization and AI-embedded firmware will reposition volume measurement as the premium standard, especially in infection-sensitive environments.

By Application: Digital Asthma Management Outpaces COPD

COPD sustained 38.10% share in 2025, cemented by GOLD guidelines that place spirometry at the diagnostic core and by payer policies conditioning inhaler coverage on lung-function confirmation. Employers now integrate spirometry into fit-for-duty exams for high-dust occupations, reinforcing repeat testing volumes. Nevertheless, the asthma segment is slated for a 9.31% CAGR, catalyzed by mobile health apps that gamify adherence and deliver personalized feedback. Randomized trials show home spirometry reduces emergency visits among moderate-to-severe asthmatics, while Bluetooth peak-flow trackers feed action-plan triggers straight to caregivers.

Cystic fibrosis programs leverage early childhood lung-volume indices to adjust antibiotic regimens, and 95% of US CF centers supplied tele-spirometers during the pandemic. Occupational lung disease screening, though smaller, is scaling in mining and ship-building hubs as silica and asbestos standards tighten. As AI combines spirometry with symptom diaries and air-quality feeds, application diversification will reinforce adoption across preventive to chronic-care settings.

By End-User: Home Healthcare Commands Growth Spotlight

Hospitals and clinics generated 50.62% of 2025 revenue thanks to comprehensive pulmonary laboratories and reimbursement alignment. Their dominance persists because complex testing—bronchodilator reversibility, methacholine challenge, and full lung volumes—demands controlled environments and licensed technologists. Yet home-care providers will chart the fastest 7.94% CAGR, buoyed by payers’ remote-patient-monitoring codes and post-discharge care bundles.

Study cohorts show 77% of COPD patients transmit FEV₁ readings on at least 70% of monitored days, enabling algorithmic alerts that reduce rehospitalizations. Diagnostic laboratories remain vital for clinical trials and pre-employment screenings, while ambulatory surgery centers increasingly purchase desktop spirometers for pre-operative risk stratification. The shifting mix underscores broader healthcare decentralization, with spirometers market participants tailoring device connectivity and user interfaces to non-specialist operators.

Geography Analysis

North America commanded 37.05% of 2025 sales, underpinned by Medicare coverage, employer wellness mandates, and early uptake of digital platforms. The U.S. OSHA framework obliges spirometry across 14 hazardous-substance standards, guaranteeing recurrent demand. Canada’s universal health plans reimburse baseline lung tests for smokers over 40, embedding spirometry in primary care. Advanced analytics vendors cluster around Boston and Silicon Valley, accelerating AI tool validation.

Europe follows with sustained investment driven by stringent ambient-air directives and ESG imperatives. The EU’s “Zero Pollution” roadmap and member-state carbon-neutral hospital targets fuel procurement of low-maintenance ultrasonic units. Germany’s DRG system reimburses pre-operative spirometry, while the UK’s NHS Long Term Plan funds remote monitoring pilots for severe asthma. Regional focus on privacy elevates demand for on-premise data-hosting options and GDPR-compliant encryption.

Asia-Pacific represents the growth engine, projected to notch an 10.89% CAGR. India’s SAVE initiative showcased scalable district-level deployments, while China’s Healthy China 2030 blueprint earmarks respiratory disease screening expansion across 3,300 county hospitals. Japan’s aging demographic drives per-capita testing volumes, complemented by government subsidies for home-monitoring kits. Southeast Asian economies experience rising occupational exposure amid construction booms, prompting corporate wellness investments.

Latin America and the Middle East & Africa together form an emerging opportunity frontier. Brazil’s Clean Air Act spawned industrial health audits requiring pulmonary testing, whereas Saudi Arabia’s Vision 2030 mandates employee health screenings in petrochemical corridors. However, fragmented reimbursement and shortages of trained technologists curb near-term penetration. Development banks and NGOs sponsor pilot projects using paper-based or smartphone-assisted devices to bridge accessibility gaps, laying groundwork for future scale-up.

Regulatory Landscape

Spirometers are regulated as medical devices across major markets, with market access shaped by device classification, quality-system compliance, and evidence requirements. In the United States, diagnostic spirometers are classified under FDA 21 CFR 868.1840 as Class II devices, and commercialization typically relies on 510(k) clearance alongside adherence to FDA-recognized consensus standards, including ISO 26782 for spirometry equipment and IEEE 11073-10429 for interoperability. A key compliance milestone is the FDA Quality Management System Regulation (QMSR), effective February 2, 2026, which aligns quality-system expectations more closely with ISO 13485:2016 and raises requirements for design controls, supplier management, and postmarket processes for connected spirometry workflows.

In Europe, spirometers are governed by the EU Medical Device Regulation, Regulation (EU) 2017/745 (MDR), where conformity assessment and notified body capacity are central constraints for manufacturers. The MDR framework was updated through Commission Implementing Regulation (EU) 2026/977, effective May 4, 2026, changing procedural requirements related to conformity assessment operations. With connected home and point-of-care spirometry expanding, regulators are increasing scrutiny of cybersecurity and data handling alongside performance and calibration, making interoperability-aligned and audit-ready quality systems a practical differentiator for tenders and deployments.

Competitive Landscape

The competitive field remains moderately concentrated with a blend of century-old respiratory brands and agile digital specialists. Vitalograph, NDD Medical Technologies, and Vyaire Medical collectively dominate premium clinical markets through validated hardware, global distribution, and deep relationships with pulmonology societies. Vitalograph deepened its software analytics bench by acquiring Morgan Scientific in September 2024, adding enterprise PFT workflow tools. NDD’s EasyOne Air leverages ultrasonic technology to position itself as a low-maintenance alternative in outpatient clinics, while Vyaire continues to refresh its Vyntus platform with cloud dashboards.

Digital disruptors inject competitive dynamism. NuvoAir won FDA clearance for home test kits and partners with payers for COPD remote-care packages. Respira Labs secured Medicare reimbursement for its Sylvee acoustic patch, signaling regulatory appetite for wearable spirometry. Doktorconnect’s May 2025 acquisition of VitalFlo added AI-powered trend analytics and CE-marked IoT hardware, broadening its virtual-care suite. MGC Diagnostics’ Ascent software, cleared by FDA in October 2024, embeds automated ATS/ERS grading and respiratory-exchange ratio analytics, smoothing workflow for pulmonary exercise labs.

Regional specialists remain influential. Shenzhen-based Huirui Medical floods price-sensitive markets with turbine portables, while Japan’s Fukuda Denshi bundles spirometry in integrated cardiopulmonary stations. German startup AioCare taps reimbursement in Poland and Scandinavia for smartphone-linked spirometers. Competition increasingly hinges on software ecosystems, cybersecurity certification, and API openness rather than pure hardware precision, nudging incumbents toward cloud partnerships and subscription business models.

Spirometers Industry Leaders

MGC Diagnostics Corporation

NDD Medical Technologies

KoKo PFT

Koninklijke Philips N.V.

ICU Medical

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Home and decentralized testing is a key whitespace area as connectivity and workflow automation, combined with payer-aligned remote programs, increasingly shape purchase decisions. FDA clearance of NuvoAir's Bluetooth-enabled home spirometer in January 2024 validated remote spirometry workflows in regulated markets, and clinical adoption is visible in care pathways such as cystic fibrosis where home devices are routinely prescribed. The provider and vendor landscape is also moving toward software-driven endpoints and longitudinal monitoring that extend beyond diagnostics, as shown by Strados Labs closing the acquisition of NuvoAir's clinical trial business in March 2026 to offer a combined remote and in-clinic respiratory endpoint suite for decentralized trial designs with standardized data capture and integration.

Regulatory digitization and national screening initiatives further widen commercialization routes beyond traditional pulmonology labs. India introduced mandatory registration for a wide set of notified respiratory medical devices via the CDSCO SUGAM portal, with enforcement activity highlighted in June 2026, which reinforces the need for compliant labeling, traceability, and scalable registration approaches for global suppliers entering price-sensitive regions. In South Korea, including pulmonary function tests in national health screening has supported demand for digital pulmonary function testing solutions, including a March 2026 supply agreement involving Daewoong Pharmaceutical and TR for a digital pulmonary function tester, and a May 2026 partnership with SEERS and TR to integrate digital PFT with smart bedside monitoring for hospital wards. Across these signals, opportunity centers on interoperable, secure, and easy-to-operate spirometry platforms that fit primary care, occupational screening, and hospital ward monitoring workflows, rather than only specialty PFT labs.

Recent Industry Developments

- May 2026: ndd Medical Technologies introduced nddHub at ATS 2026 in Orlando, adding a digital workflow layer to support connected spirometry use cases. The launch highlights the competitive shift toward platform-style offerings where data capture, integration, and usability complement hardware performance.

- May 2025: Doktorconnect acquired VitalFlo, a respiratory-care platform integrating in-office spirometry with remote monitoring and decision support. The deal broadened Doktorconnect's virtual-care suite and pointed to ongoing consolidation around software-enabled spirometry workflows.

- October 2024: MGC Diagnostics received FDA 510(k) clearance for its Ascent cardiorespiratory diagnostic software with automated pulmonary function test interpretation and ATS/ERS grading. This strengthened automated quality checks and interpretation support in clinical environments, helping labs and clinics standardize testing workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of spirometers used to measure lung volumes and airflow in clinical and monitoring settings. We count newly manufactured spirometers sold into hospitals, physician offices, occupational health, and home-care programs, reported in USD.

Scope exclusions: Disposables and consumables, standalone software upgrades, and broader pulmonary function testing systems outside spirometry are excluded.

Segmentation Overview

- By Product Type

- Hand-held

- Table-top

- By Technology

- Volume Measurement

- Flow Measurement

- Peak-flow Meter

- By Application

- Asthma

- COPD

- Cystic Fibrosis

- Occupational Lung Disease

- Other Applications

- By End-User

- Hospitals & Clinics

- Diagnostic Laboratories

- Home Healthcare

- Ambulatory Surgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- APAC

- China

- Japan

- India

- Australia

- South Korea

- Rest of APAC

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand and diagnosis context for spirometry use, then linking it to device adoption. For demand and utilization signals, we rely on public health and utilization sources such as the World Health Organization, the US Centers for Disease Control and Prevention, the US National Institutes of Health, and national health ministries where relevant. We also review peer-reviewed clinical literature on spirometry testing practice and guideline updates, because testing frequency assumptions can shift when care pathways change.

On the supply side, we use company annual reports, investor presentations, regulatory and tender notices where available, and reputable press coverage to map product mix and route to market. Select paid subscriptions for company financials and news help verify revenue splits and corporate actions. Patent databases are used to sanity-check feature cycle timing, since that can affect average selling prices. The examples above are not exhaustive, and other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focuses on how spirometers are purchased and used in real settings, so we interview and survey distributors, hospital procurement and respiratory departments, diagnostic centers, and clinician groups that run testing protocols. For a global view, inputs are balanced across APAC, EMEA, and the Americas to confirm unit demand, replacement cycles, and pricing movement by channel, then to recheck the assumptions built from desk inputs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 39% |

| Mid tier: 58% | Functional/Unit leaders: 41% | EMEA: 37% |

| Smaller Players: 17% | Managers: 46% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built first from a top-down demand pool, where diagnosed respiratory conditions and testing intensity are translated into expected spirometry procedure volumes by setting, and then converted into device demand using replacement cycles and utilization per device. Once that structure is in place, we corroborate the totals with selective bottom-up approximations, including sampled price points by product format (handheld vs tabletop), channel markups from distributor checks, and a sanity roll-up of supplier presence in key countries.

Key inputs used in the model include COPD and asthma prevalence trends, spirometry screening and monitoring frequency, average device life and replacement timing, the mix shift between handheld and tabletop formats, and average selling price movement based on feature updates and procurement type. For forecasting, we run scenario analysis supported by primary input on budget cycles and guideline-driven testing changes, then anchor results to macro health spend direction to reduce reliance on any single-variable extrapolation. When bottom-up inputs are missing in smaller markets, we use proxy adoption rates from comparable healthcare systems, followed by a recheck with regional interview feedback.

Data Validation & Update Cycle

Outputs are validated through multiple checks, where final totals are compared with independent signals such as reported respiratory testing volumes, procurement activity, and observed pricing bands. Large variances trigger a second pass on assumptions, followed by targeted re-contacts with interviewees to confirm whether the change is real or driven by timing, currency, or one-off contracts. Before sign-off, the model and its drivers are reviewed by another analyst to confirm the logic remains consistent across regions and years.

Reports are refreshed annually, and interim updates are done when major events can shift demand or pricing. Before delivery, a final review pass is completed so the latest public releases and recent primary learnings are reflected in the numbers clients receive.

Mordor Intelligence's Spirometers Market Size Versus Other Published Estimates

Published market sizes for spirometers can vary a lot, even when the topic sounds identical at first glance. The differences usually come from what is counted inside the value number, how pricing is converted into USD, and how often the model is refreshed when new signals appear.

In practice, the biggest gap drivers are whether consumables and software are bundled into the market value, whether broader pulmonary function testing platforms are mixed in, and whether price progression is treated as steady or adjusted around procurement and product cycle changes. Currency conversion timing also matters, since a single-year FX choice can move a USD total up or down even if unit demand is stable. By rechecking ASP bands and FX timing during the annual refresh and revalidating outliers with follow-up calls, the value for 2026 stays closer to the actual purchasing reality in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 675.86 M (2026) | |

| Global Research Publisher A | USD 1.00 B (2024) | Uses an earlier base year and appears to include adjacent revenue pools such as consumables and software, which expands the value beyond newly manufactured spirometers only. A longer forecast window also amplifies growth assumptions, making the size look structurally larger versus a device-only definition. |

| Industry Publisher B | USD 1.30 B (2024) | Likely counts devices plus accessories and other add-ons in the same total, and the stated estimation and forecast periods are not fully consistent on the page, which can shift the selected base and growth curve. Regional aggregation and currency timing are not clearly described, so USD conversion choices may widen the spread. |

The comparison shows that scope and timing choices explain most of the spread, more than any single demand driver. Once the value boundary is kept to newly manufactured spirometers and the price and currency steps are made explicit, the estimate becomes easier to trace back to repeatable inputs and to validate with common market signals.

Key Questions Answered in the Report

How big is the Spirometers Market?

The Spirometers Market size is expected to reach USD 675.86 million in 2026 and grow at a CAGR of 5.86% to reach USD 898.34 million by 2031.

Which segment is growing the fastest in the spirometers market?

Hand-held devices show the highest growth with a 7.71% CAGR thanks to their portability and suitability for remote care.

Why is Asia-Pacific considered the growth engine for spirometers?

Expanding healthcare infrastructure, high COPD burden, and large-scale screening programs are driving an 10.89% regional CAGR.

How are smartphone-linked spirometers changing clinical practice?

FDA-cleared portable units transmit real-time data to clinicians, improve patient engagement, and correlate strongly with laboratory-grade devices.

What technological trend is most likely to shape future spirometry?

AI-powered analytics that provide predictive exacerbation alerts and personalized insights are set to transform spirometers into comprehensive respiratory-management platforms.

Page last updated on: