Mycelium-Infused Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

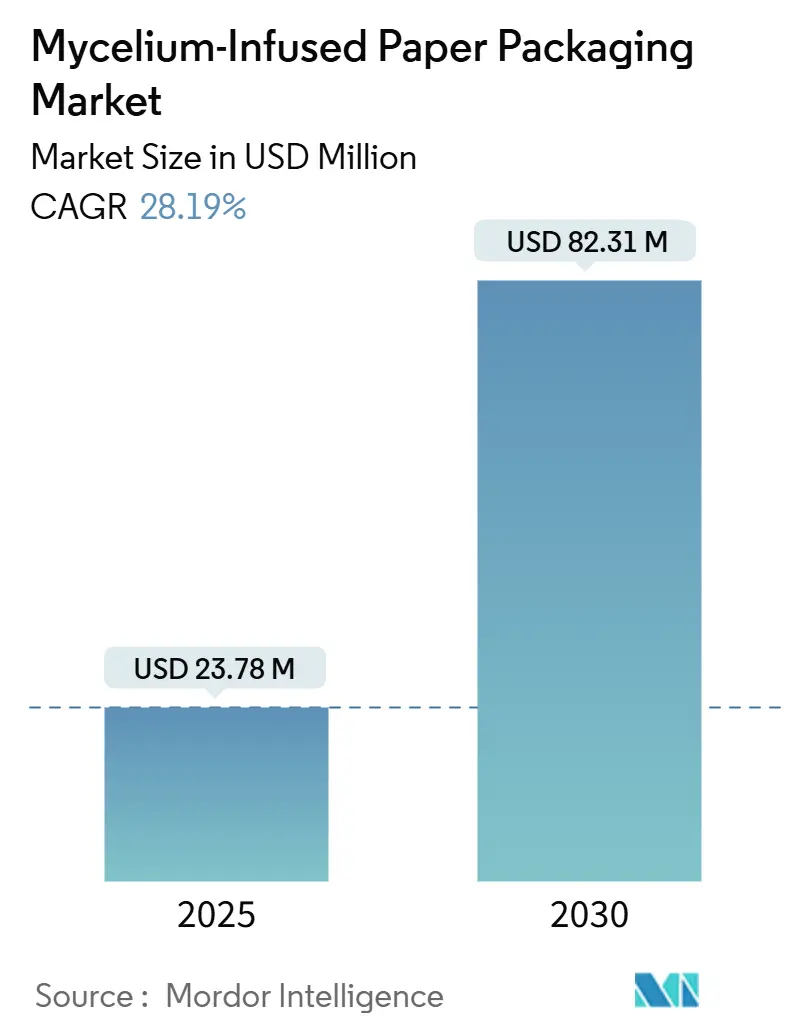

| Market Size (2025) | USD 23.78 Million |

| Market Size (2030) | USD 82.31 Million |

| Growth Rate (2025 - 2030) | 28.19% CAGR |

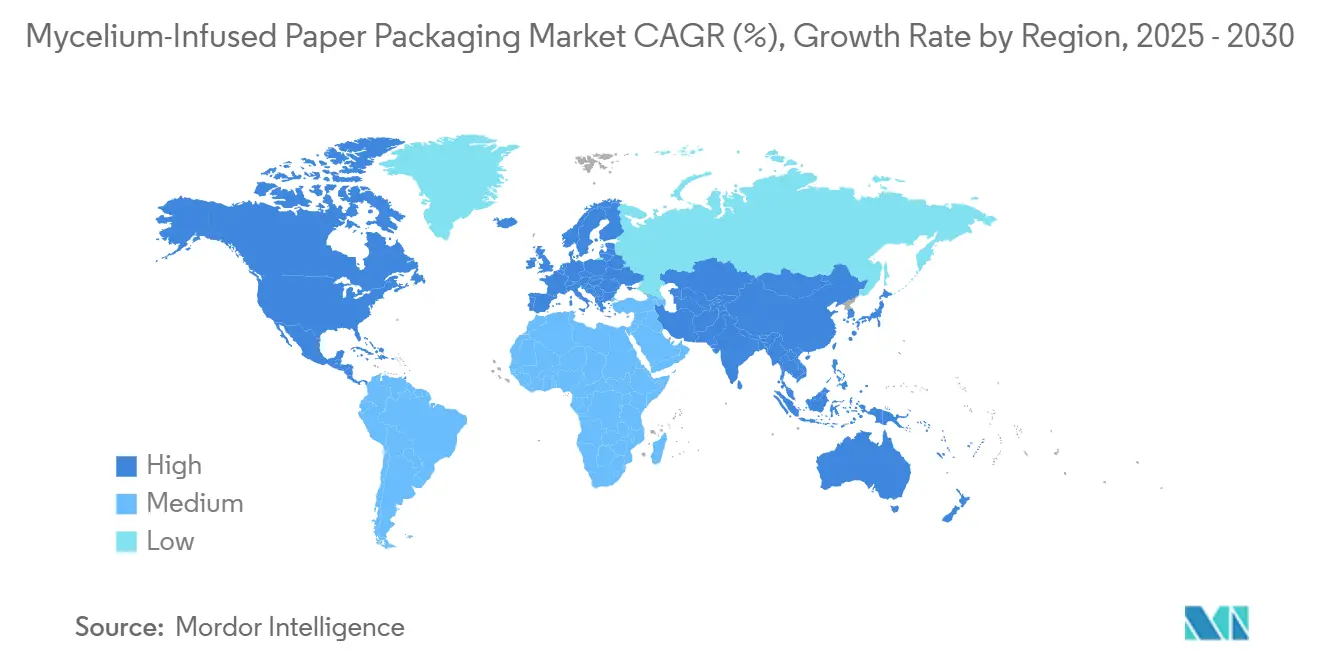

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mycelium-Infused Paper Packaging Market Analysis by Mordor Intelligence

The Mycelium-Infused Paper Packaging market size is USD 23.78 million in 2025 and is forecast to reach USD 82.31 million by 2030, reflecting a 28.19% CAGR. Rapid single-use plastic bans, expanded e-commerce volumes, and corporate net-zero pledges are accelerating the shift from polymer cushions to fully compostable mycelium-paper hybrids. Producers that master enzyme-accelerated growth media are shortening cultivation cycles from weeks to days and achieving near-parity costs with molded EPS, positioning the material for mainstream adoption. Partnerships that up-cycle paper-mill sludge into mycelium substrates simultaneously cut disposal fees and boost circular-economy credentials. Brand owners are demanding clear life-cycle data to comply with the EU Green Claims Directive, favoring suppliers able to certify 30-day biodegradation and soil nutrient return.

Key Report Takeaways

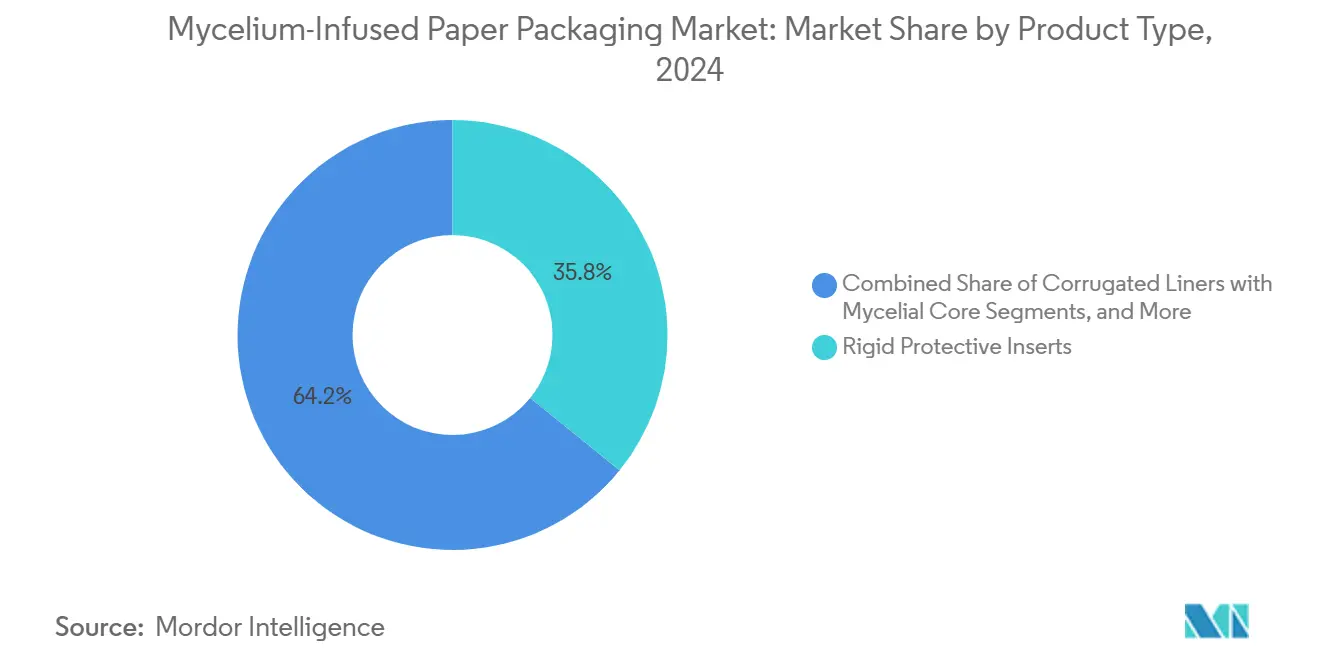

- By product type, the mycelium-infused paper packaging market size for corrugated liners with a mycelial core segment is projected to grow at a 29.43% CAGR between 2025-2030.

- By substrate, hemp hurds captured 30.78% of the mycelium-infused paper packaging market share in 2024.

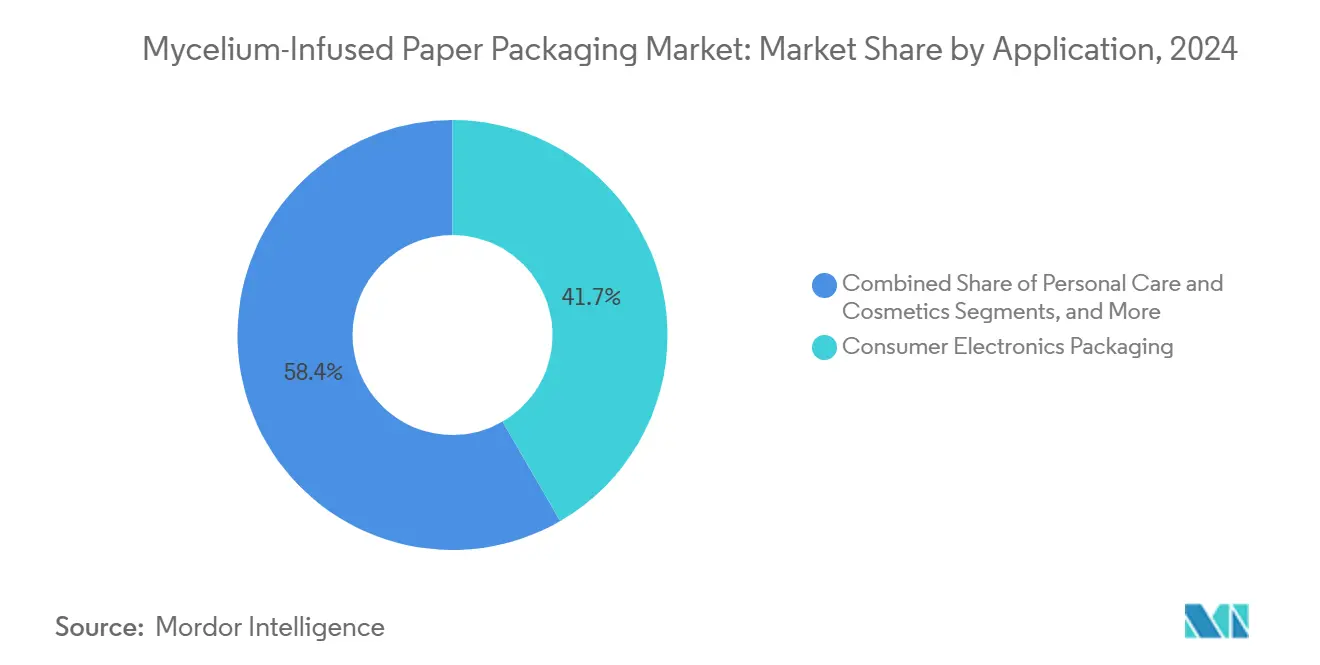

- By application, the mycelium-infused paper packaging market size for the personal care and cosmetics segment is projected to grow at a 29.14% CAGR between 2025-2030.

- By geography, Europe captured 37.96% of the mycelium-infused paper packaging market share in 2024.

Global Mycelium-Infused Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising bans on single-use plastics | +4.2% | Global, early in North America and EU | Short term (≤ 2 years) |

| Corporate net-zero commitments | +3.8% | Global, led by multinationals | Medium term (2-4 years) |

| E-commerce demand for lightweight cushioning | +3.5% | Global, esp. North America, Europe, APAC | Medium term (2-4 years) |

| Cost parity via enzyme-accelerated media | +4.1% | Global biotech hubs | Long term (≥ 4 years) |

| Paper-mill sludge up-cycling | +2.9% | Regions with pulp-paper clusters | Medium term (2-4 years) |

| EU “green claims” directive | +2.7% | Europe with global spillover | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Bans on Single-Use Plastics

Massachusetts outlawed plastic checkout bags in 2025, while California’s SB 54 requires all packaging to be recyclable or compostable by 2032.[1]Massachusetts Senate, “Massachusetts Senate Acts to Ban Plastic Bags,” malegislature.gov Similar measures across Connecticut and Washington are accelerating procurement shifts toward mycelium-infused cushions that decompose within 30 days, reducing landfill load and leachate risk. Because regulatory deadlines leave no buffer for multi-year material trials, retailers are selecting solutions already certified for backyard compostability, positioning the Mycelium-Infused Paper Packaging market for rapid early-mover gains.

Corporate Net-Zero Commitments Driving Eco-Packaging Procurement

Unilever, which reports packaging at 13% of its value-chain emissions, has pledged 100% reusable, recyclable, or compostable formats by 2030 and a 25% cut in virgin plastic by 2028. DS Smith aims to remove 1 billion plastic units by 2025, widening demand for fiber-based cushioning. These commitments embed packaging metrics into ESG scorecards and supplier audits, rewarding vendors able to validate cradle-to-grave carbon savings that the Mycelium-Infused Paper Packaging industry can document through soil-positive end-of-life data.

E-Commerce Demand for Lightweight Protective Cushioning

Dimensional-weight shipping fees make every gram pivotal. Amazon’s fully recyclable padded mailer showed 96.7% repulpability, proving that lightweight, fiber-based pads can replace PE-bubble formats without raising damage rates. Mycelium cushions add shock absorption and antistatic properties vital for tablets and smartphones, aligning with the electronics sector that already drives 41.65% of current demand.

Cost Parity Achieved Through Enzyme-Accelerated Growth Media

Optimized laccase systems now reach 200,900 U/L activity inside 50-liter fermenters in seven days, slashing cycle times and energy costs. Coupled with roll-to-roll growth chambers, producers can output stable panels in under 48 hours, closing the cost gap with molded EPS by 2027. Achieving parity unlocks mass-market SKUs such as TV corner blocks and furniture edge guards, enlarging the Mycelium-Infused Paper Packaging market size exponentially.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scale-up bottlenecks in inoculation and drying lines | -3.2% | Global, limited-infrastructure regions | Short term (≤ 2 years) |

| Variability in mechanical strength by batch | -2.8% | Global, high-spec niches | Medium term (2-4 years) |

| Limited barrier properties vs. polymers | -2.1% | Global, moisture-sensitive uses | Long term (≥ 4 years) |

| Competing cellulose nanofiber foams | -1.9% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scale-Up Bottlenecks in Inoculation and Drying Lines

Transitioning from 50-liter trials to 5,000-liter units often drops enzyme activity below 236 U/g due to shear stress and heat gradients.[2]Reaktor Journal, “Scaling Up of Xylanase Enzyme Production,” undip.ac.id Continuous roll-to-roll inoculation eliminates idle time but demands sterile corridors and inline moisture monitoring, lifting capex above USD 18 million per plant. Smaller entrants face financing hurdles, tempering early capacity growth.

Variability in Mechanical Strength Across Substrate Batches

Changes in pH, fiber length, and nutrient load can swing compressive strength by 15%, risking electronics returns. Genetic strain screening and digital-twin process control are narrowing tolerances, yet multi-supplier agricultural residues still inject variability. OEMs in automotive and aerospace remain cautious until 6-sigma consistency is proven at industrial scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protecting Fragile Goods with Bio-Foam Precision

Rigid protective inserts accounted for 35.84% of 2024 revenue. Electronics OEMs specify drop-test compliance that these molded forms deliver through tailored density gradients. Corrugated liners with mycelial cores are outpacing all other SKUs at 29.43% CAGR, riding e-commerce demand for flat-pack cushioning that ships collapsed then springs into honeycomb stiffness. Mycelium-infused paper packaging market size contributions from these two SKUs together will exceed USD 55 million by 2030.

Flexible wraps and pads trail but benefit from roll-to-roll growth breakthroughs, enabling 300 meter output reels that fit existing paper-pack lines. Overwrap-ready foams suit irregular furniture parts where cut-to-length economy matters. Adoption remains niche until cycle-time parity is reached with PE air pillows.

By Substrate Material: Hemp Consistency vs. Sludge Circularity

Hemp hurds led 2024 volume at 30.78% thanks to consistent fiber morphology that fosters even mycelial colonization. Stable supply contracts in Canada and France underpin predictable pricing, critical for large FMCG buyers. Paper-pulp sludge is scaling fastest at 29.27% CAGR as mills seek zero-waste status. Mycelium-Infused Paper Packaging market share gains here could approach 20% by 2030 once sludge dewatering logistics mature.

Agricultural residues such as straw and corn stover provide seasonal cost advantages but exhibit wider compositional swings, demanding tighter process windows. Sawdust continues largely regional, tied to forestry clusters, while coffee chaff and rice husk offer branding stories despite volume constraints.

By Application: Electronics First, Beauty Rising

Consumer electronics absorbed 41.65% of 2024 shipments, supported by anti-static treatments and form-fit cavities that replace PE foam corners. The Mycelium-Infused Paper Packaging market size for electronics inserts is forecast to widen at 27% CAGR through 2030 as smartphone and wearables units climb. Personal care and cosmetics lead growth at 29.14% CAGR; premium brands favor artisan textures that underscore natural positioning on retail shelves.

Food-and-beverage usage focuses on dry snacks and tea tins, sidestepping moisture-barrier gaps while securing compost-friendly selling points. Home-furnishing makers adopt custom molds for chair legs and artwork frames in low-volume lines where tooling agility offsets higher per-piece costs.

Geography Analysis

Europe accounted for 37.96% of global sales in 2024 under the impetus of the EU Packaging Waste Regulation and Green Claims Directive that elevate verified bio-solutions.[3]European Parliament, “Packaging and Packaging Waste Texts Adopted,” europarl.europa.eu Germany, the Netherlands, and France host dozens of pilot plants colocated with kraft mills, reducing substrate haulage. North America follows, propelled by state plastics bans and tech-sector sustainability targets led by California and Massachusetts laws.

Asia-Pacific is expanding fastest at 29.36% CAGR. China’s 2025 plastics law and Japan’s semiconductor export base drive demand, while regional venture capital funds bankroll production clusters near Shenzhen and Osaka. South Korea’s electronics exporters pilot mycelium inserts for OLED panels, pointing to mainstream uptake by 2027. Latin America and the Middle East remain nascent but signal potential via circular-economy mandates in Chile and the UAE.

Competitive Landscape

The field is fragmented: the top five players control roughly 20% of revenue. Ecovative’s AirMycelium platform lifted capacity following a USD 28 million raise in 2024, targeting multi-industry rollouts. DS Smith, Stora Enso, and Mondi embed mycelium R&D into existing corrugate assets, leveraging scale to secure early-stage brand trials.

Start-ups focus on enzyme engineering, while converters experiment with hybrid lamination to meet moisture-barrier specs. FDA GRAS clearance for mushroom-derived chitosan unlocks antimicrobial liners for food contact, granting portfolio breadth. Strategic alliances are forming: Tarkett partners with Mycocycle to valorize flooring waste by 2026, illustrating cross-sector diversification.

Mycelium-Infused Paper Packaging Industry Leaders

Ecovative LLC

Magical Mushroom Company Ltd.

Grown Bio B.V.

Mushroom Packaging LLC

Mycotech Lab (MYCL)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Stora Enso reports EUR 175 million (USD 189 million) Q1 EBIT, citing renewable-packaging investments.

- February 2025: EU Packaging and Packaging Waste Regulation enters force, mandating recyclability grades by 2030.

- October 2024: AlterPacks secures USD 1.6 million to up-cycle spent grains into rigid packaging.

- September 2024: Ecovative raises USD 28 million to scale AirLoom hides and protective inserts.

- June 2024: Tarkett partners with Mycocycle to convert construction waste into mycelium-based flooring additives.

Global Mycelium-Infused Paper Packaging Market Report Scope

| Rigid Protective Inserts |

| Molded Pulp and Mycelium Hybrids |

| Corrugated Liners with Mycelial Core |

| Flexible Wraps and Pads |

| Hemp Hurds |

| Agricultural Residues (straw, corn stover) |

| Sawdust and Wood Chips |

| Paper-pulp Sludge |

| Others (coffee chaff, rice husk) |

| Consumer Electronics Packaging |

| Food and Beverage Containers |

| Cosmetics and Personal Care |

| Home and Furniture |

| Industrial Components and Auto Parts |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Rigid Protective Inserts | ||

| Molded Pulp and Mycelium Hybrids | |||

| Corrugated Liners with Mycelial Core | |||

| Flexible Wraps and Pads | |||

| By Substrate Material | Hemp Hurds | ||

| Agricultural Residues (straw, corn stover) | |||

| Sawdust and Wood Chips | |||

| Paper-pulp Sludge | |||

| Others (coffee chaff, rice husk) | |||

| By Application | Consumer Electronics Packaging | ||

| Food and Beverage Containers | |||

| Cosmetics and Personal Care | |||

| Home and Furniture | |||

| Industrial Components and Auto Parts | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Thailand | |||

| Indonesia | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Mycelium-Infused Paper Packaging market?

The market is worth USD 23.78 million in 2025.

How fast is the Mycelium-Infused Paper Packaging market expected to grow?

It is projected to expand at a 28.19% CAGR between 2025 and 2030.

Which product segment holds the largest share today?

Rigid protective inserts lead with 35.84% of 2024 revenue.

Which region is growing the fastest?

Asia-Pacific is forecast to post a 29.36% CAGR through 2030.

What is the main barrier to broader adoption?

Scaling inoculation and drying lines without quality loss remains the top operational constraint.

Page last updated on: