Italy Paper Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

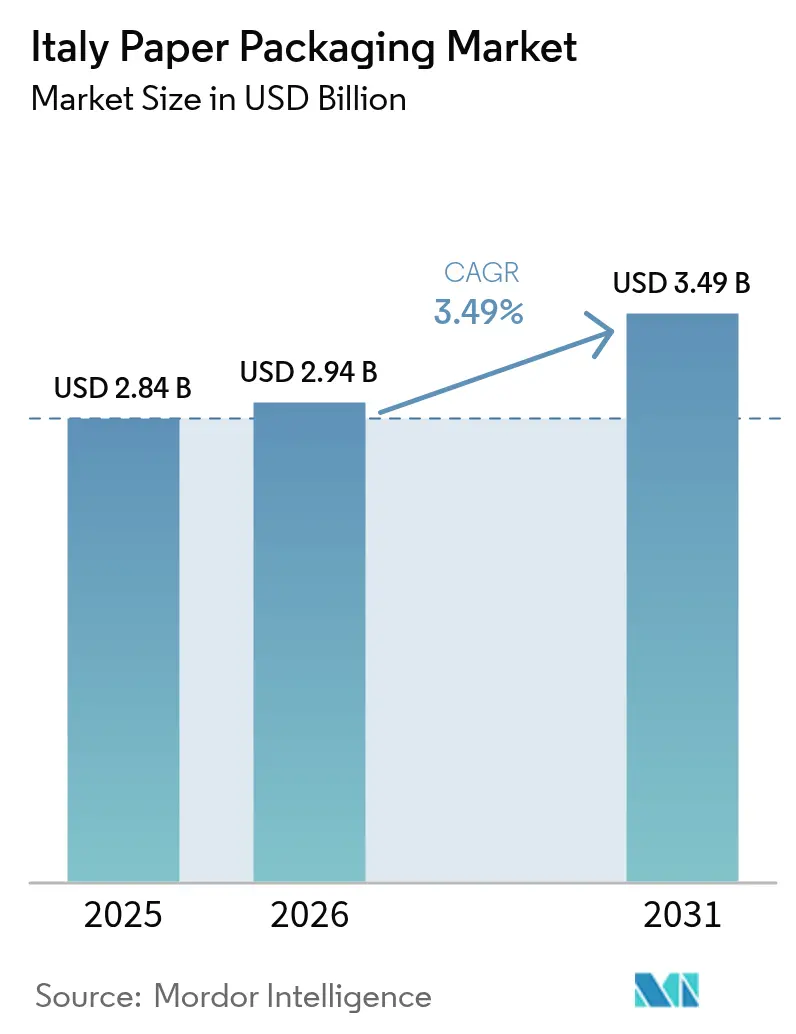

| Base Year Market Size (2025) | USD 2.84 Billion |

| Market Size (2026) | USD 2.94 Billion |

| Market Size (2031) | USD 3.49 Billion |

| Growth Rate (2026 - 2031) | 3.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Paper Packaging Market Analysis by Mordor Intelligence

Italy paper packaging market size in 2026 is estimated at USD 2.94 billion, growing from 2025 value of USD 2.84 billion with 2031 projections showing USD 3.49 billion, growing at 3.49% CAGR over 2026-2031. E-commerce parcel volumes, EU plastic phase-outs, and private-label grocery penetration anchor near-term demand, while corporate net-zero roadmaps solidify long-term visibility for recycled and fiber-composite formats. Corrugated cartons remain the backbone of outbound logistics, yet folding carton innovation is reshaping premium food, personal-care, and household-care presentations. Abundant recycled-fiber flows generated by Italy’s 87.3% paper and cardboard recycling rate fortify domestic supply, and agricultural-residue fibers are poised for the next wave of circular growth.[1]Global Recycling, “Italy: On Track to Reach the 2025 Targets,” global-recycling.info Energy-price disparities versus peer EU markets intensify cost competition, rewarding vertically integrated players that deploy on-site generation or cogeneration solutions.

Key Report Takeaways

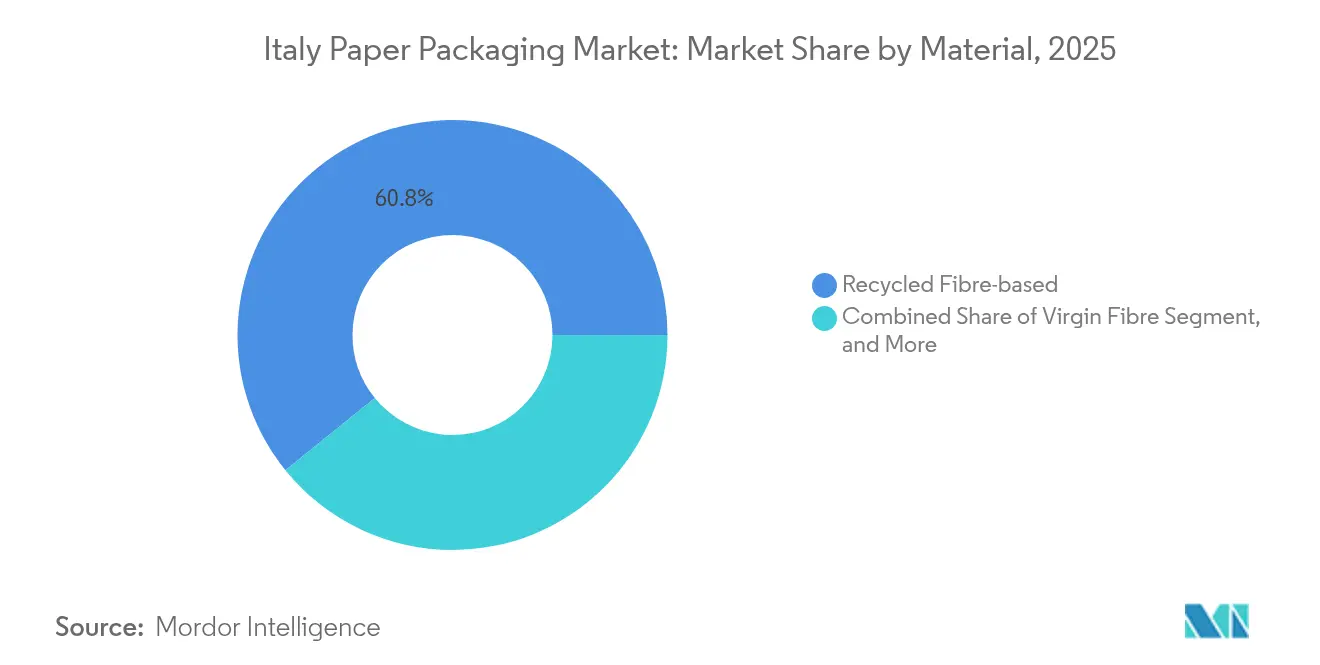

- By material, recycled fiber held 60.83% of the Italy paper packaging market share in 2025, agricultural-residue fiber is projected to deliver the fastest 5.22% CAGR through 2031.

- By product type, corrugated boxes led with 41.88% revenue share in 2025, while folding cartons are forecast to expand at a 4.66% CAGR to 2031.

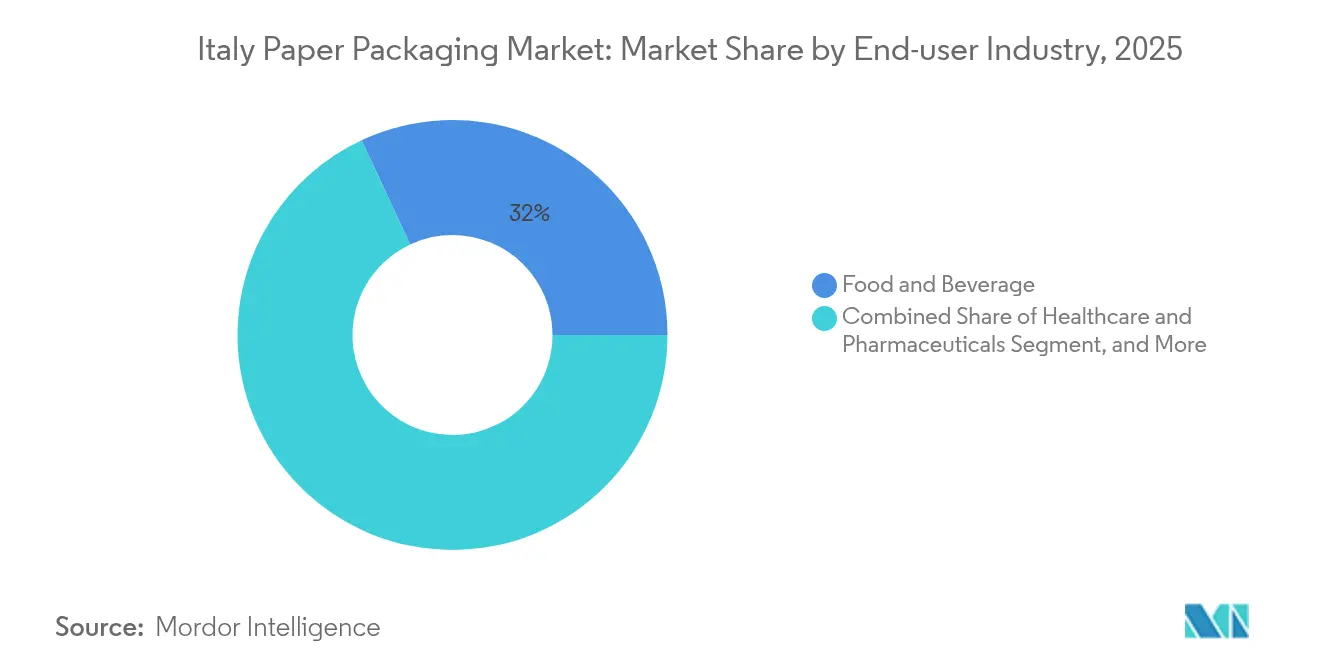

- By end-user, food captured 31.95% of the Italy paper packaging market size in 2025, and personal care plus household care segments are advancing at a 4.91% CAGR through 2031.

- By packaging level, secondary packaging accounted for 46.05% share of the Italy paper packaging market size in 2025 and is progressing at a 4.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce parcel volume boom | +0.8% | National, concentrated in Northern industrial regions | Short term (≤ 2 years) |

| EU single-use plastic phase-outs accelerating substitution | +0.6% | EU-wide, Italy implementation focus | Medium term (2-4 years) |

| Corporate net-zero roadmaps locking-in fiber-based specs | +0.4% | Global multinationals operating in Italy | Long term (≥ 4 years) |

| Private-label grocery expansion demanding cost-effective cartons | +0.5% | National, stronger in Northern retail chains | Medium term (2-4 years) |

| AI-driven box-right-sizing platforms adopted by Italian SMEs | +0.3% | National, early adoption in Lombardy and Veneto | Short term (≤ 2 years) |

| Fiber-composite barrier tech enabling shelf-stable liquid foods | +0.4% | National, export-market applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce Parcel Volume Boom

Italian e-commerce product sales reached EUR 38.2 billion (USD 41.3 billion) in 2024, growing 5% year over year, and home-living categories climbed 12% to EUR 4.4 billion (USD 4.8 billion). The surge multiplies demand for corrugated and right-sized packs that protect goods through multi-hub last-mile networks. Food and grocery e-commerce alone added EUR 4.6 billion (USD 5 billion) at 8% growth, necessitating moisture-resistant paper solutions. Northern fulfillment centers-especially in Lombardy and Veneto-face capacity constraints, prompting SMEs to integrate automated inline pack stations. CMC Packaging Automation’s 2024 partnership with Mondi typifies the shift to scalable, material-efficient e-commerce boxes. These factors translate into a measurable +0.8% uplift to the forecast CAGR for the Italy paper packaging market.

EU Single-Use Plastic Phase-Outs Accelerating Substitution

Italy’s transposition of the EU Single-Use Plastics Directive widens the addressable space for recyclable fiber-based cups, food-service wraps, and carrier bags. Established fiber supply chains and nationwide CONAI coordination simplify compliance for brands, amplifying paper uptake in quick-service restaurants and retail outlets.[2]CONAI, “Home,” conai.org Italy’s 87.3% paper packaging recycling rate exceeds the EU average of 73.9%, underscoring the systemic fit of paper solutions. Predictable compliance timelines allow converters to sequence capex, while extended producer responsibility fees penalize non-recyclable substrates. Resulting substitution momentum contributes a +0.6% contribution to CAGR forecasts for the Italy paper packaging market.

Corporate Net-Zero Roadmaps Locking-in Fiber-Based Specs

Global multinationals with Italian subsidiaries embed fiber-only criteria in procurement scorecards to attain science-based emission trajectories. Lavazza allocated EUR 25 million (USD 27 million) in 2024 to convert seven lines to recyclable or compostable formats, aiming for 100% circular packs by 2025. Suppliers with traceable, low-carbon fiber therefore secure multi-year offtake agreements. Lucart Group joined the Science Based Targets initiative in early 2024, signaling credible alignment with client climate metrics. The lock-in produces sustained baseline demand across folding carton and specialty barrier paper, adding +0.4% to the long-run Italy paper packaging market CAGR.

Private-Label Grocery Expansion Demanding Cost-Effective Cartons

Private-label grocery sales hit EUR 25.4 billion (USD 27.4 billion) in 2024, translating to 31.5% share of Italian FMCG turnover. Discount banners and supermarkets advanced 2.3% and 2.6%, respectively, and select categories now exceed 80% retailer-brand penetration. These volumes favor standardized carton footprints that slash per-unit costs yet preserve shelf pop through print quality. Converters located near Northern distribution hubs win on freight efficiency and fast artwork changeovers. The scale effect injects +0.5% CAGR impact into the Italy paper packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kraft pulp price volatility tied to Nordic supply shocks | -0.7% | Global supply chains affecting Italian mills | Short term (≤ 2 years) |

| Rising electricity prices for Italian mills post-FIT6 | -0.5% | National, particularly affecting energy-intensive operations | Medium term (2-4 years) |

| Local opposition to green-field corrugator sites | -0.3% | Regional, concentrated in Northern industrial zones | Medium term (2-4 years) |

| Limited availability of food-grade recycled fiber streams | -0.4% | National, affecting food packaging manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Kraft Pulp Price Volatility Tied to Nordic Supply Shocks

Nordic pulp costs spiked to record highs in Q2 2024, as mill outages collided with heightened energy tariffs. Billerud flagged persistent cost pressures across pulp, logistics, and power in its 2024 filings, spotlighting margin compression for Italian importers. Italian mills with exposure to virgin-fiber grades absorb the squeeze or risk ceding share in value segments. Secondary effects elevate recovered-fiber pricing, shrinking the differential between recycled and virgin inputs. The turbulence subtracts 0.7 percentage points from the forecast CAGR for the Italy paper packaging market.

Rising Electricity Prices for Italian Mills Post-FIT6

Average industrial power tariffs jumped 24% year over year to EUR 143/MWh (USD 154/MWh) in 2025, widening the gap versus Spain, France, and Germany by up to 40%. Energy accounts for 15-20% of total paper-mill cost stacks, and legacy sites without on-site generation face margin erosion. Consolidation favors sites equipped with cogeneration or solar arrays, yet retrofit paybacks lengthen at mid-single-digit margins. The cost overhang trims 0.5 percentage points from the Italy paper packaging market CAGR outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Dominance with Agricultural-Residue Momentum

The Italy paper packaging market shows recycled fiber commanding 60.83% share in 2025, leveraging a mature nationwide collection and Comieco-run quality scheme. Virgin fiber retains roles in food-grade and strength-critical uses, while composite boards service liquid food and aseptic niches. Agricultural-residue fiber-covering wheat straw, rice husk, and olive-pit derivatives register the highest 5.22% CAGR through 2031, reflecting Italian research grants and proximity to diverse crops.

Recycled streams reduce reliance on volatile Nordic imports and anchor Italy’s circular-economy reputation. Comieco logistics networks keep bale moisture under control, boosting yield per ton. Agricultural-residue scale-ups, underwritten by green-finance incentives, promise lower embedded carbon and new agrarian revenue streams. The Italy paper packaging market size expansion benefits as converters trial residue-based liners in folding cartons and corrugated fluting, supplementing recycled furnish without compromising print fidelity.

By Product Type: Corrugated Backbone, Folding Carton Upswing

Corrugated boxes delivered 41.88% of 2025 sales, surfacing as the default carrier in omni-channel logistics and heavy industrial exports. Folding cartons, however, post the swiftest 4.66% CAGR, propelled by gourmet foods, cosmetics, and household-care SKUs that seek premium graphics and structural nuances.

Corrugated plants upgrade to high-speed digital printing and AI-guided die-cutting to meet short production runs demanded by e-commerce personalization. Folding carton converters, led by firms such as Cartotecnica Moderna, harness metallized varnishes and tactile finishes to elevate shelf appeal. Flexible paper packs and molded-pulp trays expand into on-the-go snacks and consumer electronics cushioning, while liquid cartons ride the anti-plastic wave in shelf-stable beverages. The multi-track product matrix ensures the Italy paper packaging market captures value across commodity and premium niches.

By End-User Industry: Food Scale, Personal-Care Velocity

Food and beverage accounted for 31.95% of 2025 revenue, bolstered by Italy’s formidable processed-food export base and stringent product integrity norms. Personal-care and household-care lines accelerate at a 4.91% CAGR to 2031, embodying consumer trade-ups to sustainable yet aesthetically rich packs.

Food brands maintain rigorous migration and barrier standards, anchoring demand for high-strength virgin or composite boards. Personal-care labels exploit micro-flute corrugated gift sets and embossed folding cartons that encode brand narratives of naturalness. Healthcare and pharma seek serializable, tamper-evident board designs, while electronics manufacturers depend on die-cut inserts to buffer returns-prone gadgets. Together, these vectors broaden the Italy paper packaging market size across both volume and value layers.

By Packaging Level: Secondary Format Optimization

Secondary packs secured a 46.05% share in 2025, outpacing other layers with a 4.17% CAGR forecast. Retail-ready trays and shelf-displays lighten labor at the store level, while e-commerce shippers lean on crash-lock formats that collapse cube.

Primary packs integrate emerging barrier chemistries to replace plastic sachets, and tertiary pallets gain IoT sensors for traceability. Integration moves like Isem Packaging Group’s 2024 consolidation of Bartoli Packaging widen the menu of secondary solutions available to brand owners, reinforcing the Italy paper packaging market reach into store and online aisles alike.

Geography Analysis

Northern Italy anchors production and consumption, with Lombardy, Veneto, and Emilia-Romagna home to export-oriented food processors and dense fulfillment hubs. Italy’s aggregate 87.3% paper-pack recycling rate diverges regionally: Northern provinces achieve 71.8% overall waste recycling against 57.7% in the South, shaping feedstock flows and bale pricing. Proximity to Germany, Switzerland, and Austria affords Northern mills low-lead-time access to EU buyers, even as elevated domestic energy tariffs erode unit margins.

Central regions provide balanced labor costs and multimodal rail connections to the port of Livorno, favoring carton converters that serve Mediterranean shipping lanes. Southern factories benefit from regional subsidies and lower wages but grapple with thinner recovered-fiber supply chains, prompting inbound bale shipments from Central depots.

Mondi’s EUR 200 million (USD 233.56 million) upgrade of the Duino mill underscores confidence in Italy’s waypoint status for pan-EU corrugated supply. In aggregate, the geographic mosaic yields logistics agility that offsets power-price headwinds and keeps the Italy paper packaging market integrated into European just-in-time networks.

Competitive Landscape

Market concentration rests in the mid-tier range. Smurfit Kappa and Mondi anchor large-scale capacity via vertically integrated paper mills and box plants, whereas a constellation of regional converters specializes in luxury folding cartons or industrial die-cuts. Mondi’s Duino redevelopment, coupled with its 2025 acquisition of Schumacher Packaging assets, signals an appetite for premium shelf-ready formats that complement its kraft linerboard heritage.

Italian innovators such as CMC Packaging Automation pioneer AI-driven, variable-dimension systems that embed high-run-time robotics into corrugated workflows. Multivac Group’s 2024 majority stake in Italianpack introduces German mechatronics know-how to domestic tray-sealing lines. Sustainability credentials-FSC chain-of-custody, ISO 14001, and carbon-neutral mill designations are pivotal tender criteria for FMCG majors pursuing scope-3 abatements.

Energy hedging and renewable self-generation separate leaders from laggards. Lucart deploys methane cogeneration and plots photovoltaic scale-ups, while smaller independents rely on market power supply, exposing margins to tariff spikes. Overall, the Italy paper packaging market witnesses measured rivalry, with room for niche specialists under the umbrella of global multinationals.

Italy Paper Packaging Industry Leaders

International Paper Company

Sappi Limited

Smurfit WestRock

Mondi plc

Saica Group S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Ipack-Ima Milan exhibition (May 27-30) highlighted sustainable packaging breakthroughs, with the Best Packaging 2025 contest recognizing technical and technological advances that underscore Italian producers’ leadership in circular economy designs and high-precision converting.

- May 2025: Prometeia projected that Italian manufacturing turnover will edge up 1.8% to EUR 1.143 trillion (USD 1.2 trillion) in 2025, led by food, beverage, and other fast-moving consumer goods, as export recovery and deeper intra-EU trade lift packaging demand.

- April 2025: Sofidel announced the acquisition of Royal Paper’s U.S. assets, expanding the group’s tissue and paper operations beyond Europe and broadening its revenue base.

- February 2025: Mondi agreed to acquire Schumacher Packaging’s Western European assets, adding corrugated and folding-carton capacity across Europe, including Italy, to better serve premium customers and fast-growing e-commerce shipments.

Italy Paper Packaging Market Report Scope

Paper packaging encompasses materials made from paper and paperboard to protect and transport goods. These materials include cartons, boxes, bags, wrappers, and containers used across food, beverage, consumer goods, and industrial applications. Paper packaging provides durability and adaptability, enabling customization of dimensions and designs while supporting brand requirements. The material's environmental advantages, including biodegradability and recyclability, continue to drive its adoption in the packaging industry.

The Italy Paper Packaging Market is segmented by product type (folding cartons, corrugated boxes, and other product types) and by end-user industry (food, beverage, healthcare, personal and household care, electrical and electronics products, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Virgin Fibre |

| Recycled Fibre |

| Agricultural-residue Fibre |

| Composite / Multilayer Paperboard |

| Corrugated Boxes |

| Folding Cartons |

| Flexible Paper Packaging |

| Liquid Cartons |

| Molded-pulp Trays |

| Other Product Types |

| Food and Beverage |

| Healthcare and Pharmaceuticals |

| Personal and Household Care |

| Electronics and Electrical |

| Industrial and Logistics |

| Other End-User Industries |

| Primary Packaging |

| Secondary Packaging |

| Tertiary Packaging |

| By Material | Virgin Fibre |

| Recycled Fibre | |

| Agricultural-residue Fibre | |

| Composite / Multilayer Paperboard | |

| By Product Type | Corrugated Boxes |

| Folding Cartons | |

| Flexible Paper Packaging | |

| Liquid Cartons | |

| Molded-pulp Trays | |

| Other Product Types | |

| By End-User Industry | Food and Beverage |

| Healthcare and Pharmaceuticals | |

| Personal and Household Care | |

| Electronics and Electrical | |

| Industrial and Logistics | |

| Other End-User Industries | |

| By Packaging Level | Primary Packaging |

| Secondary Packaging | |

| Tertiary Packaging |

Key Questions Answered in the Report

How fast is the Italy paper packaging market expected to grow to 2031?

The market is forecast to rise from USD 2.94 billion in 2026 to USD 3.49 billion by 2031, marking a 3.49% CAGR.

Which material holds the largest share in Italian paper packs?

Recycled fiber leads with 60.83% share, supported by the nation’s 87.3% recycling rate.

What segment is expanding the quickest by product type?

Folding cartons show the fastest 4.66% CAGR as premium food and cosmetic brands upgrade shelf aesthetics.

How are energy costs influencing Italian converters?

Industrial power tariffs at EUR 143/MWh push mills to invest in cogeneration and renewables or risk margin compression.

Why are agricultural-residue fibers gaining traction?

Wheat straw, rice husk, and olive-pit residues promise lower carbon intensity and reduce exposure to volatile Nordic pulp imports.

Which end-user category is projected to post the highest growth?

Personal-care and household-care lines are advancing at a 4.91% CAGR through 2031 on rising demand for sustainable premium packaging.

Page last updated on: