Multi-Function Display Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

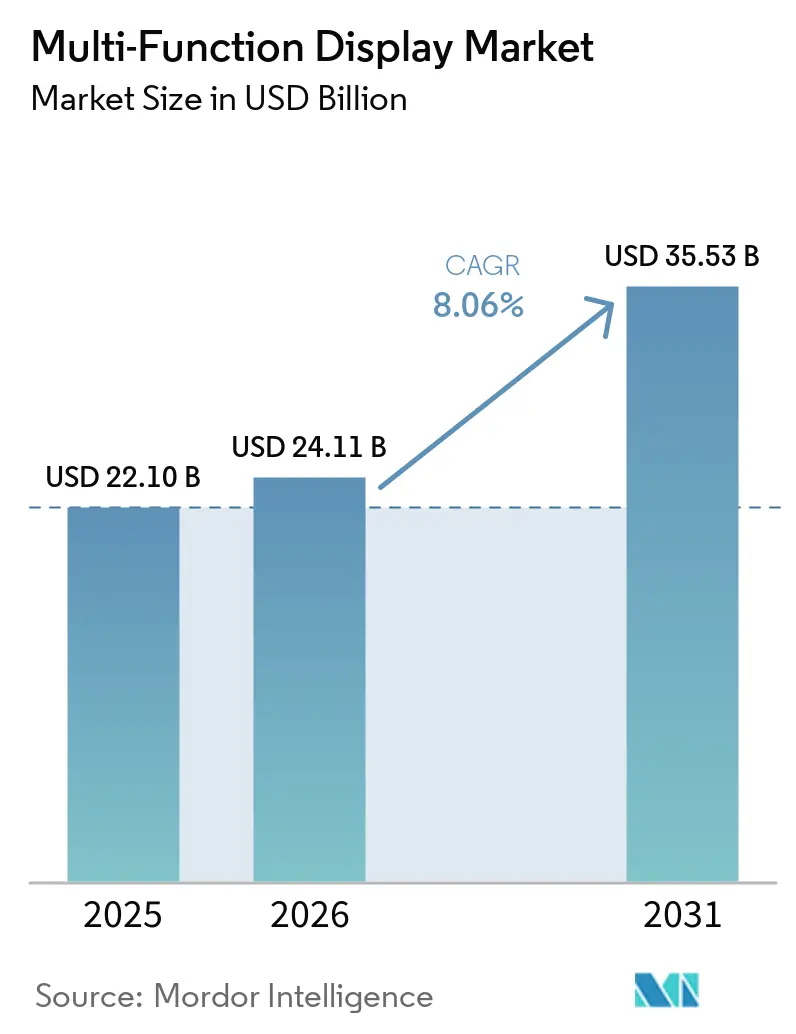

| Market Size (2026) | USD 24.11 Billion |

| Market Size (2031) | USD 35.53 Billion |

| Growth Rate (2026 - 2031) | 8.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi-Function Display Market Analysis by Mordor Intelligence

The multi-function display market size is projected to expand from USD 22.10 billion in 2025 and USD 24.11 billion in 2026 to USD 35.53 billion by 2031, registering a CAGR of 8.06% between 2026 and 2031. Rising replacement cycles in civil and military cockpits, rapid digitization of automotive dashboards, and mandatory electronic navigation upgrades in commercial shipping sustain consistent demand across end-use sectors. Larger wide-body jets and naval command centers are specifying panoramic, touch-enabled displays that consolidate multiple data streams, which lifts the average selling price despite greater commoditization of mid-sized panels. Open-architecture procurement rules now allow integrators to mix hardware and software suppliers freely, an approach that erodes historic vendor lock-in while broadening the addressable market for second-tier manufacturers. Persistent supply-chain exposure to display-driver ICs and specialty glass sourced from East Asia continues to influence lead times and working-capital commitments.

Key Report Takeaways

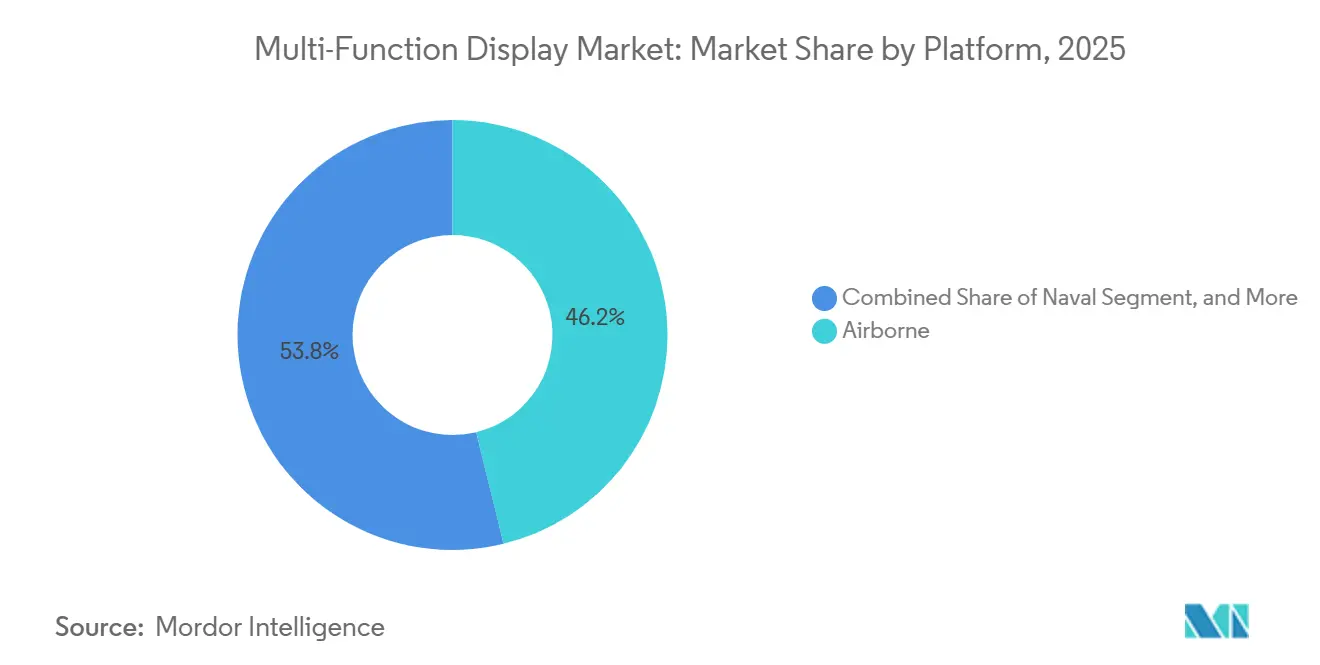

- By platform, airborne platforms led the multi-function display market share with 46.18% in 2025, while space and UAV applications are projected to record the quickest rise at an 8.68% CAGR through 2031.

- By technology, LCD and AMLCD technologies held the highest 51.37% multi-function display market share in 2025, whereas OLED and QD-OLED panels will expand fastest at an 8.91% CAGR over 2026-2031.

- By end-use industry, aerospace and defense accounted for 54.42% of the multi-function display market size in 2025, and maritime installations are on track to grow the strongest with an 8.88% CAGR to 2031.

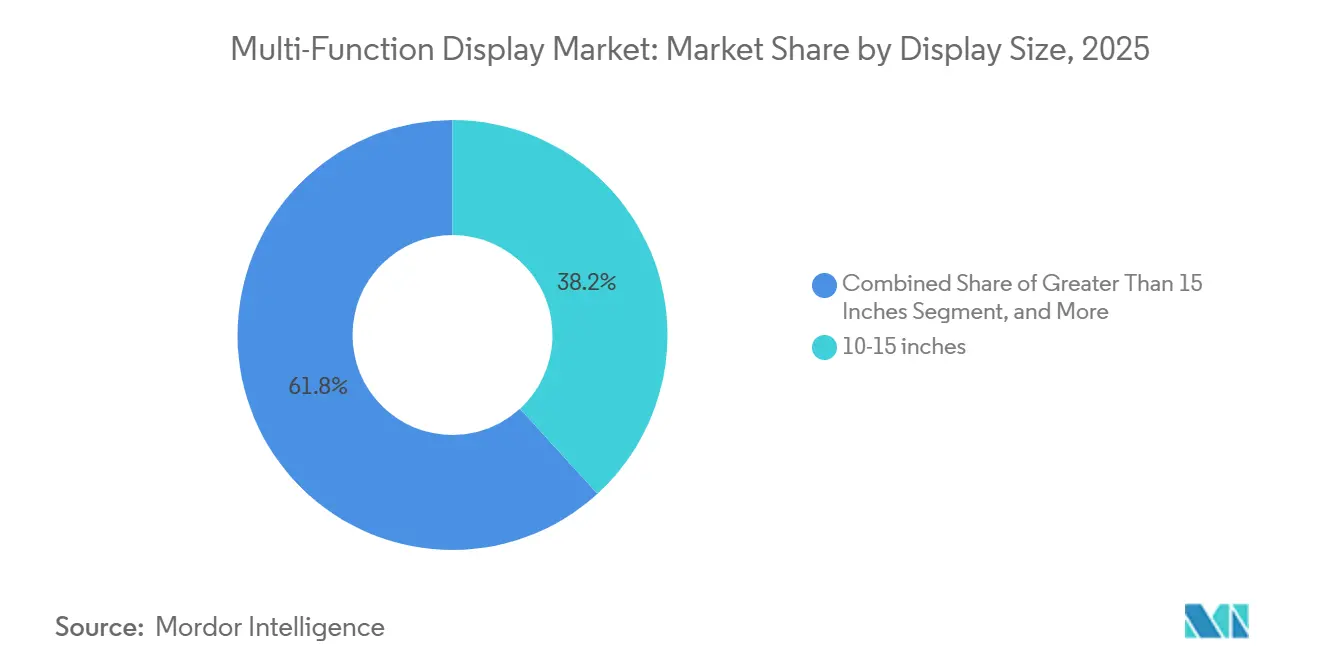

- By display size, panels measuring 10-15 inches captured 38.21% of the multi-function display market share in 2025, but screens larger than 15 inches are forecast to grow at an 8.82% CAGR over the outlook.

- By system type, electronic flight displays accounted for 41.76% of the multi-function display market in 2025; helmet-mounted displays stand out with a 9.01% CAGR forecast to 2031.

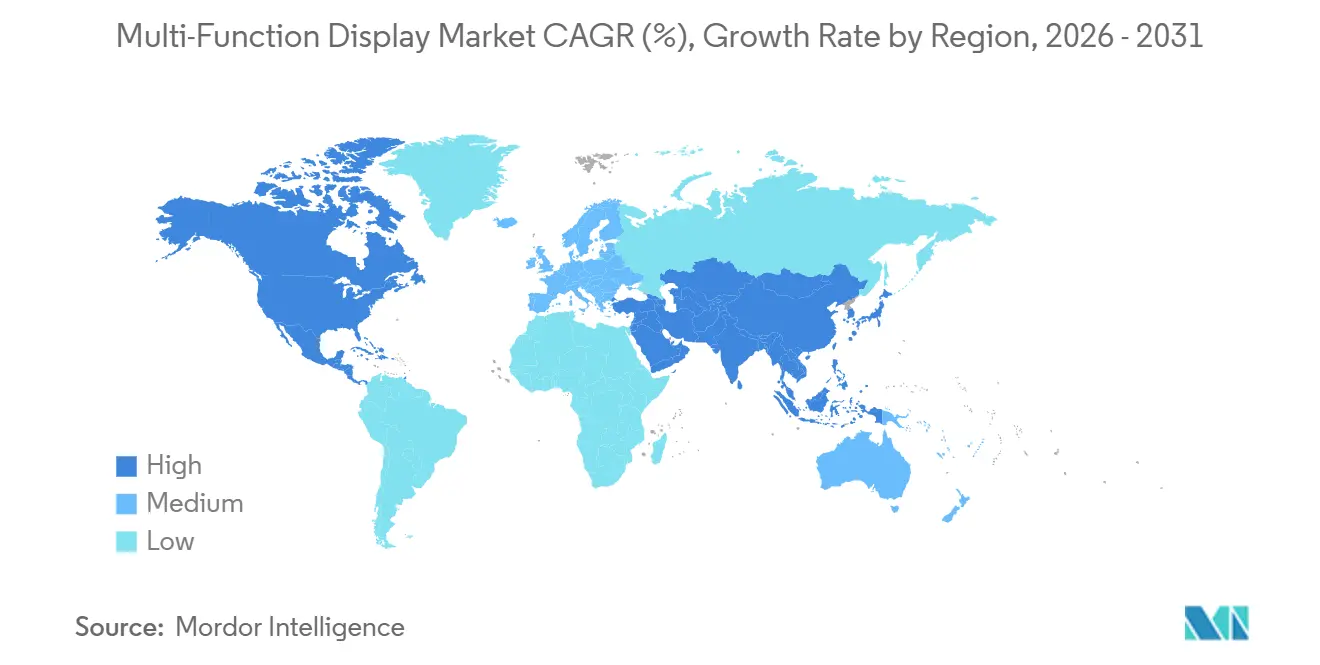

- By geography, North America dominated the multi-function display market share at 34.98% in 2025, yet Asia-Pacific is positioned for the fastest 8.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Multi-Function Display Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ongoing Commercial and Military Aircraft Deliveries | +1.8% | Global, Concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid Digitization of Automotive Cockpits | +1.5% | Europe, China, and North America | Short term (≤ 2 years) |

| Defense Modernization Programmes in Asia and Middle East | +1.3% | Asia-Pacific core, and Middle East | Long term (≥ 4 years) |

| Regulatory Mandates, ADS-B, NextGen, SESAR | +1.2% | North America , and Europe | Short term (≤ 2 years) |

| China’s Low-Cost AMLCD Capacity Expansion | +0.9% | Global supply chain, and Asia-Pacific | Medium term (2-4 years) |

| AR-Ready Marine Navigation Displays | +0.7% | Europe, and Asia-Pacific coastal nations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ongoing Commercial and Military Aircraft Deliveries

Record order backlogs at Airbus and Boeing keep production slots filled through the decade, anchoring demand for 10-15 inch primary flight and multi-function panels that fit single-aisle cockpits. Long-lead fighter upgrades such as the U.S. Air Force C-17 glass-cockpit retrofit and India’s Tejas Mk2 line elevate per-airframe display value, because each retrofit replaces aging cathode-ray tubes with modular LCD suites designed for software extensibility.[1]Airbus Staff Writers, “Commercial Aircraft Orders and Deliveries 2025,” Airbus, airbus.com Independent suppliers benefit as open-system standards let airframers decouple hardware sourcing from mission software development, which diffuses procurement across a wider vendor base while sustaining the multi-function display market beyond new-build cycles.

Rapid Digitization of Automotive Cockpits

Luxury marques and electric-vehicle startups now position expansive curved clusters as core brand identifiers, compressing analog gauges, infotainment, and driver-assistance graphics into a single bezel-free OLED or TFT surface. This consolidation reduces wiring complexity, enhances the potential for over-the-air upgrades, and shortens model-refresh timelines. Curved panels exceeding 15 inches are used on instrument panels across European premium and Chinese new-energy vehicles, encouraging panel makers to scale automotive-grade OLED capacity and to reinforce the multi-function display market. Functional-safety and cybersecurity validations, guided by ISO 26262 and UNECE R155, add development overhead but ultimately lock in suppliers capable of meeting the new documentation load.

Defense Modernization Programmes in Asia and Middle East

Indian, Japanese, South Korean, Saudi Arabian, and Emirati procurement agencies earmark budgets for home-grown fighters, naval patrol craft, and armored vehicles, each of which specifies sunlight-readable AMLCD or high-contrast OLED interfaces ruggedized to MIL-STD-810 and DO-160. Local content rules push global OEMs to license or assemble display modules regionally, sharpening competition and widening the multi-function display market footprint. Extended award cycles safeguard demand across economic swings, but shifting export controls oblige vendors to maintain multi-site supply chains that remain compliant under evolving geopolitics.

Regulatory Mandates, ADS-B, NextGen, SESAR

The FAA’s NextGen roadmap and EUROCONTROL’s SESAR initiative both require automatic dependent surveillance-broadcast equipage, thereby accelerating retrofit programs in regional and general-aviation fleets. Operators replace legacy electromechanical indicators with multi-function displays that merge GPS, ADS-B traffic, and weather on a single pane, propelling aftermarket volumes and reinforcing the multi-function display market. Mandatory software and hardware certifications under DO-178C and DO-254 lengthen the path to market, an entry barrier that protects incumbents but encourages second-tier firms to specialize in lower-criticality STC solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Bill-Of-Materials Cost Of OLED/MicroLED Panels | -1.4% | Worldwide, acute in price-sensitive automotive programs | Medium term (2-4 years) |

| Display Burn-In And Reliability Certification Hurdles | -0.8% | Global, critical for commercial and military aviation | Long term (≥ 4 years) |

| Semiconductor And Specialty-Glass Supply Chain Risks | -1.1% | Worldwide, concentrated production in East Asia | Short term (≤ 2 years) |

| Escalating Cockpit-HMI Cybersecurity Requirements | -0.6% | Worldwide, most stringent in defense platforms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High BOM Cost of OLED and MicroLED Panels

Organic-emissive and micro-emissive technologies promise unmatched contrast and power thrift, yet they still command 40-60% higher manufacturing costs than AMLCDs due to low deposition yields, complex encapsulation, and tight defect tolerances. Automotive volume builders hesitate to specify OLED outside premium trims, while industrial buyers retain LCD to contain capital expenditure. Yield improvements at recent 8.6-generation Chinese fabs are narrowing the gap, but price parity is unlikely before 2028, tempering the multi-function display market’s near-term tilt toward emissive substrates.[2]BOE Technology Group, “OLED Yield Improvement at 8.6 Gen Lines,” BOE, boe.com

Display Burn-In and Reliability Certification Hurdles

Static symbology in cockpits accelerates pixel aging in OLED panels, complicating 10,000-hour mean-time-between-failure benchmarks required under DO-160. Aircraft and military programs add further complexity by requiring electromagnetic-interference resilience and a 20-year service life. Firmware-based pixel-shifting mitigates retention but increases software complexity and must itself pass formal verification. MicroLED can circumvent organic degradation, yet solder-joint fatigue and wafer-level defectivity require separate qualification regimes that extend time-to-market, moderating its contribution to the multi-function display market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Airborne Primacy and UAV Momentum

Airborne programs secured 46.18% of the multi-function display market share in 2025, as commercial jet backlogs and fighter modernization dominate procurement. Fleet sustainment initiatives, such as the C-17 avionics refresh, replenish the multi-function display market size for existing aircraft even when new-build rates soften. Parallel growth stems from UAV ground-control stations and space-command consoles, which favor rugged, low-power AMLCD or OLED modules that communicate telemetry in real time. Platform diversity splinters qualification regimes, because airborne modules follow DO-160, naval installations meet MIL-STD-461, and automotive clusters adhere to ISO 26262.

Spacecraft, satellites, and drones are projected to register an 8.68% CAGR, the fastest among platforms, as radiation-hardened panels migrate from niche research to mainstream low-Earth-orbit constellations. Screen designs emphasize power thrift and thermal stability over color depth, but the sheer volume of satellite buses scheduled for launch broadens the market for multi-function displays. Meanwhile, land-vehicle applications follow a patchwork of defense and civil standards, slowing cross-platform economies of scale yet ensuring stable aftermarket revenues through mandatory obsolescence-management contracts.

By Technology: LCD Endurance, OLED Advancement

LCD and AMLCD kept 51.37% multi-function display market share in 2025 on the back of mature tooling, stable backlight supply, and USD 50 street pricing for 10-inch aeronautical-grade panels. Quantum-dot and miniLED backlights add incremental brightness and dimming zones, smoothing the transition to fully emissive substrates. OLED, QD-OLED, and emerging micro-LED variants will climb at an 8.91% CAGR as carmakers and fighter programs demand bezel-free, high-contrast interfaces. The multi-function display market share allocated to emissive panels is poised to expand further as mid-range automobiles adopt curved OLED clusters that balance cost with differentiation.

China’s 8.6-generation lines improved yields beyond 85% in 2025, compressing the AMLCD‐OLED cost gap. Defense buyers exploit OLED’s infinite contrast to boost night-vision compatibility and adopt flexible form factors that wrap around cockpit perimeters. MiniLED serves as a transitory solution, preserving LCD process familiarity while furnishing local dimming. Inter-technology competition is prompting panel makers to differentiate through pixel-failure compensation algorithms and low-power drive schemes, reinforcing the value of proprietary driver ICs in the multi-function display market.

By End-Use Industry: Aerospace Stronghold, Maritime Upswing

Aerospace and defense accounted for 54.42% of the multi-function display market in 2025, driven by multi-decade product life cycles, stringent certification requirements, and high aftermarket pricing for parts. Mandatory ADS-B Out upgrades and the ascendance of synthetic vision are prolonging cockpit-display refreshes across business aviation and rotorcraft fleets. While automotive applications bring higher shipment volumes, unit revenue remains lower, creating a volume-versus-value dichotomy within the multi-function display market.

Maritime retrofits, underpinned by International Maritime Organization ECDIS mandates, form the quickest 8.88% CAGR pathway.[3]International Maritime Organization, “ECDIS Performance Standards Revision,” IMO, imo.org Commercial vessels and naval surface combatants are layering augmented-reality overlays onto radar and AIS tracks, pushing demand for bridge-installed panels exceeding 20 inches. Offshore wind farms, LNG carriers, and exploration rigs likewise specify antireflective, salt-fog-resistant touchscreens. These installations diversify end-use revenue, helping suppliers cushion against the aviation industry’s cyclical volatility.

By Display Size: Mid-Range Core, Large-Format Expansion

Screens between 10 and 15 inches delivered 38.21% of the multi-function display market share in 2025, as they are ideally sized for narrow-body flight decks, ground vehicles, and naval conning stations. These displays have become a staple in such applications due to their compatibility with legacy mounting standards and avionics-bay geometry, which complicate wholesale redesigns. Their widespread adoption is further supported by their ability to balance functionality and space efficiency, making them a preferred choice across various industries.

Displays larger than 15 inches are projected to grow at an 8.82% CAGR, driven by their increasing use in wide-body aircraft, luxury vehicle dashboards, and combat-system consoles, where panoramic views are highly valued. These larger displays enhance user interface unification, offering a seamless, integrated experience. However, they also face certification challenges, particularly concerning crash-worthiness standards. To meet these demands, manufacturers are incorporating advanced technologies such as optical lamination, edge-bonding, and anti-smudge coatings. While these features add to the overall cost, they enable the bezel-less aesthetics now in high demand for both civil and military cockpits. This trend is expected to strengthen the premium tiers of the multi-function display market, as these larger displays cater to the evolving needs of high-end applications.

By System Type: Flight-Deck Leadership, Helmet Growth

Electronic flight displays accounted for 41.76% of the multi-function display market size in 2025, encompassing primary flight displays, navigation displays, and engine-indication systems. These displays are designed to comply with ADS-B (Automatic Dependent Surveillance-Broadcast) and NextGen (Next Generation Air Transportation System) regulations, ensuring compatibility with evolving aviation standards. Manufacturers are increasingly adopting modular software architectures, enabling airlines to integrate third-party applications seamlessly without requiring hardware replacements. This approach not only enhances operational flexibility but also extends the lifecycle of these displays, making them a cost-effective solution for the aviation industry.

Helmet-mounted displays, advancing at a 9.01% CAGR, embed micro-OLED modules and integrated night-vision, offering pilots off-axis targeting and augmented-reality cues. The technology migrates from fifth-generation fighters into vertical-lift and trainer aircraft, widening the application base. Portable multi-function tablets for line-maintenance and mission rehearsal round out demand, leveraging consumer supply chains but undergoing ruggedization to meet DO-160 vibration and temperature spreads. These niches collectively expand the multi-function display market while diversifying revenue streams beyond cockpit retrofits.

Geography Analysis

North America maintained the highest 34.98% multi-function display market share in 2025, anchored by the United States Department of Defense’s ongoing platform sustainment and the FAA’s retrofit compliance cycles. The C-17 cockpit refresh and the U.S. Navy Super Hornet mid-life upgrade both stipulate open-architecture displays that keep software decoupled from hardware, thereby fostering competition while preserving value for incumbents with proven, cyber-secure offerings. Canadian Arctic surveillance priorities add demand for cold-weather-rated panels in CP-140 patrol aircraft, while Mexico’s automotive exports embed digital clusters to meet infotainment expectations in the United States and Europe.

Asia-Pacific will progress at the fastest 8.61% CAGR through 2031 as China’s civil fleet doubles and indigenous fighter lines mature. COMAC’s C919 and ARJ21 jets integrate locally sourced AMLCD suites to reduce import dependency, thereby boosting domestic supply-chain maturity. India’s Tejas Mk2 and Advanced Medium Combat Aircraft head-up and helmet systems amplify regional production of high-contrast OLED visors. Japan’s maritime upgrades and South Korea’s KF-21 development furnish steady naval and aerospace pull, whereas Australia’s Hunter-class frigates keep defense-marine integration buoyant. Across Southeast Asia, ADS-B and ICAO compliance retrofits unlock incremental cockpit-display demand in aging narrow-body fleets, multiplying the multi-function display market footprint.[4]Directorate General of Civil Aviation India, “ADS-B Implementation Roadmap,” DGCA India, dgca.gov.in

Europe embraces fleet refreshes tied to SESAR mandates that couple datalink avionics with advanced surveillance. Airbus final-assembly hubs in Toulouse, Hamburg, and Seville guarantee base-load production of AMLCD units, while the UK’s Tempest and France’s carrier-borne fighter programs stipulate panoramic OLED or large-area displays. Middle Eastern outlays, primarily from Saudi Arabia and the United Arab Emirates, target fighter and naval procurements that carry local-assembly offset clauses, challenging global suppliers to embed regional manufacturing. South America and Africa trail in absolute numbers, yet offshore energy installations and rail control centers adopt ruggedized panels that seed long-tail opportunities within the multi-function display market.

Competitive Landscape

Tier-one avionics integrators, Collins Aerospace, Honeywell, L3Harris, Thales, and Elbit Systems, collectively held roughly 60% of aerospace and defense revenue in 2025, leveraging long-term platform exclusivities and proprietary mission-software ecosystems. These incumbents reinforce margins through sustainment contracts that guarantee parts and technical publications for 20-year airframe lifespans, although open-architecture rules now permit airlines and militaries to separately solicit display hardware from software upgrades. As a result, second-tier suppliers exploit commercial-off-the-shelf panels and flexible software toolkits to capture niche retrofit programs in general aviation, thereby injecting price pressure into the multi-function display market.

The automotive and maritime sectors remain more fragmented, with regional panel assemblers, consumer-electronics brands, and specialty ruggedized display firms competing chiefly on configurable form factors and lead-time agility. Regulatory heft is lighter, though the growing insistence on ISO 21434 cybersecurity standards is strengthening entry requirements that will eventually mirror those in aerospace. China’s BOE and TCL CSOT leverage domestic capacity to court export contracts, while Korean, Japanese, and Taiwanese makers diversify into micro-LED pilot lines, positioning for eventual mainstreaming of emissive displays.

Intellectual-property races now orbit around cyber-secure firmware, anti-tamper hardware, and real-time data-fusion algorithms rather than pixel density alone. Collins Aerospace’s 2024 patent filings on intrusion-detection schemes and Thales’s secure-boot microcontroller stack comply with recent RTCA DO-326A and DO-356A requirements, strengthening platform bids that prioritize cyber-resilience. Conversely, emergent entrants employ open-source operating systems paired with cost-optimized panels to undercut incumbents, especially in lower-criticality industrial and recreational aircraft segments, thereby widening the competitive field of the multi-function display market.

Multi-Function Display Industry Leaders

Barco NV

Collins Aerospace (RTX Corporation)

Honeywell International Inc.

Garmin Ltd.

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Collins Aerospace secured a USD 180 million contract to furnish next-generation touch-screen cockpit displays for the U.S. Navy F/A-18E/F Super Hornet mid-life upgrade, with deliveries commencing in 2027.

- February 2026: Garmin introduced the G3000 Prime integrated flight deck for super-midsize and large-cabin business jets, featuring 14-inch synthetic-vision displays and automatic emergency descent functionality.

- January 2026: Elbit Systems won a USD 120 million order from an undisclosed Asia-Pacific ministry for fighter helmet-mounted display systems, with deliveries targeted for 2027-2029.

- December 2025: Honeywell partnered with Mitsubishi Heavy Industries to co-develop open-architecture cockpit displays for Japan’s F-X fighter, with first prototypes expected in 2028.

Global Multi-Function Display Market Report Scope

The multi-function display (MFD) market is the global industry that designs, develops, produces, and integrates advanced display systems that consolidate and present multiple streams of information on a single screen to improve situational awareness, monitoring, and control. These displays are widely used across platforms such as airborne, land-based, naval, space, and unmanned aerial vehicles (UAVs), enabling operators to access critical data, including navigation, communication, diagnostics, and mission-specific parameters in real time.

The Multi-Function Display Market Report is Segmented by Platform (Airborne, Land-Based, Naval, and Space and UAV), Technology (LCD/AMLCD, LED/TFT, OLED/QD-OLED, and MiniLED and MicroLED), End-Use Industry (Aerospace and Defense, Automotive, Maritime, Industrial and Energy, and Other End-Use Industries), Display Size (Less Than 5 Inches, 5-10 Inches, 10-15 Inches, and Greater Than 15 Inches), System Type (Electronic Flight Displays, Head-Up Displays, Helmet-Mounted Displays, and Portable/Hand-Held MFDs), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Airborne |

| Land-Based (Ground and Automotive) |

| Naval |

| Space and UAV |

| LCD / AMLCD |

| LED / TFT |

| OLED / QD-OLED |

| MiniLED and MicroLED |

| Aerospace and Defense |

| Automotive |

| Maritime |

| Industrial and Energy |

| Other End-Use Industries |

| Less Than 5 Inches |

| 5-10 Inches |

| 10-15 Inches |

| Greater Than 15 Inches |

| Electronic Flight Displays |

| Head-Up Displays |

| Helmet-Mounted Displays |

| Portable / Hand-Held MFDs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Platform | Airborne | |

| Land-Based (Ground and Automotive) | ||

| Naval | ||

| Space and UAV | ||

| By Technology | LCD / AMLCD | |

| LED / TFT | ||

| OLED / QD-OLED | ||

| MiniLED and MicroLED | ||

| By End-Use Industry | Aerospace and Defense | |

| Automotive | ||

| Maritime | ||

| Industrial and Energy | ||

| Other End-Use Industries | ||

| By Display Size | Less Than 5 Inches | |

| 5-10 Inches | ||

| 10-15 Inches | ||

| Greater Than 15 Inches | ||

| By System Type | Electronic Flight Displays | |

| Head-Up Displays | ||

| Helmet-Mounted Displays | ||

| Portable / Hand-Held MFDs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the multi-function display market?

The multi-function display market size stands at USD 24.11 billion in 2026 and is projected to reach USD 35.53 billion by 2031.

How fast is demand for space and UAV displays growing?

Space and UAV applications are forecast to expand at the quickest 8.68% CAGR, reflecting satellite-constellation launches and autonomous-drone adoption.

Which technology segment is growing fastest within cockpit displays?

OLED and QD-OLED panels lead growth with an 8.91% CAGR, propelled by high-contrast requirements in premium automotive dashboards and next-generation military cockpits.

Why are maritime displays becoming more important?

International Maritime Organization mandates for electronic chart and augmented-reality navigation overlays drive an 8.88% CAGR in maritime display installations through 2031.

Who holds the largest share of flight-deck display contracts?

Electronic flight displays remain the largest system type, accounting for 41.76% of 2025 revenue, largely supplied by Collins Aerospace, Honeywell, and L3Harris.

Which region will record the fastest growth through 2031?

Asia-Pacific is projected to expand at an 8.61% CAGR thanks to China's growing civil fleet, India's indigenous fighter programs, and Japan's maritime modernization plans.

Page last updated on: