Large Format Display Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.63 Billion |

| Market Size (2031) | USD 25.07 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

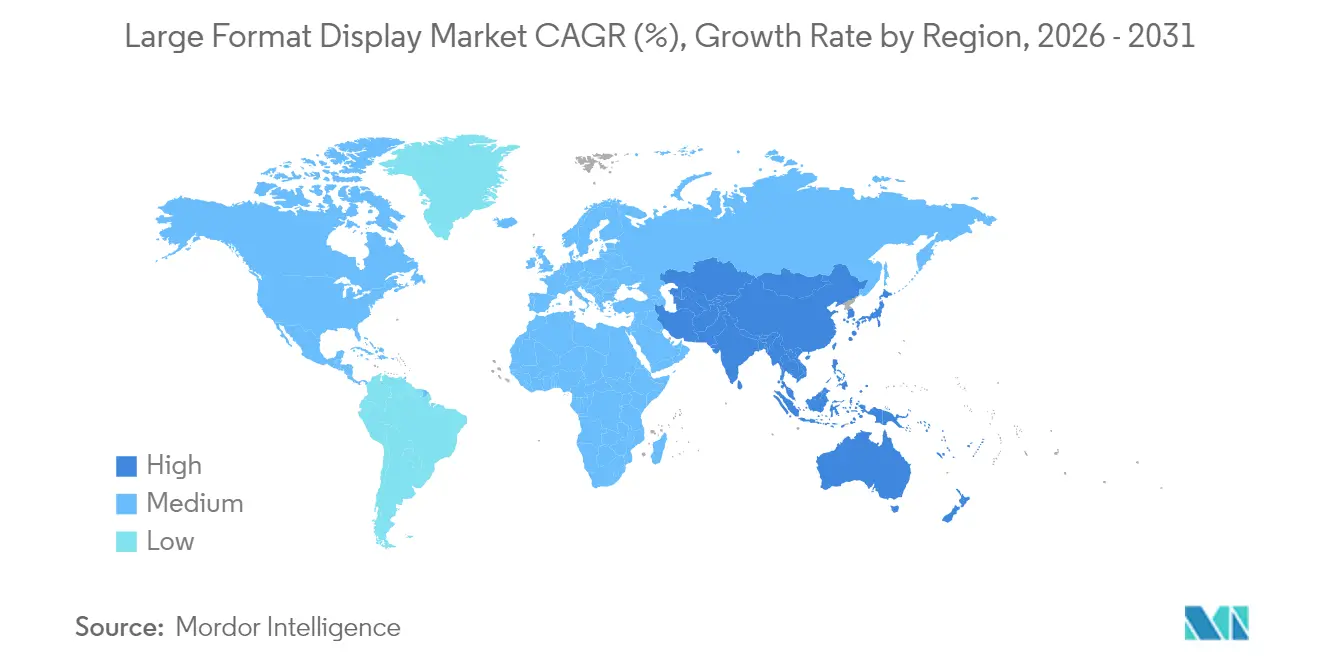

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Large Format Display Market Analysis by Mordor Intelligence

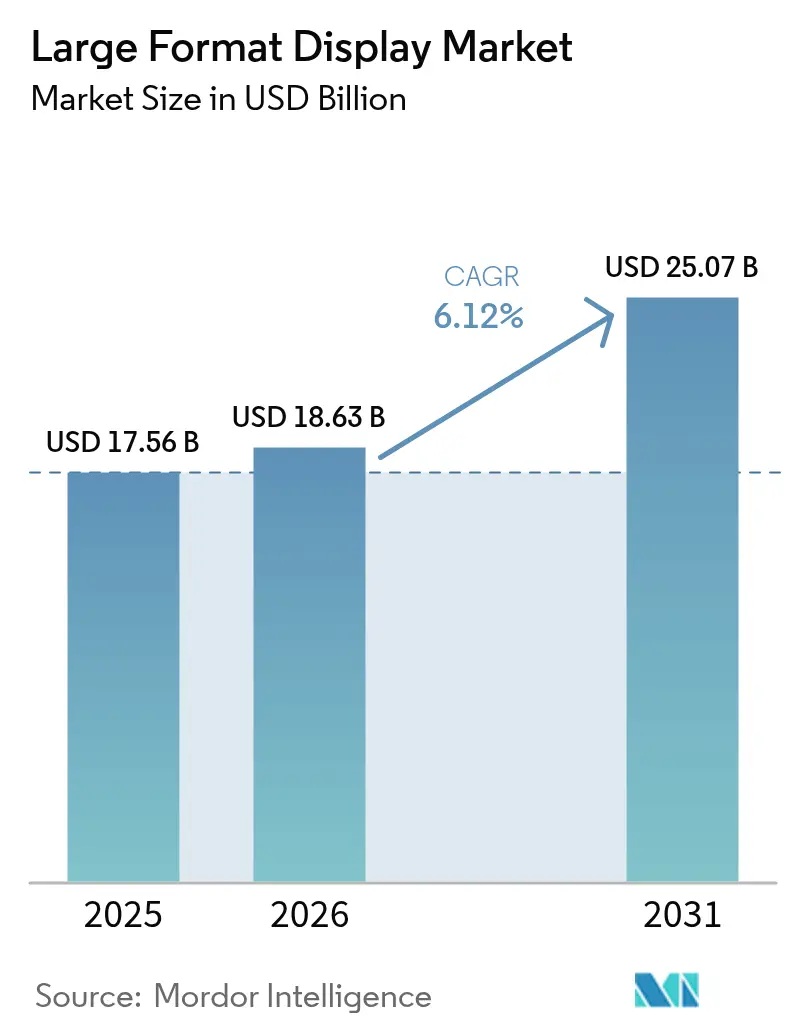

The large format display market size is expected to grow from USD 17.56 billion in 2025 to USD 18.63 billion in 2026 and is forecast to reach USD 25.07 billion by 2031 at 6.12% CAGR over 2026-2031. Momentum is shifting from pure hardware sales toward software-centric ecosystems, with roughly half of digital-signage spending now directed toward content-management platforms and cloud services, rather than panels alone. Video walls retained a 52.74% large format display market share in 2024, however, fine-pitch modular LED is narrowing the performance gap and eroding the segment’s price premium. Displays above 80 inches represent the fastest-growing size class, expanding at 6.88% as virtual-production studios, control rooms, and immersive retail lean on seamless canvases that only Micro LED and advanced LED architectures can deliver at scale. Indoor deployments accounted for 64.73% of 2024 revenue, driven by hybrid-work collaboration suites and programmatic digital-out-of-home (DOOH) networks that replace static posters with data-driven, cloud-served ads. Asia-Pacific now anchors the demand outlook with a forecast 7.02% CAGR as municipal bodies in China and India embed large format displays into smart-city infrastructure.

Key Report Takeaways

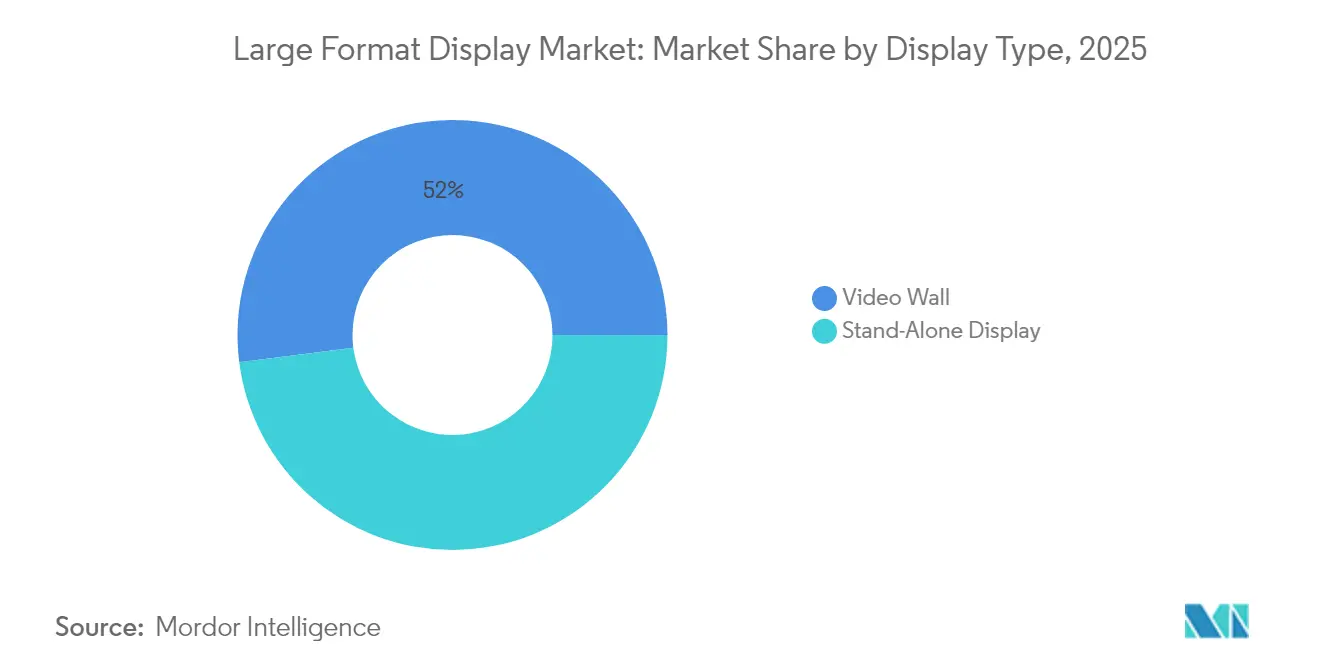

- By display type, video walls commanded 52.02% of the large format display market share in 2025 while stand-alone displays are set to post the fastest 6.64% CAGR through 2031.

- By screen size, the 41–60 inch class accounted for 38.25% of the large format display market size in 2025, whereas panels above 80 inches are advancing at 6.53% CAGR.

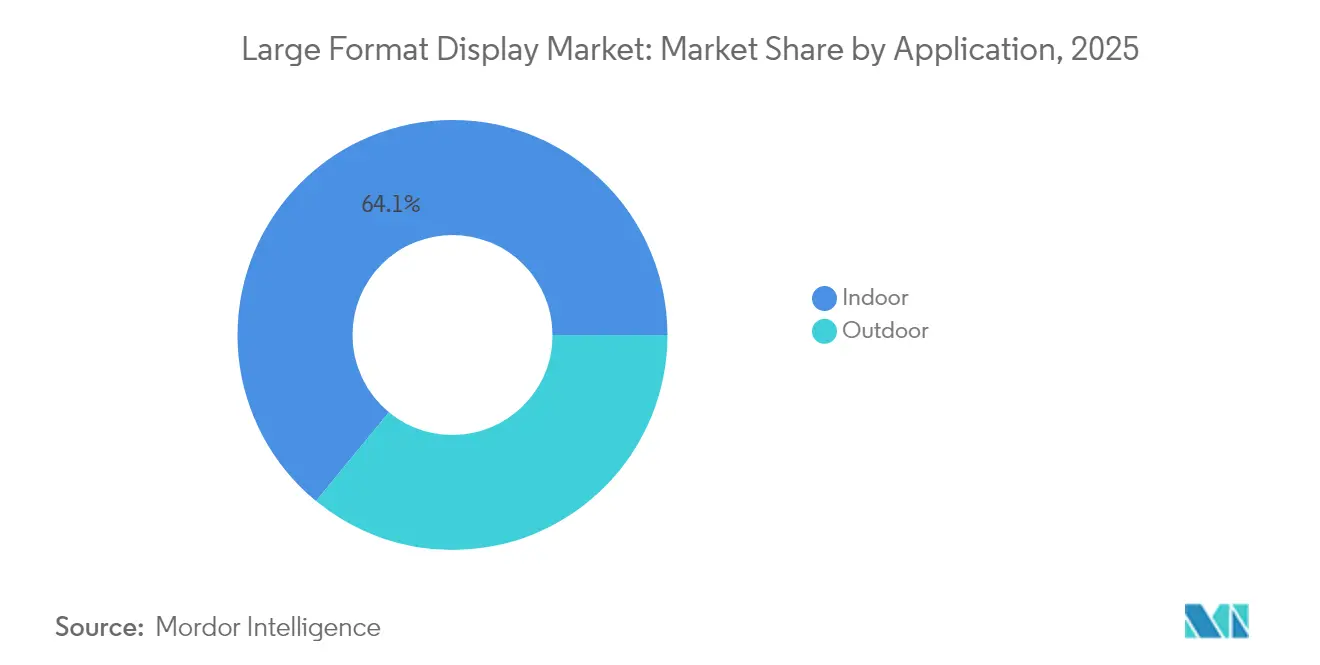

- By application, indoor venues represented 64.05% of 2025 revenue, yet outdoor installations are projected to grow at a 6.76% CAGR during 2026-2031.

- By end-user, commercial settings held 46.10% share of the large format display market size in 2025; infrastructural deployments will register the highest 6.71% CAGR through 2031.

- By geography, North America led with 35.25% share in 2025, while Asia-Pacific is slated to achieve a 6.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Large Format Display Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in high-brightness, energy-efficient LED video-wall solutions | +1.2% | Global, with strongest adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Soaring demand for digital signage in retail and smart-city infrastructure | +1.5% | Global, Asia-Pacific core with spill-over to MEA and South America | Short term (≤ 2 years) |

| Proliferation of 4K/8K and interactive displays across education and corporate collaboration | +1.0% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Cost-per-inch decline of large-area LCD/LED panels | +0.9% | Global | Long term (≥ 4 years) |

| Virtual-production LED volumes accelerating studio adoption | +0.7% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| AI-driven, cloud-based CMS enabling real-time content personalization | +1.1% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in High-Brightness, Energy-Efficient LED Video-Wall Solutions

Flip-chip chip-on-board (COB) technology is delivering IP67 durability, lower thermal loads, and 3,840 Hz refresh rates, cutting lifetime operating costs for 24/7 command-center displays. Philips’ Unite LED 5000 Series, unveiled at InfoComm 2024, uses common-cathode COB modules as fine as P0.78 to extend warranty coverage from 2 to 3 years, with optional 5-year service plans. Samsung’s long-running dominance likewise stems from similar durability investments, yet increasing commoditization across Asian fabs is compressing hardware margins and pushing incumbents to differentiate through software support offerings.[1]Samsung Insights, “The Tech and Digital Signage Behind a Smart Connected City,” insights.samsung.com Upcoming European Union draft rules aimed at reducing standby and network-standby power will further favor energy-optimized LED architectures.[2]European Commission, “Public Consultation on Updating Ecodesign and Labelling Rules for Electronic Displays,” energy.europa.eu

Soaring Demand for Digital Signage in Retail and Smart-City Infrastructure

Retail-media networks are accelerating in-store digitization, but in-aisle screens still capture less than 1% of total retail-media budgets, translating into a USD 690 million upside for U.S. retailers alone by 2028. Samsung’s July 2024 positioning frames large format displays as the connective tissue for smart cities, integrating wayfinding, transit alerts, and emergency messaging into one managed platform. VIOOH’s 2024 study found 27% of recent campaigns included programmatic DOOH buys, a share likely to reach 35% by end-2026 as advertisers seek dynamic, data-enriched impressions. Municipal agencies in Asia-Pacific are already embedding similar functionality into public tenders, making the large format display market an infrastructure line item rather than a discretionary purchase.

Proliferation of 4K/8K and Interactive Displays Across Education and Corporate Collaboration

Universities are scaling campus-wide refresh cycles that lock vendors in for up to a decade. Panasonic disclosed that the University of St. Thomas replaced more than 300 legacy projectors and displays with 4K laser solutions to meet hybrid-learning mandates.[3]Panasonic Connect, “Visual Learning Meets 4K in Business and Educational Technology,” connect.na.panasonic.com Corporate buyers mirror this trend, Manulife Plaza integrated 65-inch 4K displays and PTZ cameras into convertible boardrooms spanning 450,000 square feet to preserve collaboration equity for on-site and remote workers. Interactivity and ultra-HD resolution enable annotation, real-time polling, and content-rich presentations, pushing demand for touch-enabled large format display market solutions that bridge physical and virtual meeting spaces.

AI-Driven, Cloud-Based CMS Enabling Real-Time Content Personalization

Content-management software is evolving from scheduling utilities into AI engines that optimize ad slots, segment audiences, and auto-generate creatives. Samsung’s VXT platform delivers cloud-native device monitoring, audience analytics, and integrated ad networks, while LG Business Cloud marries CMS with electric-vehicle charging kiosks to monetize dwell time. Facial recognition and natural-language models allow messaging to adjust to demographics or contextual triggers, though GDPR and similar frameworks require robust consent and data-minimization workflows, favoring larger vendors with mature compliance resources.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capex and TCO for large format installations | -0.8% | Global, particularly acute in price-sensitive South America and MEA markets | Short term (≤ 2 years) |

| Intensifying competition from mobile / online advertising channels | -0.6% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Installation and maintenance complexity across multi-panel walls | -0.4% | Global | Medium term (2-4 years) |

| Emerging energy-consumption regulations for high-nit displays | -0.5% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capex and Total Cost of Ownership for Large Format Installations

Flagship projects can exceed USD 8 million, as shown by Captivision’s 16,000-square-foot transparent media-glass façade at COEX Magok Le-West in Seoul, completed in 2024. Costs encompass structural reinforcements, power upgrades, and multi-year maintenance contracts. Integrators such as Acuity Brands, which agreed to acquire QSC for USD 1.215 billion, are bundling audio-visual, lighting, and control systems into turnkey deals to amortize expenses over service contracts. Nevertheless, mid-market enterprises and cash-constrained municipalities often delay projects or limit deployments to single-screen pilot programs, slowing the near-term trajectory of the large format display market.

Intensifying Competition from Mobile and Online Advertising Channels

Programmatic DOOH frequently draws budget reallocations rather than fresh spend; VIOOH reported that 81% of funds came from other digital channels when DOOH was purchased by programmatic teams. Marketers cite the absence of unified cross-channel metrics and granular conversion tracking as key barriers. While audience-measurement platforms are improving, mobile and social networks still deliver richer attribution, placing pressure on display network operators to prove ROI and maintain CPMs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Display Type: Video Walls Dominate, Stand-Alone Displays Expand in Niche Verticals

In 2025, video walls captured 52.02% of the large format display market share, while stand-alone displays are projected to achieve the fastest growth rate at 6.64% CAGR through 2031. The large format display market size for stand-alone units remains smaller but is gaining share in quick-service restaurants, corporate lobbies, and wayfinding kiosks, where drop-in replacement and modular mounting are paramount. Philips’ Unite LED 5000 Series ships in 27.1-inch 16:9 cabinets that snap together into 8K canvases, blending video-wall continuity with single-panel serviceability. LG’s 118-inch MAGNIT Micro LED provides an All-in-One alternative for luxury hospitality, circumventing bezel management altogether.

The performance-price gap is narrowing as COB LED costs fall and management software converges across form factors. Samsung’s VXT and LG Business Cloud allow multi-site fleets to mix video walls and stand-alone panels under one dashboard, shifting differentiation to analytics and ad-tech hooks. Consequently, integrators report higher attach rates for managed-service contracts, a trend that elevates recurring revenue in the large format display market.

By Display Size: Above 80 Inches Chart the Fastest Growth Curve

Panels exceeding 80 inches are on track to register a 6.53% CAGR to 2031, the quickest among size tiers, driven by virtual-production stages, control-room overviews, and experiential retail façades. In contrast, 41–60 inch models held the lion’s share at 38.25% in 2025 thanks to corporate huddle spaces and drive-through menus. TCL Technology revealed that 79% of its 2024 shipments exceeded 55 inches, underscoring supply readiness for ever-larger canvases. Architectural installations add transparency and curvature to the size mix; Captivision’s media glass and LG’s Transparent OLED walls enable designers to meld digital and physical realms, feeding premium niches of the large format display market.

Energy consumption looms as a regulatory wildcard. The European Commission’s forthcoming ecodesign rules target high-nit displays, a category dominated by panels larger than 80 inches. Vendors must therefore balance luminous output against stricter efficiency thresholds without inflating total cost of ownership.

By Application: Indoor Revenues Lead, Outdoor Networks Accelerate

Indoor environments captured 64.05% of 2025 sales or USD 11.24 billion within the large format display market size. Controlled lighting conditions allow thinner profiles and lower ingress-protection ratings, which reduce bill-of-materials costs. Outdoor deployments, however, are gaining momentum at a forecast 6.76% CAGR as municipalities and media owners upgrade roadside billboards and transit shelters to IP67, 5,000-nit LED modules that support programmatic DOOH trades. Samsung projects that 50% of global DOOH campaigns will be programmatic by 2026, representing a doubling of 2023 volumes. Proof-of-play verification and audience analytics remain prerequisites for premium outdoor CPMs, prompting display vendors to integrate camera sensors and edge AI into their hardware offerings.

Indoor retail screens benefit from proximity to the point of sale. Survey data show 75% of shoppers scanned QR codes displayed in-store during 2024, converting physical engagement into e-commerce baskets. As generative-AI engines personalize messaging on the fly, the revenue mix tilts further toward software licensing in the large format display market.

By End-User: Infrastructure Deployments Outpace Commercial Installations

Commercial entities, retailers, hotels, and offices, held 46.10% of 2025 revenue, but infrastructure users, chiefly city governments and transit agencies, will grow at a 6.71% CAGR as smart-city blueprints mature. Samsung’s smart-connected-city initiative integrates displays with IoT sensors for transit updates and emergency alerts, generating advertising revenue during idle cycles. LG’s partnership with ChargePoint embeds large screens into EV charging stations, monetizing the 20–40-minute dwell window.

Regulatory procurement is increasingly tied to sustainability mandates. The EU’s Ecodesign for Sustainable Products Regulation obliges vendors to supply 10-year software support and Digital Product Passports by 2027. Vendors equipped with lifecycle-tracking systems will therefore capture a disproportionate share of forthcoming infrastructure tenders within the large format display market.

Geography Analysis

North America accounted for 35.25% of 2025 revenue in the large format display market, buoyed by hybrid-work upgrades, stadium video-wall renovations, and retail-media network rollouts. Daktronics reported an 18% spike in Live Events revenue to USD 109 million in Q1 FY2025 after winning arena projects such as UBS Arena and Allegiant Stadium, though heavy consulting and IT outlays compressed near-term margins. Programmatic DOOH saw U.S. advertisers boost spend by 29% on average in 2024, advancing the shift from static boards to cloud-managed screens.

Asia-Pacific is projected to log a 6.68% CAGR to 2031, the fastest of any region. TCL Technology’s Guangzhou G8.6 oxide line ran at full capacity throughout 2024 and contributed 21% of CSOT revenue, cementing China’s dominance in large format LCD and LED substrates. South Korea’s LG Electronics invested in Mo-Sys Engineering to integrate Micro LED panels with XR camera tracking, targeting regional studios adopting in-camera VFX. India’s Smart-City Mission plans to integrate real-time passenger information systems into 100 urban centers by 2027, though fragmented procurement and fiscal constraints moderate near-term volumes.

Europe faces the most stringent regulatory headwinds. The European Commission’s November 2024 consultation aims to slash electricity use among the 70 million electronic displays sold annually by tightening standby-power caps and mandating repairability. Vendors must embed recycled content and substance-of-concern tracking, raising entry barriers. Germany, France, and the UK are prioritizing digital signage for multimodal transit hubs, converting legacy paper timetables to dynamic displays that double as advertising inventory.

South America and the Middle East and Africa collectively generate under 10% of global revenue but represent long-range opportunities. Brazil and Mexico are digitizing quick-service restaurant menus, yet economic volatility constrains capital spend. The UAE and Saudi Arabia allocate smart-city budgets to immersive façades in airports and malls aligned with tourism initiatives. Power-reliability issues in parts of Africa continue to limit 24/7 operation, though telco tower-side displays are emerging as alternative advertising nodes.

Competitive Landscape

The large format display market remains fragmented on the software side, where the top five CMS providers controlled only 12.79% revenue in 2022. Conversely, hardware consolidation is underway as panel makers vertically integrate into software and managed services. Samsung marked its 15th consecutive year as global signage leader by bundling VXT cloud CMS, remote monitoring, and ad-tech hooks with its QLED and LED portfolio, building stickier annual-recurring-revenue streams. LG’s seed stake in Mo-Sys Engineering extends its Micro LED panels into virtual production pipelines, tapping into the fast-growing content studio niche.

TCL Technology invested RMB 10.309 billion (USD 1.42 billion) in R&D during 2024, focusing on Pol-Less LCD, Mini-LED backlights, and 1,512 PPI VR panels to escape commodity margin compression. Smaller innovators carve out architectural niches, such as Captivision’s transparent media glass, which generated USD 8 million from a single Seoul façade, proving an appetite for building-integrated displays despite project-based scalability limits.

Regulation is sharpening competitive edges. The EU’s Digital Product Passport mandate will exclude vendors lacking lifecycle transparency, advantaging incumbents with established compliance teams. Integrators are also consolidating; Acuity Brands’ USD 1.215 billion acquisition of QSC unites audio, video, lighting, and building-management stacks under one umbrella, simplifying procurement for enterprise buyers. Overall, suppliers that combine differentiated hardware, cloud software, and compliance credentials are positioned to outpace pure-play panel vendors in the large format display market.

Large Format Display Industry Leaders

Panasonic Corporation

Barco NV

LG Electronics

Samsung Electronics Co., Ltd

NEC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Captivision completed a 16,000-square-foot transparent media-glass façade at COEX Magok Le-West in Seoul, generating USD 8 million in revenue.

- October 2025: Acuity Brands agreed to acquire QSC for USD 1.215 billion to expand its Intelligent Spaces portfolio.

- September 2025: LG Electronics made a strategic seed investment in Mo-Sys Engineering to integrate Micro LED displays into virtual-production ecosystems.

- June 2025: Philips introduced the Unite LED 5000 Series featuring flip-chip COB and IP67 durability at InfoComm 2024.

Global Large Format Display Market Report Scope

The large format display market report is segmented by Display Type (Video Wall, Stand-Alone Display), Display Size (32–40 inch, 41–60 inch, 61–80 inch, Above 80 inch), Application (Indoor, and Outdoor), End-User (Commercial, Infrastructural, Institutional and Industrial), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Video Wall |

| Stand-Alone Display |

| 32–40 inch |

| 41–60 inch |

| 61–80 inch |

| Above 80 inch |

| Indoor |

| Outdoor |

| Commercial |

| Infrastructural |

| Institutional and Industrial |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Mexico | ||

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Display Type | Video Wall | ||

| Stand-Alone Display | |||

| By Display Size | 32–40 inch | ||

| 41–60 inch | |||

| 61–80 inch | |||

| Above 80 inch | |||

| By Application | Indoor | ||

| Outdoor | |||

| By End-User | Commercial | ||

| Infrastructural | |||

| Institutional and Industrial | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Mexico | |||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the large format display market?

The large format display market size reached USD 18.63 billion in 2026.

How fast is the sector expected to grow?

Revenue is forecast to expand at a 6.12% CAGR, hitting USD 25.07 billion by 2031.

Which display type holds the largest share?

Video walls dominate, accounting for 52.02% of 2025 revenue.

Which screen size is expanding the quickest?

Panels larger than 80 inches show the fastest growth, advancing at a 6.53% CAGR through 2031.

Which region is projected to outpace others?

Asia-Pacific is expected to post the highest regional CAGR at 6.68% to 2031.

Page last updated on: