Liquid Crystal On Silicon (LCoS) Display Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

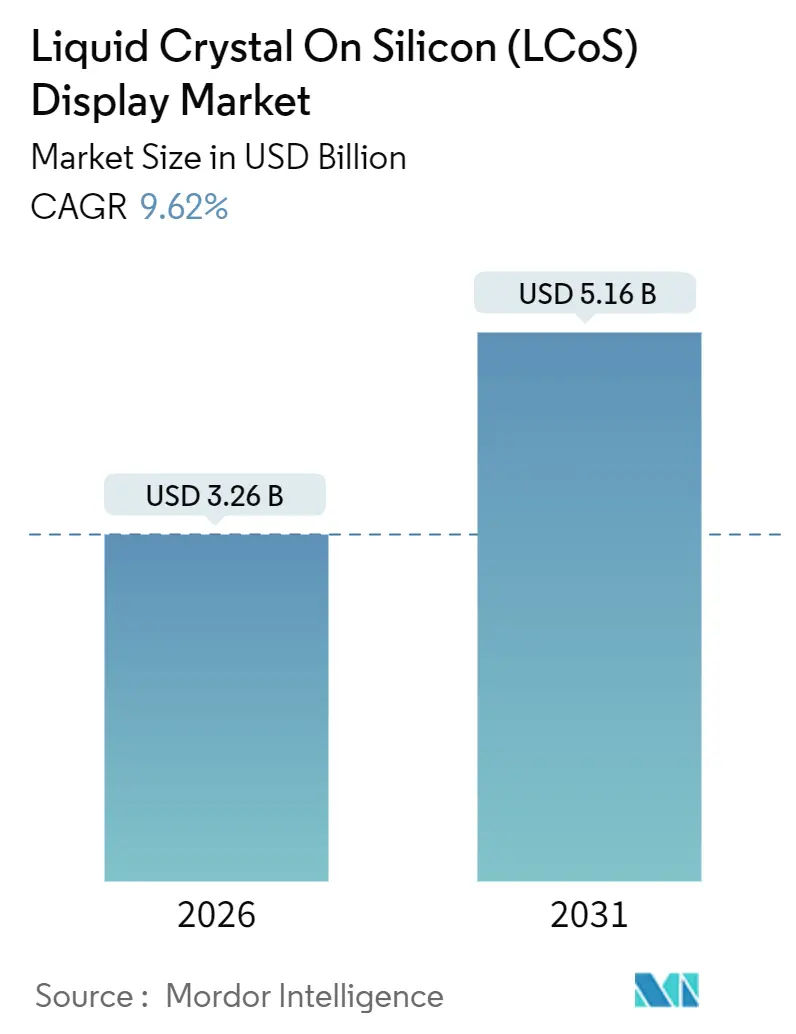

| Market Size (2026) | USD 3.26 Billion |

| Market Size (2031) | USD 5.16 Billion |

| Growth Rate (2026 - 2031) | 9.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

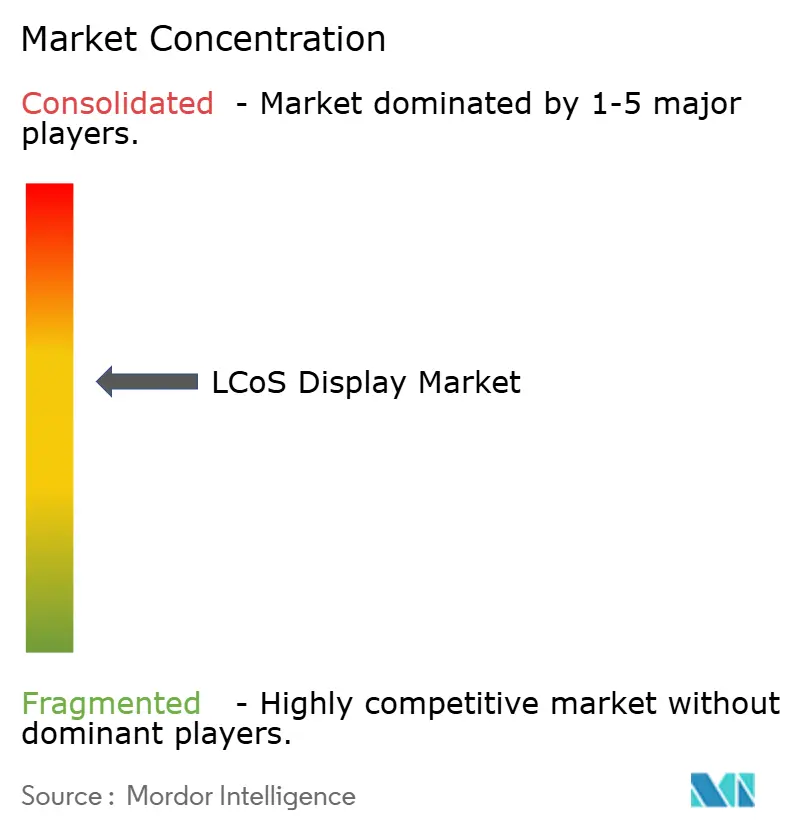

| Market Concentration | Medium |

Major Players_Display_Market_-_Major_Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Crystal On Silicon (LCoS) Display Market Analysis by Mordor Intelligence

The Liquid crystal on silicon (LCoS) display market size stood at USD 3.26 billion in 2026 and is projected to reach USD 5.16 billion by 2031, expanding at a 9.62% CAGR over 2026-2031. This growth rests on the technology’s ability to deliver very high pixel density and contrast in compact footprints. Surging demand for augmented reality headsets, panoramic automotive head-up displays, and quantum-photonics tools keeps the LCoS display market on an upward trajectory. Laser-illumination coupling is unlocking brightness levels once reserved for digital light processing, while ferroelectric liquid-crystal modes are enabling sub-millisecond switching required for holographic beam steering. Supply-chain realignments in Japan and China, together with United States and European funding for domestic fabs, are reshaping investment flows across the value chain.

Key Report Takeaways

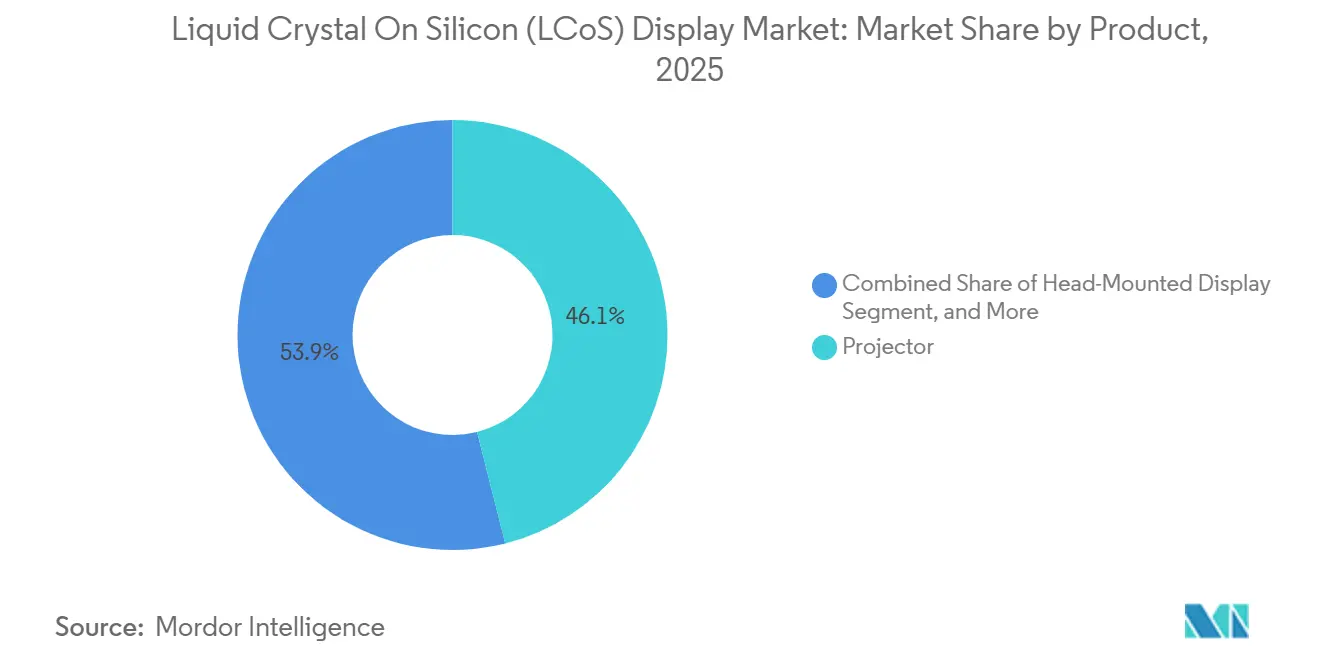

- By Product, projectors led with 46.06% of LCoS display market share in 2025, while head-mounted displays are advancing at a 10.22% CAGR through 2031.

- By Technology, Nematic technology captured 60.11% of 2025 revenue, yet ferroelectric variants are forecast to climb at a 10.54% CAGR to 2031.

- By End User, Consumer electronics accounted for 38.03% of 2025 spending, whereas automotive demand is set to grow at a 10.03% CAGR on the back of panoramic HUD rollouts.

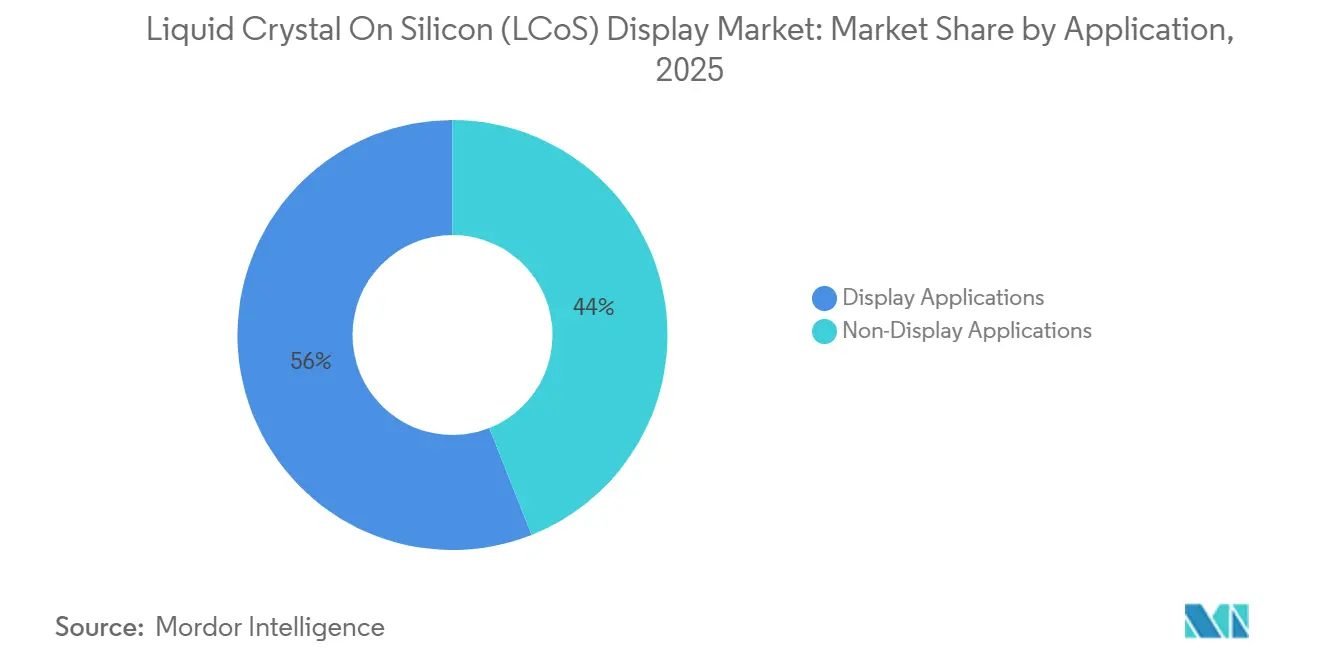

- By Application, projectors accounted for the largest share with 56% in 2025, while Non-Display Applications are expected to grow at the fastest rate of 10.2% CAGR to 2031.

- By Resolution, Full HD panels (1080p) held 40.19% of revenue in 2025, while the 4K-and-above resolution segment is poised to expand at a 10.83% CAGR.

- North America secured 34.38% of global sales in 2025, while Asia-Pacific is projected to rise at a 10.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Liquid Crystal On Silicon (LCoS) Display Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for High-Resolution Display Products | +1.80% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Deployment of AR and VR in Consumer Devices and HMDs | +2.10% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Growing Automotive Adoption of HUDs | +1.60% | North America, Europe, Asia-Pacific premium segments | Medium term (2-4 years) |

| Emergence of Laser-Illuminated LCoS for High-Brightness Projectors | +1.30% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Integration of LCoS Spatial Light Modulators in Quantum and Photonics Research | +0.90% | North America, Europe, select Asia-Pacific research hubs | Long term (≥ 4 years) |

| Government Funding for Advanced Microdisplay Manufacturing | +1.20% | North America (CHIPS Act), Europe (Horizon Europe), Asia-Pacific (national programs) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for High-Resolution Display Products

Professional simulators, surgical microscopes, and home-theater enthusiasts are converging on 4K and 8K requirements, and the Liquid Crystal On Silicon (LCoS) display market is answering with sub-3 micrometer pixel pitches. Sony’s VPL-GTZ380 stacks three 1.38-inch panels to achieve native 8K images that replicate vascular detail for surgical training.[1]Sony Corporation, “VPL-GTZ380 Native 8K Laser Projector,” sony.com Panel makers are adopting immersion photolithography to maintain yields, which raises capex but fortifies entry barriers. While price limits slow 4K adoption in mainstream consumer projectors, corporate and education customers are upgrading faster to meet fine-text readability standards. As a result, high-resolution panels are expected to corner an ever-larger slice of future revenue.

Deployment of AR and VR in Consumer Devices and HMDs

Slimmer headsets need pixel densities that eliminate the screen-door effect at arm’s-length viewing. OmniVision’s December 2025 OP03021 chip integrates 1920 × 1080 pixels on a 0.39-inch diagonal and drives 120 Hz refresh, allowing mixed-reality glasses to weigh under 100 g.[2]OmniVision Technologies, “Industry’s First Single-Chip LCoS Microdisplay,” ovt.com Himax followed with a dual-edge front-lit architecture that cuts optical-path length by 30%, letting designers carve thinner temple arms. Such gains underpin a 10.22% CAGR for HMD shipments within the wider Liquid Crystal On Silicon (LCoS) display market. Ferroelectric modes that switch in under a millisecond are also critical to reduce motion-to-photon latency below 10 ms, a threshold for user comfort.

Growing Automotive Adoption of HUDs

Automakers are expanding head-up displays from small combiner glass to windshield-spanning visuals. BMW’s Panoramic Vision system, entering series production in 2025, uses a laser-illuminated LCoS engine rated at 10,000 cd/m², high enough for noon-day readability.[3]BMW Group, “Panoramic Vision, The Future of Head-Up Displays,” bmwgroup.com JVC Kenwood’s 2025 module adds a 50 W thermal substrate so dashboards can withstand cabin heat. Euro NCAP now awards safety points for AR-HUDs that highlight vulnerable road users, making LCoS adoption a route to higher crash-test scores. As safety regulations tighten, panoramic HUDs are shifting from luxury extras to mainstream features.

Emergence of Laser-Illuminated LCoS for High-Brightness Projectors

Replacing mercury lamps with narrowband lasers boosts brightness while enabling dynamic dimming. Kyocera’s LaserLight engine delivers 5,000+ lumens from a smartphone-sized source, and Hamamatsu’s X15213-03CR panel endures optical power densities above 10 W/mm² thanks to sapphire cover glass. These advances let event-venue projectors break 30,000-lumen barriers without image degradation. Higher contrast and longer lifetimes are lowering total cost of ownership, which helps the Liquid Crystal On Silicon (LCoS) display market defend projector share against DLP incumbents.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Technology Development and Manufacturing | -1.40% | Global, particularly acute in North America and Europe | Short term (≤ 2 years) |

| Competition From OLED and MicroLED Alternatives | -1.70% | Global, with fastest substitution in consumer electronics | Medium term (2-4 years) |

| Supply Chain Dependence on Specialized Liquid Crystal Materials | -0.80% | Global, with concentration risk in Asia-Pacific | Medium term (2-4 years) |

| Thermal Management Challenges in High-Brightness LCoS Panels | -0.60% | Global, most critical in automotive and aviation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Technology Development and Manufacturing

Sub-3 micrometer patterning tools cost upward of USD 100 million each, and initial yield losses can hit 20% when liquid-crystal alignment drifts. Japan Display spun off its automotive micro display assets into AutoTech in October 2025 to ring-fence this capex pressure. Consumer-electronics buyers also demand annual price cuts, squeezing margin recovery. These economics discourage new entrants and keep most high-resolution capacity clustered in Japan, South Korea, and Taiwan.

Competition From OLED and MicroLED Alternatives

Emissive micro displays are encroaching on brightness and contrast values that once distinguished LCoS. Kopin’s Lightning OLED reached 3,000 nits at a 100,000:1 contrast ratio while drawing 40% less power than comparable LCoS panels. Samsung and Sony demoed MicroLED prototypes topping 3,000 ppi with microsecond response in 2025. As price gaps shrink, LCoS suppliers must lean on phase-only modulation and wavelength-selective switching areas where emissive rivals cannot yet compete.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wearables Outpace Legacy Projectors

The segment generated the largest slice of the Liquid Crystal On Silicon (LCoS) display market size from projectors in 2025, with projectors holding 46.06% revenue. However, head-mounted displays are set to grow faster at 10.22% annually. Pico projectors are pivoting toward smart-home interfaces that project controls on walls, while spatial-light-modulator panels, though niche, command the highest prices because laboratories pay for phase accuracy.

OmniVision’s OP03021 enabled retinal-resolution pixels within a 0.39-inch diagonal, allowing consumer AR glasses to weigh under 100 g and reinforcing HMD momentum. At the same time, professional cinema owners continue to invest in USD 80,000 8K projectors, preserving cash flow for legacy vendors. This dual narrative keeps the LCoS display market balanced between cost-sensitive consumer products and premium projection solutions.

By Technology: Ferroelectric Switching Gains Ground

Nematic modes still dominated 60.11% of 2025 revenue, yet the ferroelectric share is expanding fastest, supported by a 10.54% CAGR that outstrips the overall Liquid Crystal On Silicon (LCoS) display market. Ferroelectric liquid crystals switch in under 100 µs, essential for holographic LiDAR and varifocal AR optics.

Fraunhofer IPMS demonstrated binary ferroelectric panels that reconfigure automotive LiDAR beams in real time. Yield hurdles persist because spontaneous polarization makes alignment sensitive, lifting defect rates above 15%. Even so, buyers in defense and photonics tolerate 30% price premiums for latency gains, ensuring healthy margins for suppliers able to master the process.

By End User: Automotive Catches Up with Consumer Electronics

Consumer-electronics buyers accounted for 38.03% of the 2025 total, anchored by home-theater and VR volumes. Automotive programs, however, are climbing at a 10.03% CAGR, reflecting regulatory pushes for immersive HUDs. JVC Kenwood’s 50 W thermal substrate helps LCoS engines survive dashboard temperatures beyond 85 °C, satisfying stringent AEC-Q100 norms and widening the addressable fleet.

Aviation upgrades and optical 3D metrology remain smaller slices of the Liquid Crystal On Silicon (LCoS) display market size, yet they generate outsized R&D investment because of demanding environmental and accuracy requirements. Medical imaging is gaining momentum too, as regulators approve AR-assisted procedures that overlay patient data onto the surgical field.

By Application: Display Uses Dominate but Photonics Niches Accelerate

Display applications retained the largest share in 2025, led by projectors and fast-growing AR/VR micro displays. Head-up displays widened adoption, especially in premium vehicles, bolstering the Liquid Crystal On Silicon (LCoS) display market.

Non-display uses, including wavelength-selective switching for optical networks and phase modulators for holographic 3D printing, are expanding as telecom carriers roll out 400 G and 800 G links. Santec’s modules now route 96 channels with under-5 dB insertion loss, cutting network downtime and capex. MIT researchers also proved volumetric 3D printing that cures photopolymer in one shot using phase-only LCoS interference patterns, hinting at disruptive future demand.

By Resolution: 4K and 8K Shift the Revenue Mix

Full HD kept 40.19% of turnover in 2025, yet 4K-and-above units are rising at a 10.83% CAGR, reflecting enterprise and simulator needs for 8 million-pixel panels. The Liquid Crystal On Silicon (LCoS) display market share held by HD (720p) continues to slide as pico projectors migrate to 1080p for sharper text.

Advanced immersion scanners costing over USD 100 million are mandatory to etch sub-3 µm pixels, and only a handful of vertically integrated vendors can finance them. After DIC exited the chemical segment in 2024, Chinese supplier Slichem became the prime source for high-anisotropy liquid crystals, concentrating raw-material risk in one geography.

Geography Analysis

North America commanded 34.38% of 2025 revenue thanks to strong enterprise projector sales, defense helmet orders, and early AR pilots in surgery and logistics. Research institutes such as national laboratories purchased the bulk of phase-only spatial light modulators, reinforcing local demand. The CHIPS and Science Act is expected to seed domestic fabs, though new lines had not broken ground by early 2026.

Asia-Pacific is forecast to expand at a 10.94% CAGR, the fastest rate worldwide. Japanese incumbents are repurposing older LCD fabs for micro displays, South Korean groups are investing in AR components, and China is consolidating liquid-crystal chemical supply. Slichem’s acquisition of DIC’s fluids allows Chinese panel makers to internalize key materials, but Western defense primes now vet supply chains more closely.

Europe sits mid-pack, buoyed by automotive HUD programs. Euro NCAP’s 2025 scoring revisions reward augmented-reality displays, prompting German OEMs to standardize panoramic HUDs on new models. Horizon Europe earmarked EUR 1.2 billion (USD 1.3 billion) for photonics through 2027, part of which funds LCoS spatial-light-modulator research. Middle East markets buy LCoS systems for flight simulation, while Africa and South America remain nascent.

Regulatory Landscape

Regulation affecting LCoS shipments is shaped by display safety, automotive qualification, and trade policy. In the United States, Section 301 tariffs have continued to influence landed costs and sourcing strategies for display components, and April 2026 reporting highlighted policy attention on tariffs for digital displays in the context of reducing dependence on Chinese manufacturing for defense-relevant supply chains.

On the standards side, material and subsystem specifications used in advanced display stacks are formalizing, including the IEC publishing IEC TS 62565-4-4:2025 (April 2025) for specifying quantum dot light conversion films that can be used alongside laser-illuminated optical engines. For government-linked programs, procurement requirements also shape microdisplay designs, such as the US Navy SBIR topic N232-105 calling out performance attributes for LCoS microdisplays, reinforcing compliance focus on refresh rate and integration readiness in defense and research use cases.

Value Chain Analysis

The LCoS value chain runs from specialty liquid-crystal and alignment materials through CMOS backplane fabrication, LC cell assembly, wafer-level optics, module integration, and channel distribution into OEM platforms (projectors, AR/VR headsets, HUDs, and photonics instruments). Upstream materials include nematic and ferroelectric liquid-crystal chemistries and optical coatings, while midstream processing centers on high-resolution CMOS backplanes and tight-tolerance bonding and cleanroom assembly; capex intensity is high, with wafer bonding lines requiring cleanroom infrastructure that can exceed USD 200 million per line.

Industry structure favors players that can manage yield and secure constrained inputs. CMOS backplane capacity is concentrated in Asia (notably Taiwan and South Korea), and specialized equipment such as Japanese laser dicing tools used in wafer-level optics can create bottlenecks, with lead times reported up to 18 months. Downstream, microdisplay and SLM suppliers (for example, OmniVision for single-chip microdisplays and HOLOEYE, Hamamatsu, and other specialists for spatial light modulators) work with headset, projector, automotive, and photonics OEMs, where integration demands around thermal management, optical efficiency, and driver electronics strongly influence supplier selection and qualification cycles.

Competitive Landscape

The LCoS display market features a moderately concentrated structure. Sony, JVC Kenwood, Canon, and Epson dominate the projector and HUD niches because they design entire optical engines in-house. Sony’s SXRD line integrates proprietary liquid-crystal chemistry and laser coupling, enabling the company to sustain premium prices in cinema and simulation. JVC Kenwood’s 10,000 cd/m² HUD module shows the depth of engineering required for dashboard qualification.

Phase-only and niche photonics segments belong to Hamamatsu, HOLOEYE, Syndiant, and Fourth Dimension Displays. These specialists license or self-develop patents around sub-millisecond switching and sapphire cover-glass bonding, enabling them to serve quantum optics and LiDAR developers willing to pay USD 5,000 per panel.

Patent filings escalated in 2025, for instance, Hamamatsu lodged 14 inventions on water-cooling manifolds for laser-illuminated panels, while OmniVision patented embedded heat pipes to dissipate 10 W/cm² without exceeding 50 °C. New entrants are eyeing whitespace in ferroelectric-based holographic engines, aiming to bridge consumer-grade cost with military-grade performance.

Liquid Crystal On Silicon (LCoS) Display Industry Leaders

OmniVision Technologies Inc.

Hamamatsu Photonics KK

Sony Corporation

Koninklijke Philips NV

JVC Kenwood USA Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace around high-speed LCoS variants and system miniaturization for AR glasses, automotive HUDs, and non-display photonics is opening as providers optimize power, brightness, and thermal performance. OmniVision’s OP03021 single-chip full-color sequential LCoS microdisplay for smart glasses, introduced in December 2025, underscores the push for higher integration and lower power in wearables, while automotive programs drive higher brightness and thermal robustness in laser-illuminated optical engines. In non-display applications, spatial light modulators used for beam shaping and laser processing are gaining prominence as industrial users adopt more advanced laser control, broadening demand beyond conventional projection.

Technology roadmaps also point to opportunities in optical-stack simplification and polarization management to reduce optical path length and improve light efficiency in waveguide-based displays. Research progress on metasurface-assisted LCoS architectures and continued investment in high-resolution SLM development, including programs tied to industrial and quantum-technology objectives, support product differentiation in phase-only modulation, beam steering, and high-frame-rate operation where LCoS maintains practical advantages over emissive microdisplay alternatives in specific optical architectures.

Recent Industry Developments

- May 2026: US Navy expands SBIR topic N232-105 to include expanded LCoS microdisplay qualifications across additional platforms.

- December 2025: OmniVision introduced the OP03021 single-chip full-color sequential LCoS microdisplay for smart glasses. The launch highlights a push toward higher integration and lower power in AR wearables, strengthening LCoS competitiveness where optical-engine volume and battery constraints dominate design tradeoffs.

- June 2024: A cross-industry consortium announced a plan to scale LCoS backplane fabrication in Asia, signaling a shift toward larger-scale manufacturing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from liquid crystal on silicon (LCoS) display solutions used to create images in projection and near-eye viewing systems, where a liquid crystal layer is built on a silicon backplane and typically operates in a reflective architecture.

Scope exclusions: We exclude non-LCoS display technologies and general optical components that do not function as an LCoS imaging panel.

Segmentation Overview

- By Product

- Head-Mounted Display (HMD)

- Projector

- Head-Up Display (HUD)

- Pico Projector

- Spatial Light Modulator Panel

- By Technology

- Ferroelectrics LCoS (FLCoS)

- Nematics LCoS (NLCoS)

- Wavelength Selective Switching (WSS)

- Reflective LCoS

- Transmissive LCoS

- By End User

- Consumer Electronics

- Automotive

- Aviation

- Optical 3D Measurement

- Medical

- Military

- Industrial and Scientific

- By Application

- Display Applications

- Projectors

- Microdisplays for AR/VR HMDs

- Head-Up Displays

- Non-Display Applications

- Wavelength Selective Switching in Optical Telecom

- Beam Steering and LiDAR

- Spatial Light Modulators for Holography and 3D Printing

- Display Applications

- By Resolution

- HD (Less than equal to 720p)

- Full HD (1080p)

- WQHD (1440p)

- 4K and Above

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with a practical view of where LCoS is actually used, then maps how those end uses flow into shipments and revenues. For that mapping, we relied on public sources such as US International Trade Commission trade statistics, UN Comtrade country-level import and export series, and US Bureau of Economic Analysis macro indicators to keep the demand environment consistent across years.

We also reviewed sources such as IEEE and other peer-reviewed optics and display journals to cross-check technology direction, resolution shifts, and switching-speed narratives that influence adoption timing. Company filings, investor presentations, and reputable press coverage were used to understand product launches and any capacity or supply-chain commentary. Where needed, we used paid subscriptions for company financials and intelligence, along with patent database coverage, to confirm ownership of key design directions and to avoid double counting across adjacent display categories. These are illustrative examples, and additional public sources were referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what portion of revenue is truly tied to LCoS display panels and modules, and what gets categorized under optics, illumination, or complete devices depending on the sales model. We spoke with a mix of component-side and system-side participants, and we covered APAC, EMEA, and the Americas so regional production concentration and end-market demand signals could be checked and then normalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 17% | APAC: 39% |

| Mid tier: 57% | Functional/Unit leaders: 24% | EMEA: 35% |

| Smaller Players: 17% | Managers: 59% | Americas: 26% |

Market-Sizing & Forecasting

For sizing, we use top-down and bottom-up checks that meet in the middle, since full vendor roll-ups are not always visible for LCoS. The top-down view is built by reconstructing the demand pool from key consuming applications like near-eye displays, head-up displays, and projectors, then applying adoption and content-per-device assumptions to convert demand into revenue.

To keep the model grounded, we track a small set of fingerprints across the time series, such as shipment growth of LCoS-relevant device categories, typical resolution mix shifts (HD to 4K+), the share of display versus non-display use cases, and average selling price movement as volumes scale. Technology direction is also treated as an input, since switching behavior and brightness requirements shape which applications can expand faster. When data gaps exist, we use range-based assumptions and then narrow them after checking consistency with observed product launches and interview feedback.

Forecasting is run using scenario analysis supported by a simple multivariate regression layer, with key drivers including end-market unit growth, mix shift toward higher resolution, and adoption pacing in automotive and near-eye use cases. Selective bottom-up approximations, such as sampled ASP times estimated unit volumes for representative device categories, are used to validate totals and correct any overstatement caused by double counting between panel, module, and system revenue reporting.

Data Validation & Update Cycle

Validation is done by checking the model against independent signals, so the final numbers stay consistent with how the industry behaves in practice. We run variance checks across regions, application totals, and implied ASP trends, then review anomalies in more than one analyst pass before sign-off.

When gaps show up, re-contact is triggered, especially if a new product cycle, supply constraint, or macro event shifts the assumed mix or pricing path. Reports are refreshed annually, with interim updates for material events that could reasonably change demand or pricing. Before delivery, a final pass is completed so clients receive the most current view available at that point in time.

Mordor Intelligence's Liquid Crystal On Silicon Display Market Size Measured Against Other Published Estimates

Published market sizes for LCoS displays often differ, and the spread usually comes from what is counted as revenue and how adjacent categories are treated. Differences in base year selection, the way ASP changes are applied, and how often assumptions are refreshed can also move the final number.

The benchmark table shows a higher 2026 value than the two 2025 figures, and in the Mordor Intelligence model only LCoS display panels and related display modules are counted when they are sold into defined display uses like projectors, head-mounted displays, and head-up displays. In other publications, the total can rise or fall if complete device revenue is included, or if non-display functions such as spatial light modulation are grouped into the same pool, and these are not always separated consistently during validation.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.26 B (2026) | |

| Global Publisher A | USD 2.14 B (2025) | This estimate is anchored to a different year and can include a wider share of device-level revenue across near-eye and projection categories, which reduces comparability with panel and module revenues. |

| Industry Research Group B | USD 2.48 B (2025) | The sizing appears to use broader application mapping and a different ASP progression path, which changes the implied impact of resolution and technology mix across the forecast window. |

Taken together, the table mainly reflects scope and timing differences rather than a disagreement on where adoption is happening. By tying the calculation to visible demand indicators, realistic mix assumptions, and repeatable checks on implied pricing, we keep the final value traceable and easier to reconcile across years and regions.

Key Questions Answered in the Report

What is the current value of the LCoS display market?

The LCoS display market size reached USD 3.26 billion in 2026.

How fast is the market projected to grow?

It is forecast to advance at a 9.62% CAGR to hit USD 5.16 billion by 2031.

Which product segment is expanding the quickest?

Head-mounted displays are projected to post a 10.22% CAGR, the highest among product categories.

Why are ferroelectric LCoS panels gaining attention?

They switch in under 100 µs, which suits holographic beam steering and varifocal AR optics that nematic modes cannot serve effectively.

Which region is expected to be the fastest-growing?

Asia-Pacific is forecast to register a 10.94% CAGR, driven by Japanese, Korean, and Chinese investments in microdisplay capacity.

What key restraint could slow adoption?

Emissive OLED and MicroLED microdisplays are narrowing the performance gap, creating competitive pressure on LCoS suppliers.

Page last updated on: