Display Panel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 172.73 Billion |

| Market Size (2031) | USD 210.68 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

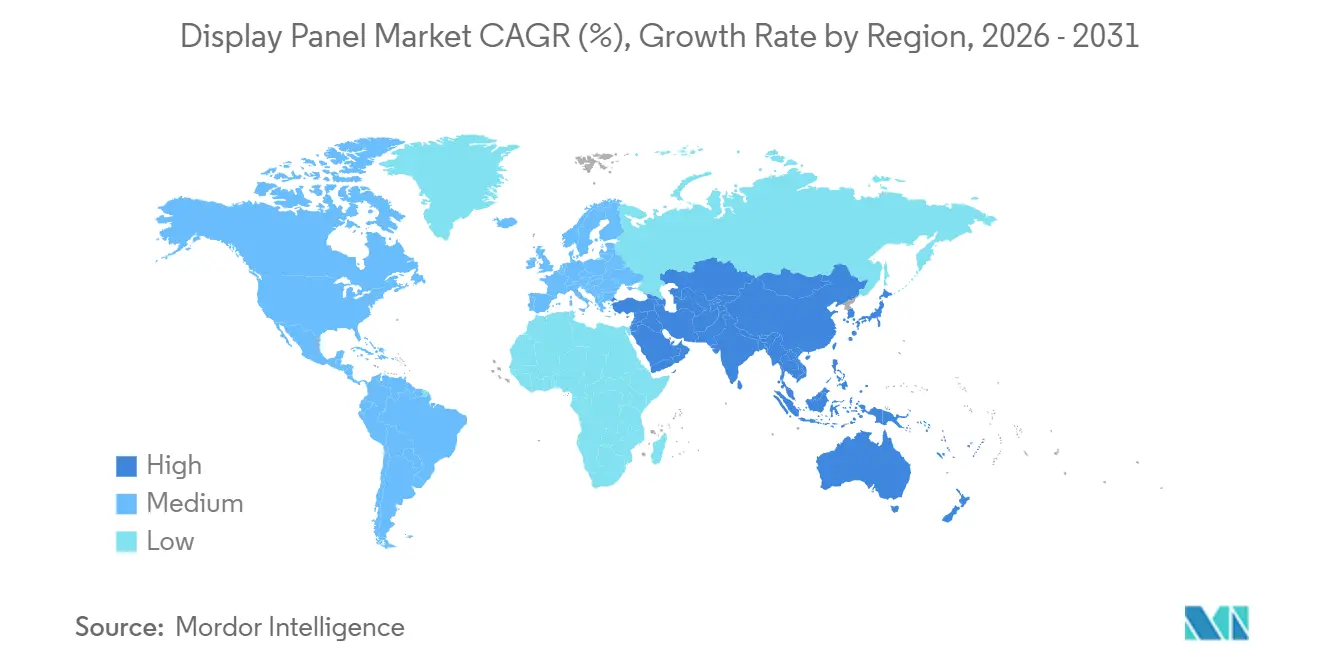

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Display Panel Market Analysis by Mordor Intelligence

The display panel market size is projected to expand from USD 167.12 billion in 2025 and USD 172.73 billion in 2026 to USD 210.68 billion by 2031, registering a 4.05% CAGR between 2026 and 2031. The transition toward high-efficiency OLEDs and emerging Micro-LED architectures is reshaping competitive dynamics as smartphone brands seek lower power budgets and automakers integrate multi-screen cockpits. Large-screen television demand, the roll-out of foldable phones and tablets, and rising volumes of AR/VR headsets are sustaining shipment momentum. Capacity additions in China’s Gen-8.6 and Gen-10.5 fabs, combined with steady investments in Gen-6 OLED lines in South Korea and Taiwan, underpin near-term supply, yet glass substrate and skilled-labor shortages continue to stretch lead-times. Regulatory pressure on PFAS-based polarizer films and the high capital intensity of Gen-10.5 fabs are reinforcing scale advantages for incumbents.

Key Report Takeaways

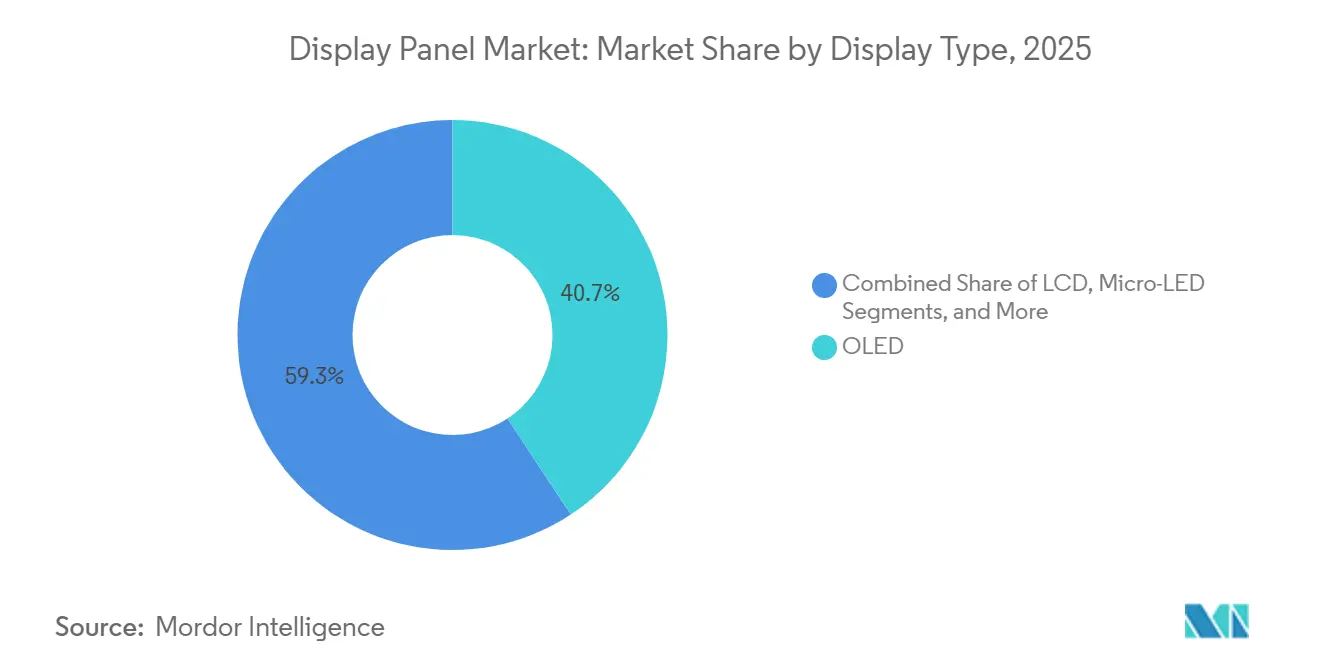

- By display type, OLED led with a 40.74% share in 2025 while Micro-LED is the fastest-growing technology at a 4.35% CAGR through 2031.

- By resolution, 4K panels held 45.36% of 2025 revenue whereas 8K and above is projected to expand at a 5.11% CAGR to 2031.

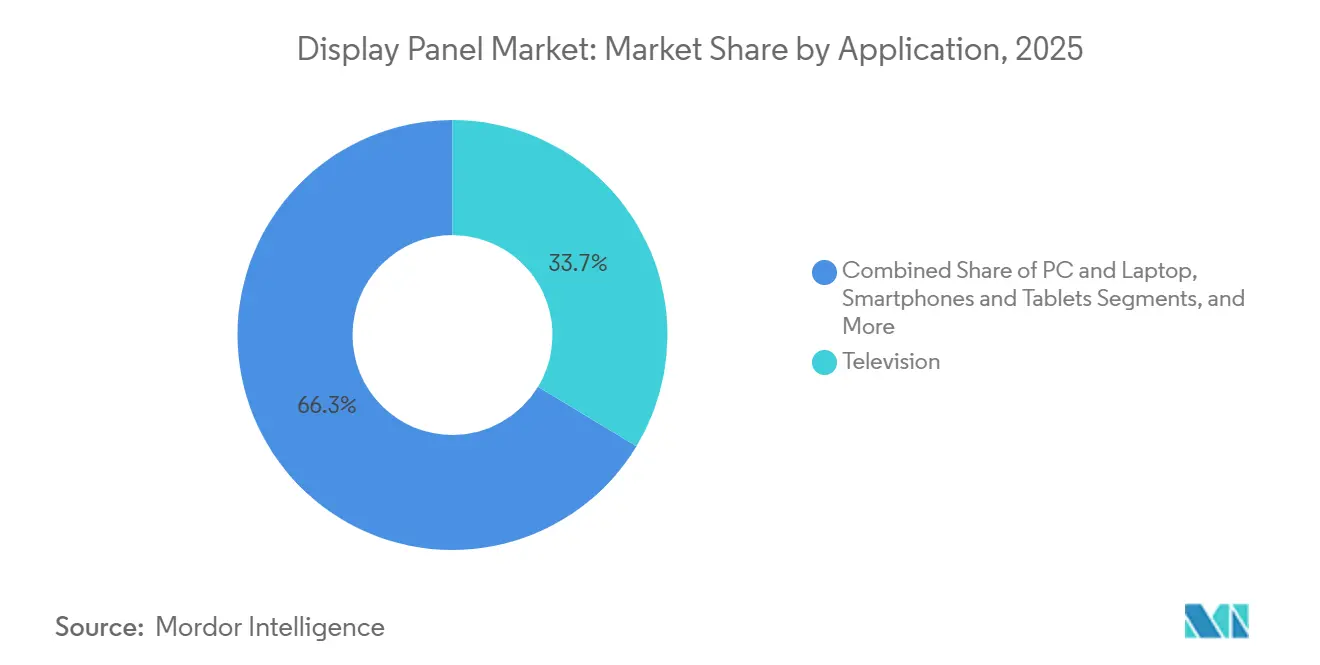

- By application, televisions accounted for 33.66% of 2025 revenue and wearables plus AR/VR are advancing at a 4.86% CAGR.

- By panel size, the 33-65 inch range controlled 36.81% of revenue in 2025 while the 6.1-13 inch category is set to rise at a 5.03% CAGR.

- By geography, Asia Pacific commanded 49.72% of 2025 revenue and the Middle East is the fastest-growing region at a 4.98% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Display Panel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for UHD (4K and Above) TVs | +0.8% | Global, with concentration in North America, Europe, and APAC premium segments | Medium term (2-4 years) |

| Smartphone OEM Pivot to OLED and Micro-LED | +1.1% | Global, led by APAC manufacturing hubs (China, South Korea, Taiwan) | Short term (≤ 2 years) |

| Automotive Cockpit Digitization Wave | +0.9% | North America, Europe, China; spillover to India and South-East Asia | Medium term (2-4 years) |

| Foldable and Rollable Form-Factor Innovation | +0.6% | APAC core (South Korea, China), expanding to Europe and North America | Short term (≤ 2 years) |

| Substrate-Free Holographic Waveguide Displays for Defense Avionics | +0.2% | North America, Europe (NATO members), Israel | Long term (≥ 4 years) |

| Localized EU Incentives for Clean-Room Glass Recycling | +0.3% | Europe (Germany, France, Netherlands) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for UHD (4K) Televisions

4K television penetration continued to rise in 2025 as retail pricing for 55-inch sets dipped below USD 400 in India and Southeast Asia, stimulating first-time purchases while replacement cycles persisted in North America and Europe. Panel makers optimized Gen-10.5 LCD lines for 65-inch 4K cuts, driving cost per area below legacy Gen-8.5 output. Although 8K panel production costs fell 18-20% year-over-year, the format remained a niche because streaming platforms offered under 100 native 8K titles as of late 2025, keeping consumer pull subdued.[1]Samsung Display Co. Ltd., “Investor Relations Presentation,” samsungdisplay.com Brands therefore configured new production lines to alternate between 4K and 8K glass cuts to hedge demand swings. This dual-format flexibility permits rapid output shifts once content ecosystems mature.

Smartphone Pivot to OLED and Micro-LED

Mainstream flagship phones adopted LTPO OLED across entire model line-ups during 2025, trimming display power draw by nearly one-fifth and consolidating share gains for leading OLED suppliers. Gen-6 fabs in South Korea and China achieved yields above 95% on 6-7 inch panels, narrowing cost gaps with high-end LCD. Commercial Micro-LED pilots moved from R&D to limited production in the smartwatch and AR-glasses categories, yet yield rates below 70% for panels larger than 2 inches and a 4-6× cost premium kept volumes modest. Material suppliers logged strong order books for OLED emitter compounds, signaling sustained capital spending through 2027.

Automotive Cockpit Digitization Wave

Electric-vehicle platforms introduced unified glass cockpits spanning 30-50 inches that consolidate instrument cluster, infotainment and passenger displays. This architecture tripled panel area per car and boosted demand for curved, low-reflectance OLED and mini-LED units certified to AEC-Q100 and ISO 26262. Tier-1 suppliers won multiyear contracts exceeding USD 2 billion in 2025, underlining automakers’ shift toward differentiated digital interiors. LTPO backplanes permit always-on graphics while meeting stringent idle-power budgets for battery-electric drivetrains, but qualification lead-times of 18-24 months reinforce barriers to entry.

Foldable and Rollable Form-Factor Innovation

Global foldable-phone shipments climbed 46% year-over-year to 22 million units in 2025 as ultra-thin-glass substrates reduced crease visibility by more than one-third versus early polyimide versions. Dominant suppliers delivered three of every four foldable OLED panels, while Chinese competitors accelerated UTG adoption to support domestic brands.[2]BOE Technology Group Co. Ltd., “BOE Lights Up B16 Gen-8.6 AMOLED Line,” boe.com Rollable prototypes expanded display area without hinge gaps, yet hinge durability remained below the 200,000-cycle threshold demanded for mass-market devices. Consequently, panel makers allocated USD 1-2 billion annually to flexible OLED R&D and forecast foldable or rollable formats to comprise up to 20% of premium mobile shipments by 2030.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex for Gen-10.5 Fabs | -0.7% | Global, concentrated in APAC (China, South Korea, Taiwan) | Medium term (2-4 years) |

| Persistent Glass Substrate Supply Bottlenecks | -0.5% | Global, with acute pressure in APAC OLED hubs | Short term (≤ 2 years) |

| Talent Scarcity in Oxide and LTPO Backplane Engineering | -0.4% | APAC (Taiwan, South Korea, Japan), spillover to China | Medium term (2-4 years) |

| Environmental Regulation Risk on PFAS-Based Polarizer Films | -0.3% | Europe (EU-27), potential expansion to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex for Gen-10.5 Fabs

Gen-10.5 LCD lines required USD 3-4 billion per build-out in 2025, roughly 30% above Gen-8.5 equivalents. Chinese leaders financed simultaneous projects valued at over USD 12 billion, but multiyear payback horizons and elevated depreciation discouraged new entrants. Owners of depreciated Gen-8.5 assets maintained 20-30% cost advantages serving price-sensitive segments, reinforcing a two-tier market and lifting the combined share of the five largest LCD producers to 78% in 2025.

Persistent Glass Substrate Supply Bottlenecks

OLED substrates require ultra-low total thickness variation (TTV) below 1 micron and alkali-free compositions to prevent sodium migration into organic layers, specifications that limit qualified suppliers to three global vendors.[3]AGC Inc., “Investor Relations,” agc.com Lead-times stretched to 16–20 weeks in 2025, delaying OLED ramp-ups by several months and compressing yields on advanced LTPO lines by 5-8 percentage points. A USD 500 million capacity expansion announced for Taiwan will lift substrate output by 30% in 2026, but demand from new Gen-6 fabs is projected to outstrip supply gains, keeping the market tight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Display Type: OLED Dominance Meets Micro-LED Disruption

OLED secured 40.74% market share in 2025, reflecting its entrenchment in premium smartphones, tablets, and automotive displays, where power efficiency and contrast ratios justify cost premiums over LCD alternatives. Samsung Display and LG Display supplied over 85% of OLED panels for flagship smartphones in 2025, leveraging Gen-6 fabs optimized for 6.1-6.7-inch formats that enable LTPO, reducing power consumption by 18-22% versus prior-generation LTPS panels.[4]Apple Inc. "Investor Relations." Accessed February 6, 2026.

Micro-LED is advancing at a 4.35% CAGR through 2031, transitioning from laboratory prototypes to commercial pilots as PlayNitride and Porotech shipped evaluation kits to tier-1 OEMs in 2025 for smartwatch and AR glasses applications. Mass transfer yield rates remain the binding constraint, currently below 70% for panels exceeding 2 inches diagonal versus 95%+ for mature OLED lines, sustaining a 4-6x cost premium that confines Micro-LED to ultra-premium segments in the near term.

By Resolution: 4K Maturity Versus 8K Content Lag

The transition from HD to ultra-high-definition formats reveals a bifurcated market where 4K has achieved mainstream penetration while 8K remains constrained by ecosystem gaps. 4K resolution commanded 45.36% market share in 2025, sustained by replacement cycles in developed markets where installed bases exceed 150 million units and by penetration gains in emerging economies where 4K pricing fell below USD 400 for 55-inch models in late 2025.

8K panel production costs declined 15-20% between 2024 and 2025 due to yield improvements and Gen-10.5 fab efficiencies, yet retail pricing remains 2-3x higher than comparable 4K models, limiting adoption to early adopters and commercial installations. Broadcast infrastructure upgrades lag by 3-5 years in most markets, with only Japan and South Korea deploying 8K terrestrial broadcasts as of 2025, further constraining content supply and delaying mass-market adoption. HD formats benefit from entrenched installed bases exceeding 1 billion units globally, ensuring sustained demand for replacement panels and aftermarket repairs through the forecast period despite migration toward higher resolutions.

By Application: Television Anchor Meets AR/VR Surge

Application segmentation reveals a market transitioning from traditional consumer electronics toward immersive computing and automotive integration. Television applications held 33.66% market share in 2025, anchored by replacement cycles in North America and Europe and first-time purchases in India and South-East Asia, yet growth is decelerating as market saturation approaches in developed economies. Smartphones and tablets command a substantial share driven by OLED adoption across flagship models and foldable form factors that integrate multiple display functions into single panels, with Samsung Display supplying approximately 75% of foldable OLED panels in 2025.

Automotive and transportation applications are expanding faster than the overall market, driven by unified glass cockpits that multiply panel area per vehicle by 2-3x as discrete instrument clusters and infotainment screens converge into single curved displays spanning 30-50 inches. The fastest-growing applications-wearables, AR/VR, and automotive-share common requirements for power efficiency, curved form factors, and high pixel density that favor OLED and emerging Micro-LED architectures over conventional LCD.

By Panel Size: Large Format Stability, Mid-Size Acceleration

Panel size segmentation reflects diverging demand patterns across consumer electronics, automotive, and commercial applications. The 33-65 inch segment captured 36.81% market share in 2025, dominated by television applications where Gen-10.5 fabs in China achieve economies of scale for 55-65 inch 4K panels that retail below USD 400 in emerging markets. The 6.1-13 inch segment is growing at 5.03% CAGR through 2031, driven by foldable smartphones that unfold to 7-8 inch tablet formats, automotive instrument clusters integrating 10-12 inch curved OLED panels, and laptop displays adopting mini-LED backlighting for premium gaming and creative professional segments.

Foldable smartphones shipped 22 million units in 2025, a 46% increase over 2024, with Samsung Display supplying approximately 75% of foldable OLED panels leveraging ultra-thin glass (UTG) substrates that reduce crease visibility by 30-40% versus polyimide films. Large format panels measuring 66 inches and above confront margin pressure as Gen-10.5 fabs optimize cutting patterns for 65-75 inch yields, creating economic disadvantages for 80+ inch production that require custom tooling and lower utilization rates.

Geography Analysis

Asia Pacific captured USD 83.1 billion, or 49.72% of 2025 revenue, as Chinese Gen-8.6 and Gen-10.5 capacity additions expanded annual output by 15 million square meters. China's dominance reflects state-backed financing that enabled BOE Technology Group and TCL CSOT to commit over USD 12 billion combined between 2024 and 2025 for Gen-10.5 capacity, creating cost structures that deter new entrants and favor incumbents with access to subsidized capital. India attracted over USD 3 billion in display manufacturing investments during 2025 under the Production-Linked Incentive (PLI) scheme, with Samsung Display and Dixon Technologies announcing partnerships to establish display module assembly facilities targeting domestic smartphone and television markets.

North America sustains a substantial share through premium television and automotive display demand, yet limited domestic panel production creates dependence on Asian imports that expose supply chains to geopolitical and logistics risks. Europe faces similar constraints with minimal domestic panel manufacturing capacity outside specialized medical and industrial segments, while PFAS restrictions on polarizer films, effective January 2026, add regulatory complexity that Asian manufacturers must navigate to maintain market access. South America confronts infrastructure limitations, with Brazil's import tariffs on display panels reaching 20-25% that incentivize local assembly but deter upstream investments in TFT and color filter production.

Africa remains an emerging market with South Africa and Egypt serving as regional distribution hubs, yet limited local manufacturing and import-dependent supply chains constrain growth relative to other developing regions. Middle East growth concentrates in Saudi Arabia's NEOM project and UAE's Dubai Silicon Oasis, which are developing electronics manufacturing clusters that include display testing and quality assurance capabilities, positioning the region to capture assembly and module integration value even as upstream panel fabrication remains in Asia.

Regulatory Landscape

Regulatory tightening around chemicals, energy efficiency, and cross-border trade continues to shape display panel design and sourcing. In the European Union, Ecodesign requirements for electronic displays under Regulation (EU) 2019/2021 and the accompanying energy labeling rules set product-level thresholds that influence backlight efficiency choices and power-management strategies for OLED and LCD panels. In the United States, TSCA enforcement by the EPA affects substances used in glass substrates, polarizers, and related display chemicals, while Section 232 actions effective January 15, 2026 introduced a 25% ad valorem duty on certain imported semiconductors and derivatives, elevating the importance of tariff classification and regional sourcing for display drivers and components. China’s MIIT published the 2026 edition of the Compliance Management Catalogue for restricted use of hazardous substances in electrical and electronic products, updating RoHS obligations.

Value Chain Analysis

The display panel value chain spans upstream materials and equipment (glass substrates, polarizers, OLED emitter materials, TFT backplane processes, lithography and deposition tools), midstream panel fabrication (Gen-10.5 LCD and Gen-6/Gen-8.6 OLED fabs), and downstream module integration and OEM consumption across TVs, smartphones/tablets, PCs/monitors, automotive, and wearables/AR/VR. A critical upstream constraint remains glass substrate qualification for OLED, where tight TTV specifications and a limited supplier base extended lead-times to 16-20 weeks during 2025, directly affecting yield and ramp schedules on advanced LTPO lines.

Midstream production is characterized by high capital intensity and shifting utilization tied to inventory and trade uncertainty. Panel makers cut fab utilization from above 80% in 1Q 2025 to around 75% by May 2025 amid inventory adjustments and tariff uncertainty, reinforcing more production-to-order behavior and heightening pricing pressure in commoditized LCD categories. Regionally, China’s scale advantages are visible in shipment shares (notably in smartphone and TV panels), while efforts to localize downstream value are expanding elsewhere, including India, where Tata Electronics signed an MoU (March 2025) with Himax Technologies and Powerchip Semiconductor Manufacturing Corporation to develop a display and ultra-low power AI sensing ecosystem, supporting local module/driver and electronics capability alongside display assembly investments referenced in the report context.

Competitive Landscape

The display panel market remains moderately concentrated. Samsung Display, LG Display and BOE controlled a high share of 2025 OLED capacity, leveraging depreciated Gen-8.5 LCD fabs to defend share in cost-sensitive segments while funding OLED and Micro-LED pilots. BOE activated its fifth Gen-8-plus OLED line in December 2025, while Visionox and TCL CSOT announced multibillion-dollar Gen-8.6 commitments for inkjet-printed OLED.

Specialty niches display higher fragmentation. E Ink maintained over 90% of its color electrophoretic shipments by capitalizing on its proprietary microcapsule IP, which expires after 2027. Defense avionics adopted substrate-free holographic waveguides, with Lumus and Kopin securing combined contracts worth USD 50 million.

Future differentiation centers on LTPO backplane engineering and Micro-LED mass transfer yields. Patent filings for flexible OLED substrates surpassed 2,500 in 2025, with Samsung Display and BOE accounting for a considerale share of the applications. Medical-grade 1,000-nit diagnostic displays are an emerging white space where incumbents face pricing pressure from Chinese entrants.

Display Panel Industry Leaders

-

Samsung Display Co., Ltd.

-

BOE Technology Group Co., Ltd.

-

LG Display Co., Ltd.

-

AUO Corporation

-

Innolux Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

IT-focused OLED capacity build-outs open whitespace in notebooks, tablets, and high-end monitors where power efficiency and thin form factors are prioritized alongside higher refresh rates. BOE’s Gen-8.6 OLED B16 facility ramp in Chengdu, lit up in December 2025 and referenced in 2026 industry updates as entering mass production for IT AMOLED, expands larger-area OLED formats beyond smartphones. Parallel investments by LG Display announced in April 2026 for a new 6th-generation OLED line at Paju and by Samsung Display’s A4 OLED site in Asan with June 2026 updates reinforce a supply-side shift toward advanced OLED stacks and backplanes that can support premium IT and automotive requirements.

Performance-driven monitor panels and near-eye XR displays mark a clear commercialization lane where manufacturers are moving beyond concept demonstrations to production-ready specifications and manufacturing plans. In 2026 Samsung Display highlighted 4K 360Hz QD-OLED monitor technology and disclosed mass production plans for 31.5-inch 4K 360Hz QD-OLED panels in 2H 2026, while LG Display began mass production of a 27-inch 240Hz RGB stripe OLED panel for high-end monitors. On XR, Samsung Display showcased RGB OLEDoS technology at AWE USA 2026, aligning with the market shift toward specialized high-PPI microdisplays; these launches create opportunities across equipment, materials, and module integration where yield, reliability, and qualification remain key gating factors.

Recent Industry Developments

- July 2026: BOE Technology Group established a project team focused on Micro LED optical interconnect systems and glass-substrate CPO packaging. The move signals deeper convergence between display manufacturing know-how and advanced packaging approaches, with potential spillover into high-bandwidth, high-density interconnect needs for next-generation display modules and adjacent electronics.

- May 2026: Samsung Display unveiled 4K 360Hz QD-OLED monitor panel technology at SID Display Week 2026 and stated a mass production plan for 31.5-inch 4K 360Hz QD-OLED panels in 2H 2026. The announcement sharpens competition in premium gaming and professional monitors where refresh rate and image quality are key differentiators, and it increases demand for high-performance materials and tighter process control to sustain yield at higher specifications.

- December 2025: BOE lit up its B16 Gen-8.6 AMOLED line in Chengdu ahead of schedule, targeting 48,000 substrates per month by mid-2026. Bringing forward Gen-8.6 AMOLED capacity supports larger-area OLED formats for IT and other applications, and it raises competitive pressure on incumbent OLED suppliers as buyers diversify sources.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the display panel market is defined as revenue earned from panels and modules that create a visual interface in electronic products, across consumer, commercial, and industrial uses, and counted at the panel supply level in USD.

Scope exclusions: We exclude downstream device revenue and most standalone accessories (such as brackets, cables, and external controllers) unless they are sold as part of a panel module.

Segmentation Overview

-

Display Type

- LCD

- OLED

- Micro-LED

- AMOLED

- Other Display types

-

By Resolution

- HD (HD/WQHD/FHD)

- 4K

- 8K and Above

-

By Application

- Smartphones and Tablets

- PC and Laptop

- Television

- Automotive and Transportation

- Wearables and AR/VR

- Industrial, Medical and Others

-

By Panel Size

- ≤6-inch

- 6.1-13-inch

- 13.1-32-inch

- 33-65-inch

- ≥66-inch

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

-

Asia Pacific

- China

- Japan

- India

- South Korea

- South-East Asia

- Rest of Asia Pacific

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

-

Africa

- South Africa

- Egypt

- Rest of Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building a fact base for units, trade flows, and technology adoption, so the model does not rely on one data series. Public sources were used to anchor definitions and trends, such as international trade and tariff statistics, electronics and display industry association publications, government manufacturing indices and industrial output releases, and patent databases that show the direction of innovation.

We also reviewed annual reports, investor presentations, earnings call transcripts, and credible press coverage to track capacity additions, utilization comments, and panel price trends. For context that is harder to collect directly, we used approved paid subscriptions that support company financials and intelligence, news and financials, patent searching, and shipment-level import and export checks where trade visibility was helpful. These sources are illustrative and not exhaustive, and we used additional references to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions and to fill gaps that are common in panel pricing and mix shifts across applications. We spoke with a spread of panel ecosystem participants, including manufacturers, component suppliers, distributors, and large buying organizations, balancing APAC-heavy supply dynamics with demand signals from EMEA and the Americas. When disagreements surfaced, follow-up questions were used to reconcile the reason, and those outcomes were then fed back into the final model inputs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 39% |

| Mid tier: 57% | Functional/Unit leaders: 28% | EMEA: 34% |

| Smaller Players: 14% | Managers: 58% | Americas: 27% |

Market-Sizing & Forecasting

Market sizing was built using a mix of top-down and selective bottom-up checks. On the top-down side, production and trade signals were used to reconstruct the addressable panel demand pool by major applications, and then translated into value using blended pricing by technology and size mix. To keep the totals realistic, we corroborated the results with bottom-up approximations, such as sampled panel shipments multiplied by average selling prices, plus channel checks on mix changes, and then adjusted where the two views did not align.

Key inputs in the model included panel shipment trends by application (smartphones, TVs, PCs, automotive, and wearables), average panel prices and price erosion rates, technology mix shifts (LCD versus OLED and emerging types), resolution and size mix changes that move ASPs, and capacity and utilization commentary that explains supply tightness. Where coverage was thin, gaps were handled using conservative interpolation across adjacent years and by applying mix-weighted pricing rather than single point ASPs.

Forecasts were produced using scenario analysis supported by a simple multivariate regression layer for demand drivers, so that changes in consumer electronics production, vehicle output, and replacement cycles could be translated into panel value movement. Assumptions were then tuned using what interviewees flagged as realistic for near-term pricing, utilization, and technology adoption.

Data Validation & Update Cycle

Validation is done through multiple checks so the final number is not dependent on one assumption. We compare the modeled value trend against independent signals, such as shipment momentum, pricing direction, and capacity narratives, and then investigate any large variance before the numbers are finalized. Cross-tab checks are also run across technology, size, and application mixes to ensure that the implied ASPs and growth rates remain practical.

Before publication, the work goes through a multi-step internal review, including logic checks, year-on-year variance screens, and a final pass for currency consistency and unit alignment. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major capacity shifts, step changes in pricing, or sharp demand swings. Right before delivery, an analyst revisits the latest public disclosures so clients receive the most current view available.

Mordor Intelligence's Display Panel Market Size Versus Other Published Estimates

Published market sizes for display panels often do not match because the scope line is drawn differently and the pricing build is handled in different ways. The biggest differences usually come from whether the estimate is counting only panels, or it is also folding in more of the finished device value, and from how fast ASP declines are assumed in years when the mix changes.

Some sources report a broader number that can lean toward device-led revenue, or they apply an aggressive growth case that assumes sustained price stability across technologies. In Mordor Intelligence, panels are counted at the module and panel revenue level with mix-based ASP progression, and the total is checked against application shipments and capacity signals so outlier pricing assumptions are less likely to pass through.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 172.73 B (2026) | |

| Regional Consultancy A | USD 136.64 B (2024) | Uses an earlier base year and can understate the step-up from post-2024 mix upgrades, and the scope description is less explicit on whether module-level value is consistently captured across applications. |

| Global Consultancy B | USD 149.99 B (2025) | Applies a broader segmentation lens that may treat certain display categories and form factors as a single pooled market, which can change ASP weighting and inflate growth when premium mixes are assumed to scale quickly. |

The table shows that the spread mainly comes from year selection and what is included in the value chain, and then it is amplified by how ASPs are projected when technology mix is shifting. By keeping inputs tied to shipment direction, size and resolution mix, and realistic price erosion patterns, the final number stays traceable to repeatable steps rather than a single high-level growth assumption.

Key Questions Answered in the Report

How large will the display panel market be by 2031?

It is projected to reach USD 210.68 billion by 2031, growing at a 4.05% CAGR between 2026 and 2031.

Which technology leads unit shipments today?

OLED held a 40.74% share of 2025 revenue, driven by broad smartphone and television adoption.

What is the fastest-growing resolution segment?

8K and above panels post the highest forecast growth at a 5.11% CAGR through 2031, although content scarcity still limits volumes.

Which region will expand the quickest?

The Middle East is forecast to grow at 4.98% CAGR as Saudi Arabia and the UAE invest in local display assembly capacity.

Page last updated on: