Morocco Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

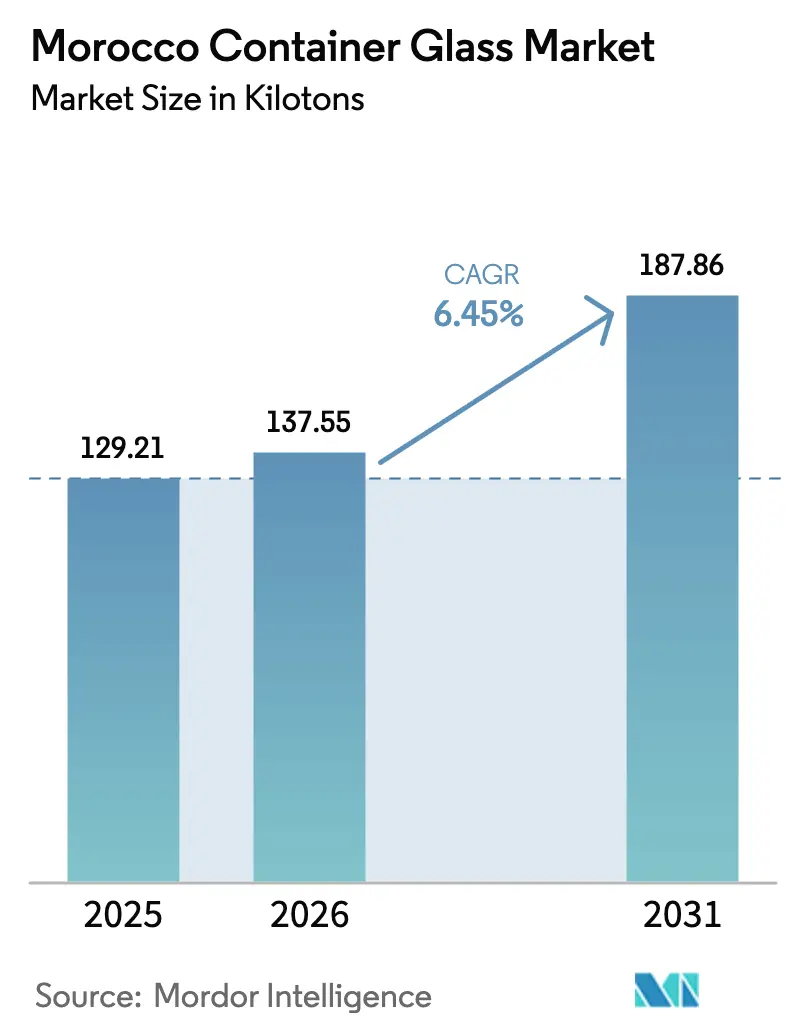

| Base Year Market Size (2025) | 129.21 kilotons |

| Market Volume (2026) | 137.55 kilotons |

| Market Volume (2031) | 187.86 kilotons |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Container Glass Market Analysis by Mordor Intelligence

Morocco container glass market size in 2026 is estimated at 137.55 kilotons, growing from 2025 value of 129.21 kilotons with 2031 projections showing 187.86 kilotons, growing at 6.45% CAGR over 2026-2031. Steady growth is driven by rising urban incomes, beverage premiumization, and Morocco’s position as a regional export hub that supplies compliant glass packaging to both European Union and U.S. buyers. Sustained investments in Tanger Med port, high-speed rail, and industrial acceleration zones help lower time-to-market and reinforce the country’s role as a bridge between sub-Saharan Africa and Europe. Policy tailwinds, most notably the 2024 circular economy law with mandatory recycled-content targets, push manufacturers to upgrade cullet processing lines, integrate renewable power, and differentiate themselves on sustainability credentials. At the same time, tourism rebounds and preparations for the 2030 FIFA World Cup boost on-trade demand for premium glass bottles across hotels, bars, and restaurants in Casablanca, Marrakech, and emerging coastal resorts.

Key Report Takeaways

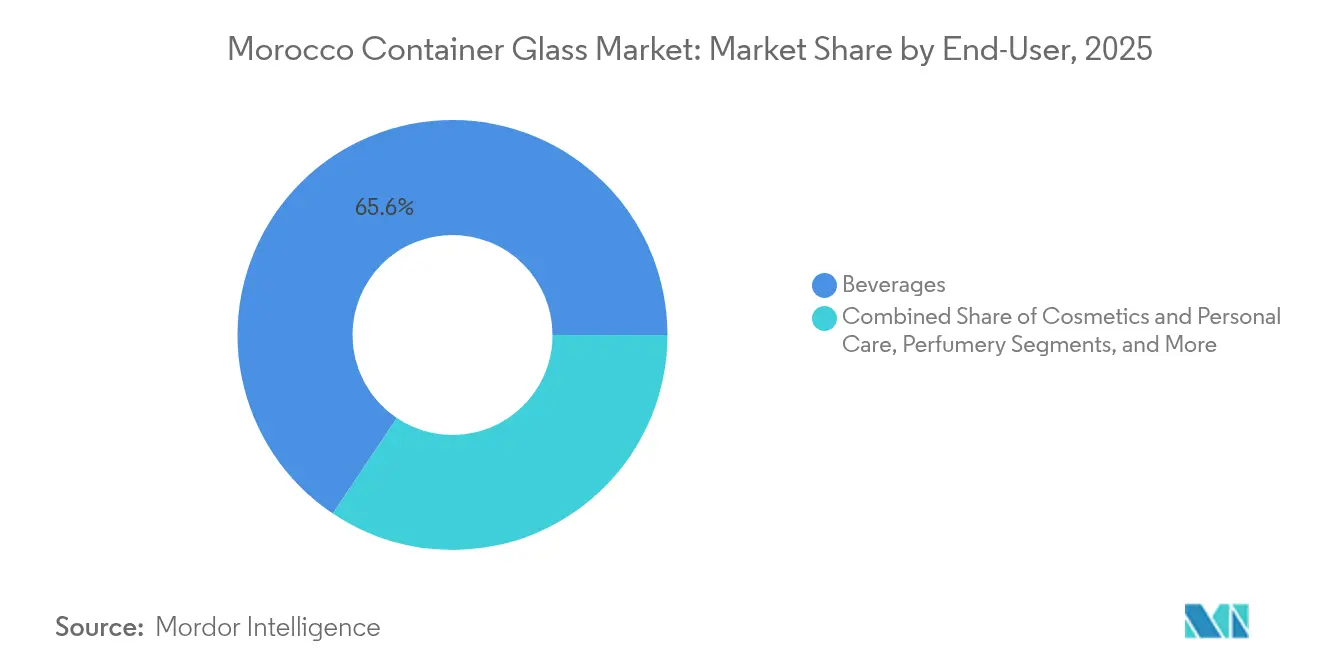

- By end-user, beverages captured 65.60% of the Morocco container glass market share in 2025.

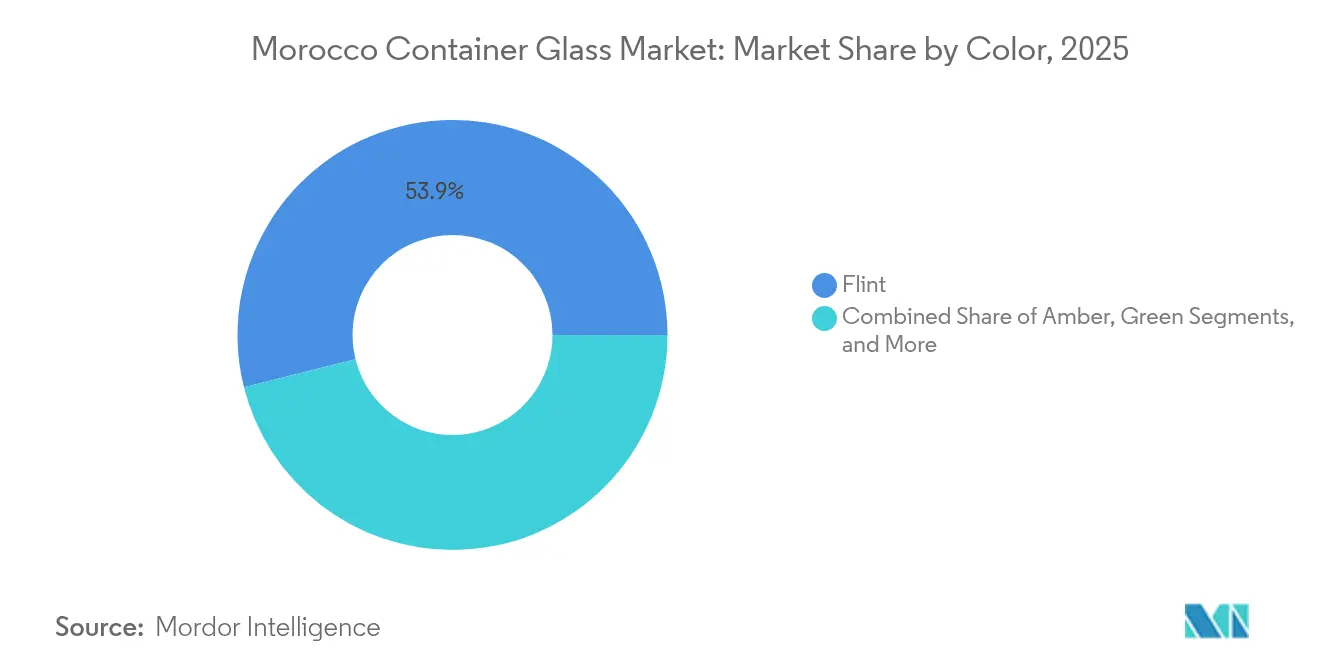

- By color, the Morocco container glass market for amber glass is projected to grow at a 7.42% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Morocco Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanisation and premiumisation of beverages | +1.2% | National, concentrated in Casablanca-Rabat corridor | Medium term (2-4 years) |

| Export-oriented agri-food growth (olive oil, fruit preserves) | +0.9% | National, with export focus to EU markets | Long term (≥ 4 years) |

| Mandatory recycled-content targets (circular-economy law 2024) | +0.8% | National implementation with regional variations | Short term (≤ 2 years) |

| Tourism and 2030 FIFA World Cup–linked on-trade demand | +1.1% | National, concentrated in major cities and tourist zones | Medium term (2-4 years) |

| Renewable-energy build-out lowering furnace OPEX | +0.7% | National, with highest impact in solar-rich southern regions | Long term (≥ 4 years) |

| Craft and niche perfumery boom in Marrakech and Casablanca | +0.3% | Regional, focused on Marrakech and Casablanca | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Beverage Premiumization

Morocco’s urbanization rate increased to 65.2% in 2024 and is projected to reach 67.8% by 2030, concentrating jobs and purchasing power in cities that already generate 80% of the country's productive output. Urban consumers in Casablanca-Settat are increasingly trading up to premium beer, wine, and functional drinks packaged in glass, which signals quality and sustainability. Although Kantar recorded 12% volume declines in fruit juices in 2024, glass bottles remain the preferred pack for value-added SKUs, where clarity and brand embossing are key. Beverage firms have responded by piloting sleek-panel flint bottles that reduce weight by 8% compared to 2023 formats, thereby lowering freight costs without compromising premium cues. As beverage assortments diversify into craft sodas and hard seltzers, the Morocco container glass market gains incremental orders for smaller-size bottles optimized for portion control.

Export-Oriented Agri-Food Growth

Morocco exported 77,700 tonnes of table olives in 2023, ranking third globally and underscoring the strategic importance of value-added agri-food exports. European retailers are increasingly demanding recyclable glass jars that deliver extended shelf life and premium shelf presence, commanding price points of EUR 12–30/kg (USD 13–33/kg) in specialty aisles. The national Generation Green 2020-2030 program channels USD 40 billion into desalination and irrigation, fostering higher-value olive, citrus, and berry clusters that fuel steady demand for food-grade flint jars. Preferential access under the EU Association Agreement and the US-Morocco Free Trade Agreement gives local fillers an edge in terms of duties, further propelling the Moroccan container glass market across export lanes. To capture the opportunity, Société d’Exploitation de Verreries au Maroc (SEVAM) invested in a new narrow-neck press-and-blow line with a 150 t/day capacity, dedicated to 314-ml olive jars that comply with U.S. FDA and EU migration limits.

Mandatory Recycled-Content Targets

The 2024 circular economy law obliges container glass to incorporate progressively higher recycled content, starting at 20% cullet in 2025 and rising to 35% by 2028. Current municipal recycling captures only 6% of glass waste, leaving a structural cullet deficit that prompts producers to bankroll buy-back schemes and color-sorted collection centers. Verallia is piloting a closed-loop program in Rabat, issuing QR-tagged crates to on-trade accounts that return empties for centralized color sorting, which has lifted cullet yield by 12 percentage points in the first six months.[1]Verallia, “2025 First Quarter Results,” verallia.com Compliance drives cost savings, as every 10% substitution of cullet reduces furnace energy by 2.5% and lowers CO₂ emissions by 5%. The regulatory push positions the Morocco container glass industry to supply EU buyers seeking low-carbon packaging certified under forthcoming Carbon Border Adjustment Mechanism rules.

Tourism and 2030 FIFA World Cup Demand

Morocco welcomed a record 14.6 million tourists in 2024, generating USD 10 billion (MAD 100 billion) in receipts, equivalent to 7.4% of the country's GDP. Hotel pipelines in Marrakech, Tangier, and the northern coastal corridor added more than 11,000 keys between 2024 and 2025, most of which specified glass for in-room water, minibar spirits, and tabletop condiments. Host-city tenders for the 2030 FIFA World Cup require beverage sponsors to use packaging with at least 40% recycled content and demonstrable recyclability, a criterion that intrinsically favors glass over multilayer PET. Craft breweries in Agadir and Fez have responded by contracting local flint bottle producers for limited-edition 250-ml formats that feature national motifs, thereby deepening volumes in the Moroccan container glass market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastics substitution and lightweight PET proliferation | -1.4% | National, with higher impact in cost-sensitive segments | Medium term (2-4 years) |

| Energy-price volatility despite renewables ramp-up | -0.8% | National, with regional variations based on grid connectivity | Short term (≤ 2 years) |

| Structural cullet shortage and informal recycling chain | -0.6% | National, with acute shortages in industrial centers | Long term (≥ 4 years) |

| High domestic freight costs from port to inland fillers | -0.5% | National, with highest impact on inland manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plastics Substitution and Lightweight PET Proliferation

Elopak’s 2025 goal to double addressable volumes in Morocco via fiber-based cartons exemplifies organized substitution that chips away at commodity juice and dairy glass demand. Plastic converters have reduced 1-L PET bottle weights from 36 g in 2020 to 29 g in 2024, decreasing transport fuel consumption per unit by up to 24% and attracting price-sensitive fillers to regional depots. Although the 2016 Zero Mika law curbed the use of single-use plastic bags, enforcement gaps revealed the difficulty of shifting entrenched habits, suggesting that anti-plastic activism alone cannot guarantee a reduction in glass volume. Beverage multinationals hedge by running dual glass-PET lines, allowing rapid format switching that raises planning uncertainty for domestic glass plants with long furnace cycles. In response, glassmakers are prototyping 190-ml returnable bottles that promise 25 rotations and 35% lower lifecycle emissions than their PET equivalents, incentivizing the hospitality and foodservice (HORECA) channels to stick with glass.

Energy-Price Volatility Despite Renewables Ramp-Up

Morocco aims to achieve 52% renewable electricity by 2030; however, grid integration and storage constraints lead to spot-market volatility that squeezes energy-intensive melters. A standard 300-t/day furnace incurs energy costs that account for nearly 30% of ex-factory bottle pricing, rising sharply when LNG imports surge. Solar-thermal feasibility studies in Zagora and Ouarzazate indicate a levelized heat cost below 2.5 cents/kWh-thermal; however, deployment hinges on securing long-term purchase agreements, which few container glass producers have achieved. Electric boosting increases melt efficiency to 84%, yet concerns about capital intensity and grid reliability delay adoption, forcing furnace rebuild deferrals beyond 2026. As a result, producers hedge their fuel with multi-year LNG contracts, sacrificing some variable-cost flexibility but preserving baseline melt capacity, which is vital for the Moroccan container glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Retain Volume Leadership While Cosmetics Surge

Beverages accounted for 65.60% of Morocco's container glass market share in 2025, contributing to the total throughput for both alcoholic and non-alcoholic fillers. The segment’s momentum rests on regulatory mandates that enforce the use of glass for vintage wine denominations and the integrity of spirit tax stamps, locking in baseline demand despite category fluctuations. Craft beer start-ups benefit from duty differentials on small-batch production, prompting orders for 330-ml amber bottles with embossed branding that commands shelf premiums in tourist districts. Non-alcoholic beverage fillers feel margin pressure as soft-drink volumes slip, yet they continue to specify 1-L lightweight flint bottles for premium mixers targeting hospitality accounts.

Parallel to the beverages, cosmetics, and personal care markets, the market is projected to log the fastest 7.15% CAGR through 2031, underpinned by Morocco’s ascent as an aroma hub for niche perfumeries centered in Marrakech. Fragrance exporters favor high-clarity flint flacons with thick heels and decorative metallization, which raises the average revenue per ton compared to standard beverage ware. Pharmaceutical demand adds stability, as Moroccan drug packers prefer type-II amber vials to meet International Council for Harmonisation guidelines, nudging the Moroccan container glass industry toward higher-margin medical packaging lines.

By Color: Flint Dominates While Amber Accelerates

Flint controlled 53.90% of the Moroccan container glass market in 2025, thanks to its versatility across the food, beverage, and cosmetics sectors. Exporters of extra-virgin olive oil insist on transparent flint to showcase the color grades prized by European buyers, which translates to sustained orders for 500-ml Dorica and Marasca formats. Glassworks optimizes optical sorting to capture mixed-color cullet and repurpose it into flint batches, bolstering sustainability claims amid recycled-content mandates.

Amber, although smaller, is forecast to grow at a 7.42% CAGR through 2031, driven by demand for UV-blocking performance from pharma, craft beer, and specialty spirits. Ardagh’s 2024 acquisition of Consol unlocks proprietary amber formulations with refined Fe2O3 profiles that cut melt temperatures by 15 °C, appealing to energy-intensive furnaces in Morocco. Green glass usage remains primarily in still-wine bottles but faces substitution by bag-in-box for economy SKUs, while blue and other niche tints serve limited-edition perfumery, collectively contributing less than 3% to the Moroccan container glass market size.

Geography Analysis

The Moroccan container glass market is concentrated along the Casablanca-Rabat economic axis, which accounts for roughly one-third of GDP and hosts the bulk of fillers and decorators that consume daily truckloads of flint and amber ware. Proximity to Mohammed V airport and an upgraded 3 million TEU seaport shortens replenishment cycles for imported soda ash and export shipments of finished bottles to Iberian co-packers.

Tanger Med’s expansion to 9 million TEU capacity establishes northern Morocco as a transshipment hub that funnels glass containers into West African growth markets such as Senegal and Côte d’Ivoire. Inland clusters in Marrakech and Fez specialize in artisanal perfumery and craft beverage startups, collectively representing 11.60% of the Morocco container glass market size in 2025. However, high domestic freight rates often exceeding USD 0.11 per ton-kilometer dilute margins for suppliers trucking bottles from coastal furnaces to these highland fillers.

Southern coastal zones, such as Agadir and Laayoune, capitalize on desalination-backed agri-food processing, also demanding food-grade flint jars for seafood paste and citrus preserves bound for EU buyers. As the renewable-energy buildout accelerates, solar-rich Saharan regions may attract new all-electric furnaces that lower delivered cost into West African corridors, diversifying geographic production footprints across the Morocco container glass market.

Competitive Landscape

The Moroccan container glass market remains moderately fragmented, featuring a mix of domestic incumbents and European multinationals that co-locate warehousing and sales offices rather than establishing new greenfield furnaces. SEVAM operates the only integrated plant with multiple IS machines, leveraging 90 years of tooling expertise and deep relationships with olive and argan oil fillers to defend its market share against importers.

Verallia, Ardagh, and Vetropack service Moroccan demand by backhauling truckloads from Spanish plants across the Strait of Gibraltar within 48 hours, balancing currency risk while testing local volume thresholds that could justify future brownfield builds. Competitive advantage is increasingly hinging on sustainability: Verallia’s Rabat cullet-recovery pilot boosts recycled content to 54%, meeting EU buyer requirements ahead of the 2026 compliance deadline.

Domestic players counteract with shorter lead times, custom embossing, and smaller production runs, which enable craft beverages to switch labels frequently, a flexibility that giant regional furnaces struggle to match. New entrants in alternative packaging, namely Elopak’s fiber cartons, fuel competitive cross-pressures but also motivate glassmakers to market the lifecycle CO₂ benefits of high-rotation returnable bottles, thereby safeguarding their share in premium channels within the Moroccan container glass market.[3]Elopak, “Annual Report 2024,” elopak.com

Morocco Container Glass Industry Leaders

Société d’Exploitation de Verreries au Maroc

Saverglass SAS

Feemio Group Co., Ltd

Ardagh Group S.A

Verallia SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Verallia confirmed volume recovery in Q1 2025 and ruled out additional permanent furnace shutdowns.

- February 2025: Morocco’s Ministry of Energy Transition published updated transmission tariffs that facilitate private solar power projects for industrial users, including glassworks.

- January 2025: Elopak continued to integrate Naturepak in Morocco, scaling fiber-based packaging lines that compete with glass in the dairy and juice sectors.

- November 2024: Foreign direct investment revenues reached MAD 43.195 billion (USD 4.3 billion), with industrial allocations favoring potential capacity addition in glass packaging.

Morocco Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

The Morocco container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the current size of the Morocco container glass market?

The Morocco container glass market size stands at 137.55 kilotons in 2026 and is forecast to reach 187.86 kilotons by 2031.

Which end-user segment generates the most demand?

Beverages dominate with 65.60% share in 2025, led by premium beer, wine, and soft-drink applications.

How fast is the cosmetics and personal care segment growing?

Cosmetics and personal care record the fastest 7.15% CAGR through 2031, fueled by Morocco’s expanding perfumery exports.

What impact will the 2024 circular economy law have?

The law mandates recycled-content targets that lift cullet demand and compel manufacturers to upgrade collection and sorting infrastructure quickly.

Which color segment shows the highest growth momentum?

Amber glass leads in growth with a 7.42% CAGR on rising pharmaceutical and craft beverage demand.

How will the 2030 FIFA World Cup influence demand?

Stadium and hospitality build-outs tied to the event are expected to boost hore-ca glass bottle volumes, especially in premium beverage categories.

Page last updated on: