Egg Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

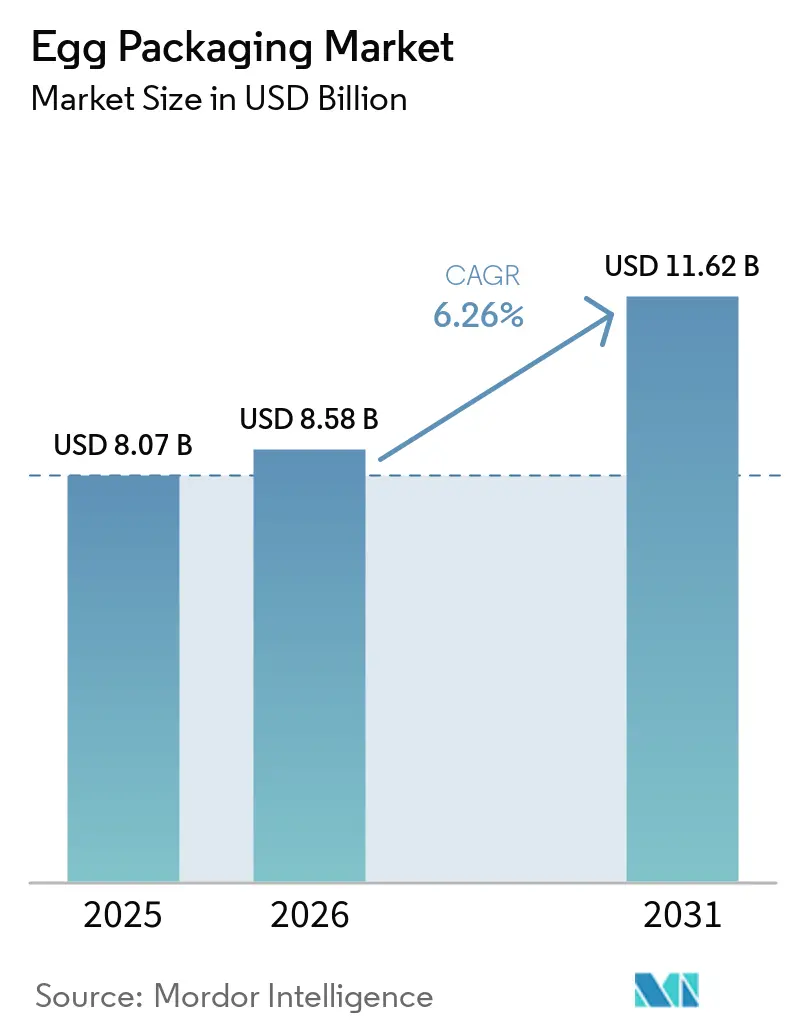

| Market Size (2026) | USD 8.58 Billion |

| Market Size (2031) | USD 11.62 Billion |

| Growth Rate (2026 - 2031) | 6.26% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egg Packaging Market Analysis by Mordor Intelligence

The egg packaging market size is projected to be USD 8.07 billion in 2025, USD 8.58 billion in 2026, and reach USD 11.62 billion by 2031, growing at a CAGR of 6.26% from 2026 to 2031. The egg packaging market is expanding even while avian influenza continues to disrupt flock availability and short-term purchase planning in several producing countries. Demand remains supported by steady egg consumption and by rising poultry output in Asia, South America, and Africa, where packaged retail formats are still gaining penetration. The shift from plastic formats toward molded fiber is also changing capital allocation, because larger converters can add compliant capacity and material flexibility faster than smaller regional suppliers. Online fulfillment, modern grocery retail, and traceability rules are raising performance requirements for pack strength, denesting consistency, and print capability across the egg packaging market. Competition therefore depends on scale, local proximity to egg farms, raw material access, and the ability to serve both cost-sensitive and premium retail programs across regions.

Key Report Takeaways

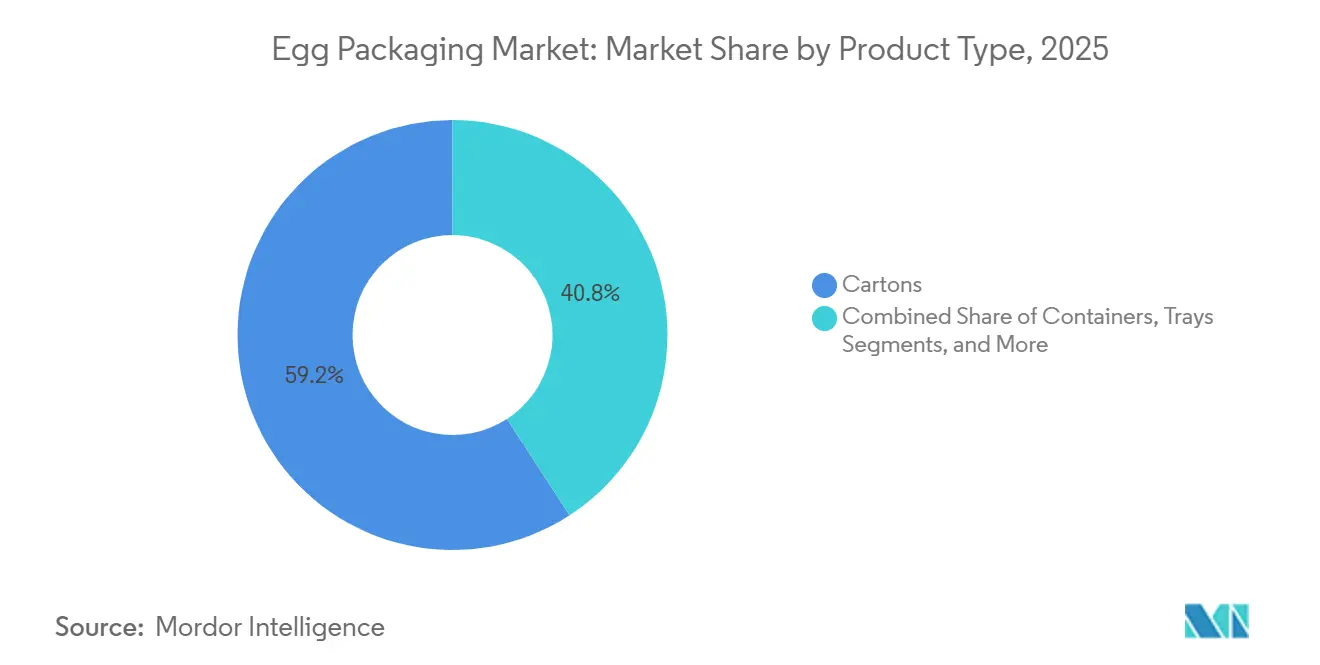

- By product type, cartons accounted for 59.16% of the egg packaging market share in 2025.

- By material type, the egg packaging market for molded fiber is projected to grow at a 7.57% CAGR through 2031.

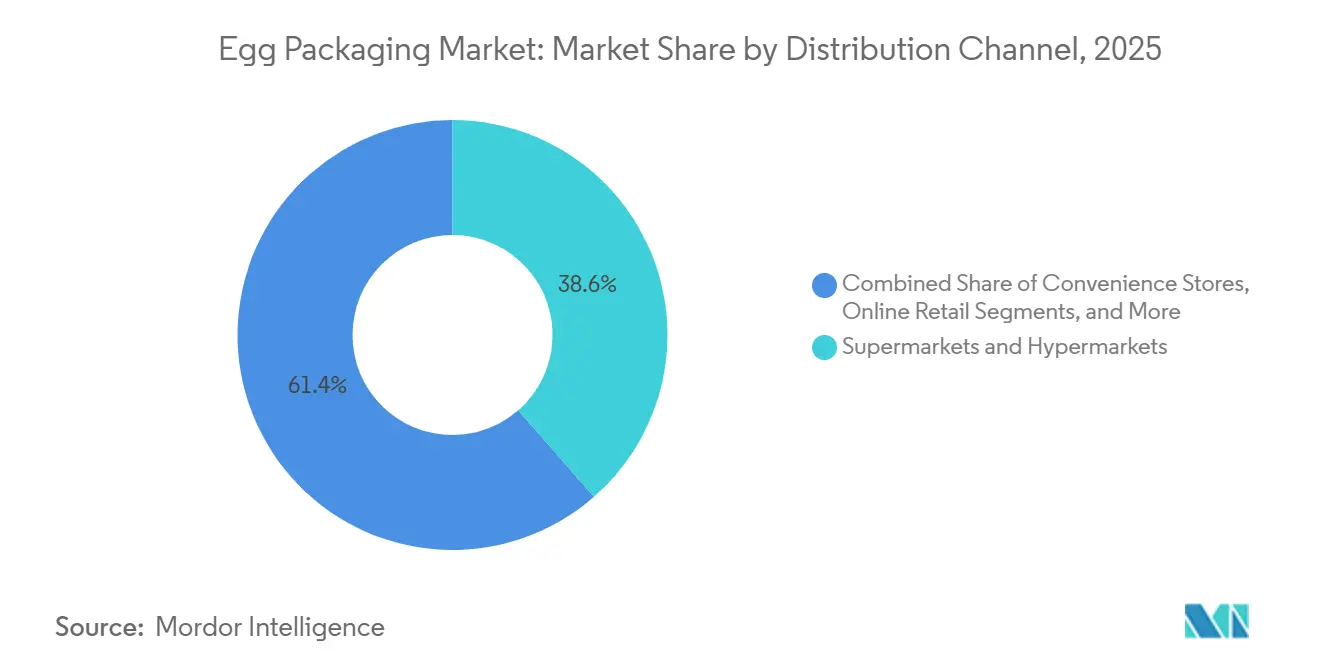

- By distribution channel, supermarkets and hypermarkets accounted for 38.56% of the egg packaging market in 2025.

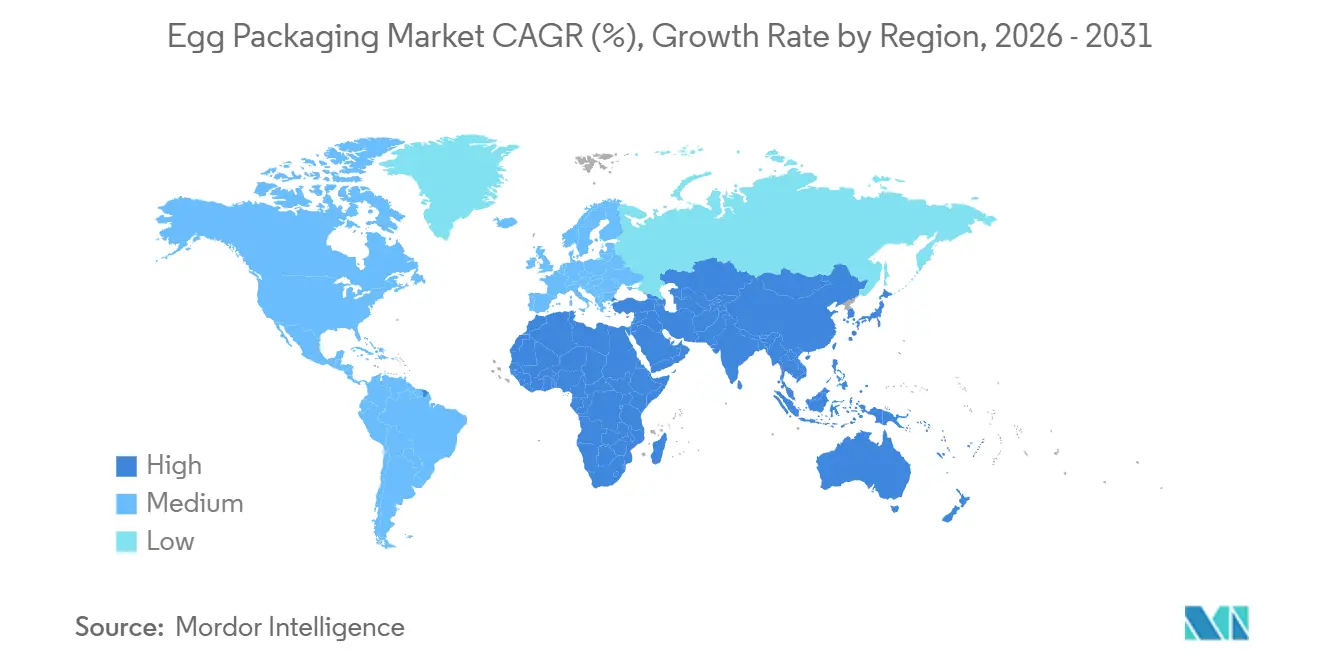

- By geography, the egg packaging market for Asia-Pacific is projected to grow at a 7.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Egg Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Egg Consumption and Poultry Output | +1.6% | Global, with core volume gains in Asia-Pacific, South America, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Accelerating Shift Toward Molded Fiber and Recyclable Packs | +1.3% | Global, with stronger near-term pull in Europe, North America, and Australia and New Zealand | Medium term (2-4 years) |

| Expansion of Modern Grocery Retail and Online Grocery Fulfillment | +0.9% | North America and Europe for online retail, Southeast Asia for modern trade expansion, and South America for urban supermarket growth | Medium term (2-4 years) |

| Tightening Food Safety, Labeling, and Traceability Requirements | +0.7% | North America, Europe, Asia-Pacific, and export-oriented producing countries | Medium term (2-4 years) |

| Premium Packaging Demand for Cage-Free, Organic, and Functional Eggs | +0.6% | North America, Western Europe, Australia and New Zealand, Japan, and South Korea | Short-term (≤ 2 years) and medium-term (2-4 years) |

| Automation-Ready Pack Designs for High-Speed Grading and Fulfillment | +0.4% | North America and Europe, with gradual adoption in the Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Egg Consumption and Poultry Output

Global hen egg production exceeded 91 million MT in 2023, which kept the base demand floor for the egg packaging market broad, even when flock losses affected some producing regions. Asia accounted for more than 70% of global egg output, and China alone accounted for nearly half of global production, keeping Asia at the center of packaging demand growth. The OECD-FAO Agricultural Outlook 2025-2034 stated that protein consumption from meat, dairy, and eggs will continue rising in lower-middle-income countries, which supports additional packaging demand as retail systems formalize.[1]OECD and FAO, “OECD-FAO Agricultural Outlook 2025-2034,” OECD/FAO, fao.org India ranked second globally in egg production in 2023, with an 8% share, and its shift from loose egg sales to packaged retail formats is increasing packaging intensity faster than production alone would suggest. HPAI also changed trade flows between 2022 and 2024, increasing the role of standardized protective packs in cross-border shipments and strengthening the long-term demand profile of the egg packaging market.

Accelerating Shift Toward Molded Fiber and Recyclable Packs

The egg packaging market is moving toward molded fiber and paper-based formats as retailers, regulators, and consumers place greater emphasis on recyclable, lower-plastic packaging. In the European Union, marketing and packaging rules have continued to increase the compliance burden on conventional plastic formats, supporting a broader migration toward fiber-based alternatives in egg packs. Germany reported a 4.2% increase in egg production in 2024, while free-range and organic output also grew, which supported formats that better match premium and sustainability-led shelf positioning. Japan has also been moving through a policy-led packaging transition, with plastic resource circulation measures and retailer decarbonization programs drawing more attention to molded pack formats. Cascades reinforced this direction in June 2024 when it launched Fresh GUARD EnVision, a hybrid design that combines a molded pulp base with a recycled-board sleeve, showing that the egg packaging market is moving toward integrated sustainable formats rather than a simple one-for-one material switch.

Expansion of Modern Grocery Retail and Online Grocery Fulfillment

The egg packaging market is also changing because modern grocery retail and online fulfillment expose eggs to more handling steps and more demanding logistics routines than older bulk retail models. U.S. online grocery sales reached USD 12.7 billion in December 2025, up 32% year over year, which signaled that fragile categories such as eggs are now part of mainstream digital grocery purchasing rather than a niche use case. Amazon also expanded same-day fresh grocery delivery and micro-fulfillment testing for perishables in several U.S. cities, which showed that delivery speed and dense order handling are becoming standard operating expectations. That shift matters because eggs face extra pick, tote, transfer, and last-mile handling in digital channels, which raises the value of stronger lids, taller sidewalls, and packs that hold shape through repeated movement. In Southeast Asia and South America, modern trade expansion is also shifting sales from loose-egg presentation to labeled retail packs, broadening the addressable market for egg packaging even before online grocery reaches North American levels.

Tightening Food Safety, Labeling, and Traceability Requirements

Traceability rules are pushing the egg packaging market toward higher-specification surfaces and better printing capability across both cartons and trays. In the United States, shell eggs remain on the Food Traceability List, and the FDA requires firms to maintain traceability lot codes and key data elements linked to critical tracking events under the FSMA traceability framework. In the European Union, Commission Delegated Regulation (EU) 2023/2464 shifted egg marking to the production site from November 2024, which changed how packaging suppliers need to think about on-pack data placement and production-line compatibility. These requirements spread beyond domestic markets because export-oriented producers in countries supplying Europe and North America must align with importer expectations on labeling and traceability. The result is a clearer divide inside the egg packaging market between low-spec commodity packs and higher-margin formats that can carry variable data, QR codes, and machine-readable coding without adding process complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pulp, Recycled Paper, And Resin Price Volatility | -1.2% | Global, with strong exposure in Europe, North America, and import-dependent Asia-Pacific markets | Short-term (≤ 2 years) and medium-term (2-4 years) |

| Rising Compliance Costs for Food-Contact and Packaging-Waste Rules | -0.8% | Europe, North America, and the Asia-Pacific | Medium term (2-4 years) |

| Avian Influenza-Driven Egg Supply Swings and Carton Demand Volatility | -0.6% | North America, Europe, and the affected export corridors | Short term (≤ 2 years) |

| Food-Contact PCR Scarcity and Approval Bottlenecks | -0.3% | Europe, North America, and the Asia-Pacific | Medium term (2-4 years) and long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pulp, Recycled Paper, and Resin Price Volatility

Input cost volatility remains one of the clearest operating restraints in the egg packaging market because fiber, paper, and resin swings can pass through converter margins faster than customer contracts adjust. Fastmarkets reported a sharp rise in European paper packaging cost indices during 2025, which reflected how quickly energy and fiber inputs can move against pack producers. In North America, Packaging Dive reported containerboard price increases of up to USD 70 per ton entering 2025, which continued to put pressure on corrugated and paper-based packaging economics. PaperIndex also noted that pulp commonly accounts for 40-60% of kraft paper production costs, which explains why even short spikes in fiber pricing quickly affect mill-gate economics and converter margins. Smaller regional converters are more exposed when these cycles persist, because they usually have less buying leverage, less hedging capacity, and fewer options to rebalance between materials within the egg packaging market.

Rising Compliance Costs for Food-Contact and Packaging-Waste Rules

The egg packaging market also faces rising compliance costs as recycled food-contact rules and packaging-waste requirements become more detailed across major regions. In the European Union, Regulation (EU) 2022/1616 and the 2025/2269 correction tightened the authorization framework for recycled plastic materials in food-contact applications, while EFSA continues to assess approved recycling technologies and process pathways. In the United States, the FDA's No Objection Letter process for post-consumer recycled plastics remained active through 2025 and 2026, confirming demand for compliant recycled-content packaging but also highlighting the time and documentation burden on producers. These approval systems favor larger companies that can fund testing, regulatory review, and repeated submissions across multiple material streams. Smaller suppliers, therefore, face a harder path to product innovation, and that slows the pace at which new entrants can scale within the egg packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cartons Hold the Lead While Trays Gain from Cage-Free Logistics

Cartons held 59.16% of the egg packaging market share in 2025, while trays are projected to record the fastest CAGR at 7.63% from 2026 to 2031. Cartons remain central to retail-led supply chains because they offer strong brand visibility, familiar consumer handling, and broad compatibility across supermarket, hypermarket, and specialty shelf formats. Trays are gaining popularity faster because cage-free and free-range systems rely heavily on 30-egg transport formats for farm-to-grader movement, food-service supply, and higher-volume handling. High-speed grading equipment is also shaping product design, as SANOVO's OptiGrader 600 can process up to 216,000 eggs per hour and therefore requires packs with stable dimensions and reliable denesting performance.[2]SANOVO Technology, “OptiGrader 600 Egg Grading Machine | Large-Scale Hygiene and Precision,” SANOVO Group, sanovogroup.com Containers and other formats remain present in premium and specialty programs, but they do not alter the broad structure of the egg packaging market during the forecast period.

What matters operationally is that cage-free systems often produce wider egg-size variation than conventional cage operations, which makes shock-absorbing tray geometry more useful in earlier handling stages. That pattern supports tray demand even before eggs reach branded retail packs, so the growth driver is embedded in production practices rather than in merchandising preferences. Within the egg packaging market, product development is also moving toward hybrid structures that combine transport protection with branded shelf appeal in a single pack. Cascades illustrated that direction with Fresh GUARD EnVision, which paired a molded pulp base with a coated recycled-board sleeve and showed how tray and carton functions are starting to overlap in higher-value formats. The egg packaging industry is therefore placing more value on designs that can reduce changeovers, support automation, and serve both retail presentation and distribution protection without forcing separate packaging systems.

By Material Type: Molded Fiber Leads While Plastic Retains Selected Use Cases

Molded fiber accounted for 43.64% of the egg packaging market size in 2025 and is projected to expand at a 7.57% CAGR through 2031. That combination of leading share and leading growth reflects more than a short material cycle, because sustainability mandates, retailer preferences, and cage-free branding are moving in the same direction. Germany's 2024 increase in egg production, together with faster growth in free-range and organic categories, supported fiber-based sourcing patterns that fit premium positioning and recyclable-pack expectations. Plastic still retains meaningful relevance where visibility, moisture resistance, and lower-cost distribution remain important, especially in markets where waste-paper recycling infrastructure is still limited. Paper-based folded cartons are also gaining ground in premium branded segments, while EPS continues to lose ground in more regulated markets.

The strategic issue in this part of the egg packaging market is no longer just fiber versus plastic, as approved recycled-plastic pathways are now shaping investment choices within the egg packaging industry. In Europe, EFSA and the recycled-plastic regulations continue to set the pace for which technologies can move into food-contact use, and in the United States, the FDA process plays a similar gatekeeping role for post-consumer recycled materials. Those approval costs are easier for large converters to absorb, which gives them an advantage in both recycled-plastic development and multi-material portfolio planning. At the same time, plastic remains functionally relevant in humid environments and in value-focused channels, so full substitution will not happen evenly across regions. Material competition in the egg packaging market will therefore remain active, but the strongest momentum still sits with molded fiber and recyclable paper-led solutions.

By Distribution Channel: Supermarkets Stay Largest While Online Retail Changes Pack Design

Supermarkets and hypermarkets accounted for 38.56% share of the egg packaging market size in 2025, while online retail is forecast to grow at an 8.12% CAGR through 2031. Supermarkets and hypermarkets kept the lead because they offer standardized shelf dimensions, stable replenishment routines, and well-established supplier relationships for egg cartons and trays. Convenience stores remained a smaller channel, but they supported lower pack counts and impulse-oriented formats that align with urban purchasing behavior. Specialty stores carried lower volumes, yet they often required the highest per-unit packaging value because organic, cage-free, and pasture-raised eggs rely on stronger branding and clearer product differentiation. The egg packaging market is therefore seeing a split between volume-efficient shelf packs and premium packs designed for claims, visibility, and product storytelling.

Online retail is changing specifications more directly because eggs move through more touchpoints before delivery than they do in a conventional pallet-to-shelf model. U.S. e-grocery growth in late 2025 showed that digital grocery demand is no longer marginal, and Amazon's fresh grocery activity further confirmed that fragile food categories are part of same-day fulfillment strategies. That raises demand for reinforced lids, better corner strength, taller sidewalls, and packs that remain stable in robotic picking and vertical tote stacking. Suppliers that cannot support both in-store and digital formats from a unified offering face a higher risk of delisting as large retailers simplify their packaging base. The egg packaging industry is therefore moving toward channel-specific engineering, even when the egg itself remains a standard commodity.

Geography Analysis

Asia-Pacific held 42.64% of the egg packaging market share in 2025 and is projected to expand at a 7.38% CAGR through 2031. China remained the core anchor because FAO data showed it accounted for nearly 49% of global egg production, providing the region with a very large domestic demand base for trays and cartons.[3]Food and Agriculture Organization of the United Nations, “FAOSTAT,” FAO, fao.org India ranked second globally with an 8% share of output, and its ongoing move from loose egg sales toward organized packaged retail is adding structural packaging demand in urban and peri-urban channels. Japan has a different demand profile, as policy pressure on plastic use and retailer decarbonization programs are driving greater adoption of molded packs and paper-based formats. Across the wider Asia-Pacific egg packaging market, retail formalization and food-safety awareness are gradually converting open-tray sales into labeled consumer packs.

North America and Europe did not match Asia-Pacific in volume, but they remained among the highest-value parts of the egg packaging market because traceability, cage-free conversion, and premium merchandising standards were already well established. Germany's egg production rose 4.2% in 2024 to 13.7 billion eggs, with stronger growth in free-range and organic output, which supported demand for premium molded-fiber formats. In Europe, the regulatory path continued to support tighter production and labeling standards, while in the United States the FDA traceability framework kept pressure on packaging suppliers to support lot coding and tracking capability. Several U.S. state cage-free laws that took effect in 2025 also supported stronger demand for higher-value cartons tied to animal welfare claims and differentiated retail positioning.

South America, the Middle East, and Africa represent the next structural growth frontier for the egg packaging market, even though packaging penetration remains lower and more uneven than in mature markets. Brazil and Argentina are benefiting from supermarket expansion, cold-chain improvement, and urban consumption growth, which together support movement from bulk presentation toward pre-packed formats. In the Middle East, domestic poultry self-sufficiency programs and export-led trade flows are strengthening the need for standardized protective packaging, and Turkey's role in emergency egg exports during 2025 showed how trade disruptions can quickly expand demand for transport-ready pack formats. In Africa, commercial poultry operations are expanding, but infrastructure gaps and limited recycled fiber capacity still favor lower-cost plastic formats in the near term while leaving room for molded-fiber growth later in the forecast period.

Competitive Landscape

The egg packaging market is moderately consolidated at the top and fragmented across the wider supplier base, with Hartmann Packaging, Huhtamaki Oyj, and Cascades Inc. holding strong positions in molded fiber while many regional players compete on proximity, price, and narrower product lines. Huhtamaki made one of the clearest strategic moves in April 2025 when it acquired Zellwin Farms Company for USD 18 million, adding molded fiber capacity and strengthening its position in the Southeastern United States. Cascades also used product development to strengthen its position in the egg packaging market when it launched Fresh GUARD EnVision in June 2024, targeting customers who wanted both sustainability and shelf impact in a single format.[4]Cascades Inc., “Cascades Brings Innovation to the Egg Market with a New Packaging Solution,” PR Newswire, prnewswire.com Those moves show that scale players are not competing only on volume, because they are also building deeper positions in regional capacity and differentiated pack design. The broader result is a market where the top tier shapes innovation direction, but many purchasing decisions still remain local and cost-sensitive.

Below the global leaders, competition is more fragmented and often tied to regional farm clusters, shorter transport distances, and converters that can respond quickly to customer format changes. Some smaller suppliers are trying to stand out through FSC-certified board, renewable power use, hybrid paper-fiber structures, or premium graphics aimed at specialty egg brands. That approach is relevant because premium cage-free and organic programs need stronger communication on pack, while mainstream retail accounts still focus on protection, cost, and steady replenishment. The egg packaging market therefore supports both scale-led competition at the top and focused differentiation at the regional level.

The next stage of rivalry is likely to center on automation compatibility, e-commerce durability, and traceability integration rather than on material choice alone. High-speed grading systems already require consistent tolerances and stable denesting, and that screens out suppliers whose packs disrupt line throughput at scale. Traceability rules in North America and Europe also favor suppliers that can support clear coding, lot marking, and machine-readable data without extra processing steps. As those requirements tighten, the egg packaging market should keep rewarding companies that combine material flexibility, regulatory readiness, and plant-level production reliability across multiple customer channels.

Egg Packaging Industry Leaders

Hartmann Packaging A/S

Huhtamaki Oyj

Tekni-Plex, Inc.

Cascades Inc.

Ovotherm International Handels GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Graphic Packaging International implemented a precision-cut 100% recycled carton board sleeve variant designed for bulk egg multi-packs. The design utilizes high-caliper, unbleached kraft fibers to provide puncture resistance without increasing the total weight of the primary packaging assembly.

- April 2026: Omnisource Packaging unveiled a hybrid pulp-and-cardboard retail egg pack engineered for automated side-loading machinery. The unit pairs a 100% pre-consumer recycled fiber base with an open-window structural top sleeve to maximize visibility while maintaining required top-load stacking strength.

- March 2026: Huhtamaki Oyj expanded its distribution of automated-fit packaging solutions by introducing a retail-ready molded fiber carton utilizing a physical mechanical interlocking rim. The container dispenses with synthetic adhesives, relying entirely on die-cut fiber tabs to maintain closure integrity under high stacking pressure.

- February 2026: Hartmann AG commercialized its modular, high-ventilation molded fiber cartons configured specifically for industrial top-loading logistics lines. The updated cell architecture increases lateral airflow around the eggshells, mitigating humidity buildup and cooling delays during rapid cold-chain fulfillment.

Global Egg Packaging Market Report Scope

The scope of the report covers the analysis of the egg packaging market, including packaging materials and solutions designed for the storage, transportation, and protection of eggs. The report evaluates market trends, growth drivers, challenges, and opportunities, offering insights into the competitive landscape and key players.

The Egg Packaging Market Report is Segmented by Product Type (Cartons, Trays, Containers, and More), Material Type (Plastic, Paper, Molded Fiber, and More), Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online Retail, and Specialty Stores), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cartons |

| Trays |

| Containers |

| Other Product Types |

| Plastic |

| Paper |

| Molded Fiber |

| Other Material Types |

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Online Retail |

| Specialty Stores |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Cartons | ||

| Trays | |||

| Containers | |||

| Other Product Types | |||

| By Material Type | Plastic | ||

| Paper | |||

| Molded Fiber | |||

| Other Material Types | |||

| By Distribution Channel | Supermarkets and Hypermarkets | ||

| Convenience Stores | |||

| Online Retail | |||

| Specialty Stores | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the egg packaging market in 2026, and what is the 2031 outlook?

The egg packaging market stands at USD 8.58 billion in 2026 and is forecast to reach USD 11.62 billion by 2031, growing at a 6.26% CAGR over 2026-2031.

Which region leads to global demand for egg packs?

Asia-Pacific led with a 42.64% share in 2025 and is also the fastest-growing region, supported by China's production scale and India's shift toward packaged retail.

Which product format is expanding the fastest?

Trays are projected to grow at a 7.63% CAGR through 2031, helped by cage-free logistics, bulk handling needs, and food-service demand.

Why is molded fiber gaining share over plastic?

Molded fiber held 43.64% share in 2025 and is growing at 7.57% because it aligns with retailer sustainability goals, recyclable-pack demand, and tighter plastic-related rules.

How is online grocery changing egg pack design?

Online retail is projected to grow at an 8.12% CAGR, which is pushing suppliers toward stronger lids, better stacking strength, and packs suited for multi-step fulfillment.

What are the main risks affecting supplier margins?

Raw material volatility, food-contact compliance costs, and avian influenza-related egg supply swings remain the main margin pressures for converters and carton suppliers.

Page last updated on: