Land Professional Mobile Radio Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

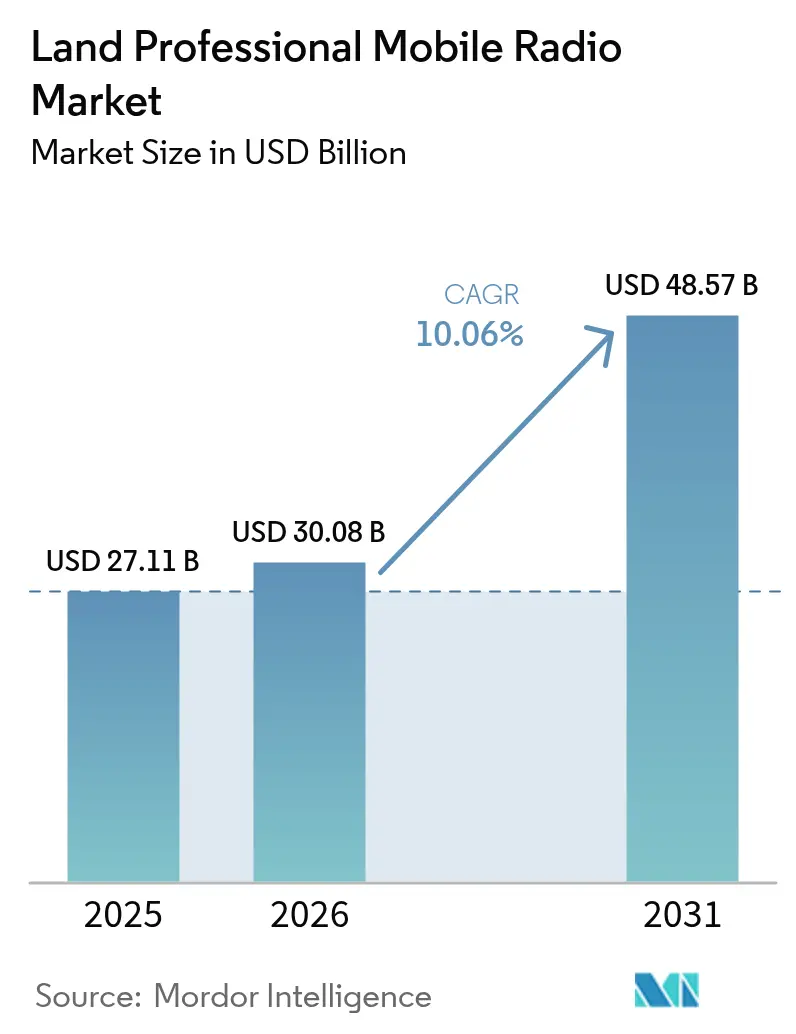

| Market Size (2026) | USD 30.08 Billion |

| Market Size (2031) | USD 48.57 Billion |

| Growth Rate (2026 - 2031) | 10.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Land Professional Mobile Radio Market Analysis by Mordor Intelligence

The land professional mobile radio market size is expected to increase from USD 27.11 billion in 2025 to USD 30.08 billion in 2026 and reach USD 48.57 billion by 2031, growing at a CAGR of 10.06% over 2026-2031. Public-safety agencies are replacing analog networks with interoperable digital protocols, utilities are embedding radios in smart-grid control systems, and rail operators are preparing for GSM-R sunset by adopting hybrid TETRA-5G architectures. Digital platforms already account for more than two-thirds of 2025 revenue, yet analog demand persists in remote mining and construction sites where cellular coverage is poor. Handheld and portable radios dominate shipments, helped by stricter first-responder safety mandates, while repeaters and gateways are scaling quickly as agencies fill dead zones inside tunnels and wildfire corridors. Regulatory refarming in North America and Europe is freeing 700/800 MHz spectrum for public protection and disaster relief, spurring upgrades that combine narrowband voice with broadband backhaul. Moderate vendor concentration is prompting incumbents to bundle hardware with cloud software, while smaller specialists win niche contracts by offering software-defined radios that bridge legacy and broadband systems.

Key Report Takeaways

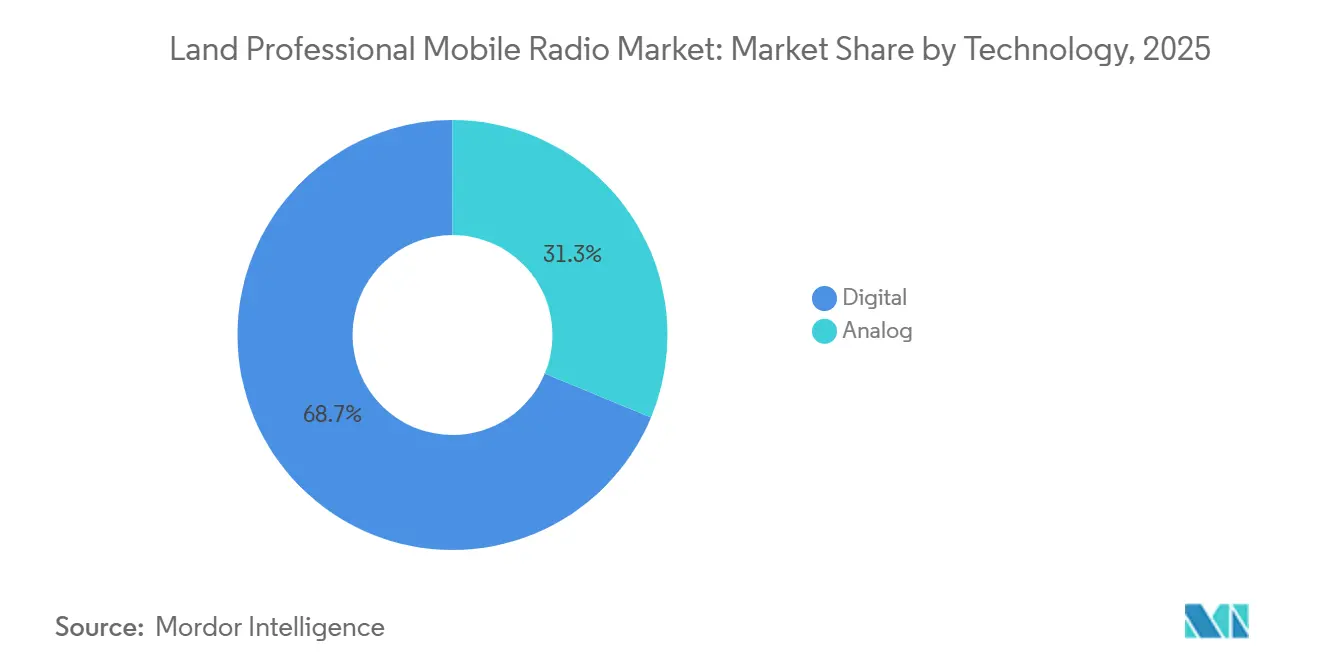

- By technology, digital systems captured 68.73% of the land professional mobile radio market share in 2025, whereas analog is forecast to grow at a 10.12% CAGR through 2031.

- By form factor, handheld and portable units held 53.28% of 2025 revenue, while repeaters and gateways are projected to expand at a 10.25% CAGR between 2026-2031.

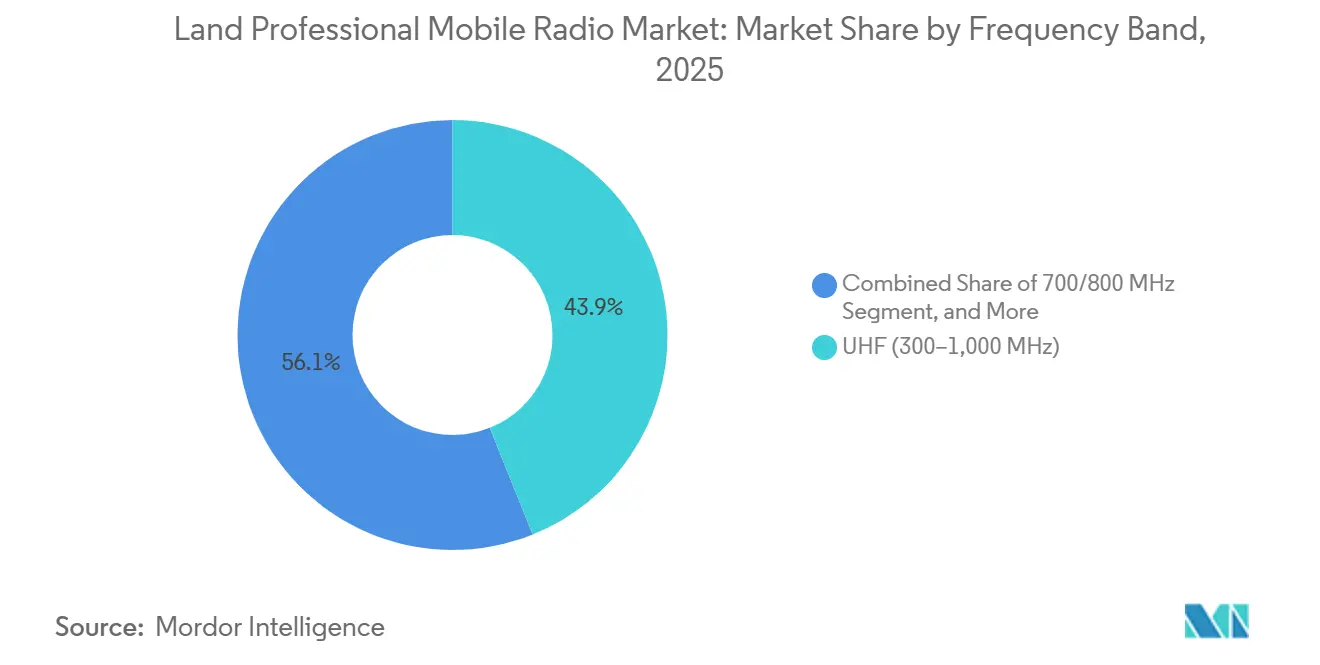

- By frequency band, UHF accounted for 43.91% of the land professional mobile radio market in 2025, and the 700/800 MHz segment is advancing at a 10.21% CAGR through 2031.

- By end-user sector, public safety accounted for 45.74% of revenue in 2025; utilities and energy are the fastest-growing segment, with a 10.32% CAGR forecast to 2031.

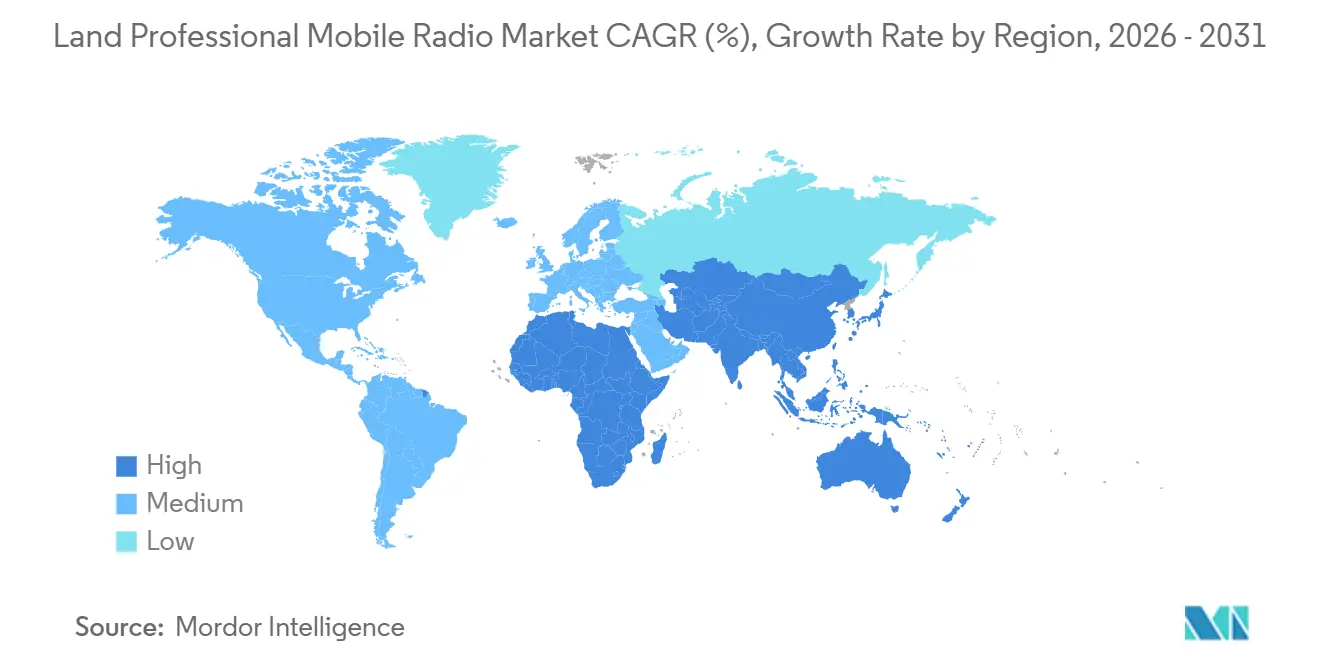

- By geography, North America retained a 33.57% share in 2025, whereas Asia-Pacific is projected to post the highest regional CAGR of 10.42% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Land Professional Mobile Radio Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G-Enabled PMR Backhaul Demand Surge | +2.1% | Global, with early traction in North America, Europe, and Asia-Pacific urban corridors | Medium term (2-4 years) |

| Transition From Analog To Digital Protocols | +2.5% | Global, led by North America and Europe; accelerating in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Public-Safety Network Modernisation Mandates | +1.9% | North America, Europe, Australia, Japan, South Korea | Short term (≤ 2 years) |

| AI-Driven Dispatch And Predictive Maintenance | +1.3% | North America and Europe; pilot deployments in Asia-Pacific | Medium term (2-4 years) |

| Integration With Private LTE and MC-X Platforms | +1.6% | Global, with concentration in North America, Europe, and GCC | Medium term (2-4 years) |

| Inter-Agency Interoperability Needs Amid Climate-Driven Disasters | +1.2% | Global, acute in wildfire-prone regions (North America, Australia), flood zones (Asia-Pacific), and hurricane corridors (Caribbean, US Gulf Coast) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G-Enabled PMR Backhaul Demand Surge

Private LTE and 5G networks surpassed 6,500 live enterprise deployments in 2025, and mission-critical users are increasingly routing land professional mobile radio market traffic over these new pipes to gain high-bandwidth video and IoT data services without sacrificing dedicated spectrum for voice.[1]GSMA Intelligence, “Private Mobile Networks Enterprise Adoption,” gsma.com The 3GPP Release 18 specification, finalized in 2024, enables seamless handover between TETRA trunks and MCPTT over LTE, reducing infrastructure duplication costs. Utilities are first movers, deploying 5G small cells at substations to stream real-time imaging from inspection drones, while rail yards add millimeter-wave nodes to support autonomous shunting. These capabilities attract new budgets and reinforce the growth trajectory of the land professional mobile radio market.

Transition from Analog to Digital Protocols

Digital PMR variants such as TETRA, Project 25, DMR, and NXDN already hold a 68.73% share, yet analog remains prevalent in cost-sensitive sectors. The U.S. Department of Homeland Security certified more than 1,200 interoperable P25 products by late 2025, which accelerated county-level upgrade programs.[2]Department of Homeland Security, “P25 Compliance Assessment Program Listings,” dhs.gov Europe’s Electronic Communications Code obliges member states to clear 700 MHz spectrum for harmonized public-protection services by 2026, compelling migration from MPT-1327 and analog PMR446. Digital options provide twice the spectral efficiency, secure encryption, and GPS features that analog lacks, directly underpinning the double-digit CAGR of the land professional mobile radio market.

Public-Safety Network Modernization Mandates

National programs such as FirstNet in the United States, the United Kingdom’s Emergency Services Network, and South Korea’s PS-LTE compel agencies to retire legacy systems or risk losing federal grants. Japan earmarked 27.5–28 GHz for public safety in 2024 and is layering high-capacity links over existing 800 MHz voice channels. These policies shorten replacement cycles, drive multicurrency procurement, and sustain demand across the land professional mobile radio industry.

Integration with Private LTE and MC-X Platforms

Standards published by the TETRA and Critical Communications Association in 2024 define interfaces that enable a conventional PMR handset to communicate with a broadband user via an interworking gateway. Public-safety agencies see operational savings from shared infrastructure, while industrial sites leverage LTE for data-heavy tasks and retain narrowband for mission-critical voice. Such hybrid designs improve coverage resilience, boosting equipment sales and service revenues within the land professional mobile radio market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum Scarcity In Sub-1 GHz Bands | -1.4% | Global, acute in densely populated urban markets (North America, Europe, Asia-Pacific) | Short term (≤ 2 years) |

| Capital-Intensive Multi-Technology Overhaul Cycles | -1.8% | Global, pronounced in budget-constrained public-safety agencies in South America, Africa, and parts of Asia-Pacific | Medium term (2-4 years) |

| Rising Cyber-Security Compliance Costs | -0.9% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Regulatory Uncertainty Over PMR-LTE Spectrum Sharing | -1.1% | Global, with heightened impact in markets undergoing spectrum refarming (North America, Europe, GCC) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Multi-Technology Overhaul Cycles

Deploying a nationwide TETRA network typically costs USD 500-800 per subscriber, and adding MCPTT over LTE can double that outlay once core upgrades and dual-mode devices are included. Many municipalities exhausted federal grants on initial LTE coverage and now struggle to fund cybersecurity licenses and spectrum leases. As a result, hybrid fleets of analog, digital, and LTE radios persist, increasing training complexity and delaying fresh orders in the land professional mobile radio market.

Spectrum Scarcity in Sub-1 GHz Bands

World Radiocommunication Conference 2023 did not allocate additional global PMR spectrum below 1 GHz, intensifying competition with commercial 5G providers.[3]International Telecommunication Union, “Outcomes of WRC-23 for Land Mobile Services,” itu.int The U.S. 900 MHz auction in 2024 excluded public safety, forcing agencies to squeeze more users onto congested 700/800 MHz channels or migrate to shared LTE, which raises latency risks. Limited low-bandwidth inventory increases device costs and introduces regulatory uncertainty, tempering near-term spending across the land mobile radio market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Digital Adoption Outpaces but Does Not Eliminate Analog

Digital platforms TETRA, P25, DMR, and NXDN accounted for 68.73% of the land professional mobile radio market share in 2025, reflecting national mandates that push agencies toward encryption, GPS, and over-the-air programming features absent in legacy systems. Analog installations remain entrenched on remote mining and construction sites and are forecast to expand at a 10.12% CAGR during 2026-2031, as operators prefer incremental upgrades that leverage existing repeater networks. The land professional mobile radio market, driven by digital equipment, will expand as European rail operators deploy FRMCS to replace GSM-R, adding 200,000 new terminals by 2030. U.S. agencies gain twice the spectral efficiency when they shift from P25 Phase 1 to Phase 2, reducing channel congestion without new spectrum allocations.

Analog resilience is time-bound. Australia plans to phase out 400 MHz analog licenses by 2027, and similar proposals are under review in parts of the Asia-Pacific, signaling that analog growth will plateau late in the decade. Falling radio prices and broader vendor ecosystems are narrowing the total-cost gap between digital and analog, further tilting spending toward multi-mode handsets that can toggle between TETRA or P25 and LTE. Consequently, the land professional mobile radio market for digital equipment is poised to capture a larger share of refresh budgets, even as a niche analog fleet endures in coverage-challenged regions.

By Form Factor: Portables Dominate While Infrastructure Rises Fastest

Handheld and portable units accounted for 53.28% of 2025 revenue, underscoring their role as the primary communication lifeline for police, firefighters, and utility line crews working in hazardous environments, and are certified to IECEx standards. Repeaters and gateways represent the fastest-growing hardware class, advancing at a 10.25% CAGR between 2026-2031 as agencies extend coverage into subway tunnels, high-rise basements, and wildfire canyons. Software-defined radios, such as Tait’s TP9600, enable field teams to load new waveforms via firmware, reducing inventory complexity and accelerating digital migration.

Infrastructure modernization is equally important. IP-connected repeaters can consolidate traffic from multiple remote sites into a single fiber or microwave backhaul, cutting leased-line costs and enabling real-time network analytics. These capabilities fuel sustained demand for gateway nodes that bridge narrowband voice with broadband data, reinforcing revenue diversity in the land professional mobile radio market. As agencies adopt predictive-maintenance dashboards, downtime linked to radio failures is falling, which frees budget for proactive expansions rather than break-fix cycles.

By Frequency Band: UHF Retains Lead as 700/800 MHz Accelerates

UHF (300–1000 MHz) delivered 43.91% of the land professional mobile radio market share in 2025 because it balances propagation range with antenna size, making it the default choice for nationwide networks. The 700/800 MHz segment will grow at a 10.21% CAGR to 2031, driven by FirstNet in the United States, harmonized 700 MHz PPDR allocations in Europe, and similar refarming in Australia and South Korea. Agencies value 700 MHz signals for superior in-building penetration, reducing the number of cell sites needed to meet coverage targets.

Cross-border interference remains a constraint along the United States–Canada and United States–Mexico corridors, where regulators must align adjacent-channel plans to avoid spillover that degrades call quality. VHF persists in maritime and aviation channels reserved by the International Civil Aviation Organization, insulating that slice from rapid digital migration. Above 900 MHz, niche firefighter body networks and short-range industrial links are seeing limited but growing adoption, though fragmented allocations hinder scale. Overall, spectrum trends amplify the land professional mobile radio market, driving growth in newer bands while preserving UHF as today’s revenue anchor.

By End-User Sector: Public Safety Dominates, Utilities Post Fastest Growth

Public-safety organizations accounted for 45.74% of 2025 revenue, driven by FirstNet adoption in the United States and parallel mandates in Europe and Asia-Pacific that require interoperability and end-to-end encryption. Yet utilities and energy companies are projected to log the strongest expansion, rising at a 10.32% CAGR through 2031 as grid operators integrate radios with IEC 61850 substation automation for deterministic control of distributed energy resources. Transportation continues to invest in rail signaling and airport ground coordination, while manufacturing plants adopt intrinsically safe handsets for petrochemical and grain-processing lines.

Construction and mining crews favor rugged analog devices that withstand dust, vibration, and extreme temperatures, keeping a residual share of the broader land professional mobile radio market. Hospitality, retail, and event venues often buy license-free radios to avoid regulatory fees, trading range for lower cost. As climate-driven disasters intensify, cross-sector mutual-aid initiatives push agencies and private operators to procure interoperable gateways, further expanding the addressable land professional mobile radio market size across public- and private-sector boundaries.

Geography Analysis

Asia-Pacific is projected to post the fastest regional CAGR of 10.42% between 2026-2031, as China’s Ministry of Public Security mandates TETRA for provincial police forces and India commits USD 1.2 billion to modernize state networks under its National Public Safety Communication program. Japan showcased seamless voice-and-data interoperability during the 2025 Osaka Kansai Expo, proving that PS-LTE overlays can coexist with 800 MHz PMR and strengthening the region’s upgrade roadmap. Australia and New Zealand extend coverage through satellite-augmented repeaters that link remote fire, ambulance, and police units to national command centers. South Korean factories embed 5 G-backhauled radios to support smart-manufacturing mandates, creating new equipment orders. These combined projects expand the land professional mobile radio market size in Asia-Pacific far more quickly than in any other geography.

North America retained 33.57% of the land professional mobile radio market share in 2025, buoyed by the United States’ FirstNet network, which reached 99% geographic coverage and enrolled more than 3.5 million public-safety subscribers. Canada set aside USD 750 million for a national public-safety broadband platform that will interoperate with provincial P25 systems, addressing cross-border incident response gaps. The United States also reallocated part of the 900 MHz band for critical-infrastructure broadband, giving utilities fresh spectrum for hybrid LTE-PMR deployments. Mexico continues to rely on 2010-era TETRA systems outside major cities, limiting near-term digital refresh volumes. Public- and private-sector projects across the continent, therefore, concentrate new spending in corridors where wide-area coverage already exists.

Europe remains a substantial but maturing market, anchored by Germany’s BOS network, which serves 400,000 users across federal and state agencies. France completed a nationwide ANTARES refresh in 2025, adding Release 2 packet-data functions to strengthen encryption. The United Kingdom’s protracted Emergency Services Network transition has slowed procurement, yet interim extensions on legacy Airwave contracts keep demand for maintenance services steady. In the Middle East and Africa, Gulf Cooperation Council nations finance mega-projects such as Saudi Arabia’s NEOM, which relies on a new USD 200 million TETRA backbone for smart-city security. South America experiences uneven growth, with Brazil upgrading state police fleets to P25 while rural areas lag due to funding and spectrum constraints.

Competitive Landscape

The five largest suppliers, Motorola Solutions, Hytera Communications, L3Harris Technologies, Airbus Defence and Space, and JVCKenwood Corporation, collectively controlled about 42% of 2025 revenue, giving the sector a moderately consolidated structure. This concentration encourages incumbents to bundle radios with cloud software and managed services, locking customers into long-term contracts that stabilize cash flow. Regional specialists such as Tait Communications and Sepura win niche tenders by offering open-architecture platforms that integrate easily with third-party dispatch and analytics tools.

Recurring revenue now shapes competitive strategy. Motorola Solutions generated more than USD 1 billion in annual subscription revenue from its CommandCentral suite, demonstrating that software margins can exceed hardware returns. Hytera emphasizes multi-mode devices that switch among TETRA, DMR, and LTE through firmware, catering to agencies with mixed fleets. L3Harris registered a rise in European public-safety bids after acquiring a regional TETRA service provider in October 2025, immediately adding multi-year maintenance contracts. Patent activity underscores differentiation: Motorola filed 127 PMR-related patents in 2024-2025, compared with Hytera’s 89, many of which cover AI-assisted dispatch and mesh networking.

Strategic moves also target technology gaps and high-growth regions. Airbus Defence and Space partnered with Saudi authorities to roll out a nationwide TETRA network for NEOM, embedding cybersecurity controls that meet ETSI TS 102 361 standards. JVCKenwood and East Japan Railway launched a Future Railway Mobile Communication System pilot on Tokyo’s Yamanote Line to prove TETRA-5 G interworking ahead of broader Asian rail tenders. Iridium entered the arena with the Certus 200 satellite backhaul, which extends PMR coverage to maritime and wilderness zones where terrestrial repeaters are impractical. Together, these initiatives illustrate how vendors leverage acquisitions, regional alliances, and new service layers to capture market share as the market transitions from hardware dependence to integrated critical-communications ecosystems.

Land Professional Mobile Radio Industry Leaders

Motorola Solutions, Inc.

Hytera Communications Corporation Limited

Airbus Defence and Space S.A.S.

L3Harris Technologies, Inc.

Thales S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Motorola Solutions won a USD 120 million contract with the State of California to supply APX NEXT XE radios and expand the statewide P25 network, including cloud dispatch and AI resource allocation.

- November 2025: Hytera Communications secured a EUR 85 million (USD 93.5 million) order to refresh Germany’s Federal Police TETRA infrastructure with Release 2 features.

- October 2025: L3Harris Technologies closed the acquisition of a European TETRA service provider, adding multi-year public-safety contracts in France and Belgium.

- September 2025: Airbus Defence and Space partnered with a Middle Eastern government to build a nationwide TETRA network for Saudi Arabia’s NEOM project valued at about USD 200 million.

Global Land Professional Mobile Radio Market Report Scope

The Land Professional Mobile Radio Market Report is Segmented by Technology (Analog, and Digital), Form Factor (Handheld/Portable, Mobile, Fixed/Base-Station, Repeaters and Gateways), Frequency Band (VHF (30–300 MHz), UHF (300–1,000 MHz), 700/800 MHz, Above 900 MHz), End-User Sector (Public Safety and Security, Transportation and Logistics, Utilities and Energy, Manufacturing and Industrial, Construction and Mining, Hospitality and Retail, Other End-User Sectors), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Analog | |

| Digital | TETRA |

| P25 | |

| DMR | |

| NXDN / dPMR |

| Handheld / Portable |

| Mobile (Vehicular) |

| Fixed / Base-Station |

| Repeaters and Gateways |

| VHF (30–300 MHz) |

| UHF (300–1,000 MHz) |

| 700/800 MHz |

| Above 900 MHz |

| Public Safety and Security |

| Transportation and Logistics |

| Utilities and Energy |

| Manufacturing and Industrial |

| Construction and Mining |

| Hospitality and Retail |

| Other End-User Sectors |

| North America | United States |

| Canada | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Analog | |

| Digital | TETRA | |

| P25 | ||

| DMR | ||

| NXDN / dPMR | ||

| By Form Factor | Handheld / Portable | |

| Mobile (Vehicular) | ||

| Fixed / Base-Station | ||

| Repeaters and Gateways | ||

| By Frequency Band | VHF (30–300 MHz) | |

| UHF (300–1,000 MHz) | ||

| 700/800 MHz | ||

| Above 900 MHz | ||

| By End-User Sector | Public Safety and Security | |

| Transportation and Logistics | ||

| Utilities and Energy | ||

| Manufacturing and Industrial | ||

| Construction and Mining | ||

| Hospitality and Retail | ||

| Other End-User Sectors | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the land professional mobile radio market by 2031?

The market is forecast to reach USD 48.57 billion by 2031.

Which technology segment holds the largest share today?

Digital platforms such as TETRA, P25, and DMR account for 68.73% of 2025 revenue.

Which region will grow the fastest through 2031?

Asia-Pacific is expected to post the highest CAGR at 10.42% over 2026-2031.

Why are utilities investing heavily in professional mobile radio?

Grid operators integrate radios with IEC 61850 automation to achieve deterministic, low-latency control of distributed energy resources.

How are vendors differentiating themselves?

Leading suppliers bundle hardware with cloud-based dispatch and analytics, while challengers offer open-architecture radios and hybrid LTE-PMR gateways.

Page last updated on: