Cellular Interception Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

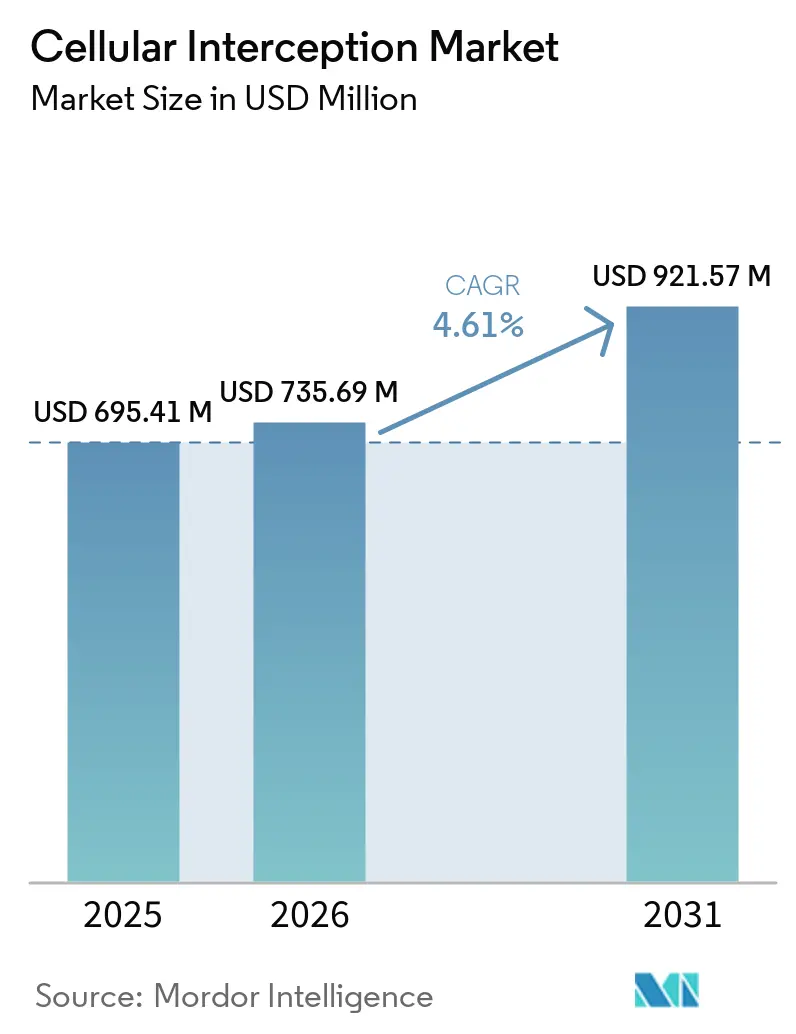

| Market Size (2026) | USD 735.69 Million |

| Market Size (2031) | USD 921.57 Million |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cellular Interception Market Analysis by Mordor Intelligence

The cellular interception market size is expected to increase from USD 695.49 million in 2025 to USD 735.69 million in 2026 and reach USD 921.57 million by 2031, growing at a CAGR of 4.61% over 2026-2031. Defense-modernization calendars, classified procurement cycles, and the methodical rollout of 5G standalone cores set the tempo, making the sector less volatile than consumer telecom segments. Government security budgets, especially for counter-terror and border-protection missions, remain the primary demand anchor, yet the pivot from passively listening to 2G-3G traffic toward penetrating 5G network-slice architectures is raising per-unit costs and elongating integration timelines. Vendors able to satisfy ETSI TS 33.127 v18.11.0 lawful-intercept mandates and 3GPP Release 17 interface standards are best positioned, as agencies increasingly require multi-band receivers, artificial-intelligence analytics, and automated compliance auditing in a single platform. At the same time, the migration to software-defined radios and cloud-hosted analytics is boosting gross margins, encouraging prime contractors to embed interception hooks into broader command, control, communications, computers, intelligence, surveillance, and reconnaissance suites rather than selling one-off probes.

Key Report Takeaways

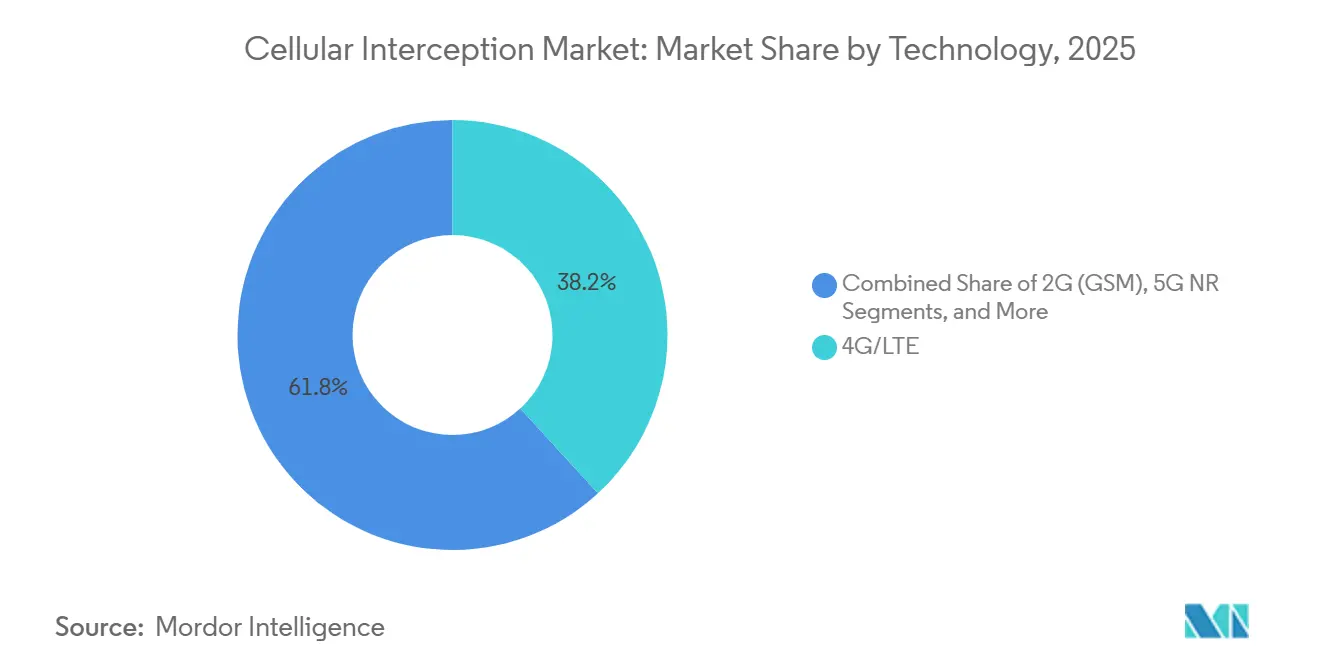

- By technology, 4G/LTE held 38.17% of cellular interception market share in 2025, while 5G NR is projected to record the fastest 5.36% CAGR through 2031.

- By system type, tactical and portable IMSI catchers accounted for 31.53% of revenue in 2025 and are forecast to advance at a 5.21% CAGR over 2026-2031.

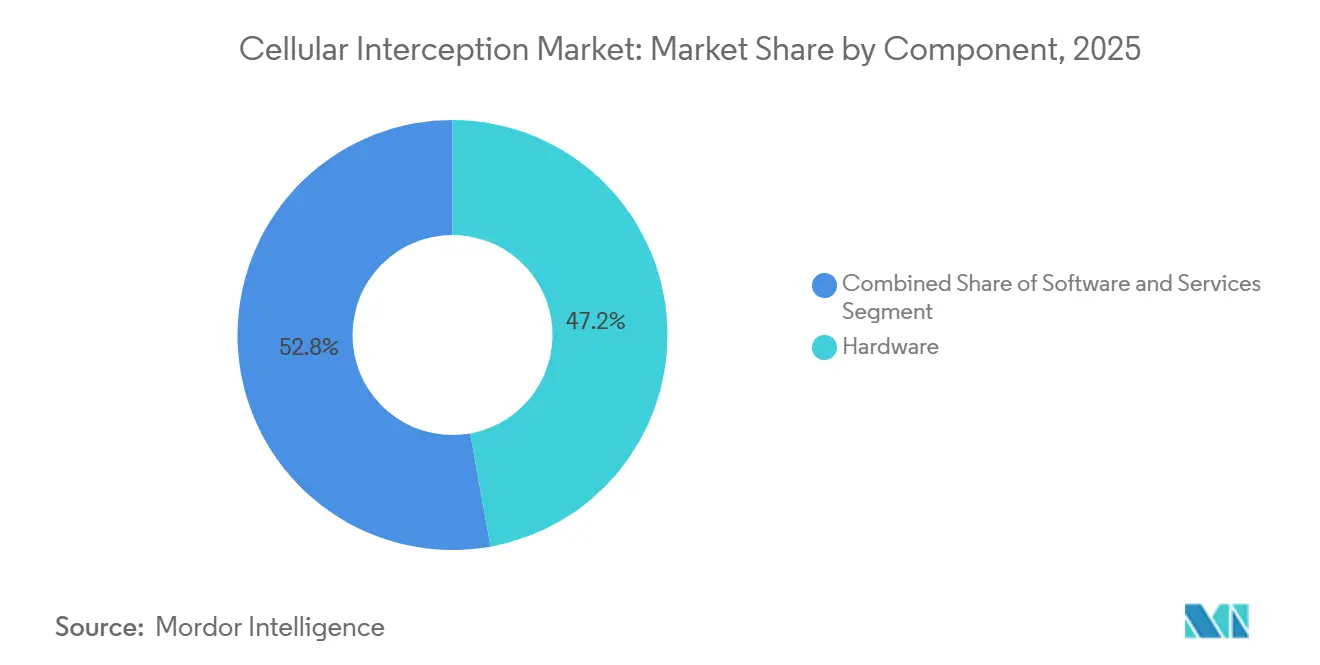

- By component, software platforms recorded the highest 5.42% growth outlook to 2031, even though hardware still contributed 47.18% of the cellular interception market size in 2025.

- By end-user, national security and intelligence services commanded 35.42% of spending in 2025, but military and defense agencies are expected to expand at a 5.16% CAGR.

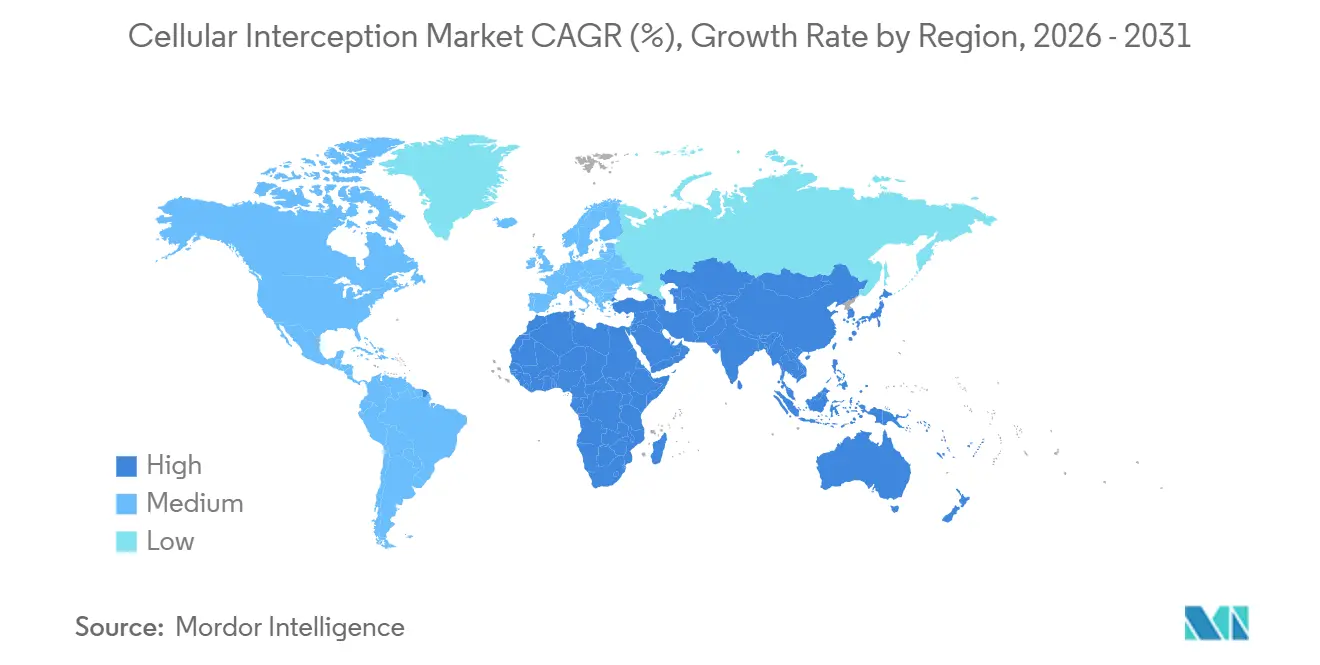

- By geography, North America captured 32.21% of 2025 revenue, whereas Asia-Pacific is set to post the quickest 5.09% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cellular Interception Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Counter-Terror and Public-Safety Budgets | +1.2% | Global, concentrated in North America, Middle East and Europe | Short term (≤ 2 years) |

| Mandatory Lawful-Interception Compliance in 5G Core Upgrades | +1.0% | Global, led by Europe, North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid LTE and 5G Network Densification, Small-Cell Roll-Outs | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Modernisation of Military SIGINT and EW Programmes | +0.8% | North America, Europe and Middle East | Long term (≥ 4 years) |

| Rise of UAV-Borne Interception Payloads | +0.4% | North America, Middle East, select Asia-Pacific nations | Medium term (2-4 years) |

| Exploitation of Femtocell Vulnerabilities for Urban Surveillance | +0.3% | Urban centers worldwide, early adoption in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Counter-Terror and Public-Safety Budgets

National security appropriations remain the single biggest catalyst for the cellular interception market. The United States Department of Homeland Security earmarked USD 43.8 billion in FY 2026 for covert surveillance technologies, Canada set aside CAD 81.8 billion (USD 62.1 billion) over five years for defense modernization, and Saudi Arabia approved a USD 101 million foreign military sales package for advanced monitoring equipment. While central government funding is stable, several U.S. states tightened judicial oversight rules after media investigations into IMSI-catcher misuse, slowing local agency purchases. The bifurcation between well-funded federal programs and constrained municipal budgets is reshaping vendor opportunity maps.

Mandatory Lawful-Interception Compliance in 5G Core Upgrades

Operators migrating to standalone 5G must expose interception interfaces across user-plane, session-management, and policy-control functions in accordance with ETSI TS 33.127 v18.11.0 and 3GPP Release 17. As of late 2025, 181 carriers in 73 nations had invested in standalone cores, and 85 had gone live. Europe’s High-Level Group urged members to harmonize data-retention rules and enable real-time decryption, while India required vendors to hand over intercepted data within 72 hours of a warrant being issued. Compliance carries seven-figure license fees for mediation gateways, but non-compliance risks exclusion from national tenders, cementing this driver’s strength

Rapid LTE and 5G Network Densification, Small-Cell Roll-Outs

The push to relieve urban congestion via outdoor small cells concentrates traffic at fewer aggregation points, simplifying lawful taps. The United States counted 198,100 outdoor small cells in mid-2025, and the Small Cell Forum projects cumulative shipments of 61 million by 2030. China operates 4.6 million 5G sites, 79% of which are in standalone mode, while India has blanket district-level coverage with at least 469,000 base stations. Dense architectures lower deployment costs for interception appliances tapping the core, but they also expose unprotected femtocells that law-enforcement units increasingly exploit for covert probes

Modernisation of Military SIGINT and EW Programmes

Defense ministries are consolidating cellular, satellite, and tactical datalink interception into software-defined, multi-band platforms. The U.S. Army’s FY 2025 budget allocates USD 95.4 million to Tactical Line-of-Sight Beyond-Line-of-Sight Communications and USD 99.9 million to Forward Tactical Exploitation, both aligned with Modular Open Systems Approach doctrines.[1]U.S. Government Publishing Office, “Fiscal Year 2026 Budget of the United States Government,” govinfo.gov L3Harris won a USD 214 million award from Germany in 2025 for Falcon IV radios that embed interception hooks, exemplifying how primes bundle signals-intelligence capabilities into broader communications deals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Lifecycle Costs of Multi-Band Systems | -0.7% | Global, acute in Africa and South America | Short term (≤ 2 years) |

| Strengthening Data-Privacy Legislation and Judicial Oversight | -0.6% | Europe, North America, Asia-Pacific (India, Japan, South Korea) | Medium term (2-4 years) |

| End-to-End Smartphone Encryption and Frequent Protocol Updates | -0.4% | Global, most pronounced in North America and Europe | Long term (≥ 4 years) |

| Activist and Media Scrutiny Triggering Procurement Push-Back | -0.3% | North America, Europe, select Asia-Pacific democracies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Lifecycle Costs of Multi-Band Systems

Turnkey platforms that monitor 2G through 5G, satellite links, and emerging low-earth-orbit constellations cost more than USD 5 million per site, while annual maintenance contracts add 15-20%. Smaller agencies in South America and sub-Saharan Africa, therefore, defer procurements or rely on outdated 2G probes that miss most smartphone traffic. Vendors offer modular rollouts starting with LTE and adding 5G later but fragmented upgrades complicate data fusion and drive total cost of ownership higher.

Strengthening Data-Privacy Legislation and Judicial Oversight

The European Union Data Act and evolving GDPR case law enforce purpose-limitation tests that lengthen tender cycles from nine to 18 months. India’s Digital Personal Data Protection Act requires the review of every interception order within 7 days and the purging of data after 180 days, unless extended, adding new administrative steps. China obliges commercial interception vendors to register with the Cyberspace Administration and undergo annual audits, discouraging some Western suppliers from entering that market. Agencies now demand platforms with audit trails, role-based access, and automated redaction, adding both features and costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Standalone 5G Cores Redefine Interception Architecture

The 5G NR category will grow at 5.36% between 2026-2031, the quickest pace among technology segments, as carriers accelerate shifts to standalone cores compliant with ETSI TS 33.127. This re-architecture exposes richer metadata such as slice identifiers and edge-compute routes, elevating demand for probes that decode 3GPP Release 17 signaling. China’s 4.6 million 5G sites underscore the scale: operators require appliances that can process massive-MIMO streams without packet loss. The cellular interception market for 5G equipment is therefore expanding even faster than overall spending, intensifying competition among compliant vendors.

4G/LTE still dominated revenue with 38.17% cellular interception market share in 2025 because most mobile data continues to traverse LTE networks, especially in rural zones. Yet operators freeing 700 MHz and 2100 MHz bands for 5G are steadily dismantling legacy gear, shrinking the addressable LTE interception pool. Satellite and non-terrestrial links are niche today, but Cobham’s USD 52 million U.S. Navy award for SATCOM probes signals the convergence of orbital and terrestrial interception workflows.

By System Type: Tactical Portability Commands Premium Pricing

Tactical IMSI catchers, comprising 31.53% of 2025 revenue, benefit from growing urban-policing and counter-narcotics operations. Agencies prize systems that fit inside unmarked vans or backpacks, spoof 2G through 5G, and evade electronic-countermeasure detection. TechOps Specialty Vehicles’ USD 825,000 award in May 2025 highlights the premium for covert form factors. As UAV-mounted payloads proliferate, portability now extends vertically; drone-borne probes combine the fixed-system range of a fixed system with the mobile flexibility of a mobile system, particularly along remote borders.

Strategic fixed systems connect directly to carrier cores via ETSI-compliant handovers and are well-suited for agencies that need long-term, bulk collection. Although less visible, their hardware refresh cycles align with operators’ 5G core upgrades, locking in multi-year revenue streams. Passive receivers still attract military customers tasked with electronic support measures in contested theaters. The cellular interception market, therefore, bifurcates: high-volume tactical deals with quicker replacements, and lower-volume strategic contracts with robust annuity services.

By Component: Software Margins Drive Vendor Strategies

Software platforms post the strongest CAGR of 5.42% because agencies now subscribe to analytics, threat intelligence feeds, and firmware updates rather than buying static licenses. Intersec’s AI-powered metadata correlation and TeleFortress AI Defender’s anomaly scoring exemplify this pivot. Vendors enjoy margins above 70%, compared with 30-40% for hardware, incentivizing roadmaps that emphasize cloud-native microservices and continuous deployment pipelines.

Hardware still accounted for 47.18% of 2025 revenue, as multi-band receivers, field-programmable gate arrays, and high-speed digital signal processors remain indispensable for capturing raw IQ samples. Future 5G upgrades with beamforming will require even wider instantaneous bandwidths, driving per-unit costs upward.[2]China Ministry of Industry and Information Technology, “5G Network Development Statistics,” miit.gov.cn Service revenue training, integration, and managed operations stay sticky: the U.S. Army’s tactical communications programs allot roughly one-quarter of contract value to post-delivery support.

By End-User: Military Budgets Outpace Intelligence Services

Although national security and intelligence services accounted for 35.42% of demand in 2025, military and defense agencies are set to deliver a faster 5.16% CAGR, as the multi-domain doctrine demands real-time situational awareness at the battalion level. The USD 33.6 billion FY 2026 Military Intelligence Program budget funds edge-processing nodes that fuse intercepted cellular, satellite, and cyber telemetry onsite, reducing latency and backhaul costs. BAE Systems and Elbit Systems secured contracts of USD 380 million and USD 95 million, respectively, to embed lawful-intercept hooks in tactical radios, underscoring cross-domain alignment.

Federal and state law enforcement agencies still drive high-volume procurement of IMSI catchers for narcotics, human trafficking, and fugitive tracking missions. Yet activist litigation and transparency laws in North America and Europe impose longer review cycles, pushing vendors to include automated privacy safeguards. Private security contractors, particularly in the Gulf and parts of Africa, purchase turnkey systems that governments operate indirectly, creating incremental demand but also inviting scrutiny under export controls.

Geography Analysis

North America led the cellular interception market, accounting for 32.21% of revenue in 2025, underpinned by the United States’ USD 43.8 billion Homeland Security and USD 113.3 billion Defense allocations. Canada’s CAD 81.8 billion (USD 62.1 billion) five-year defense envelope earmarks Arctic surveillance systems where cellular interception augments satellite and high-frequency monitoring. Although mature legal frameworks simplify federal procurements, state-level activist lawsuits have curtailed certain IMSI-catcher deployments, forcing agencies to demonstrate proportionality and data minimization in warrant requests. Mexico’s intensifying counter-cartel operations sustain orders for portable probes, but fiscal austerity limits nationwide rollouts.

Asia-Pacific will generate the fastest 5.09% CAGR as network density concentrates traffic at fewer 5G aggregation nodes. China has 4.6 million 5G sites, India covers 99.6% of districts with at least 469,000 base stations, and Japan plus South Korea invest in quantum-resistant encryption that obliges vendors to advance decryption toolkits. Australia, aligned with Five Eyes security partners, specifies U.S. and U.K. interoperability, steering contracts toward primes holding multiple clearances. The Asian Development Bank’s USD 254 billion infrastructure initiative guarantees a multi-year pipeline for lawful-intercept appliances adapted to standalone cores.[3]Asian Development Bank, “Asia-Pacific Telecommunications Investment Program,” adb.org

Europe balances stringent privacy statutes with security imperatives. Germany, the United Kingdom, and France collectively exceed 50% of regional demand and co-fund the POLIIICE quantum-decryption project. The European Data Act and GDPR push agencies to buy platforms featuring role-based controls and immutable audit logs, adding 10-15% to capital costs but lowering litigation risk. The Middle East, dominated by Saudi Arabia and the United Arab Emirates, funnels oil windfalls into persistent surveillance grids; Saudi Arabia’s USD 101 million FMS deal and a February 2026 memorandum between L3Harris and the Saudi Ministry of Defense portend steady purchases. Africa and South America lag on budget, yet South Africa, Brazil, and Argentina selectively deploy tactical IMSI catchers for urban policing.

Competitive Landscape

The cellular interception market remains moderately concentrated. Defense primes L3Harris Technologies, Rohde & Schwarz, Thales, BAE Systems, Leonardo, and Elbit Systems retain incumbency advantages through export licenses, classified program experience, and proprietary waveform libraries. They dominate strategic fixed systems connecting directly to carrier cores. Tactical segments, however, are more fragmented: Septier Communication, Netline Communications, Stratign, and PKI Electronic Intelligence win based on covert form factor, low power consumption, and resilience against jamming.

Industry strategy centers on modular open-systems architectures that limit vendor lock-in. The United States Department of Defense’s Acquisition Transformation Strategy prioritizes commercial off-the-shelf solutions and government data rights, compelling primes to expose application programming interfaces and adopt open source frameworks.[4]Asian Development Bank, “Asia-Pacific Telecommunications Investment Program,” adb.org ETSI TS 33.127 v18.11.0 codifies interoperability across user-plane and control-plane taps, accelerating commoditization at the hardware layer and shifting competitive focus to artificial-intelligence analytics and cloud delivery.

Emerging disruptors leverage software strengths. SS8 Networks packages subscription-based analytics, Ability Inc. targets sanctioned regimes needing plug-and-play monitoring, and Gamma International extends into enterprise fraud detection. First movers in post-quantum decryption, UAV-borne payloads, and low-earth-orbit interception enjoy green-field runway because standards remain fluid. Success increasingly hinges on securing recurring software revenue that offsets hardware commoditization.

Cellular Interception Industry Leaders

L3Harris Technologies, Inc.

Thales S.A.

BAE Systems plc

Leonardo S.p.A.

SS8 Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: L3Harris Technologies signed a memorandum of understanding with Saudi Arabia’s Ministry of Defense covering command, control, communications, computers, intelligence, surveillance, and reconnaissance plus artificial-intelligence applications for security operations.

- January 2026: The U.S. National Security Agency cleared L3Harris to market its ROVER 6Sc tactical video receiver and TNR 2c networked radio internationally.

- January 2026: Thales secured a EUR 350 million (USD 375 million) contract from Belgium’s Ministry of Defence for tactical communications and electronic-warfare systems that include cellular-network monitoring modules.

- December 2025: Thales received a EUR 4.95 billion (USD 5.3 billion) contract from France’s procurement directorate to develop the Rafale F5 fighter with upgraded SIGINT suites.

Global Cellular Interception Market Report Scope

The Cellular Interception Market encompasses technologies and solutions designed to intercept, monitor, and analyze cellular communications. These systems are widely used by law enforcement agencies, intelligence organizations, and government bodies to ensure national security and combat criminal activities. The market's scope includes hardware, software, and services that facilitate the interception of voice, text, and data communications across various cellular networks.

The Cellular Interception Market Report is Segmented by Technology (2G GSM, 3G UMTS/CDMA2000, 4G/LTE, 5G NR, Satellite and Other Waveforms), System Type (Strategic/Fixed, Tactical/Portable IMSI Catchers, Passive, and Active), Component (Hardware, Software, and Services), End-User (Military and Defence, National Security and Intelligence, Federal and State Law-Enforcement, and Private Security Contractors), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). Market Forecasts are Provided in Terms of Value (USD).

| 2G (GSM) |

| 3G (UMTS/CDMA2000) |

| 4G/LTE |

| 5G NR |

| Satellite and Other Waveforms |

| Strategic / Fixed Interception Systems |

| Tactical / Portable IMSI Catchers |

| Passive Interception Systems |

| Active Interception Systems |

| Hardware |

| Software |

| Services |

| Military and Defence Agencies |

| National Security and Intelligence Services |

| Federal and State Law-Enforcement |

| Private Security Contractors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | 2G (GSM) | |

| 3G (UMTS/CDMA2000) | ||

| 4G/LTE | ||

| 5G NR | ||

| Satellite and Other Waveforms | ||

| By System Type | Strategic / Fixed Interception Systems | |

| Tactical / Portable IMSI Catchers | ||

| Passive Interception Systems | ||

| Active Interception Systems | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By End-User | Military and Defence Agencies | |

| National Security and Intelligence Services | ||

| Federal and State Law-Enforcement | ||

| Private Security Contractors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current cellular interception market size and its forecast growth?

The cellular interception market size stands at USD 695.49 million in 2025, is projected at USD 735.69 million in 2026, and is expected to reach USD 921.57 million by 2031 with a 4.61% CAGR.

Which technology segment will grow the fastest through 2031?

5G NR equipment is set to deliver the quickest 5.36% CAGR as operators transition to standalone cores that embed mandatory lawful-intercept hooks.

Why are software platforms attracting higher margins than hardware?

Agencies now subscribe to AI analytics, threat-intelligence updates, and cloud orchestration, pushing software gross margins above 70% while hardware averages 30-40%.

Which region is forecast to post the highest growth rate?

Asia-Pacific is projected to expand at a 5.09% CAGR because of dense 5G rollouts in China, India, Japan, and South Korea.

How are privacy regulations affecting procurement cycles?

The EU Data Act, GDPR interpretations, and India’s data-protection law add audit and warrant-review steps that can extend tenders to 18 months, encouraging agencies to buy platforms with built-in compliance automation.

What is the main restraint for agencies in emerging economies?

High capital and lifecycle costs often exceeding USD 5 million per multi-band installation limit adoption in Africa and South America, where budgets force deferrals or partial upgrades.

Page last updated on: