Mobile Anti-Malware Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

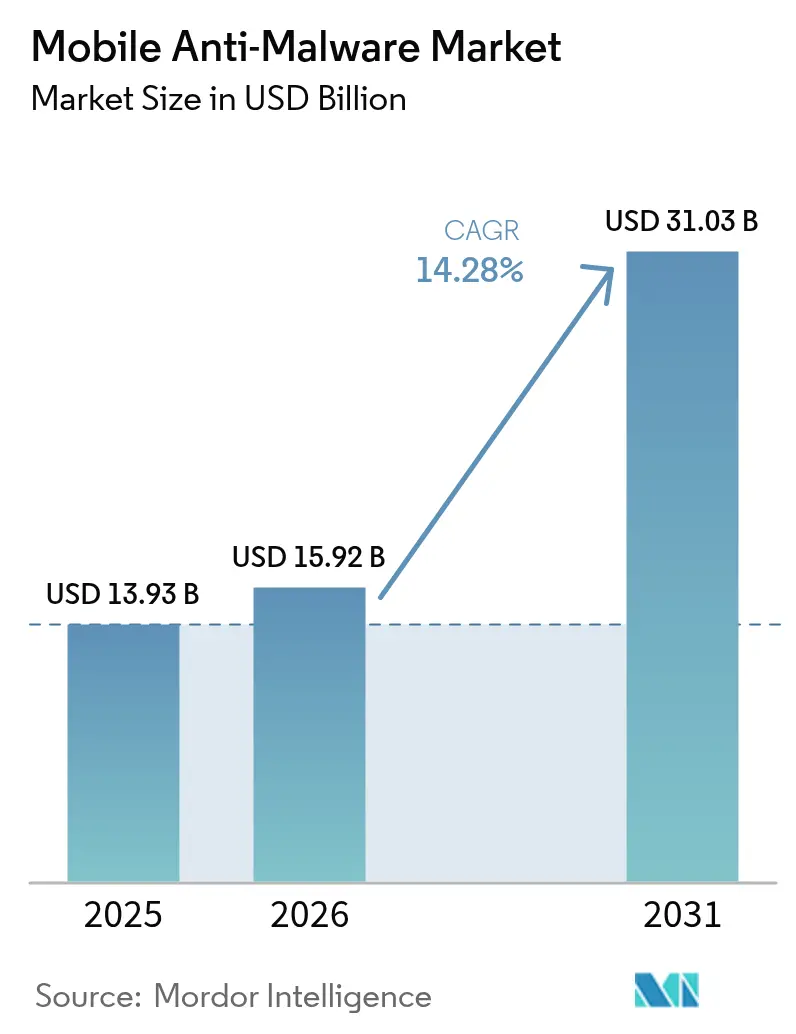

| Market Size (2026) | USD 15.92 Billion |

| Market Size (2031) | USD 31.03 Billion |

| Growth Rate (2026 - 2031) | 14.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Anti-Malware Market Analysis by Mordor Intelligence

The mobile anti-malware market size in 2026 is estimated at USD 15.92 billion, growing from 2025 value of USD 13.93 billion with 2031 projections showing USD 31.03 billion, growing at 14.28% CAGR over 2026-2031. Rapid enterprise digitization, generative-AI-driven malware creation, and zero-trust mandates have turned mobile endpoints into primary attack surfaces for threat actors. Large organizations now treat mobile security as core infrastructure, investing in behavioral analytics that detect malicious intent rather than relying on legacy signature scans. Cloud-delivered threat intelligence, geopolitical vendor restrictions, and new device-embedded AI chips also influence adoption patterns, giving vendors with strong research pipelines and managed-service offerings a clear advantage in the mobile anti-malware market[1]Verizon Business, “2025 Mobile Security Index,” verizon.com.

Key Report Takeaways

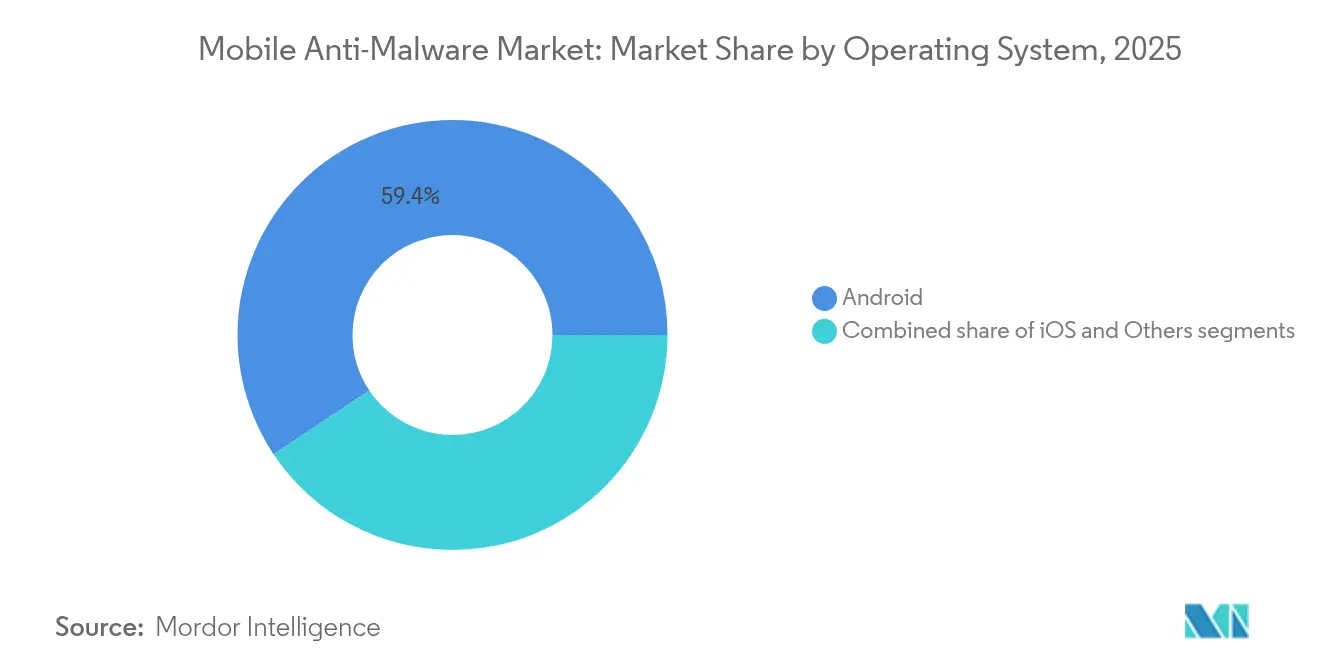

- By operating system, Android led with 59.35% of mobile anti-malware market share in 2025 while iOS is expected to expand at a 15.02% CAGR through 2031.

- By deployment mode, on-premise installations controlled 69.90% of the mobile anti-malware market size in 2025 whereas cloud platforms are set to grow at 15.76% CAGR to 2031.

- By solution type, integrated endpoint-protection suites commanded 55.60% revenue share in 2025 and security-as-a-service is projected to increase at 14.72% CAGR through 2031.

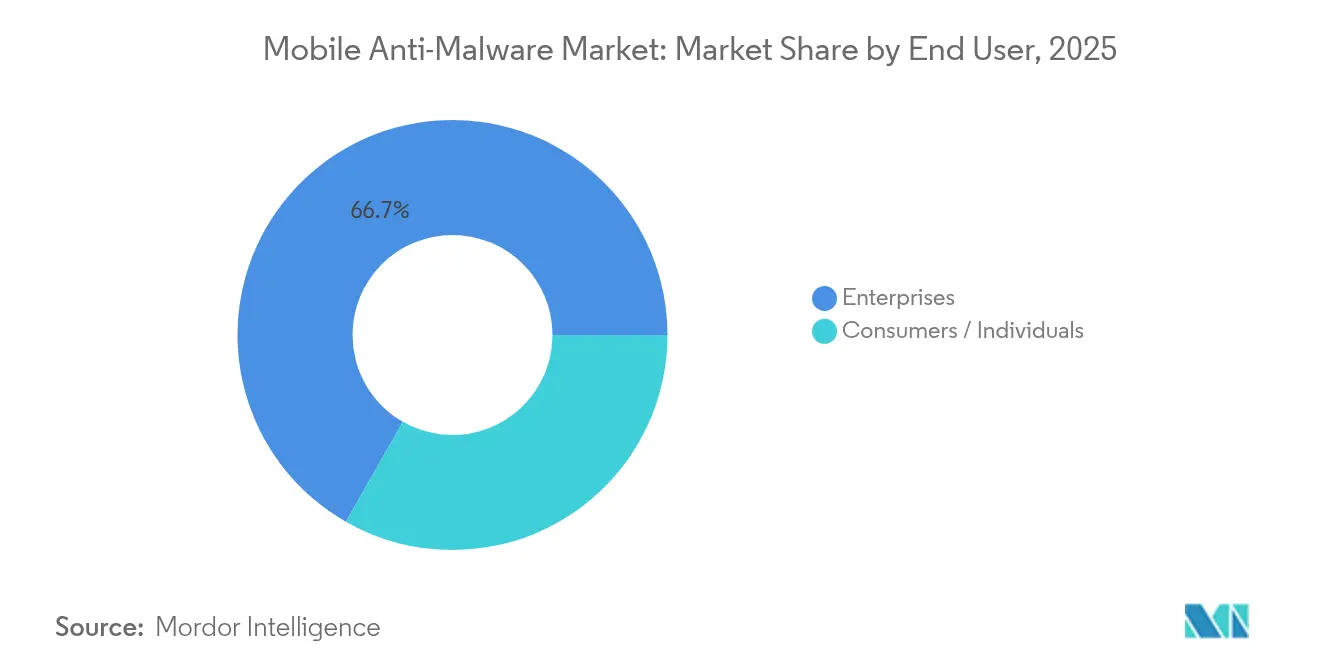

- By end user, enterprise customers held 66.74% of the mobile anti-malware market share in 2025; the same segment is forecast to post the fastest 15.40% CAGR through 2031.

- By industry vertical, BFSI accounted for 43.85% share of the mobile anti-malware market size in 2025 while healthcare is advancing at a 14.32% CAGR through 2031.

- By geography, North America led with 37.75% revenue share in 2025; Asia-Pacific is poised for the fastest 14.46% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile Anti-Malware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding mobile-specific malware variants post-Generative-AI era | +2.8% | Global, concentrated in North America and EU | Short term (≤ 2 years) |

| BYOD 2.0 and hybrid work driving corporate demand | +3.2% | North America and EU core, expanding to APAC | Medium term (2-4 years) |

| Expansion of mobile payment ecosystems in emerging economies | +2.1% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Regulatory mandates for zero-trust on employee-owned devices | +2.4% | North America and EU, early adoption in Australia | Medium term (2-4 years) |

| Rise of app-clone supply-chain attacks in third-party Android stores | +1.7% | Global, higher impact in Android-dominant regions | Short term (≤ 2 years) |

| Proliferation of on-device AI security chips enabling real-time scanning | +1.3% | North America and EU initially, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding Mobile-Specific Malware Variants Post-Generative-AI Era

Generative AI tooling now automates the creation of polymorphic code that mutates on each installation, producing 560,000 unique mobile threats every day in 2025. These campaigns blend code obfuscation with GAN-generated phishing screens that mimic trusted apps on both public and private stores. Signature databases can no longer keep pace, prompting vendors to embed device-side machine learning models that score behavior in milliseconds. Providers that combine cloud-scale correlation with on-device heuristics are gaining enterprise preference because they identify intent before execution. This structural shift places continuous R&D and data-engineering capacity at the center of competitive advantage in the mobile anti-malware market.

BYOD 2.0 and Hybrid Work Driving Corporate Demand

Corporate mobility has evolved from convenience to mission-critical access. In 2024, 84% of large North American firms lifted mobile security budgets to secure employee-owned devices that now handle CRM, ERP, and confidential data workflows[2]Verizon Business, “2025 Mobile Security Index,” verizon.com. BYOD 2.0 policies prescribe runtime monitoring of applications, network calls, and hardware state, closing gaps left by conventional MDM tools. Security teams prefer consolidated suites that apply one policy across phones, laptops, and tablets, which strengthens demand for integrated platforms. As a result, premium subscription tiers that bundle threat hunting and automated response drive revenue resilience in the mobile anti-malware market.

Expansion of Mobile Payment Ecosystems in Emerging Economies

Cashless programs in Asia-Pacific generate huge transaction volumes on smartphones, creating direct monetization opportunities for banking trojans and overlay attacks. Financial regulators in India, Indonesia, and the Philippines now require app integrity verification and device attestation before authorizing high-value transfers, turning robust mobile security into a license-to-operate for payment providers. Vendors that integrate anti-fraud telemetry and real-time risk scoring are capturing new projects from banks and fintechs. The same payment-led digitization trend also fuels small-business adoption, enlarging the total addressable mobile anti-malware market in price-sensitive economies.

Regulatory Mandates for Zero-Trust on Employee-Owned Devices

The U.S. Department of Justice introduced data-transfer safeguards in April 2025 that oblige any contractor handling sensitive records to prove continuous device risk evaluation. Canada’s OSFI Guideline B-13 imposes risk-based identity controls in the financial sector, extending zero-trust concepts to all endpoints. Similar directives are under consultation in Germany and Australia. Because penalties for non-compliance include fines and data-access curbs, spending on advanced mobile threat defense remains insulated from budget cycles. Regulatory alignment also simplifies cross-border device administration, encouraging multinational firms to roll out unified cloud consoles for all regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently low consumer willingness to pay for mobile AV | -1.8% | Global, higher impact in price-sensitive markets | Long term (≥ 4 years) |

| OS-level security hardening shrinking threat surface | -1.2% | Global, iOS leading and Android following | Medium term (2-4 years) |

| Geopolitical distrust of foreign cybersecurity vendors | -0.9% | Primarily US and EU, spill-over to allied nations | Short term (≤ 2 years) |

| Privacy-centric OS features reducing AV visibility | -0.7% | iOS-dominant markets initially, expanding to Android | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistently Low Consumer Willingness to Pay for Mobile AV

Retails users view built-in protections as adequate and often ignore premium tiers that lack visible utility. Conversion rates on freemium apps stay in single digits even during high-profile breach cycles, limiting revenue scalability outside enterprise contracts. Vendors experiment with ad-supported versions, identity-protection bundles, and family plans, yet monetization remains challenging. The gap places a ceiling on consumer revenue, making the enterprise segment pivotal for long-term growth in the mobile anti-malware market.

OS-Level Security Hardening Shrinking Threat Surface

Apple and Google continue to sandbox applications, restrict kernel access, and enforce strict permission regimes. While these improvements raise baseline safety, they also narrow the incremental benefit derived from third-party tools. Providers must therefore showcase value in detecting zero-days, malicious sideloads, or social-engineering exploits rather than general malware. Those that fail to innovate risk commoditization and price erosion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operating System: Enterprise Interest Tilts Toward iOS Security Premium

Android retained 59.35% of mobile anti-malware market share in 2025 due in large part to its vast installed base and lower average device cost. At the same time, iOS units are growing at a 15.02% CAGR, supported by hardware attestation and stricter code-signing controls that simplify compliance in regulated sectors. The mobile anti-malware market size for iOS endpoints is projected to almost double by 2031 as hospital groups, insurers, and financial institutions standardize on Apple devices to lower breach-response expenses. Android remains essential in high-growth economies where value phones dominate, so vendors position AI-powered behavioral engines to offset fragmentation and inconsistent patching.

Enterprises increasingly compare total cost of ownership rather than purchase price alone. Security leaders note that fewer critical incidents on iOS translate into lower forensics spending and downtime. However, Android’s open ecosystem spurs innovation in ruggedized devices and specialized toolsets for logistics and field services, ensuring steady demand for next-generation protection agents. Niche operating systems—mainly hardened Linux builds for the defense sector—hold marginal volume yet command high per-seat pricing due to strict accreditation requirements.

By Deployment Mode: Cloud Momentum Outpaces Legacy On-Premise

On-premise installations accounted for 69.90% of the mobile anti-malware market size in 2025 because many banks and public agencies still store telemetry inside national borders. Nevertheless, cloud subscriptions are accelerating at 15.76% CAGR as boards approve security-as-operating-expenditure budgets that scale with device counts. Large enterprises cite 40% lower administrative overhead once signature updates, model retraining, and threat-intelligence feeds shift to vendor-managed clouds.

Carrier-grade network connectivity and edge PoPs further reduce latency, making cloud consoles viable for always-on validation even under poor Wi-Fi conditions. Vendors assure compliance via regional datacenters and granular data-retention policies. As a result, hybrid rollouts mixing on-prem for crown-jewel assets with cloud for remote staff are now standard. This transition unlocks incremental revenue because customers expand license volumes rather than perform one-off hardware refreshes.

By Solution Type: Integrated Suites Dominate While SECaaS Scales Fast

Integrated endpoint suites captured 55.60% of 2025 revenue because security teams prefer single-pane management for desktops and phones. Suite vendors embed mobile threat defense, EDR, and identity posture checks into one agent, cutting duplication in policy workflows. That consolidation drives stickiness and higher renewal rates within the mobile anti-malware market.

Security-as-a-service is the fastest-rising offer at 14.72% CAGR, propelled by a global shortage of skilled analysts. Organizations hand off alert triage and proactive hunting to provider SOCs while retaining policy control. Pure-play mobile antivirus apps linger mainly in consumer channels, where lightweight footprints satisfy basic needs. Over the forecast horizon, feature parity between suites and SECaaS will blur, resulting in consumption-based pricing models that combine device and data volume metrics.

By End User: Enterprise Revenues Anchor Long-Term Growth

Enterprise accounts produced 66.74% of revenue in 2025 and are forecast to grow at 15.40% CAGR, ensuring they remain the bedrock of the mobile anti-malware market. These buyers accept multiyear contracts with outcome-based SLAs that penalize vendors for missed detections. They also drive feature roadmaps toward automated remediation, identity correlation, and audit-ready reporting demanded by auditors.

Consumers still represent a sizable installed base but deliver limited ARPU. Many rely on free tiers bundled with VPN or password-manager upsells. Small businesses fall between the two extremes, preferring MSP-delivered mobile security that integrates with broader IT support. The gulf in requirements leads to segmented product lines and divergent marketing channels.

By Industry Vertical: BFSI Leadership Coupled With Healthcare Upside

Banks, insurers, and capital-markets firms controlled 43.85% of mobile anti-malware market size in 2025 as regulators insist on device attestation and secure channels for mobile banking. Attackers target one-time passwords, session tokens, and push-notification gimmicks to drain accounts, so financial institutions invest in telemetry enrichment and behavioral AI.

Healthcare is expanding fastest at 14.32% CAGR because clinicians now use phones for electronic health record access, companion diagnostics, and telehealth. HIPAA and comparable global rules assign heavy fines for data leaks, motivating hospital boards to adopt real-time scanning, jailbreak detection, and remote-wipe functions. Government, telecom, and education sectors comprise the balance, each with unique compliance overlays that shape procurement criteria.

Geography Analysis

North America captured 37.75% of 2025 revenue. This lead stems from large enterprise budgets, established mobility programs, and stringent laws such as the U.S. DOJ data-transfer safeguards that require continuous risk scoring on every endpoint. Canadian banks comply with OSFI-B-13, further cementing demand for certified platforms capable of reporting device posture to regulators. Local vendors also benefit from geopolitical screening that sidelines certain foreign suppliers, reallocating spending toward trusted domestic ecosystems.

Asia-Pacific is the fastest-growing region with a projected 14.46% CAGR to 2031. Cashless commerce, super-app ecosystems, and mobile-first workforces expand the total device pool faster than in mature markets. Enterprises in India, Indonesia, and Vietnam adopt threat-defense agents to satisfy payment-security mandates, while Japanese and Australian organizations upgrade to meet zero-trust guidelines. Regional channel partners bundle managed detection services with connectivity plans, accelerating outreach into mid-market enterprises.

Europe ranks third by revenue, yet remains pivotal because GDPR fines link data breaches to material financial penalties. Multinationals demand local data centers and strict contractual clauses on data export, encouraging vendors to open EU-based threat-intelligence nodes. In Southern Europe and the Middle East, uptake increases as 5G rollouts push mobile workflows deeper into oil, logistics, and smart-city projects. Latin America follows similar patterns, though macroeconomic volatility keeps some deployments in pilot phases rather than full production.

Regulatory Landscape

Regulation is increasingly formalizing mobile threat defense as a compliance control for both manufacturers and enterprise operators. In the European Union, the Cyber Resilience Act, Regulation (EU) 2024/2847, sets horizontal cybersecurity requirements for products with digital elements, including obligations around vulnerability handling and secure-by-default configurations. This affects how mobile devices and related remote processing services are secured and monitored.

In the United States, NIST guidance such as SP 800-124r2 (2023) frames Mobile Threat Defense as a core enterprise capability to detect malicious apps, network attacks, and platform vulnerabilities on mobile endpoints. Executive Order 14028 also expands federal focus on software supply chain controls, including treatment of mobile device management as critical software. Together, these anchor frameworks increase the audit value of continuous posture, vulnerability, and threat telemetry from mobile endpoints, reinforcing demand for anti-malware platforms that integrate with enterprise control planes and standardized security baselines.

Value Chain Analysis

The mobile anti-malware value chain begins with platform and trust anchors controlled by OS vendors (Android/AOSP and Apple) and device OEMs, then extends through app distribution (first-party and third-party stores), mobile network operators, and enterprise mobility stacks (MDM/UEM, identity, and access). Security vendors build agents and cloud analytics on top of these layers, using inputs such as threat intelligence, on-device machine learning, behavioral detection, code obfuscation and Runtime Application Self-Protection (RASP) for in-app protection, and API-level integrations that connect mobile risk signals to broader endpoint and identity workflows.

Route-to-market is shaped by enterprise procurement, MSP/MSSP delivery, and carrier bundles, with integrations and policy alignment acting as key commercialization gates. Android fragmentation and firmware over-the-air update dependency create friction, while buyers weigh tradeoffs between deep inspection, privacy controls, performance, and battery life. As buyers consolidate tools, vendors are shifting from point antivirus toward platforms that combine device posture, telemetry correlation, and automated response, supported by partnerships with OEMs, carriers, and managed service providers that affect deployment velocity.

Competitive Landscape

The mobile anti-malware industry displays moderate concentration. Top platforms integrate advanced EDR, cloud analytics, and identity controls, but niche innovators still disrupt with specialized AI models or privacy-preserving architectures. Sophos finalised its USD 859 million Secureworks acquisition in February 2025 to expand managed detection coverage and add XDR telemetry from 500,000 endpoints. CrowdStrike agreed to acquire Adaptive Shield for USD 300 million in November 2024 to weave SaaS posture management into its Falcon platform.

Technology differentiation now revolves around three pillars. First, proprietary data lakes enrich ML algorithms that spot zero-days faster than reliance on public feeds. Second, frictionless deployment via MDM APIs or carrier SIM binding eases large-scale rollouts. Third, ecosystem breadth matters because clients want one console for endpoints, cloud workloads, and identities. Vendors are unable to offer unified telemetry risk marginalisation.

Geopolitics also shapes buying behaviour. The 2024 prohibition on Kaspersky software in the United States redirected government and critical-infrastructure contracts to Western suppliers[3]U.S. Department of Commerce, “Notice of Final Determination on Kaspersky Lab,” commerce.gov. Similar security-of-supply debates influence EU defence procurement. Partnerships between network operators and security firms, such as the 2025 T-Mobile / Palo Alto Networks SASE launch, illustrate convergence between connectivity and protection layers. Emerging vendors focusing on vertical use cases—like medical-device scanning or industrial-control isolation—attract venture capital, signalling continued competitive churn in the mobile anti-malware market.

Mobile Anti-Malware Industry Leaders

AO Kaspersky Lab

Avast Software SRO

BitDefender LLC

Lookout Inc.

Malwarebytes Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Government and regulated-enterprise compliance is creating a clear whitespace for continuous Mobile Threat Defense deployments that can meet prescriptive baselines and support audit-ready posture reporting. DISA STIG baselines for mobile platforms have been moving toward explicit Mobile Threat Defense requirements on managed devices, which increases demand for products that integrate with UEM/MDM controls, enforce policy at runtime, and generate evidence for oversight bodies.

On the threat side, operator tooling and malware commercialization are pushing buyers toward behavioral, on-device detection that stays effective when signatures lag. In 2026, Android platform security additions (for example, Android 17 security and anti-theft features) and Google-led efforts such as staged developer verification rollouts highlight a market shift toward identity- and integrity-based controls around apps. That creates opportunities for anti-malware vendors to complement OS protections with enterprise-grade telemetry, fraud and scam defense, and cross-channel correlation. At the channel level, telecom-led secure access service edge offers, including the T-Mobile and Palo Alto Networks SASE launch in 2025, expand carrier distribution as a way to bundle mobile endpoint security with connectivity and policy enforcement.

Recent Industry Developments

- June 2026: Google released Android 17 with expanded security features, including enhanced threat detection and stronger theft protection controls. These platform-level upgrades raise the baseline for consumer devices while pushing anti-malware vendors to differentiate with behavioral analytics, enterprise reporting, and response workflows that sit above OS-native protections.

- June 2025: Malwarebytes launched Scam Guard inside its Mobile Security app, adding AI-assisted, real-time guidance for scam scenarios. The development reflects vendor investment in social-engineering defense on mobile endpoints, extending mobile anti-malware beyond pure malware detection into user-facing fraud and scam prevention.

- November 2024: CrowdStrike agreed to acquire Adaptive Shield to add SaaS security posture management capabilities into the Falcon platform. The deal supports tighter linkage between mobile endpoint risk signals and broader cloud and SaaS exposure management, reinforcing the market shift toward consolidated platforms rather than stand-alone mobile antivirus tools.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers software and related services that prevent, detect, and remove malicious activity on mobile devices, mainly smartphones and tablets. It includes spending tied to mobile-focused anti-malware capabilities delivered through apps, enterprise tools, or cloud-based security services.

Scope exclusions: We exclude general desktop and server anti-malware, and we also exclude pure mobile device management tools that do not include malware prevention and remediation features.

Segmentation Overview

- By Operating System

- Android

- iOS

- Others

- By Deployment Mode

- On-premise

- Cloud

- By Solution Type

- Stand-alone Mobile Antivirus Apps

- Integrated Endpoint-Protection Suites

- Security-as-a-Service (SECaaS) for Mobile

- By End User

- Enterprises

- Consumers / Individuals

- By Industry Vertical

- BFSI

- Healthcare

- IT and Telecom

- Government and Defense

- Education

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by grounding the demand pool for protected mobile endpoints and the risk environment that drives spending. We reviewed public sources such as the US Cybersecurity and Infrastructure Security Agency (CISA) advisories, the National Institute of Standards and Technology (NIST) guidance, FCC releases on mobile ecosystem security, and statistical releases from the International Telecommunication Union (ITU) on connectivity and smartphone penetration.

To translate this context into model inputs, we also checked company public filings, investor presentations, product documentation, and reputable press coverage for pricing logic and packaging changes. Where needed, we used paid databases for company financials and intelligence, and we referenced patent databases to track mobile-threat detection techniques and feature evolution. These desk research sources are illustrative, and other public documents were used to collect data, validate inputs, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to pressure-test assumptions on mobile security budget allocation, typical contract structures, and how buyers split spend between consumer apps and enterprise deployments. We spoke with stakeholders across solution providers, channel partners, enterprise security teams, and mobility administrators. Coverage was balanced across APAC, EMEA, and the Americas so regional adoption differences and pricing levels could be normalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 39% |

| Mid tier: 56% | Functional/Unit leaders: 30% | EMEA: 36% |

| Smaller Players: 19% | Managers: 58% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand reconstruction where the device base, mobile data usage, and enterprise mobility adoption are translated into an addressable pool for paid mobile threat protection. That pool is then filtered through adoption rates by operating system and buyer type (consumer versus enterprise) so we avoid counting devices that are covered only by general endpoint tools.

The totals are corroborated with selective bottom-up approximations, mainly sampled vendor pricing and volume logic, channel checks on subscription mix, and sanity checks using reported cybersecurity spend splits for mobile endpoints. Key inputs used in the model include smartphone and tablet installed base, malware and mobile phishing incidence trends, cloud versus on-prem deployment share, average subscription price progression, and renewal behavior in enterprise accounts (illustrative, not exhaustive). Forecasting uses scenario analysis supported by expert consensus on regulation intensity, zero-trust rollouts, and the pace of cloud security adoption, and then outputs are checked for realistic year-over-year movement. Where bottom-up signals are incomplete for smaller geographies, gaps are handled through penetration-based scaling anchored to device base and verified with interview feedback.

Data Validation & Update Cycle

Validation is done through triangulation across independent indicators, where modeled spend levels are compared with device growth, security incident trends, and observed pricing direction. If the model produces unexpected jumps for a region or buyer type, the assumptions are rechecked and the team revisits the relevant public inputs and interview notes before sign-off.

A multi-step review is followed so calculation logic, unit consistency, and currency handling are double-checked by another analyst. The report is refreshed annually, and interim updates are triggered when material events occur, such as major OS policy changes, large-scale mobile malware outbreaks, or significant packaging shifts in security subscriptions. Before delivery, we run a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Mobile Anti Malware Market Sizing Compared With Other Published Estimates

Published market numbers for mobile anti-malware can vary because firms count different product bundles, use different anchor years, and apply different pricing and adoption assumptions for consumer versus enterprise use cases.

The main gap comes from whether broader mobile security suites and adjacent endpoint services are folded into the total, where Mordor Intelligence counts only spending tied to mobile anti-malware functions and then calibrates adoption by OS mix and deployment mode before projecting forward. Differences also show up when estimates use aggressive price uplift, apply a single global penetration rate, or do not normalize currency timing and regional price levels, which can inflate the apparent size in earlier years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.92 B (2026) | |

| Industry Research Publisher A | USD 5.70 B (2024) | Uses an earlier base year and a narrower monetization view in public highlights, and the coverage of enterprise mobility suites versus stand-alone mobile anti-malware is not clearly separated, which can shift what is counted as in-scope spend. |

| Global Consultancy B | USD 6.90 B (2024) | Reports a 2024 value and appears to mix feature-led security categories, so the split between pure anti-malware and broader mobile security functions is not consistently stated, and price progression assumptions are not transparent. |

The table shows that year selection and scope clarity drive most of the spread, especially around whether bundled mobile security functions are included and how pricing is stepped up over time. Our approach stays traceable because the total is built from a defined protected-device pool, is adjusted with realistic adoption and price checks, and is re-validated when market signals do not align.

Key Questions Answered in the Report

What is the projected value of the mobile anti-malware market by 2031?

The market is forecast to reach USD 31.03 billion by 2031 at a 14.28% CAGR.

Which operating system offers the fastest growth opportunity for vendors?

IOS endpoints are expected to post a 15.02% CAGR through 2031 as enterprises embrace its hardware-rooted security advantages.

Why are cloud deployment models gaining ground over on-premise systems?

Cloud platforms simplify updates, provide scalable machine-learning analytics, and cut administrative overhead by about 40% compared with maintaining local servers.

Which industry vertical spends the most on mobile anti-malware today?

Banking, financial services, and insurance entities hold 43.85% of 2025 revenue due to strict regulatory mandates and the high value of mobile transactions.

How do zero-trust regulations affect market growth?

New laws from the U.S. DOJ and Canadian OSFI require continuous mobile risk evaluation, making advanced threat defense unavoidable for compliant organizations.

What strategic moves are leading vendors making to stay competitive?

Recent acquisitions such as Sophos-Secureworks and CrowdStrike-Adaptive Shield illustrate a shift toward integrating managed detection, identity posture, and SaaS security into unified platforms.

Page last updated on: