Middle East Telecom Towers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

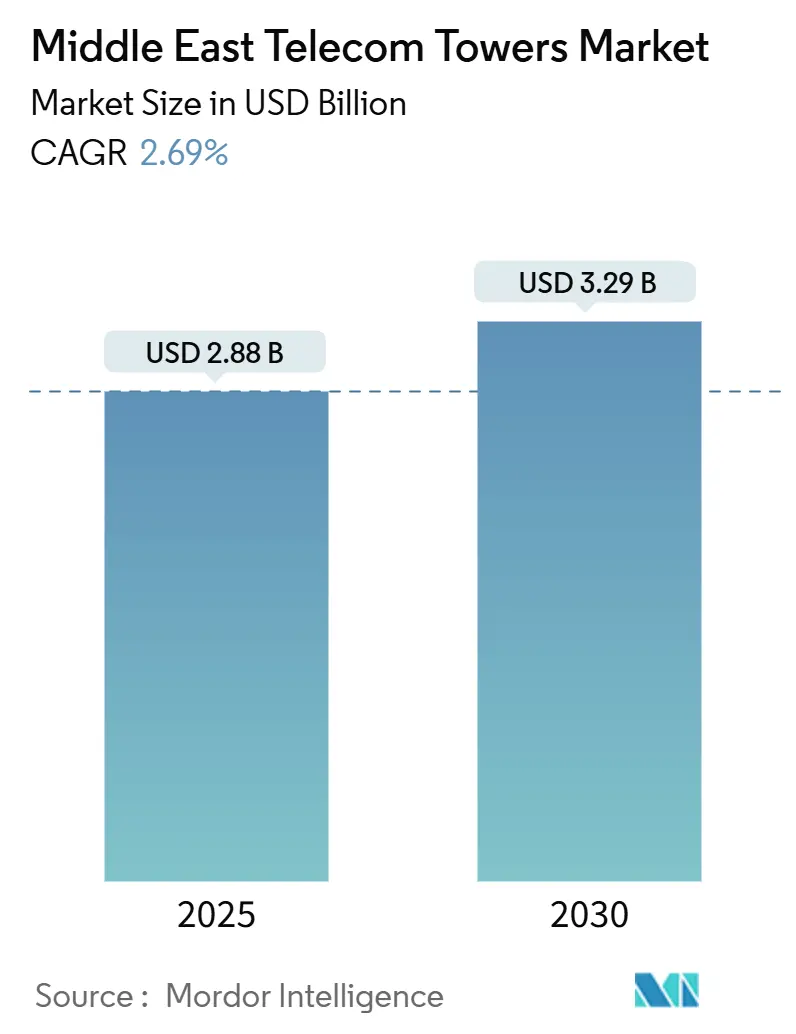

| Market Size (2025) | USD 2.88 Billion |

| Market Size (2030) | USD 3.29 Billion |

| Growth Rate (2025 - 2030) | 2.69% CAGR |

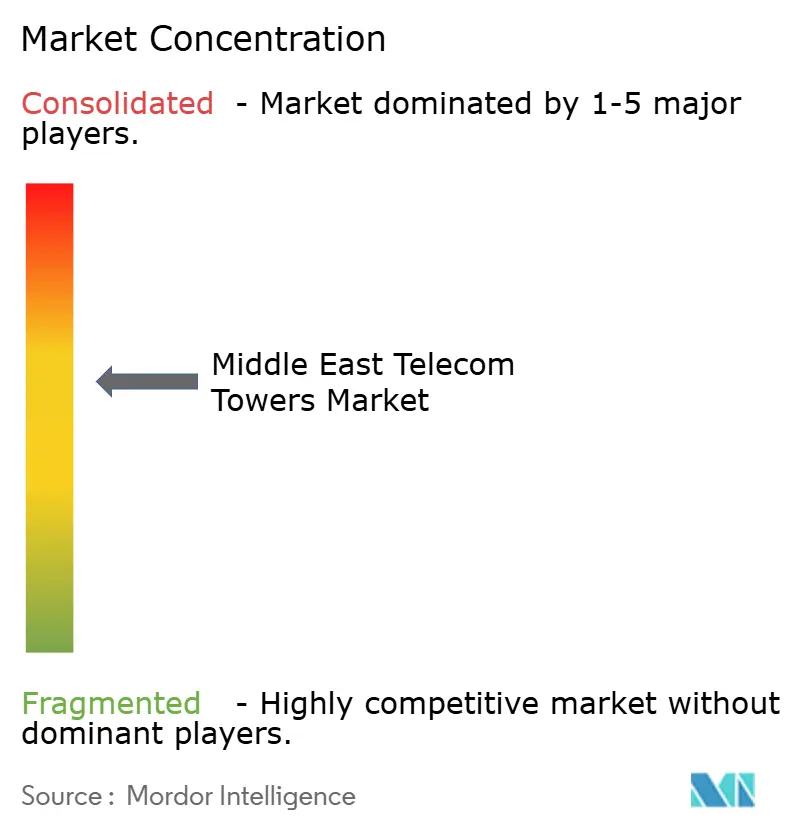

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Telecom Towers Market Analysis by Mordor Intelligence

The Middle East Telecom Towers Market size is estimated at USD 2.88 billion in 2025, and is expected to reach USD 3.29 billion by 2030, at a CAGR of 2.69% during the forecast period (2025-2030). In terms of installed base, the market is expected to grow from 89.98 thousand units in 2025 to 102.03 thousand units by 2030, at a CAGR of 2.55% during the forecast period (2025-2030).

This steady trajectory is underpinned by sovereign-backed infrastructure deals, operator divestments that unlock capital for 5G rollouts, and a growing appetite for neutral-host models that compress deployment cost and time. Independent TowerCos are capturing assets at scale, while giga-projects such as NEOM and Lusail oblige denser site grids and small-cell overlays that lift tenancy ratios. Monetization proceeds from tower sales is being recycled into private LTE/5G networks for energy corridors, advancing a virtuous cycle in which tower companies gain uplift from both macro builds and edge densification. ESG mandates, meanwhile, accelerate renewable power retrofits that create incremental equipment sales opportunities and long-term opex savings, but they also raise near-term capex hurdles in markets with high diesel dependence.

Key Report Takeaways

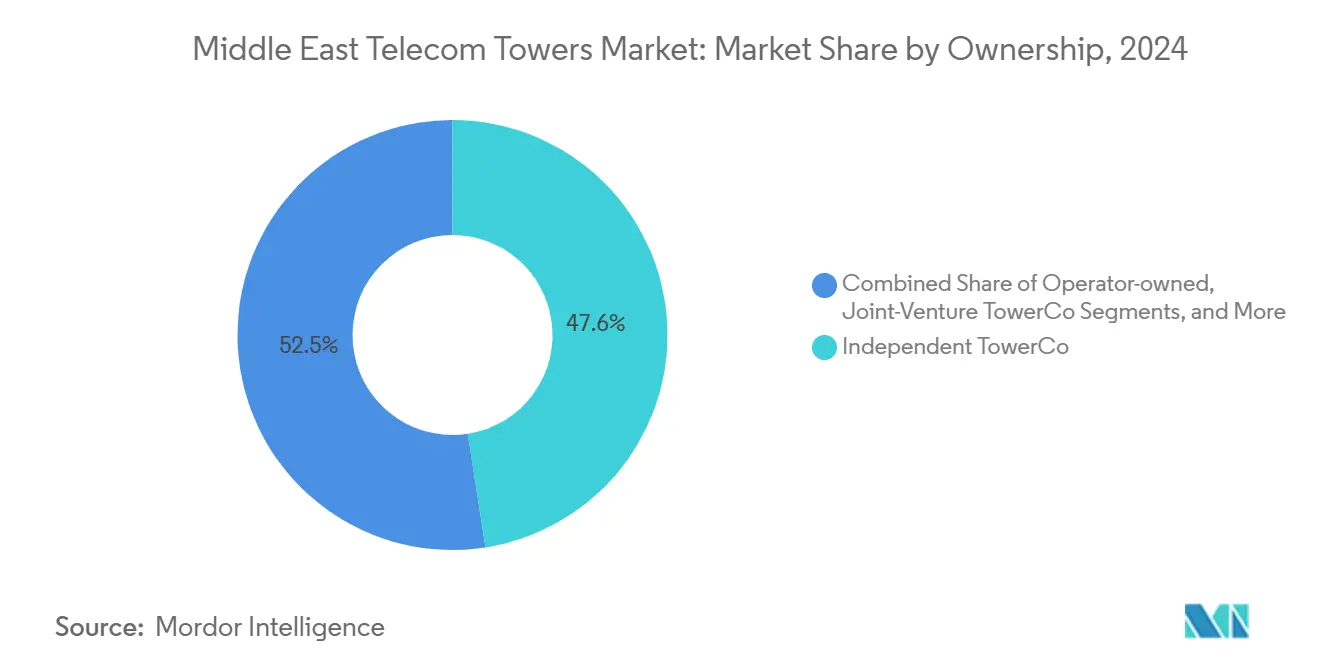

- By ownership, independent TowerCos led with 47.55% of the Middle East telecom towers market share in 2024, and is expanding at a 6.52% CAGR to 2030.

- By installation, ground-based sites accounted for a 59.71% share of the Middle East telecom towers market size in 2024, while rooftop sites are expanding at a 3.39% CAGR to 2030.

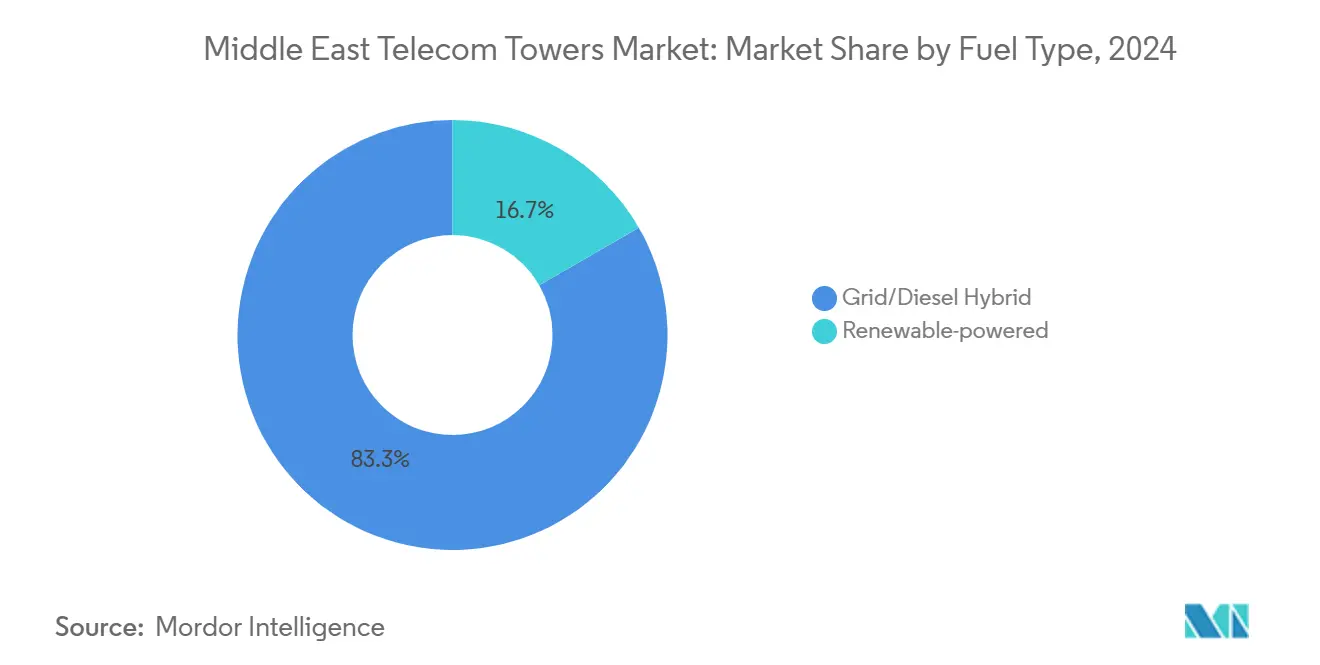

- By fuel type, the grid/diesel hybrid segment led with 83.31% share of the Middle East telecom towers market size in 2024, while renewable-powered towers are advancing at a 16.67% CAGR through 2030.

- By tower type, monopole designs commanded 48.55% share of the Middle East telecom towers market in 2024, while stealth or concealed formats are expanding at 12.22% CAGR.

- By country, Saudi Arabia captured 30.10% of the Middle East telecom towers market size in 2024, whereas the Rest of Middle East segment is projected to expand at 6.01% CAGR to 2030.

Middle East Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 5G rollouts by GCC operators | +0.8% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Mobile-data explosion from video and gaming | +0.6% | Urban GCC hubs | Short term (≤ 2 years) |

| Regulatory push for active and passive tower sharing | +0.4% | GCC expanding to wider MENA | Long term (≥ 4 years) |

| Portfolio-monetization by MNOs to cut capex | +0.5% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Private LTE/5G demand from oil and gas corridors | +0.3% | Saudi Arabia, UAE, Oman | Long term (≥ 4 years) |

| Giga-projects (NEOM, Lusail, etc.) driving small-cell densification | +0.2% | Saudi Arabia, Qatar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G roll-outs by GCC operators

GCC operators are building 5G at unprecedented scale, translating densification into higher revenue and tenancy demand for tower companies. Shared Open RAN trials have validated 40-60% capex savings, reinforcing the neutral-host case. Ongoing trials of 5G-Advanced that top 32 Gbps signal looming capacity upgrades, ensuring a multi-year pipeline of macro enhancements and small-cell infill. These dynamics create predictable demand visibility for tower owners, who earn from both new site builds and collocation amendments. The uplift is strongest in Saudi Arabia and the UAE, where statewide coverage targets are mandated [1]GCC Communications Authority, “5G Deployment Progress Report 2025,” cca.gov.sa.

Mobile-data explosion from video and gaming

Average mobile speeds in the UAE have surpassed 360 Mbps, mirroring a region-wide surge in video streaming and real-time gaming that requires low-latency links [2]UAE Telecom Regulator, “Mobile Data Traffic Statistics 2025,” tra.gov.ae . Fixed-wireless access is piggybacking on 5G, allowing operators to sweat tower assets across consumer broadband and enterprise verticals. In dense cities, traffic peaks justify rooftop small-cell clusters that raise tenancy ratios and premium SLAs. Predictable diurnal usage profiles also let tower owners optimize power and backhaul provisioning, trimming energy waste and unlocking new service-level pricing models.

Regulatory push for active and passive tower sharing

GCC regulators now embed sharing mandates into licensing, aiming to curb visual pollution and accelerate rural coverage. Policies favor neutral hosts that can guarantee non-discriminatory access, prompting operators to spin out towers into independent vehicles. Compliance frameworks are moving toward ISO 14001 certification, linking license grants to demonstrable ESG credentials. These measures expand addressable tenancy counts per site, lifting long-run utilization and revenue per tower.

Portfolio monetization by MNOs to cut capex

Operators continue unlocking cash by selling towers under long-term master lease-back contracts that preserve service control yet relieve balance sheets. Profit spikes reported post-divestiture illustrate the capital efficiency of this route, enticing additional carriers to explore similar deals. Tower buyers gain inflation-linked rental escalators, while sellers redeploy proceeds into network software, spectrum, and customer-facing digital services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical instability and conflict zones | -0.3% | Iraq, Syria, Yemen | Long term (≥ 4 years) |

| Complex municipal permitting in heritage areas | -0.2% | Historic GCC city centers | Medium term (2-4 years) |

| ESG pressure on diesel-generator emissions | -0.4% | UAE, Saudi Arabia | Short term (≤ 2 years) |

| Limited fiber backhaul in remote desert sites | -0.1% | Rural Saudi Arabia, Oman | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Geopolitical instability and conflict zones

Persistent conflict deters cross-border capital, raises insurance premiums, and fragments regional scale aspirations [3]UN ESCWA, “Conflict Impact on Digital Infrastructure 2024,” unescwa.org. Investors face sanctions compliance risks and currency volatility that constrain syndicated financing for multi-country platforms. As a consequence, tower companies often limit exposure to high-potential but high-risk frontier markets, slowing infrastructure catch-up in those territories.

ESG pressure on diesel-generator emissions

Net-zero pledges and regulatory penalties around diesel exhaust force tower owners to accelerate solar and hybrid conversions [4]International Energy Agency, “Middle East Diesel Price Tracker 2025,” iea.org. Up-front costs are substantial, especially where sites are remote and logistics complex. Operators with thin balance sheets may struggle to meet transition timelines, potentially delaying new builds until financing for renewable retrofits is secured. Over time, however, fuel-price volatility and carbon levies should make solar paybacks compelling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Accelerate Consolidation

Independent TowerCos held 47.55% of the Middle East telecom towers market in 2024, expanding at a 6.52% CAGR as carriers offload passive assets for 5G funding. The New TASC transaction that aggregated 30,000 towers across six MENA states underscores the scale advantages pursued. Neutral hosts typically secure multi-tenant anchor leases that grow revenue per tower faster than operator-owned models. Independent platforms also benefit from regulatory goodwill because their footprint combats site duplication and environmental impact.

Operator-controlled portfolios remain material, especially where national security or strategic sovereignty is prioritized. Yet even these entities increasingly form joint ventures with capital partners to de-risk expansion. Such hybrid structures blend incumbent market knowledge with financial firepower, effective in politically sensitive regions. Sovereign wealth fund backing lowers financing costs for large-scale build-outs.

By Installation: Ground-Based Sites Dominate but Rooftops Outpace Growth

Ground sites comprised 59.71% share of the Middle East telecom towers market size in 2024, owing to vast desert coverage needs and highway corridors. Rooftops, while smaller in base, are projected to grow 3.39% CAGR through 2030, propelled by urban densification and aesthetic ordinances that discourage new green-field masts. Smart-city blueprints in Lusail and NEOM specify integrated rooftop or street-level smart poles that fuse connectivity with lighting and IoT sensors, opening ancillary revenue lines.

Ground towers face rising scrutiny in heritage precincts where skyline preservation is legally protected. Permitting cycles, therefore, elongate, shifting operator preference toward low-profile rooftops or concealed poles. For tower owners, rooftop deployments can yield higher blended tenancy because multiple carriers often share prime downtown positions where spectrum scarcity presses for infill coverage.

By Fuel Type: Renewable-Powered Towers Gain Momentum

Grid/diesel hybrids still represent 83.31% of active sites, reflecting limited rural grid penetration. However, renewable-powered towers are forecast to post a 16.67% CAGR to 2030, outstripping all other categories in the Middle East telecom towers market. Solar retrofits paired with intelligent battery and ultracapacitor arrays lower lifetime opex and hedge against diesel price spikes. Major operators are committing to multi-hundred-megawatt solar procurement programs that will gradually transition fleets toward carbon neutrality and regulatory compliance.

The economics are particularly compelling where diesel logistics inflate the total delivered fuel cost. Hybrid solar-storage configurations also curb generator runtime, slashing maintenance intervals and engine overhaul expenditure. Government clean-energy targets further sweeten financing terms via green-bond instruments, widening the pool of investors willing to fund rollouts.

By Tower Type: Monopole Leads While Stealth Structures Surge

Monopole designs accounted for 48.55% share of the Middle East telecom towers market in 2024, owing to efficient land use and streamlined installation. Yet stealth and concealed variants, growing at 12.22% CAGR, are reshaping urban deployments. Municipalities increasingly stipulate camouflaged poles or tree-imitating structures in culturally sensitive zones. Innovations in composite materials permit lighter loads and easier modular upgrades, allowing hidden antennas without compromising structural integrity.

Lattice towers remain essential where high wind loads and multi-technology stacking demand robust frameworks, notably along coastal corridors. Guyed masts occupy budget-constrained applications in wide-open terrain. Overall, aesthetic considerations plus municipal cooperation capabilities will become differentiators for tower firms when bidding for infill contracts in heritage and tourist districts.

Geography Analysis

Saudi Arabia’s 30.10% share underscores its status as the single-largest revenue pool inside the Middle East telecom towers market. Vision 2030 funnels public and private capital into smart city spines requiring thousands of small cells. Sovereign-fund backing of TAWAL ensures strategic alignment with national connectivity goals, fostering expedited permitting and right-of-way access. Private industrial 5G licenses spanning energy, logistics, and manufacturing create parallel revenue channels that tower firms can monetize via bespoke campus deployments.

The UAE retains premium ARPU and world-leading 360 Mbps average speeds, translating into dense multi-technology layering across rooftops and street-level sites. ADNOC’s energy-sector 5G rollout exemplifies how vertical integration projects can double site utilization. Qatar continues investing post-World Cup, channeling tower builds into smart districts such as Lusail, where poles double as lighting and IoT nodes.

Turkey’s wait-and-see stance on 5G spectrum belies extensive 4.5G infrastructure that will need wholesale upgrades once auctions finalize. Meanwhile, Oman, Bahrain, and Kuwait pursue steady modernization, with Oman upgrading 5,600 sites in 2024 alone. Frontier states inside the Rest-of-Middle East cluster carry the highest upside given low baseline coverage, yet investors price in conflict-related risk premiums.

Competitive Landscape

Competitive intensity is moderate as three archetypes coexist. Legacy operator-owned portfolios are yielding to independent TowerCos that aggregate assets regionally, chasing economies of scale and sophisticated asset-management systems. Joint-venture vehicles blend carrier anchor tenancy with external capital and often satisfy local ownership quotas. Transactions such as New TASC’s 30,000-site megamerger and TAWAL’s cross-border expansion validate the rising threshold needed to compete effectively.

Technology differentiation revolves around shared infrastructure. Open RAN pilots cutting deployment cost by 40-60% strengthen the neutrality case. Predictive maintenance via IoT sensors and AI analytics is emerging as a key operational lever, reducing truck rolls and downtime. ESG alignment is turning into a procurement prerequisite, with bidders showcasing renewable-power roadmaps and community energy-access projects to win tenders.

Middle East Telecom Towers Industry Leaders

TAWAL SA

Helios Towers plc

Oman Tower Company

Tasc Towers Limited

STC Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ULAK and TURKSAT signed a 5G private-network deal covering 19 sites along the Istanbul Airport corridor.

- February 2025: Airgain launched a solar-powered 5G smart repeater tailored for off-grid locations.

- December 2024: Zain Group took full ownership of 2,345 Kuwait towers.

- December 2024: Turkcell and ZTE achieved 32 Gbps in a 5G-Advanced trial.

Middle East Telecom Towers Market Report Scope

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| Turkey |

| Rest of the Middle East (Jordan,Yemen, Syria, Palestine, Israel, Lebanon, Iraq, and others) |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman | |

| Turkey | |

| Rest of the Middle East (Jordan,Yemen, Syria, Palestine, Israel, Lebanon, Iraq, and others) |

Key Questions Answered in the Report

How large is the Middle East telecom towers market in 2025?

The market is valued at USD 2.88 billion in 2025 and is on track to reach USD 3.29 billion by 2030.

What is driving 5G tower demand across the Gulf?

Aggressive 5G roll-outs, data-heavy applications, and small-cell needs tied to giga-projects are spurring new site builds and upgrades.

Why are operators selling their tower assets?

Divestments free capital for spectrum and digital services while long-term lease-backs preserve network control.

Which fuel type is growing fastest at tower sites?

Renewable-powered systems are expanding at a 16.67% CAGR as ESG rules and diesel cost inflation bite.

Which country leads tower revenues in the region?

Saudi Arabia commands 30.10% market share, leveraging Vision 2030 and sovereign-fund tower investments.

What challenges slow tower deployment?

Geopolitical instability, heritage-zone permitting, diesel emission rules, and sparse rural fiber backhaul all constrain roll-out speed.

Page last updated on: