UAE Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

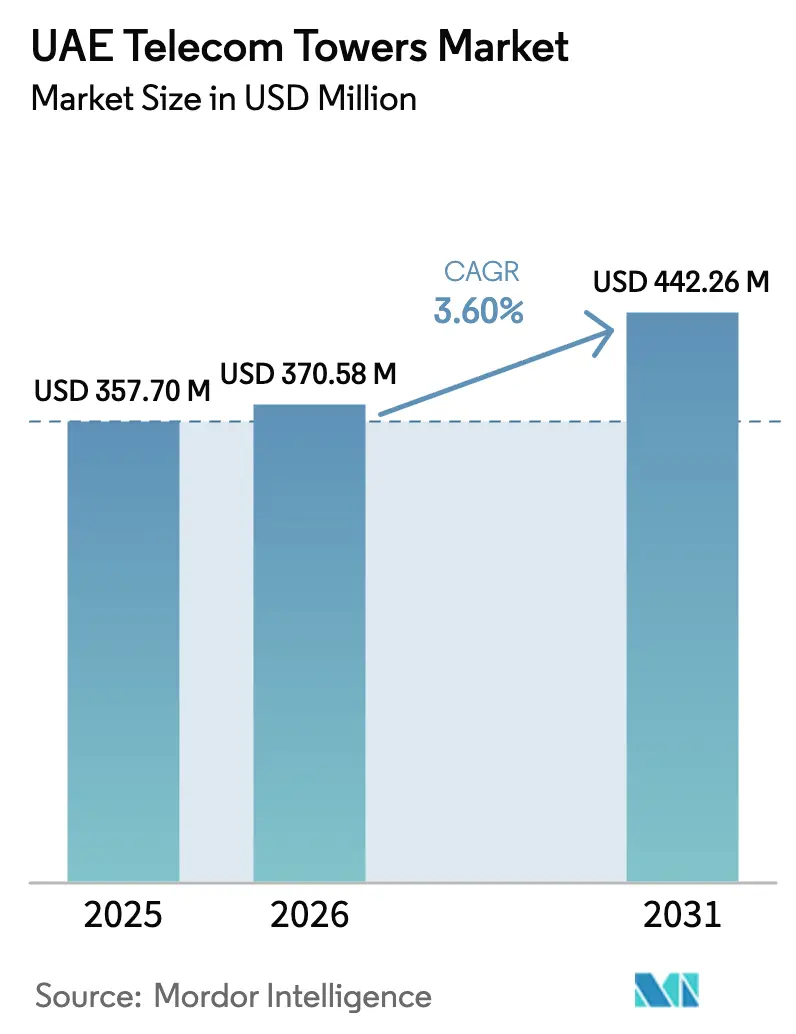

| Base Year Market Size (2025) | USD 357.70 Million |

| Market Size (2026) | USD 370.58 Million |

| Market Size (2031) | USD 442.26 Million |

| Growth Rate (2026 - 2031) | 3.60% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Telecom Towers Market Analysis by Mordor Intelligence

The UAE Telecom Towers market size is expected to grow from USD 357.70 million in 2025 to USD 370.58 million in 2026 and is forecast to reach USD 442.26 million by 2031 at 3.60% CAGR over 2026-2031.

The modest growth pace signals a maturing infrastructure landscape where selective densification and 5G-Advanced upgrades drive investment rather than greenfield expansion. Macro-to-small-cell migration in Dubai and Abu Dhabi, operator sale-leaseback strategies, and the federal net-zero road map combine to sustain tower demand even as fiber backhaul ubiquity tempers the need for additional macro sites. Independent tower companies gain relevance as neutral hosts, while operator-owned portfolios optimize for co-location efficiency. Environmental constraints such as sandstorms and high ambient temperatures shape tower design, operating costs, and lifecycle economics.

Key Report Takeaways

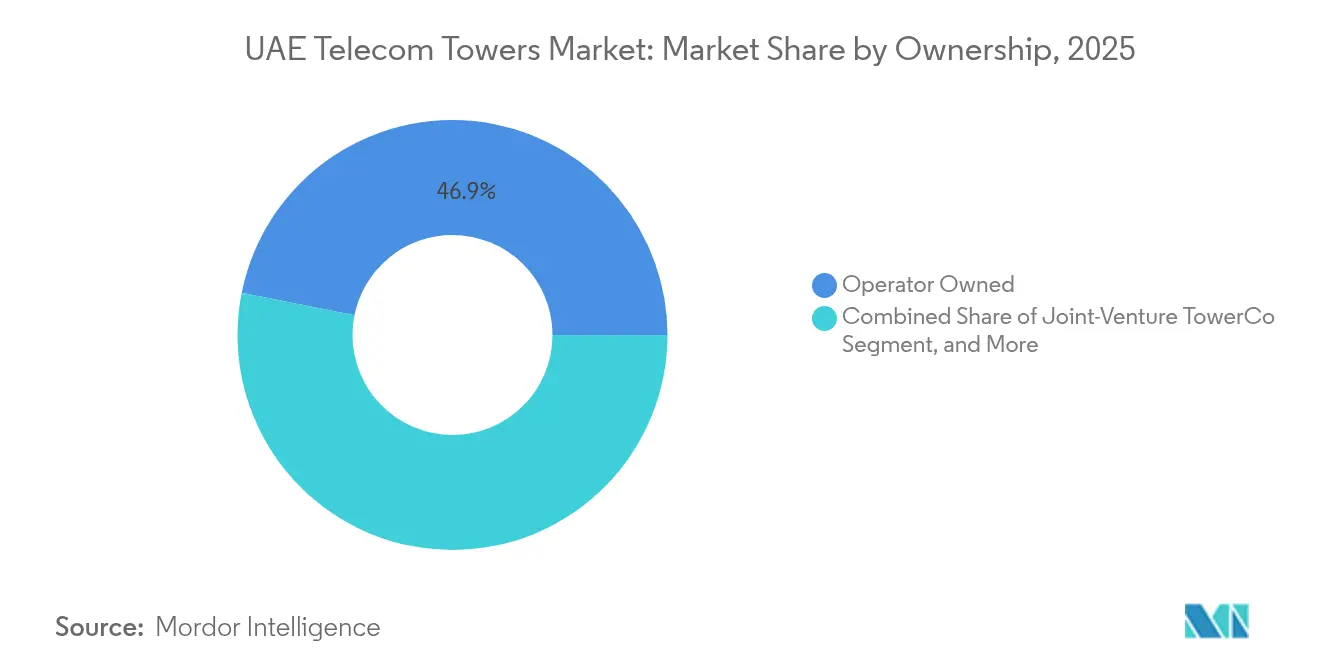

- By ownership, operator-owned sites led with 46.85% of the UAE telecom towers market share in 2025.

- Independent tower companies are projected to deliver the fastest 13.86% CAGR through 2031.

- By installation, ground-based structures commanded 49.92% of the UAE telecom towers market size in 2025.

- Rooftop solutions are advancing at a 4.42% CAGR to 2031.

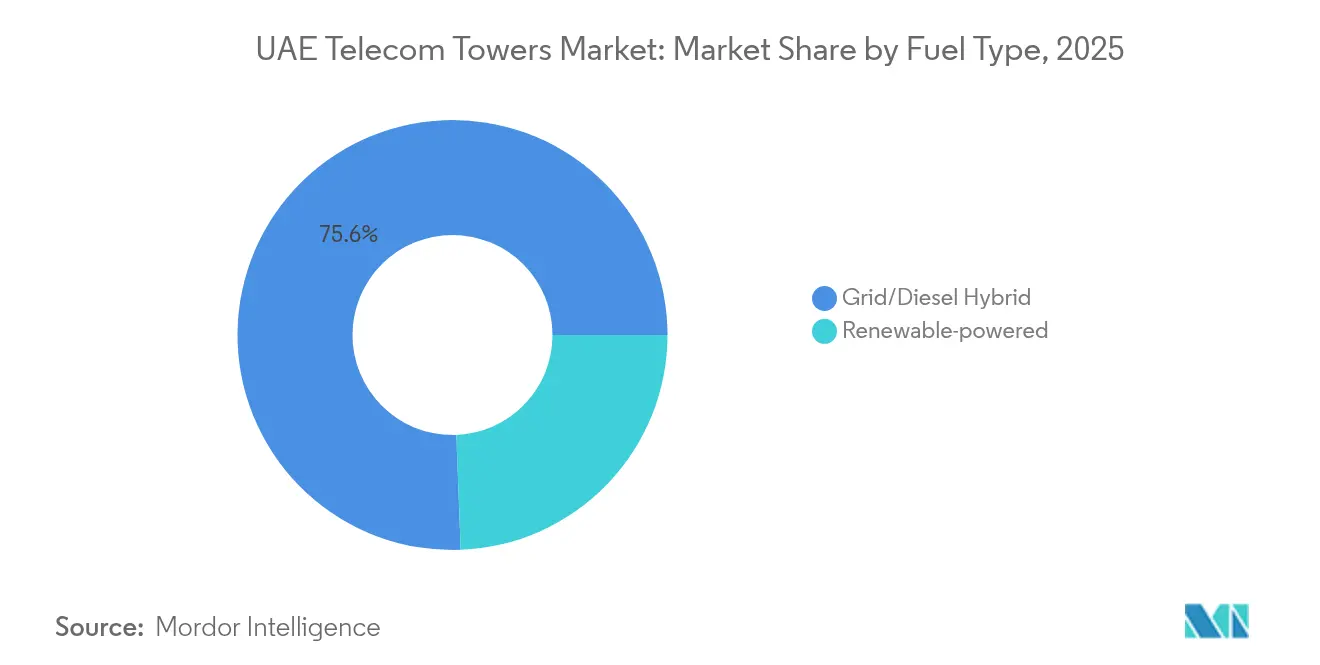

- By fuel type, grid-diesel hybrids held 75.61% of the UAE telecom towers market size in 2025, while renewables grow at 17.64% CAGR.

- By tower type, monopoles accounted for 53.55% of the UAE telecom towers market share in 2025, and stealth formats record the highest 8.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G densification mandates | +1.2% | National focus on Dubai, Abu Dhabi, Sharjah | Short term (≤ 2 years) |

| Mobile-data surge and high download speeds | +0.8% | All emirates, peak in urban corridors | Medium term (2-4 years) |

| Operator tower monetisation and sale-leasebacks | +0.6% | Nationwide asset portfolios | Medium term (2-4 years) |

| Smart-city IoT macro-to-small-cell transition | +0.4% | Dubai, Abu Dhabi smart-city zones | Long term (≥ 4 years) |

| Private 5G demand in industrial clusters | +0.3% | Abu Dhabi industrial zones, Dubai South | Medium term (2-4 years) |

| Renewable-energy retrofits and green mandates | +0.2% | Nationwide sustainability projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Densification Mandates Drive Infrastructure Expansion

TDRA’s spectrum licensing criteria obligate minimum coverage quality that pushes operators to add sites in high-traffic corridors where millimeter-wave propagation losses are acute. Etisalat by e& and du have begun 5G-Advanced rollouts in central business districts that require closely spaced low-power nodes to maintain throughput and latency performance. These deployments target enterprise use cases such as autonomous mobility, cloud gaming, and industrial automation; each demands sustained gigabit-class speeds that traditional macro coverage cannot maintain. The selective densification strategy helps the UAE telecom towers market balance network quality with capital efficiency.

Mobile Data Surge Demands Enhanced Network Capacity

Average mobile data consumption per user climbed above 25 GB per month in 2024, spurred by streaming, AR applications, and connected-device proliferation. To relieve congestion, du aggregates 3.5 GHz and 2.1 GHz spectrum and expands massive-MIMO antenna panels that require structurally modified mounts and upgraded power systems. Elevated capacity requirements lead operators to refarm 1.8 GHz spectrum for 5G-NSA overlays, which in turn drives selective tower reinforcement and antenna swap cycles across rooftop sites.[1]du, “5G-Advanced Network Enhancement Press Release 2024,” du.com

Operator Tower Monetisation Reshapes Market Structure

Sale-leaseback transactions free capital for core network software upgrades while transferring passive assets to specialist TowerCos. Etisalat by e& Infrastructure evaluates partial portfolio divestments; du already carved out a tower subsidiary that manages site leasing to emerging MVNO tenants. Independent owners such as TASC Towers and American Tower negotiate multi-tenant lease models that raise average tenancy ratios from 1.2 to 1.6, improving site economics and lowering cost-per-megabyte for hosted operators.

Smart-City IoT Transitions Create Infrastructure Complexity

Dubai’s smart-city roadmap integrates real-time traffic management, digital ID authentication, and municipal sensor networks that necessitate ubiquitous, low-latency coverage. Operators deploy edge compute cabinets at priority tower sites so AI workloads remain within the emirate for compliance and latency reasons. Concealed smart-pole designs blend with urban aesthetics and house multi-band antennas, Wi-Fi offload nodes, and environmental sensors in a single street-furniture format. [2]Dubai Smart City Office, “Smart Dubai Strategy Update 2024,” dubai.ae

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Site-acquisition hurdles and zoning limits | -0.7% | Dubai and Abu Dhabi central districts | Short term (≤ 2 years) |

| Fibre back-haul ubiquity reduces macro need | -0.5% | National FTTH coverage | Medium term (2-4 years) |

| Capex diversion toward indoor DAS and small cells | -0.4% | Commercial hubs | Medium term (2-4 years) |

| Sand-storm and heat-related O&M inflation | -0.3% | Nationwide, seasonal variance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Site-Acquisition Challenges Constrain Network Expansion

High land values and stringent zoning bylaws in premium districts lengthen approval cycles past 12 months and drive lease costs above USD 110,000 per site annually. Municipal aesthetic rules insist on stealth wraps or architectural integration that add 30% to structural cost. These hurdles delay revenue realization for TowerCos and moderate new-site growth in the UAE telecom towers market.

Fibre Infrastructure Reduces Macro Tower Dependencies

With a 99.5% FTTH penetration rate, operators rely on ubiquitous fiber backhaul to deploy compact small cells within commercial properties. This substitutes indoor DAS for outdoor macro infill, suppressing large-tower demand in densely cabled zones. Independent TowerCos shift focus toward rural expressways and industrial perimeters where fiber reach is thinner and macro structures remain economical. [3]UAE Telecommunications Sector Review 2024, “FTTH Penetration Statistics,” uae-telecom-review.ae

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent Models Gain Momentum

Operator-owned infrastructure retained 46.85% of the UAE telecom towers market share in 2025, reflecting legacy footprint advantages and regulatory familiarity. However, the UAE telecom towers market size for independent portfolios is projected to climb at a 13.86% CAGR, propelled by sale-leaseback pipelines and the appeal of capital-light strategies. Multi-tenant economics allow TowerCos such as TASC Towers to underwrite greenfield projects adjacent to logistics corridors where mobile network operators prefer to lease rather than build. Sharia-compliant financing vehicles and sovereign wealth participation further lower capital costs for independent entrants.

Rising tenancy ratios, remote diagnostics, and predictive maintenance solutions elevate operating margins for independents, encouraging foreign players to form joint ventures with local partners. Conversely, operator-controlled sites focus on mission-critical areas like government districts and oil-and-gas precincts where network sovereignty remains paramount. These dual models coexist as TDRA promotes infrastructure sharing while protecting national security interests.

By Installation: Rooftop Solutions Address Urban Constraints

Ground-based towers accounted for 49.92% of the UAE telecom towers market size in 2025 owing to their historical dominance across highways and suburban belts. Rooftop formats grow at a 4.42% CAGR as vertical densification outpaces horizontal sprawl in Dubai and Abu Dhabi. Building owners monetize air rights through lease agreements that often exceed USD 45,000 per annum, converting idle space into recurring revenue. The lighter weight of 5G active-antenna units lets operators install three-sector sites without structural reinforcement, accelerating deployment cycles from six months to ten weeks.

Though line-of-sight propagation can be challenging among skyscrapers, new beamforming algorithms and tilt optimization boost rooftop coverage reliability. Ground-based structures remain indispensable along arterial highways, desert corridors, and industrial zones where building stock is sparse. TowerCos adopt hybrid rollout plans, combining street-level monopoles with rooftop nodes to achieve contiguous service.

By Fuel Type: Renewable Transition Accelerates

Grid-diesel hybrids sustained 75.61% of the UAE telecom towers market size in 2025, supported by a well-developed national electricity grid and mandatory backup runtime requirements. Nevertheless, the renewable category grows at 17.64% CAGR as photovoltaic costs slide below USD 0.015 per kWh and lithium-iron-phosphate storage becomes mainstream. Operators pilot solar-plus-battery retrofits on desert corridors vulnerable to fuel logistics delays. These pilot sites show a 28% fall in total cost of ownership within three years, validating broader rollouts coinciding with the UAE Energy Strategy 2050.

Policy incentives like green-loan interest rebates and carbon-credit eligibility enhance project viability. Hybrid microgrid controllers let TowerCos sequence battery discharge to minimize generator hours, slashing diesel consumption by 55% over baseline. Grid reliability in metropolitan areas keeps conventional power favored for rooftop sites, yet any new remote tower tender now mandates renewable feasibility analysis.

By Tower Type: Stealth Designs Meet Urban Requirements

Monopoles achieved 53.55% UAE telecom towers market share in 2025 thanks to compact footprints, modular sections, and rapid installation. Stealth and concealed variants post the fastest 8.62% CAGR, driven by municipal ordinances that protect skyline aesthetics near heritage sites, luxury resorts, and waterfront promenades. Wrap-around panel designs imitate lamp posts or palm trees, allowing site approvals within 60 days versus 120 days for exposed steel structures.

Lattice structures remain preferred for heavy-loading scenarios such as multi-operator co-locations or broadcast antennas exceeding 200 kg. Guyed masts are rare due to land scarcity and safety clearances. The 5G era raises antenna counts per site, prompting TowerCos to retrofit monopoles with stronger mount brackets and to employ cathodic-protection coatings that withstand abrasive sandstorms.

Geography Analysis

Dubai and Abu Dhabi account for roughly 74.62% of active tower sites, reflecting population density, commercial activity, and data-heavy service demand. Dubai’s financial hubs, tourism corridors, and metro rail lines require low-latency coverage, prompting roofline micro sites every 300 m along Sheikh Zayed Road. The city’s ExploritY smart-mobility district integrates smart poles with edge compute modules that host AI workloads for traffic analytics, supporting multi-operator tenants under a neutral-host agreement.

Abu Dhabi leverages its industrial diversification initiative to deploy private 5G networks across petrochemical complexes and logistics hubs near Khalifa Port. ADNOC’s dedicated spectrum allocation produces bespoke tower clusters with elevated ground clearances to minimize hazardous-area risks. These private installations feed incremental tenancy for TowerCos as subcontractors manage passive infrastructure under long-term service contracts. Sharjah, Ajman, and Ras Al Khaimah represent emerging growth nodes where mixed-use developments add rooftop leasing demand. Coastal industrial estates at Ras Al Khaimah deploy renewable-powered monopoles to cope with grid intermittency during summer peak loads. Fujairah and Umm Al Quwain exhibit smaller footprints yet present white-spot coverage mandates along cross-emirate highway corridors, drawing modest but steady tower investment. TDRA’s infrastructure-sharing policy ensures that every new macro site hosts at least two operator tenants wherever feasible, driving improved capital utilization across all seven emirates.

Competitive Landscape

The UAE telecom towers market hosts a moderate concentration profile where the top five players control about 68% of the installed base. Etisalat by e& Infrastructure and du Tower Operations safeguard strategic locations but increasingly lease capacity to MVNOs like Virgin Mobile UAE, reflecting regulatory encouragement for service-level competition. Both incumbents deploy AI-enabled predictive maintenance, cutting downtime by 18% and lowering truck rolls.

Independent TowerCos raise their profile through scale economics and differentiated service offerings. TASC Towers pursues build-to-suit contracts along energy corridors and industrial estates, while American Tower’s representative office negotiates portfolio acquisitions to gain rapid foothold. Partnerships with local investors support compliance with foreign ownership limits and streamline municipal engagement.

Technology trends accelerate competitive intensity. Cloud-native RAN, Open RAN pilots, and smart-pole form factors demand tower upgrades that smaller owners may struggle to finance. Meanwhile, green-financing instruments favor TowerCos that commit to renewable retrofits, giving sustainability-focused portfolios a cost-of-capital advantage. The interplay of asset monetization, technological shifts, and environmental mandates shapes a marketplace where ownership structure adaptability equates to lasting competitive edge.

UAE Telecom Towers Industry Leaders

Emirates Integrated Telecommunications Company (du)

Etisalat

TASC Towers

American Tower

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: e& UAE invested USD 50 million in Microsoft Azure Operator Nexus to extend edge computing across tower sites.

- December 2024: du finalized its 5G-Advanced rollout, adding carrier aggregation for millimeter-wave coverage.

- November 2024: Abu Dhabi unveiled an AED 13 billion digital modernization plan that raises demand for AI-ready tower infrastructure.

- October 2024: ADNOC and e& completed the region’s largest private 5G network spanning industrial clusters.

UAE Telecom Towers Market Report Scope

Telecommunication towers come in various structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and similar configurations. These towers house one or more telecommunication antennas, facilitating radio communications. They can be situated on the ground or atop a building, often including equipment and electronic components storage. While these towers don't need constant staffing, they require periodic maintenance. Driven by the rollout of 5G infrastructure, the expansion of telecom towers is poised to persist during the forecast period.

The UAE telecom towers market report is segmented by ownership (operator-owned, private-owned, and MNO captive), installation (rooftop and ground-based), and by fuel type (renewable and non-renewable). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How large is the UAE telecom towers market in 2026?

The UAE telecom towers market size is USD 370.58 million in 2026.

What CAGR is forecast for UAE tower revenues to 2031?

Revenue is projected to rise at a 3.60% CAGR between 2026 and 2031.

Which tower ownership model is growing fastest?

Independent TowerCos record the highest 13.86% CAGR due to sale-leaseback activity.

Why are rooftop installations gaining traction?

Limited ground space in major cities and lighter 5G hardware make rooftops quicker to permit and install.

How are sustainability goals affecting tower power systems?

Renewable-powered sites are expanding at a 17.64% CAGR as operators align with the UAE net-zero target.

What is driving demand for stealth towers?

Aesthetic zoning rules in premium urban areas favor concealed structures, leading to an 8.62% CAGR for stealth formats.

Page last updated on: