China Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 18.84 Billion |

| Market Size (2026) | USD 19.57 Billion |

| Market Size (2031) | USD 23.66 Billion |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

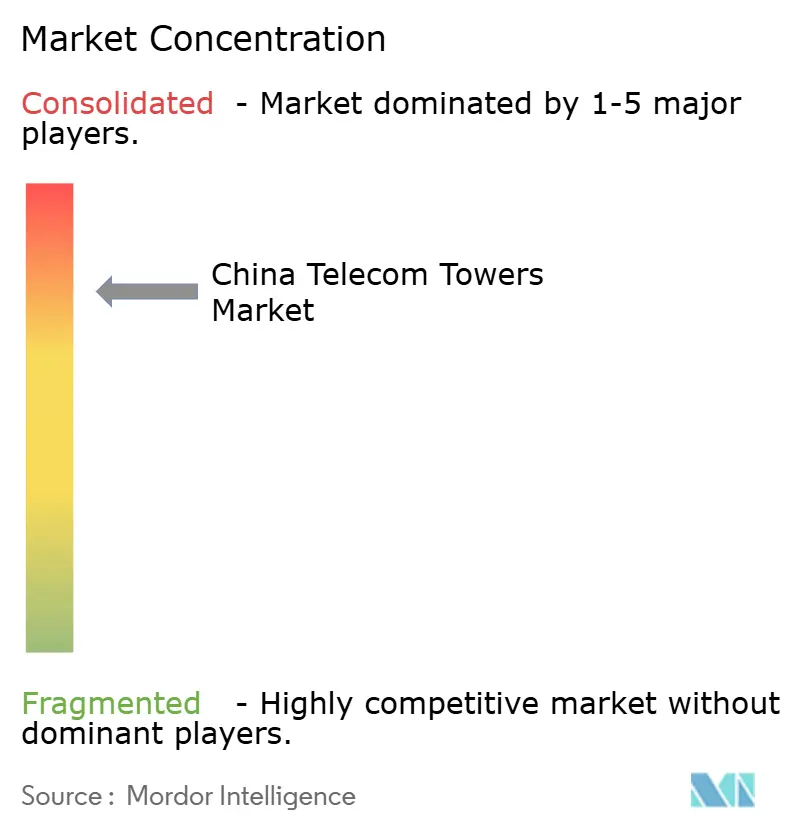

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Telecom Towers Market Analysis by Mordor Intelligence

The China Telecom Towers Market size was valued at USD 18.84 billion in 2025 and estimated to grow from USD 19.57 billion in 2026 to reach USD 23.66 billion by 2031, at a CAGR of 3.88% during the forecast period (2026-2031).

The current expansion phase is less about raw site proliferation and more about squeezing capacity out of existing footprints, particularly through tower densification, indoor systems, and the conversion of passive structures into digital nodes. Scale advantages enjoyed by China Tower Corporation (CTC)—which oversees more than 2.1 million sites—translate into lower procurement costs, coordinated multi-tenant loading, and data-driven maintenance savings. Urban land scarcity keeps operators focused on rooftops and low-profile designs, while state-backed rural programs sustain green-field demand. The steady addition of edge-computing cabinets, electric-vehicle battery-swap kiosks, and IoT gateways is broadening revenue pathways and boosting the long-run value of the China telecom towers market.

Key Report Takeaways

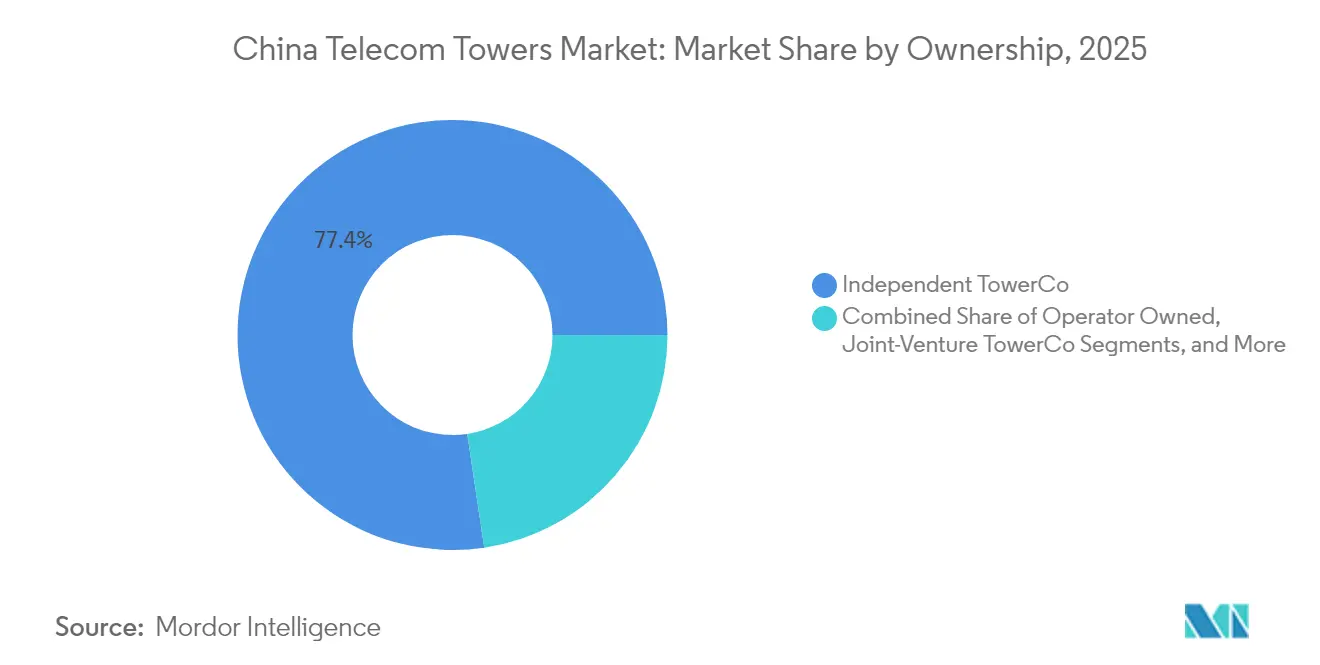

- By ownership, independent TowerCo operations led with 77.36% of the China telecom towers market share in 2025; the MNO-captive segment is advancing at a 7.32% CAGR through 2031.

- By installation, rooftops commanded 54.12% of the China telecom towers market size in 2025 and are expanding at a 4.34% CAGR.

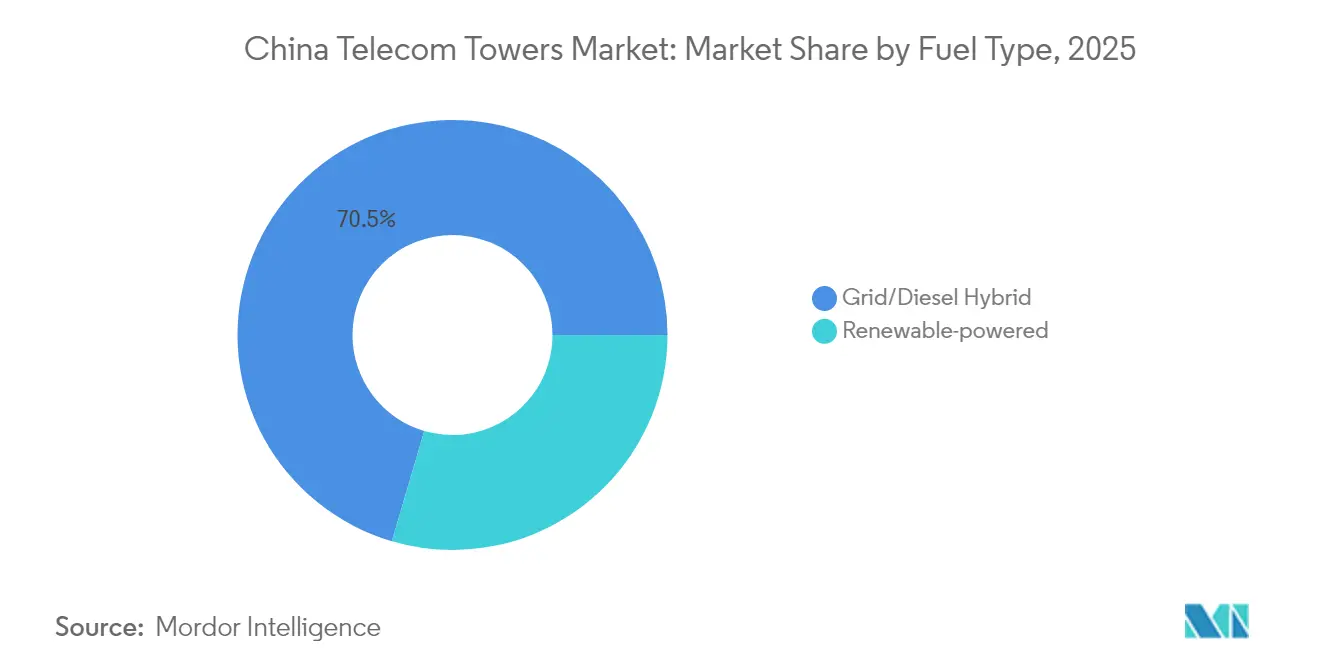

- By fuel type, grid/diesel hybrids held 70.45% of the overall market size in 2025, while renewable-only sites are scaling at a 16.45% CAGR.

- By tower type, monopoles controlled 41.98% of the China telecom towers market share in 2025; stealth designs are recording the quickest growth at a 8.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 5G macro-site densification | +1.2% | National; Tier-1/2 cities | Medium term (2-4 years) |

| Rural digital-connectivity mandates | +0.8% | Western and rural provinces | Long term (≥ 4 years) |

| Indoor DAS & small-cell boom | +0.9% | Beijing, Shanghai, Shenzhen, Guangzhou | Short term (≤ 2 years) |

| Surging mobile-data & IoT traffic | +0.7% | National with urban concentration | Medium term (2-4 years) |

| Edge-computing rollout at tower base | +0.4% | Tier-1 cities; industrial zones | Long term (≥ 4 years) |

| EV battery-swap monetization | +0.3% | Eastern coastal cities; major highways | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G Macro-Site Densification

China’s present 5G-Advanced phase is raising structural loads and power draw, forcing the replacement of legacy poles with stronger formats that can host 5.5G-ready antenna arrays. A showcase in Hangzhou achieved 25 Gbps downlink and 17 Gbps uplink, proving the commercial upside of upgrading rather than merely adding sites. [1]ZTE Corporation, “ZTE and China Telecom Complete 5G-Advanced Showcase in Hangzhou,” zte.com.cnEmerging reconfigurable intelligent surfaces have recorded six-fold downlink and 20-fold uplink improvements, tying tower revenue to performance gains instead of simple coverage growth. Operators are therefore focusing capital on high-value replacements capable of longer economic life cycles. This mix of technology renewal and capacity pressure is expected to keep the China telecom towers market on a measured but resilient growth trajectory.

Rural Digital-Connectivity Mandates

Universal-service policies compel carriers to extend 4G and 5G to sparsely populated western provinces where pay-back periods are lengthy. Hybrid satellite-terrestrial towers now combine low-band cellular gear with low-earth-orbit backhaul, providing seamless footprints. CTC’s newest rural kits pair solar panels with lithium-iron-phosphate batteries, cutting diesel runtime by 65% and aligning with carbon-neutral targets. [2]China Tower Corporation, “2024 Interim Report,” chinatower.com.cnSubsidies further de-risk deployments, anchoring a durable pipeline of sites that smooth revenue cyclicality. Consequently, rural mandates add steady ballast to the China telecom towers market even as urban areas mature.

Indoor DAS and Small-Cell Boom

Roughly 80% of mobile data originates indoors, prompting operators to blanket malls, transit hubs, and office towers with dense nodes. Huawei’s LampSite platform integrates fiber backhaul and power feeds directly from nearby tower assets, simplifying roll-outs. Private 5G in factories and logistics parks intensifies demand for dedicated indoor coverage, enabling TowerCos to lease backhaul links, edge racks, and power in a single package. Each rooftop or monopole effectively becomes a gateway that feeds indoor hotspots, cementing towers as the control point for dense urban coverage. This virtuous indoor-outdoor loop underpins continued investment within the China telecom towers market.

Surging Mobile-Data and IoT Traffic Volumes

China registered more than 150 million IoT endpoints on carrier networks in 2024, and NB-IoT alone spanned 410,000 base stations. Video streaming, cloud gaming, and industrial telemetry inflate uplink requirements, pushing asymmetric capacity designs. AI-driven resource allocation now tunes power and spectrum at individual towers in real time, boosting network efficiency and delaying costly spectrum auctions. By integrating compute, storage, and power management, towers transition from passive hosts to active edge nodes, widening the service envelope of the China telecom towers market.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Site-acquisition and zoning bottlenecks | -0.6% | Urban; scenic and environmentally sensitive zones | Short term (≤ 2 years) |

| Escalating steel and power-equipment costs | -0.4% | National | Medium term (2-4 years) |

| Regulatory scrutiny on RF emissions | -0.3% | Urban residential areas; scenic locations | Medium term (2-4 years) |

| Net tower retirements from 2G/3G switch-off | -0.2% | Legacy rural footprints | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Site-Acquisition and Zoning Bottlenecks

Urban projects typically require extended municipal approvals and environmental studies, stretching build times by 6–12 months. Camouflaged pine or palm designs cost USD 1,300–2,000 per ton and add material premiums that smaller developers struggle to absorb.[3]Debao Tower, “Camouflaged Antenna Pole Catalog,” debaotower.com While CTC’s centralized land-lease model trims paperwork, community consultations remain unavoidable. These hurdles slow near-term expansion and shave several basis points off projected growth for the China telecom towers market.

Escalating Steel and Power-Equipment Costs

Steel prices swung between USD 800 and USD 1,600 per ton during 2024–25, compressing TowerCo margins. Adding solar panels and lithium-iron-phosphate batteries raises project budgets by 20–30%, while currency fluctuations complicate bid pricing. Smaller firms therefore hesitate to lock into multi-year build programs, limiting competitive pressure. Although demand fundamentals are intact, rising input costs are a clear headwind to the China telecom towers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Consolidation Enhances Efficiency

Independent TowerCos controlled 77.36% of the China telecom towers market size in 2025, a dominance rooted in CTC’s unmatched footprint. The remaining carrier-owned portfolios, although smaller, are on a brisk 7.32% CAGR trajectory for 2026–31. CTC’s “One Core Two Wings” strategy added 220,000 “digital towers” with smart power, sensors, and edge compute, unlocking predictive maintenance and procurement savings. Capital-light tenancy fees allow mobile operators to divert cash toward spectrum and core-network upgrades. Over the forecast period, TowerCos plan to expand offerings—fiber backhaul, renewable power, and edge hosting—to deepen share of tenant spending, reinforcing the China telecom towers market as a structurally consolidated arena.

Carrier-owned sites persist where ultra-low latency or proprietary control is essential, such as isolated factory floors. Even here, non-core parcels increasingly migrate to TowerCos via sale-and-leaseback deals, further concentrating ownership. This symbiotic model distributes cost savings across both asset classes while preserving service quality, strengthening the competitive fabric of the China telecom towers market.

By Installation: Rooftop Dominance Mirrors Urban Realities

Rooftop sites accounted for 54.12% of the China telecom towers market size in 2025 and are growing at a 4.34% CAGR. Building-integrated designs reduce street-level clutter and expedite approvals, especially in cities enforcing strict skyline rules. Rooftop poles now bundle multi-band radios, microwave links, and solar panels, turning unused air-rights into high-yield utility hubs. Each urban block frequently needs two or three low-power cells to deliver 5G throughput, anchoring rooftops as indispensable to the China telecom towers market.

Ground-based macros face mounting resident pushback, forcing operators toward innovative stealth wraps, paint schemes, and façade-mounted antennas. Landlords often shoulder structural support, trimming capital outlays for TowerCos and lifting returns. As densification accelerates, tower owners continue to favor vertical real estate, reinforcing revenue momentum across the China telecom towers market.

By Fuel Type: Renewables Accelerate, Hybrids Hold Sway

Grid/diesel hybrids retained 70.45% of the China telecom towers market share in 2025, prized for resilience during power outages. Yet renewable-only sites are scaling at a 16.45% CAGR as carbon-neutral pledges collide with falling solar levelized costs. CTC’s bulk procurement shaved 15% off photovoltaic-battery kits compared with 2023 levels, narrowing the cost gap with diesel backups. AI-based controllers now orchestrate generation, storage, and grid draw, slashing genset runtime to single-digit hours annually. These efficiencies attract ESG-aligned capital, channeling investment toward the China telecom towers market.

Smaller operators still rely on hybrids to manage power volatility, but subsidies and carbon pricing are tilting economics in favor of renewables. Over time, hybrid portfolios are expected to transition toward higher renewable fractions, reshaping opex profiles across the sector.

By Tower Type: Stealth Solutions Gain Ground

Monopoles held 41.98% of the China telecom towers market share in 2025 due to lower material costs and rapid deployment. However, stealth formats—pines, palms, lamp posts—are growing at a 8.78% CAGR as municipal councils clamp down on visual impact. Premium designs fetch margins 15–20 percentage points above standard steel and can cut permit cycles in half. Lattice towers retain relevance along highways and energy corridors that demand high loading and wind tolerance, ensuring a balanced asset mix within the China telecom towers market.

Advanced composites and modular kits meet seismic and wind codes while trimming on-site labor. Such innovations reconcile aesthetic and engineering goals, maintaining healthy margins for both TowerCos and suppliers.

Geography Analysis

Eastern economic hubs—Beijing, Shanghai, Guangdong, and Zhejiang—concentrated the largest slice of the China telecom towers market in 2025, fueled by dense populations, high data consumption, and bandwidth-hungry industries. Hangzhou’s 5G-Advanced trial achieving 25 Gbps underscores the region’s appetite for next-generation capacity. Within these megacities, a single commercial district can host dozens of rooftop nodes, indoor DAS hubs, and micro-datacenters, translating urban density into recurring revenue for tower owners.

Central provinces such as Henan and Hubei trail eastern peers in absolute counts but exhibit higher growth rates thanks to universal-service subsidies and the Rural Revitalization Plan. Renewable-powered sites dominate remote locations where grid extension is uneconomic, aligning telecom roll-outs with local carbon-reduction strategies. TowerCos often bundle satellite backhaul with solar-battery packs, delivering contiguous broadband that supports distance learning and e-health services.

Along Belt-and-Road corridors, specialized security-hardened towers manage cross-border data flows and logistics telemetry. China Communications Services booked USD 325 million in overseas infrastructure revenue during 2024, illustrating how domestic expertise is exported to Asia and Africa. These projects diversify income streams and embed geopolitical influence, adding depth to the China telecom towers market across geographies.

Competitive Landscape

China Tower Corporation’s management of more than 2.1 million structures gives it quasi-monopoly status, with predictive analytics lowering maintenance costs by 12% year-over-year and raising tenancy ratios to 1.34. Scale economics allow the firm to negotiate favorable steel and battery prices, widening the moat around its core business. Smaller TowerCos and original-equipment manufacturers therefore carve niches in stealth aesthetics, modular kits, and AI-driven power systems rather than attempting to match site counts.

Huawei binds radios, transport, and edge compute into turnkey bundles whose 2024 ICT-infrastructure revenue reached USD 55.9 billion. ZTE complements this stack with software-defined orchestration, while AsiaInfo focuses on private-network services, collectively expanding spend beyond steel and concrete. Debao Tower and Hebei Teng Yang meet municipal aesthetic codes with camouflaged offerings that command price premiums and shorten permit cycles.

Regulatory scrutiny on RF emissions, cybersecurity, and carbon benchmarks steers customers toward proven suppliers, reinforcing an incumbent-friendly environment. As a result, competitive intensity manifests more in service scope and technological differentiation than in price wars, sustaining the profitability of the China telecom towers market.

China Telecom Towers Industry Leaders

China Tower Corporation Limited

Guodong Network Communication Group

Zhejiang Debao Tower Manufacturing Co.,Ltd

Daji Group

XH Tower Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Huawei released its 2024 Annual Report showing ICT-infrastructure revenue of USD 55.9 billion, up 4.9% YoY, reflecting robust demand for tower-centric solutions.

- February 2025: AsiaInfo Technologies and Hong Kong Telecommunications formed a pact to co-develop private 5G, IoT, and AI services, deepening opportunities for customized tower infrastructure.

- January 2025: UTStarcom secured a multi-million-dollar order from China Telecom Research Institute for 5G routers that will underpin new tower sites.

- November 2024: MTN South Africa, China Telecom, and Huawei agreed to collaborate on 5G, cloud, IoT, and AI, highlighting Chinese tower know-how crossing borders.

China Telecom Towers Market Report Scope

Telecommunication towers come in various structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and similar configurations. These towers house one or more telecommunication antennas, facilitating radio communications. They can be situated on the ground or atop a building, often including storage for equipment and electronic components. While these towers don't need constant staffing, they do require periodic maintenance. Driven by the rollout of 5G infrastructure, the expansion of telecom towers is expected to increase during the forecast period.

The Chinese telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive), installation (rooftop and ground-based), and fuel type (renewable and non-renewable). The market sizes and forecasts are provided in terms of volume (Units) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How large is the China telecom towers market in 2026?

The China telecom towers market size reached USD 19.57 billion in 2026 and is forecast to rise to USD 23.66 billion by 2031.

Which ownership model holds the largest site share?

Independent TowerCos led by China Tower Corporation controlled 77.36% of national sites in 2025.

What fuel source is growing the fastest?

Renewable-only power systems are expanding at a 16.45% CAGR between 2026 and 2031 as operators aim for carbon neutrality.

Why are rooftop sites so common in Chinese cities?

Rooftops sidestep land scarcity and strict zoning, giving them a 54.12% deployment share in 2025.

How are towers being monetized beyond antenna hosting?

TowerCos now add edge compute racks, EV battery-swap kiosks, and IoT gateways, diversifying income streams and boosting returns.

What segment of tower type is advancing quickest?

Stealth designs such as camouflaged pines and palms are posting a 8.78% CAGR between 2026 and 2031 as municipalities tighten aesthetic rules.

Page last updated on: