Saudi Arabia Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

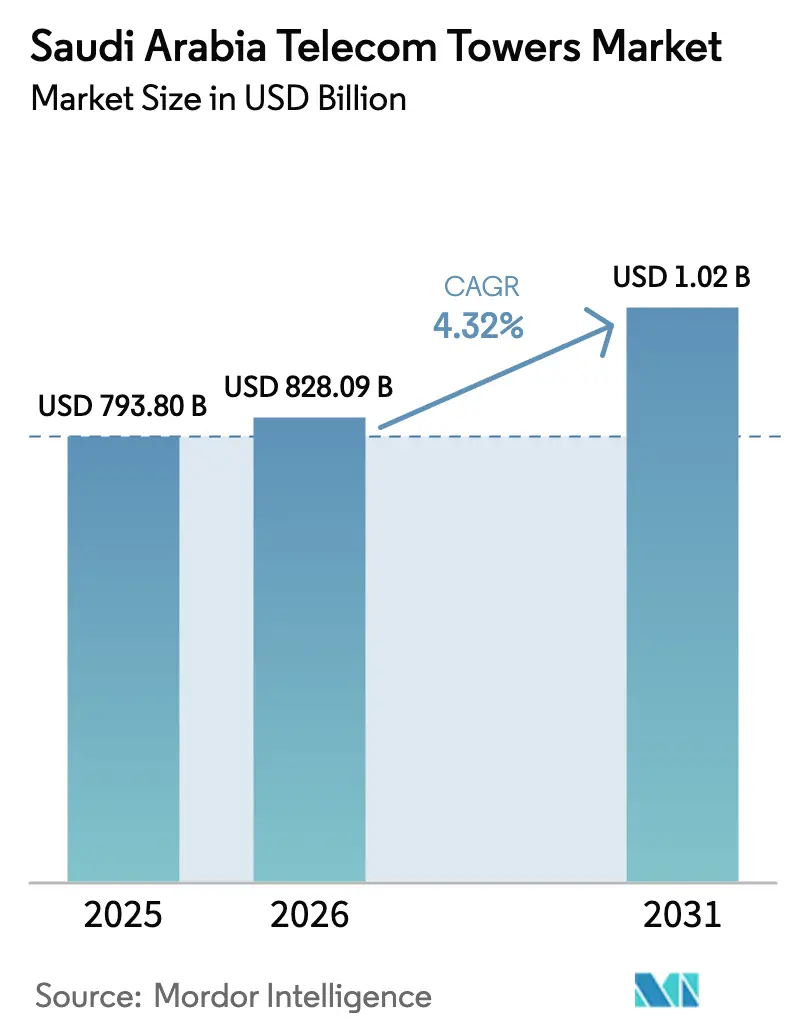

| Base Year Market Size (2025) | USD 793.80 Million |

| Market Size (2026) | USD 828.09 Million |

| Market Size (2031) | USD 1023.28 Million |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

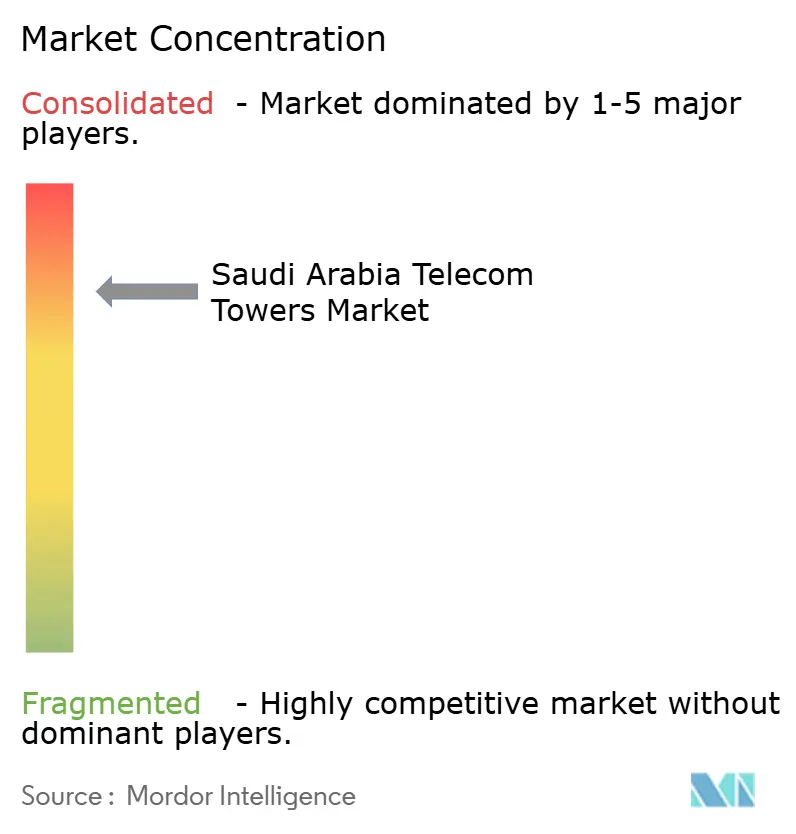

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Telecom Towers Market Analysis by Mordor Intelligence

Saudi Arabia Telecom Towers market size in 2026 is estimated at USD 828.09 million, growing from 2025 value of USD 793.80 million with 2031 projections showing USD 1023.28 million, growing at 4.32% CAGR over 2026-2031.

Solid growth stems from synchronized 5G spectrum releases, Vision 2030 infrastructure budgets, and the Public Investment Fund’s (PIF) large‐scale asset consolidation strategy, all of which direct capital toward passive‐infrastructure upgrades instead of fresh green-field builds. Independent tower companies are scaling rapidly as operators monetize real-estate assets to fund active-network rollouts, while giga-projects such as NEOM and Red Sea mandate ultra-dense, low‐latency coverage requirements that push colocation ratios higher. Renewable-hybrid power solutions are gaining traction as diesel logistics inflate operating expenses at off-grid sites, reinforcing demand for solar-battery retrofits. Competitive pressure now centers on tenancy optimization, predictive maintenance, and stealth designs that satisfy municipal aesthetic rules, rather than on raw tower counts. The Saudi Arabia telecom towers market therefore offers sustained revenue visibility through long-term master lease agreements, backed by regulatory support for hybrid terrestrial–satellite coverage models that help close rural gaps.

Key Report Takeaways

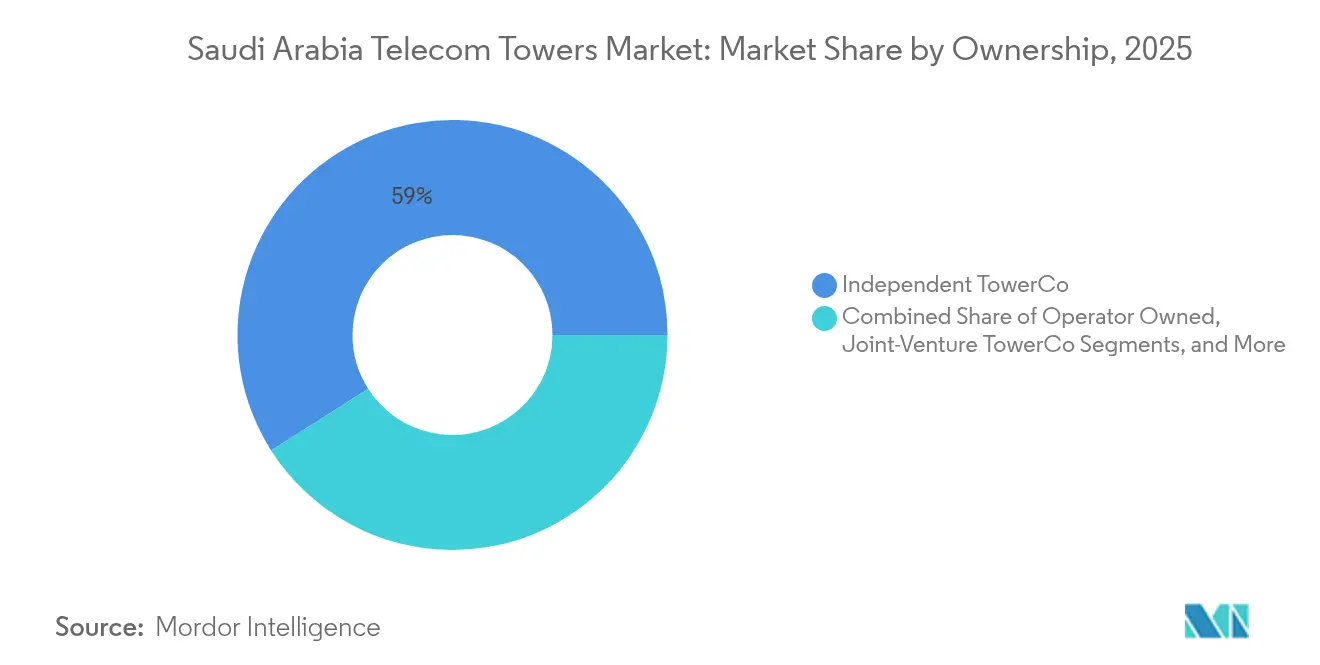

- By ownership, independent TowerCos held 59.02% of the Saudi Arabia telecom towers market share in 2025; operator divestitures are forecast to lift this segment at a 6.28% CAGR through 2031.

- By installation type, ground-based sites controlled 58.74% of the Saudi Arabia telecom towers market size in 2025, whereas rooftop deployments are set to expand at a 5.87% CAGR between 2026-2031.

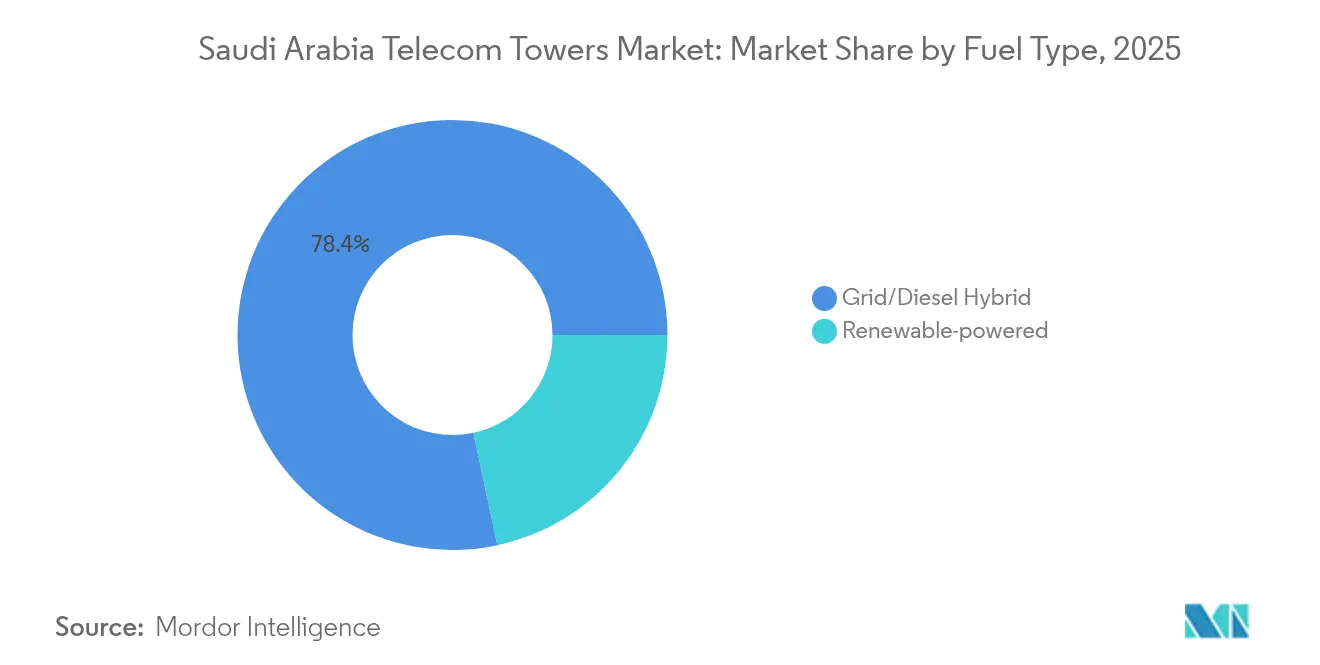

- By power system, grid-and-diesel hybrids accounted for 78.35% of the Saudi Arabia telecom towers market size in 2025, while renewable-only towers are progressing at a robust 16.41% CAGR to 2031.

- By tower design, monopoles captured 49.12% of the Saudi Arabia telecom towers market share in 2025; stealth and concealed structures represent the fastest-growing design at an 8.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G spectrum releases and densification wave | +1.2% | Riyadh, Jeddah, Eastern Province | Medium term (2-4 years) |

| Vision 2030 infrastructure spending push | +0.9% | National, giga-project zones | Long term (≥ 4 years) |

| Tower‐asset monetization & PIF consolidation | +0.8% | National | Short term (≤ 2 years) |

| Mobile data usage surge (video, cloud, IoT) | +0.7% | Urban centers, suburban rings | Medium term (2-4 years) |

| Neutral-host DAS demand in giga-projects | +0.4% | NEOM, Red Sea, Qiddiya, New Murabba | Long term (≥ 4 years) |

| Railway & utility tower licensing | +0.3% | Northern and eastern rail corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Spectrum Releases and Densification Wave

Equal 3.4-3.8 GHz assignments to all three mobile operators removed spectrum-holding advantages and redirected competition toward network-quality metrics, triggering an aggressive build program that may lift site densities three to five times above LTE norms. Nokia’s standalone (SA) mmWave field trial with TAWAL validated 5 Gbps peak throughput but underscored the need for dense rooftop and street-level assets because mmWave signals decay quickly. [1]Nokia, “TAWAL and Nokia Complete World-First 5G SA mmWave Trial,” nokia.comSaudi malls, which record -95.5 dBm indoor signal strength versus -87.4 dBm in UAE centers, illustrate the immediate colocation opportunity for distributed-antenna systems. The Communications, Space and Technology Commission (CST) has also licensed non-terrestrial network services to SKYFive Arabia, foreshadowing hybrid satellite backhaul that could ease rural macro demand without suppressing urban densification.

Vision 2030 Infrastructure Spending Push

Government-backed giga-projects link construction permits to digital-connectivity milestones, pushing tower rollout into early project phases. The Ministry of Communications and Information Technology has earmarked edge-computing zones inside new economic clusters, prompting operators to add low-latency microwave and fiber backhaul at existing tower pads. [2]Ministry of Communications and Information Technology, “National Technology Development Program Overview,” mcit.gov.saNEOM’s USD 5 billion deal with DataVolt for a 1.5 GW net-zero AI data-center campus demands redundant, ultra-dense small-cell grids to support 1.5 Tbps cross-campus traffic by 2028. Railway expansion adds another 5,500 km of fiber-ready rights-of-way, and newly issued carrier-service-provider licenses allow utilities to monetize dark fiber and lattice structures, opening rural corridors for fast-track deployments.

Tower-Asset Monetization and PIF-Led Consolidation

PIF purchased 51% stakes in both TAWAL and Golden Lattice Investment Company, merging them into a 30,000-site national champion valued near USD 5.85 billion. The new entity starts with a 1.05x tenancy ratio, which management plans to lift toward the 1.7x regional benchmark through multi-operator sharing and neutral-host indoor solutions. Capital unlocked via the merger has already financed an EUR 1.22 billion acquisition in Eastern Europe, highlighting outbound ambitions and signaling that Saudi tower know-how will scale regionally. Mobily’s 11,000-site portfolio remains a final monetization target; once transferred, the Saudi Arabia telecom towers market is likely to transition fully to third-party ownership, fostering uniform service-level agreements and predictive-maintenance programs.

Mobile Data Usage Surge (Video, Cloud, IoT)

Peak traffic loads surged after pandemic-era behavioral shifts embedded video streaming and remote work into daily routines. Zain KSA’s enterprise cloud-connect revenue grew 36% in 2024, compelling upgrades at colocated towers to add 8T8R massive-MIMO radios and 25G backhaul links. NEOM alone projects 200 million IoT end-points by 2030, demanding tower-mounted edge nodes capable of sub-10 ms round-trip latency. Edge mini-data-centers housed at tower bases shorten data paths for autonomous-vehicle fleets in the Red Sea giga-project, reinforcing the economic case for site densification and fiberization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Municipal site-permitting delays and visual rules | -0.6% | Urban centers, heritage districts | Short term (≤ 2 years) |

| Rising energy and diesel OPEX for off-grid sites | -0.4% | Desert regions, remote corridors | Medium term (2-4 years) |

| Construction-cost inflation | -0.3% | Giga-project zones | Short term (≤ 2 years) |

| mmWave capex risk | -0.2% | Dense commercial districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Municipal Site-Permitting Delays and Visual-Impact Objections

Municipalities wield broad discretion over tower approvals, and heritage precincts require visual-impact statements that can prolong projects by up to 12 months. Riyadh has tightened setback distances near residential compounds, compelling operators to swap lattice towers for costlier stealth poles that blend into street furniture.[3]Ministry of Municipal and Rural Affairs, “Urban Planning Guidelines for Telecom Infrastructure,” momrah.gov.sa Building‐compliance certificates can be revoked if passive-infra violates zoning height ratios, pushing tower companies to prefabricated camouflaged designs that satisfy both 5G coverage and municipal aesthetics. The result is an 8.95% CAGR uptick in concealed structures, albeit at a 15-20% capex premium.

Rising Energy and Diesel-Backup OPEX for Off-Grid Sites

Diesel haulage over desert tracks inflates site OPEX by up to 90% relative to grid-fed urban peers. Logistics complexity, plus a 5-7% annual rise in construction material costs, squeezes margins on rural builds. Hybrid solar-battery retrofits, however, cut runtime fuel consumption by 65%, and TAWAL’s IoT energy-monitoring pilot on 2,000 towers has already achieved a 13% electricity reduction. Red Sea Global’s 1.3 GWh lithium microgrid—powering the world’s first zero-carbon 5G network—confirms technical viability but requires high upfront capex that only large TowerCos can currently absorb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Consolidated Independent TowerCos Accelerate Scale Efficiency

Independent TowerCos commanded 59.02% of the Saudi Arabia telecom towers market share in 2025 and are tracking a 6.28% CAGR through 2031. The Saudi Arabia telecom towers market size attributable to these entities is thus poised to widen as operators exit real-estate management and redirect cash toward spectrum and active-layer upgrades. The PIF-backed TAWAL-Golden Lattice merger spawned a 30,000-site powerhouse valued near USD 5.85 billion, improving purchasing leverage and enabling country-wide predictive-maintenance rollouts.

Operator-captive portfolios are shrinking; Mobily’s review of its 11,000 sites signals another imminent transfer to the independent ecosystem. Joint-venture models such as the Zain-Ooredoo-TASC vehicle are emerging regionally, illustrating that cross-border asset platforms can extract procurement synergies and share best-practice energy retrofits. As tenancy ratios climb toward international benchmarks, revenue per tower rises faster than tower count, reinforcing the sector’s annuity-style cash flows.

By Installation: Rooftops Gain Momentum Amid Urban Densifications

Ground-based structures still hold 58.74% of the Saudi Arabia telecom towers market size, yet rooftops are pacing ahead at a 5.87% CAGR to satisfy 5G indoor coverage mandates. In Riyadh’s new financial district, municipal height limits and scarce land parcels tilt economics toward lightweight rooftop monopoles anchored to steel-reinforced elevator shafts.

Rooftop colocation cuts permitting cycles by 30% because no separate land lease is required, and small-cell clusters can share in-building fiber risers. NEOM’s design blueprint includes 1,800 telecom “street boxes” across 60 nodes, each integrating rooftop radios with smart-city sensors, demonstrating how giga-projects redefine installation typologies. For TowerCos, balanced portfolios hedge regulatory risks: ground sites ensure macro coverage while rooftops deliver high-margin tenancy gains in dense zones.

By Fuel Type: Renewable-Powered Sites Deliver Rapid OPEX Relief

Hybrid grid-diesel systems dominate at 78.35%, but renewable towers are advancing at a blistering 16.41% CAGR to 2031. Saudi Arabia telecom towers market size for green-energy configurations is therefore accelerating from a modest base as solar-battery LCOE drops below USD 0.11 per kWh. STC’s AI-driven retrofit program lowered remote-site energy draw by 13% within 12 months and cut preventive-maintenance runs by 18% thanks to sensor-based alerts.

The Red Sea project’s zero-carbon network sets a new benchmark: its 1.3 GWh lithium microgrid eliminated 18 million liters of diesel annually and slashed CO₂ by 70 kilotons. Challenges remain—dust accumulation drops panel efficiency by 4-6%, and lithium storage adds capex—but favorable net-present-value calculations and ESG scoring benefits motivate TowerCos to lock in long-term OPEX savings while meeting corporate decarbonization pledges.

By Tower Type: Stealth Designs Capture Aesthetic-Driven Growth

Monopoles lead with 49.12% of the Saudi Arabia telecom towers market share owing to low fabrication and maintenance costs. However, municipalities increasingly favor stealth cladding that hides antennas in fiberglass flagpoles or minaret-styled spires. Demand for such designs is growing at 8.61% CAGR because they accelerate permitting in heritage hubs like Jeddah’s Al-Balad district.

Lattice towers retain importance for heavy multi-operator loads and high wind-load tolerances along the Red Sea coast, whereas guyed masts remain niche in mountainous Asir. Smart-tower retrofits, incorporating IoT sensors into all form factors, now enable real-time structural health monitoring and remote camera surveillance, minimizing unplanned climbs and improving technician safety. Consequently, tower design selection increasingly balances structural economics with urban aesthetics and sensor integration readiness.

Geography Analysis

Riyadh, Jeddah, and Dammam represent the primary demand nodes, each accounting for more than 15% of existing sites and hosting the bulk of 3.5 GHz 5G traffic. These commercial corridors combine high average revenue per user with dense enterprise clusters that require edge compute zones adjacent to towers, pushing colocation ratios closer to 1.4x. Ensuring continuity of the Saudi Arabia telecom towers market size here depends on quick municipal clearances and multi-operator active-sharing pacts.

Giga-project corridors along the Red Sea and Gulf Coast create fresh green-field requirements. NEOM’s sprawling construction zone will require over 10,000 new tower touchpoints by 2030, many designed as neutral-host street poles equipped with micro-edge nodes. Red Sea Global’s resort archipelago demonstrates effective renewable and salt-spray-resistant tower engineering, piquing interest from TowerCos active in similarly harsh environments.

Sparse interior provinces such as Al-Qassim and the Northern Borders rely on single macro sites for 50-km zones, making back-up power the critical cost driver. CST’s recent utility-carrier licenses let Saudi Arabia Railways and Water Transmission and Technologies Company commercialize existing pylons and fiber trenches, enabling lower-cost buildouts than standalone macropoles. In mountainous Asir, guyed masts positioned on ridges deliver line-of-sight microwave backhaul to coastal towns, highlighting terrain-driven design diversity across the Saudi Arabia telecom towers market.

Competitive Landscape

The sector’s concentration is moderate. The TAWAL-Golden Lattice entity governs roughly 30,000 sites—about 58% of national inventory—while Zain-Ooredoo-TASC’s cross-GCC platform and IHS Towers’ strategic watch point inject contestable pressure. Competition pivots on tenancy growth, energy efficiency, and rapid-deployment stealth formats rather than brute tower numbers.

Nokia’s mmWave spectrum-sharing pilot showcased a software-defined neutral-host layer capable of hosting three operators over shared antennas, lowering incremental capex by 27% per tenant. ZTE’s 2025 partnership with TAWAL extends collaboration into digital energy, leverages lithium-iron-phosphate chemistries, and integrates AI-driven power controllers that trim diesel runtime by 72 hours per month.

Utilities entering the market via carrier-service-provider licenses offer fresh site options along pipelines and power-transmission routes, posing both partnership and substitution threats to incumbent TowerCos. In response, incumbents are bundling edge-compute cabinets with colocation leases, creating stickier client relationships and opening ancillary revenue streams.

Saudi Arabia Telecom Towers Industry Leaders

Golden Lattice Investment Co. (GLIC)

TAWAL

Mobily Tower Assets

Etihad Salam Telecom Company

IHS Towers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ZTE and TAWAL forged a strategic cooperation agreement spanning telecom infrastructure and digital-energy solutions, including lithium-battery retrofits for 1,000 off-grid sites.

- February 2025: NEOM and DataVolt agreed to co-develop a USD 5 billion net-zero AI data-center campus that will depend on ultra-dense neutral-host tower grids.

- February 2025: CST issued four new telecom licenses, channeling roughly SAR 1 billion into fresh tower and fiber assets along rail and utility corridors.

- January 2025: STC unveiled a USD 9 billion network expansion emphasizing 5G tower densification and fiber backhaul upgrades.

Saudi Arabia Telecom Towers Market Report Scope

Telecom towers are pivotal in wireless transmission, serving as the backbone for antennas and communication equipment. By supporting mobile networks, these towers cover extensive areas, guaranteeing uninterrupted signal broadcasting and reception between mobile devices and the network. Telecom towers come in various sizes, including lattice towers, monopoles, and guyed towers, each customized to address specific network and location requirements.

The Saudi Arabia telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive sites), by installation (rooftop and ground-based), and by fuel type (renewable and non-renewable). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How big is the Saudi Arabia telecom towers market in 2026?

It is valued at USD 828.09 million and is forecast to reach USD 1023.28 million by 2031 at a 4.32% CAGR.

Why are independent TowerCos gaining share in Saudi Arabia?

Operators are monetizing passive assets to free capital for 5G spectrum and radio upgrades, allowing TowerCos to capture 59.02% share in 2025.

What role does Vision 2030 play in tower demand?

Vision 2030 giga-projects require ultra-dense, low-latency coverage, driving new site builds and rooftop small-cell deployments.

How fast are renewable-powered towers growing?

Renewable-only sites are expanding at a 16.41% CAGR as TowerCos cut diesel OPEX and align with national sustainability targets.

Which tower design leads the market?

Monopoles hold 49.12% share, but stealth designs are the fastest-growing segment because they comply with stricter urban aesthetic rules.

What is the main operational challenge for off-grid sites?

Rising diesel and logistics costs inflate OPEX, pushing TowerCos toward solar-battery hybrids that reduce fuel use by up to 65%.

Page last updated on: