United Kingdom Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

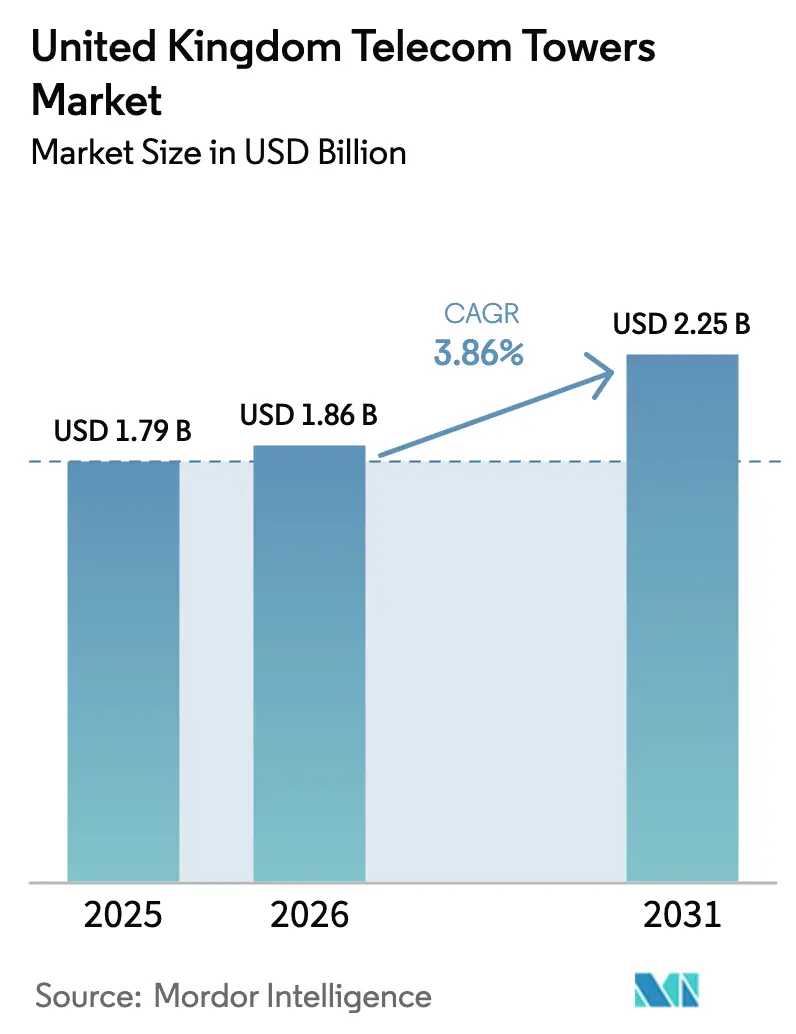

| Base Year Market Size (2025) | USD 1.79 Billion |

| Market Size (2026) | USD 1.86 Billion |

| Market Size (2031) | USD 2.25 Billion |

| Growth Rate (2026 - 2031) | 3.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Telecom Towers Market Analysis by Mordor Intelligence

The United Kingdom Telecom Towers Market size was valued at USD 1.79 billion in 2025 and estimated to grow from USD 1.86 billion in 2026 to reach USD 2.25 billion by 2031, at a CAGR of 3.86% during the forecast period (2026-2031).

This measured trajectory reflects a mature infrastructure base that still requires densification to meet aggressive 5G obligations, sustain enterprise private-network demand, and monetize assets through sale-leasebacks. Independent TowerCos continue to acquire operator portfolios, squeezing more tenants onto each site and thereby improving cash-flow resilience. Urban rooftop deployments outpace greenfield builds because they face fewer planning hurdles, while renewable-powered sites gain traction as operators hedge volatile energy prices and progress toward net-zero targets. Consolidation and neutral-host models, including smart-street-furniture micro-sites, further strengthen the medium-term growth outlook for the United Kingdom telecom tower market.

Key Report Takeaways

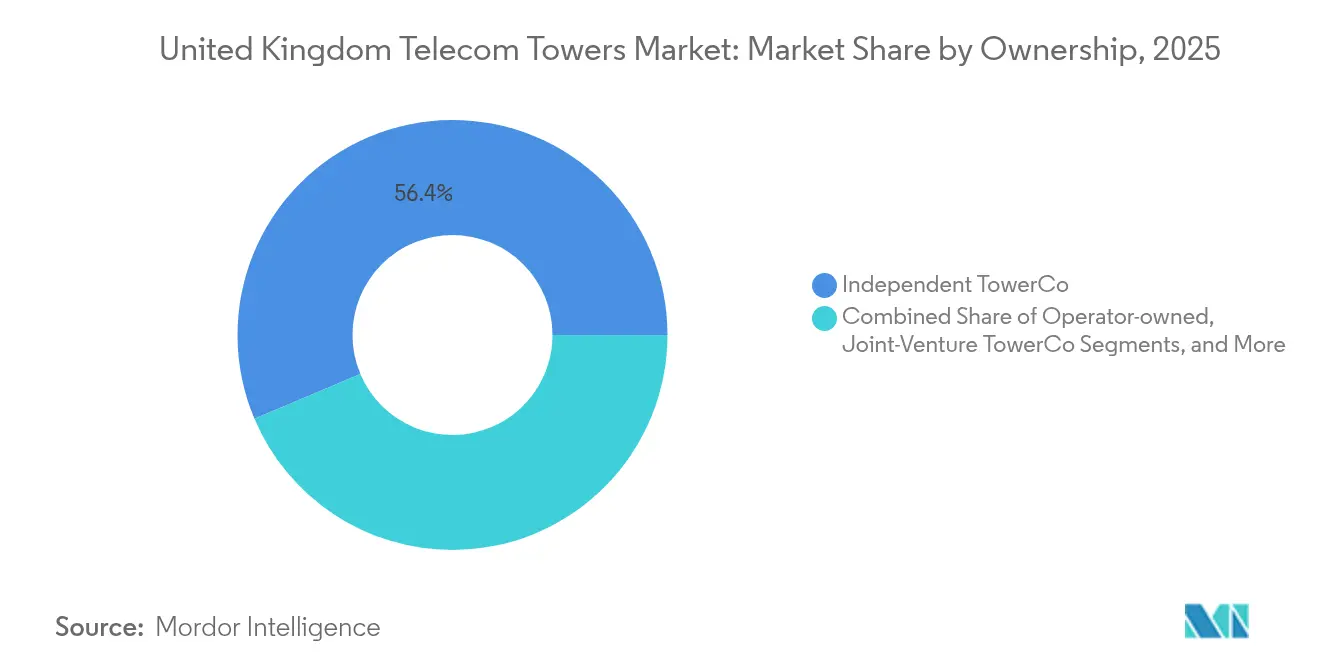

- By ownership, independent tower companies held 56.36% of the United Kingdom telecom tower market share in 2025 and are expanding at a 6.22% CAGR to 2031.

- By installation, rooftop sites accounted for 52.02% of the United Kingdom telecom tower market size in 2025 and are tracking a 4.62% CAGR through 2031.

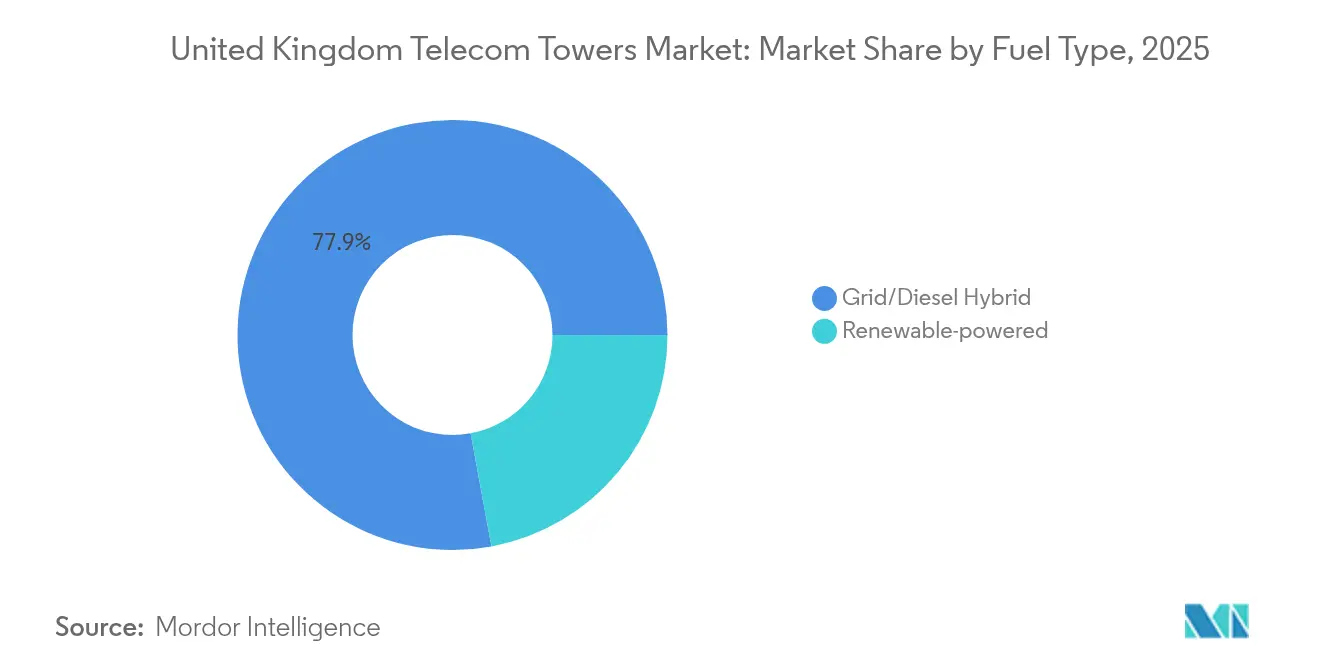

- By fuel type, renewable-powered towers represented 22.10% of the United Kingdom telecom tower market size in 2025 and are growing at an 11.21% CAGR to 2031.

- By tower type, monopole tower type represented 41.95% of the United Kingdom telecom tower market size in 2025, and stealth and concealed structures are advancing at a 5.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory 5G coverage and densification obligations | +1.2% | National, concentrated in urban centers and SRN target areas | Medium term (2-4 years) |

| Shared Rural Network (SRN) public-private funding | +0.8% | Rural Scotland, Wales, Northern Ireland, Southwest England | Medium term (2-4 years) |

| MNO tower-portfolio monetization and sale-leasebacks | +0.9% | National, with focus on high-value urban assets | Short term (≤ 2 years) |

| Urban neutral-host small-cell demand surge | +0.7% | London, Manchester, Birmingham, Edinburgh city centers | Short term (≤ 2 years) |

| Enterprise private-5G network rollout momentum | +0.4% | Industrial corridors, manufacturing hubs, logistics centers | Long term (≥ 4 years) |

| Smart-street-furniture conversions for micro-sites | +0.3% | Dense urban areas with aesthetic planning requirements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory 5G Coverage and Densification Obligations

The government’s 95% geographic coverage milestone for 2025 continues to generate steady site additions nationwide [1]Ofcom, “Electronic Communications Code Grants,” OFCOM, ofcom.org.uk. Ofcom’s refined Electronic Communications Code now trims average site-acquisition timelines from 18 months to 12 months, enabling faster rollout cycles for Independent TowerCos that rely on multi-tenant economics. Operators facing stiff penalties for missing coverage targets have prioritized leasing new locations over extending existing footprints, which lifts recurring rental income for tower owners. The policy framework, therefore, anchors predictable demand, sustains predictable cash flows, and underpins disciplined capital-expenditure forecasts across the United Kingdom telecom tower market.

Shared Rural Network Public-Private Funding

The USD 1.33 billion Shared Rural Network (SRN) scheme pools government and operator funding to deliver service to 280,000 rural premises across four nations [2]Department for Science, Innovation and Technology, “Shared Rural Network Programme to Boost Mobile Coverage Across the UK,” GOV.UK, gov.uk. Neutral-host design lets several operators share the same asset, improving economic viability for remote builds. Early field reports show a 15% shorter planning-approval cycle than for purely commercial projects, because predefined community-engagement protocols accelerate local consent. That faster cadence enlarges the rural addressable base for the United Kingdom telecom tower market and diversifies revenue streams away from saturated metro corridors.

MNO Tower-Portfolio Monetization and Sale-Leasebacks

Operator balance sheets have benefited from multi-billion-dollar disposals, such as Virgin Media O2’s USD 236 million Cornerstone stake sale to Equitix [3]Gill Plimmer, “Cornerstone Telecommunications Infrastructure Stake Sale,” Financial Times, ft.com. Sale-leasebacks typically value UK tower assets at 15-18× annual rent, unlocking capital for core-network upgrades while shifting operational risk to Independent TowerCos. Those TowerCos, in turn, drive 20-25% higher efficiency through multi-tenant occupancy, reinforcing the virtuous cycle of consolidation, tenancy growth, and margin expansion within the United Kingdom telecom tower market.

Urban Neutral-Host Small-Cell Demand Surge

Mobile operators now rely on dense grids of shared small cells to satisfy surging 5G traffic in city centers. EE alone deployed more than 1,000 nodes across London and major regional hubs during 2024, cutting street-level congestion and boosting capacity. Neutral-host integrators such as Freshwave reduce deployment costs by around 40% compared with single-tenant models, while also defusing local objections to duplicated infrastructure. This momentum sustains a healthy project pipeline that supplements macro-tower growth, particularly for stealth and concealed formats that blend into historic streetscapes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent planning and zoning approvals in dense areas | -0.6% | London, heritage sites, conservation areas nationwide | Medium term (2-4 years) |

| Escalating site-energy costs and power-price volatility | -0.4% | National, with higher impact on remote rural sites | Short term (≤ 2 years) |

| 5G-SA core delays limiting multi-tenancy uptake | -0.3% | National, affecting neutral-host deployment models | Medium term (2-4 years) |

| Steel-supply disruptions amid UK decarbonization shift | -0.2% | National, concentrated in new tower construction | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Planning and Zoning Approvals in Dense Areas

Local councils rigorously police the visual impact of new telecommunications structures, especially near heritage landmarks. Planning approval rates average 65% for ground-based sites in dense boroughs, compared with 85% for rooftop alternatives. To secure consent, operators are turning to stealth enclosures that mimic lamp posts or chimneys, but these bespoke designs cost 25–30% more and extend build schedules by up to six months. The additional complexity softens near-term expansion across some hot-spot postcodes, muting a portion of overall growth in the United Kingdom telecom tower market.

Escalating Site-Energy Costs and Power-Price Volatility

Wholesale electricity prices spiked 15-20% above 2023 highs during the 2024 winter peak, inflating operating expenses for energy-intensive rural sites. Power now accounts for up to 30% of operating outlays at off-grid locations, compared with 20% at grid-fed urban roofs. TowerCos are responding with solar-battery hybrids and micro-wind turbines that cut cost volatility by roughly 40%. Although these systems demand 20-25% more upfront capital, the life-cycle savings justify continued investment and bolster the environmental credentials of the United Kingdom telecom tower market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Drive Market Consolidation

Independent TowerCos controlled 56.36% of 2025 revenue and are projected to expand at a 6.22% CAGR. Rising operator appetite for asset-light models fuels a steady pipeline of sale-leaseback deals that enlarge TowerCo portfolios and lift tenancy ratios. Independent owners can spread maintenance costs across multiple clients, thereby enhancing margins and reinvesting in digital monitors that automate fault detection. As a result, investors continue to value mature portfolios at double-digit EBITDA multiples, underscoring sustained confidence in recurring cash flows.

The regulatory tilt toward open infrastructure further cements TowerCo's primacy. Ofcom’s code revision standardizes site-rental negotiations and streamlines dispute resolution, reducing legal overhead for independent landlords while preserving fair-access rules for tenants. The United Kingdom telecom tower market, therefore, revolves increasingly around a handful of scale players able to integrate renewable energy, deploy predictive maintenance, and negotiate planning offsets. Operator-captive estates remain relevant for ultra-dense urban clusters, yet their share is sliding as carriers monetize non-core assets to fund 5G Stand-Alone upgrades.

By Installation: Rooftop Deployments Capitalize on Urban Densification

Rooftops represented 52.02% of sector revenue in 2025 and are marching ahead at a 4.62% CAGR through 2031, mirroring persistent high-density data demand in cities. Building-top sites offer 30-40% faster delivery because owners can combine communications upgrades with façade refurbishments, pleasing both tenants and municipal planners. The higher approval rate grants operators confidence to pre-commit long leases, securing predictable occupancy for landlords. Those advantages keep rooftops pivotal to the United Kingdom telecom tower market size, even as greenfield construction becomes scarcer in built-out metros.

Emerging in-building antenna systems amplify the rooftop thesis by extending indoor 5G coverage without adding mast clutter at street level. Furthermore, many councils now bundle digital-connectivity targets into urban-renewal grants, which can subsidize rooftop conversions on municipal properties. Such financial sweeteners accelerate project payback periods and stimulate additional tenancy layers, driving compound revenue growth for TowerCos with technical expertise in complex roof layouts.

By Fuel Type: Renewable Energy Integration Accelerates

Renewable-powered towers already represent 22.10% of revenue and are sprinting forward at an 11.21% CAGR, making them the most dynamic slice of the United Kingdom telecom tower market. Operators view self-generation as a hedge against price spikes and a lever for meeting corporate climate goals. Modern lithium-ion batteries now store enough energy to ride through multi-day outages, improving uptime for critical transport corridors and remote islands. Integration of IoT sensors allows real-time energy-yield analytics, letting asset managers dispatch technicians only when predictive models flag anomalies.

Policy also tilts in favor of renewables. The UK Net-Zero Act mandates steep decarbonization across telecoms by 2050, and early movers benefit from potential carbon-credit revenues. Solar hybrid deployments in rural Scotland by EdgePoint Towers demonstrate 25-30% annual opex savings and 10-year paybacks, findings that resonate with infrastructure-fund investors seeking ESG-aligned assets. As battery prices fall and micro-wind turbines mature, renewable penetration is poised to widen further, reinforcing the long-run competitiveness of the United Kingdom telecom tower market.

By Tower Type: Stealth Solutions Address Aesthetic Concerns

Monopole structures held 41.95% revenue in 2025, yet stealth and concealed formats, though smaller, are advancing at a brisk 5.05% CAGR. Boroughs keen to preserve skyline aesthetics increasingly condition approval on disguised poles that resemble lamp posts or flagpoles. Clients accept premium rents in exchange for faster sign-offs and reduced community pushback, which ultimately lowers the total cost of delay. The trend dovetails with the rise of smart street furniture, where 5G radios share space with public Wi-Fi, CCTV, and environmental sensors.

Lattice and guyed masts remain vital for long-span rural coverage and broadcast payloads, but growth is tepid as incremental capacity shifts toward denser, lower-profile sites. Advances in composite materials now let manufacturers embed antennas inside fiberglass skins without compromising RF performance, broadening stealth-design options. Accordingly, the United Kingdom telecom tower market continues to bifurcate between high-capacity rural lattices and visually discreet urban nodes, each governed by distinct economic and regulatory rationales.

Geography Analysis

England captured roughly 74.65% of 2025 revenue, reflecting its population density and early 5G adoption, as the network footprint edges toward saturation. London and the South-East command the highest site valuations thanks to multi-tenant stacking and complex planning that constrains fresh supply. Average monthly rent in Zone 1 London stands 40-50% above national norms, supporting robust cash-flow margins for asset owners.

Scotland, Wales, and Northern Ireland collectively contribute 25.35% of 2025 revenue yet enjoy stronger 4.66% CAGR prospects to 2031, buoyed by SRN co-funding that closes long-standing coverage gaps. Early SRN trials in the Highlands shaved 15% off standard acquisition timelines, proving that aligned stakeholder incentives can accelerate rural rollouts. Remote islands are also attractive for renewable hybrids because diesel logistics are costly, a variable that pushes TowerCos toward solar and micro-wind arrays for energy independence.

The Midlands and Northern England benefit from an industrial renaissance anchored in private 5G networks across automotive and advanced-manufacturing clusters. TowerCos taps incremental tenancy demand from factory owners who require deterministic wireless links for robotics, adding utilization layers to existing macro-sites. Cross-border synergies with the Republic of Ireland further diversify revenue for TowerCos that manage assets in both jurisdictions, enabling transnational neutral-host contracts with multinational carriers.

Competitive Landscape

The United Kingdom telecom tower market shows moderate concentration as Independent TowerCos, including Cornerstone and Freshwave, roll up fragmented portfolios and integrate small-cell assets. Equitix’s Cornerstone stake purchase and EQT’s USD 4.25 billion acquisition of Crown Castle’s small-cell arm underscore investor appetite for scale efficiencies and robust free-cash yields. Multi-tenant strategies allow leading players to attain EBITDA margins north of 60%, reinforcing competitive barriers against new entrants that lack diversified tenancy rosters.

Strategic emphasis now centers on renewable power retrofits, AI-driven monitoring, and city-center stealth deployments that command premium rents. TowerCos are digitizing asset registries, feeding drone-scanned imagery into predictive-maintenance software that cuts unscheduled downtime and curbs insurance losses. Partnerships with local authorities to convert lamp posts into micro-sites unlock air-rights at lower cost, giving incumbents an early-mover advantage in the nascent smart-furniture sub-segment.

Emergent challengers specialize in enterprise-campus networks and public-venue DAS, but they often collaborate with macro owners for backhaul and core-tower rights. Consequently, the competitive dynamic is less about volume share and more about complementary niches that broaden the service stack. Overall, sustained consolidation and technology differentiation underpin stable, long-term cash flows across the United Kingdom telecom tower market.

United Kingdom Telecom Towers Industry Leaders

Cornerstone

Mobile Broadband Network Ltd (MBNL)

Cellnex UK

Wireless Infrastructure Group (WIG)

Arqiva Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: EQT completed acquisition of Crown Castle's small cells business for USD 4.25 billion, creating the largest neutral-host small-cell platform globally with significant U.K. operations and expansion plans across dense urban markets.

- October 2024: Virgin Media O2 completed sale of 8.33% economic interest in Cornerstone to Equitix for USD 236 million, demonstrating continued appetite for U.K. tower infrastructure investments among institutional investors.

- August 2024: EE completed deployment of 1,000+ small cells across London and major cities, expanding urban capacity while demonstrating neutral-host deployment models for dense-area coverage requirements.

- March 2024: Boldyn Networks completed the acquisition of Cellnex's private networks business, strengthening enterprise 5G deployment capabilities across the UK industrial markets.

United Kingdom Telecom Towers Market Report Scope

Telecommunication towers encompass a variety of structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and other similar forms. These towers, equipped with one or more telecommunication antennas, facilitate radio communications. They can be situated on the ground or atop a building's rooftop and often include storage for equipment and electronic components.

The UK telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive sites), installation (rooftop and ground-based), and fuel type (renewable and non-renewable). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How large is the United Kingdom telecom tower market in 2026?

The market is valued at USD 1.86 billion in 2026 and is projected to reach USD 2.25 billion by 2031.

Which ownership model is expanding the fastest?

Independent TowerCos are growing at a 6.22% CAGR, well ahead of other ownership categories.

Why are renewable-powered towers gaining share?

They stabilize energy costs and support operator net-zero targets, leading to an 11.21% CAGR in their segment.

What impact does the Shared Rural Network have on growth?

The SRN injects USD 1.33 billion into rural builds, shortening planning cycles and lifting nationwide coverage.

How are planning restrictions influencing tower design?

Strict urban zoning rules drive demand for stealth and concealed structures that achieve faster approvals despite higher build costs.

What is the outlook for rooftop installations?

Rooftops dominate urban expansions with a 52.02% share and grow at a 4.62% CAGR due to easier planning and faster deployment.

Page last updated on: