Africa Telecom Towers And Allied Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

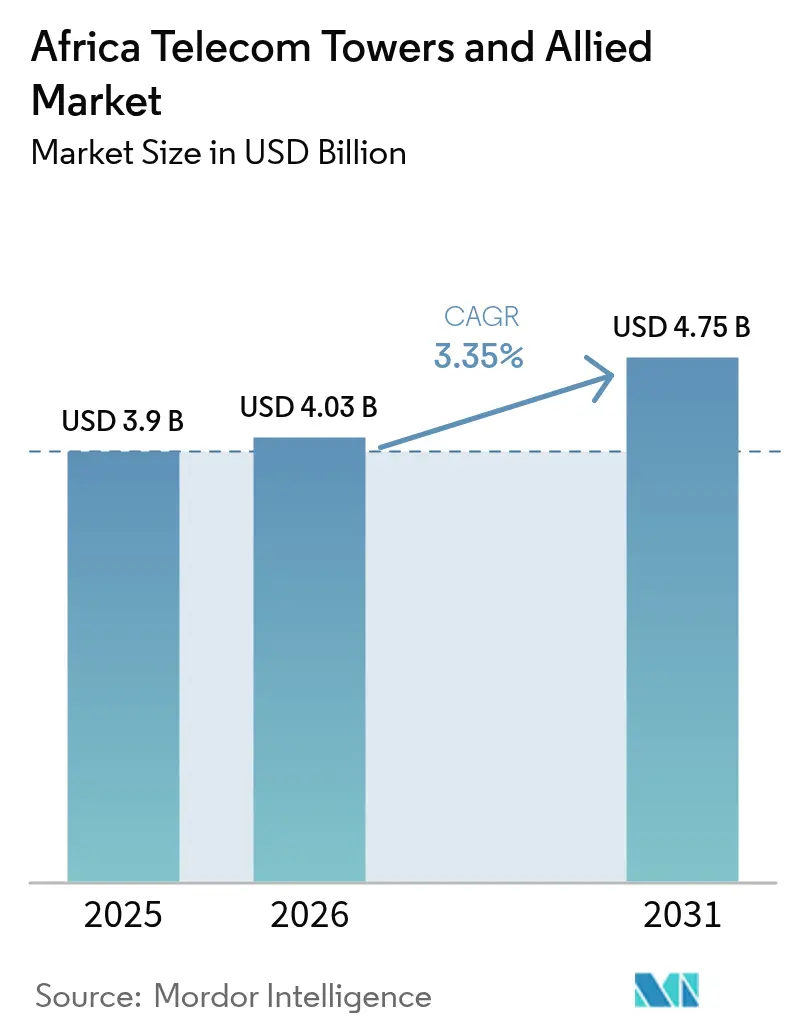

| Base Year Market Size (2025) | USD 3.9 Billion |

| Market Size (2026) | USD 4.03 Billion |

| Market Size (2031) | USD 4.75 Billion |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

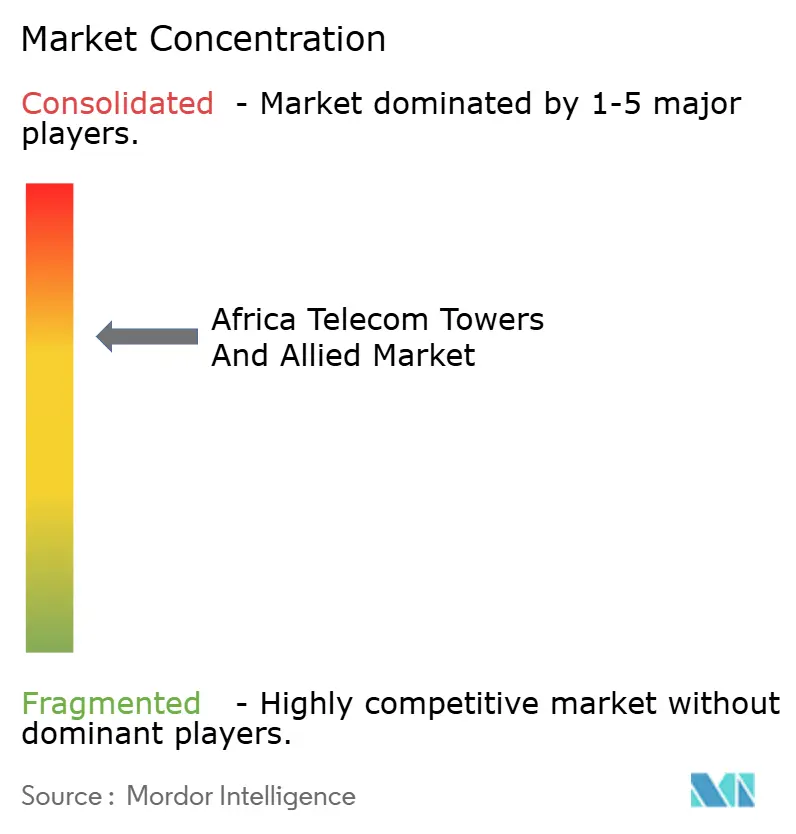

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Telecom Towers And Allied Market Analysis by Mordor Intelligence

The Africa Telecom Towers And Allied Market size in 2026 is estimated at USD 4.03 billion, growing from 2025 value of USD 3.9 billion with 2031 projections showing USD 4.75 billion, growing at 3.35% CAGR over 2026-2031.

Accelerated 4G and newly launched 5G rollouts, rising data consumption, and government-backed rural coverage mandates underpin this steady expansion. Independent TowerCos continue to win large multi-year outsourcing contracts from pan-African mobile network operators, a trend that lifts tenancy ratios and improves operating cash flows. Renewable-powered systems are gaining momentum as green financing incentives offset the volatility of diesel fuel costs. Meanwhile, country-specific programs, such as Algeria’s fiber-to-the-home build-out and Kenya’s digital-economy blueprint, add geographic depth to overall demand for ground-based and rooftop sites across the Africa telecom tower market.

Key Report Takeaways

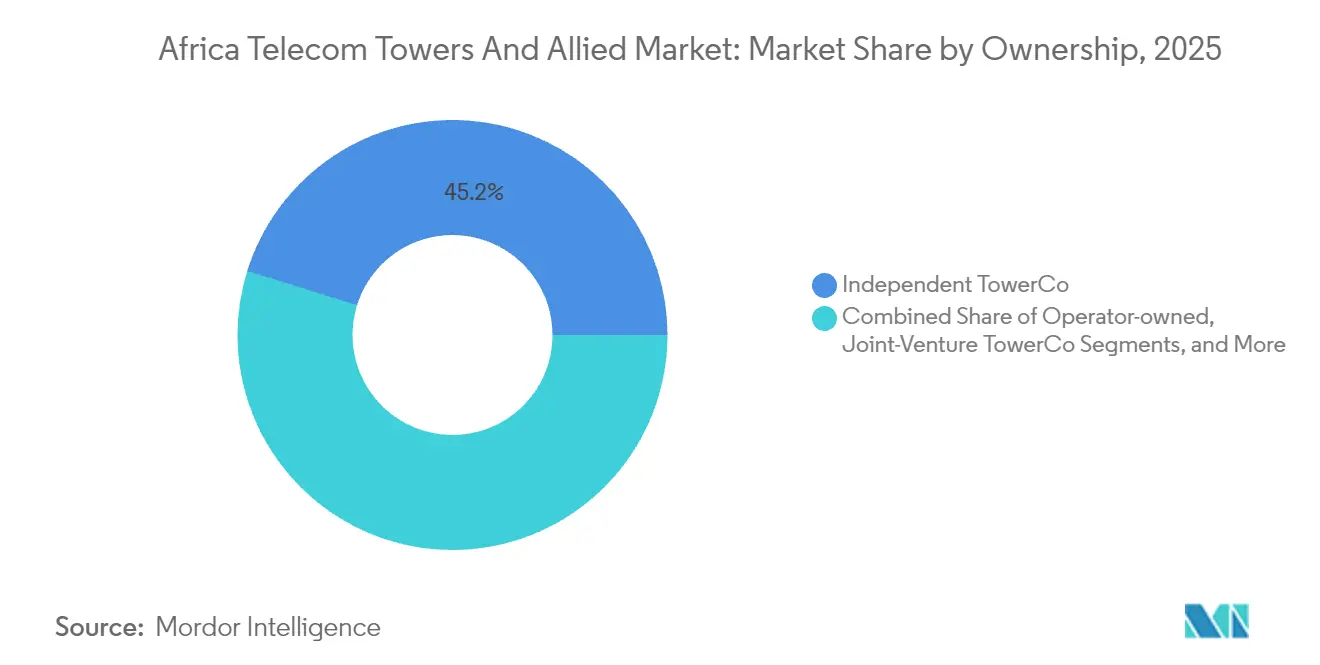

- By ownership, independent TowerCos held 45.18% of the Africa telecom tower market share in 2025 and are advancing at a 6.53% CAGR through 2031.

- By installation, ground-based towers accounted for 76.20% of the Africa telecom tower market size in 2025, while rooftop sites represent the fastest-growing segment with a 7.34% CAGR to 2031.

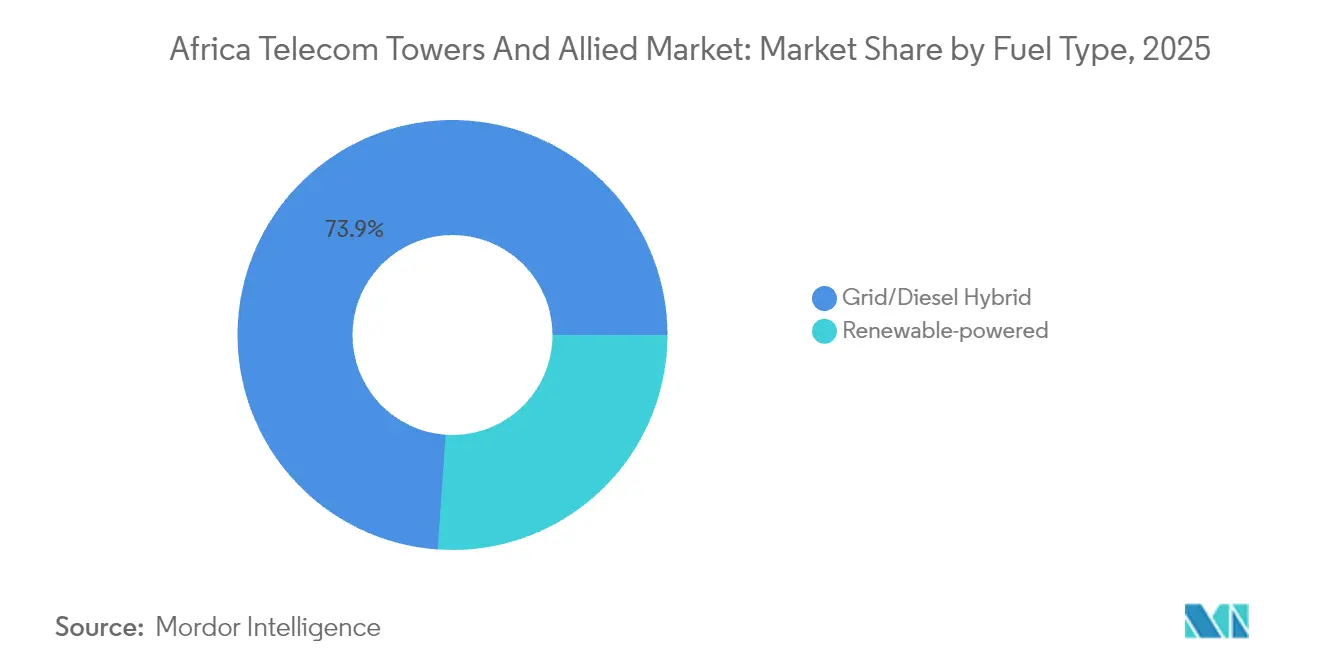

- By fuel type, grid/diesel hybrid systems dominated with 73.90% of the Africa telecom tower market share in 2025; renewable-powered sites are expanding at 11.68% CAGR to 2031.

- By tower type, monopole structures captured 36.40% share of the Africa telecom tower market size in 2025, whereas stealth and concealed designs exhibit the highest 9.46% CAGR to 2031.

- By country, Algeria led with 49.30% Africa telecom tower market share in 2025; Kenya shows the strongest 5.03% growth trajectory through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Telecom Towers And Allied Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 4G/5G rollout by pan-African MNOs | +1.2% | Global, with concentration in Nigeria, South Africa, Kenya | Medium term (2-4 years) |

| Rising data consumption and smartphone penetration | +0.9% | Global, with highest impact in North and West Africa | Long term (≥ 4 years) |

| Government-led rural coverage mandates and universal service funds | +0.7% | Sub-Saharan Africa, particularly Kenya, Tanzania, Ghana | Medium term (2-4 years) |

| Asset-light network strategies by MNOs boosting tower outsourcing | +1.1% | Global, with early adoption in Nigeria, Morocco, Algeria | Short term (≤ 2 years) |

| Green financing incentives for renewable power retrofits | +0.4% | Global, with focus on off-grid sites across rural Africa | Long term (≥ 4 years) |

| Expansion of neutral-host indoor DAS and small-cell backhaul demand | +0.3% | Urban centers in Algeria, Nigeria, South Africa, Morocco | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated 4G/5G rollout by pan-African MNOs

Pan-African mobile network operators added hundreds of 5G sites in 2024 and early 2025, lifting total 5G subscriptions in Sub-Saharan Africa toward Ericsson’s 420 million projection for 2030 [1]Ericsson, “Mobility Report June 2025,” ericsson.com. MTN Group alone expanded its 5G footprint to more than 3,000 sites, prompting a surge in colocation requests across the Africa telecom tower market [2]MTN Group, “Integrated Report 2024,” mtn.com. The densification imperative is especially acute in Lagos, Nairobi, and Johannesburg, where 5G mid-band spectrum requires closer site spacing. Independent TowerCos capitalize on this urgency by offering turnkey build-to-suit programs that shorten time-to-market for operators migrating from legacy 4G networks. The momentum is reinforced by the recent commercial 5G launch in Tunisia, underscoring the broad regional commitment to next-generation connectivity [3]Tunisia Telecom, “5G Commercial Launch,” tunisietelecom.tn.

Rising data consumption and smartphone penetration

Video streaming, social media, and mobile payments are elevating per-subscriber data use into double-digit gigabyte ranges across North and West Africa. Young demographics and low-cost smartphone imports sustain this demand curve, compelling operators to add capacity faster than originally budgeted. Higher data volumes translate into larger leaseable antenna counts per site, pushing tenancy ratios across the Africa telecom tower market from 1.5x toward 2x in core metros. TowerCos are therefore incentivized to future-proof structures with stronger load capacities and fiber-ready backhaul, ensuring revenue upside as data-heavy services proliferate.

Government-led rural coverage mandates and universal service funds

Kenya, Tanzania, and Ghana channel universal service funds into new tower builds in hard-to-reach areas, guaranteeing baseline tenancy and 10-year lease commitments for TowerCos. Nigeria’s approval for 7,000 additional towers highlights the scope of public-sector intervention aimed at closing the digital divide. Because these mandates often stipulate minimum coverage ratios and performance KPIs, TowerCos secure predictable cash flows that de-risk greenfield investments. Rural subsidies also accelerate the adoption of solar-hybrid power systems, a shift that further differentiates the Africa telecom tower market from more mature regions.

Asset-light network strategies by MNOs boosting tower outsourcing

IHS Towers’ decade-long renewal with MTN Nigeria covering roughly 13,500 tenancies showcases the stickiness of the sale-leaseback model. Operator balance sheets benefit from an immediate capital infusion, while TowerCos unlock recurring revenue through multi-tenant leasing. Joint-venture structures, such as the new Maroc Telecom-inwi vehicle targeting 2,000 towers, illustrate how competitors can share passive infrastructure yet preserve brand-level differentiation in active radio assets. This outsourcing momentum is expected to boost the Africa telecom tower market well into the next decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile foreign-exchange and high sovereign risk | -0.8% | Global, with highest impact in Nigeria, Ghana, Egypt | Short term (≤ 2 years) |

| Lengthy permitting and land-acquisition bottlenecks | -0.6% | Global, with severe constraints in Algeria, Morocco, South Africa | Medium term (2-4 years) |

| Diesel supply disruptions raising opex at off-grid sites | -0.4% | Rural areas across Sub-Saharan Africa | Short term (≤ 2 years) |

| Fiber backhaul deficits limiting tenancy ratios in secondary cities | -0.5% | Secondary cities across West and East Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile foreign-exchange and high sovereign risk

Revenue is largely denominated in local currencies, but debt and capex remain USD-linked, exposing TowerCos to material conversion losses during currency depreciations. IHS Towers reported notable FX headwinds in several African markets during 2024, underscoring sensitivity to macroeconomic cycles. Sovereign credit downgrades trigger higher interest rates that can render new builds unviable or slow refinancing efforts. Operators and TowerCos are increasingly exploring natural hedges such as USD-indexed lease escalators, but uptake remains limited by regulatory caps on foreign-currency billing.

Lengthy permitting and land-acquisition bottlenecks

Environmental clearances, zoning approvals, and community consultations can extend site rollout timelines from 3 months to more than 18 months, especially in dense urban cores. The African Development Bank notes that these procedural delays inflate project costs and reduce investor returns across the continent. As 5G pushes coverage deeper into city centers, administrative complexity becomes an even bigger drag on the Africa telecom tower market growth. Streamlined one-stop permitting windows are emerging in Morocco and South Africa, but have yet to reach scale across the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Multi-tenant scale widens Independent TowerCo lead

Independent TowerCos commanded 45.18% of the Africa telecom tower market share in 2025 and are on track for a 6.53% CAGR through 2031. The superior returns stem from 92.4% utilization rates and diversified country portfolios that smooth FX and regulatory risk. Operator-owned assets persist in markets with infrastructure-sharing constraints, but monetization pressure is rising as balance-sheet light strategies take hold. The Africa telecom tower market size for Independent TowerCos could exceed USD 2.07 billion in annual lease revenue by 2031 if current divestiture pipelines close on schedule.

MNO captive sites remain critical in politically sensitive geographies where network control is paramount; however, cash-strapped operators increasingly favor sale-leasebacks to fund 5G spectrum fees. Joint-venture TowerCos offer a middle path, letting rivals co-invest in passive plant without sacrificing active-layer differentiation. American Tower’s selective entry strategy validates the margin advantage enjoyed by global specialists in complex metros, a dynamic likely to accelerate consolidation across the Africa telecom tower industry.

By Installation: Rooftops race ahead inside land-constrained metros

Ground-based towers held 76.20% of the Africa telecom tower market size in 2025, proving cost-effective for suburban and rural macro coverage. Rooftop installations, though smaller in absolute footprint, are gaining a 7.34% CAGR as 5G mid-band frequencies demand tighter grid spacing in densely populated business districts. Municipal aesthetic guidelines and mounting land prices make rooftops the only viable option in central Nairobi, Casablanca, and Johannesburg.

Ground-based towers still deliver higher absolute revenue per site thanks to greater antenna load capacity and ease of renewable-power retrofits. Yet rooftops promise faster permitting and reduced civil works expenditure, allowing TowerCos to capture incremental revenue within established coverage zones. This nuanced mix of site types ensures the Africa telecom tower market remains flexible as data-traffic patterns evolve.

By Fuel Type: Solar-hybrid economics eclipse diesel volatility

Grid/diesel hybrids controlled 73.90% of the Africa telecom tower market share in 2025, but renewable-powered systems are expanding at a 11.68% CAGR, buoyed by falling photovoltaic costs and green-bond financing. GreenWish Partners earmarked USD 800 million for solar-powered towers, spotlighting the commercial viability of renewables in off-grid areas. The Africa telecom tower market size tied to renewable-powered sites could top USD 694 million by 2031 if current retrofit targets are met.

Diesel logistics account for up to 40% of opex at remote sites, a figure that renewable systems can cut in half once battery storage is amortized. IHS Towers’ Project Green saved USD 49 million annually, strengthening the business case for aggressive renewable adoption. Solar-hybrid systems also improve uptime, a key KPI in service-level agreements with MNOs.

By Tower Type: Stealth designs satisfy urban regulators

Monopoles captured 36.40% of the Africa telecom tower market share in 2025, favored for their balance between cost efficiency and structural strength. The Africa telecom tower market size, attributable to stealth or concealed designs, while small today, is climbing at a 9.46% CAGR as municipalities impose visual-impact caps on new towers. Lattice and guyed structures remain indispensable for heavy-load rural sites, but their share is declining because urban densification now drives incremental demand.

Stealth installs cost up to 25% more than standard monopoles, yet TowerCos often recoup the premium via higher rents from multiple tenants eager to secure downtown coverage. New composite materials and integrated antenna shrouds are cutting installation times, thus mitigating the added capex burden.

Geography Analysis

North Africa benefits from clear policy frameworks that prioritize telecom infrastructure as an economic enabler. Algeria’s leadership with 49.30% market share is anchored in state-backed fiber programs that lower backhaul costs and elevate tower economics. Morocco’s strategy to reach 5.6 million fiber households by 2030 and Tunisia’s national 5G launch in 2025 further underscore the region’s forward-leaning stance.

West Africa exhibits scale-driven dynamics, with Nigeria’s 7,000-tower expansion underscoring the sheer volume required to serve the continent’s largest population. Ghana’s regulatory stability attracts regional TowerCos, whereas Côte d’Ivoire leverages infrastructure-sharing rules to accelerate rural coverage. Currency volatility and inconsistent grid power remain common hurdles across the sub-region.

East Africa combines innovation with rapid adoption. Kenya’s 5.03% CAGR stands out amid regional peers, propelled by mobile money ecosystems that demand low-latency coverage. Tanzania’s universal-service incentives guarantee tenancy for new rural sites, while Uganda and Rwanda represent sizeable white-space potential once financing hurdles ease.

Regulatory Landscape

Regulation across key African markets is converging around enforceable infrastructure sharing and faster deployment rules, which directly affects tower colocation, leaseability, and permitting timelines. In Rwanda, the Rwanda Utilities Regulatory Authority (RURA) issued Regulation No. 20/R/ICT/RURA/2026 on 27 January 2026, mandating telecommunication infrastructure sharing and setting a six-month compliance window for existing non-compliant assets. This raises the pressure to regularize legacy sites and formalize co-location terms.

In Kenya, the Communications Authority of Kenya released the Revised Telecommunications Market Structure in February 2026, introducing a technology-neutral licensing approach (including NFP-T3) that allows entities to develop towers for leasing to third parties. This broadens the pool of potential infrastructure providers beyond traditional MNOs and major TowerCos. Uganda Communications Commission published a February 2026 framework for optical fiber installation, maintenance, protection, and disposal to curb duplication and standardize build practices that influence tower backhaul readiness. In parallel, South Africa issued a policy direction on 12 March 2026 under the Electronic Communications Act to review Facilities Leasing Regulations and advance a framework for Rapid Deployment Regulations, keeping facilities leasing and deployment compliance central to expansion planning.

Value Chain Analysis

The value chain covers site origination (radio planning inputs from MNOs, local agents, and landlords), design and build (civil works, steel structures, power systems, and security), operations (energy management, preventive maintenance, and field services), and commercialization (lease contracting, colocation onboarding, and SLA reporting). Independent TowerCos sit at the center as integrators, coordinating EPC contractors, equipment OEMs, fuel and power vendors (diesel logistics, batteries, and solar), and backhaul providers. Their operations increasingly rely on digital tools for energy optimization and uptime management, with NEC Africa and PowerX announcing an AI-driven energy management partnership in July 2026 for telecom tower infrastructure across Africa.

Financing and procurement have also become decisive links, with more blended and locally anchored funding supporting both acquisitions and expansion. A March 2026 financing close involved Paradigm Tower Ventures and a consortium of Rwandan banks (Project Zorro) to support the acquisition and rebranding of IHS Rwanda to Ishara Towers Rwanda Ltd. In July 2026, Standard Bank and Helios Towers partnered on a USD 29 million Social Documentary Credit Facility to support infrastructure procurement and working capital. On the demand side, MNO outsourcing and long-term tenancy commitments remain the main revenue engine, while large capex programs in markets such as DR Congo (including Helios Towers and Eastcastle commitments reported in June 2026) highlight how logistics, importation capacity, and local contractor ecosystems influence rollout speed and cost.

Competitive Landscape

Three international TowerCos, IHS Towers, American Tower, and Helios Towers, collectively control a significant share of tenable sites across the Africa telecom tower market. IHS Towers leads with 39,229 global towers, achieving 92.4% utilization that outperforms regional averages. American Tower channels more than USD 350 million into renewable upgrades across its African portfolio, using sustainability as a competitive lever. Helios Towers posts a 2.05x tenancy ratio across 14,325 sites, illustrating how operational focus can offset smaller scale.

Competition is shifting from build-volume races toward tenancy-ratio optimization and service-quality differentiation. AI-based energy management, predictive maintenance, and digital customer portals are becoming must-have capabilities. Smaller regional players may become acquisition targets as they struggle to match the financing clout and technology stack of the top three. Nevertheless, white-space in secondary cities and off-grid corridors still provides room for nimble local operators that possess superior site-acquisition networks.

Africa Telecom Towers And Allied Industry Leaders

American Tower Corporation

IHS Towers (IHS Holding Limited)

Helios Towers Plc

SBA Communications Corporation

Pan African Towers

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Active investment programs and financing structures are creating near-term whitespace for new shared sites, energy retrofits, and fiber-ready tower upgrades, especially where universal service obligations and development-finance participation reduce the risks of buildouts. In Kenya, Atlas Tower Kenya announced a USD 52.5 million investment (including USD 30 million from IFC) to build 300 new macro towers and deploy solar power, battery storage, and hybrid energy solutions. This supports a clear scale path for independent operators through green power and colocation-focused builds. In Tanzania, Helios Towers completed 133 rural sites under the Universal Communications Service Access Fund (UCSAF) programme in April 2026, reinforcing an opportunity set tied to government-backed rural coverage mechanisms that combine baseline tenancy with rollout funding.

A second opportunity cluster is emerging in resource-rich and under-served territories where operators need both coverage and capacity but want shared infrastructure to manage capex. DR Congo is illustrative, with Helios Towers outlining a USD 100 million expansion plan across provinces (with ANAPI support), and IFC advancing a proposed USD 59 million financing package for Eastcastle Infrastructure DRC to expand shared tower infrastructure, linking capital availability to neutral-host buildouts. In Nigeria, the Universal Communication Access Project (NUCAP) gained additional momentum in June 2026 when China Industrial Bank committed support for deploying at least 1,000 tower sites by end-2026, complementing the broader mandate-driven tower pipeline cited in the market context. Across these programs, renewable and hybrid power configurations, standardized infrastructure sharing, and fiber/backhaul coordination are the main execution levers for TowerCos to improve uptime, reduce diesel exposure, and raise tenancy ratios across both metro densification and rural inclusion corridors.

Recent Industry Developments

- May 2026: Helios Towers reported Q1 2026 results and raised its FY 2026 tenancy addition target to 3,000 to 3,500, adding 1,000 tenancies versus prior guidance. The update signals accelerated colocation momentum across its African footprint and reinforces the competitive focus on tenancy growth and service delivery rather than only new site builds.

- October 2025: IHS Towers completed the sale of its 100% interest in IHS Rwanda Limited (about 1,467 sites) to Paradigm Tower Ventures. The divestment reshaped ownership in Rwanda and supported portfolio rebalancing toward core African markets while enabling a local-led platform to operate and expand the acquired sites.

- August 2024: IHS Towers renewed and extended Master Lease Agreements covering about 26,000 tenancies with MTN Group across multiple African countries, including Nigeria, Rwanda, Cote d'Ivoire, Cameroon, Zambia, and South Africa. The multi-country renewal increased contract visibility and strengthened the long-duration anchor tenancy base that underpins colocation-led revenue expansion.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is sized as the revenues and activity linked to telecom tower infrastructure across Africa, covering tower leasing and related allied tower activities that support mobile and broadband network coverage expansion.

Scope exclusions: We exclude handset, core network equipment, and pure retail telecom services, and we only count tower-related value when it is tied to site infrastructure and associated tower revenue streams.

Segmentation Overview

- By Ownership

- Operator-owned

- Independent TowerCo

- Joint-Venture TowerCo

- MNO Captive

- By Installation

- Rooftop

- Ground-based

- By Fuel Type

- Renewable-powered

- Grid/Diesel Hybrid

- By Tower Type

- Monopole

- Lattice

- Guyed

- Stealth / Concealed

- By Country

- Algeria

- Kenya

- Morocco

- South Africa

- Nigeria

- Ghana

- Egypt

- Tanzania

- Rest of Africa (Tunisia, Uganda, Zambia, Senegal, and Others)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building the country-level tower footprint and the operating environment for sites, then converting that into a consistent revenue view. We refer to public sources such as ITU connectivity and mobile subscription indicators, GSMA regional mobile economy releases, World Bank macro series (inflation, FX, and GDP), national telecom regulator publications for select African countries, and IEA energy access and power reliability context where diesel and hybrid power use is common.

Next, we layer in reported tower ownership moves, leasing announcements, and coverage rollouts from operator and TowerCo filings, investor decks, and reputable press, followed by trade data checks where relevant for major tower equipment inputs. Paid subscriptions are used selectively for company financials and intelligence, patent lookups where a technology shift needs validation, and shipment-level import and export cuts in a few cases to sanity check activity in tower build cycles. These examples are not exhaustive, and many other public references and paid tools are consulted to compile data, validate assumptions, and clarify the scope for the market model.

Primary Interviews and Surveys

Primary work focuses on validating how tower leasing revenue is realized in practice, what drives tenancy and amendment demand, and how energy choices (grid, diesel, and renewables) change site economics. We speak with TowerCo and operator functions, rollout and site teams, and local experts across Africa so gaps from desk research can be closed and the final assumptions can be tested against market realities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | |

| Mid tier: 41% | Functional/Unit leaders: 43% | |

| Smaller Players: 22% | Managers: 45% |

Market-Sizing & Forecasting

We size the market using a top-down structure where the tower installed base and active tenancy signals are combined with typical lease rates, escalation patterns, and rollout intensity to reconstruct leasing and allied revenue pools for Africa. Those totals are then corroborated with selective bottom-up approximations using sampled country roll-ups of tower counts, tenancy ratios, and observed leasing price ranges, followed by adjustments where the field feedback indicates a consistent bias.

Inputs that are tracked in the model include tower counts (installed base), tenancy ratio trends, 4G and 5G rollout pace, power mix at sites (grid vs diesel hybrid vs renewable add-ons), and inflation and currency movements that affect local pricing and reported USD values. Where data is thin for smaller countries, we apply proxy assumptions based on nearby markets with similar coverage gaps and power reliability, and then cap results to realistic build and colocation capacity.

Forecasting uses scenario analysis supported by trend smoothing for stable series and regression checks for variables like mobile data growth and rollout plans, so the forecast remains explainable and repeatable. Assumptions are finalized after reconciling what is reported publicly with what practitioners confirm as feasible on timing, pricing, and tenancy additions.

Data Validation & Update Cycle

Validation is done through repeated checks across independent signals, including tower volume direction, leasing revenue movement, and country-level rollout news, and then outliers are reviewed before sign-off. We also run variance checks across countries so any unusual jumps in tower additions, lease pricing, or USD conversions are flagged and reworked.

A multi-step review is followed internally, and callbacks are triggered when primary respondents highlight a material change in tenancy, power cost, or rollout timing that could move the totals. Reports are refreshed annually, and material events such as major tower carve-outs, policy shifts, or sharp currency movements can prompt interim updates. Before delivery, a final analyst pass is done so clients receive the latest updated view.

Mordor Intelligence's Africa Telecom Towers and Allied Markets Market Size Compared With Other Published Estimates

Published market sizes for Africa telecom towers often look different because the boundary of what counts as a tower-related revenue stream is not consistent, and the timing of currency conversion also affects the reported USD number. Differences also come from how each study treats allied items, such as whether small cells and DAS are grouped in, and whether construction activity is counted the same way as recurring lease revenue.

Tower count direction, tenancy ratio checks, and country-level rollout signals are the evidence used to keep Mordor Intelligence's estimate tied to the Africa installed base and to the combined revenue streams tracked in the model (leasing revenue and construction revenue), rather than expanding into adjacent radio access or core network spending.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.03 B (2026) | |

| Industry Publisher A | USD 3.50 B (2024) | The figure is stated for an earlier base year and appears to include a broader set of allied assets such as small cells and DAS, without a clear split between recurring tower leasing revenue and other infrastructure spend, which can shift the total. |

| Trade Journal B | USD 2.07 B (2031) | This value reads like a leasing revenue potential number for a future year, rather than a full market total that also reflects construction revenue and other tower allied activity, so it is not directly comparable to a total market size. |

Across the three figures, the spread is mainly explained by year alignment and whether the number reflects total tower market value or a narrower revenue slice like leasing. By keeping inputs anchored to installed base, tenancy behavior, and pricing mechanics that can be cross-checked, the final size stays traceable and easier to update when conditions change.

Key Questions Answered in the Report

What is the current value of the Africa telecom tower market?

The sector is valued at USD 4.03 billion in 2026 and is forecast to reach USD 4.75 billion by 2031.

Which ownership model dominates the continent’s tower landscape?

Independent TowerCos lead, holding 45.18% share and growing at the fastest 6.53% CAGR through 2031.

Why are renewable-powered tower sites gaining traction?

Solar-hybrid systems cut diesel opex and tap green financing, producing a segment CAGR of 11.68%.

Which country shows the highest growth momentum?

Kenya posts a 5.03% CAGR, driven by Safaricom’s network upgrades and a supportive digital-economy plan.

How are foreign-exchange risks managed by tower operators?

Leading TowerCos use partial USD-indexed lease escalators and natural hedges, though FX volatility still trims forecast CAGR by 0.8%.

What strategic moves stand out among market leaders?

IHS Towers’ 13,500‐tenancy renewal with MTN Nigeria and American Tower’s USD 350 million renewable program underscore a pivot toward long-term contracts and sustainability.

Page last updated on: