United Arab Emirates Freight Brokerage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

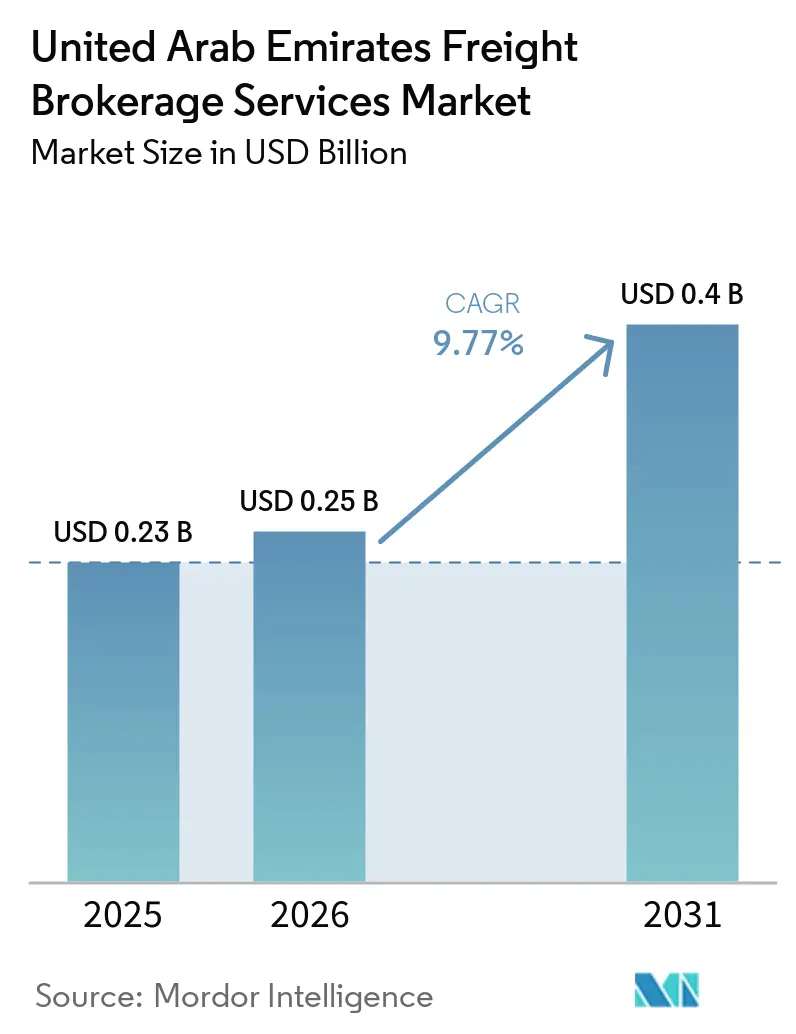

| Base Year Market Size (2025) | USD 0.23 Billion |

| Market Size (2026) | USD 0.25 Billion |

| Market Size (2031) | USD 0.4 Billion |

| Growth Rate (2026 - 2031) | 9.77% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Freight Brokerage Services Market Analysis by Mordor Intelligence

The UAE freight brokerage services market size was valued at USD 0.23 billion in 2025 and is estimated to grow from USD 0.25 billion in 2026 to reach USD 0.40 billion by 2031, at a CAGR of 9.77% during the forecast period (2026-2031). Robust rail infrastructure, bonded e-fulfillment expansion, and temperature-controlled re-exports are reshaping competitive positioning. Freight intermediaries are adopting railroad intermodal routing to bypass congested highways, while heavy-lift opportunities tied to ADNOC megaprojects elevate demand for specialist brokerage. Digital platforms, backed by venture capital, are displacing traditional, relationship-based booking through price transparency and real-time visibility. Persistently high empty-backhaul ratios on UAE-to-Saudi lanes and escalating cybersecurity compliance outlays temper margin gains, prompting brokers to double down on data-driven network optimization.[1]Etihad Rail Freight Network Launches Full Operations,” United Arab Emirates Ministry of Energy and Infrastructure, moei.gov.ae

Key Report Takeaways

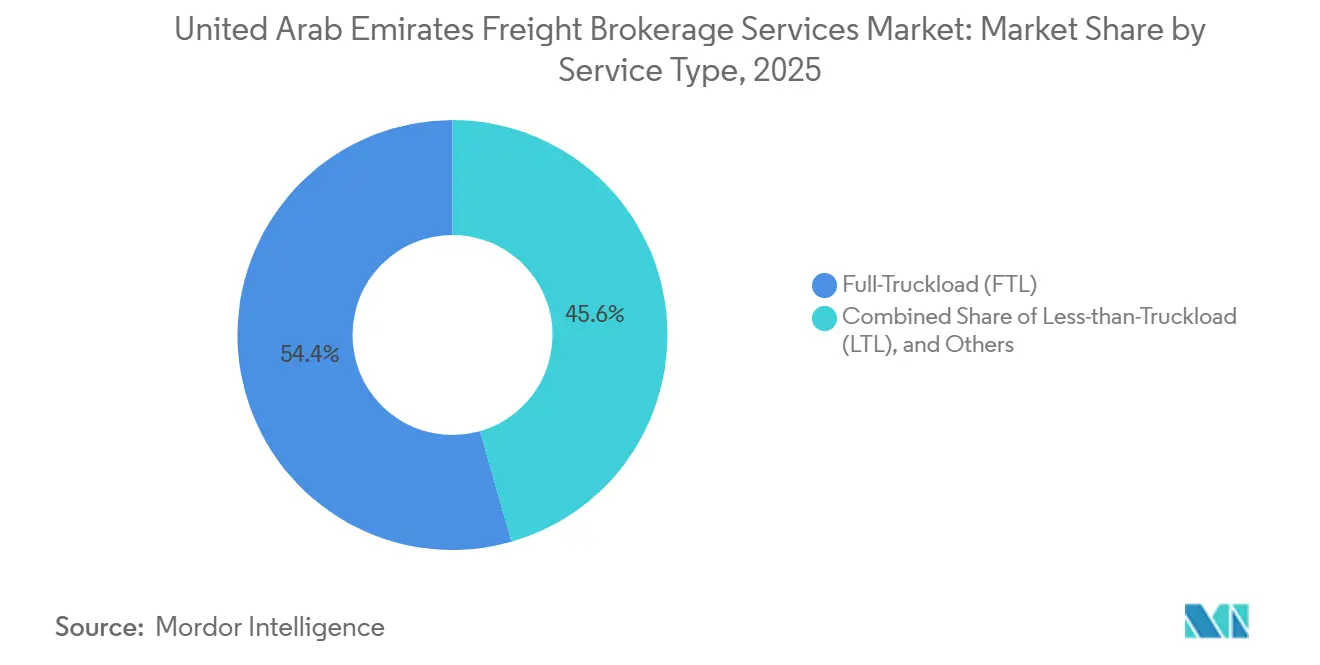

- By service, Full-Truckload led with 54.43% of the UAE freight brokerage services market share in 2025, while Less-than-Truckload is projected to advance at an 11.88% CAGR through 2031.

- By equipment type, Dry Van transport accounted for 48.58% share of the UAE freight brokerage services market size in 2025, and Refrigerated Van is growing fastest at a 12.15% CAGR.

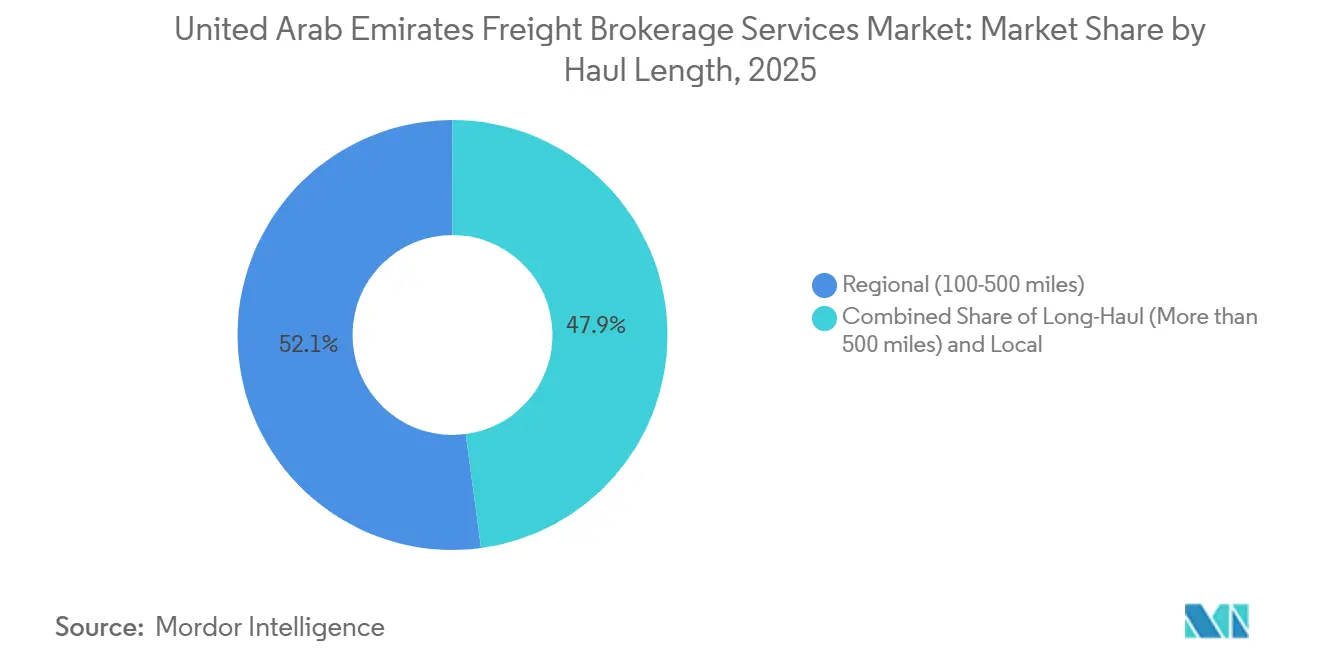

- By haul length, regional routes held 52.11% of 2025 revenue, whereas Local services are forecast to record a 13.14% CAGR over 2026-2031.

- By business model, Traditional brokerage retained 38.09% share in 2025, yet Digital platforms are expanding at an 18.71% CAGR to 2031.

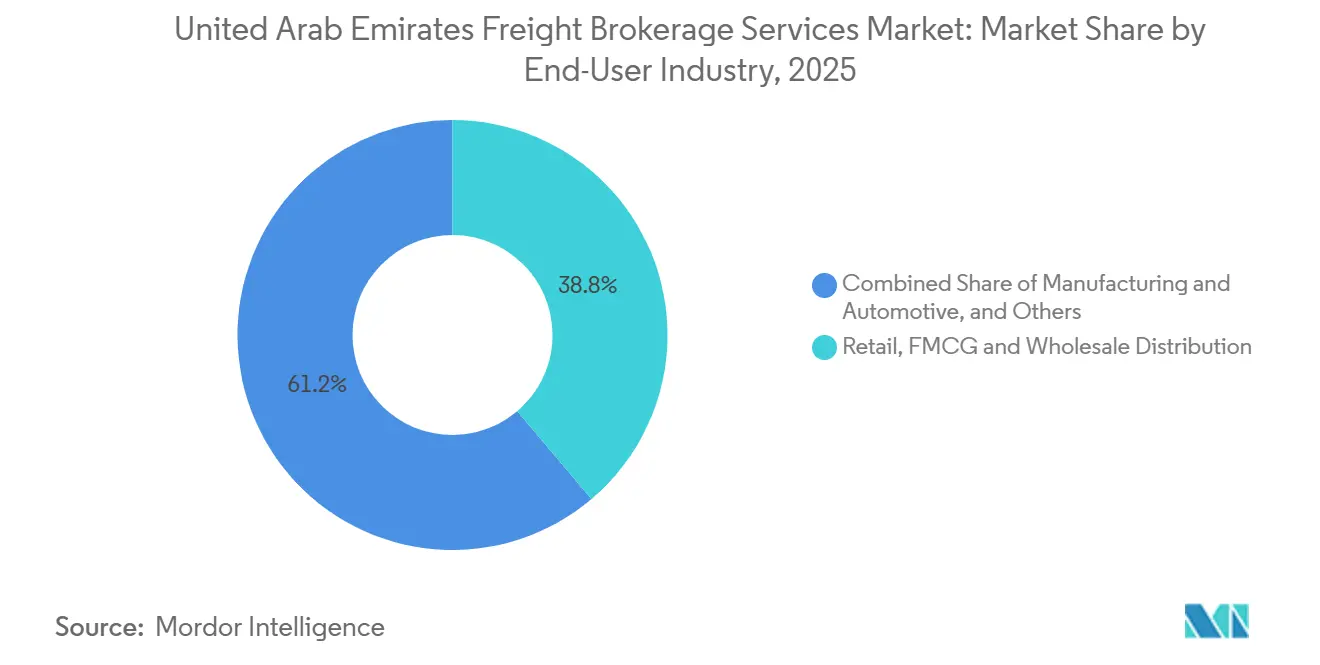

- By end-user industry, Retail, FMCG & Wholesale Distribution captured 38.80% of 2025 demand, while E-commerce & 3PL Fulfillment is set to climb at a 19.61% CAGR.

- By customer size, Large Enterprise Shippers represented 41.92% of spending in 2025, but Small Businesses are projected to grow at a 14.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates Freight Brokerage Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GCC Rail Link-Up and Etihad Rail Freight Launch | +2.4% | UAE nationwide, Saudi Arabia, and Oman borders | Long term (≥ 4 years) |

| Surge in Temperature-Controlled Perishables Re-exports | +2.1% | Dubai and Abu Dhabi cold-chain hubs | Medium term (2-4 years) |

| Expansion of Bonded E-Fulfilment Centres | +1.9% | Dubai CommerCity and free zones | Short term (≤ 2 years) |

| ADNOC Mega-Projects Driving Heavy-Lift & Project Logistics | +1.6% | Abu Dhabi offshore & industrial zones | Medium term (2-4 years) |

| Autonomous Truck Pilot Corridors Boosting Overland Efficiency | +0.9% | Dubai-Abu Dhabi highways | Long term (≥ 4 years) |

| VC-Fueled Logistics Tech Start-ups Creating Digital Capacity Liquidity | +0.8% | UAE nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

GCC Rail Link-Up and Etihad Rail Freight Launch

Spanning 900 km, the Etihad Rail network has been fully operational for freight since 2023, with passenger services scheduled to debut in 2026. This infrastructure establishes a high-capacity land bridge that is set to transform UAE logistics through significant modal shifts, while also promising to reduce passenger commute times by 30% to 40% compared to road travel. DHL’s dedicated rail service illustrates how predictable schedules and bulk capacity strengthen broker value propositions. Direct access to Fujairah Port diversifies routing options for landlocked Saudi industries during peak seaport congestion. The planned UAE-Saudi rail connection by 2030 will turn medium-haul corridors into viable rivals against short-sea shipping. Brokers investing early in railroad intermodal systems are expected to widen margins as freight volumes surpass 20 million tons annually.

Surge in Temperature-Controlled Perishables Re-exports

Dubai’s cold storage capacity, which already surpassed 1.2 million m³ by 2023, continues to scale through 2026 as the UAE cold-chain market reaches a USD 1.83 billion valuation, underpinned by pharmaceuticals and high-value perishables bound for Africa and South Asia. Refrigerated moves earn baseline premiums of 30-40%, with specialized biologics corridors commanding up to 50%, incentivizing brokers to partner with GDP-certified (Good Distribution Practice) fleets. Localization of biologics manufacturing in the UAE now supports oncology drugs and biologics requiring –80 °C logistics, broadening revenue pools. Specialized compliance keeps market entry barriers high, insulating niche brokers from rate commoditization. Operators without temperature-controlled networks risk being confined to low-margin ambient lanes.

Expansion of Bonded E-Fulfilment Centres (“One-Inventory” Model)

Dubai CommerCity enables merchants to defer duties until a final GCC sale, trimming working capital needs by up to 50%. Freight brokers orchestrate cross-border distribution, customs clearance, and last-mile scheduling from a single hub. Small e-commerce sellers gain scale benefits formerly reserved for large retailers, widening the pool of available shippers. Brokers inside bonded zones secure privileged volume flows and generate add-on revenue through kitting and returns handling. With bonded capacity set to reach 2.1 million ft² by 2027, demand for integrated brokerage is expected to accelerate.[2]Federal Decree-Law No. 45 of 2021 on the Protection of Personal Data,” United Arab Emirates Ministry of Industry and Advanced Technology, moe.gov.ae

ADNOC Mega-Projects Driving Heavy-Lift & Project Logistics

ADNOC’s USD 170 billion capital plan through 2027 fuels episodic but lucrative heavy-lift requirements. The Hail and Ghasha offshore project alone needs oversized modules surpassing road weight limits, triggering complex route surveys and permit regimes lasting up to 12 months. Brokers with marine coordination and modular transport partners secure high-ticket contracts while asset-heavy fleets struggle with utilization gaps between projects. Upcoming Lower Zakum upgrades extend visibility to 2030, justifying investment in specialized competencies. However, 90-120-day payment cycles strain brokers lacking robust balance sheets.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cyber-Security & Data-Sovereignty Compliance Costs | –1.4% | UAE nationwide | Short term (≤ 2 years) |

| Chronic Empty-Backhaul Imbalance on UAE-GCC Road Lanes | –1.1% | UAE-Saudi & UAE-Omani corridors | Medium term (2-4 years) |

| Emiratization Quotas Straining Specialist Talent Supply | –0.8% | Dubai & Abu Dhabi | Medium term (2-4 years) |

| Limited Rail Last-Mile Links to Industrial Zones | –0.6% | Northern emirates’ inland sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cyber-Security and Data-Sovereignty Compliance Costs

Local data-hosting mandates force brokers onto UAE-based clouds that are 25-35% pricier than global hyperscalers. Annual penetration tests, encryption upgrades, and consent-management tooling inflate fixed costs, pinching smaller intermediaries. Digital platforms bear additional scrutiny because multi-shipper data aggregation raises competitive-intelligence concerns. Parallel compliance across divergent GCC regimes fragments system architecture and magnifies maintenance overhead. As costs escalate, sub-scale brokers face consolidation or exit.

Chronic Empty-Backhaul Imbalance on UAE-GCC Road Lanes

Imports flowing inward to GCC neighbors generate 35-40% deadhead runs on the return leg, slashing effective broker margins by as much as 30%. Manual dispatchers lack the density to fill empty equipment, whereas digital load-matchers mitigate imbalances through dynamic pricing. Seasonal peaks tighten outbound capacity but leave inbound lanes under-utilized, exaggerating volatility. Industrial diversification in Saudi Arabia and Oman may realign flows post-2030, yet near-term pain persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: LTL Consolidation Captures E-commerce Growth

The Less-than-Truckload (LTL) and Other services segment accounted for 45.57% of UAE freight brokerage revenue in 2025, trailing the 54.43% dominance of Full-Truckload but rising as e-commerce fragmentation intensifies and shipment frequency increases. LTL’s 11.88% CAGR reflects the surge of bonded e-fulfillment models, where merchants dispatch multi-parcel orders to diverse GCC addresses daily. Digital algorithms now cluster orders by delivery window, shaving transit costs by 15-25% compared to manual routing.

Full-Truckload still underpins construction, oil, and industrial cargo where volume justifies dedicated assets, yet its margin compresses as rate-comparison portals sharpen buyer power. Hybrid brokers that offer both modes leverage real-time data to recommend optimal service on a load-by-load basis, thereby increasing retention. Consolidation tech also unlocks the small-shipper segment, broadening the UAE freight brokerage services market and diversifying revenue away from cyclical bulk sectors.

By Equipment Type: Refrigerated Vans Outpace Dry Fleets

Dry Vans retained 48.58% of 2025 turnover, anchoring general merchandise flows, but Refrigerated Vans are projected to log a 12.15% CAGR, the segment’s fastest trajectory. Pharma re-exports, supported by GDP-certified hubs, require sustained –20 °C conditions that command 30-40% rate premiums. Brokers outsource chilled capacity to specialist fleets, converting fixed asset costs into variable fees while up-selling compliance auditing.

Flatbeds and Step-decks gain from ADNOC construction modules, although demand is episodic. Emerging green mandates spurred GEODIS to debut biofuel rigs in 2025, hinting at sustainability as a differentiator. Asset-light brokers increasingly rely on tech-enabled capacity pooling to guarantee availability during seasonal peaks in perishables and vaccine drives, stabilizing yield in an otherwise rate-sensitive arena.

By Haul Length: Local Deliveries Lead Growth Curve

Regional legs (100-500 miles) generated 52.11% of 2025 revenue thanks to GCC cross-border flows, yet Local hauls under 100 miles are forecast to expand at 13.14% CAGR on the back of last-mile complexity. Dubai’s new road-restriction zones heighten route-planning sophistication, rewarding brokers with automated scheduling. Urban densification in Abu Dhabi fuels demand for micro-fulfillment shuttles, compressing delivery windows to sub-12 hours.

Etihad Rail offers new land-bridge options for mid-range lanes, enticing shippers to shift loads from all-road truck convoys to rail-truck combinations. Long-haul routes still link ports with northern Saudi sites, but the drag of empty backhaul keeps growth modest. Brokers that harmonize local drop-density algorithms with regional consolidation can optimize fleet rotation and reduce idle time, thereby directly boosting profitability.

By Business Model: Digital Platforms Gain Momentum

Traditional brokerage commanded a 38.09% slice of 2025 transactions, yet Digital platforms are accelerating at an 18.71% CAGR to 2031, propelled by venture-backed scale effects. Real-time rate discovery, automated documentation, and live tracking drive adoption among small shippers. Locad’s USD 9 million pre-Series B and OTO’s USD 8 million Series A illustrate external capital confidence in asset-light scalability.

Asset-based brokers still win on guaranteed capacity during peak demand, but capital intensity curbs agility. Hybrid models emerge as incumbents integrate technology while retaining relationship-based account management. Agent networks extend geographical reach without payroll expansion yet require strict brand governance. Ultimately, platforms that blend digital self-service with consultative support will shape the next competitive baseline of the UAE freight brokerage services market.

By End-User Industry: E-commerce & 3PL Fulfillment Sets Pace

Retail, FMCG & Wholesale Distribution held a 38.80% share in 2025, but E-commerce & 3PL Fulfillment is growing at a 19.61% CAGR, driven by direct-to-consumer brands bypassing legacy wholesalers. Dubai CommerCity’s bonded blueprint enables single-inventory coverage for all GCC markets, slashing duty liabilities and spurring parcel volumes. Brokers tailor pick-and-pack, labeling, and return-logistics bundles to lock in sticky contracts.

Industrial stalwarts such as Manufacturing, Automotive, Oil & Gas need specialized handling and compliance, preserving premium niches even as growth moderates. Healthcare & Pharmaceuticals extend cold-chain relevance, while Agriculture & Food ride re-export demand. Each vertical’s distinct service expectations force brokers to segment operations, with tech dashboards mapping commodity-specific capacity forecasts.[3]Dubai E-commerce Strategy: Accelerating the Digital Economy,” Dubai Economy and Tourism (DET), economy.ae

By Customer Size: SMEs Accelerate on Digital Access

Large Enterprises provided 41.92% of spending in 2025 through multi-year contracts, yet Small Businesses with revenue under USD 10 million are slated for 14.84% CAGR growth as self-service portals democratize freight booking. AI-enabled credit scoring on platforms like those partnered with SME10X unlocks working-capital lines to cover freight invoices, further widening the accessible customer base.

Mid-market firms balance bespoke service and digital ease, forming a stable core that anchors revenue visibility. Brokers segment account strategies accordingly: key account teams for large shippers, automated workflows for micro-merchants, and hybrid dashboards for mid-sizes. The diversification cushions cyclicality and expands the addressable pool for the UAE freight brokerage services industry.

Geography Analysis

Jebel Ali Port’s 14 million TEU throughput and Dubai International Airport’s express connectivity cement Dubai as the country’s logistics epicenter. Etihad Rail’s network, fully operational for freight since 2023, creates a land bridge from Fujairah to the Saudi border, with passenger services slated to launch across the network in 2026. Abu Dhabi’s ADNOC-led industrialization injects heavy-lift volumes, while Sharjah’s manufacturing clusters and Fujairah’s Indian Ocean-facing terminal diversify shipment patterns, granting brokers flexibility in routing.

Following the implementation of CEPAs with India (2022), Indonesia (2023), and Turkey (2023), the UAE is now seeing record trade flows, with additional agreements with nations like Japan and the EU expected to further slash barriers by late 2026, channeling incremental flows through UAE gateways. Yet 35-40% of empty backhauls on UAE-to-Saudi lanes persist, reinforcing the importance of digital load matching to sustain margins. Free-zone governance offers brokers 100% foreign ownership and tax holidays, intensifying competition but also fostering service innovation.

Autonomous-truck pilot corridors between Dubai and Abu Dhabi show potential cost savings of 20-30% once regulations mature, positioning the UAE as a first-adopter market. Meanwhile, bonded e-commerce zones in Dubai CommerCity are expanding to 2.1 million ft² by 2027, cementing the emirate’s role as the GCC’s fulfillment nucleus. Political stability, top-tier telecoms, and skilled multilingual labor further reinforce the country’s standing as the natural staging ground for regional brokerage operations.[4]Abu Dhabi Launches First Autonomous Truck Pilot in MENA Logistics Sector,” Integrated Transport Centre (Abu Dhabi Mobility), itc.gov.ae

Competitive Landscape

No single broker controls more than a single-digit share, rendering the UAE freight brokerage services market moderately fragmented. Global players such as DHL and Kuehne+Nagel integrate customs brokerage, warehousing, and last-mile delivery to create sticky ecosystems. Regional specialists attack niches like project cargo and cold-chain, leveraging deep regulatory expertise to sustain premium pricing. Venture-backed platforms scale rapidly on asset-light models, but profitability hinges on monetizing data insights and ancillary services.

Incumbents respond by digitizing operations, exemplified by DHL’s rail partnership with Etihad Rail that combines multimodal capacity with live tracking. Asset-heavy carriers hedge by renting slot capacity to tech platforms, converting fixed costs into guaranteed revenue. Emiratization mandates add a talent-development differentiator; brokers with structured training satisfy quotas while building loyalty among national staff.

Sustainability pledges enter the strategy mix: GEODIS’ biofuel refrigerated fleet and autonomous-truck trials signal an emerging green premium that could reshape procurement criteria. Consolidation pressures loom for mid-sized brokers lacking both scale and technology depth, setting the stage for M&A activity as platforms hunt network density and incumbents seek digital capabilities.

United Arab Emirates Freight Brokerage Services Industry Leaders

DHL Group

C.H. Robinson

Trukkin

Trukker

Trukko

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Dubai authorities extended the temporary 24/7 truck access across all major city roads until further notice to support peak logistics demand and alleviate supply chain bottlenecks.

- January 2026: Etihad Rail officially unveiled the full 11-city scope of its national rail network, integrating its 2023-launched freight operations with the first phase of passenger services slated for 2026.

- September 2025: Etihad Rail signed a landmark agreement with Abu Dhabi/Fujairah Customs and Noatum Logistics to establish a secure customs corridor for faster rail-linked cargo clearance.

- June 2025: DP World announced a USD 2.5 billion global investment to expand its end-to-end logistics network, including the launch of a new multi-user bonded warehouse in Singapore to mirror its successful UAE models.

United Arab Emirates Freight Brokerage Services Market Report Scope

| Full-Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Others |

| Dry Van |

| Refrigerated Van |

| Flatbed / Step-Deck |

| Tanker (Bulk Liquid and Chemical) |

| Others |

| Long-Haul (More than 500 miles) |

| Regional (100-500 miles) |

| Local (Less than 100 miles) |

| Traditional Freight Brokerage |

| Asset-Based Freight Brokerage |

| Agent Model Freight Brokerage |

| Digital Freight Brokerage |

| Manufacturing and Automotive |

| Construction and Infrastructure Projects |

| Oil, Gas, Mining and Chemicals |

| Agriculture and Food / Beverage |

| Retail, FMCG and Wholesale Distribution |

| Healthcare and Pharmaceuticals |

| E-commerce and 3PL Fulfilment |

| Other End-User Industry |

| Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) |

| Small Businesses (Less than USD 10 M) |

| By Service | Full-Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| Others | |

| By Equipment / Trailer Type | Dry Van |

| Refrigerated Van | |

| Flatbed / Step-Deck | |

| Tanker (Bulk Liquid and Chemical) | |

| Others | |

| By Haul Length | Long-Haul (More than 500 miles) |

| Regional (100-500 miles) | |

| Local (Less than 100 miles) | |

| By Business Model | Traditional Freight Brokerage |

| Asset-Based Freight Brokerage | |

| Agent Model Freight Brokerage | |

| Digital Freight Brokerage | |

| By End-User Industry | Manufacturing and Automotive |

| Construction and Infrastructure Projects | |

| Oil, Gas, Mining and Chemicals | |

| Agriculture and Food / Beverage | |

| Retail, FMCG and Wholesale Distribution | |

| Healthcare and Pharmaceuticals | |

| E-commerce and 3PL Fulfilment | |

| Other End-User Industry | |

| By Customer Size | Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) | |

| Small Businesses (Less than USD 10 M) |

Key Questions Answered in the Report

How big is the UAE freight brokerage services market in 2026?

The UAE freight brokerage services market size is estimated at USD 0.25 billion in 2026, on track to reach USD 0.40 billion by 2031.

Which segment grows fastest within UAE brokerage services?

E-commerce & 3PL Fulfilment is projected to expand at a 19.61% CAGR, almost double the overall market pace.

What is driving demand for refrigerated freight in the UAE?

Rapid growth of pharmaceutical re-exports and perishables transshipped through Dubai and Abu Dhabi is pushing refrigerated van demand at a 12.15% CAGR.

How are digital platforms changing freight brokerage in the UAE?

Platforms deliver real-time pricing, automated paperwork, and capacity pooling, enabling an 18.71% CAGR surge that erodes traditional brokers’ share.

What challenges constrain brokerage profitability?

Rising cybersecurity compliance costs, empty-backhaul imbalances, and Emiratization quotas collectively shave between 0.6% and 1.4% off forecast CAGR.

When is the UAE–Saudi rail link expected to be fully operational, and how will it affect freight brokers?

The cross-border line is scheduled for completion by 2030, after which brokers will be able to offer seamless rail-road land-bridge services that can trim GCC transit times by about 30% and unlock new intermodal capacity for time-sensitive cargo.

Page last updated on: