Middle East And Africa Express Delivery Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

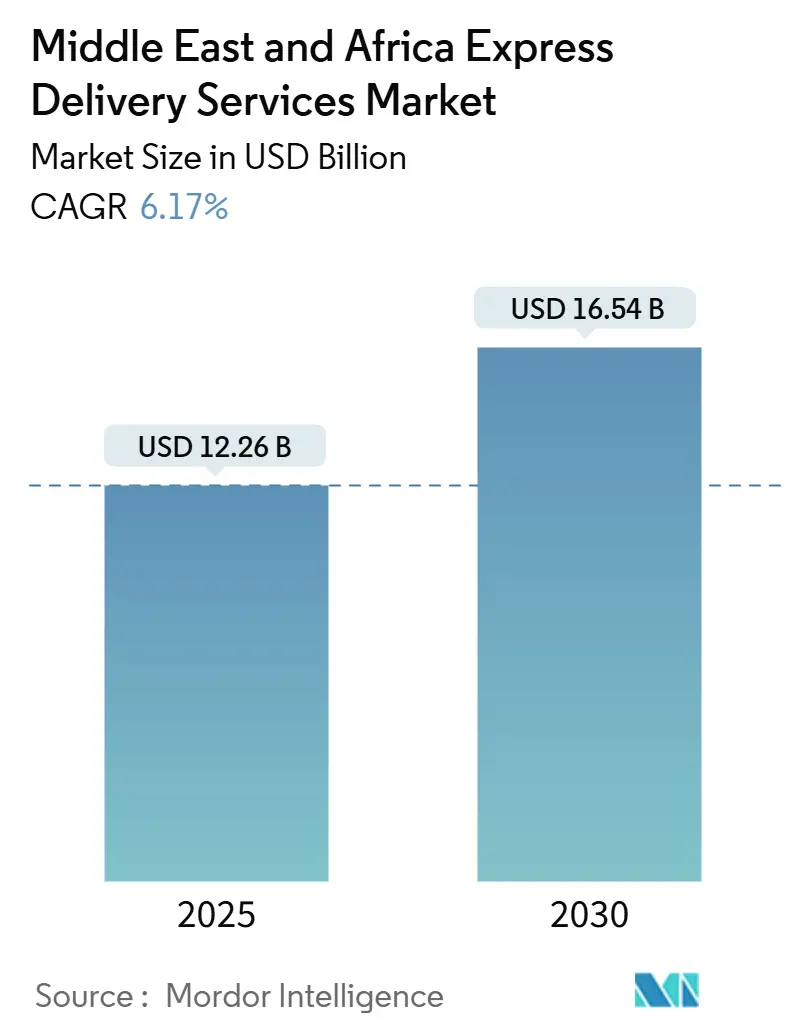

| Market Size (2025) | USD 12.26 Billion |

| Market Size (2030) | USD 16.54 Billion |

| Growth Rate (2025 - 2030) | 6.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Express Delivery Services Market Analysis by Mordor Intelligence

The Middle East And Africa Express Delivery Services Market size is estimated at USD 12.26 billion in 2025, and is expected to reach USD 16.54 billion by 2030, at a CAGR of 6.17% during the forecast period (2025-2030).

The trajectory reflects rapid e-commerce adoption, supportive government logistics agendas, and expanding free-trade zones, all of which drive sustained parcel volume growth and intensify competition among international and regional carriers. Accelerated digital payments, rising urban middle-class consumption, and infrastructure upgrades across air, road, and warehousing assets are further accelerating network expansion. Express operators are prioritizing automation, dedicated cargo capacity, and last-mile technology to protect margins as fuel surcharges and geopolitical rerouting lift operating costs. The result is a marketplace where speed, visibility, and flexible pricing now outweigh basic rate competition, reinforcing a premium on technology-led service differentiation.

Key Report Takeaways

- By destination, domestic services commanded 62.44% of the Middle East and Africa express delivery services market share in 2024, whereas international shipments are projected to expand at a 6.40% CAGR through 2030.

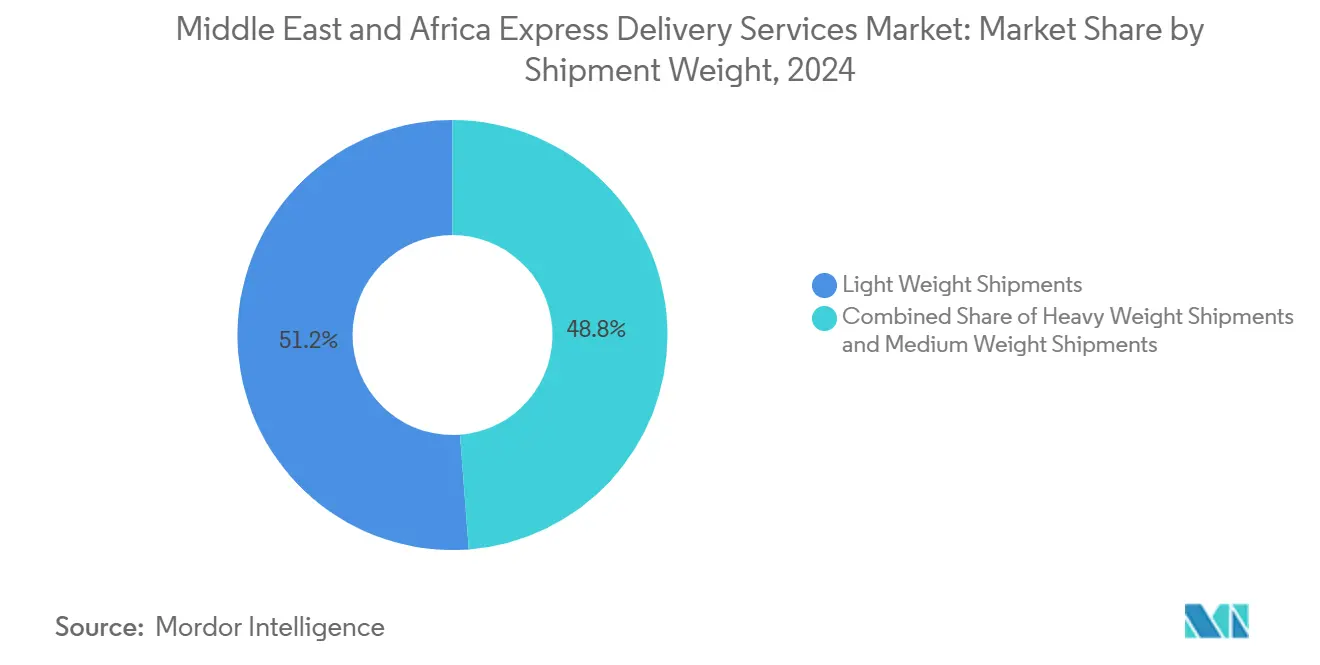

- By shipment weight, lightweight parcels accounted for 51.20% of the Middle East and Africa express delivery services market size in 2024 and will advance at a 6.30% CAGR to 2030.

- By model, the B2C segment held 54.22% of the Middle East and Africa express delivery services market size in 2024, while recording the fastest growth at 6.51% through 2030.

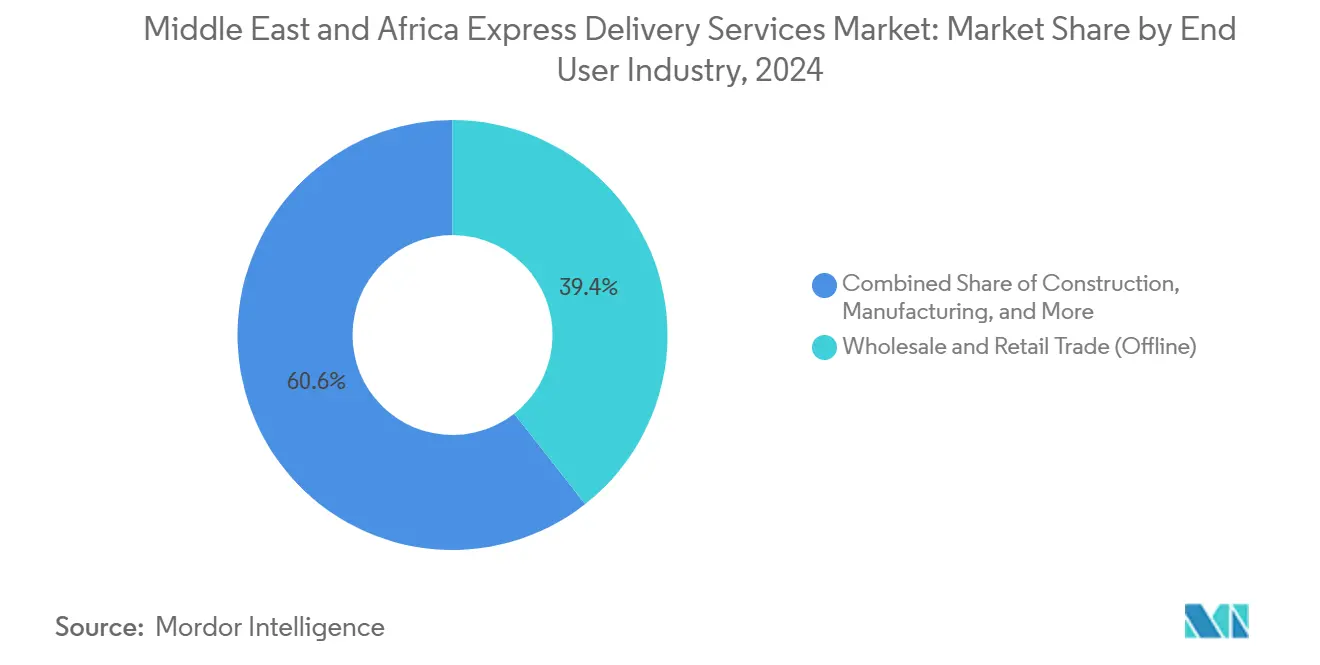

- By end user industry, wholesale and retail trade (offline) led with 39.44% of the Middle East and Africa express delivery services market share in 2024; e-commerce end users exhibit the highest 6.65% CAGR to 2030.

- By mode of transport, road maintained a 51.29% share of the Middle East and Africa express delivery services market size in 2024, whereas air transport is rising at a 6.31% CAGR through 2030.

- By country, Saudi Arabia contributed 9.30% of regional revenue in 2024, while the United Arab Emirates shows the strongest 6.69% CAGR potential through 2030.

Middle East And Africa Express Delivery Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid e-commerce penetration post-COVID-19 | +1.8% | Global, with UAE and Saudi Arabia leading adoption | Short term (≤ 2 years) |

| Growing cross-border online retail demand | +1.2% | Gulf states to Africa corridors, intra-GCC trade | Medium term (2-4 years) |

| Government vision programs (e.g., Saudi Vision 2030 logistics pillar) | +1.5% | Saudi Arabia, UAE, with spillover to regional hubs | Long term (≥ 4 years) |

| Surge in SME-driven last-mile tech platforms | +0.9% | Urban centers across MEA, concentrated in major cities | Short term (≤ 2 years) |

| Expansion of free-trade & special economic zones | +0.7% | UAE, Saudi Arabia, Egypt, South Africa | Medium term (2-4 years) |

| B2B same-day delivery for critical spares (oil & gas) | +0.6% | Gulf states, Algeria, Nigeria, Angola | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid E-commerce Penetration Post-COVID-19

Online spending in the UAE touched USD 8.8 billion in 2024[1]UAE Ministry of Economy, “UAE E-commerce Market Report 2024,” economy.gov.ae. The behavioral pivot toward home delivery has locked in higher shipment frequency, especially for fashion, beauty, and grocery categories that favor next-day service. Regional parcel integrators re-timed schedules, opened weekend sort cycles, and introduced doorstep cashless options to capture the surge. Dedicated air freight lanes from China and South Asia now cut lead times to five–seven days, down from two–three weeks pre-pandemic, making international express a default mode for fast-moving stock. Because urban consumers now equate reliable tracking with brand trust, operators that invest in real-time visibility solutions are posting higher retention and basket sizes.

Growing Cross-Border Online Retail Demand

Gulf-to-Africa e-commerce flows climbed as customs protocols aligned with the African Continental Free Trade Area, trimming clearance to two–three days in several pilot corridors[2]African Union, “African Continental Free Trade Area Implementation Progress Report,” au.int. Apparel, electronics, and specialty foods top the order mix, pushing express firms to add bonded regional sort hubs in Jebel Ali and Nairobi. Duty-paid consolidation enables merchants to ship in bulk and break down orders closer to the destination, smoothing landed cost volatility. Platforms integrating multi-currency checkout and last-mile partner APIs have shortened end-to-end delivery from 10–14 days to three–five days, attracting repeat shoppers and boosting basket sizes. The volume upswing is expected to persist as African middle-class disposable income rises and GCC sellers localize inventory in free-zone fulfillment centers.

Government Vision Programs Drive Infrastructure Investment

Saudi Arabia’s Vision 2030 earmarks USD 267 billion for transport modernization, targeting a jump in logistics GDP contribution from 6% to 10% by 2030[3]Saudi Press Agency, “Saudi Arabia Allocates USD 267 Billion for Vision 2030 Logistics Infrastructure,” spa.gov.sa. Projects include cargo-dedicated terminals at Riyadh and Jeddah, autonomous sorting facilities, and paperless customs gates. The UAE’s ambition to become a top-ten global logistics hub has attracted more than USD 571 million in DHL infrastructure commitments for 2025–2030, including robotic sorters calibrated for e-commerce parcel profiles. Egypt is expanding the Suez Canal Economic Zone, adding air-rail-sea interchanges aimed at 24-hour transshipment. These sovereign programs create anchor volumes and accelerate private capital inflows, rewarding express providers that co-invest in hub-and-spoke capacity early in the cycle.

Surge in SME-Driven Last-Mile Tech Platforms

Venture-backed startups such as Kwik Delivery and Borzo leverage GPS routing, crowdsourced driver fleets, and mobile payments to achieve on-time rates above 95% in Lagos and Dubai, compared with 60–70% for legacy couriers. Partnerships with supermarkets and pharmacies supply predictable peak-hour volumes, improving driver asset utilization. Established express brands increasingly white-label these platforms to extend same-hour reach without owning fleets, accelerating network densification. As small merchants gain access to affordable dispatch dashboards, daily shipment frequency rises, feeding the broader Middle East and Africa express delivery services market. The scalability of these tech models is catalyzing a shift from depot-centric to hyperlocal delivery architectures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited address standardization & postal codes | -0.8% | Sub-Saharan Africa primarily, some Middle East rural areas | Medium term (2-4 years) |

| High customs clearance bureaucracy on intra-Africa lanes | -0.6% | Cross-border African corridors, limited Middle East impact | Long term (≥ 4 years) |

| Rising air-freight costs due to capacity squeeze | -1.1% | Global impact, particularly affecting international express | Short term (≤ 2 years) |

| Geopolitical flashpoints disrupting key corridors | -0.9% | Red Sea routes, North Africa, select Gulf corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Air-Freight Costs Due to Capacity Squeeze

Freight rates from East Asia into Gulf hubs doubled between Q4 2024 and Q2 2025 as diverted Red Sea cargo consumed available belly hold capacity[4]International Air Transport Association, “Air Cargo Market Analysis Q4 2024,” iata.org. Fuel surcharges rose in lockstep, eroding margin on lower-value parcels and prompting selective rate hikes. Express integrators responded by chartering dedicated freighters and re-routing some Asia-bound volumes through Istanbul and Muscat, albeit at the expense of longer transit. While passenger aircraft reactivation will eventually moderate supply tightness, carriers expect elevated spot prices through 2026. Efficiency gains from load-planning AI and zone-skipping consolidation aim to cushion cost escalation but cannot fully offset the squeeze on price-sensitive consumer electronics and apparel categories.

Geopolitical Flashpoints Disrupting Key Corridors

Houthi attacks have rerouted up to 15% of global container traffic away from the Suez-Red Sea passage, adding 10–14 days and significant bunker costs to sea legs. Express operators have countered with air-bridging and multimodal detours via Mediterranean gateways, but the agility comes at a higher variable cost. Insurance premiums on vulnerable lanes rose sharply, and additional security escorts are now standard on select North African routes. Contingency stock positioning in Gulf free zones has alleviated some risk, yet the unpredictability of flashpoints keeps network planners in constant rerouting mode, absorbing management bandwidth and capital that might otherwise scale growth corridors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Digital Retail Reshapes Volume Mix

Wholesale and retail trade (offline) accounted for 39.44% revenue in 2024, yet its share is slipping as omnichannel giants pivot to warehouse-to-consumer direct shipping. E-commerce end users will register a 6.65% CAGR through 2030, the highest among all verticals, as local merchants onboard marketplace storefronts and leverage seller-fulfilled prime models.

Healthcare demand is surging for temperature-controlled biologics and direct-to-patient clinical trial kits, driving investment in GDP-certified packaging and IoT monitors. Manufacturing and primary industries depend on critical spare part delivery that prevents costly production halts, particularly in petrochemical zones. Financial institutions’ document volumes decline with digital signatures, freeing capacity for higher-value categories. The rebalancing of vertical exposure underscores the adaptive breadth of the Middle East and Africa express delivery services industry.

By Destination: Cross-Border Momentum Redefines Network Economics

International shipments accounted for 37.56% of revenue in 2024 and are projected to expand at a 6.40% CAGR through 2030, outpacing domestic growth within the Middle East and Africa express delivery services market. Preferential trade agreements, harmonized e-invoicing, and bonded fulfillment nodes reduce frictions that once made cross-border delivery uncompetitive. Greater airlift frequency from Emirates, Saudia Cargo, and Ethiopian Airlines provides daily uplifts into rising consumer centers such as Lagos, Nairobi, and Johannesburg.

Domestic deliveries nonetheless remain the volume anchor, supported by extensive road corridors that keep per-parcel costs low. However, flat GDP growth in mature Gulf cities caps organic expansion, prompting carriers to upsell value-added services such as same-day delivery guarantees and Reverse Logistics. The convergence of customs-light “in-country international” programs blurs traditional boundaries, enabling merchants to list regional storefronts that promise 48-hour delivery without import duty complications. This structural shift ensures both domestic and international segments remain synergistic pillars of the Middle East and Africa express delivery services market.

By Mode of Transport: Airlift Expands Despite Cost Pressures

Road transport led with a 51.29% share in 2024, favored for its cost-effectiveness on regional lanes linking Saudi Arabia, the UAE, and Oman via the GCC Customs Union. Fleet renewal toward Euro VI trucks and smart-tagged trailers boosts fuel efficiency and border throughput, enhancing reliability.

Air transport, though pricier, records a 6.31% CAGR on the back of rising high-value electronics, fashion drops, and perishables. Built-for-e-commerce freighters—Boeing 777F and Airbus A350F—promise lower unit cost per kilogram and reduced emissions, making premium transit more defensible. Rail and sea play niche roles: Egypt’s logistics stakeholders are piloting a short-haul rail express link from Port Said to Cairo, while Kenya tests Lake Victoria ferries for regional parcel distribution. The multimodal mosaic creates redundancy that is vital for maintaining service commitments across the Middle East and Africa express delivery services market.

By Shipment Weight: Light Parcels Dominate Capacity Planning

Lightweight shipments contributed 51.20% of the Middle East and Africa express delivery services market size in 2024 and will climb at a 6.30% CAGR through 2030, buoyed by e-commerce’s preference for single-item orders and subscription replenishment. Medium-weight parcels serve SMEs shipping replenishment stock, while heavyweight consignments remain the preserve of oil-gas spare parts, renewables, and capital equipment.

Specialized handlers retain a pricing premium based on dimensional weight and crane-equipped vehicles, but high fuel overheads mute volume share growth. Express firms deploying electric vans and compact three-wheelers in dense districts reduce per-stop costs, allowing profitable monetization of small-ticket orders. The trend underlines why network design increasingly orbits the lightweight segment of the Middle East and Africa express delivery services market.

By Model: B2C Surge Reinforces Last-Mile Innovation

The B2C channel held 54.22% of the Middle East and Africa express delivery services market size in 2024 and is forecast to compound at 6.51% through 2030. Platform-agnostic couriers now integrate with over 150 regional e-commerce checkouts, offering plug-and-play APIs that auto-populate airway bills and send proactive SMS updates. Carrier alliances with grocery marketplaces add peak-hour density that raises route profitability.

B2B shipments, although growing more slowly, remain margin-accretive due to contractual service-level agreements with industries such as aerospace and pharma, where downtime or compliance penalties far outweigh freight costs. C2C activity is rising in sub-Saharan cities where informal commerce and social-media classifieds rely on flexible pick-up windows. Payment-on-delivery services mitigate trust deficits and unlock new addressable users, expanding the overall Middle East and Africa express delivery services market.

Geography Analysis

Saudi Arabia was responsible for 9.30% of regional revenue in 2024, anchored by government-funded cargo airports, bonded trucking lanes, and a nationwide addressing system. Express operators leverage Vision 2030 incentives—duty rebates, land grants, and co-location in logistics clusters—to expedite hub build-outs and automated sort deployment.

The UAE is projected to clock the highest 6.69% CAGR through 2030, thanks to its gateway position. Expansion of Al Maktoum International Airport to 12 million tons annual cargo capacity, coupled with two-hour customs release, makes Dubai a natural consolidation point for Asia-Europe-Africa flows. Free-zone fulfillment centers in Jebel Ali and Ras Al Khaimah provide duty-suspended inventory that feeds Gulf and East African orders within 48 hours, strengthening the country’s hub stature in the Middle East and Africa express delivery services market.

Egypt, South Africa, and the broader sub-Saharan cluster collectively contribute a growing share as mobile wallets, address standardization drives, and trade facilitation programs narrow historical service gaps. While road density remains uneven, targeted public-private partnerships are unlocking last-mile routes in Nairobi, Lagos, and Johannesburg. Cross-border e-commerce corridors linking GCC sellers to African consumers underpin a virtuous cycle of network investment and volume scaling.

Competitive Landscape

The Middle East and Africa express delivery services market hosts a mix of global integrators, regional incumbents, and tech-native disruptors, producing a moderate concentration environment. DHL Express, FedEx, and UPS exploit worldwide network breadth to offer consistent transit times and customs brokerage expertise, securing large multinational accounts. Aramex and SMSA Express counters with localized pricing and cultural intimacy often win SME loyalty.

Strategic investment is tilting toward automation: DHL’s USD 571 million Gulf program allocates funds to robotic sorters and electric vans, while FedEx’s direct-serve entry into Saudi Arabia features a Riyadh regional hub with AI-enabled capacity forecasting. Partnerships also play a pivotal role. Aramex integrates with Shopify and WooCommerce plugins to simplify seller onboarding, whereas emerging platforms like Fetchr provide mobile-based address pins that bypass legacy street naming gaps in Dubai and Cairo.

Competitive intensity is heightened by marketplace logistics arms such as Amazon.ae and Noon Minutes, which internalize part of their delivery to lock in service quality and negotiate volume-based airline block space. Regional M&A is likely as carriers seek scale economies in linehaul and technology spend, setting the stage for a dynamic yet consolidating Middle East and Africa express delivery services market.

Middle East And Africa Express Delivery Services Industry Leaders

Aramex

DHL Group

Saudi Post-SPL (Naqel Express)

Emirates Post

FedEx

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: FedEx completed its transition to a direct-serve presence in Saudi Arabia, inaugurating a dedicated weekly flight and breaking ground on a Riyadh hub at King Salman International Airport.

- June 2025: DHL Group confirmed a USD 571 million investment plan to boost express and e-commerce infrastructure across Saudi Arabia and the UAE through 2030.

- April 2025: Nigeria’s postal authority (NIPOST) rolled out a modernization roadmap focusing on track-and-trace upgrades and private-sector partnerships.

- February 2024: UPS purchased two Boeing 747-8 freighters from Qatar Airways for delivery in early 2025, enabling fleet modernization and incremental Asia-MEA capacity.

Middle East And Africa Express Delivery Services Market Report Scope

| Domestic |

| International |

| Heavy Weight Shipments |

| Light Weight Shipments |

| Medium Weight Shipments |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Consumer-to-Consumer (C2C) |

| E-Commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

| Road |

| Air |

| Others |

| United Arab Emirates |

| Saudi Arabia |

| Egypt |

| South Africa |

| Rest of Middle East and Africa |

| By Destination | Domestic |

| International | |

| By Shipment Weight | Heavy Weight Shipments |

| Light Weight Shipments | |

| Medium Weight Shipments | |

| By Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Consumer-to-Consumer (C2C) | |

| By End User Industry | E-Commerce |

| Financial Services (BFSI) | |

| Healthcare | |

| Manufacturing | |

| Primary Industry | |

| Wholesale and Retail Trade (Offline) | |

| Others | |

| By Mode of Transport | Road |

| Air | |

| Others | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

How large is the Middle East and Africa express delivery services market in 2025?

It reaches USD 12.26 billion in 2025 and is projected to grow at a 6.17% CAGR to USD 16.54 billion by 2030.

Which destination segment grows the fastest?

International shipments, benefiting from cross-border e-commerce, post a 6.40% CAGR through 2030.

Why do lightweight parcels dominate volume?

E-commerce favors single-item orders, keeping average parcel weight under 2 kg and securing 51.20% share in 2024.

Which country shows the highest growth potential?

The UAE leads with a 6.69% CAGR due to free-zone expansion and two-hour customs clearance.

How are rising air-freight costs managed?

Carriers charter dedicated freighters, diversify routing, and deploy AI load-planning to mitigate fuel and capacity premiums.

What is the current competitive landscape?

Global integrators hold scale advantages, but regional players and tech-driven startups increase service diversity and pressure incumbents.

Page last updated on: